US Video-based Automatic Incident Detection Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

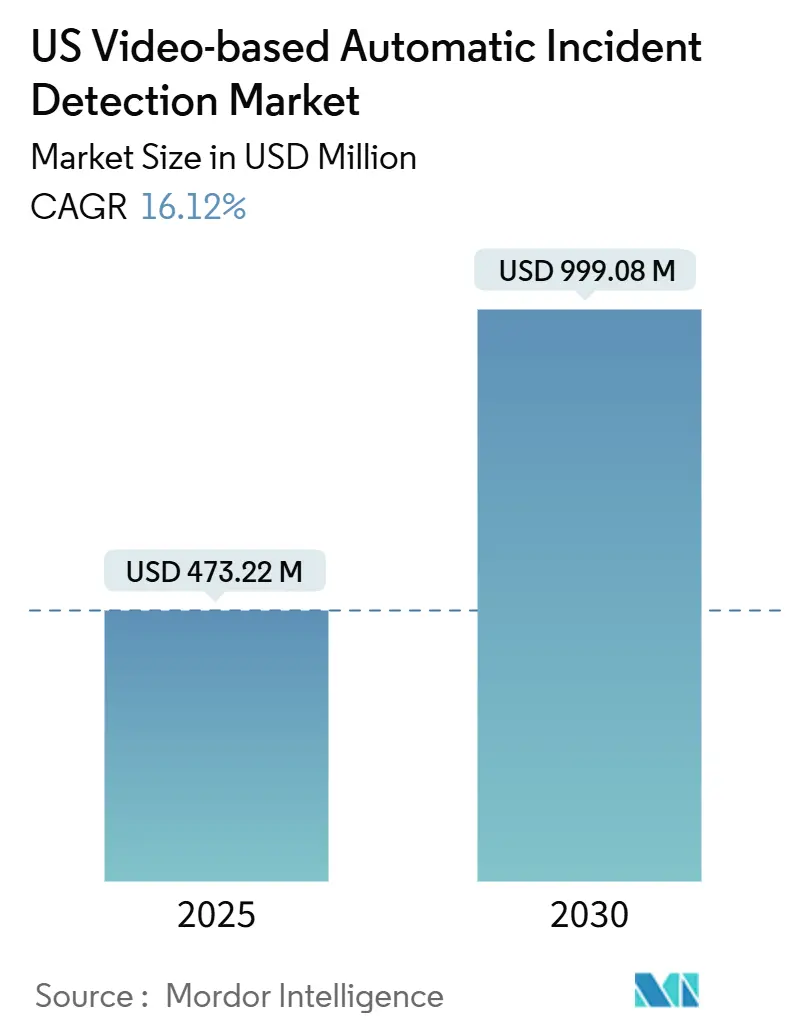

| Market Size (2025) | USD 473.22 Million |

| Market Size (2030) | USD 999.08 Million |

| Growth Rate (2025 - 2030) | 16.12% CAGR |

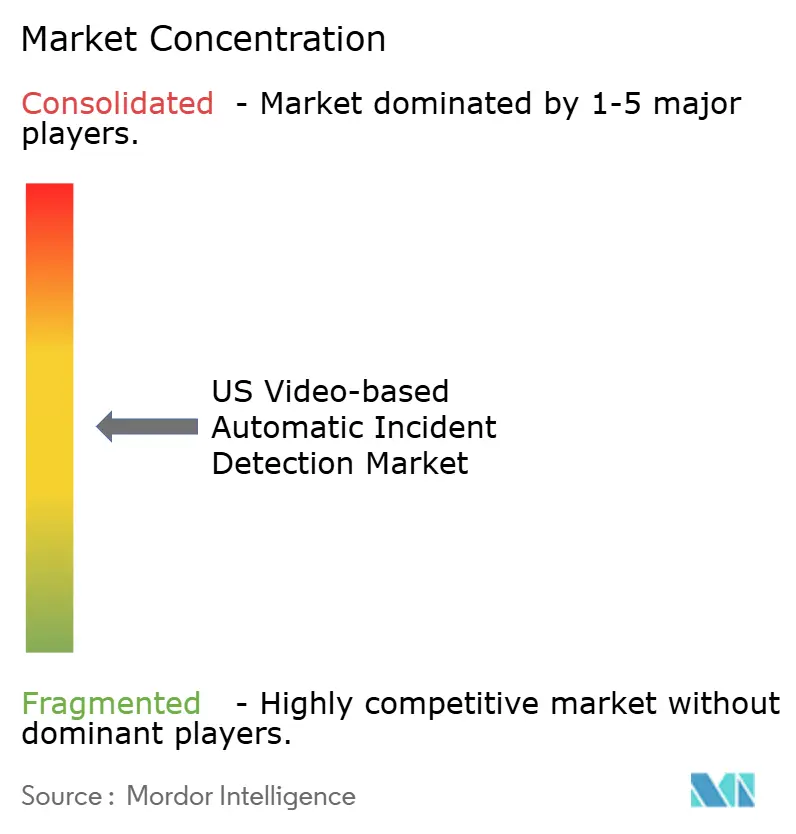

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Video-based Automatic Incident Detection Market Analysis by Mordor Intelligence

The US video-based automatic incident detection market reached USD 473.22 million in 2025 and is projected to attain USD 999.08 million by 2030, reflecting a robust 16.12% CAGR across the forecast period. This expansion stems from the federal Vision Zero framework, growing state investments in smart highways, and bipartisan political backing for technologies that cut emergency response times while curbing secondary crashes. Hardware platforms dominate today’s spending, but the shift toward managed services and cloud-native analytics is accelerating as transportation agencies prioritize operational flexibility. Regional dynamics amplify growth: southern states allocate record budgets to interstate modernization, western states race ahead with wrong-way detection mandates, and technology suppliers form partnerships to deliver integrated solutions. These factors combine to create a fertile environment for vendors that can prove high detection accuracy, low false-positive rates, and rapid deployment capabilities.

Key Report Takeaways

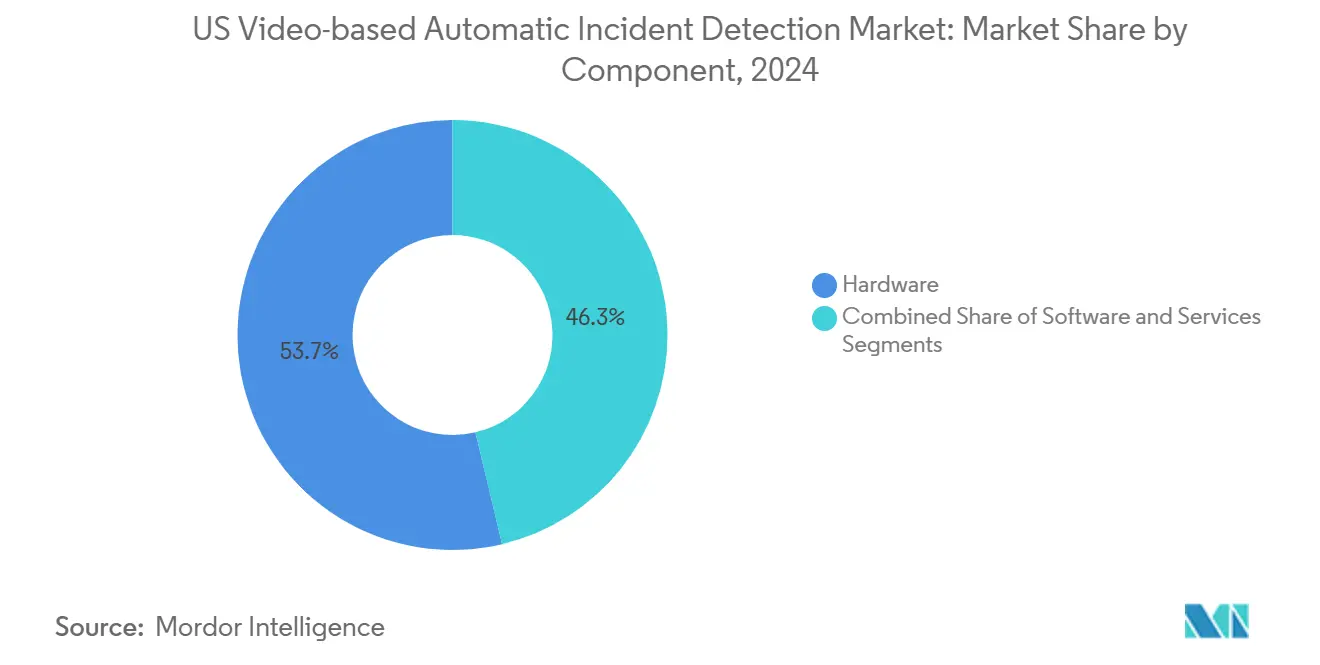

- By component, hardware captured 53.7% of the US video-based automatic incident detection market share in 2024; services are forecast to expand at a 17% CAGR through 2030.

- By deployment model, on-premise solutions accounted for 54.71% of the US video-based automatic incident detection market size in 2024, while cloud-based platforms are projected to advance at a 17.5% CAGR through 2030.

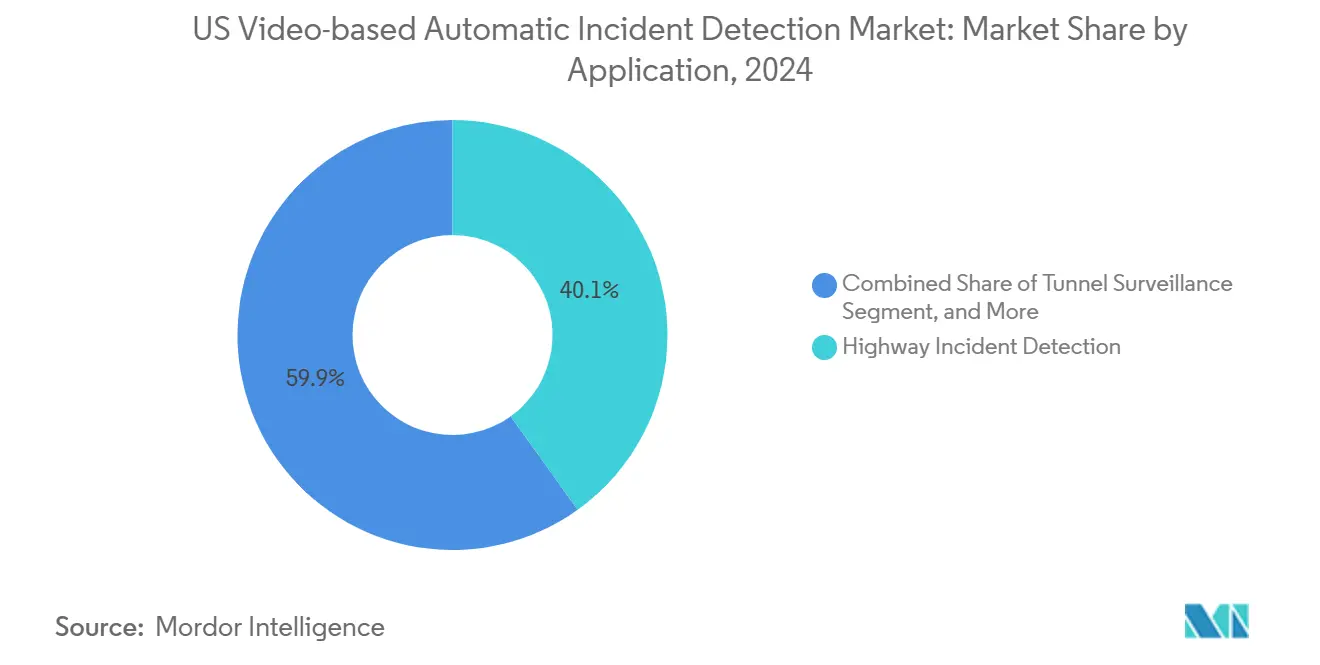

- By application, highway incident detection accounted for a 40.1% share of the US video-based automatic incident detection market size in 2024, and tunnel surveillance is projected to grow at an 18.4% CAGR through 2030.

- By end-user, the departments of transportation accounted for a 39.02% share of the US video-based automatic incident detection market size in 2024; smart city authorities are expected to exhibit the fastest CAGR at 18.9% through 2030.

- By region, the South led with a 36.88% revenue share of the US video-based automatic incident detection market in 2024, whereas the West region is projected to record the highest CAGR of 18.1% from 2024 to 2030.

US Video-based Automatic Incident Detection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rollout of Vision-Zero policies | +3.2% | National, with early gains in California, New York, Washington | Medium term (2-4 years) |

| Mandates for wrong-way detection systems on interstate ramps | +2.8% | South and West regions, expanding nationally | Short term (≤ 2 years) |

| Rising integration of AI-enabled edge cameras | +4.1% | National, with technology hubs leading adoption | Medium term (2-4 years) |

| Growing public-private funding for smart corridor projects | +2.9% | Northeast and West regions, federal highway corridors | Long term (≥ 4 years) |

| Uptake of cloud-native video analytics platforms | +1.8% | National, with rural areas lagging | Medium term (2-4 years) |

| State DOT pivot to bundled managed service contracts | +1.4% | National, with budget-constrained states leading | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Rollout of Vision-Zero Policies

Vision Zero adoption has accelerated the use of automated incident detection across 45 states, shifting traffic safety from a reactive to a predictive model. In 2024, Federal Highway Administration guidance required states receiving safety funds to demonstrate progress toward zero fatalities, sparking an immediate increase in technology procurements. California demonstrated 23% faster emergency response after deploying these systems, prompting replication in New York and Washington. The National Highway Traffic Safety Administration later confirmed a 31% drop in secondary crashes on equipped corridors, giving agencies data-backed justification for expansion.[1]National Highway Traffic Safety Administration, “Traffic Safety Facts: Wrong-Way Driving,” U.S. Department of Transportation, nhtsa.gov As states expand Vision Zero scopes to encompass pedestrian zones and work areas, demand increases for cameras equipped with sophisticated AI models that meet the 30-second detection benchmark.

Mandates for Wrong-Way Detection Systems on Interstate Ramps

Congressional directives have made wrong-way detection a near-term priority, channeled through USD 2.3 billion of dedicated funding from the Infrastructure Investment and Jobs Act.[2]Infrastructure Investment and Jobs Act, “Smart Transportation Infrastructure,” congress.gov Twelve states completed statewide deployments in 2024, and Texas alone installed 847 systems with 94% accuracy, shaping national technical standards. Vendors report that order volumes have quadrupled compared to 2023 as agencies rush to meet the 2025 federal compliance deadline. Standardized integration protocols enable rapid scaling without requiring overhauls to existing centers, reducing the average deployment time by six months.

Rising Integration of AI-Enabled Edge Cameras

Edge computing shifts processing from centralized clouds to camera hardware, delivering sub-second response even on bandwidth-limited roadways. NVIDIA’s partnerships yielded cameras that run multiple AI models simultaneously, supporting incident, weather, and flow analytics on-device.[3]NVIDIA Corporation, “Metropolis for Transportation Platform Launch,” nvidia.com The Department of Transportation now mandates edge-ready hardware for new builds, ensuring resilience during network outages. This architectural pivot also trims data-center costs and unlocks rural deployments where fiber backhaul is sparse.

Growing Public-Private Funding for Smart Corridor Projects

Public-private partnerships have mobilized USD 8.7 billion toward multi-state smart corridors, often structured as 20-year managed service deals that tie payments to performance metrics. The I-95 Corridor Coalition’s model cuts per-mile costs by 42% by aggregating demand across jurisdictions, while federal loan guarantees lower private financing risk. Private partners introduce faster tech refresh cycles and supply-chain efficiencies that most agencies cannot achieve independently, stimulating adoption beyond major metropolitan areas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High retrofit costs for legacy analog networks | −2.1% | National; older-infrastructure states | Medium term (2-4 years) |

| Algorithmic bias concerns delaying procurement | −1.3% | National; progressive states more active | Short term (≤ 2 years) |

| Limited fiber backhaul in rural highways | −1.8% | Rural zones nationwide | Long term (≥ 4 years) |

| Data-privacy litigation risk under surveillance laws | −0.9% | States with strict privacy statutes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Retrofit Costs for Legacy Analog Camera Networks

Thirty-four states still rely on analog cameras that cannot support AI analytics, forcing full replacement at USD 125,000 per highway mile. Pennsylvania found that 78% of units were below minimum resolution specifications, making piecemeal upgrades impractical. Grants rarely cover more than half of capital needs, prompting agencies to adopt phased deployments that fragment system coverage and diminish their overall impact. Bond financing and multi-year budgets help, but cost remains a primary drag on the video-based automatic incident detection market.

Algorithmic Bias Concerns Triggering Procurement Delays

Eighteen states extended their evaluation cycles to audit AI algorithms for bias after civil-society studies revealed divergent false-positive rates across communities. This expanded vetting stretches procurement timelines from 12 to 24 months and raises vendor liability insurance costs. The forthcoming National Institute of Standards and Technology testing framework promises harmonized benchmarks, yet uncertainty keeps some projects in limbo, slowing near-term growth in the video-based automatic incident detection industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Edge Hardware Strengthens, Managed Services Accelerate

Hardware retained a 53.7% share of the video-based automatic incident detection market in 2024, underscoring the capital-heavy requirements for ruggedized cameras and edge processors. Services, however, deliver the fastest 17% CAGR as agencies pivot to pay-as-you-go contracts that bundle deployment, analytics, and maintenance. This structure aligns expenses with yearly budgets and ensures continuous upgrades without new capital outlays. Implementation specialists command premium rates due to the complexity of integrating AI platforms with legacy traffic centers. As a result, agencies opting for managed services reduced roll-out times 34%, positioning services to erode hardware’s dominance over the forecast horizon.

Software remains a smaller slice but gains traction through modular analytics that plug into cloud dashboards. Vendors are embedding machine-learning ops to push updates automatically, enriching functionality without hardware swaps. Overall, component dynamics illustrate how budget pressures and technology cycles converge to diversify spending patterns across the video-based automatic incident detection market.

By Deployment Model: Hybrid Architectures Bridge Cloud and Edge

On-premise deployments held a 54.71% share in 2024, reflecting state preferences for data sovereignty and minimal latency. Edge hardware processes incidents locally and then streams metadata into centralized repositories, striking a balance between speed and historical analysis. Cloud platforms, recording a 17.5% CAGR, capitalize on this edge-plus-cloud paradigm, offering agencies centralized dashboards while offloading infrastructure upkeep to certified hyperscalers. Microsoft Azure Government’s FedRAMP authorization addresses security hurdles, and Amazon Web Services’ 2024 transport partnership signals deepening vendor investment in public-sector traffic solutions.

Hybrid models now dominate new RFPs, weaving cloud analytics atop local inference engines. Agencies leverage cloud elasticity for long-term storage and machine-learning retraining, while maintaining real-time decision-making capabilities on-site. This architecture underpins the next evolution of the video-based automatic incident detection market, unlocking scale without compromising incident-response latency.

By Application: Tunnel Surveillance Rises From Niche to Necessity

Highway monitoring accounted for 40.1% of the 2024 demand, anchoring the video-based automatic incident detection market size due to its sheer mileage and high traffic density. Tunnel surveillance, historically a niche market, is expected to accelerate at an 18.4% CAGR as infrastructure security reviews highlight elevated risks in confined corridors. Thermal-visible sensor fusion now delivers 96% accuracy in smoke-filled tunnels, as proven by the Port Authority of New York and New Jersey’s 2024 upgrade. Urban road, rail, and airport use cases generate incremental demand but require tailored algorithms to handle complex lighting, weather, and operational environments.

Incident detection vendors adapt by creating modular application packs optimized for each setting, extending their market reach while leveraging common core models. This strategy elevates tunnel surveillance from experimental pilot to mainstream growth vector in the broader video-based automatic incident detection market.

By End-user: Smart City Authorities Ignite Cross-Domain Synergies

Departments of Transportation captured 39.02% of the 2024 value, reflecting statutory responsibility for interstate safety. Smart city administrations, however, expand at an 18.9% CAGR as municipalities embed incident detection within broader urban mobility platforms. Integrating AI cameras with adaptive signals and connected-vehicle beacons unlocks synergies across congestion management, emissions control, and emergency services. Federal Smart City Challenge grants catalyze adoption among mid-size cities, enlarging the pool of buyers beyond traditional highway agencies.

Toll road operators and airport authorities also adopt the technology to enhance throughput and safety, but procurement cycles differ in governance, funding, and ROI metrics. These diverse buyer profiles compel vendors to craft flexible commercial models, ranging from capital sales to performance-based managed services, broadening addressable demand within the video-based automatic incident detection industry.

Geography Analysis

The South retains a 36.88% share, as sprawling interstate networks throughout Texas, Florida, and Georgia necessitate wide-area incident coverage. Georgia’s 1,200-camera build-out showcases the region's commitment, while hurricane-prone corridors rely on automated alerts to orchestrate rapid evacuations, reinforcing the adoption.

The West leads growth with 18.1% CAGR, fueled by California’s USD 1.2 billion Vision Zero program and Washington’s corridor PPPs. Proximity to Silicon Valley and Seattle tech clusters accelerates pilot testing and knowledge transfer. Nevada’s Interstate 80 connected-vehicle testbed exemplifies cross-channel synergy, marrying vehicle telemetry with AI cameras to enrich situational awareness.

Northeastern states confront aging infrastructure; 67% of cameras fail to meet modern analytics standards, according to Pennsylvania’s audit. Multi-state efforts along the I-95 Corridor aim to harmonize specifications and pool procurement, seeking scale efficiencies similar to those found in western models. Federal incentives penalize lagging deployments, nudging budgets toward modernization despite fiscal constraints.

Midwestern adoption proceeds steadily, driven by freight-heavy corridors critical to national supply chains. Severe winter weather underscores the value of rapid incident alerts, although funding competition with bridge rehabilitation tempers spending velocity. Collectively, regional variations create a mosaic of opportunities, positioning the video-based automatic incident detection market for sustained nationwide expansion.

Competitive Landscape

The market structure remains moderately fragmented, with legacy traffic integrators, semiconductor innovators, and telecom infrastructure players competing for market share. Iteris and Siemens Mobility leverage long-standing agency relationships, while NVIDIA and Intel embed AI accelerators in next-gen cameras, raising performance benchmarks. Teledyne FLIR’s acquisition of TrafficVision merges thermal imaging with analytics, signaling consolidation among complementary specialists.[4]Teledyne FLIR LLC, “TrafficVision Acquisition Completion,” teledyne.com

Edge computing proficiency has become a table-stakes requirement; vendors tout sub-second detection and under 2% false-positive rates to ease emergency-center workloads. Patent filings for traffic-centric computer vision increased by 340% in 2024, reflecting heightened research and development (R&D) intensity. Cloud alliances deepen differentiation: Axis partners with Azure for scalable management, and AWS collaborates with camera OEMs to streamline deployment pipelines.

Competition also hinges on commercial models; managed services resonate with cash-constrained agencies seeking predictable outlays. Vendors offering turnkey financing and outcome-based contracts gain an edge, especially as public-private corridors proliferate. As the video-based automatic incident detection market matures, integration breadth, solution accuracy, and financing creativity will decide long-term winners.

US Video-based Automatic Incident Detection Industry Leaders

Iteris Inc.

Teledyne FLIR LLC

Axis Communications AB

Citilog SAS

Sensys Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Iteris secured a USD 45 million contract with Texas DOT to cover 800 miles of interstate highways with AI incident detection.

- August 2025: NVIDIA introduced Metropolis for Transportation, unifying edge AI with cloud analytics for sub-second detection.

- July 2025: Teledyne FLIR finalized its USD 125 million TrafficVision acquisition to strengthen tunnel and adverse-weather solutions.

- June 2025: California DOT awarded Siemens Mobility a USD 180 million managed services deal for 1,200 wrong-way detection systems.

- May 2025: Axis Communications partnered with Microsoft Azure to release cloud-native traffic analytics, simplifying multi-state scaling.

- March 2025: Bosch Security Systems has launched a 98% accuracy AI detection suite tuned for local traffic patterns.

US Video-based Automatic Incident Detection Market Report Scope

| Hardware | Cameras |

| Sensors | |

| Edge Devices | |

| Software | Analytics Engines |

| Incident Detection Dashboards | |

| Services | Implementation |

| Managed Services | |

| Training and Support |

| On-premise |

| Cloud-based |

| Hybrid |

| Urban Road Traffic Monitoring |

| Highway Incident Detection |

| Tunnel Surveillance |

| Rail and Mass Transit |

| Airport Infrastructure |

| Other Applications |

| Departments of Transportation |

| Toll Operators |

| Smart City Authorities |

| Airports and Seaports |

| Rail Operators |

| Law Enforcement Agencies |

| Other End-users |

| Northeast |

| Midwest |

| South |

| West |

| By Component | Hardware | Cameras |

| Sensors | ||

| Edge Devices | ||

| Software | Analytics Engines | |

| Incident Detection Dashboards | ||

| Services | Implementation | |

| Managed Services | ||

| Training and Support | ||

| By Deployment Model | On-premise | |

| Cloud-based | ||

| Hybrid | ||

| By Application | Urban Road Traffic Monitoring | |

| Highway Incident Detection | ||

| Tunnel Surveillance | ||

| Rail and Mass Transit | ||

| Airport Infrastructure | ||

| Other Applications | ||

| By End-user | Departments of Transportation | |

| Toll Operators | ||

| Smart City Authorities | ||

| Airports and Seaports | ||

| Rail Operators | ||

| Law Enforcement Agencies | ||

| Other End-users | ||

| By Region | Northeast | |

| Midwest | ||

| South | ||

| West | ||

Key Questions Answered in the Report

How large is the U.S. video-based automatic incident detection market in 2025?

It stands at USD 473.22 million and is projected to almost double by 2030 at a 16.12% CAGR.

Which component leads spending?

Edge-ready hardware holds 53.7% of 2024 revenue due to widespread camera and processor installations.

What drives the fastest growth segment?

Managed service contracts grow 17% CAGR as agencies favor operational budgets over one-time capital purchases.

Which region shows the highest growth potential?

Western states post an 18.1% CAGR, propelled by California’s Vision Zero mandates and smart corridor PPPs.

Why are tunnel applications expanding quickly?

Heightened security assessments and improved thermal-visible camera fusion push tunnel surveillance to an 18.4% CAGR.

How are agencies addressing algorithmic bias concerns?

States now mandate independent audits during procurement, extending evaluation cycles but standardizing fairness benchmarks.

Page last updated on: