United States Vibration Control System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 0.99 Billion |

| Market Size (2030) | USD 1.36 Billion |

| Growth Rate (2025 - 2030) | 6.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Vibration Control System Market Analysis by Mordor Intelligence

The United States vibration control system market size is estimated at USD 0.99 billion in 2025 and is projected to reach USD 1.36 billion by 2030, growing at a 6.57% CAGR from 2025 to 2030. This expansion reflects the deeper adoption of Industry 4.0 practices, the wider use of precision manufacturing in semiconductor fabs, data center builds, and electric vehicle assembly, as well as stricter nationwide noise and vibration workplace standards. Investments tied to the CHIPS Act, the Inflation Reduction Act, and state-level clean-energy incentives are concentrating fresh demand in battery, electronics, and advanced-materials corridors, while IoT-enabled condition monitoring and smart materials are redefining buyer expectations for sub-micron stability. Competitive intensity is rising as incumbents integrate active algorithms and edge analytics that support predictive maintenance, a capability commanding premium prices among hyperscale data-center operators and semiconductor toolmakers. Rising capital allocation toward smart damping platforms, coupled with qualified workforce shortages, is creating service opportunities around integration, retrofit, and validation testing across the United States vibration control system market.

Key Report Takeaways

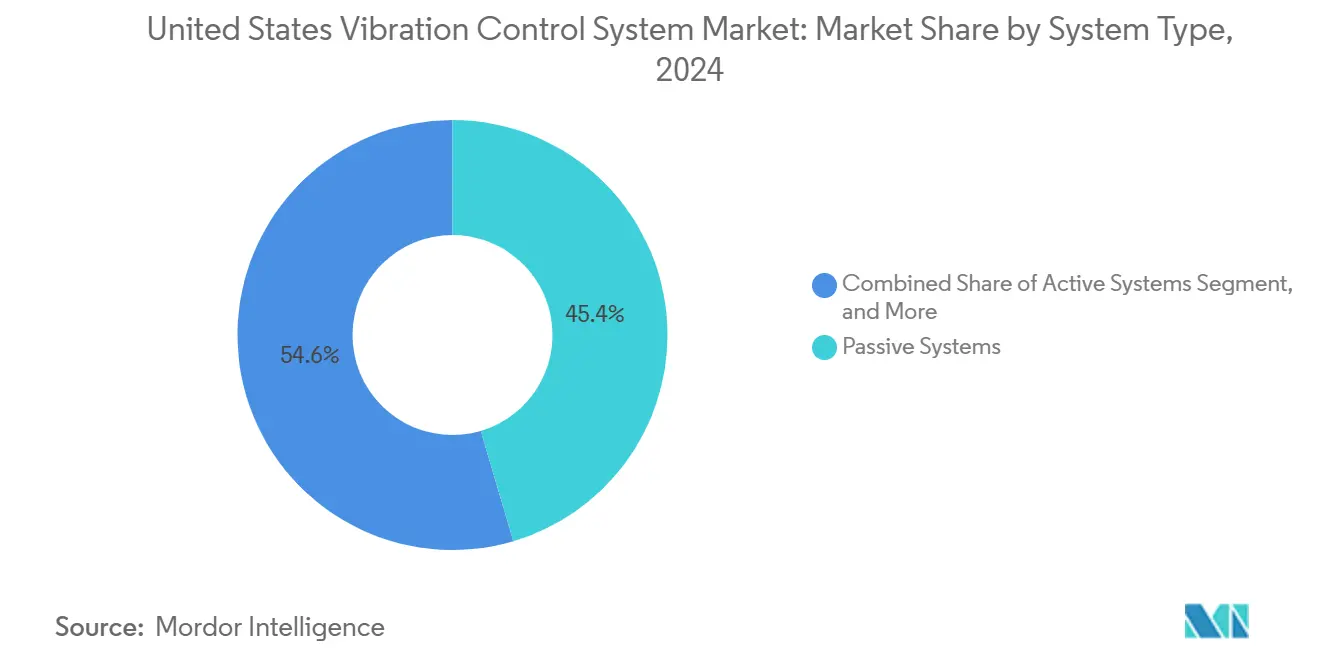

- By system type, passive solutions held 45.43% revenue share in 2024; active platforms are projected to expand at a 7.23% CAGR through 2030.

- By component, isolators and mounts dominated the United States vibration control system market with a 38.71% market share in 2024, whereas pads and sheets are expected to grow at the fastest rate, at a 6.73% CAGR.

- By end-user, automotive lines retained leadership at 27.87% in 2024; healthcare and laboratory installations are expected to accelerate at a 6.61% CAGR through 2030.

- By material, elastomer-based designs captured a 39.86% share in 2024, while air/pneumatic formats are forecast to post the strongest growth at a 7.36% CAGR.

United States Vibration Control System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification of manufacturing footprints | +1.2% | National (South and Midwest focus) | Medium term (2-4 years) |

| Stricter NVH regulations in vehicles and plants | +0.9% | National (early adoption California and Northeast) | Short term (≤ 2 years) |

| Data-center expansion needing seismic-grade mounts | +1.1% | Virginia, Texas, Oregon clusters | Medium term (2-4 years) |

| Reshoring semiconductor fabs | +1.4% | Arizona, Texas, Ohio | Long term (≥ 4 years) |

| Urban-air-mobility prototype adoption | +0.6% | West Coast metros | Long term (≥ 4 years) |

| Venture funding for tunable smart dampers | +0.8% | Tech hubs nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electrification of the U.S. manufacturing sector is boosting demand for precision vibration isolation.

Moving toward electric-drive production lines requires ±0.1 mm accuracy when inserting battery cells, forcing factories to transition from legacy elastomeric pads to adaptive active platforms that can compensate for high-frequency inverter noise. Tesla’s Austin site already operates more than 2,000 pneumatic isolation tables to meet these tolerances, demonstrating clear payback in reduced scrap and rework. [1]Technical Manufacturing Corporation, “Precision Vibration Control Solutions,” techmfg.com Hybrid approaches that combine active piezo stages with polyurethane isolators are now standard in steel mini-mills that deploy electric arc furnaces, where vibration spectra differ significantly from those of conventional casting equipment.

Stricter NVH regulations for vehicles and industrial equipment

EPA proposals to tighten occupational noise limits intersect with OSHA whole-body-vibration thresholds of 0.5 m/s² for an 8-hour shift, compelling factory upgrades in stamping, forging, and paper-converting lines. [2]Occupational Safety and Health Administration, “Occupational Noise Exposure Guidelines,” osha.gov In vehicles, the absence of combustion masking in EV cabins means that chassis-borne excitations, which were once acceptable, now trigger compliance risks, prompting OEMs to integrate magnetorheological mounts at the sub-assembly level.

Growth of data-center construction requiring seismic-grade vibration mounts

Hyperscale projects in northern Virginia and central Texas specify isolation that holds <10 Hz spectra under magnitude-7 seismic shocks. Meta’s USD 800 million Illinois campus installed 15,000 isolators engineered for such events. [3]Meta Platforms, “Data Center Infrastructure Investments,” about.fb.com Liquid-cooling pumps and AI-accelerator racks introduce broadband vibration that passive pads cannot attenuate, thereby accelerating the adoption of air-spring platforms coupled with sensor feedback loops.

Reshoring of semiconductor fabs demanding sub-micron vibration control

Intel’s USD 20 billion Ohio mega-fab stipulates floor stability within 25 nm peak-to-peak over the frequency range of 1–200 Hz, a benchmark unachievable by passive means alone. NIST now recommends VC-E limits as baseline for 3-nm lithography suites, favoring pneumatic tables with real-time piezo trim. Tool makers note yield losses above 10 nm drift, translating into multimillion-dollar wafer risk per hour, which fortifies spending across the United States' vibration control system market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of active systems for SMEs | −0.8% | Nationwide (Midwest concentrated) | Short term (≤ 2 years) |

| Supply-chain volatility in specialty elastomers | −0.6% | Automotive and aerospace clusters | Medium term (2-4 years) |

| Patent thickets around adaptive algorithms | −0.4% | Technology hubs | Long term (≥ 4 years) |

| Slow retrofit cycles in legacy plants | −0.5% | Midwest and Northeast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High upfront cost of active systems for SMEs

Fully integrated active lines can exceed USD 100,000 per cell, a tenfold premium over functionally adequate passive mounts, deterring facilities with revenues under USD 50 million. Vendors now trial subscription-style vibration-as-a-service bundles that cut capital outlay by 60%, yet engineering know-how and commissioning complexity remain non-trivial hurdles.

Supply-chain volatility in specialty elastomers

Fluoroelastomer disruptions prompted a 35% price spike in 2024 following U.S. production incidents, which extended lead times to eight weeks for high-temperature compounds. Aerospace and EV driveline programs that rely on 200 °C stability face redesign or dual-sourcing costs, which curbs near-term adoption speed in segments that value cost certainty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Active Platforms Outpace Passive Mainstays

The United States vibration control system market size for passive solutions remained dominant in 2024; however, active formats are expected to post a 7.23% CAGR from 2025 to 2030, as semiconductor fabs and battery lines demand real-time correction. Hybrid semi-active mounts connect elastomer layers with magnetorheological fluid cores, enabling 40% higher attenuation under EV drivetrain harmonics. OEMs value the maintenance-free nature of passive designs, but edge-analytics dashboards bundled with active systems now quantify yield gains, narrowing perceived cost gaps. Future contracts are increasingly specifying mean-time-between-failure clauses that favor systems with integrated sensor diagnostics, a differentiator that lifts the active slice of the United States vibration control system market.

In parallel, passive technologies are advancing through graphene-doped polyurethane, which lifts damping by 25% while keeping the cost below USD 5 per kilogram. Semi-active algorithms can deactivate energy-hungry actuators during steady-state phases, lowering life-cycle energy draw by 30%. Such energy-aware controls may unlock broader SME uptake once first-generation equipment depreciates, further shifting the demand profile.

By Component: Isolators Maintain Lead, Pads Surge in IT Deployments

Isolators and mounts accounted for 38.71% of 2024 revenue, underscoring their widespread use across rotary equipment. Nevertheless, pads and sheets will rise fastest at 6.73% CAGR as colocation operators refit existing data halls; a single 30 MW build can consume 50,000 square feet of sheet damping. Springs and washers remain relevant in legacy engine facilities, although electric platforms are redirecting R&D toward lightweight composite couplers. Advanced fasteners embedding piezo shims emerge as a micro-category, winning pilot orders in aerospace hull pylon interfaces. ISO 10816 conformance drives OEMs to request factory-fit sensors, transforming traditionally static hardware into quasi-instrumented nodes that feed plant-wide predictive analytics. Component modularity now serves as a procurement criterion, allowing integrators to swap failed mounts within two hours, thereby minimizing downtime costs. Consequently, pads and isolators will remain central to the United States vibration control system market through the decade.

By End-User Industry: Healthcare Momentum Builds on Precision Imaging

Although automotive lines accounted for 27.87% of revenue in 2024, hospital investments are expected to accelerate at a 6.61% CAGR, driven by the demand for 0.1 µm stability in new MRI and robotic-surgery suites. EV manufacturers still dominate unit volumes, but competitive differentiation now hinges on ride comfort, driving the deployment of smart sub-frame dampers across mid-priced models. Aerospace/defense users specify operating envelopes of −55 °C to +125 °C, steering them toward metal-rubber hybrids. Industrial machinery has the broadest installed base, although capital refresh cycles average 12 years, which slows short-term penetration of active upgrades. Semiconductor and electronics plants, despite smaller absolute spending, purchase the highest-priced solutions per square foot, thereby elevating the value mix of the United States vibration control system market.

Healthcare labs are adopting bench-top pneumatic isolators for gene-sequencing robots, a niche market expected to triple the number of installed units by 2030. Oil and gas offshore rigs are increasingly equipped with tuned mass dampers tailored for platform sway. Building and construction markets pivot from HVAC isolation alone to holistic seismic retrofits for life-safety infrastructure, reflecting recent code updates in California and Washington.

By Material Type: Air Systems Capture Low-Frequency Niche

Elastomers retained a 39.86% share in 2024, owing to their cost-performance balance. However, air/pneumatic designs are expected to log a 7.36% CAGR, winning clean-room and metrology contracts where sub-5 Hz isolation is mandatory. The United States vibration control system market size for air formats in semiconductor tool bays is forecast to double by 2030, alongside the ramp-up to 3-nm node technology. Compact bellows achieving 90% attenuation below 5 Hz while occupying 40% less volume now fit under EV laser-welding cells. Metal-based springs remain indispensable for presses exceeding 50 tons; composite and smart alloys unlock shape-adaptive dampers for aerospace lifting surfaces. Bio-derived silicones under evaluation may reduce petrochemical exposure, aligning with buyer ESG mandates, but thermal limits restrict them to <120 °C use cases for now. Vendors expect mixed-material stacks, air bladders backed by graphene-elastomer mats, to define the next generation of high-bandwidth isolation.

Geography Analysis

The South accounted for 34.23% of 2024 revenue and is projected to advance at a 7.43% CAGR through 2030, cementing its dual leadership in size and velocity across the United States vibration control system market. Georgia-to-Texas battery and EV hubs, supported by the Inflation Reduction Act’s cell tax credits, drive blanket demand for isolation tables in cathode calendaring, battery cell stacking, and drivetrain testing bays. Semiconductor-grade elastomer consumption in Austin and Phoenix corridors further elevates order flows, while Gulf Coast elastomer producers provide near-site supply assurance, shaving logistics costs and lead times.

The West follows as the technology epicenter, propelled by USD 60 billion worth of announced fab and hyperscale data center builds that elevate per-unit isolation spending. OEM contracts for nanometer-level stability in Arizona and Oregon shift the revenue mix toward active air systems, reinforcing high average selling prices. Earthquake-prone zoning codes intensify architectural demand for base-isolation bearings in Californian hospitals and municipal buildings, creating a resilient retrofit market despite softening residential construction.

The Midwest and Northeast show steadier trajectories. Midwestern auto facilities undergo EV retooling, swapping engine-block shake rigs for battery-pack assembly isolators, sustaining a mid-single-digit growth clip. Northeastern aerospace and defense primes prioritize reliability programs over greenfield capacity, resulting in predictable but slower-growing spares demand. Incentives for on-shore pharmaceutical fill-finish plants in Pennsylvania and Massachusetts introduce new hospital-grade isolation use cases, modestly lifting the regional contribution within the United States vibration control system market.

Competitive Landscape

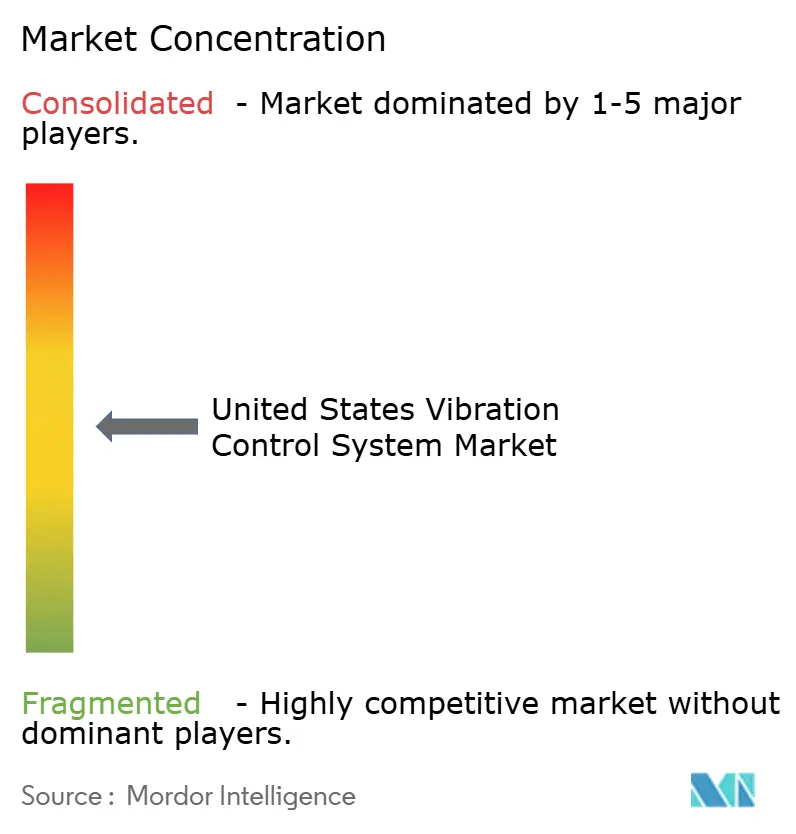

The playing field remains moderately fragmented, with the top five vendors controlling just under 55% of the 2024 turnover; however, consolidation is gathering pace. Parker-Lord’s 2020 integration set a precedent for material-to-controls vertical mergers, later echoed by Trelleborg’s 2024 buyout of Dynamic Solutions Systems that broadened its semiconductor reach. Price competition is muted because purchasers prioritize uptime and certified attenuation performance, allowing suppliers to differentiate themselves through adaptive algorithms, magnetorheological fluids, and IoT diagnostics.

Disruptors such as Phononics develop metamaterial plates that target discrete frequency bands, potentially leapfrogging elastomer-air hybrids in aerospace payload mounts. Start-ups also deploy AI to predict damping coefficient drift, feeding automatic calibration routines that slash manual maintenance by half. Patent walls around piezoelectric feedback loops and MR-fluid valve designs create entry barriers; newcomers either license IP or focus on niche geometries that are unsheltered by strong claims.

Service layers—from site vibration audits to retrofit commissioning-grow faster than hardware, especially among SMEs that lease rather than buy. Vendors with cloud-based dashboards bundle lifetime analytics contracts, booking recurring revenues while deepening customer lock-in. Consequently, the United States vibration control system market exhibits a market concentration score of 6, reflecting a setting where the top five suppliers command approximately 55% of the collective share, yet still face differentiated rivals in specialized niches.

United States Vibration Control System Industry Leaders

Parker-Lord Corporation

Hutchinson S.A.

Trelleborg AB

Getzner Werkstoffe GmbH

Fabreeka International LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Fabreeka earned ISO 14001 certification for its Boston plant.

- January 2025: VibraSystems debuted compact pneumatic lab isolators with a 50% smaller footprint.

- January 2025: Parker Hannifin invested USD 150 million to expand its Dayton, Ohio, facility, adding magnetorheological damper lines that lift aerospace system output 40%.

- December 2024: Trelleborg closed an USD 85 million acquisition of Dynamic Solutions Systems, enhancing sub-micron isolation offerings for fabs.

United States Vibration Control System Market Report Scope

| Passive Systems |

| Active Systems |

| Semi-Active/Hybrid Systems |

| Isolators and Mounts |

| Pads and Sheets |

| Hangers and Dampers |

| Springs and Washers |

| Other Components |

| Automotive |

| Aerospace and Defense |

| Industrial Machinery |

| Oil and Gas |

| Building and Construction |

| Electronics and Semiconductor |

| Healthcare and Laboratory |

| Metal-Based |

| Elastomer-Based |

| Air/Pneumatic |

| Composite and Smart Materials |

| By System Type | Passive Systems |

| Active Systems | |

| Semi-Active/Hybrid Systems | |

| By Component | Isolators and Mounts |

| Pads and Sheets | |

| Hangers and Dampers | |

| Springs and Washers | |

| Other Components | |

| By End-User Industry | Automotive |

| Aerospace and Defense | |

| Industrial Machinery | |

| Oil and Gas | |

| Building and Construction | |

| Electronics and Semiconductor | |

| Healthcare and Laboratory | |

| By Material Type | Metal-Based |

| Elastomer-Based | |

| Air/Pneumatic | |

| Composite and Smart Materials |

Key Questions Answered in the Report

What is the 2025 market value for vibration control solutions in the United States?

The United States vibration control system market size is USD 0.99 billion in 2025.

How fast will the sector grow through 2030?

Aggregate demand is projected to expand at a 6.57% CAGR between 2025 and 2030.

Which system type is advancing quickest?

Active solutions lead growth with a 7.23% CAGR, driven by semiconductor fabs and data-center builds.

Why is the South region outperforming other areas?

Concentrated EV battery, semiconductor, and incentives under the CHIPS and Inflation Reduction Acts push the South to a 7.43% CAGR and 34.23% 2024 share.

What primary restraint affects small manufacturers?

High capital costs of active platforms, often ten times that of passive mounts, slow adoption among SMEs.

Which material technology is gaining share for low-frequency isolation?

Air/pneumatic systems are expected to post a 7.36% CAGR owing to superior performance below 5 Hz.

Page last updated on: