Industrial Grade Urea Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

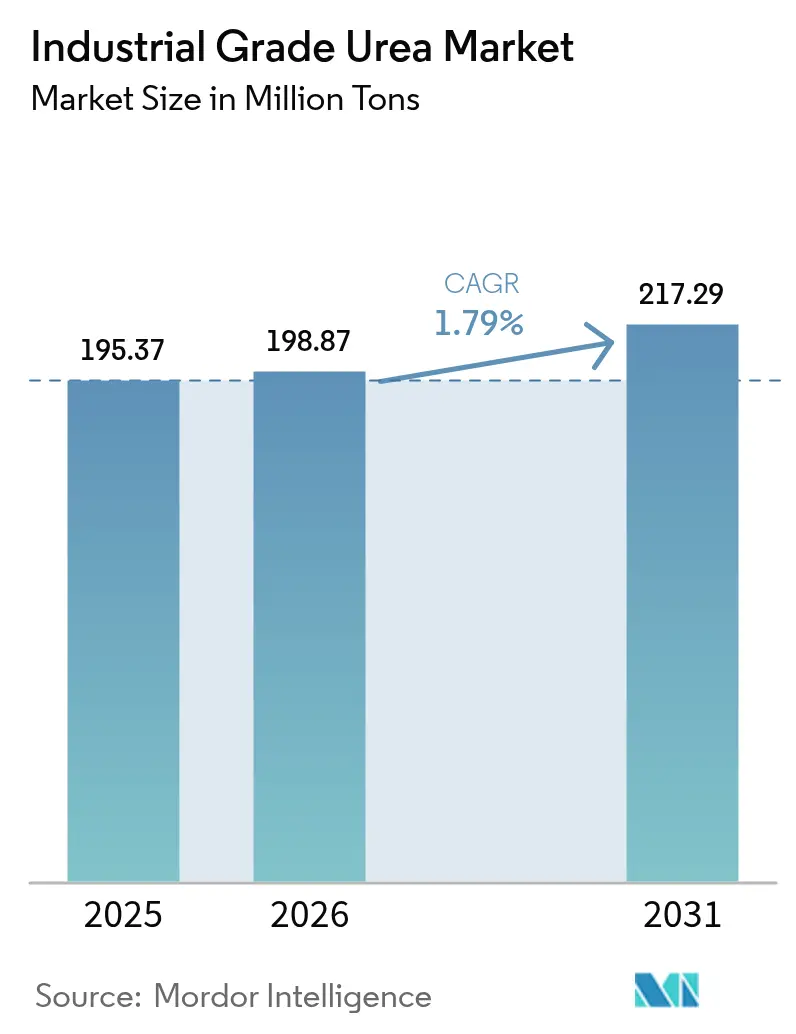

| Market Volume (2026) | 198.87 Million tons |

| Market Volume (2031) | 217.29 Million tons |

| Growth Rate (2026 - 2031) | 1.79% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Grade Urea Market Analysis by Mordor Intelligence

The Industrial Grade Urea Market size was valued at 195.37 Million tons in 2025 and estimated to grow from 198.87 Million tons in 2026 to reach 217.29 Million tons by 2031, at a CAGR of 1.79% during the forecast period (2026-2031). The market’s modest trajectory reflects a mature landscape balancing cost-driven production economics with rising sustainability expectations. Demand growth flows mainly from agriculture, yet a new pull from diesel exhaust fluid (DEF) and engineered-wood resins diversifies the revenue base. Energy-price volatility, consolidation among large producers, and stricter emissions targets dominate strategic conversations, while process innovations aimed at green ammonia integration promise longer-term competitiveness.

Key Report Takeaways

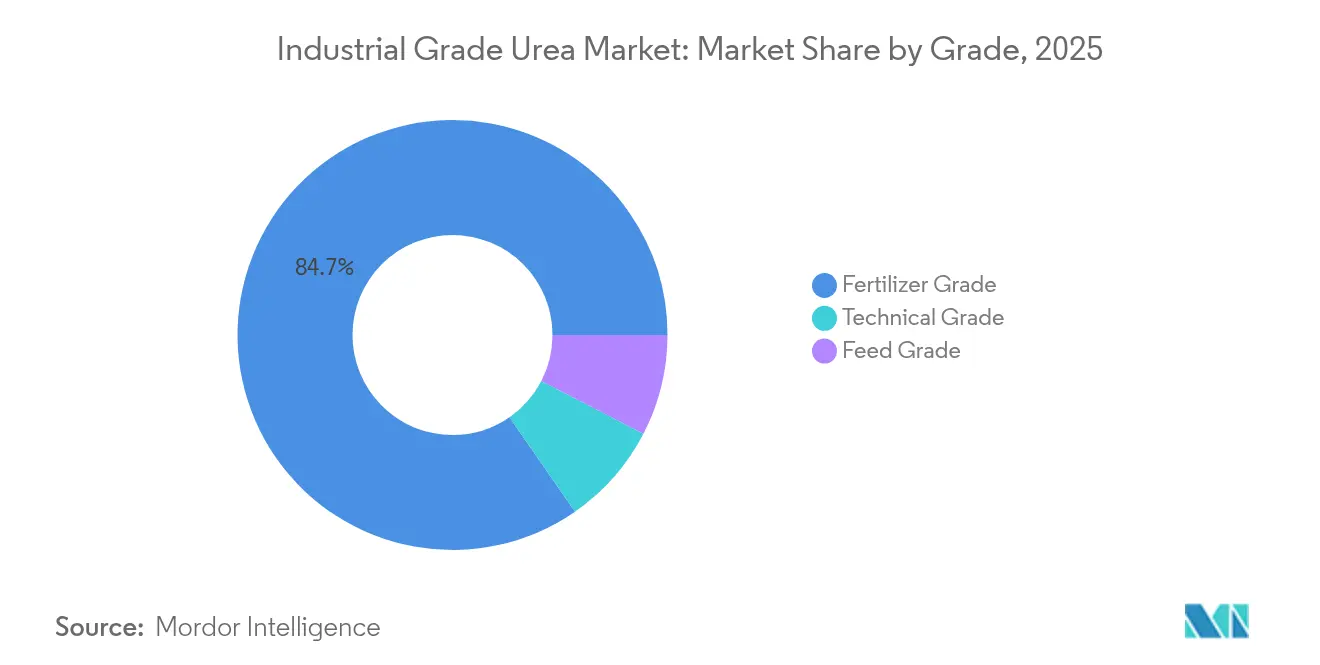

- By grade, fertilizer grade retained 84.65% revenue share in 2025 and is projected to advance at a 1.83% CAGR through 2031.

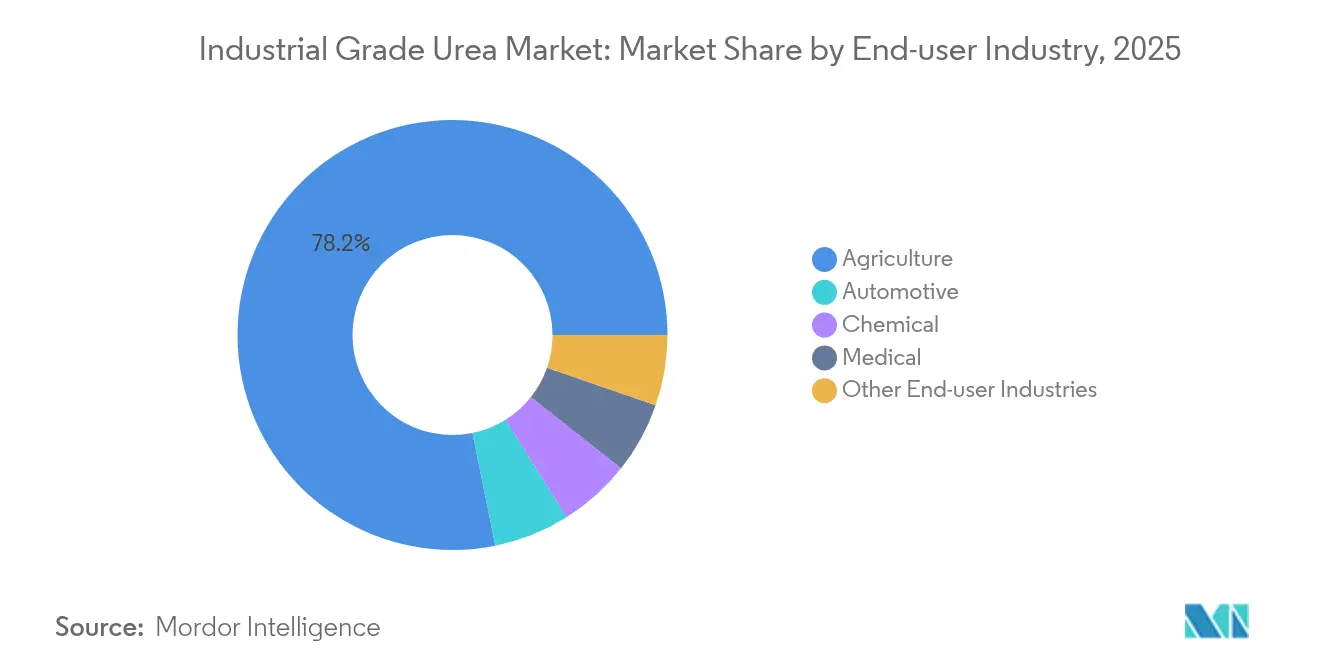

- By end-user industry, agriculture held 78.20% of the industrial grade urea market share in 2025 and also records the highest 1.85% CAGR to 2031.

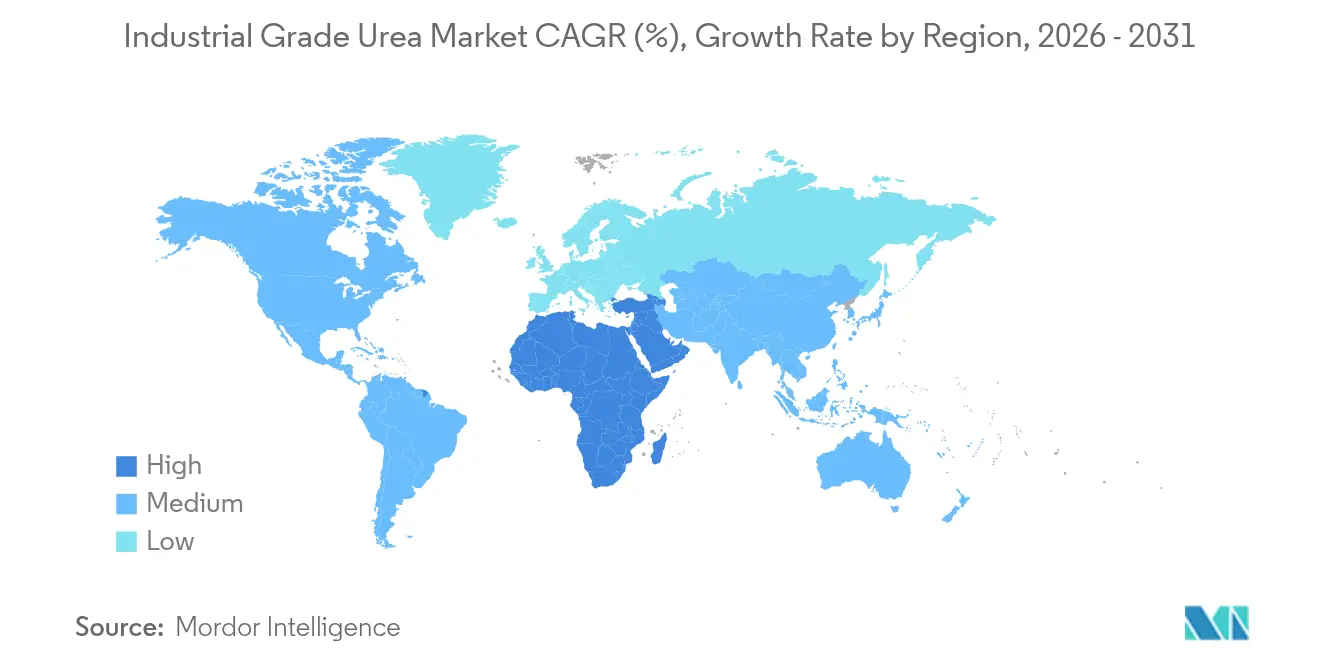

- By geography, Asia-Pacific commanded 66.10% of the industrial-grade urea market size in 2025, while the Middle East and Africa region is set to grow at a 2.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Grade Urea Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising DEF adoption in on-road and off-road vehicles | +0.3% | Global (early gains in China, Europe, North America) | Medium term (2-4 years) |

| High applicability of technical-grade urea | +0.2% | Asia-Pacific core, spill-over to MEA | Short term (≤ 2 years) |

| Expanding fertilizer consumption in emerging Asia | +0.4% | Asia-Pacific, notably India and Southeast Asia | Long term (≥ 4 years) |

| Increased melamine and resin output for engineered wood | +0.1% | Global | Medium term (2-4 years) |

| Shift toward green-ammonia-based urea | +0.2% | Europe, North America, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Diesel Exhaust Fluid Adoption Transforms Technical Grade Demand

Commercial vehicle emission standards underpin a robust uptake of DEF, with China’s National VI regulations alone expected to lift DEF consumption to 25 million tons in 2025[1]Siavash Khadem Masjedi et al., “DEF Growth and Emissions Standards,” pubmed.ncbi.nlm.nih.gov. European players are integrating DEF lines into existing ammonia-urea complexes, illustrated by CF Industries’ Blue Point project that will add 1.4 million tpy low-carbon ammonia from 2029. This defensively hedges against seasonal fertilizer swings and supports premium pricing. North American fleets following EPA 2027 rules further reinforce a medium-term demand floor, while off-road machinery in construction and mining extends the addressable market. Overall, DEF’s rise shifts a portion of the industrial-grade urea market toward higher-purity products, indirectly raising margins and encouraging investments in purification infrastructure.

Green Ammonia Integration Reshapes Production Economics

The European Union’s RED III requirement for 42% renewable hydrogen by 2030 accelerates low-carbon ammonia adoption, turning electrolyzer costs and renewable power availability into new profit levers. Stamicarbon’s NX Stami Green Ammonia modules slash CAPEX 25-30% at 50-500 t per day scale, enabling regional supply hubs that shorten freight routes and curb scope 3 emissions. Pilot projects in the Middle East aim to couple solar-powered electrolysis with urea synthesis, signaling a shift away from single-site mega-plants. Early adopters gain compliance advantages in carbon-regulated export markets and secure offtake agreements from food and beverage firms seeking lower-footprint supply chains. Over the long term, these developments could moderate the industrial-grade urea market’s exposure to natural-gas price spikes and carbon costs.

Technical Grade Applications Drive Premium Segment Growth

Technical-grade urea serves melamine, formaldehyde resins, pharmaceutical intermediates, and de-icing agents, generally selling at a 15-25% price premium over fertilizer material[2]thyssenkrupp Uhde, “Urea 2000plus Technical Brochure,” thyssenkrupp-uhde.com. Construction-led demand for engineered wood boosts melamine consumption, while emerging pyrolysis routes unlock co-production of ammonia and cyanuric acid for advanced polymers. Producers leveraging thyssenkrupp Uhde’s Urea 2000plus pool-condenser design can seamlessly switch between fertilizer and technical grades, smoothing plant utilization. Such flexibility attracts investment as long-cycle fertilizer markets plateau, allowing operators to chase margin-accretive industrial niches.

Emerging Asia Fertilizer Demand Sustains Long-term Growth

India’s fertilizer usage climbed despite subsidy rationalization, with population growth and protein-rich diet shifts setting a durable consumption baseline. Southeast Asia shows parallel momentum. Precision-agriculture tools gradually lift nutrient-use efficiency, yet rising harvested-area intensity offsets per-hectare rate moderation. Long-term government support for food security secures a steady offtake channel, anchoring a majority share of the industrial-grade urea market through 2030.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile natural-gas pricing | -0.4% | Global, acute in Europe and net-gas-importing regions | Short term (≤ 2 years) |

| Indiscriminate over-application in groundwater-stressed regions | -0.2% | Asia-Pacific, notably China and India | Medium term (2-4 years) |

| Stricter fertilizer subsidy reforms | -0.3% | India, China, Brazil, Indonesia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Natural Gas Price Volatility Threatens Production Viability

Spot gas swung from USD 6.54/MMBtu in 2022 to USD 2.66/MMBtu in 2023, exposing producers whose feedstock can constitute 70-90% of cash costs. European plants curtailed utilization to 75% amid the 2022 energy crisis, redirecting trade flows toward Middle Eastern suppliers. U.S. operators with shale-based gas benefit from structural cost advantages, whereas net-importing areas confront negative margins during price spikes. Hedging strategies, dual-fuel capabilities, and green ammonia investments are emerging defenses but require substantial capital and policy support.

Environmental Regulations Constrain Application Growth

The EU Fertilising Products Regulation (EU 2019/1009) enforces tighter contaminant thresholds, raising compliance costs and incentivizing controlled-release formulations. Canada attributes 72% of national N₂O emissions to agriculture, prompting incentives for urease-inhibitor adoption. Studies show up to 50% of surface-applied urea volatilizes under unfavorable conditions, leading policymakers to cap per-hectare application or mandate stabilizers. Although these measures elevate product innovation, they may temper bulk-volume growth in the industrial grade urea market over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Fertilizer Dominance Faces Technical Grade Disruption

Fertilizer grade accounted for 84.65% of the industrial grade urea market in 2025 and is forecast to expand at a 1.83% CAGR to 2031. The technical grade slice, while smaller, accelerates on DEF demand, potentially lifting its share by 130 basis points within the outlook period. Feed grade addresses ruminant nutrition niches with stringent purity needs. Process innovations such as pool-condenser reactors lower CAPEX by up to 30%, enabling multiproduct configurations that respond swiftly to shifting margins.

Flexibility matters because DEF and melamine demand decouple from crop cycles, smoothing revenue seasonality. Producers certified for automotive-grade urea meet ISO 22241 quality thresholds, commanding sustained premiums. In contrast, fertilizer producers remain exposed to subsidy regimes and environmentally driven application caps. This divergence underlines why technical grade is the fastest growing component of the industrial grade urea market size across the forecast.

By End-user Industry: Agriculture Maintains Dominance Despite Diversification

Agriculture absorbed 78.20% of global volume in 2025, yet its CAGR to 2031 stalls at 1.85% as precision application curbs per-acre rates. Automotive DEF, though under 8% by volume, represents a resilient outlet driven by emission mandates in trucking, mining, and marine sectors. Chemical manufacturing—including melamine, resins, and pharmaceuticals—benefits from construction booms and specialty chemical expansion. Small, high-value medical uses for diagnostic reagents also grow, albeit from a low base.

Biotechnology alternatives pose discrete threats: enzyme blends in ethanol fermentation can displace up to 90% of urea previously added as a nitrogen source. Successful scale-up could erode certain industrial volumes, demanding proactive diversification among suppliers. Overall, the industrial-grade urea industry remains anchored in farming, but growth momentum gravitates toward regulatory-backed technical applications.

Geography Analysis

Asia-Pacific dominated the industrial-grade urea market size with a 66.10% share in 2025, driven by India’s and China’s crop inputs and rising DEF uptake. Local production expansion in India aims for self-sufficiency by 2025, potentially trimming import reliance.

The Middle East and Africa region posts the fastest 2.33% CAGR through 2031, fueled by low-cost gas feedstock and export-oriented capacity additions in Saudi Arabia, Egypt, and Algeria. New complexes integrate green-hydrogen pilot lines to future-proof carbon competitiveness. Europe’s share contracts amid high gas costs and decarbonization policies; several plants operate seasonally or under curtailment, increasing import reliance on North Africa and the United States.

North America maintains steady demand, benefiting from abundant shale gas and ongoing DEF adoption in heavy-duty fleets. Trade patterns continue shifting: China’s H1 2024 export volumes fell 90% following policy restrictions, creating spot shortages in Southeast Asia and Latin America. Middle Eastern producers quickly captured these gaps, affirming their swing-supplier status. Over the long term, Asia-Pacific retains leadership, yet its growth moderates as sustainability policies and domestic supply priorities reshape external trade.

Competitive Landscape

Global supply exhibits oligopolistic traits. Technology licensing stands out as a differentiation lever. Stamicarbon and thyssenkrupp Uhde market new synthesis loops that cut energy use by 5-7% and enable wider feedstock flexibility. Potential disruption looms from biotech solutions that slash urea usage in industrial fermentation. Novozymes reports enzyme packages displacing bulk urea at multiple ethanol plants, hinting at demand erosion in specific end-markets. Incumbents respond by investing in enhanced-efficiency fertilizers and DEF production, betting on regulatory-anchored outlets. Smaller regional firms survive by serving localized markets with lean logistics and flexible grade switching, yet remain vulnerable to feedstock price shocks.

Industrial Grade Urea Industry Leaders

SABIC

Yara

CF Industries Holdings Inc.

Nutrien Ltd

OCI

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Genesis Fertilizers advanced construction of its Saskatchewan unit targeting 2,500 t/day urea capacity, slated for 2029 start-up.

- April 2024: India’s government announced plans to cease urea imports by the end of 2025, as a massive push for domestic manufacturing.

Global Industrial Grade Urea Market Report Scope

Urea is extensively used in urea-formaldehyde (UF) resin, a non-transparent thermosetting polymer. It is manufactured mainly from urea and methanal (formaldehyde).

The industrial grade urea market is segmented by grade, end-user industry, and geography. By grade, the market is segmented into fertilizer, feed, and technical. By end-user industry, the market is segmented into agriculture, chemical, automotive, medical, and other end-user industries. The report also covers the market size and forecasts for the urea market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (kilotons).

| Fertilizer Grade |

| Technical Grade |

| Feed Grade |

| Agriculture |

| Chemical |

| Automotive |

| Medical |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Fertilizer Grade | |

| Technical Grade | ||

| Feed Grade | ||

| By End-user Industry | Agriculture | |

| Chemical | ||

| Automotive | ||

| Medical | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the industrial grade urea market in 2026?

The industrial grade urea market size is 198.87 million tons in 2026.

What is the expected growth rate for industrial grade urea to 2031?

Volume is projected to rise at a 1.79% CAGR, reaching 217.29 million tons by 2031.

Which region leads demand for industrial grade urea?

Asia-Pacific accounts for 66.10% of 2025 global consumption, anchored by China and India.

Why is DEF important to industrial grade urea suppliers?

Diesel exhaust fluid requires high-purity urea and is mandated by emission standards, creating a fast-growing premium segment.

How are producers addressing carbon pressure?

Companies invest in green-ammonia projects and energy-efficient process designs to cut emissions and qualify for low-carbon certifications.

Page last updated on: