Mobile ECG Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

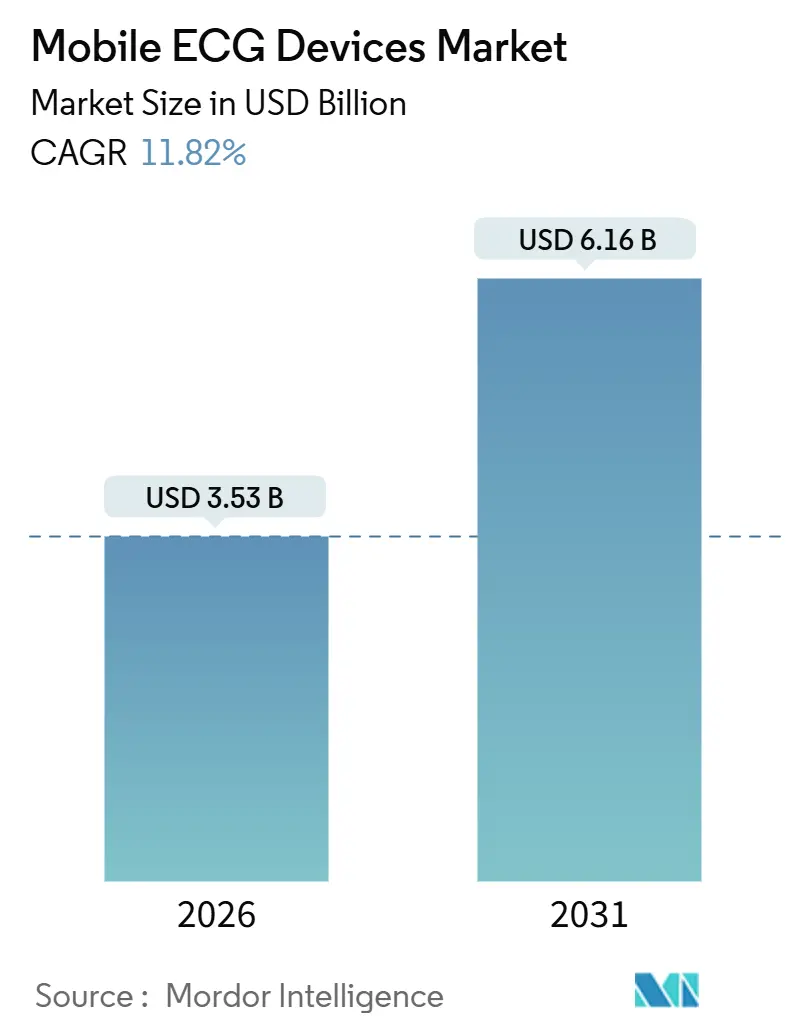

| Market Size (2026) | USD 3.53 Billion |

| Market Size (2031) | USD 6.16 Billion |

| Growth Rate (2026 - 2031) | 11.82% CAGR |

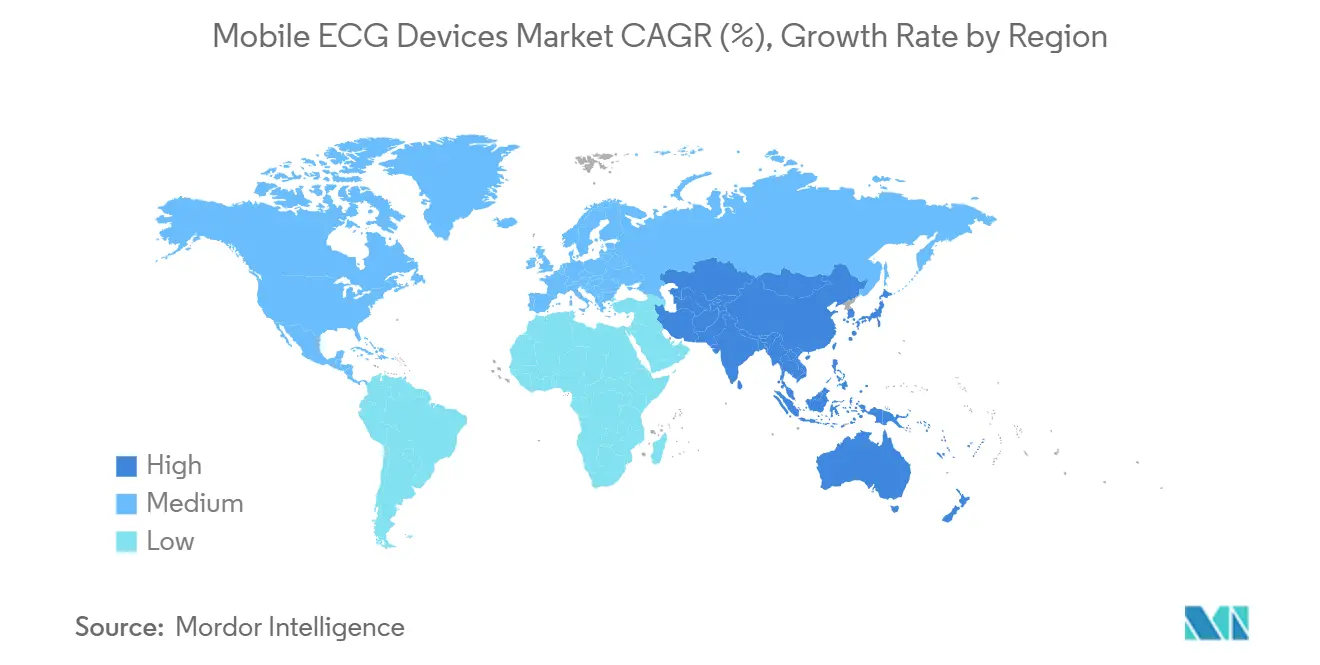

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

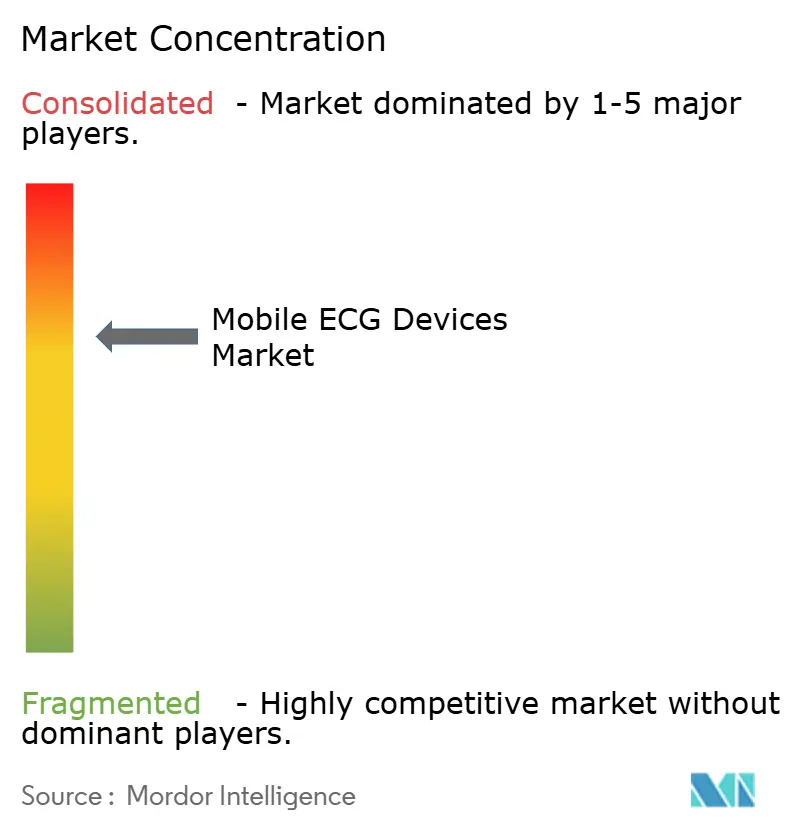

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile ECG Devices Market Analysis by Mordor Intelligence

The mobile ECG devices market size is projected to account for USD 3.53 billion in 2026 and is forecast to reach USD 6.16 billion by 2031, reflecting an 11.82% CAGR as cardiovascular disease prevalence, supportive reimbursement, and AI-driven diagnostics combine to accelerate adoption FDA. Uptake is strongest where payer policy rewards remote patient monitoring, semiconductor near-shoring cuts hardware lead times, and AI algorithms outperform manual interpretation. Continuous patch sensors, reimbursement for home-based care, and flexible electronics that lengthen wearable life are reinforcing one another, steadily shifting demand from episodic, clinic-based spot checks toward always-on cardiac surveillance. Competitive intensity remains moderate because leading brands still account for less than half of global revenue, which leaves room for region-focused specialists that offer tightly integrated hardware-software bundles. Even so, looming security mandates and state-by-state Medicaid variation add cost and timing uncertainty that could widen the gap between well-funded incumbents and start-ups.

Key Report Takeaways

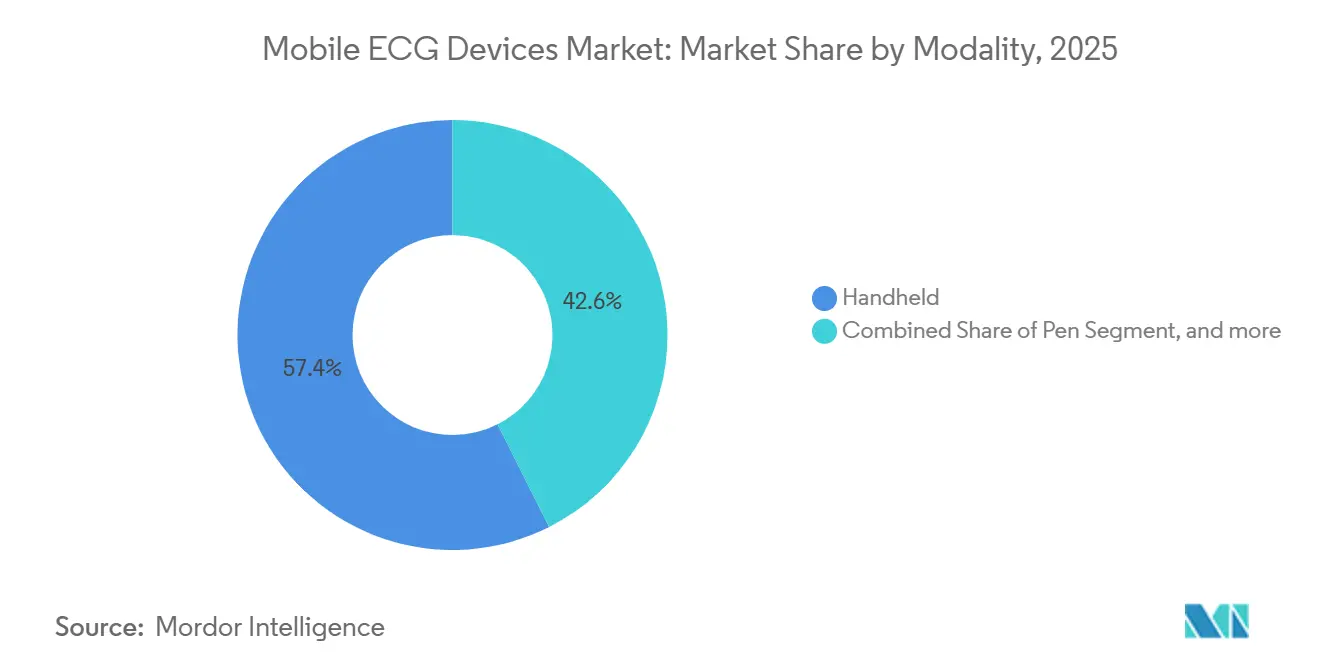

- By modality, handheld systems led with 57.43% revenue share in 2025, while patch-style sensors are projected to expand at a 13.54% CAGR through 2031.

- By end user, hospitals and diagnostic centers controlled 65.43% of spending in 2025, but home care settings are poised for 13.21% CAGR growth through 2031.

- By lead count, single-lead units supplied 42.45% of 2025 volume, yet systems with more than 12 leads will advance at a 13.65% CAGR.

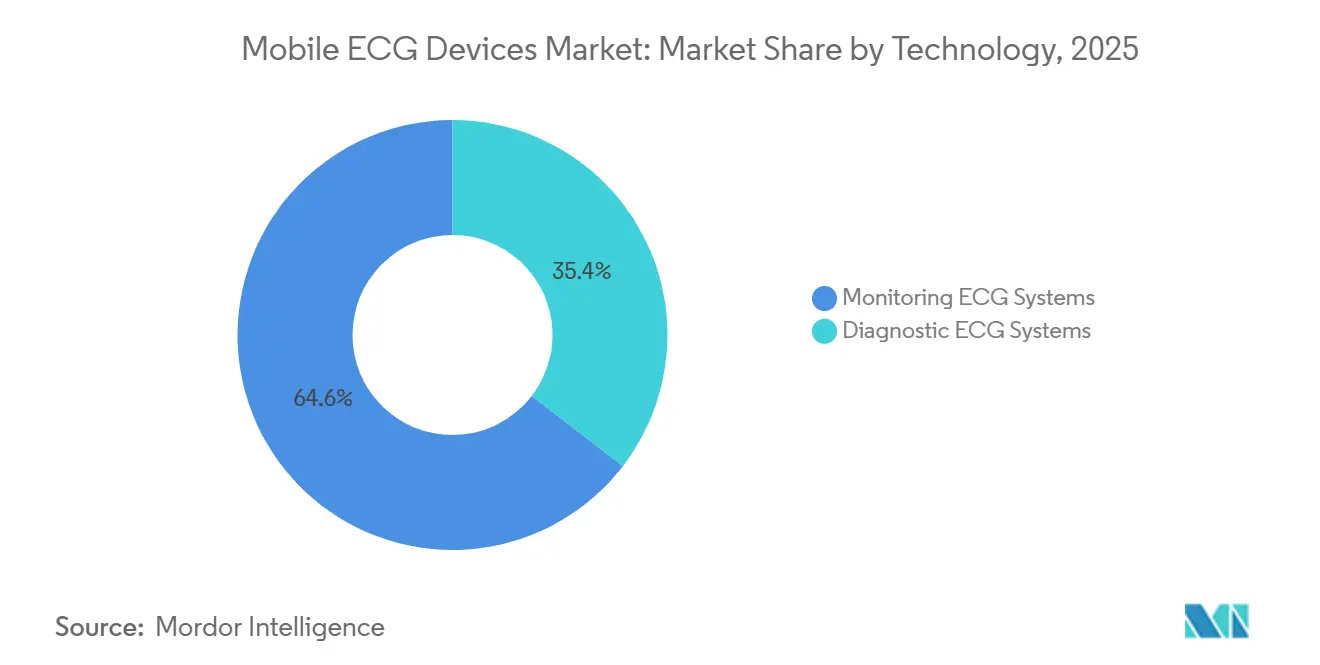

- By technology, monitoring platforms delivered 64.56% of 2025 sales, whereas diagnostic ECG systems will accelerate at a 14.32% CAGR on the back of AI-enabled interpretation.

- By application, arrhythmia detection generated 56.76% of 2025 revenue, but myocardial infarction monitoring is forecast to post the fastest 14.62% CAGR through 2031.

- By geography, North America captured 42.65% of 2025 revenue, while Asia-Pacific is set to record the highest CAGR of 12.54% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mobile ECG Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cardiovascular Disease Burden | +3.2% | Global, acute in North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Growing Adoption of Remote Patient Monitoring and Telehealth | +2.8% | North America and Europe lead, APAC accelerating | Medium term (2-4 years) |

| Technological Advancements in Miniaturization, AI, and Connectivity | +2.4% | Global R&D hubs in North America, Europe, East Asia | Medium term (2-4 years) |

| Integration into Consumer Wearables and DTC Health Platforms | +1.9% | North America, Western Europe, affluent APAC metros | Short term (≤ 2 years) |

| Reimbursement Expansion for Remote ECG CPT Codes | +1.5% | United States, selectively in Canada and U.K. | Short term (≤ 2 years) |

| Supply-Chain Nearshoring Reducing Device Lead Times | +1.2% | United States and Mexico manufacturing corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Cardiovascular Disease Burden

Cardiovascular diseases caused 19.8 million deaths in 2022, equal to 32% of all global mortality, and associated disability continues to climb. In 2025, the American Heart Association reported that 48.6% of U.S. adults live with at least one cardiac diagnosis[1]American Heart Association, “Heart Disease and Stroke Statistics 2025 Update,” heart.org. Health systems are therefore shifting resources toward proactive surveillance that can identify silent arrhythmias missed by annual check-ups. Aging demographics intensify the need; Japan made remote ECG compulsory for all patients after myocardial infarction as part of its Society 5.0 program. India followed suit through Ayushman Bharat, adding mobile ECG screening for 500 million beneficiaries.

Growing Adoption of Remote Patient Monitoring and Telehealth

Medicare began paying providers for each 30-day ECG monitoring cycle under CPT codes 99454 and 99457 in 2024, creating a recurring revenue stream of USD 110–150 per patient. Commercial insurers such as UnitedHealthcare adopted parallel policies in 2025, shortening mandated monitoring windows and lowering dropout rates. Telecardiology accounted for 34% of cardiology visits in 2025, after parity laws were enacted in 42 U.S. states. Europe mirrored these moves when the U.K. National Health Service recommended remote ECGs for all atrial fibrillation patients post-ablation.

Integration into Consumer Wearables and DTC Health Platforms

Apple Watch Series 10 received FDA clearance for atrial fibrillation detection with 98.3% specificity in late 2024. Samsung followed up with the Galaxy Watch 7, which covers heart-rate ranges from 30 to 200 bpm, and sold 8.2 million units in nine months. Subscription platforms such as Hims & Hers bundle a mobile ECG and virtual cardiology consults for USD 79 per month, below typical clinic fees. Fitbit’s link to Google Health Connect lets users share wearable ECG data directly with hospital EHRs, closing a long-standing interoperability gap.

Technological Advancements in Miniaturization, AI, and Connectivity

Graphene electrodes only 0.3 mm thick entered mass production in 2025, bringing skin-conformal patches that do not degrade signal during exercise. AI models trained on 10 million annotated ECGs now detect arrhythmias with AUROC > 0.95, outperforming general cardiologists. The FDA cleared 14 new AI-enabled ECG algorithms in 2025, underscoring regulatory confidence. Power-efficient Bluetooth 5.3 and NB-IoT radios have extended patch battery life from 7 to 21 days, allowing patients to wear a single device throughout a complete diagnostic cycle[2]Institute of Electrical and Electronics Engineers, “Bluetooth Low Energy 5.3 Specification,” ieee.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device and Ownership Costs | –1.8% | Emerging APAC, Latin America, sub-Saharan Africa; U.S. uninsured | Medium term (2-4 years) |

| Inconsistent Reimbursement Policies | –1.5% | United States, fragmented EU systems | Long term (≥ 4 years) |

| Tariff Volatility on Electronic Components | –1.2% | U.S.–China trade lanes, EU imports from Asia | Short term (≤ 2 years) |

| Increasing Cybersecurity Certification Requirements | –1.0% | United States, EU, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Device and Ownership Costs

Retail prices run from USD 79 to USD 449 for handhelds and up to USD 600 for a single 14-day patch cycle, levels that exceed annual per-capita health spend in many low-income countries[3]World Bank, “World Development Indicators: Health Expenditure Per Capita,” worldbank.org. Even insured U.S. patients in high-deductible plans must often pay the full cost until their deductibles, averaging USD 1,644, are met. Budget models under USD 50 exist in China and India but lack FDA or CE clearance, confining them to wellness rather than diagnostic use and fragmenting demand by regulatory grade. Component prices have not fallen as quickly as expected; analog front-end ICs still add USD 3–8 per unit and radio chips another USD 2–4, limiting room for meaningful price cuts.

Inconsistent Reimbursement Policies

Texas Medicaid pays USD 64.44 per 30-day ECG cycle, while New York reimburses USD 51.88, and eight states exclude RPM entirely, forcing providers to either absorb losses or forgo Medicaid patients. Private-payer hurdles persist; Cigna requires prior authorization and 21-day monitoring windows, although FDA-cleared devices can meet diagnostic needs in 14 days. Fragmentation in Europe mirrors that in the U.S.; Germany’s DiGA pathway reimburses mobile ECG apps nationwide, whereas Italy leaves decisions to regions, resulting in eightfold variability in payments. In India, the Ayushman Bharat reimbursement rate of INR 150 (USD 1.80) per test does not cover device amortization, limiting hospital uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: Patch Sensors Gain Momentum

Patch and other skin-conformable sensors are set to achieve a 13.54% CAGR through 2031, after holding 42.57% of the mobile ECG devices market share in 2025. Handheld systems, while still dominant, increasingly serve acute-care snapshots rather than multi-day surveillance. Patch wear-time now reaches 21 days thanks to thin graphene electrodes, and real-world studies show 96% arrhythmia capture versus 67% with 24-hour Holter monitors, compelling payers to back longer tracking windows. Early discomfort issues have faded because hydrogel adhesives with lower pH irritation scores replaced traditional silver chloride. In 2024, FDA guidance also established a clear 510(k) predicate pathway for patch devices equivalent to Holter systems, reducing review cycles to about 5 months. Handheld units now emphasize AI-assisted 12-lead diagnostics for emergency-department triage, a niche where patches cannot yet deliver rapid full-lead placement.

Continuous innovation and recurring reimbursement reinforce patch uptake. The combination of lower battery drain and cloud analytics supports a subscription revenue model that appeals to providers shifting to value-based contracts. Handheld sales remain healthy for spot checks but lack the continuous data streams that underpin AI algorithm refinement. Patches, therefore, capture more training data, improving algorithm sensitivity and further widening the performance gap. As a result, POC diagnostics in community settings increasingly default to disposable patches mailed back to central labs, moving handheld devices toward secondary roles in physician offices and urgent-care centers.

By End User: Homecare Accelerates

Hospitals retained 65.43% of 2025 demand, yet home-based deployment is on track for a 13.21% CAGR. The mobile ECG devices market size generated in home care rose sharply once Medicare introduced separate RPM service codes in 2024. Unbundling RPM payments from evaluation-and-management visits has helped small practices adopt subscription monitoring in place of fee-for-service ECG strips. Hospital-at-home pilots in the United Kingdom reduced 30-day readmissions by 22%, demonstrating that post-discharge cardiac surveillance can shift costs away from inpatient wards.

At-home monitoring dovetails with caregiver fatigue solutions such as automated cloud alerts that spare family members from constant watch. Cellular-enabled patches eliminate smartphone dependency, expanding reach to older adults who do not own high-end handsets. Hospitals will continue to dominate acute-care diagnostics, but accelerating bundled-payment models and steep facility overheads make it attractive for health systems to push routine rhythm checks into the home. Ambulatory clinics face margin compression because a single in-office ECG visit reimburses at USD 17. In contrast, the same provider can earn several times that across a month of remote monitoring with only modest extra labor.

By Lead Type: Multi-Lead Portables Expand

Single-lead wearables provided 42.45% of 2025 shipments. However, systems with more than 12 leads will grow at a 13.65% CAGR, as rural clinics and EMS teams use portable, diagnostic-equivalent devices to avoid patient transfers. Adding extra leads raises the bill-of-materials by only USD 4-7 yet elevates clinical value enough to win higher reimbursement. Such devices detect posterior and right ventricular infarctions that a standard 12-lead ECG can miss, improving early MI triage accuracy by 19 percentage points in multicenter trials.

The mobile ECG devices market size linked to 3-6-lead systems is also climbing, but faces commoditization because manufacturing complexity tails off quickly once electrode counts exceed one. Regulatory perception favors full 12-lead capability; hospitals often select complete diagnostic systems even for outpatient use to avoid multiple device inventories. For consumer wearables, single-lead units still dominate because cost, battery life, and comfort matter more than ischemia localization. Yet even there, software-based vector reconstruction is under development, suggesting that future smartwatch ECGs may virtually simulate multi-lead functionality.

By Technology: Diagnostic Platforms Powered by AI

Monitoring devices accounted for 64.56% of spending in 2025, but diagnostic platforms are set for a 14.32% CAGR as AI improves interpretation accuracy to cardiologist-level performance. The boundary between the two categories is blurring; patches like Zio AT combine continuous monitoring with near-real-time ST-segment analysis that alerts clinicians within minutes. Medicare pays more for diagnostic encounters than for strip interpretation, motivating manufacturers to embed AI modules and seek higher-value CPT codes.

Regulatory oversight tightened in 2025 when the FDA required annual retraining of AI models to mitigate demographic bias. Compliance adds USD 150,000–300,000 per algorithm per year, favoring incumbents with large datasets. Still, algorithmic sensitivity above 98% for life-threatening arrhythmias convinced payers to broadly cover AI-enhanced diagnostics. Monitoring-only devices will remain the standard for chronic arrhythmia management. Still, their relative share will slide as precision improves and payers recognize that a single 30-second diagnostic tracing may obviate weeks of surveillance.

By Application: MI Monitoring Takes Off

Arrhythmia detection accounted for 56.76% of 2025 revenue, as atrial fibrillation prevalence remains high, while myocardial infarction monitoring is forecast to grow at the fastest 14.62% CAGR. Continuous ST-segment analysis detects ischemia 30–90 minutes before symptom onset, shortening door-to-balloon times and saving muscle. Preventive screening for asymptomatic adults is growing through employer and insurer programs, even though Medicare does not reimburse. Research use is small in terms of revenue but vital for pipeline validation, with more than 140 active clinical trials using mobile ECG endpoints.

The mobile ECG devices market share for MI monitoring will rise as algorithms gain FDA clearance for automated ischemia alerts and as EMS services integrate patch telemetry into dispatch protocols. Meanwhile, policy experiments in Europe that reimburse preventive ECG once every three years could broaden population screening and unlock a fresh consumer base.

Geography Analysis

North America accounted for 42.65% of global revenue in 2025, driven by RPM codes, dense cardiology networks, and fast FDA clearance pathways. Nearly 9 in 10 U.S. hospitals already integrate device feeds into their EHRs, allowing clinicians to review remote tracings without disrupting workflow. Canadian uptake trailed until federal funds earmarked for virtual care began flowing in late 2024, accelerating deployment in underserved provinces.

Asia-Pacific is the clear growth engine with a 12.54% CAGR projected for 2026–2031. China earmarked CNY 50 billion for telehealth infrastructure and aims to achieve 70% population coverage by 2030. India’s Ayushman Bharat Digital Mission links mobile ECG readings to unique health IDs, reducing rural referral waits from 18 days to 36 hours. Japan subsidizes 60% of monthly device costs for seniors, and South Korea added a wearable ECG to its national fee schedule in 2024.

Europe accounted for 23% of 2025 revenue but remains fragmented. Germany’s DiGA pathway reimbursed 14 ECG apps by 2025, whereas Italy still lacks a nationwide policy. Middle East & Africa and South America together supplied 11% of sales, constrained by low health-spend baselines but supported by World Bank-backed pilot buys of handheld 12-lead devices that reduced acute MI mortality by 17% in early deployments. Harmonized regulation is still years away; the new African Medicines Agency has yet to issue device guidance, elongating launch timelines.

Competitive Landscape

The top five players—AliveCor, iRhythm Technologies, Medtronic, Philips, and GE Healthcare—command roughly 38% of revenue, giving the mobile ECG devices market a moderate concentration profile. Incumbents differentiate through global regulatory footprints and peer-reviewed evidence: AliveCor’s KardiaMobile 6L holds clearances across three continents and is referenced in 47 clinical publications. Business models are tilting toward recurring service revenue; iRhythm derives 73% of its income from monitoring fees, delivering margins 18% higher than those from pure hardware sales.

Start-ups focus on pediatric monitoring, post-operative surveillance, and price points in emerging markets. One example is Corsano Health, which is trialing an on-device machine-learning patch that operates without cloud connectivity, appealing to GDPR-sensitive European hospitals. The FDA’s 2024 cybersecurity rule now requires SBOMs and post-market vulnerability patching, raising annual compliance costs by USD 200,000–400,000 and potentially squeezing smaller vendors. Patent data show 142 grants in 2024–2025, 38% of which cover AI algorithms, confirming that software remains the main battleground.

Hospitals that select devices with HL7-FHIR APIs adopt new ECG platforms 2.3 times faster, according to a 2024 KLAS survey, and vendors able to meet this interoperability bar are securing enterprise-level contracts. Supply-chain near-shoring under the CHIPS Act has reduced PCB and ASIC lead times from 14 to 9 weeks, enabling vendors to roll out annual hardware refreshes and to tighten feedback loops between clinicians and R&D teams.

Mobile ECG Devices Industry Leaders

AliveCor

iRhythm Technologies Inc.

Medtronic

Koninklijke Philips N.V.

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: HeartBeam, Inc., a medical technology company focused on transforming cardiac care by providing powerful personalized insights, announced that the U.S. Food and Drug Administration (FDA) has granted 510(k) clearance for the Company’s groundbreaking 12-lead electrocardiogram (ECG) synthesis software for the assessment of arrhythmias. This clearance follows HeartBeam’s successful appeal of a prior Not Substantially Equivalent (NSE) determination.

- May 2025: AliveCor, one of the leader in FDA-cleared personal electrocardiogram (ECG) technology launched its most advanced personal ECG system, the groundbreaking AI-powered KardiaMobile® 6L Max, alongside KardiaAlert — a first-of-its kind feature–available exclusively to KardiaCare subscribers.

- September 2024: Apple released Watch Series 10, adding sleep-apnea detection alongside its single-lead ECG app

Global Mobile ECG Devices Market Report Scope

As per scope of the report, mobile ECG devices are portable tools used to monitor and record the electrical activity of the heart remotely. They enable quick, convenient heart health assessments outside clinical settings. These devices help detect cardiac issues early and support continuous heart monitoring.

The Mobile ECG Devices Market is Segmented by Modality (Pen, Band, Handheld, and Other Modalities), End-User (Hospitals And Diagnostic Centers, Ambulatory Care, and Homecare), Lead Type (Single-lead, 3-6 lead, and Greater Than 12-lead), Technology (Monitoring ECG Systems and Diagnostic ECG Systems), Application (Arrhythmia Detection, Myocardial Infarction Monitoring, Preventive Health Screening, and Research & Clinical Trials), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Pen |

| Band |

| Handheld |

| Other Modalities |

| Hospitals And Diagnostic Centers |

| Ambulatory Care |

| Homecare |

| Single-lead |

| 3-6 lead |

| Greater Than 12-lead |

| Monitoring ECG Systems |

| Diagnostic ECG Systems |

| Arrhythmia Detection |

| Myocardial Infarction Monitoring |

| Preventive Health Screening |

| Research & Clinical Trials |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Modality | Pen | |

| Band | ||

| Handheld | ||

| Other Modalities | ||

| By End-User | Hospitals And Diagnostic Centers | |

| Ambulatory Care | ||

| Homecare | ||

| By Lead Type | Single-lead | |

| 3-6 lead | ||

| Greater Than 12-lead | ||

| By Technology | Monitoring ECG Systems | |

| Diagnostic ECG Systems | ||

| By Application | Arrhythmia Detection | |

| Myocardial Infarction Monitoring | ||

| Preventive Health Screening | ||

| Research & Clinical Trials | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the mobile ECG devices market in 2031?

The market is expected to reach USD 6.16 billion by 2031.

How fast is Asia-Pacific expected to grow for mobile ECG devices?

Asia-Pacific is projected to expand at a 12.54% CAGR from 2026 to 2031.

Which modality is forecast to grow fastest within mobile ECG deployments?

Patch-based and other skin-conformable sensors are forecast for a 13.54% CAGR through 2031.

What share did handheld ECG devices hold in 2025?

Handheld modalities captured 57.43% of 2025 revenue.

Which application segment is poised for the highest growth?

Myocardial infarction monitoring is projected to post a 14.62% CAGR through 2031.

Who are the leading players in mobile ECG devices?

AliveCor, iRhythm Technologies, Medtronic, Philips, and GE Healthcare together control about 38% of global revenue.

Page last updated on: