360-Degree Camera Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

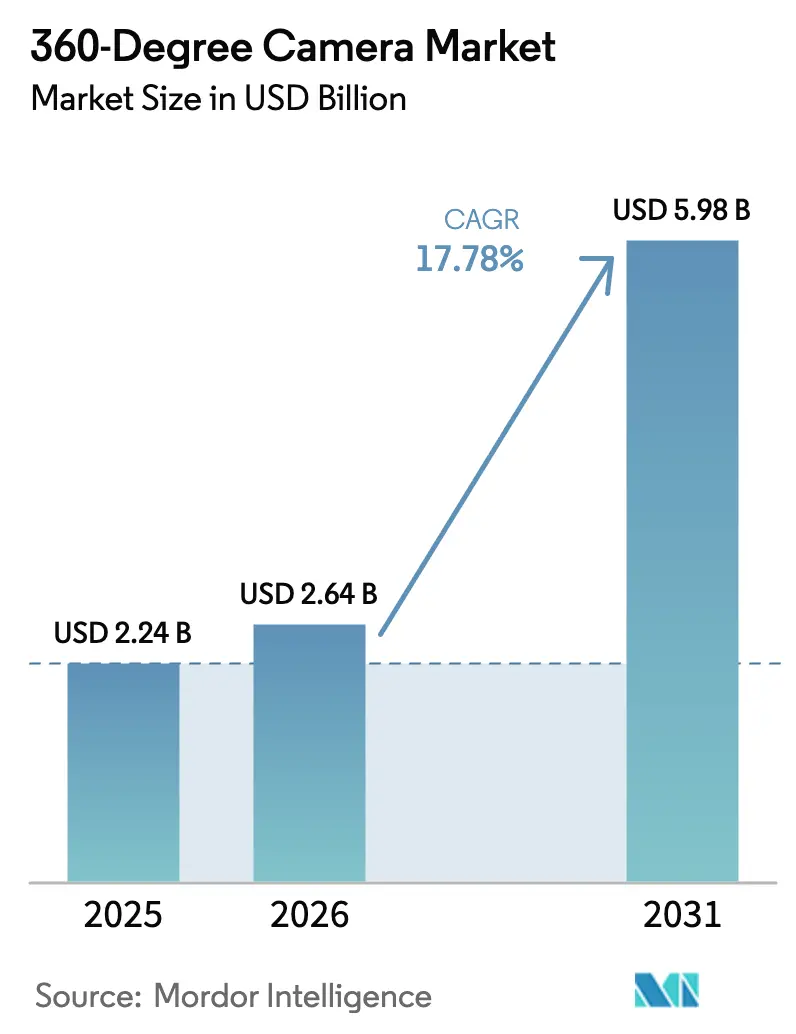

| Market Size (2026) | USD 2.64 Billion |

| Market Size (2031) | USD 5.98 Billion |

| Growth Rate (2026 - 2031) | 17.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

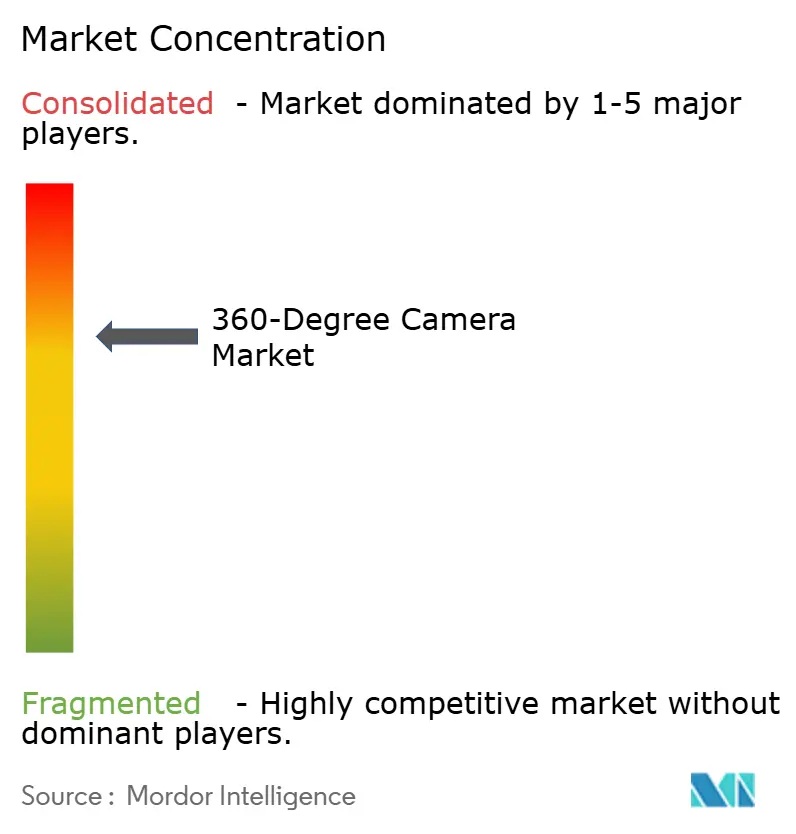

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

360-Degree Camera Market Analysis by Mordor Intelligence

The 360° camera market size was valued at USD 2.24 billion in 2025 and estimated to grow from USD 2.64 billion in 2026 to reach USD 5.98 billion by 2031, at a CAGR of 17.78% during the forecast period (2026-2031). Automotive perception stacks, immersive live-streaming, and defense training programs are transforming what was a niche gadget segment into critical infrastructure for mobility, media, and security. Autonomous-vehicle pilots in North America and Europe increasingly specify surround-view rigs to complement LiDAR and radar arrays, while Asia Pacific’s esports producers adopt glass-to-glass 360° workflows to satisfy 5G-enabled audiences. Fleet insurers now mandate dash-cams capable of 360° capture for telematics-driven underwriting, accelerating OEM partnerships. Supply-chain tightness for sub-11 nm chipsets, coupled with intensifying intellectual-property disputes, is prompting vertically integrated firms to secure foundry capacity and legal defensibility.

Key Report Takeaways

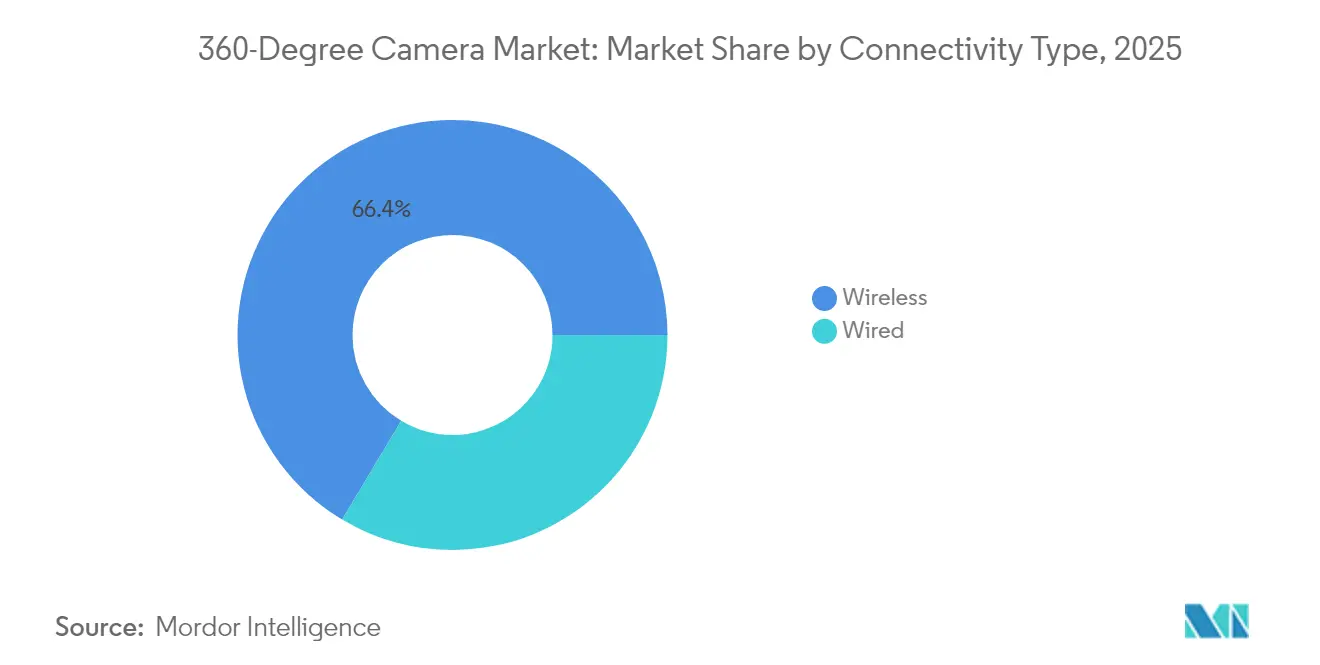

- By connectivity type, wireless captured 66.42% of 360° camera market share in 2025 and is advancing at an 17.98% CAGR through 2031.

- By product type, single-lens pocket cameras held 53.35% revenue share in 2025; in-vehicle 360° dash-cams are forecast to expand at an 18.22% CAGR to 2031.

- By resolution, Ultra-HD 4K accounted for 57.12% share of the 360° camera market size in 2025; Ultra-HD 8K+ is the fastest-growing resolution band at an 18.41% CAGR.

- By end-user, automotive applications registered the highest trajectory with a 19.01% CAGR through 2031, outpacing the consumer segment’s 37.62% share in 2025.

- By distribution channel, online marketplaces dominated with 61.25% share in 2025 while progressing at an 18.05% CAGR.

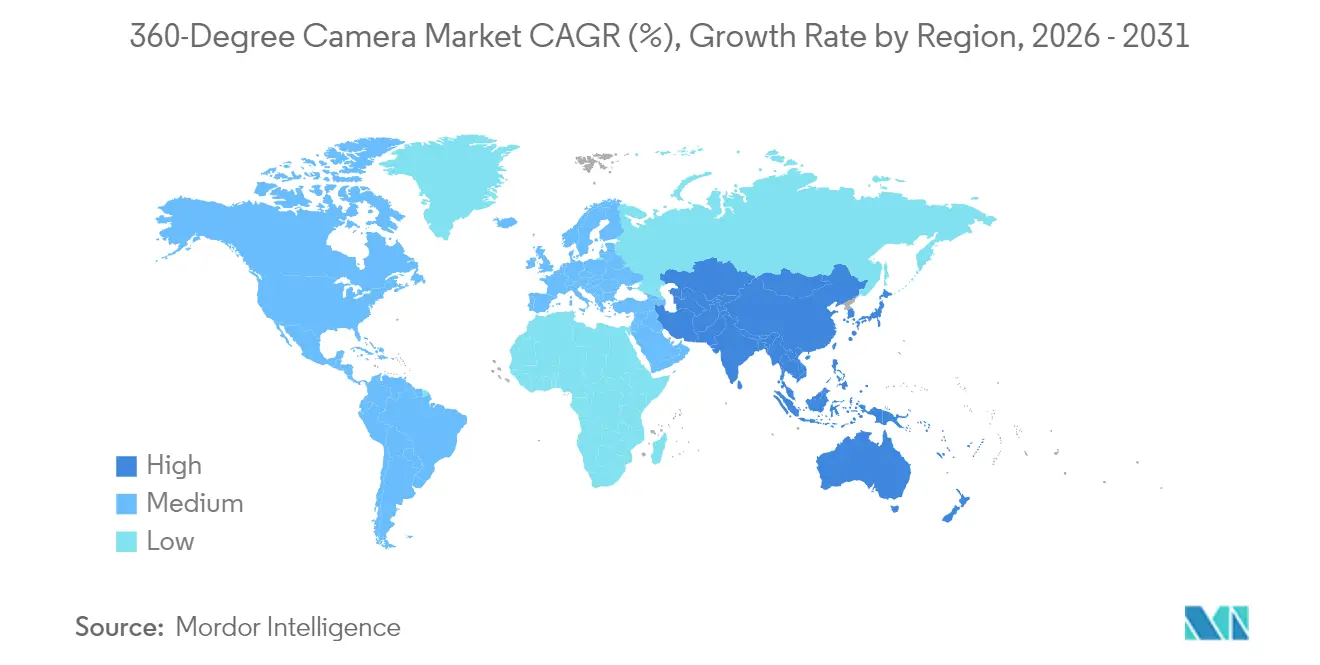

- By geography, Asia Pacific led with a 41.50% revenue contribution in 2025 and remains the quickest-expanding region at a 18.74% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of 360-Degree Camera Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of 360° cameras into autonomous-vehicle perception stacks | +3.2% | North America and Europe | Medium term (2–4 years) |

| Immersive live-streaming demand for esports and concerts | +2.8% | Asia Pacific; global spill-over | Short term (≤ 2 years) |

| VR-based training adoption by Middle-East defense agencies | +1.9% | Middle East; global defense | Medium term (2–4 years) |

| Virtual property-tour services in European luxury real-estate | +1.5% | Europe; North America extension | Short term (≤ 2 years) |

| Remote industrial-robot inspection of offshore energy assets | +2.1% | Global; North Sea, Gulf of Mexico | Long term (≥ 4 years) |

| Fleet insurers mandating 360° dash-cams for telematics scoring | +2.4% | North America; global adoption | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Integration of 360° cameras into autonomous-vehicle perception stacks in NA and EU pilot programs

Multimodal perception frameworks such as OmniDet demonstrate that surround-view fisheye arrays deliver depth estimation, visual odometry, and object detection at real-time throughput, supplying cost-effective blind-spot coverage that LiDAR alone cannot guarantee.[1]OmniDet: Surround View Cameras based Multi-task Visual Perception Network for Autonomous Driving,” sites.google.com Pilot fleets across Germany and California embed these rigs to move from Level 2 toward Level 4 capabilities, validating 360° vision as a critical path sensor. Research consortia like CoCar NextGen show the technology’s role in data-centric development pipelines that shorten validation cycles for edge cases . The result is a measurable +3.2 percentage-point lift to forecast CAGR as automotive suppliers lock in multi-year sourcing commitments.

Surge in immersive live-streaming demand for esports and concerts across Asia

Production houses in Seoul, Singapore, and Shanghai now leverage glass-to-glass 360° workflows, integrating Panasonic AK-UC4000 chains with the KAIROS IP platform to eliminate moiré under LED walls while pushing HDR feeds at sub-2-frame latency.[2]Panasonic, “A True Glass-to-Glass Solution from Capture to Delivery for eSports,” eu.connect.panasonic.com Esports arenas report dwell-time extensions and monetizable viewpoint switching that translate into new advertising inventory. Concert promoters replicate the model, and national 5G rollouts underpin bandwidth headroom, driving a +2.8 percentage-point CAGR uplift.

Rapid VR-based training adoption by Middle-East defense agencies

Procurement programs in the UAE, Saudi Arabia, and Qatar have shifted live-fire budgets toward XR simulators using Varjo XR-3 headsets fed by high-fidelity 360° footage. DHS market-survey benchmarks confirm that gaze-tracking and biometrics-based performance scoring require such omnidirectional video to maintain training realism.[3]U.S. Department of Homeland Security, “Virtual Reality Training Systems for First Responders Market Survey Report,” dhs.gov Reduced live-munition costs and higher training-throughput ratios move defense buyers toward long-term service contracts that embed 360° capture devices.

Growth of virtual property-tour services in European luxury real-estate

Luxury brokers in Paris, Berlin, and Zurich embed Matterport-enabled 360° walkthroughs, cutting cross-border travel while broadening prospect funnels. Engel & Völkers disclosed a 30% revenue jump after scaling virtual tours during disrupted showing conditions. Integration with drone exteriors forms hybrid listings that accelerate decision cycles for high-net-worth buyers, sustaining premium equipment demand.

Restraints Impact Analysis of 360-Degree Camera Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented stitching-software standards hindering professional broadcast interoperability | −2.1% | Global professional markets | Medium term (2–4 years) |

| High bandwidth cost for UHD 360° streaming in emerging APAC | −1.8% | Emerging Asia Pacific | Short term (≤ 2 years) |

| GDPR-driven privacy-litigation risk for public-space recording in EU | −1.3% | Europe; global privacy adoption | Long term (≥ 4 years) |

| Thermal-management constraints in compact wearable form-factors | −1.6% | Global consumer wearables | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Fragmented stitching-software standards hindering professional broadcast interoperability

Broadcasters face vendor lock-in as proprietary SDKs, such as NVIDIA VRWorks, dominate high-quality stitching workflows yet remain closed. VSF and EBU guidelines address transport but omit 360° stitching specifics, forcing studios to develop in-house tools that inflate capex and delay live-production rollouts . Until SMPTE ratifies a uniform mezzanine format, adoption stagnates, shaving 2.1 percentage points off CAGR.

High bandwidth cost for UHD 360° streaming in emerging APAC

Last-mile connectivity gaps documented by the Asian Development Bank combine with uneven wholesale rates to keep per-GB costs elevated in Indonesia, Philippines, and rural India. UHD 8K streams exceed affordable data caps, curbing consumer and SME deployment potential and tempering regional growth by −1.8 percentage points

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

360-Degree Camera Market Segment Analysis

By Connectivity Type:

Wireless dominance acceleratesWireless systems commanded 66.42% of the 360° camera market in 2025 and are forecast to grow at an 17.98% CAGR. Automotive integrators favor Wi-Fi 6 and ultra-wideband links that simplify head-unit retrofits, while offshore inspection drones rely on sub-sea acoustic relays that remove tether requirements. Wired SDI continues in studio control rooms where zero-dropout reliability is non-negotiable. A wave of multi-path video-over-5G prototypes suggests further displacement of cabling in field production.

Emerging use cases in warehouse automation pair 360° vision with private 5G slices, allowing forklifts to stream low-latency feeds to edge AI servers. As battery densities advance, operating hours extend, eroding the few remaining objections to wireless deployments. Vendor roadmaps prioritize firmware-level encryption to protect telematics data, cementing wireless as the default transport layer for the 360° camera market.

By Product Type:

Single-lens simplicity meets specialized demandSingle-lens pocket units held the largest share at 53.35% in 2025, popular among social-media creators for tap-to-share convenience. However, fleet insurers’ mandates propel in-vehicle 360° dash-cams to an 18.22% CAGR. Automotive-grade enclosures with −40 °C cold-start ratings and ASIL-B compliant image sensors differentiate this sub-segment.

Professional multi-lens rigs, though niche, underpin premium volumetric video shoots and XR stages requiring sub-pixel parallax fidelity. Vendors address weight constraints through carbon-fiber housings and remove extraneous cabling to meet drone lift limits. As the 360° camera market size for industrial inspection widens, ruggedized multi-lens designs secure procurement from oil and gas operators seeking explosion-proof certifications.

By Resolution:

Ultra-HD 4K dominance under pressureUltra-HD 4K maintained 57.12% share of the 360° camera market size in 2025, balancing clarity with manageable bitrates. Demand for 8K and above grows at 18.41% CAGR, powered by cinematic VR and sports replay systems that monetize replay-angle merchandising. 5G millimeter-wave deployments in stadiums enable real-time 8K streaming, eroding prior bandwidth objections.

Chiplet-based ISP architectures now compress 8K equirectangular feeds at sub-15 W, mitigating thermal concerns. Nevertheless, cost-sensitive surveillance buyers in emerging markets still opt for HD, citing storage overheads. The net effect is a bifurcated resolution ladder that equipment vendors exploit via tiered SKU strategies.

By End-User:

Automotive applications accelerate past consumer marketsAutomotive deployments log a 19.01% CAGR, overtaking consumer hobbyists. Regulatory frameworks in California and Bavaria incorporate 360° coverage into lane-keeping-assist validation, while insurers rebate policies when fleets install surround-view dash-cams. Consumer adoption remains robust, yet its 37.62% 2025 share erodes as industrial and defense contracts yield higher annual-recurring revenue.

Media-production houses push the envelope with volumetric-stage builds that house 100+ synced 360° cameras. Defense agencies request export-controlled SKUs with hardware encryption. Healthcare researchers explore telesurgery visualization, piloting 360° endoscopic rigs for remote mentoring—an emerging yet unquantified TAM.

By Distribution Channel:

Online marketplaces dominateE-commerce captured 61.25% share in 2025, catalyzed by livestream demos and influencer affiliate models. Global shipping options allow niche gear to reach prosumers within 48 hours. Specialist brick-and-mortar retains relevance for high-ticket broadcast rigs requiring on-site lens calibration.

Manufacturers now integrate IoT telemetry into packaging, allowing dropship tracking and automated firmware activation post-delivery. As online storefronts refine virtual try-before-buy AR widgets, conversion lifts boost the 360° camera market. Strategic partnerships with global 3PLs mitigate customs-related downtime, sustaining double-digit growth for the online channel.

Geography Analysis

APAC 360-Degree Camera Market

Asia Pacific led the 360° camera market with a 41.50% share in 2025 and is forecast to grow at 18.74% CAGR. Chinese OEM clusters around Shenzhen integrate optics, ASICs, and casing under one roof, slashing lead times and enabling agile SKU pivots. Domestic players dominate local e-commerce festivals, then leverage scale to undercut competitors abroad, creating a virtuous production-volume loop. Regional 5G penetration and youth-skewing content consumption fuel prosumer upgrades, further enlarging addressable demand.

North America 360-Degree Camera Market

North America remains the largest individual national bloc by value, underpinned by autonomous vehicle pilots, Hollywood XR studios, and a risk-centric fleet insurance ecosystem. Regulatory momentum in states such as California mandates multi-sensor redundancy, embedding 360° cameras in perception stacks. The entertainment sector’s premium for real-time volumetric capture fortifies pricing power, while defense contracts supply downside protection during consumer-market fluctuations.

Europe 360-Degree Camera Market

Europe delivers steady adoption anchored in luxury real-estate virtual tours and industrial automation. GDPR compliance pressures have spawned privacy-by-design camera lines that auto-blur faces in public spaces, giving regional manufacturers a differentiation wedge. Cross-border live-production workflows—London galleries streaming Milan fashion catwalks—require interoperable stitching solutions; until standards mature, integrators bundle proprietary toolchains as value-added services.

Competitive Landscape

Moderate concentration defines the 360° camera market. Insta360’s 67.2% share in consumer panoramic units reflects first-mover advantage and a full-stack approach spanning optics, firmware, and SaaS editing. The firm’s June 2025 IPO raised fresh capital to scale R&D and to buffer legal costs tied to outstanding USITC patent investigations. DJI’s rumored Osmo 360 entry threatens price compression, prompting incumbents to accelerate feature cycles.

Patent litigation emerges as a strategic lever. GoPro’s Section 337 complaint seeks exclusion orders against Insta360 imports, aiming to slow a rival’s US momentum. Simultaneously, Meta secures foundational patents on virtual-camera abstraction layers that could evolve into platform-licensing plays, mirroring GPU IP models. Ricoh targets industrial niches with the THETA A1, bundling SaaS twin-creation tools to lock in enterprise clients.

Channel power shifts as Amazon Business and Alibaba International Station consolidate B2B ordering. Smaller brands differentiate via open-source firmware and repairability pledges aligned with EU Right-to-Repair directives. Semiconductor constraints through 2027 incentivize OEM-foundry partnerships; firms with pre-allotted wafer starts at TSMC gain delivery reliability and bargaining leverage over late-comers.

360-Degree Camera Industry Leaders

Insta360 (Arashi Vision Inc)

GoPro, Inc.

SZ DJI Technology Co., Ltd.

Panasonic Holdings Corporation

Canon Inc.

- *Disclaimer: Major Players sorted in no particular order

360-Degree Camera Market Companies Covered in this Report

- Insta360 (Arashi Vision Inc.)

- GoPro Inc.

- Samsung Electronics Co. Ltd.

- Sony Group Corp.

- Ricoh Co. Ltd.

- SZ DJI Technology Co. Ltd.

- Panasonic Holdings Corp.

- Nikon Corp.

- Canon Inc.

- LG Electronics Inc.

- Kandao Tech.

- Kodak Pixpro (JK Imaging)

- Immervision

- Panono (Professional360 GmbH)

- FeiyuTech

- Garmin Ltd.

- Rylo Inc. (Apple Vision Team)

- Xiaomi Corp.

- Wodsee Electronics Ltd.

- Hikvision

- FIMI Technology Ltd

Recent Industry Developments in 360-Degree Camera Market

- June 2025: Insta360 completed its IPO at a USD 9.8 billion valuation, earmarking proceeds for AI-driven editing software and automotive-grade sensor R&D.

- March 2025: Ricoh launched the RICOH360 THETA A1, extending its rugged lineup into extreme-environment inspection; the move positions Ricoh to secure energy-sector contracts requiring IP67 housings.

- March 2025: GoPro outlined a turnaround plan centered on the MAX 2 360° line, targeting 5-10% of revenue; the strategy pivots from low-margin action cams toward SaaS-bundled immersive capture.

- March 2025: Elbit Systems reported USD 1.9 billion Q1 sales, attributing backlog growth partly to VR training modules that integrate 360° cameras, signaling defense-sector stickiness.

Global 360-Degree Camera Market Report Scope

A 360 camera (omnidirectional camera) has a 360-degree field of view to capture around the sphere. These cameras are essential for covering expansive visual fields, such as in panoramic shots. With the increasing importance of virtual and augmented reality (AR/VR) in video games and interactive entertainment, the demand for 360 cameras has surged. The study tracks the revenue from selling such cameras in several end-user industries. It also tracks underlying growth trends and macroeconomic trends impacting the market.

The 360-degree camera market is segmented by connectivity type (wired and wireless), resolution (high-definition (HD), and ultra-high-definition (UHD)), end-user industry (media and entertainment, consumer, military and defense, travel and tourism, automotive, commercial, and healthcare), and geography (North America, Europe, Asia, Australia and New Zealand, Latin America, and Middle East and Africa). The market sizes and forecasts for all the above segments are provided in value (USD).

Segmentation Overview

| Wired |

| Wireless |

| Single-Lens Pocket Cameras |

| Multi-Lens Professional Rigs |

| In-Vehicle 360- Dash-Cams |

| High-Definition (less than or equal to1080p) |

| Ultra-HD 4K |

| Ultra-HD 8K and Above |

| Consumer |

| Media and Entertainment Production |

| Automotive (Surround-View and AD AS) |

| Defence and Security |

| Commercial Surveillance and Retail |

| Healthcare and Tele-Surgery |

| Travel, Tourism and Hospitality |

| Industrial and Robotics Inspection |

| Other End-user |

| Online Marketplaces |

| Offline / Specialist Retail |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Connectivity Type | Wired | ||

| Wireless | |||

| By Product Type | Single-Lens Pocket Cameras | ||

| Multi-Lens Professional Rigs | |||

| In-Vehicle 360- Dash-Cams | |||

| By Resolution | High-Definition (less than or equal to1080p) | ||

| Ultra-HD 4K | |||

| Ultra-HD 8K and Above | |||

| By End-User | Consumer | ||

| Media and Entertainment Production | |||

| Automotive (Surround-View and AD AS) | |||

| Defence and Security | |||

| Commercial Surveillance and Retail | |||

| Healthcare and Tele-Surgery | |||

| Travel, Tourism and Hospitality | |||

| Industrial and Robotics Inspection | |||

| Other End-user | |||

| By Distribution Channel | Online Marketplaces | ||

| Offline / Specialist Retail | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the 360° camera market?

The market stands at USD 2.64 billion in 2026 with a projected value of USD 5.98 billion by 2031.

Which segment is growing fastest within the 360° camera market?

Automotive applications lead with a 19.01% CAGR as autonomous-vehicle and fleet-insurance mandates converge.

Why are wireless 360° cameras gaining traction over wired models?

Wireless designs simplify installation in vehicles, drones, and industrial robots while benefiting from 5G and Wi-Fi 6 bandwidth.

How do privacy regulations impact 360° camera deployments in Europe?

GDPR enforcement introduces fines for public-space recordings lacking lawful basis, prompting vendors to embed on-device anonymization.

Page last updated on: