Mobility Scooters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

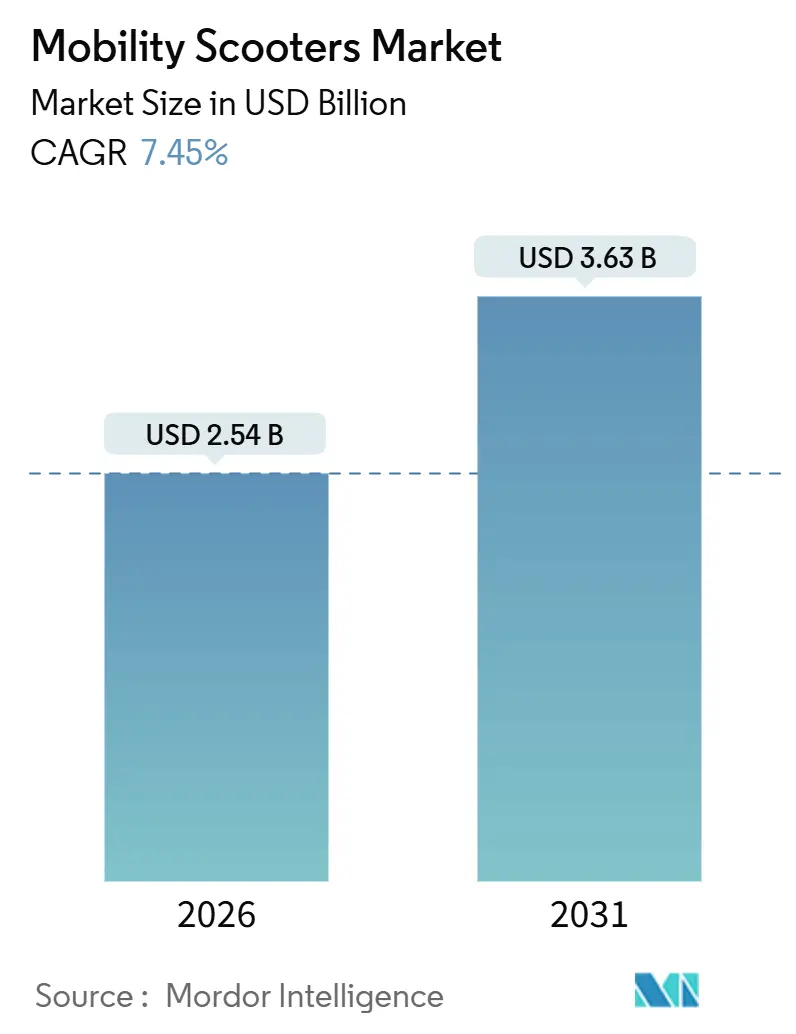

| Market Size (2026) | USD 2.54 Billion |

| Market Size (2031) | USD 3.63 Billion |

| Growth Rate (2026 - 2031) | 7.45% CAGR |

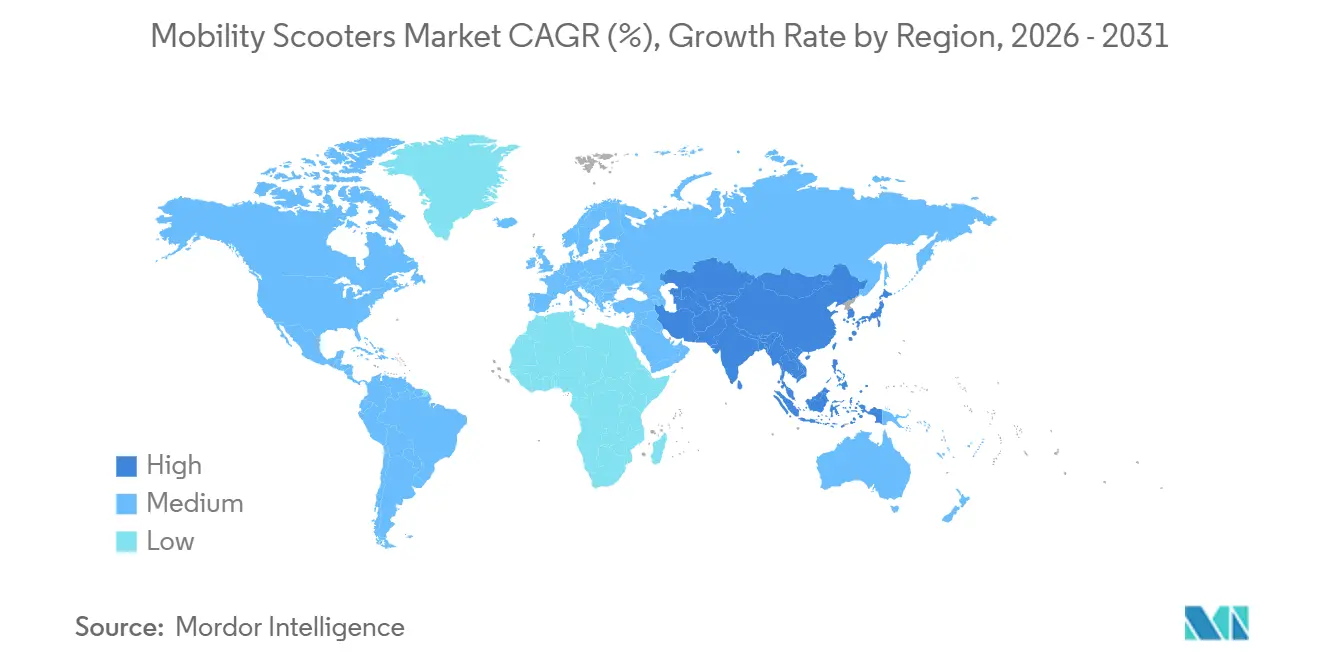

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobility Scooters Market Analysis by Mordor Intelligence

The Mobility Scooters Market size is estimated at USD 2.54 billion in 2026, and is expected to reach USD 3.63 billion by 2031, at a CAGR of 7.45% during the forecast period (2026-2031).

This expansion is underpinned by a confluence of rapid population aging, falling lithium-ion battery costs, and broader health-insurance coverage that increasingly treats mobility devices as preventive healthcare assets[1]International Energy Agency, “Global EV Outlook 2023,” International Energy Agency, iea.org. Component innovations such as carbon-fiber frames and smart-connected telematics continue to widen the addressable customer base. At the same time, fleet buyers in airports, hospitals, and senior living communities are adopting data-driven asset management platforms to boost utilization and reduce downtime. At the same time, reimbursement reforms in the United States and pilot programs in Australia and Japan reduce out-of-pocket expenses, encouraging first-time ownership and predictable five-year replacement cycles[2]Centers for Medicare & Medicaid Services, “Medicare Coverage of Mobility Assistive Equipment,” cms.gov . The Asia-Pacific region is experiencing the fastest incremental demand growth, driven by China’s and India’s expanding elderly populations and the emergence of local private-insurance riders that mirror U.S. Medicare Advantage benefits. Finally, price volatility for battery raw materials and mismatched global safety regulations temper near-term margins but do not derail the overarching growth trajectory.

Key Report Takeaways

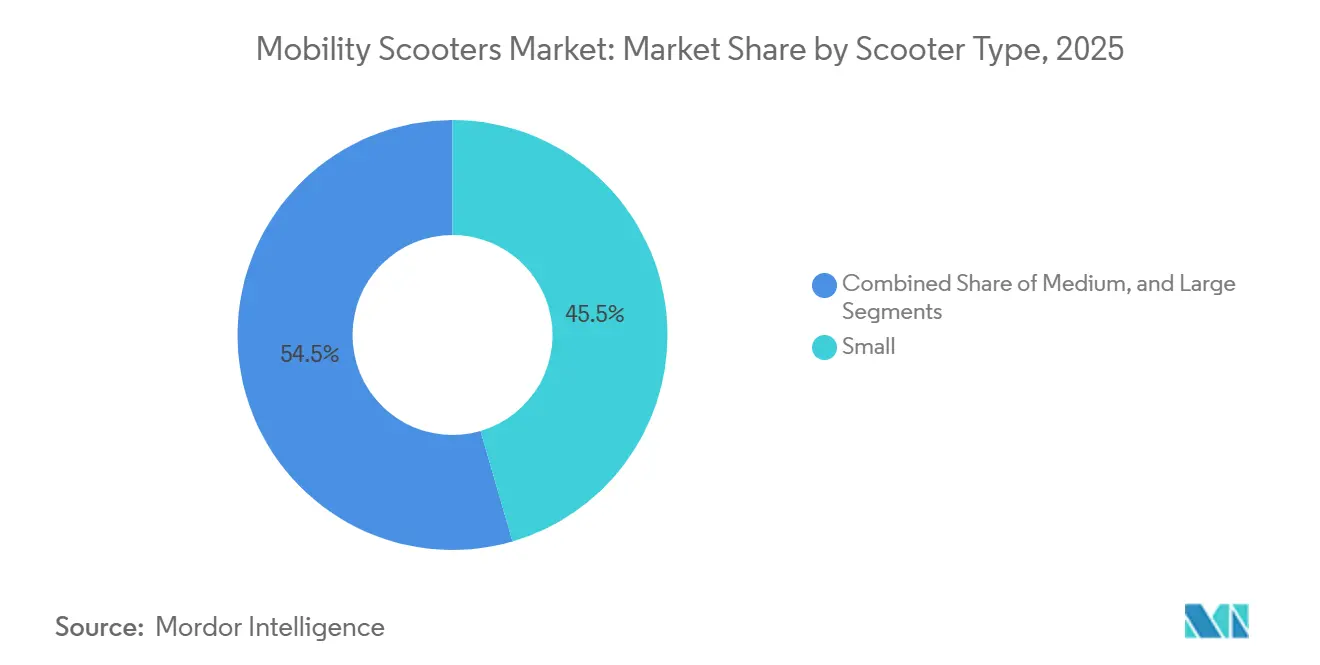

- By scooter type, compact models under 110 centimeters held 45.55% of the mobility scooters market share in 2025; large scooters above 150 centimeters are forecast to expand at a 9.25% CAGR through 2031.

- By wheel count, four-wheel designs commanded 57.53% of the mobility scooter market in 2025, and the segment will advance at a 7.85% CAGR through 2031.

- By battery range, the 10-20 mile segment accounted for 45.23% of the mobility scooter market in 2025; models offering more than 20 miles are growing at a 9.55% CAGR through 2031.

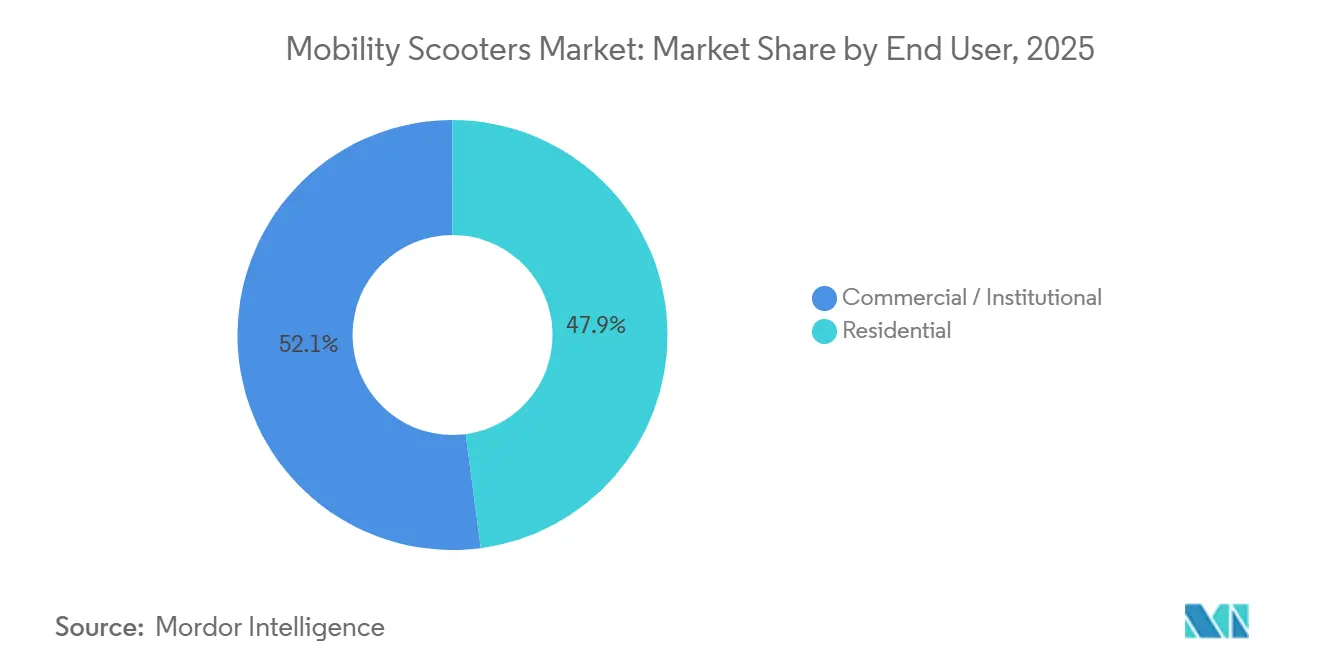

- By end user, commercial and institutional buyers accounted for 52.13% of 2025 revenue in the mobility scooters market and are projected to grow at an 8.81% CAGR through 2031.

- By geography, North America led with a 39.13% revenue share in 2025, while Asia-Pacific recorded the fastest regional CAGR of 8.52% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mobility Scooters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Global Aging and Chronic-Disease Prevalence | +2.1% | Global, with highest intensity in Asia-Pacific (China, Japan, South Korea) and Europe (Italy, Germany) | Long term (≥ 4 years) |

| Lithium-Ion Battery Cost Per Kwh Below USD 100 Enables Longer-Range Models | +1.3% | Global, with early adoption in North America and Europe; spillover to Asia-Pacific urban centers | Medium term (2-4 years) |

| Medicare and Private-Insurance Reimbursement Expansion | +1.5% | North America core; emerging in select Asia-Pacific markets (Australia, Japan) | Medium term (2-4 years) |

| Smart-Connected Scooters with IOT and GPS Enable Remote Monitoring and Fleet Management | +0.9% | North America and Europe commercial/institutional segments; pilot deployments in Asia-Pacific airports and hospitals | Short term (≤ 2 years) |

| Duty-Free Imports of Mobility Aids in ASEAN Emerging Markets | +0.6% | ASEAN member states (Thailand, Vietnam, Indonesia, Philippines); limited spillover to South Asia | Medium term (2-4 years) |

| Carbon-Fiber Chassis Cuts Scooter Weight by Over 30%, Widening Eligible User Base | +1.1% | Global, with premium-segment penetration in North America and Europe; gradual diffusion to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Global Aging And Chronic-Disease Prevalence

Japan’s elderly share reached 29.1% in 2023, while China counted 297 million people aged 60+ and is on course to surpass 400 million by 2035[3]Statistics Bureau of Japan, “Population Estimates by Age,” stat.go.jp. Cardiovascular and diabetic comorbidities climb in parallel, shifting the user profile from episodic rehabilitation to daily mobility needs. Demographic pressure is particularly acute in India, where the elderly cohort is projected to more than double from 149 million in 2022 to 347 million by 2050. These structural forces translate into rising first-time purchases and a shortening replacement cycle as users depend on scooters for full-time independence[4]World Health Organization, “Noncommunicable Diseases Country Profiles 2024,” who.int.

Lithium-Ion Battery Cost Below USD 100/kWh Enables Longer-Range Models

Average lithium-iron-phosphate pack prices fell beneath the USD 100/kWh threshold in 2023, rendering 20-mile-plus scooters cost-competitive with legacy 10-mile lead-acid units. The over-20-mile category is growing at 9.55% CAGR, as rural owners and outdoor enthusiasts value all-day autonomy. Faster four-to-six-hour charging further widens appeal, while carbon-fiber chassis offsets the added battery mass. As battery costs continue to decline, extended-range models become accessible to mid-income households that previously rented equipment for infrequent outings.

Medicare And Private-Insurance Reimbursement Expansion

The 2024 update to U.S. HCPCS codes K0800–K0808 raised the covered payload to 600 pounds, opening reimbursement to bariatric users. Medicare Advantage enrollment surpassed 54% of eligible beneficiaries in 2025, frequently lowering copays to zero for in-network providers and supporting a predictable five-year renewal cycle. Australia’s National Disability Insurance Scheme and Japan’s national health program are piloting similar reimbursement pathways, signaling a worldwide shift toward preventive coverage for personal mobility devices.

Smart-Connected Scooters With IoT And GPS Enable Remote Monitoring And Fleet Management

WHILL Inc. and Scootaround deploy telematics-enabled fleets that track real-time location, battery status, and usage metrics, delivering 22% lower idle time and a 15% boost in asset turns compared with manual dispatch. Teltonika and Wialon solutions feed predictive-maintenance analytics that minimize downtime and extend battery life. Such data-centric efficiencies encourage airports, hospitals, and convention centers to expand their scooter inventories, thereby reinforcing the commercial share of the mobility scooter market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sparse Public Charging and Curb-Cut Infrastructure in Developing Economies | -1.2% | Sub-Saharan Africa, South Asia, Southeast Asia (excluding Singapore), Latin America (excluding Chile urban centers) | Long term (≥ 4 years) |

| Fragmented Safety Regulations Raise Certification Costs for OEMs | -0.8% | Global, with highest friction at FDA-EU MDR-TGA-NMPA regulatory boundaries | Medium term (2-4 years) |

| Lithium Price Volatility Inflates Battery Pack Average Selling Prices by Over 15% Year-Over-Year | -0.6% | Global, with highest exposure in Asia-Pacific manufacturing hubs (China, South Korea) and spillover to all geographies | Short term (≤ 2 years) |

| Rising Product-Liability Claims Inflate Insurance Costs for Manufacturers | -0.4% | North America and Europe core; emerging risk in Asia-Pacific as litigation frameworks mature | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sparse Public Charging And Curb-Cut Infrastructure In Developing Economies

World Bank studies highlight that only 38% of surveyed bus stops in Madrid met minimum boarding-area dimensions, underscoring universal gaps that are more severe in low-income regions. Limited curb cuts, steep ramp grades, and the absence of charging facilities impede daily use, particularly in Sub-Saharan Africa and South Asia. Without accessible infrastructure, potential users rely on caregivers or public transport, slowing household adoption despite latent demand.

Fragmented Safety Regulations Raise Certification Costs For OEMs

Manufacturers face parallel 510(k) submissions to the FDA, conformity assessments under EU MDR 2017/745, and localized dossiers for Australia’s Therapeutic Goods Administration. Overlapping test protocols and language-specific documentation inflate development expenses by 12-18%, a burden most acutely felt by small and mid-sized brands. This fragmentation delays multi-region launches and encourages OEMs to prioritize single-region rollouts, limiting global volume efficiencies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Scooter Type: Compact Models Dominate, Yet Large Variants Accelerate

Compact units under 110 centimeters accounted for 45.55% of the mobility scooter market in 2025, favored for tight indoor turns in apartments, supermarkets, and hospitals. Medium designs serve dual indoor-outdoor roles but face incremental competition from increasingly lightweight large models. The large-segment mobility scooter market is projected to expand at a 9.25% CAGR through 2031 as carbon-fiber frames shed over 30% of chassis mass, enabling vehicle loading for older adults. Carbon constructions also damp vibration by 18%, improving ride comfort over rough terrain and elevating recreational appeal.

Weight reduction dovetails with evolving user behavior: one in two large-scooter owners transport the device in personal vehicles for leisure travel. Pride Mobility’s 35-pound Go-Go Carbon and Rascal’s 46-pound Carbon Cruiser exemplify this pivot to portability. Manufacturers maintain ISO 7176 stability compliance, ensuring safety parity across sizes. Collectively, these innovations raise large-segment share without cannibalizing compact indoor demand.

By Wheel Count: Four-Wheel Stability Preference Entrenched

Four-wheel platforms dominated the mobility scooter market with 57.53% market share in 2025, rising at a 7.85% CAGR as outdoor users value enhanced traction and payload capacity. A 2024 comparative study recorded 23% less lateral sway on 5-degree slopes and 31% better gravel grip versus three-wheel peers. The 60/40 rear-front weight balance lowers tip-over risk, a critical safety factor given rising product-liability claims.

Indoor-only riders still favor three-wheel maneuverability, but expanding curb-cut infrastructure and recreational popularity tilt preferences toward four-wheel stability. Flagship lines from Pride, Invacare, and Golden Technologies now default to four-wheel configurations, signaling an entrenched market trend.

By Battery Range: Mid-Range Dominates, Extended Range Surges

Scooters offering 10–20 miles captured 45.23% of 2025 revenue, matching typical daily errands that seldom exceed 15 miles. Models below 10 miles serve hospitals and retirement campuses where chargers are pervasive. However, the over-20-mile segment is the fastest-growing, up 9.55% CAGR, as rural residents and campers demand single-charge autonomy.

Charge times have fallen to four to six hours for lithium-ion packs, and destination-charging pilots at parks and malls may further lift mid-range model appeal. Until then, extended-range versions remain the solution for car-free day trips, hiking trails, and suburban commutes.

By End User: Commercial Buyers Lead, Residential Segment Accelerates

Commercial and institutional customers held 52.13% of 2025 turnover, driven by data-enabled fleet services that promise higher asset turns. WHILL’s autonomous airport program and Scootaround’s revenue-share resort fleets illustrate a shift from one-time sales to recurring service income. The residential segment is expected to post an 8.81% CAGR through 2031 as aging-in-place incentives, lighter models, and better insurance coverage spur ownership.

Economic logic supports purchase over rental: at a retail price of USD 1,500, a mid-range scooter breaks even after 5 months, versus weekly rentals costing USD 150. Residential buyers prioritize aesthetics and folding mechanisms, while institutional purchasers demand modular parts and multi-year warranties, creating divergent design roadmaps for suppliers.

Geography Analysis

North America contributed 39.13% of the 2025 mobility scooters market revenue, sustained by Medicare Part B’s 80% reimbursement and an 8,000-strong durable medical equipment retail network. The United States had 58 million people aged 65+ in 2024, a figure projected to hit 82 million by 2050, anchoring replacement demand as five-year coverage terms lapse. Canada’s provincial assistive-device programs complement private insurance, although income testing and variable copays introduce regional disparities.

Asia-Pacific is the fastest-growing region, forecast to grow at an 8.52% CAGR through 2031. China’s 21.1% elderly share equates to 297 million people, and India’s elderly population is on a path to 347 million by 2050, fueling large-scale adoption once reimbursement frameworks mature. Japan’s long-term care insurance and Australia’s NDIS subsidies further accelerate uptake, while South Korea’s aging trajectory boosts demand for compact scooters that fit dense urban layouts.

Europe remains steady, with elders comprising 21.3% of the EU population in 2023 and uniform MDR regulations simplifying cross-border product approvals. Italy and Germany post the highest national shares at 24.5% and 26.8%, respectively, preserving baseline sales despite budget-strained health systems. South America and the Middle East are nascent yet record double-digit growth in Brazil and the Gulf Co-operation Council where subsidy pilots begin to mirror Western insurance models

Competitive Landscape

The mobility scooters market is moderately fragmented. The top five brands—Pride Mobility, Invacare, Drive DeVilbiss, Golden Technologies, and Sunrise Medical—collectively command a sizable share but leave headroom for regional specialists. Private-equity consolidation is reshaping dynamics: Platinum Equity bought Sunrise Medical in June 2024, and MIGA Holdings acquired Invacare’s North American unit in November 2024, unlocking cross-portfolio economies of scale.

Technology and cost form the competitive cleavage. Premium brands integrate IoT sensors, GPS tracking, and smartphone apps. At the same time, value-tier Chinese manufacturers such as Shanghai Wisking serve price-sensitive ASEAN and Latin American buyers through offshore assembly lines operated at 30–40% lower cost. Carbon-fiber innovation, exemplified by Pride’s Go-Go Carbon, reduces unit weight by 35%, attracting users who drive personal vehicles. Conversely, modular battery bays and auto-fold designs like Quingo’s Flyte Mk2, which cuts setup time to 12 seconds, cater to travelers and urban commuters.

Regulatory hurdles persist. Distinct FDA, EU MDR, and TGA pathways favor incumbents that maintain dedicated regulatory teams. Fleet services remain under-penetrated at below 15% of total revenue but promise stickier recurring income. Scootaround and Mobility Equipment Recyclers pioneer venue-based models that tie equipment supply to revenue-share contracts, converting what was once a purely transactional sale into a life-cycle service relationship.

Mobility Scooters Industry Leaders

Drive DeVilbiss

Golden Technologies

Invacare

Pride Mobility Products Corp.

Sunrise Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: ALIMCO launched an electric scooter tailored for Divyangjan and seniors, advancing India’s accessible-mobility landscape.

- February 2025: Pride Mobility unveiled the Go Go Elite Traveller 2 Platinum with upgraded features for enhanced ride comfort.

Global Mobility Scooters Market Report Scope

As per the report's scope, mobility scooters are battery-powered personal mobility devices designed to assist individuals with limited mobility in traveling short to moderate distances independently. They typically feature a seat, handlebars or tiller steering, and multiple wheels for stability. Mobility scooters are widely used by elderly and physically challenged users for indoor and outdoor mobility, enhancing independence and quality of life.

The mobility scooters market segmentation includes scooter type, wheel count, battery range, end user, and geography. By scooter type, the market is segmented into small, medium, and large. The wheel count, the market is segmented into three-wheel and four-wheel. The battery range is segmented into < 10 miles, 10–20 miles, and > 20 miles. The end user market is segmented into residential and commercial/institutional. By geography, the global market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Small (< 110 cm) |

| Medium (110–150 cm) |

| Large (> 150 cm) |

| Three-Wheel |

| Four-Wheel |

| < 10 miles |

| 10–20 miles |

| > 20 miles |

| Residential |

| Commercial / Institutional |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Scooter Type | Small (< 110 cm) | |

| Medium (110–150 cm) | ||

| Large (> 150 cm) | ||

| By Wheel Count | Three-Wheel | |

| Four-Wheel | ||

| By Battery Range | < 10 miles | |

| 10–20 miles | ||

| > 20 miles | ||

| By End User | Residential | |

| Commercial / Institutional | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current global value of the mobility scooters market?

The market is valued at USD 2.54 billion in 2026, with a forecast to reach USD 3.63 billion by 2031.

How fast is demand expected to grow in Asia-Pacific?

Asia-Pacific is projected to advance at an 8.52% CAGR through 2031, the fastest regional pace.

Which scooter type is growing quickest?

Large models over 150 centimeters are expanding at a 9.25% CAGR thanks to lightweight carbon-fiber frames.

What share do four-wheel scooters hold?

Four-wheel designs accounted for 57.53% of global revenue in 2025.

How are reimbursement policies affecting ownership?

U.S. Medicare and similar pilots in Australia and Japan now cover up to 80% of unit costs, lowering financial barriers and encouraging predictable five-year replacements.

Page last updated on: