Commercial UV Water Purifier Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

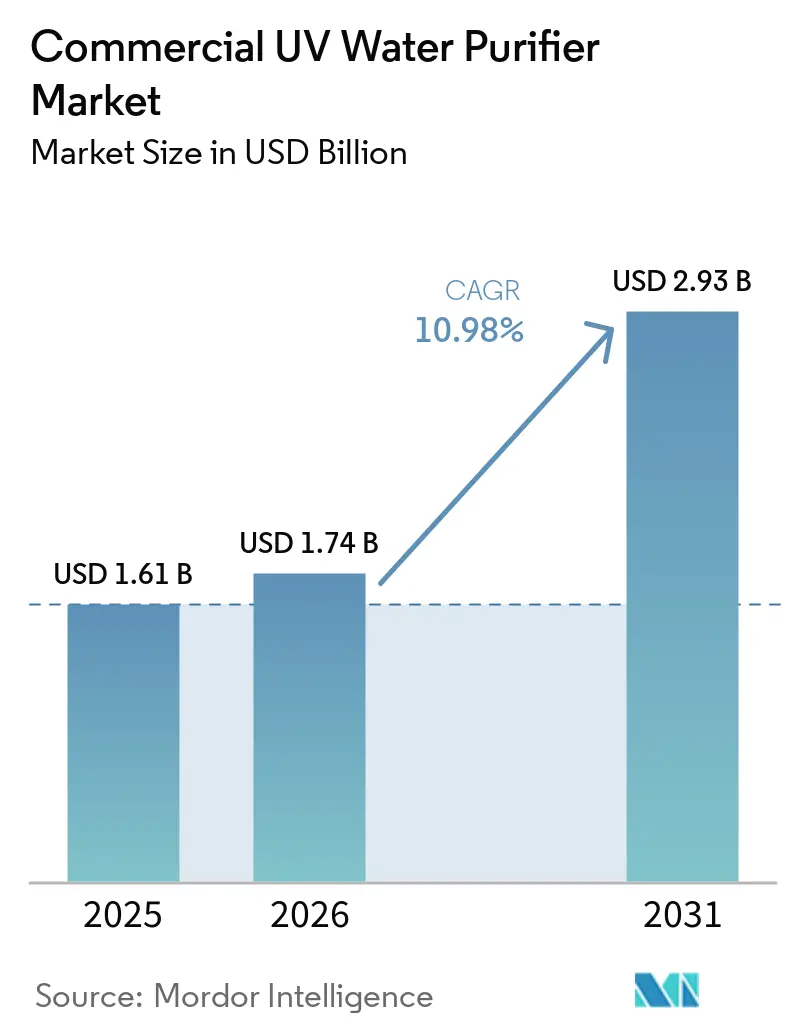

| Market Size (2026) | USD 1.74 Billion |

| Market Size (2031) | USD 2.93 Billion |

| Growth Rate (2026 - 2031) | 10.98% CAGR |

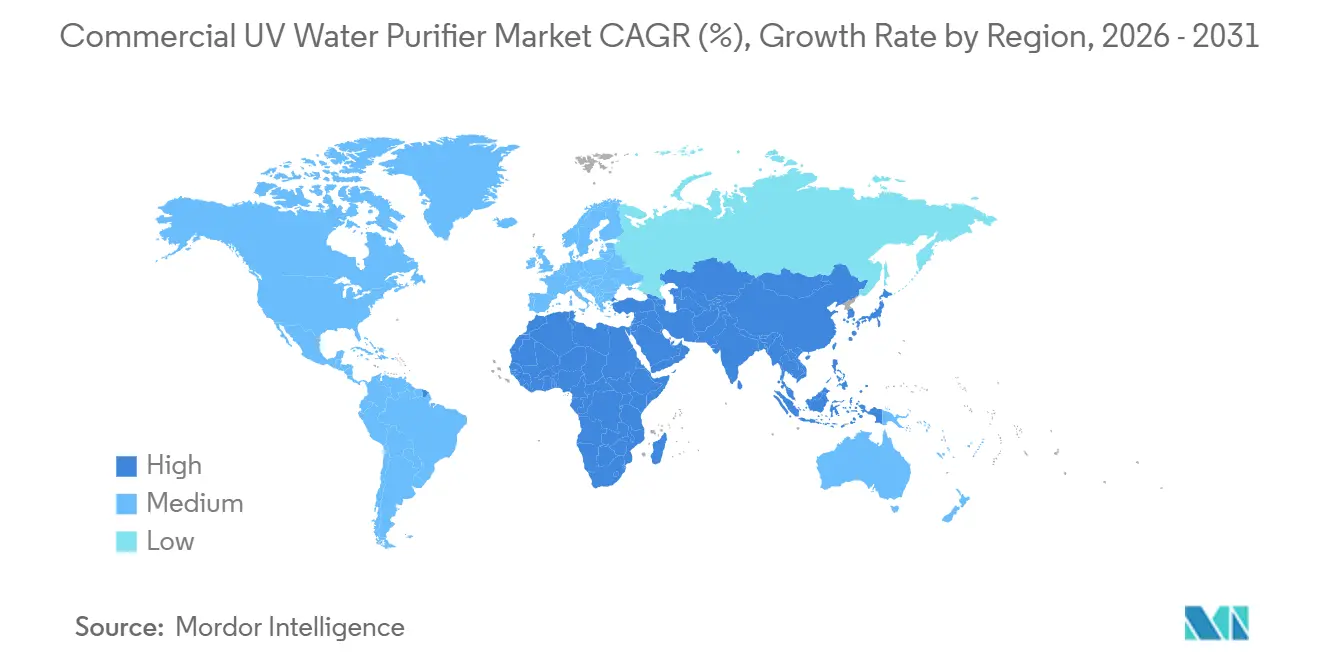

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

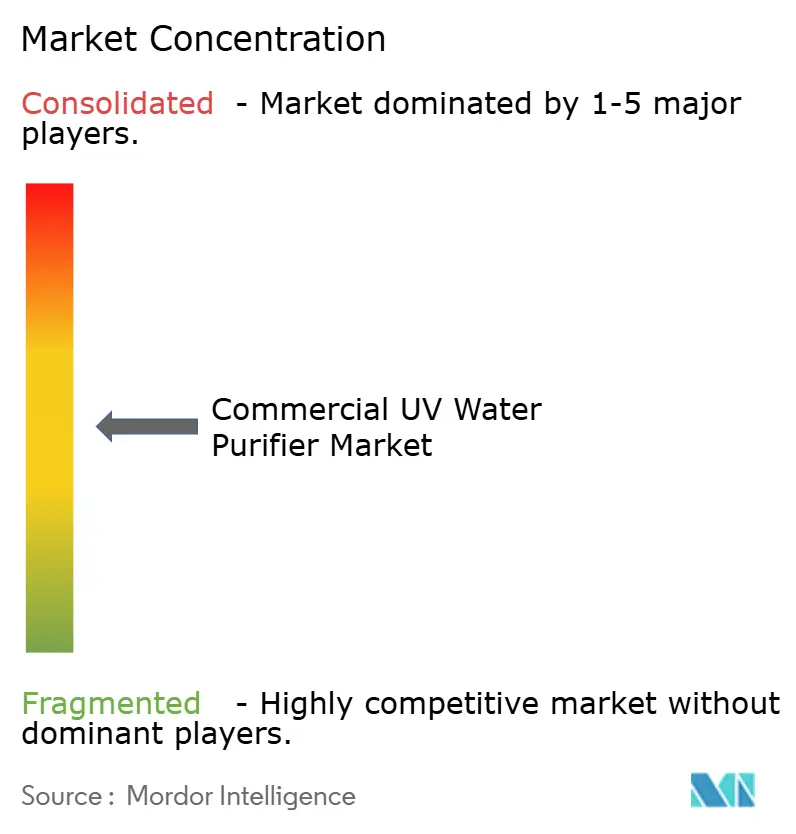

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial UV Water Purifier Market Analysis by Mordor Intelligence

The commercial UV water purifier market size is expected to grow from USD 1.61 billion in 2025 to USD 1.74 billion in 2026 and is forecast to reach USD 2.93 billion by 2031 at 10.98% CAGR over 2026-2031. Low-pressure UV systems continued to anchor municipal retrofits due to predictable operating costs, while UV-C LED systems advanced faster as regulatory pressure on mercury intensified across developed markets. Drinking water purification led demand in 2025 as utilities adopted multi-barrier designs that place UV after membrane separation and oxidation for validated inactivation. Asia-Pacific expanded faster than North America as countries invested in both chlorine-dependent plant upgrades and greenfield aquaculture biosecurity lines that favor chemical-free treatment. Healthcare facilities moved up the priority list as United States device classifications tightened validation expectations for UV-based microbial reduction across clinical water points.

Key Report Takeaways

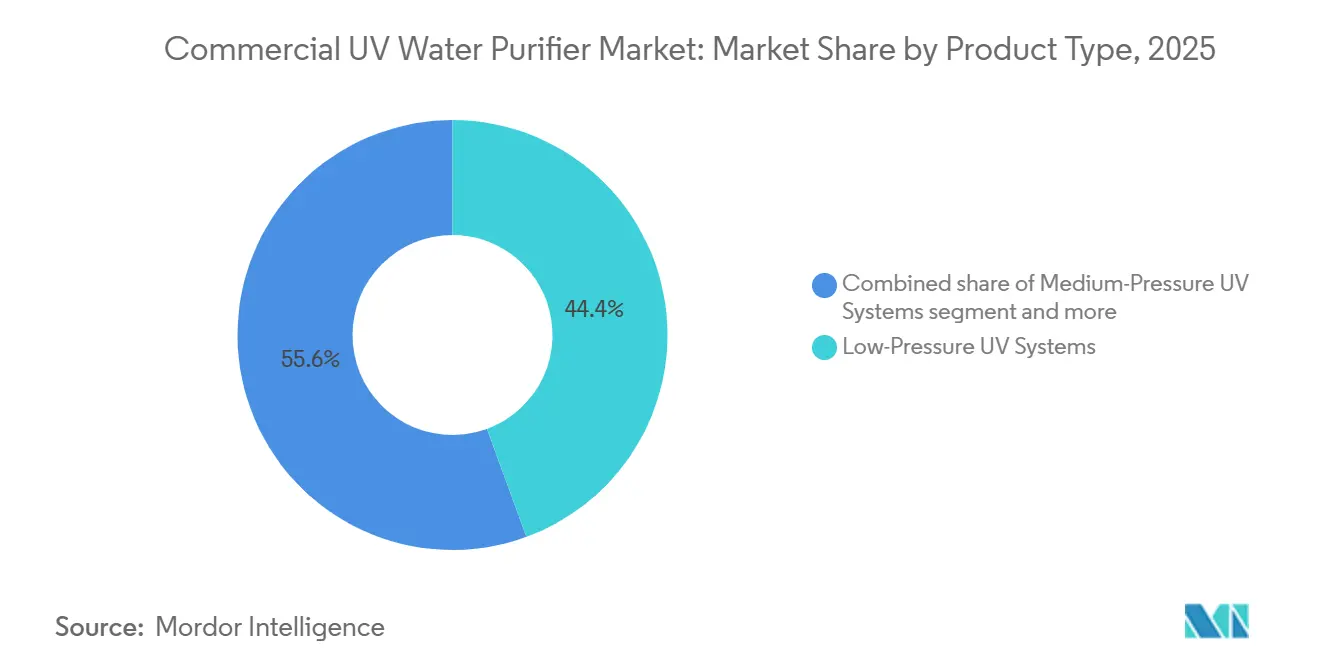

- By product type, low-pressure UV led with 44.4% revenue share in 2025 in the commercial UV water purifier market, while UV-C LED systems are projected to post a 14.7% CAGR through 2031.

- By application, drinking water purification held 53.8% in 2025 in the commercial UV water purifier market, while aquaculture water treatment is advancing at a 12.8% CAGR through 2031.

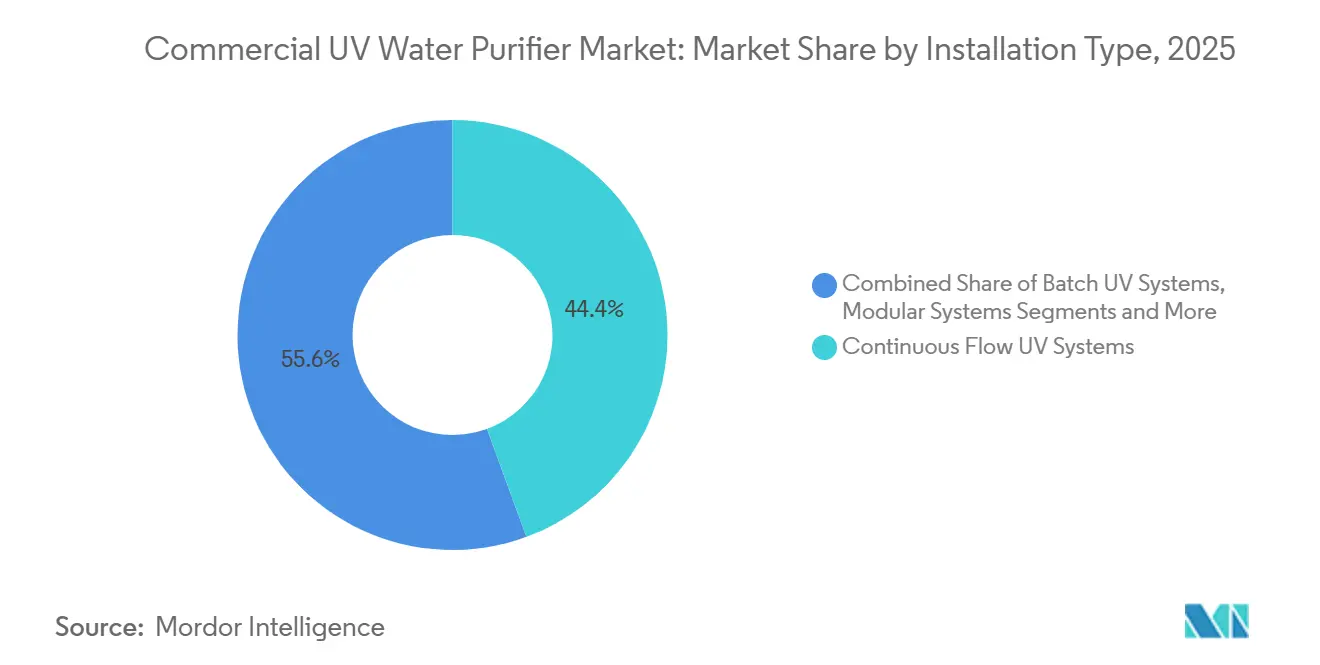

- By installation type, continuous-flow systems led with 44.4% in 2025 in the commercial UV water purifier market, while skid-mounted systems are set to grow at a 12.9% CAGR through 2031.

- By system configuration, single-stage units held 49.3% in 2025 in the commercial UV water purifier market, while multi-stage systems are projected at a 12.4% CAGR through 2031.

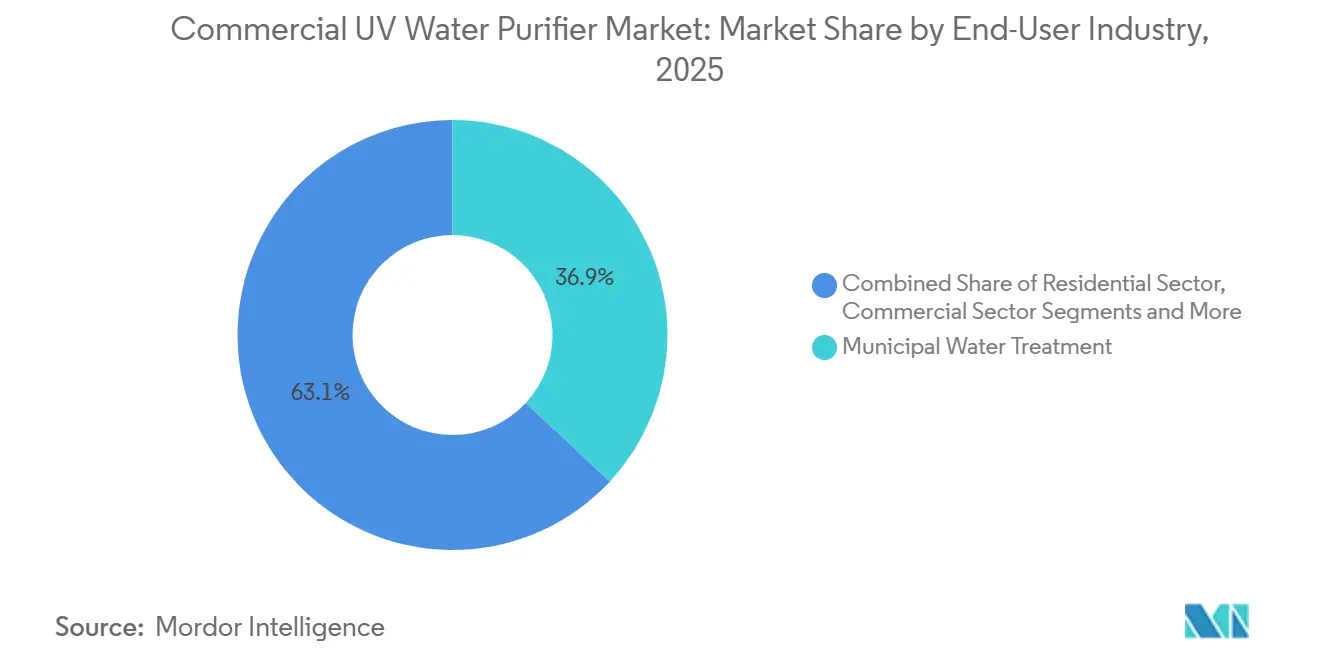

- By end-user, municipal water treatment accounted for 36.9% of revenue in 2025 in the commercial UV water purifier market, while healthcare facilities are set to expand at a 12.1% CAGR through 2031.

- By distribution channel, direct sales captured 51.82% in 2025 in the commercial UV water purifier market, while online B2B marketplaces and D2C channels are poised for a 12.3% CAGR through 2031.

- By geography, North America commanded 36.25% in 2025 in the commercial UV water purifier market, while Asia-Pacific leads growth with a 13.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Commercial UV Water Purifier Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter potable, reuse, and industrial water quality rules | + 3.2% | Global, led by California, Colorado, and the European Union | Short term (≤ 2 years) |

| Shift to chemical-free, DBP-free disinfection | + 2.8% | North America & the European Union, spillover to the Asia-Pacific municipal | Medium term (2-4 years) |

| UV-C LED performance gains enabling compact POE/POU | + 2.1% | Asia-Pacific core, early adoption in Japan, South Korea | Long term (≥ 4 years) |

| Aging water assets and retrofit programs in utilities and industry | + 1.9% | North America, Western Europe | Medium term (2-4 years) |

| Validation-driven, IoT-dosed UV enabling performance contracts | + 1.5% | Global municipal, concentrated in OECD | Medium term (2-4 years) |

| Decarbonizing cooling/process loops by replacing biocides | + 1.3% | National, early gains in European Union industrial clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

California and Colorado DPR Rules Force Multi-Barrier UV Integration

California’s 2025 direct potable reuse framework elevates UV disinfection from an optional polishing step to a required component in a multi-barrier train that includes membrane separation and advanced oxidation, with stringent log-reduction targets for viruses and protozoa [1]California State Water Resources Control Board, “Direct Potable Reuse Regulations,” California State Water Resources Control Board, waterboards.ca.gov. Colorado’s potable reuse rule mirrors the multi-barrier concept, sets default log-reduction values, and requires at least one eligible disinfection barrier, such as UV or ozone, as a critical control point, reinforcing design convergence across state-level programs [2]United States Environmental Protection Agency, “Water Reuse and Potable Reuse Technical References,” U.S. EPA, epa.gov. Utilities are responding by procuring validated, controller-integrated UV units tied into SCADA with continuous UVT monitoring, automated lamp intensity control, and data-logged dose assurance to streamline compliance reporting. The North City Pure Water facility in San Diego illustrates the protocol, placing UV/AOP after ozonation, biologically activated carbon, and reverse osmosis to complete a five-step process that has passed tens of thousands of quality tests. This regulatory clarity supports the commercial UV water purifier market as procurement teams prioritize proven validation pathways, cybersecurity-ready controls, and factory-integrated performance monitoring to limit commissioning delays and verification costs.

Mercury Phase-Outs Accelerate UV-C LED Adoption Despite Cost Gaps

Global and regional policy shifts are tightening constraints on mercury-based lamps, with the Minamata Convention’s upcoming controls, the European Union’s lamp phase-out timeline, and Japan’s fluorescent lamp ban pushing OEM portfolios toward solid-state UV-C LED systems. Miura’s 2026 commercial launch of a 25 m³/h UV-LED sterilizer, built on high-output Nichia emitters with a compact footprint, shows how industrial POE and POU designs are scaling in cosmetics, pharma, and beverage lines. Nikkiso’s PearlAqua platform spans from compact point-of-entry modules to municipal-scale units, positioning deep-UV LEDs under 280 nm for flexible deployment across water servers, factory wash lines, aquaculture tanks, and treatment plants. Materials advances also matter, with Crystal IS reporting 100 mm single-crystal AlN wafer readiness in 2024 to support serial production of germicidal LEDs at 260–270 nm, which underpins future emitter performance and reliability. These developments do not erase today’s capital premium for LEDs, yet they reduce maintenance touchpoints, simplify end-of-life compliance, and curb mercury handling, which together strengthen the commercial UV water purifier market’s long-run shift toward solid-state systems where policy and lifetime cost models align.

IoT-Enabled UV Systems Unlock Performance-Based Contracting

UV systems with embedded UVT sensors, integrated flow and temperature monitoring, and cloud dashboards now support performance contracts that commit suppliers to delivered log-reduction outcomes instead of one-time equipment sales. Atlantium’s Hydro-Optic UV solutions, already validated for open-channel reuse duty, leverage continuous transmittance data and lamp performance indicators to automate dose control and cut manual interventions. ProMinent’s digital stack shows how UV hardware pairs with monitoring platforms to detect chemical or process excursions in near real time and to protect upstream assets like RO membranes, which aligns with warranty terms and reduces downtime risks. Peer-reviewed work using multispectral sensors and machine-learning classifiers demonstrates 100% accuracy in distinguishing clean, contaminated, and UV-disinfected water, indicating a path to automate efficacy verification and reduce the need for frequent lab assays. As these tools spread, water utilities and industrial buyers can structure outcome-based contracts with shared-savings models, anchoring the commercial UV water purifier market in multi-year service revenue rather than volatile capex cycles.

Aging Infrastructure and Municipal Retrofit Cycles Drive Replacement Demand

Aging municipal UV assets in North America and Western Europe have reached the point where upgrades are required to align with current validations and with new reuse mandates that place UV after membranes and oxidation. The North City facility in San Diego exemplifies how utilities are rebuilding advanced treatment into integrated trains with UV at the end of the sequence to meet potable reuse standards and ensure contaminant destruction. European utilities have followed a similar triple-barrier path in drinking water sites, reinforcing a procurement bias toward validated systems that tie into existing plant controls and maintenance workflows. Norway’s municipal-scale LED pilot funded by public health agencies signals growing confidence in solid-state UV for large systems, a signal that will likely appear in more tenders as results mature. These needs reward suppliers with factory validation capabilities, domestic compliance footprints, and multi-year service models, reinforcing a measured but steady replacement wave for the commercial UV water purifier market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| No residual, efficacy sensitive to UVT and turbidity | - 1.8% | Global, acute in surface-water-dependent regions | Short term (≤ 2 years) |

| Quartz sleeve and controller electronics supply constraints | - 1.5% | Global supply chain, amplified in Asia-Pacific assembly hubs | Short term (≤ 2 years) |

| Skilled labor gaps for UV system design and validation | - 1.2% | Emerging markets, rural North America | Medium term (2-4 years) |

| High capex and O&M for medium and large-flow systems | - 1.0% | Municipal and industrial buyers in cost-sensitive markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Turbidity Sensitivity and Lack of Residual Disinfection Constrain Standalone Deployment

UV dose delivery drops when turbidity exceeds regulatory thresholds because particulate and dissolved matter shield pathogens, which is why drinking water rules require low turbidity and high UV transmittance before UV application [3]FranceEnvironnement, “UV Disinfection Conditions for Potable Water,” FranceEnvironnement, franceenvironnement.com. Unlike chlorine, UV provides no residual in pipelines, so networks with biofilm risks still need an additional barrier at distribution ends or a downstream disinfectant to avoid recontamination. In tropical regions with seasonal surges in turbidity and humic content, utilities must pair UV with upstream coagulation and filtration, which raises lifecycle costs and adds maintenance tasks. Studies from large-scale plants have shown UV’s effectiveness against protozoa after proper filtration, while affirming the need for a final residual within the distribution system to keep water safe to the tap. These constraints limit UV’s standalone role in remote sites unless used with filtration, which fragments procurement across multiple vendors and complicates warranty administration for combined systems in the commercial UV water purifier market.

Quartz Sleeve Supply Constraints and Controller Electronics Shortages Throttle Scaling

The supply of high-purity fused silica for quartz sleeves is tight as water OEMs share upstream capacity with semiconductor and LED makers, which lengthens lead times and forces higher working capital in spares. Controller electronics also face semiconductor allocation pressure because modern ballasts and panels integrate smart sensing, PLC connectivity, and control algorithms that rely on specialized chipsets with long queue times. These bottlenecks can delay multi-lamp skid shipments for food, pharma, and data center loops, as each skid needs parallel ballasts and matched sensors to pass validation. Some assemblers attempt to bridge gaps with lower-grade glass sleeves, but faster UVT degradation undermines log-reduction guarantees and threatens certification status, which is unacceptable for regulated uses. As a result, buyers sometimes turn to chemical systems with commodity controllers when timing is critical, a shift that can compress near-term wins for technically superior UV solutions in the commercial UV water purifier market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mercury-Free LED Systems Disrupt Established Low-Pressure Dominance

Low-pressure UV systems held 44.4% of the commercial UV water purifier market share in 2025, supported by long lamp life and predictable O&M profiles across municipal and industrial lines. Momentum is shifting as UV-C LED units gain on policy changes that penalize mercury in OECD markets, which accelerates asset owners’ shift toward solid-state designs in new lines and selective retrofits where lifetime costs and disposal risks carry weight. Medium-pressure UV remains relevant in high-flow conditions and lower-UVT wastewater trains, although its shorter lamp life increases service frequency compared to amalgam low-pressure designs [4]BIO-UV Group, “UV Solutions for Wastewater and Potable Applications,” BIO-UV, bio-uv.com. Hybrid UV-RO skids are expanding in decentralized packaged plants for hotels, bottled water sites, and greenhouses where footprint limits and commissioning speed favor integrated designs over field-built sequences. Emergency and mobile container solutions continue to gain traction, including UV-LED carts that allow rapid deployment and supervised operation in disaster response, which broadens access points for chemical-free disinfection.

UV-C LED systems are on track for a 14.7% CAGR through 2031 as major components mature and as early adopters in Japan, South Korea, and Scandinavia expand use cases from compact POE/POU to mid-scale industrial loops. Miura’s 25 m³/h UV-LED release underscores how footprint and operational simplicity improve with high-output emitters, which lowers mechanical complexity and lamp handling risks. Nikkiso’s portfolio positioning demonstrates how LED-based units can flex into municipal and industrial roles with scalable arrays and integrated monitoring for verified dose delivery. The enduring presence of low-pressure and medium-pressure lamps ensures a gradual transition as cost-sensitive buyers wait for further LED price declines, yet the direction of change is clear, where regulations and lifecycle cost models align. This dynamic will keep the commercial UV water purifier market competitive across technology lines while encouraging OEMs to maintain dual-track portfolios during the forecast window.

By Application: Aquaculture Surges on RAS Expansion and Mercury-Free Biosecurity

Drinking water purification held 53.8% in 2025 due to potable reuse mandates and municipal retrofits that codify UV inside multi-barrier designs for verified pathogen inactivation. Wastewater reuse projects continue to replace chemical contact basins with UV-based polishing to eliminate disinfection byproducts, supported by validated open-channel systems in major reuse centers. Industrial process water needs around ultra-low TOC and high log-reduction standards drive the use of high-performance UV reactors that fit into compact skids with multireactor manifolds. Food and beverage operators rely on UV to disinfect sugar syrups and condensate recoveries, avoiding thermal methods that can degrade product characteristics. Regional wastewater upgrades that pair UV with membranes to meet discharge and reuse standards illustrate the long-term role of UV in environmental protection.

Aquaculture water treatment is advancing at a 12.8% CAGR through 2031 as RAS farms scale in Asia, Europe, and the Americas and as export markets require mercury-free biosecurity measures. As LED options expand, hatcheries adopt compact, solid-state reactors that simplify maintenance and reduce lamp disposal liabilities while meeting dose targets for pathogen control at high stocking densities. System designers integrate UV into central loops and localized tanks to contain outbreaks and to protect expensive fry inventories, which lowers insurance risks and aligns with stricter audit trails. UV’s chemical-free profile fits aquaculture, where residuals can stress stock and alter water chemistry, although influent conditioning remains necessary to secure a dose where solids and organics elevate. These factors keep aquaculture as one of the faster-growing application lines in the commercial UV water purifier market during the forecast period.

By Installation Type: Skid-Mounted Systems Capture Industrial Modularity Premium

Continuous-flow units held the largest share in 2025 as utilities and large industrial customers embedded in-line reactors within existing trains to satisfy validated log-reduction targets. Skid-mounted systems are outpacing with a 12.9% CAGR as buyers prioritize factory-assembled solutions that compress installation windows, avoid civil works, and improve startup predictability. Modularization reduces field variability and concentrates validation efforts at the factory, which eases documentation and simplifies expansion in phases. Mobile and containerized variants bring the same ideas to emergency response and remote operations where on-site expertise is limited, which broadens access to validated disinfection in time-sensitive settings. This install strategy supports performance-based service models because OEMs control more of the hardware stack and can deliver uptime guarantees with telemetry visibility.

Batch systems persist in laboratory and specialty cases where precise dwell time is required, but they compete poorly on throughput and labor demands versus continuous skids. European policy focuses on energy, and verified performance supports the rise of modular skids that arrive with lifecycle energy models and environmental documentation pre-compiled. In the Commercial UV Water Purifier industry, this reinforces a migration away from field-built assemblies with multiple subcontractors toward packaged, validated solutions that shift interface risk to the OEM. The direction benefits buyers who want assured timelines and service accountability while allowing suppliers to standardize components and scale manufacturing. That combination will hold the commercial UV water purifier market on a modular growth path in industrial and resilience-focused public projects.

By System Configuration: Multi-Stage Systems Gain Share on Hybrid AOP Integration

Single-stage systems led with 49.3% in 2025 due to the simplicity of meeting typical log targets in a single pass, where influent quality is conditioned. Multi-stage systems are expanding at a 12.4% CAGR as UV couples with hydrogen peroxide or ozone to create AOP trains for micropollutant destruction and taste-and-odor control in surface supplies. Utilities adopt these hybrids to address changing influent chemistry and to maintain flexibility across seasons while maintaining verification confidence through validated UV placement after filtration. This sequencing secures dose efficiency and reduces sleeve fouling, which preserves uptime and aligns with operating budget constraints. The approach supports the commercial UV water purifier market as project finance teams value resilience, redundancy, and verified outcomes in underwriting.

Compact and custom-configurable systems widen addressable cases, from under-sink POE in small commercial jobs to specialized duties like ballast water disinfection, where UV-based designs have secured IMO and USCG approvals. Advanced membrane and carbon steps upstream make UV more efficient by removing organics and particulates that would otherwise absorb or scatter UV rays, so the market leans into integrated multi-stage designs for reliability. This is most visible where potable reuse rules are in place, which will continue to guide procurement templates for other jurisdictions that want consistent, tested recipes with proven monitoring. The result is greater standardization in documentation, instrumentation, and verification, which helps suppliers industrialize multi-stage offerings. Over time, that standardization should reduce capex gaps while maintaining the performance premium for multi-stage systems in the commercial UV water purifier market.

By End-User Industry: Healthcare Facilities Lead Growth on HAI Mitigation and FDA Validation

Municipal water treatment represented 36.9% of revenue in 2025 on the strength of long-term service agreements, but healthcare facilities are the fastest-growing end user with a projected 12.1% CAGR to 2031. FDA’s December 2025 device reclassifications established special controls for UV-based microbial reduction devices used in clinical environments, which raised validation requirements and pushed hospitals to replace unverified units. Operators target real-time monitoring and controller integration to verify dose in ice machines, sinks, and therapy pools, given the link between biofilms and opportunistic pathogens in premise plumbing. Centralized hospital water systems show how UV fits with filtration and automated purge routines to maintain quality across sensitive departments. These procurement shifts support service tie-ins for UVT sensors, lamp replacements, and remote diagnostics, which favor reputable suppliers in the commercial UV water purifier market.

Residential and commercial sites continue to adopt compact UV reactors, often as the final step after sediment and carbon filtration to secure microbial barriers without chemical tastes or odors. Direct potable reuse strategies in regions with water stress also add new municipal demand, where UV is sequenced after membranes for enhanced verification and control. Food and beverage installations benefit from non-thermal disinfection of sensitive liquids, with UV preserving flavor and avoiding residues in syrups and washes. Industrial loops in pharma and electronics integrate UV to sustain low TOC and to protect critical rinses and WFI lines, where skid-based packages limit downtime and simplify validation. Collectively, these end users keep the commercial UV water purifier market diversified across public, private, and clinical settings.

By Distribution Channel: Online B2B Marketplaces Fragment Traditional EPC Dominance

Direct sales held 51.82% in 2025 as top OEMs bundled engineering, financing, and multi-year services that lock in lamp and sensor revenues with IoT dashboards and performance guarantees. System integrators and EPCs remain central in mid-scale municipal and brownfield industrial jobs, although modular skids reduce on-site labor and coordination overhead and shift margin pools upstream. Authorized distributors continue to stock spares and support emergency service windows, but online portals allow OEMs to sell compact NSF-certified reactors and consumables with transparent pricing and verifiable quality marks. Marketplace operators now enforce verification badges that require formal documentation uploads, which helps filter out counterfeit lamps and glass components. This shift keeps the commercial UV water purifier market in a two-track posture where direct and online channels grow while traditional distribution consolidates.

Online B2B and D2C channels are projected to expand at a 12.3% CAGR through 2031 as SME bottlers, greenhouses, and aquaculture firms buy compact, validated UV systems without integrator markups. For OEMs, the strategic choice is whether to scale DTC infrastructure or to keep indirect networks for reach and service density, a choice that is prompting acquisitions of regional distributors to secure customer experience. Over time, this will change who captures data and how it is used to drive preventive maintenance and cross-sell opportunities. It will also shape warranty approaches and counterfeiting controls, given the need to track lamps, sleeves, and sensors with clear provenance. The balance will likely favor hybrid models that use both direct and online routes to keep the commercial UV water purifier market accessible across buyer sizes.

Geography Analysis

North America held 36.25% of revenue in 2025 and is projected to grow at a 6.5% CAGR through 2031 as utilities focus on replacements and compliance-driven upgrades rather than greenfield expansions. The North City Pure Water project in San Diego demonstrates how UV/AOP final barriers fit into advanced reuse, providing a model for other cities that are now planning or piloting DPR programs. Utilities in the region are adopting validated, sensor-rich reactors and open-channel UV for reuse, with suppliers emphasizing real-time dose assurance and automated controls to meet state-specific mandates. Differences among states on TOC and LRV targets create localized compliance documentation requirements that favor incumbents with specialized regulatory teams. A combination of replacement cycles and compliance upgrades will maintain a steady base for the commercial UV water purifier market in North America during the forecast period.

Asia-Pacific is projected to expand at a 13.8% CAGR through 2031, led by municipal wastewater upgrades, piped-water expansion programs, and aquaculture growth that demands chemical-free barriers. The Philippines installed a municipal UV disinfection system at the Calamba Water District in 2024 with a PHP 100 million budget, equal to USD 1.8 million using 2024 average exchange rates, which signals growing municipal adoption in Southeast Asia. Japan’s industrial sector is deploying higher-capacity UV-LED systems as mercury lamps exit the market, which is expanding POE and POU use cases in process lines. LED providers now offer both compact and municipal-scale models, which helps diversify options for municipalities and industrial buyers across the region. These shifts position Asia-Pacific as the fastest-growing region for the commercial UV water purifier market.

Europe maintains a mature installed base with a measured 6% growth path that is supported by aggressive mercury phase-outs and by the expansion of “chlorine-free” UV disinfection in selected municipalities. France and neighboring countries illustrate how local OEMs deliver certified systems for drinking water while Scandinavia pilots municipal-scale LED deployments for potential nationwide rollouts. Southern Europe uses proven low-pressure systems at scale for wastewater polishing, demonstrating how different subregions follow distinct technology curves inside the same policy block. Western Asia and Africa outpace Europe’s growth rates as new reuse and desalination projects add polishing steps and as donor programs expand rural systems, while South America grows unevenly with pockets of resort city retrofits. These regional patterns give suppliers an incentive to maintain portfolios that span mercury and LED, municipal and industrial, and packaged and component models to fit different adoption drivers in the commercial UV water purifier market.

Competitive Landscape

The commercial UV water purifier market is moderately fragmented, with the top five players holding about half of global revenue and a long tail of regional specialists and LED-focused entrants contesting niche opportunities. Xylem closed its Evoqua acquisition in 2026, consolidating municipal UV installed bases and reinforcing the company’s role in reuse and disinfection projects. Veralto moved to strengthen its Trojan Technologies platform in Europe by agreeing to acquire AQUAFIDES in early 2025, adding capabilities in low-flow drinking water, reuse, and high-purity industrial systems. These moves reflect continued interest in validated portfolios with strong services, software, and sensor integration.

Competition pivots around technology posture, service models, and regulatory positioning. Incumbents defend mercury-based installed bases through multiyear service programs, while LED specialists push energy, safety, and end-of-life advantages as policy tides turn against mercury. Suppliers with verified compliance footprints in NSF/ANSI and state-specific regimes can earn price premiums in North America and the European Union, while cost-optimized offerings target local standards in parts of Asia and Latin America. IoT-enabled performance contracts are shifting value from stand-alone hardware to guaranteed outcomes and recurring subscriptions for analytics and remote diagnostics. This is shaping channel strategies as OEMs weigh direct sales and online routes against distributor and integrator networks.

Examples of product and project execution illustrate how suppliers navigate these shifts. Atlantium advanced open-channel UV for wastewater reuse and secured validation in large-scale Californian projects that rely on continuous UVT sensing and lamp performance indicators. BIO-UV documented projects in France where UV with membrane filtration achieves Class 1 water quality for irrigation and public uses under expanding reuse targets. North American municipal reuse builds, including San Diego’s UV/AOP final barrier, showcase integrated architectures with strong data logging, which fit performance contracting and continuous audit needs. These examples indicate where the commercial UV water purifier market is most defensible and where challengers can find entry points with LED and modular skids.

Commercial UV Water Purifier Industry Leaders

Xylem

Trojan Technologies (Veralto)

Nuvonic (Halma)

SUEZ (Aquaray)

Atlantium Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Miura began taking orders for a mercury-free UV-LED sterilization device rated at 25 m³/h that reduces footprint by 75% through high-output Nichia emitters and targets industrial pure water maintenance across cosmetics, pharmaceuticals, beverages, chemicals, and electronics.

- September 2025: Atlantium unveiled next-generation open-channel UV disinfection systems and reported validation at California’s Groundwater Replenishment System to help municipalities meet stringent wastewater reuse standards without chemicals.

- August 2025: BIO-UV Group supplied two UV reactors to the Mandelieu-la-Napoule WWTP in France, integrating with membranes to achieve Class 1 water quality for irrigation and public cleaning as part of a broader reuse plan.

- February 2025: Veralto entered a definitive agreement to acquire Austria-based AQUAFIDES for about USD 20 million to enhance Trojan’s coverage across drinking water, water reuse, and high-purity industrial applications in Europe.

Global Commercial UV Water Purifier Market Report Scope

The Commercial UV Water Purifier market covers ultraviolet disinfection systems and related components used in water treatment. These systems use UV-C radiation in the 200-280 nanometer band, with peak germicidal action around 254 nanometers. The energy disrupts the DNA and RNA of bacteria, viruses, protozoa, and spores. Once inactivated, these organisms cannot reproduce or cause disease. The scope focuses on equipment designed for consistent dose delivery and reliable pathogen control in commercial and municipal environments.

The Commercial UV Water Purifier Market Report is Segmented by Product Type (Low-Pressure UV Systems, Medium-Pressure UV Systems, UV LED Systems, Hybrid UV-RO Units, and Mobile/Containerised UV Units), Application (Purification of Drinking Water, Wastewater Treatment, Industrial Process Water Treatment, Aquaculture Water Treatment, and Food & Beverage Processing), Installation Type (Batch UV Systems, Continuous Flow UV Systems, Skid-Mounted Systems, and Modular Systems), System Configuration (Single-Stage UV Systems, Multi-Stage UV Systems, Compact UV Systems, and Custom Configurable Systems), End-User Industry (Municipal Water Treatment, Residential Sector, Commercial Sector, Healthcare Facilities, and Food Processing Industry), Distribution Channel (Direct Sales, EPC and System Integrators, Authorized Distributors and Value Added Resellers, and Online (B2B marketplaces and D2C)), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD Billion).

| Low-Pressure UV Systems |

| Medium-Pressure UV Systems |

| UV LED Systems |

| Hybrid UV-RO Units |

| Mobile/Containerised UV Units |

| Purification of Drinking Water |

| Wastewater Treatment |

| Industrial Process Water Treatment |

| Aquaculture Water Treatment |

| Food & Beverage Processing |

| Batch UV Systems |

| Continuous Flow UV Systems |

| Skid-Mounted Systems |

| Modular Systems |

| Single-Stage UV Systems |

| Multi-Stage UV Systems |

| Compact UV Systems |

| Custom Configurable Systems |

| Municipal Water Treatment |

| Residential Sector |

| Commercial Sector |

| Healthcare Facilities |

| Food Processing Industry |

| Direct Sales |

| EPC and System Integrators |

| Authorized Distributors and Value Added Resellers |

| Online (B2B marketplaces and D2C) |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Low-Pressure UV Systems | |

| Medium-Pressure UV Systems | ||

| UV LED Systems | ||

| Hybrid UV-RO Units | ||

| Mobile/Containerised UV Units | ||

| By Application | Purification of Drinking Water | |

| Wastewater Treatment | ||

| Industrial Process Water Treatment | ||

| Aquaculture Water Treatment | ||

| Food & Beverage Processing | ||

| By Installation Type | Batch UV Systems | |

| Continuous Flow UV Systems | ||

| Skid-Mounted Systems | ||

| Modular Systems | ||

| By System Configuration | Single-Stage UV Systems | |

| Multi-Stage UV Systems | ||

| Compact UV Systems | ||

| Custom Configurable Systems | ||

| By End-User Industry | Municipal Water Treatment | |

| Residential Sector | ||

| Commercial Sector | ||

| Healthcare Facilities | ||

| Food Processing Industry | ||

| By Distribution Channel | Direct Sales | |

| EPC and System Integrators | ||

| Authorized Distributors and Value Added Resellers | ||

| Online (B2B marketplaces and D2C) | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the commercial UV water purifier market size and projected growth through 2031?

The commercial UV water purifier market size was USD 1.61 billion in 2025 and is projected to reach USD 2.93 billion by 2031 at an 11% CAGR.

Which product types are leading and growing fastest within the commercial UV water purifier market?

Low-pressure UV led with 44.4% in 2025, while UV-C LED systems are the fastest-growing with a projected 14.7% CAGR through 2031.

What applications drive most demand for Commercial UV Water Purifier solutions today?

Drinking water purification accounted for 53.8% in 2025, and aquaculture water treatment is the fastest-growing application at a 12.8% CAGR.

Which regions are the largest and fastest growing for Commercial UV Water Purifier adoption?

North America held 36.25% in 2025, while Asia-Pacific leads growth at a 13.8% CAGR through 2031 based on municipal upgrades and aquaculture expansion.

How are regulations such as DPR rules in the U.S. affecting the commercial UV water purifier market?

DPR regulations in California and Colorado require UV as part of multi-barrier treatment, which is increasing procurement of validated, controller-integrated UV systems with continuous monitoring.

Why are UV-C LED systems gaining share despite higher initial costs?

Mercury phase-outs and simplified maintenance favor LEDs over time, with suppliers launching higher-capacity models and materials advances that support future performance and reliability.

Page last updated on: