US Conducted Energy Weapons Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2019 - 2024 |

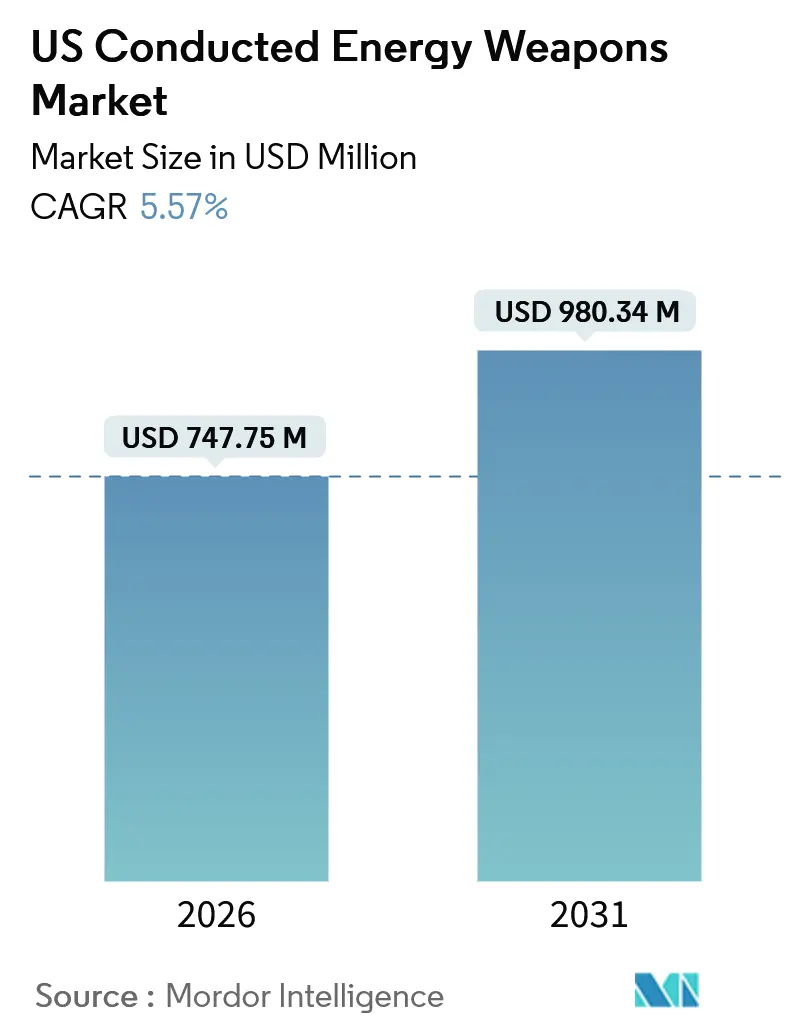

| Market Size (2026) | USD 747.75 Million |

| Market Size (2031) | USD 980.34 Million |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

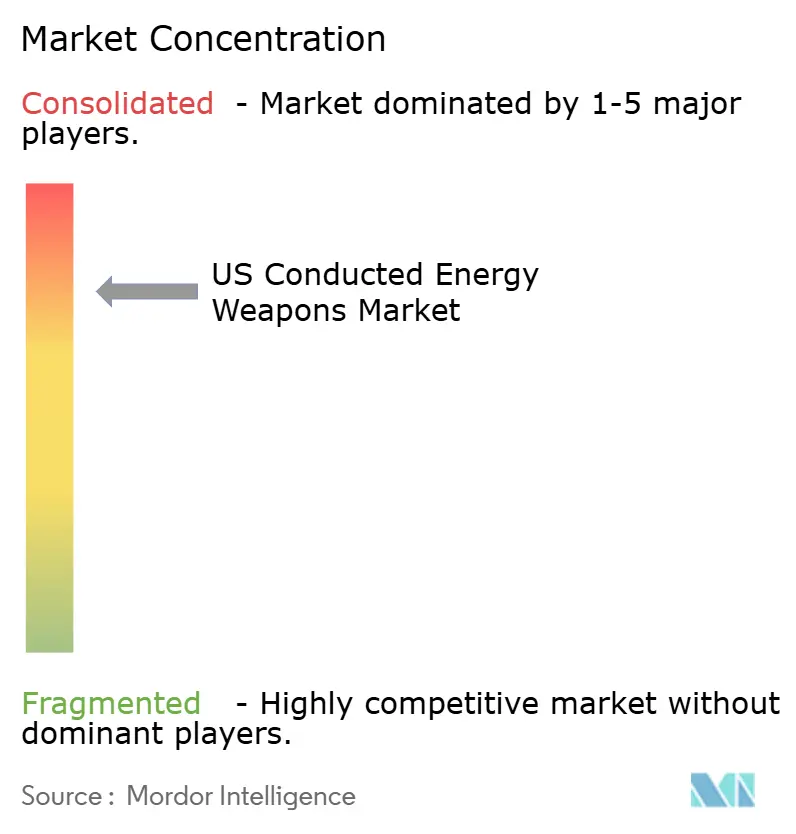

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Conducted Energy Weapons Market Analysis by Mordor Intelligence

The conducted energy weapons market size in the United States is projected to reach USD 980.34 million by 2031, reflecting a 5.57% CAGR over the forecast period, from USD 747.75 million in 2026. This steady headline growth conceals a shift in demand drivers, with law enforcement replacement cycles giving way to rising civilian purchases and rapid upgrades to dual-shot, innovative platforms. Federal de-escalation mandates, bundled training requirements, and integration with cloud-based evidence systems continue to drive agency spending, even as litigation risks rise. Civilian buyers tend to gravitate toward lightweight, rechargeable stun guns priced under $30, thereby fragmenting the personal protection segment across multiple brands. Meanwhile, corrections facilities are fueling demand for extended-reach stun batons that operate reliably in confined spaces, and weapon upgrades are outpacing cartridge replenishment as agencies migrate to TASER 10.

Key Report Takeaways

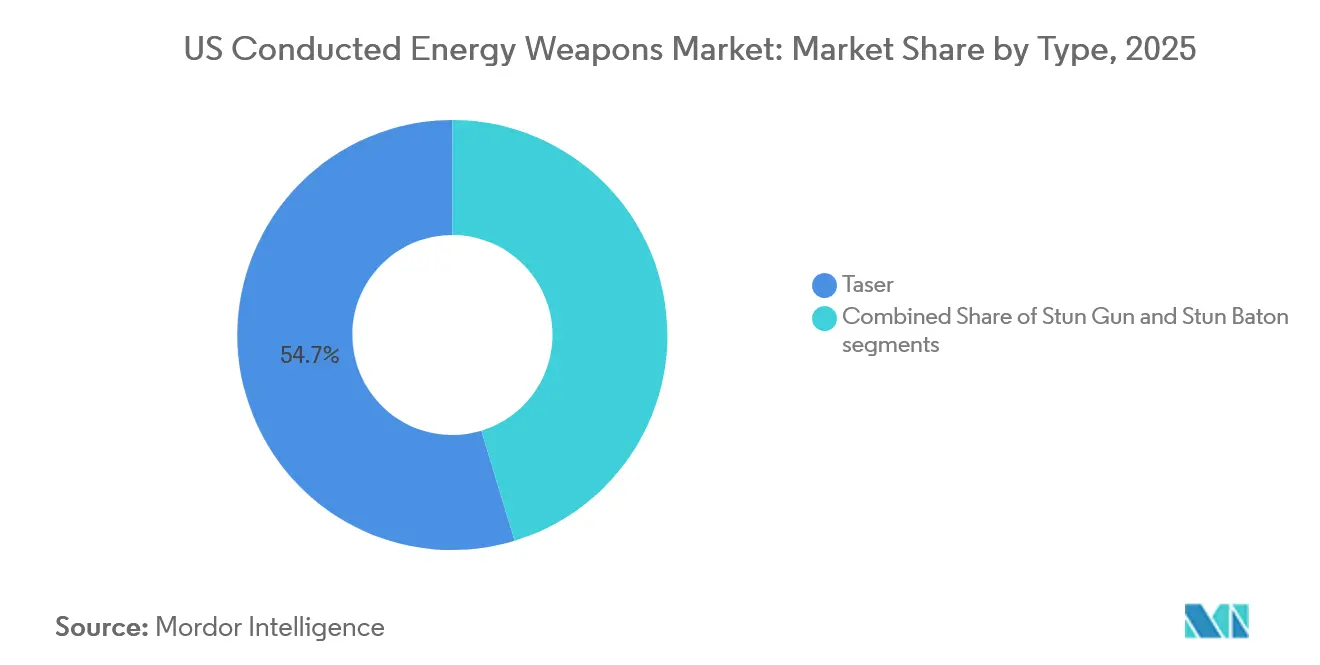

- By product type, tasers led with 54.67% revenue share in 2025; stun batons are projected to expand at a 5.97% CAGR through 2031.

- By equipment type, weapon platforms commanded 64.78% of the conducted energy weapons market size in 2025 and are projected to advance at a 6.12% CAGR through 2031.

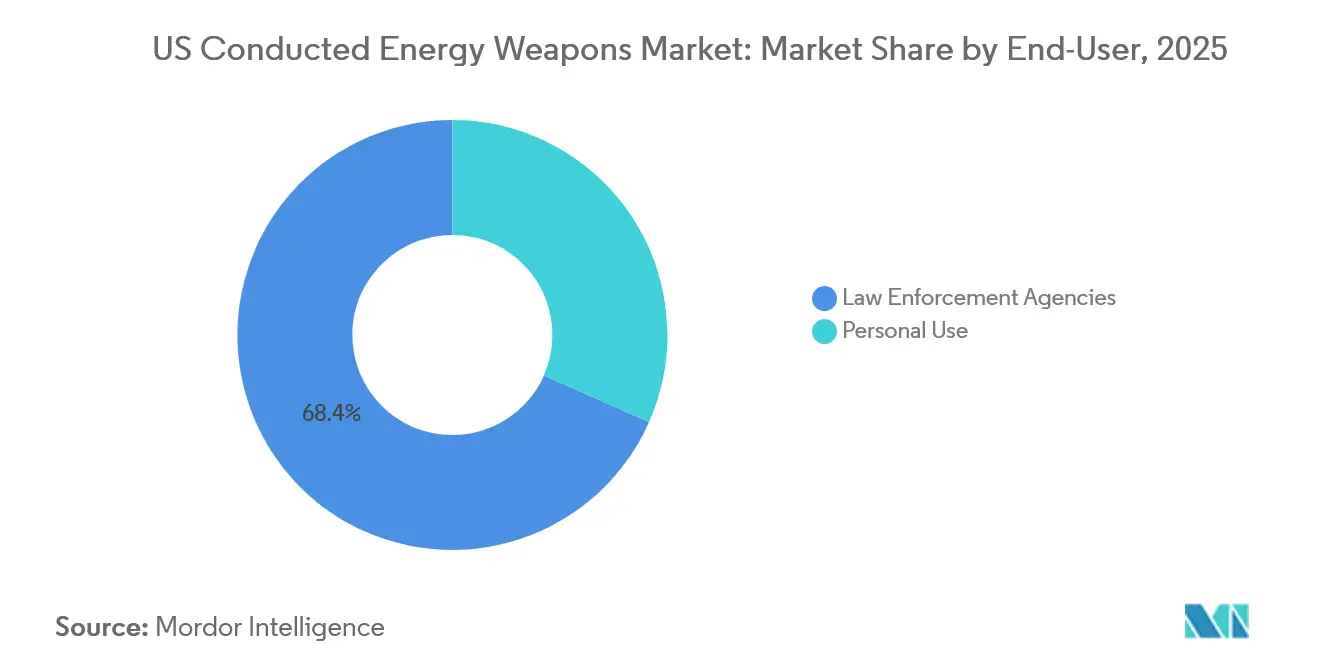

- By end-user, law enforcement agencies held 68.37% of the conducted energy weapons market share in 2025, while personal use is forecast to grow at a 6.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

US Conducted Energy Weapons Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal de-escalation grants fueling LE procurement | +1.2% | National, urban jurisdictions benefiting from BJA JAG and COPS BWC funding | Medium term (2-4 years) |

| Rising civilian demand for non-lethal self-defense devices | +1.5% | National, strongest in 49 states permitting ownership | Short term (≤ 2 years) |

| Smart CEWs with data analytics and AI capabilities | +1.1% | National, led by large metro departments adopting Evidence.com ecosystems | Long term (≥ 4 years) |

| State-level legalization expanding retail addressable market | +0.8% | State-specific jurisdictions easing permit requirements | Medium term (2-4 years) |

| Wearable CEWs for corrections and prisoner transport | +0.6% | National, early uptake in federal and large state corrections systems | Long term (≥ 4 years) |

| Integration with body-worn cameras and evidence ecosystems | +0.9% | National, mandated where BWC policies tie to grant compliance | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Federal De-escalation Grants Fueling LE Procurement

The Law Enforcement De-Escalation Training Act of 2022 links federal funding to alternative-force training, effectively positioning CEWs as compliant tools in grant-eligible purchase plans. JAG guidelines classify standalone weapons as “generally unallowable,” so agencies increasingly buy training-and-hardware bundles that satisfy eligibility rules. Axon reported TASER segment revenue of USD 238 million for Q3 2024, a 17% year-over-year increase, driven by upgrades to TASER 10 packages that include VR simulators and Evidence.com subscriptions.[1]“Axon Enterprise Q3 2024 Earnings Report,” Axon Investor Relations, investor.axon.com The COPS Office Body-Worn Camera program further reinforces this pattern by subsidizing systems that synchronize weapon data with video evidence. As a result, agency refresh cycles shorten despite municipal budget headwinds, sustaining the conducted energy weapons market.

Rising Civilian Demand for Non-Lethal Self-Defense Devices

Personal-use sales are rising at a 6.78% CAGR through 2031, nearly a percentage point faster than institutional procurement. Google Trends reported a 23% surge in searches for “self-defense stun guns with flashlights” between April and August 2025, confirming heightened safety concerns in urban and suburban areas. Budget-friendly Vipertek VTS-880 units sell for USD 15.99, while SABRE’s premium rechargeable models reach USD 199 and promote NIJ-compliant microcoulomb ratings. Forty-nine states allow civilian ownership; only Rhode Island bans CEWs outright, and Hawaii requires permits, adding complexity for national retailers. This fragmentation contrasts with Axon’s dominance in policing, creating a white space for brands that can navigate regulatory variance while offering transparent performance metrics.

Smart CEWs with Data Analytics and AI Capabilities

TASER 10, introduced in 2023, delivers dual-shot capacity, 45-foot range, and automatic data upload to Evidence.com, embedding AI analysis into every use-of-force report. Agencies adopting the platform also commit to multi-year cloud subscriptions and VR training, raising switching costs. The Los Angeles Police Department’s 2023 directive mandates the automatic transfer of data within 24 hours of deployment, a workflow reliant on Axon’s ecosystem. Competitors such as PhaZZer cannot match this software stack, limiting their appeal outside price-sensitive departments. Consequently, innovative capability, not voltage specs, drives procurement, reinforcing Axon’s platform strategy.

Integration with Body-Worn Cameras and Evidence Ecosystems

Federal BWC grant rules encourage equipment packages that auto-activate cameras when a CEW is armed, streamlining evidence capture and reducing report errors.[2]“Body-Worn Camera Policy and Implementation Program,” U.S. Department of Justice COPS Office, cops.usdoj.gov TASER 10 supports this synchronized workflow, turning each deployment into a data-rich event that populates Axon’s cloud dashboard. The LAPD’s 2023 policy exemplifies the compliance load, requiring uploads within 24 hours and immediate submission of medical documentation. Vendors without camera ecosystems must rely on agencies to manage separate platforms, raising administrative friction. The resulting integration advantage underpins Axon’s 17% TASER revenue growth in Q3 2024 despite flat officer headcounts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Litigation and liability cost escalation | -1.3% | National, concentrated in jurisdictions with high-profile cases | Short term (≤ 2 years) |

| Municipal budget constraints on LE spend | -0.9% | National, pronounced in mid-size cities facing revenue gaps | Medium term (2-4 years) |

| Patchwork regulations limiting civilian sales | -0.7% | State-specific, notably Rhode Island and Hawaii | Long term (≥ 4 years) |

| Public scrutiny calling for bans/moratoria | -0.6% | Urban jurisdictions with active reform coalitions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Litigation and Liability Cost Escalation

More than 1,000 deaths following CEW exposure have been cataloged by the Congressional Research Service, keeping wrongful-death suits in the spotlight and pushing insurers to raise municipal premiums.[3]“Report on Conducted Energy Devices,” Congressional Research Service, crsreports.congress.gov High-profile cases such as Keenan Anderson in 2023 intensified scrutiny, prompting directives that mandate medical exams and rapid data uploads after each use. Axon acknowledged “elevated legal expenses” during its Q3 2024 call, although it argues that robust training mitigates the risk. Smaller rivals have thinner balance sheets, which reduces their resilience to protracted litigation and consolidates market power among established players. Rising liability costs, therefore, dampen the overall growth of the conducted energy weapons market even as they entrench incumbent dominance.

Municipal Budget Constraints on LE Equipment Spend

Post-pandemic revenue gaps compel many cities to triage capital budgets, delaying CEW refresh cycles despite federal grants. Because JAG funds generally prohibit standalone CEW purchases unless paired with training, agencies must allocate scarce dollars to bundled packages that cost more upfront. The TASER 10 carries a significant premium over legacy TASER 7 units, forcing departments to justify their investments on data analytics grounds. COPS BWC grants offset some expenses, yet matching-fund requirements exclude fiscally strained jurisdictions. Budget pressure thus splits demand between large urban departments that can afford upgrades and smaller agencies that extend service lives or seek lower-cost alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Stun Batons Extend Reach for Corrections Operators

Tasers account for 54.67% of 2025 revenue, reflecting long-standing agency preference for ranged incapacitation platforms that integrate with cloud evidence systems. This share stems chiefly from Axon’s TASER 10 upgrade wave, which boosted CEW revenue by 17% in Q3 2024. In contrast, stun batons are projected to register the fastest growth at a 5.97% CAGR, driven by corrections officers who require a reliable drive-stun capability without the logistical burden of cartridge usage. Baton Rouge PD’s 2024 policy review endorses weekly function tests and capped exposure, reinforcing preference for contact devices in inmate transfer corridors.

Stun guns occupy the budget-friendly middle ground for civilians. Vipertek’s VTS-880 integrates flashlight and alarm functions at USD 15.99, appealing to buyers in 49 permissive states. SABRE’s rechargeable models, rated at 1.820 microcoulombs, command a premium price of USD 199 by leveraging their law enforcement pedigree.[4]“SABRE Product Catalog,” SABRE Security Equipment Corp., sabrered.com As NIJ pushes performance metrics beyond voltage claims, informed consumers are shifting evaluations toward charge delivery effectiveness, a trend that may alter future category shares.

By Equipment Type: Weapon Platforms Outpace Cartridge Sales

Weapons captured 64.78% of 2025 revenue and are projected to climb 6.12% annually to 2031, outperforming cartridges despite Axon’s consumable-centric business model. Agencies prioritize dual-shot TASER 10 upgrades to meet analytics and training requirements, compressing replacement cycles for older single-shot units. Extended-range cartridges priced at a premium elevate per-unit economics but slow volume replenishment, especially in budget-constrained municipalities. The personal segment relies on rechargeable designs that bypass cartridges entirely, shifting recurring revenue toward battery sales and accessories.

Legacy TASER 7 inventories still function adequately, encouraging some departments to stretch cartridge stockpiles rather than commit to complete platform swaps. BJA grant language accentuates this pattern by tying cartridge purchases to curriculum spending, further tempering demand growth for consumables. Over time, however, data-driven reporting obligations may prompt lagging agencies to undertake holistic platform refreshes, thereby maintaining a higher trajectory for weapon revenue within the conducted energy weapons market.

By End-User: Civilian Sales Accelerate While Agencies Consolidate

Law-enforcement buyers held 68.37% of the conducted energy weapons market share in 2025, with nearly 94% of agencies authorizing the deployment of CEWs. The installed base now focuses on upgrading to interconnected TASER 10 systems that synchronize with body-worn cameras and evidence platforms, locking departments into recurring SaaS payments. Axon’s Q3 2024 TASER revenue of USD 238 million underscores the durability of this channel despite plateauing officer headcounts.

Personal purchasers represent the fastest-growing end-user group, with an annual expansion rate of 6.78% through 2031. Portability, USB rechargeability, and pricing under USD 30 drive volume, while premium buyers seek NIJ-validated charging ratings. Regulatory friction persists in Rhode Island and Hawaii, but most states permit mail-order delivery, granting e-commerce retailers a broad reach. The divergence between consolidated institutional demand and fragmented civilian demand defines competitive strategy within the conducted energy weapons market.

Geography Analysis

The conducted energy weapons market shows pronounced regional variation within the United States. Urban departments in California, Texas, and New York allocate larger budgets to dual-shot innovative platforms that integrate with evidence clouds, contributing a disproportionate share of TASER 10 sales. Federal grants flow heavily to these jurisdictions, accelerating refresh cycles even as litigation risk remains elevated. Suburban counties in the Midwest follow at a measured pace, often deferring upgrades until grant matches materialize. Rural departments across the Plains states face tighter operating budgets, which slow platform replacement and sustain demand for lower-cost alternatives such as PhaZZer Enforcer units.

Civilian adoption likewise differs by region. Southern states with permissive carry laws show higher retail velocity for compact stun guns, aided by big-box distribution. In contrast, Northeastern states maintain more rigorous training mandates, channeling sales toward premium NIJ-rated devices from brands like SABRE. Western states exhibit robust e-commerce activity, although logistical hurdles persist in Hawaii due to its unique permit structure. Overall, regional regulatory heterogeneity both restrains and redistributes the growth of the conducted energy weapons market.

The corrections segment's growth mirrors the distribution of the inmate population. Large state systems in Florida, Texas, and California spearhead the adoption of stun batons for prisoner transport, whereas smaller Northeastern facilities rely on existing probe-mode inventories. Federal Bureau of Prisons facilities scattered nationwide account for a steady baseline of demand as they standardize compliance logging protocols that favor wearable devices. Across all regions, post-incident documentation requirements, as narrowed by grant programs, reinforce the shift toward data-integrated platforms, confirming the nationwide orientation of conducted energy weapons market dynamics.

Competitive Landscape

Dominance within law enforcement procurement remains firmly with Axon, whose Evidence.com integration, VR training modules, and automatic BWC synchronization establish a closed platform that smaller vendors struggle to penetrate. Axon’s 17% year-over-year increase in TASER revenue in Q3 2024 illustrates the payoff from ecosystem lock-in. The firm regularly secures multi-year contracts that bundle weapons, cartridges, software, and training, minimizing churn and elevating the entry barriers to the conducted energy weapons market.

In the civilian market, competition is concentrated among various brands. SABRE leverages its policing heritage to justify premium pricing for NIJ-rated rechargeable models, while Vipertek captures consumers prioritizing price and USB convenience. Guard Dog Security fills a niche with multi-function flashlights that incorporate low-voltage stun outputs. PhaZZer positions its Enforcer as a budget-friendly option for rural agencies, but lags behind Axon in range, analytics, and cloud connectivity.[5]“PhaZZer Enforcer Specifications,” PhaZZer LLC, phazzer.com Byrna competes indirectly by selling chemical irritant launchers rather than electro-shock devices, limiting overlap but drawing from the same personal-defense wallet share.

Technology integration is the primary differentiation lever. Axon’s VR training simulators, AI-driven use-of-force analytics, and automated evidence upload tie each weapon deployment into a broader data ecosystem, raising exit costs for agencies. Smaller vendors attempt to close the gap by offering open-API firmware or partnering with third-party camera makers; yet, they seldom match the one-vendor convenience that departments prefer. As a consequence, the conducted energy weapons market remains bifurcated, with highly concentrated institutional sales and intensely competitive civilian sales.

US Conducted Energy Weapons Industry Leaders

Axon Enterprises Inc.

Streetwise Security Products

PhaZZer LLC

Guard Dog Security

Vipertek

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: AeroVironment, Inc. announced the successful delivery of the first two mobile counter-unmanned aircraft system (C-UAS) prototype Laser Weapon Systems (LWS) to the US Army Rapid Capabilities and Critical Technologies Office (RCCTO). This delivery was part of the initial phase of the Army Multi-Purpose High Energy Laser (AMP-HEL) prototyping initiative.

- March 2025: HII announced that its Mission Technologies division had been selected to develop an open-architecture High-Energy Laser (HEL) weapon system for the US Army’s Rapid Capabilities and Critical Technologies Office (RCCTO). HII will design and test an HEL prototype capable of acquiring, tracking, and destroying Groups 1-3 UAS used in multi-domain operations. The system will support fixed-site defense and integration onto Army vehicles.

- May 2023: the US Department of Defense (DoD) announced the issuance of two contracts to advance the adoption of directed-energy weapon (DEW) systems for air defense and to support research on pulsed laser technology. The first contract was awarded to Kord Technologies, a defense company based in Alabama, to develop, integrate, test, and sustain directed-energy short-range air defense systems for the US Army. The second contract allocated USD 14.9 million to the University of Rochester Laboratory for Laser Energetics to support the Missile Defense Agency’s (MDA) research on pulsed laser lethality as part of its innovation, science, and technology initiatives.

US Conducted Energy Weapons Market Report Scope

Conducted energy weapons (CEWs) are considered to be less lethal alternatives to firearms. These weapons are designed to incapacitate a person temporarily without causing significant injury or death. Thus, these weapons can be effective in subduing individuals who are armed, violent, or resisting arrest. By temporarily immobilizing suspects, these weapons can prevent further harm to officers, suspects, and bystanders.

The US conducted energy weapons (CEWs) market is segmented by type, equipment type, and end user. By type, the market is segmented into stun guns, tasers, and stun batons. By equipment type, the market is segmented into weapons and cartridges. By end user, the market is segmented into law enforcement agencies and personal use. The market sizing and forecasts have been provided in terms of value (USD).

| Stun Gun |

| Taser |

| Stun Baton |

| Weapon |

| Cartridges |

| Law Enforcement Agencies |

| Personal Use |

| By Type | Stun Gun |

| Taser | |

| Stun Baton | |

| By Equipment Type | Weapon |

| Cartridges | |

| By End-User | Law Enforcement Agencies |

| Personal Use |

Key Questions Answered in the Report

How large is the Conducted Energy Weapons market in the United States today?

The Conducted Energy Weapons market size stands at USD 747.75 million in 2026 and is forecast to reach USD 980.34 million by 2031.

Which product type is growing fastest?

Stun batons show the quickest rise, expanding at a 5.97% CAGR through 2031.

What drives agency upgrades to TASER 10?

Federal de-escalation mandates and automatic integration with body-worn cameras and Evidence.com spur departments to adopt dual-shot TASER 10 platforms.

Why are civilian CEW purchases accelerating?

Portability, USB rechargeability and sub-USD 30 pricing are boosting civilian demand, particularly in states with minimal ownership restrictions.

Which states restrict civilian CEWs the most?

Rhode Island bans them outright, and Hawaii enforces a permit requirement, creating notable distribution hurdles.

Page last updated on: