Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

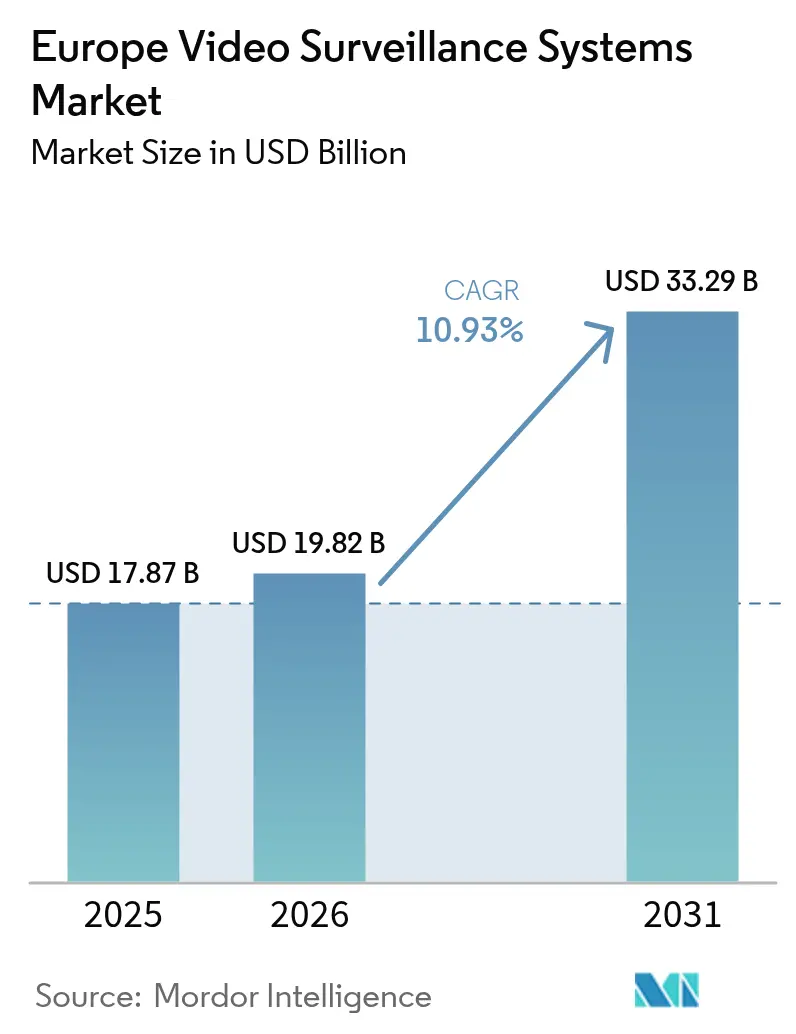

| Base Year Market Size (2025) | USD 17.87 Billion |

| Market Size (2026) | USD 19.82 Billion |

| Market Size (2031) | USD 33.29 Billion |

| Growth Rate (2026 - 2031) | 10.93% CAGR |

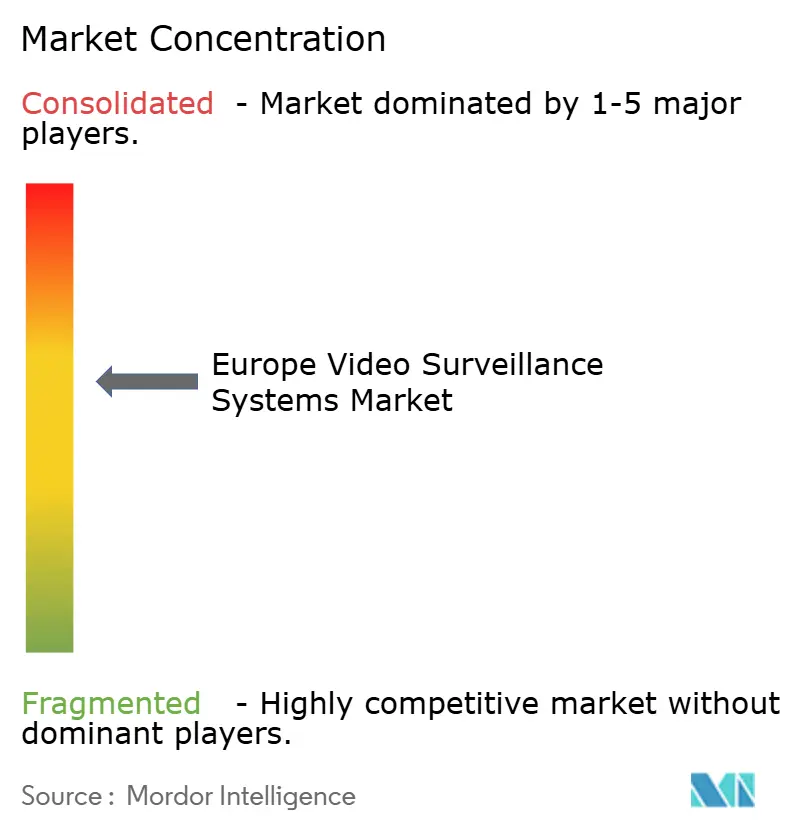

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Video Surveillance Systems Market Analysis by Mordor Intelligence

The Europe video surveillance systems market size in 2026 is estimated at USD 19.82 billion, growing from 2025 value of USD 17.87 billion with 2031 projections showing USD 33.29 billion, growing at 10.93% CAGR over 2026-2031. Adoption momentum is shifting from passive monitoring toward predictive, AI-driven platforms that mesh with smart-city roadmaps and ESG disclosure rules. Stringent geosecurity policies such as the United Kingdom’s April 2025 ban on Chinese-made gear are creating short-cycle replacement demand that benefits European and allied suppliers.[1]UK Government, “Police Facial Recognition Funding Announcement,” GOV.UK Parallel legislation the EU AI Act and Cyber Resilience Act forces vendors to re-architect products around edge processing and federated learning, thereby reducing cross-border data transfers. Cloud-managed Video as a Service models appeal to small enterprises that wish to convert capital expense into operating expense, while 5G connectivity accelerates municipal roll-outs in heritage city centers where trenching fiber is infeasible. AI-ready 4K cameras now underpin analytics that lower false-alarm rates, raising the baseline specification for new procurements.

Key Report Takeaways

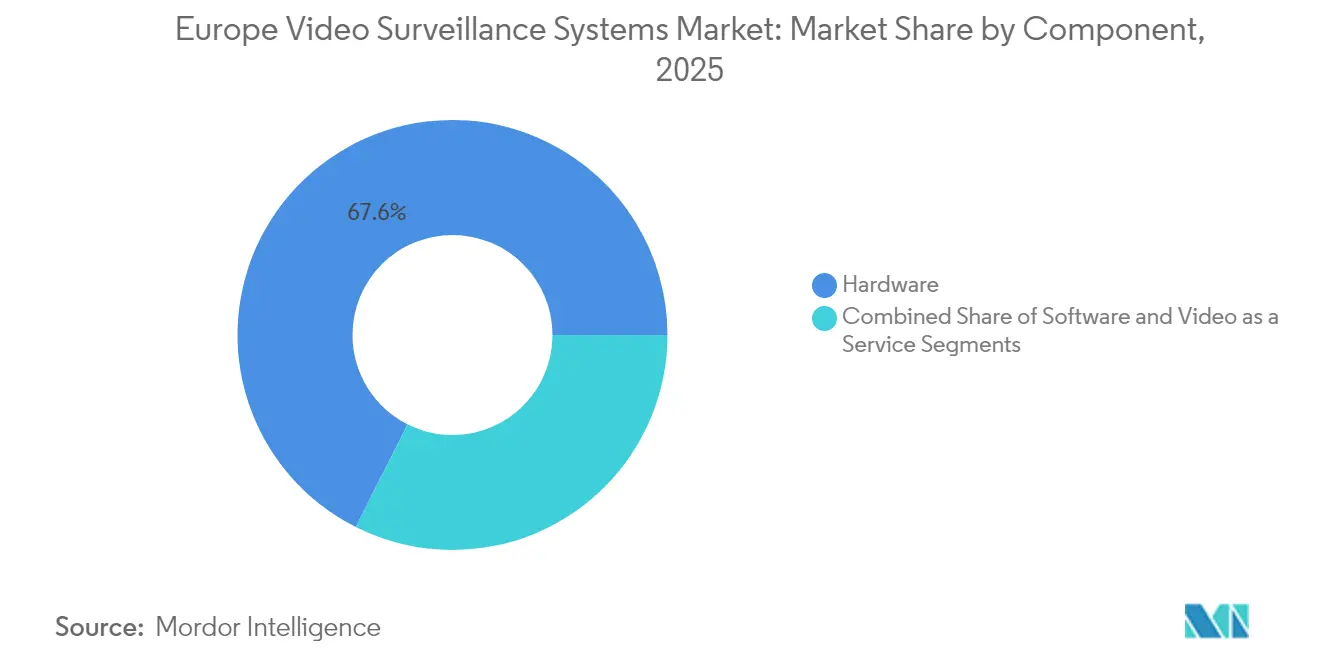

- By component, hardware led with 67.58% of Europe video surveillance systems market share in 2025, whereas Video as a Service is advancing at an 11.48% CAGR to 2031.

- By deployment mode, on-premises retained 60.55% share of the Europe video surveillance systems market size in 2025 and cloud is poised to expand at 11.95% through 2031.

- By connectivity, wired installations dominated with 52.10% share in 2025 while cellular and 5G cameras are forecast to rise at 12.65% CAGR to 2031.

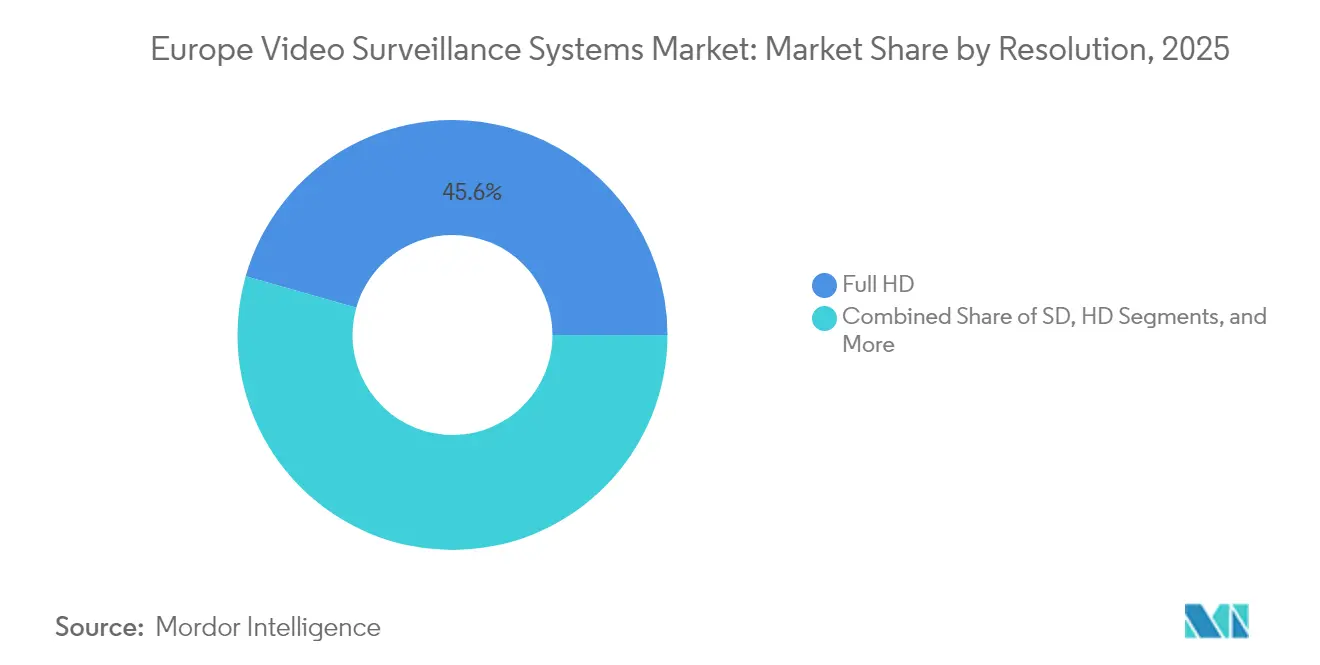

- By resolution, Full HD captured 45.60% share in 2025; 4K Ultra HD is projected to climb at 11.92% CAGR to 2031.

- By end-user, commercial sites held 42.85% in 2025, and the residential segment is expected to register an 11.55% CAGR to 2031.

- By country, the United Kingdom commanded 23.55% revenue in 2025, but Italy is projected to grow at 12.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Video Surveillance Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased Spending in Advanced Security Systems | +2.1% | UK, Germany, France, Italy, Rest of Europe | Medium term (2-4 years) |

| Growth in Public and Private Infrastructure | +1.9% | Italy, France, UK, Rest of Europe | Medium term (2-4 years) |

| Regulatory Push for Public Safety Compliance | +1.7% | EU-wide, strongest in Germany and France | Short term (≤ 2 years) |

| Rapid Adoption of AI-Enabled Video Analytics | +2.3% | UK, Germany, Italy, France | Short term (≤ 2 years) |

| Integration of Surveillance with ESG Retrofits | +1.2% | Germany, UK, France, Nordic nations | Long term (≥ 4 years) |

| Demand for GDPR-Compliant Edge Storage | +1.6% | EU-wide, notably Germany and France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increased Spending in Advanced Security Systems

Public budgets climbed sharply in 2024 as the United Kingdom earmarked GBP 230 million (USD 289 million) for police facial-recognition upgrades, while France set aside EUR 46 million (USD 49 million) to install AI traffic cameras across 4,000 roadside sites. Italy’s EUR 97.7 million (USD 104.3 million) Rome 5G CCTV program modernizes 2,000 analog cameras ahead of the 2025 Jubilee. Germany’s civil security framework funds pilots that favor domestic analytics vendors, reinforcing technological sovereignty. Commercial real-estate owners are mirroring these moves, embedding surveillance into building-management suites to meet ESG metrics that insurers and tenants now demand.

Growth in Public and Private Infrastructure

Critical-asset operators embrace multi-sensor networks to meet EU resilience directives. Europol budgeted EUR 67.8 million (USD 72.3 million) for biometric upgrades linking cameras to travel databases during 2025-2027. Genoa’s Project Hafnia integrates 2,700 cameras with NVIDIA-accelerated analytics for real-time traffic management. France’s defense plan allocates space-based funds for maritime surveillance, highlighting terrestrial-to-satellite convergence. The UK Ministry of Defence’s rising budget includes perimeter-security overhauls at sensitive sites. Utilities deploy thermal and hyperspectral cameras that cut physical patrols by 40%.

Regulatory Push for Public Safety Compliance

The EU AI Act, effective 2024, mandates algorithmic transparency and human oversight for high-risk video analytics. Europol ethical guidelines favor privacy-preserving methods such as federated learning, giving certified vendors a procurement edge.[2]Europol, “Programming Document 2025-2027,” EUROPOL.EUROPA.EU Germany’s NIS2 rollout compels essential-service operators to devote roughly 9% of IT budgets to cybersecurity, boosting demand for hardened cameras. Under the Cyber Resilience Act, manufacturers must patch firmware for five years, accelerating the pivot to edge-based designs that minimize network exposure.

Rapid Adoption of AI-Enabled Video Analytics

Edge processors embedded in cameras now conduct object recognition and license-plate capture locally, slashing bandwidth needs by up to 80%. Axis introduced 4K models with on-device AI that achieve 95% classification accuracy in low-light scenes. Bosch’s new FLEXIDOME line cuts false alarms by 70% via behavioral triggers. Lombardy municipalities saw park-crime fall 80% after deploying i-PRO cameras in 2024. Milestone’s XProtect integrates NVIDIA Metropolis to orchestrate federated learning across multivendor fleets. EU Digital Europe funding of EUR 390 million (USD 454.12million) backs privacy-compliant analytics research through 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security Concerns Regarding Video Data | −1.4% | EU-wide, notably Germany and France | Short term (≤ 2 years) |

| High Implementation and Maintenance Costs | −1.8% | Southern Europe, Eastern Europe | Medium term (2-4 years) |

| Fragmentation of National Standards | −0.9% | EU-wide, multi-country projects | Long term (≥ 4 years) |

| Semiconductor Supply-Chain Volatility | −1.1% | EU-wide, Asian dependencies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Security Concerns Regarding Video Data

Breaches targeting unpatched firmware intensified in 2024, prompting Germany’s BSI to recommend edge-level encryption with locally held keys. ENISA surveys show 89% of critical operators adding staff to manage surveillance vulnerabilities. GDPR Article 44 restricts exporting footage to non-adequate jurisdictions, complicating cloud back-ups. Italy’s security trade body reports a pivot to Western hardware amid worries over hidden backdoors, reinforced by the UK’s imminent Chinese-equipment ban. Hardware-level secure enclaves raise unit prices 15-20%, slowing purchases by budget-constrained municipalities.

High Implementation and Maintenance Costs

Enterprise-grade cameras range from EUR 500 (USD 533) to EUR 3,000 (USD 3,200), excluding installation, network upgrades, and software licenses. Southern and Eastern European SMEs often extend analog lifecycles to defer these expenditures. Annual maintenance, including firmware support, adds 10-15% to total cost. Rome’s 5G project earmarked EUR 20 million (USD 21.3 million) solely for upkeep. Subscription VSaaS reduces upfront spend but can exceed on-premises costs over long contracts once bandwidth fees escalate. Fragmented tender rules further erode scale economies, although Germany’s research pilots explore lower-cost deployment archetypes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Subscription Uptake Outpaces Hardware Dominance

Hardware retained 67.58% share in 2025. Cameras, recorders, and ancillary devices underpin most installed systems across the Europe video surveillance systems market. Yet, Video as a Service is projected to log an 11.48% CAGR, the fastest rise among components, as municipalities and SMEs pivot toward bundled leases that encompass equipment, cloud storage, and analytics within a single monthly invoice. Software platforms orchestrate heterogeneous fleets and embed AI that trims bandwidth by processing events at the edge. Axis released four GDPR-compliant models in Q3 2024 with on-board inference engines. Storage appliances still appeal in banking and defense, where auditors demand air-gapped evidence trails.

Operating-expense preferences give VSaaS momentum as enterprises guard cash in uncertain macro conditions. Verkada’s London hub markets a hybrid cloud that stores data locally for 30–120 days before archiving it to GDPR-aligned data centers. Eagle Eye has added federated learning support, allowing AI to refine models without viewing raw footage. Genetec’s Security Center 5.12 integrates AutoVu ALPR to help police trace vehicle movements while meeting AI Act audit mandates. Hardware OEMs counter by embedding stronger chips, positioning against pure-cloud rivals with hybrid value propositions, thereby sustaining the Europe video surveillance systems market as a balanced capex-opex landscape.

By Deployment Mode: Hybrid Designs Reconcile Compliance and Flexibility

On-premises architectures accounted for 60.55% share in 2025, favored by finance, defense, and critical-infrastructure segments that disallow public-cloud footage. Cloud services are forecast to expand at 11.95% CAGR, tapping SMEs that lack IT resources. Hybrid architectures blend local retention with cloud analytics, satisfying GDPR residency while accessing scalable AI. Milestone’s 2024 releases let operators tag streams for on-prem versus cloud processing. Rome’s city network keeps 30 days on local edge servers and archives older data inside national cloud facilities.

Bandwidth economics also shape choices. France’s 4,000 traffic cameras transmit only violation snapshots, lowering LTE overhead. Germany steers procurement toward EU-hosted infrastructure, minimizing foreign dependency. The UK’s Chinese-equipment sunset accelerates swaps to allied hybrid systems. Encryption keys under direct custody further mitigate third-party breach risk, supporting the Europe video surveillance systems market trajectory toward federated hybrid estates.

By Camera Connectivity: 5G Spurs Rapid Urban Deployment

Wired Ethernet and fiber remained dominant at 52.10% in 2025, yet cellular and 5G cameras should register 12.65% CAGR to 2031. Historic city centers avoid disruptive trenching; wireless installs reduce lead times from weeks to days. Rome installed 2,000 5G cameras in 2024 using national telecom networks. France’s EUR 46 million (USD 53.56 million) roadside program banks on LTE uploads of enforcement snapshots.

Dedicated network slices guarantee <20 ms latency and strong uplink, enabling real-time analytics. Germany’s research pilots test 5G standalone links for emergency response. Axis’ modular cellular sensor targets remote construction sites, using solar panels to power dormant-until-motion designs that conserve bandwidth. Hanwha’s Wisenet X Plus integrates LTE modems for railway corridors. Police mobility units in the UK feed biometric data to central watch lists over encrypted 5G, underlining the Europe video surveillance systems market’s move toward ultra-flexible connectivity.

By Resolution: 4K Becomes AI-Friendly Norm

Full HD commanded 45.60% share in 2025, an incumbent workhorse. 4K Ultra HD is projected to climb at 11.92% CAGR as higher pixel density boosts detection accuracy by roughly 25-30%. Axis’ 4K bullet model recognizes license plates at speeds of 120 km/h under 0.1 lux light. Bosch sensors pair 4K with analytics that slash false alerts 70%.

Italy’s Genoa Project Hafnia leaned on 4K streams to train NVIDIA vision-language models for congestion prediction. France’s roadside cameras specify 4K clarity to automate seatbelt and phone enforcement, cutting manual review by 60%. Compression advances (H.265+, H.266) lower storage need nearly 50%, making 4K affordable at scale and reinforcing the Europe video surveillance systems market evolution toward high-definition baselines.

By End-User: Residential Uptake Accelerates

Commercial premises led with 42.85% share in 2025, covering retail, banking, and hospitality. Residential projects are forecast for 11.55% CAGR through 2031 as multi-family developers bundle surveillance into smart-building dashboards to satisfy ESG-minded tenants. Government deployments shape marquee roll-outs such as Italy’s Rome Jubilee network and the UK’s police facial-recognition expansion.

Retailers overlay analytics on POS data to flag internal shrinkage, reporting 10-15% conversion boosts when layout tweaks align with heat-map insights. Banks require tamper-evident housings and encrypted streams at ATMs. Hospitality chains deploy privacy-masking in guest corridors while leaving lobby views unblurred to enhance safety assurances. Manufacturers use thermal cameras to detect PPE compliance and avert downtime. Utilities observe substations with fusion-sensor units, reducing patrols 40%. The Europe video surveillance systems market therefore spans disparate risk profiles, yet converges on AI-enabled insight extraction.

Geography Analysis

Southern Europe exhibits the fastest compound growth because EU recovery funds subsidize smart-city retrofits that bundle surveillance with traffic management. Italy’s EUR 97.7 million (USD 113.76 million) upgrade ahead of the 2025 Jubilee exemplifies event-linked stimulus that yields lasting infrastructure. Northern Europe, led by the United Kingdom and Germany, emphasizes data sovereignty. German pilots use federated learning to comply with strict privacy norms, while the UK’s procurement terms now prioritize allied supply chains. Eastern European municipalities, constrained by budget, gravitate toward subscription VSaaS models delivered from regional data centers. Collectively, these dynamics shape a mosaic where each subregion balances security imperatives against privacy culture, reinforcing the multifaceted expansion of the Europe video surveillance systems market.

Central European states deploy hybrid architectures that route analytics to in-country clouds, curbing latency and aligning with the Cyber Resilience Act’s five-year patch mandate. France’s nationwide AI traffic camera initiative signals how safety enforcement can drive high-volume camera deployments beyond traditional city-center grids. Nordic countries leverage renewable-powered edge nodes, aligning surveillance carbon footprints with local climate targets and ESG reporting. Such geographically varied drivers underpin steady demand yet compel vendors to localize feature sets, certifications, and data-residency options, thereby sustaining competitive diversification within the Europe video surveillance systems market.

Cross-border data-sharing projects, including Europol’s biometric interoperability upgrades, encourage harmonization of video metadata schemas. Yet divergent national cybersecurity labels still slow continent-wide roll-outs. EU cohesion programs increasingly fund joint tenders that aggregate smaller orders across Balkans and Baltics, improving purchasing power. As these mechanisms mature, they are expected to reduce fragmentation, enabling broader adoption of AI-ready cameras and cloud management tools in less urbanized areas, enlarging the addressable base of the Europe video surveillance systems market.

Competitive Landscape

Axis grew its Q3 2024 sales by 14% year-over-year and released four AI-equipped models that support GDPR-aligned edge inference. Bosch is partnered with Microsoft Azure and AWS to offer scalable video analytics, underscoring the growing importance of hyperscale partners. Milestone’s NVIDIA alliance, under Project Hafnia, demonstrates how software vendors leverage AI ecosystems to differentiate themselves.

Cloud-native challengers Verkada and Eagle Eye gain mindshare among SMEs by bundling hardware leasing with low-touch cloud management. Their expansion pressures incumbents to enrich firmware security and subscription offerings. Geopolitical factors reshape the share, the UK ban on certain Chinese brands prompts public agencies to shift toward European and allied portfolios, reallocating contracts worth tens of millions. Vendors achieving early compliance with the EU AI Act and Cyber Resilience Act gain bid advantages as public purchasers demand audit-ready documentation.

Regional specialists thrive in niche verticals, such as MOBOTIX in critical manufacturing and i-PRO in municipal crime reduction, leveraging deep domain expertise. Partner ecosystems remain pivotal, with open-architecture mandates prompting camera makers to certify integrations across Milestone, Genetec, and Hanwha platforms. The evolving mix of hardware, software, and service models keeps the Europe video surveillance systems market competitively dynamic while gradually tilting toward subscription economics and AI-centric differentiation.

Europe Video Surveillance Systems Industry Leaders

-

Hangzhou Hikvision Digital Technology Co. Ltd.

-

Robert Bosch GmbH

-

Axis Communications AB

-

Hanwha Vision Co., Ltd.

-

MOBOTIX AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Axis Communications updated its Q4 launch schedule, confirming volume shipment of AXIS Q1961-TE and AXIS P1468-LE across European distributors.

- September 2024: Axis Communications introduced four new AI-ready camera families and reported SEK 4.159 billion (USD 0.44 billion) in Q3 sales, a 14% annual uplift.

- August 2024: Milestone Systems rolled out XProtect 2024 R2, embedding zero-trust authentication that addresses NIS2 compliance.

- July 2024: Bosch launched FLEXIDOME IP starlight 8000i and MIC IP fusion 9000i for extreme environments, plus Azure and AWS analytics partnerships.

Europe Video Surveillance Systems Market Report Scope

The Europe video surveillance systems market encompasses the technologies and services used to capture, store, analyze, and manage video data for security and operational purposes across commercial, industrial, residential, and government sectors. It includes hardware, software, and cloud-based video services deployed through various connectivity options and resolutions. Overall, the market focuses on enhancing safety, real-time monitoring, and intelligent analytics across diverse environments in Europe.

The Europe Video Surveillance Systems Market Report is Segmented by Component (Hardware, Software, Video as a Service), Deployment Mode (On-Premises, Cloud, Hybrid), Camera Connectivity (Wired, Wireless, Cellular/5G), Resolution (SD, HD, Full HD, 4K Ultra HD, 8K and Above), End-User (Commercial, Industrial, Residential, Government), and Geography (United Kingdom, Germany, France, Italy, Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

By Component

| Hardware | Camera |

| Storage | |

| Software | Video Analytics |

| Video Management Software | |

| Video as a Service (VSaaS) |

By Deployment Mode

| On-Premises |

| Cloud |

| Hybrid |

By Camera Connectivity

| Wired |

| Wireless (Wi-Fi) |

| Cellular/5G |

By Resolution

| Standard Definition (SD) |

| High Definition (HD) |

| Full HD |

| 4K Ultra HD |

| 8K and Above |

By End-User

| Commercial | Retail |

| Banking, Financial Services and Insurance (BFSI) | |

| Hospitality | |

| Industrial | Manufacturing |

| Energy and Utilities | |

| Residential | Single-Family |

| Multi-Family | |

| Government | City Surveillance |

| Transportation Infrastructure |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Rest of Europe |

| By Component | Hardware | Camera |

| Storage | ||

| Software | Video Analytics | |

| Video Management Software | ||

| Video as a Service (VSaaS) | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| Hybrid | ||

| By Camera Connectivity | Wired | |

| Wireless (Wi-Fi) | ||

| Cellular/5G | ||

| By Resolution | Standard Definition (SD) | |

| High Definition (HD) | ||

| Full HD | ||

| 4K Ultra HD | ||

| 8K and Above | ||

| By End-User | Commercial | Retail |

| Banking, Financial Services and Insurance (BFSI) | ||

| Hospitality | ||

| Industrial | Manufacturing | |

| Energy and Utilities | ||

| Residential | Single-Family | |

| Multi-Family | ||

| Government | City Surveillance | |

| Transportation Infrastructure | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe video surveillance systems market in 2026?

The market stands at USD 19.82 billion in 2026, with a 10.93% CAGR outlook to 2031.

Which component segment is growing fastest?

Video as a Service is projected to expand at 11.48% annually as users favor subscription models over capital purchases.

Why are 5G cameras gaining ground?

5G connectivity enables rapid deployment in heritage city centers where fiber trenching is costly and provides low-latency links for real-time analytics.

What drives Italys leading growth rate?

Smart-city projects such as Romes EUR 97.7 million (USD 113.76 million) 5G CCTV and Genoas AI-powered traffic network push Italy toward a 12.05% CAGR to 2031.

How is EU regulation shaping vendor strategy?

The AI Act and Cyber Resilience Act compel manufacturers to provide transparent, edge-processed analytics and five-year firmware support, favoring compliant vendors in public tenders.

Who are the major market players?

Hikvision, Bosch, Axis Communications, Hanwha Vision, and Milestone Systems together hold roughly 45-50% of regional revenue, with cloud-native firms like Verkada rising fast.

Page last updated on: