Europe Cylinder Lock Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 0.65 Billion |

| Market Size (2030) | USD 0.81 Billion |

| Growth Rate (2025 - 2030) | 4.47% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Cylinder Lock Market Analysis by Mordor Intelligence

The Europe cylinder lock market size stands at USD 650 million in 2025 and is projected to reach USD 810 million by 2030, reflecting a 4.47% CAGR that underscores the sector’s steady pivot from purely mechanical hardware to smart-enabled security ecosystems. Robust retrofit demand in the continent’s aging housing stock anchors volumes, while the recovery of multi-family construction and the enforcement of updated EU Construction Products Regulation (CPR) requirements add fresh growth momentum. Price-sensitive homeowners continue to favor proven mechanical pin-tumbler designs, but higher-income users increasingly adopt electronic cylinders for remote credential management, especially in Germany, the Netherlands, and Nordic markets. Insurers’ growing preference for EN 1303 and TS007-certified cylinders drives premiumization, and social-media-driven anti-snap campaigns further accelerate replacement cycles in the residential segment. On the cost side, copper and zinc volatility challenge mechanical platforms, nudging suppliers toward electronic and hybrid designs with lower metal content.

Key Report Takeaways

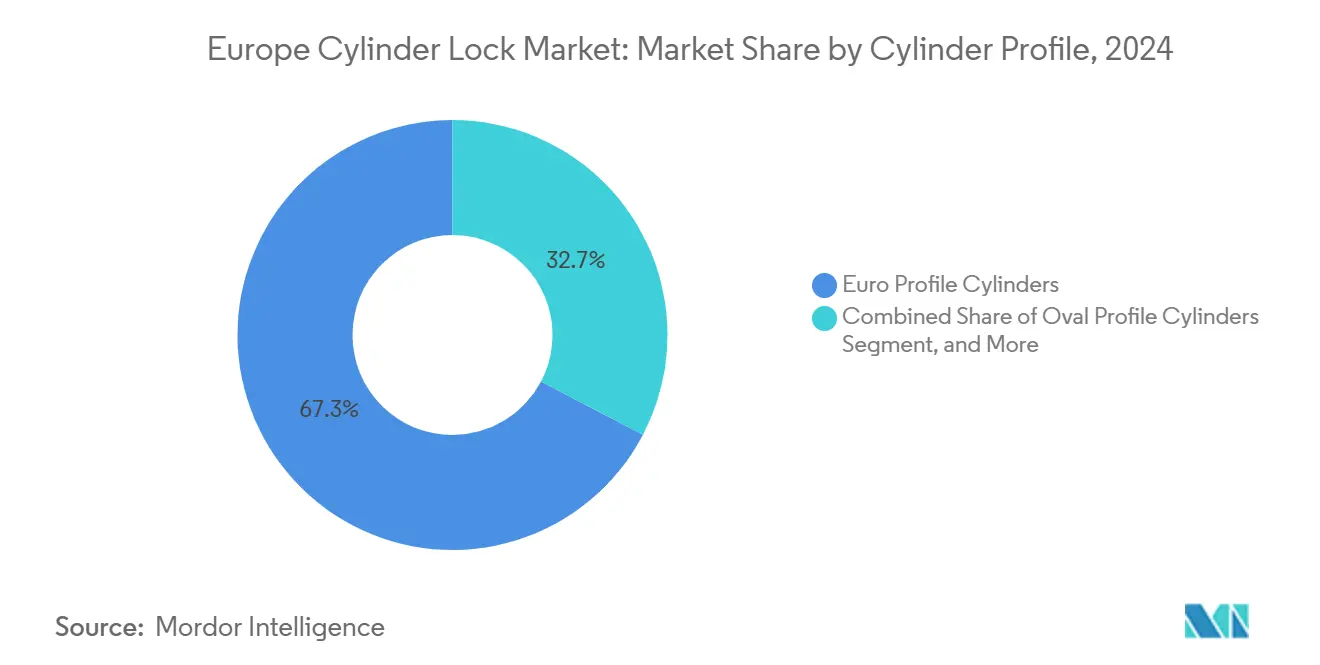

- By cylinder profile, Euro profile cylinders led with 67.32% of Europe cylinder lock market share in 2024, while smart electronic cylinders are forecast to expand at a 4.47% CAGR through 2030.

- By operation mechanism, mechanical pin-tumbler systems held 69.21% of the Europe cylinder lock market size in 2024; electronic RFID/Bluetooth variants are set to grow at a 4.47% CAGR to 2030.

- By end-user, residential captured 76.48% revenue share in 2024, but commercial applications are projected to post a 4.47% CAGR to 2030.

- By security grade, standard products accounted for 54.32% share of the Europe cylinder lock market size in 2024; premium high-assurance solutions will progress at a 4.47% CAGR to 2030.

- By geography, Germany commanded a 21.76% share in 2024, whereas Poland is anticipated to register the fastest 4.64% CAGR over the forecast period.

Europe Cylinder Lock Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residential renovation and security-upgrade boom | +1.2% | Germany, France, UK | Medium term (2-4 years) |

| Pan-European multi-family construction recovery | +0.8% | Poland, Netherlands, Spain | Long term (≥ 4 years) |

| Compliance with EN 1303 / TS007 insurance standards | +1.0% | UK, Germany, Netherlands | Short term (≤ 2 years) |

| Smart-home and IoT retrofit adoption | +0.9% | Germany, Netherlands, Nordics | Medium term (2-4 years) |

| Social-media-fueled anti-snap awareness | +0.4% | UK, Ireland, Netherlands | Short term (≤ 2 years) |

| EU CPR recyclability disclosure push | +0.2% | EU-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Residential Renovation and Security-Upgrade Boom

Replacement demand remains the backbone of the Europe cylinder lock market as homeowners prioritize essential safety improvements over discretionary remodeling. German renovation outlays stayed positive in 2024 even as new-build activity retreated, signaling structural resilience. [1]German Construction Industry Association, “Construction Market Outlook 2025,” bauindustrie.de Insurance discounts of 5–10% for TS007-certified cylinders further incentivize upgrades, creating a direct monetary benefit for adopting premium hardware. Many households now view locks as a value-preserving asset instead of a maintenance expense, which fosters demand for high-assurance models. The shift also widens the revenue mix toward aftermarket channels with higher margins for service-oriented installers. Consequently, manufacturers that bundle certified products with rapid locksmith support are positioned to capture a disproportionate share of this renovation-led cycle.

Pan-European Multi-Family Construction Recovery

Institutionally financed apartment projects are outperforming single-family starts, particularly in Poland where EU structural funds back large social housing pipelines. Each complex specifies hundreds of identical cylinders, creating volume leverage and lowering unit procurement costs. Timber-frame multifamily builds are spreading in the Netherlands and the Baltics, requiring special fire-rated Euro profiles that few low-cost importers can supply at scale. Suppliers with EN 1634-1 and EN 13501-2 certifications gain preferred-vendor status, reinforcing brand stickiness among general contractors. As project backlogs stretch past 2028, this construction rebound guarantees steady baseline demand even if DIY renovation spending slows.

Compliance with EN 1303 / TS007 Insurance Standards

Insurers increasingly embed EN 1303 Grade 6 or TS007 3-star criteria into commercial property policies, transforming voluntary upgrades into mandatory compliance costs. UK underwriters routinely refuse coverage for new retail sites that lack certified anti-snap cylinders. Building code authorities in Germany and the Netherlands have started referencing these same standards, forcing architects to specify compliant hardware at the design stage to avoid later retrofits. Manufacturers with full test reports from ift Rosenheim and BRE Group can command a 15–20% price premium, yet still deliver a net cost saving to end users through lower annual insurance fees. This standards-driven cycle rewards innovation in bump-resistance, drill-proof cores and modular key control platforms.

Smart-Home and IoT Retrofit Adoption

Matter- and Thread-compatible cylinders make it possible to upgrade legacy doors without replacing mortises or strike plates, a key advantage in Europe’s mature housing stock. Early adopters in the Netherlands and Nordic countries report quicker vacancy turnover in rental units equipped with smartphone entry, highlighting a revenue upside for property managers. German makers now bundle ultra-wideband proximity unlock with mechanical fail-safe overrides so that electronic convenience does not sacrifice physical resilience. [2]iLOQ, “Smart Locking Solutions,” iloq.com Software-defined features like guest access codes and audit trails create recurring subscription streams that decouple revenue from one-off hardware sales. Over the medium term, IoT penetration will underpin the Europe cylinder lock market’s transition toward service-centric business models that dampen exposure to raw-material swings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price pressure from low-cost Asian imports | -0.6% | EU-wide value segment | Short term (≤ 2 years) |

| Cyber-security and data-privacy concerns | -0.3% | Germany, France | Medium term (2-4 years) |

| Copper and zinc price volatility | -0.4% | Manufacturing hubs EU-wide | Short term (≤ 2 years) |

| Skilled locksmith labor shortage | -0.2% | Germany, UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Pressure from Low-Cost Asian Imports

Value-tier residential cylinders face acute price competition from importers that replicate Euro-profile dimensions at a fraction of local production cost. Home-center buyers in Southern Europe often select the lowest-priced SKUs, squeezing margins for domestic manufacturers already burdened by higher energy costs. Yet compliance hurdles partly shield premium suppliers: every imported unit still requires EN 1303 testing and CE marking, adding 8–10 weeks of lead time and thousands of euros in certification fees. Vendors with localized assembly can undercut those shipping finished goods by posting shorter delivery windows and customized keying services. The net impact trims topline growth in the low-end segment but simultaneously reinforces migration toward high-assurance categories where importers struggle to pass rigorous test cycles.

Copper and Zinc Price Volatility

Metal prices climbed 15–20% during 2024, inflating bill-of-materials for brass cores and zinc die-cast housings. [3]London Metal Exchange, “Copper and Zinc Price Data,” lme.com Makers bound by annual OEM supply contracts absorbed most of the spike, eroding gross profit until catalog repricing took effect. Exposure remains highest for pure mechanical portfolios, whereas electronic cylinders rely more on PCBs and plastics. To hedge, several firms shifted to aluminum-alloy plugs in noncritical areas, cutting brass mass by up to 30% without compromising strength. Others introduced service kits that refurbish cores instead of replacing entire cylinders, lowering metal consumption and stabilizing margins. Persistent volatility continues to pressure the Europe cylinder lock market, but it also accelerates adoption of alternative materials and hybrid electronic designs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cylinder Profile: Euro Standard Drives Market Consolidation

Euro profile cylinders accounted for 67.32% of the Europe cylinder lock market size in 2024 and will remain the default specification across new construction and renovation projects. The modular nature of Euro dimensions lets wholesalers hold fewer SKUs while covering multiple door types, which improves inventory turns and cuts logistics costs. Manufacturers leverage this scale to reinvest in anti-pick technologies and smart inserts, further entrenching the standard. Smart electronic Euro cylinders are tracking a 4.47% CAGR through 2030 thanks to Bluetooth adoption in high-density apartment retrofits.

Round and oval profiles collectively occupy a shrinking share as heritage building refurbishments complete and new structures gravitate to standardized hardware. Nonetheless, niche demand endures in the UK for oval replacements and in Sweden for traditional round mortises. Suppliers that maintain small-batch tooling for these shapes can capture above-average margins because competition is thinner, albeit on low volumes. Over the forecast horizon, consolidation around Euro profiles will simplify certification pipelines and shorten product-development cycles, reinforcing network effects that lift the Europe cylinder lock market.

By Operation Mechanism: Electronic Systems Challenge Mechanical Dominance

Mechanical pin-tumbler cores commanded 69.21% of the Europe cylinder lock market share in 2024, favored for low cost, locksmith familiarity and proven durability. Even so, their share is projected to slip as electronics gain credibility for audit trails and remote unlock features. Electronic RFID and Bluetooth models mirror the overall market’s 4.47% CAGR yet start from a smaller base, which makes them the prime engine of incremental revenue.

Mechatronic hybrids bridge the gap, combining mechanical keyways with battery-powered credential modules. Facility managers appreciate this redundancy because it maintains physical override during power outages. Adoption of cloud-based credential management also reduces key-control costs in coworking offices and student housing. As semiconductor shortages ease, cost parity between basic electronic cylinders and premium mechanical units could materialize before 2028, accelerating the digitization wave across the Europe cylinder lock market.

By End-User Sector: Commercial Growth Challenges Residential Leadership

Residential projects represented 76.48% of the Europe cylinder lock market size in 2024, reflecting the continent’s vast installed base of housing units and a steady churn in refurbishment cycles. Homeowner priorities center on affordability and quick installation, which sustains volume demand for Grade 5 mechanical Euro cylinders. Nevertheless, smart-home marketing is nudging higher-income households toward electronic retrofits that can be commissioned in under 15 minutes.

Commercial premises-offices, retail sites and mixed-use buildings—are anticipated to deliver a 4.47% CAGR up to 2030 as biometric readers and time-stamped audit logs become standard for access-controlled zones. Institutional buyers such as hospitals and airports adopt high-assurance cylinders integrated with centralized alarm panels, valuing compliance and traceability over unit price. Because commercial contracts often bundle maintenance, suppliers can secure recurring revenue streams under multiyear service agreements, thereby diversifying the Europe cylinder lock industry’s earnings profile.

By Security Grade: Premium Solutions Gain Market Traction

Standard Grade ≤5 products captured 54.32% of the Europe cylinder lock market size in 2024, largely due to bulk residential refurbishments and entry-level new builds. Insurer incentives and social-media awareness are moving consumers up the value curve, lifting demand for Grade 6–7 anti-snap cylinders. Manufacturers bundle patented cam designs and restricted key profiles that thwart illicit duplication, features now perceived as must-have in high-risk urban corridors.

Premium high-assurance models post the fastest 4.47% CAGR as banks, data centers and critical-infrastructure operators migrate to cylinders certified under VdS B or UL 437. These buyers also require end-to-end key tracking and cloud credential revocation, extending vendor relationships beyond hardware delivery. As cyber-physical threats converge, premium cylinders that pair hardened mechanical cores with encrypted electronics will underpin the Europe cylinder lock market’s margin expansion.

Geography Analysis

Germany retained 21.76% of Europe cylinder lock market share in 2024, supported by stringent insurance mandates and a mature distribution network that favors high-security products. Although residential new-build permits sagged during 2024, a EUR 3.5 billion social-housing allocation for 2025 channels procurement toward certified Grade 6 cylinders, partially offsetting volume softness in the private sector. German manufacturers also act as regional export hubs, shipping finished Euro cores to neighboring markets with shorter lead times than Asian competitors.

Poland is forecast to deliver the fastest 4.64% CAGR to 2030 as EU-funded multi-family projects and infrastructure upgrades stipulate EN 1303 compliance across thousands of units. Urban housing associations in Warsaw and Kraków negotiate framework contracts that bundle installation and five-year maintenance, creating predictable annuity streams for participating vendors. Rapid urbanization and improving disposable income further elevate the attach rate of electronic cylinders in new apartments.

Mature markets in France, the United Kingdom, Italy, Spain and the Netherlands exhibit divergent trajectories. French construction posted 12,700 company closures in 2024, yet renovation incentives stabilize cylinder demand, especially for anti-snap replacements in suburban dwellings. The UK enforces TS007 3-star standards in insurance underwriting, hastening the rollout of premium cores in both residential and small-business properties. Italy and Spain benefit from hotel modernization tied to tourism recovery, while the Netherlands leads electronic adoption due to high broadband penetration and strong DIY culture. Collectively, these dynamics support a balanced geographic spread that mitigates single-country risk for suppliers active in the Europe cylinder lock market.

Competitive Landscape

Competitive intensity is moderate, with the top five players estimated to control roughly 60% of total revenue through extensive patent portfolios and pan-European distribution. ASSA ABLOY has deepened its smart-lock bench by acquiring 3millID and Third Millennium for USD 21 million in January 2025, securing digital-identity capabilities that complement its mechanical heritage. Dormakaba’s purchases of Van den Berg and TANlock extend its footprint in Benelux and Germany while adding in-house expertise in electronic cylinder firmware, which shortens time to market for Thread-compatible models.

Allegion’s acquisition of Trimco Hardware expands its architectural hardware suite, enabling bundled bids that pair cylinders, closers and panic devices for commercial retrofits. Schneider Electric is a rising adjacent competitor: its Energy Management unit clocked 9.4% organic growth in H1 2024, with building access solutions cited as a key contributor. Smaller specialists such as iLOQ exploit SaaS-based credential platforms to undercut incumbents on total cost of ownership. Meanwhile, Chinese entrants target price-sensitive Grade 5 niches but face hurdles in passing European fire- and durability tests.

Strategic focus areas now center on cyber-hardened electronics, cloud credential ecosystems and life-cycle service contracts. Players investing in UWB proximity unlock, biometric keyways and post-quantum encryption stand to widen the technology gap. Those reliant on mature mechanical volumes must either climb the value chain or risk commoditization as the Europe cylinder lock industry transitions toward recurring revenue models.

Europe Cylinder Lock Industry Leaders

ASSA ABLOY AB

dormakaba Holding AG

Allegion plc

EVVA Sicherheitstechnologie GmbH

ABUS August Bremicker Söhne KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Allegion completed its acquisition of Trimco Hardware, deepening its architectural hardware portfolio for commercial door-security solutions.

- February 2025: The German federal budget allocated EUR 3.5 billion (USD 3.8 billion) for social-housing construction, triggering large-scale procurement of EN 1303-compliant cylinder locks.

- January 2025: ASSA ABLOY finalized the USD 21 million takeover of 3millID and Third Millennium, expanding its digital-identity and electronic-cylinder capabilities.

- January 2025: Updated EU Construction Products Regulation provisions entered into force, mandating environmental and recyclability disclosures for cylinder-lock manufacturers.

Europe Cylinder Lock Market Report Scope

| Euro Profile Cylinders |

| Oval Profile Cylinders |

| Round Profile Cylinders |

| Smart / Electronic Cylinders |

| Mechanical Pin-Tumbler |

| Mechatronic (Mech + Electronic) |

| Electronic Keypad / RFID / Bluetooth |

| Residential |

| Commercial |

| Institutional and Government |

| Industrial |

| Standard Security (≤Grade 5 EN1303) |

| High Security (Grade 6–7 EN1303 / TS007 3-Star) |

| Premium High-Assurance (VdS / BHMA / UL) |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Poland |

| Russia |

| Rest of Europe |

| By Cylinder Profile | Euro Profile Cylinders |

| Oval Profile Cylinders | |

| Round Profile Cylinders | |

| Smart / Electronic Cylinders | |

| By Operation Mechanism | Mechanical Pin-Tumbler |

| Mechatronic (Mech + Electronic) | |

| Electronic Keypad / RFID / Bluetooth | |

| By End-User Sector | Residential |

| Commercial | |

| Institutional and Government | |

| Industrial | |

| By Security Grade | Standard Security (≤Grade 5 EN1303) |

| High Security (Grade 6–7 EN1303 / TS007 3-Star) | |

| Premium High-Assurance (VdS / BHMA / UL) | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe cylinder lock market in 2025?

The Europe cylinder lock market size is USD 650 million in 2025 and is projected to reach USD 810 million by 2030.

Which cylinder profile is most popular across Europe?

Euro profile cylinders hold 67.32% market share due to standardized dimensions and interchangeable installation.

What growth rate is expected for smart electronic cylinders?

Smart electronic cylinders are forecast to advance at a 4.47% CAGR through 2030, outpacing mechanical units.

Why are insurers driving demand for premium cylinders?

Insurers increasingly require EN 1303 or TS007-certified hardware and offer premium discounts of up to 10% for compliant installations.

Which European country is expanding fastest in cylinder-lock adoption?

Poland leads growth with a 4.64% CAGR, backed by EU-funded social housing and infrastructure projects.

How are raw-material costs influencing product design?

Volatile copper and zinc prices propel manufacturers to adopt alternative alloys and electronic cores that rely less on metals.

Page last updated on: