Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

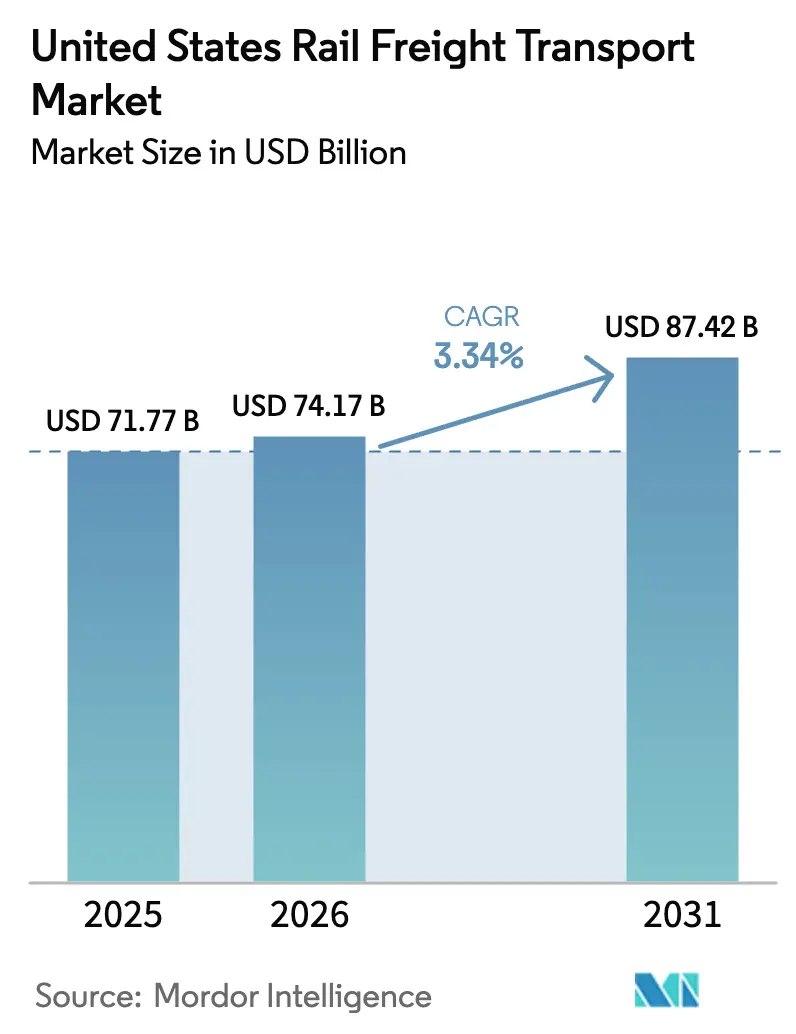

| Base Year Market Size (2025) | USD 71.77 Billion |

| Market Size (2026) | USD 74.17 Billion |

| Market Size (2031) | USD 87.42 Billion |

| Growth Rate (2026 - 2031) | 3.34% CAGR |

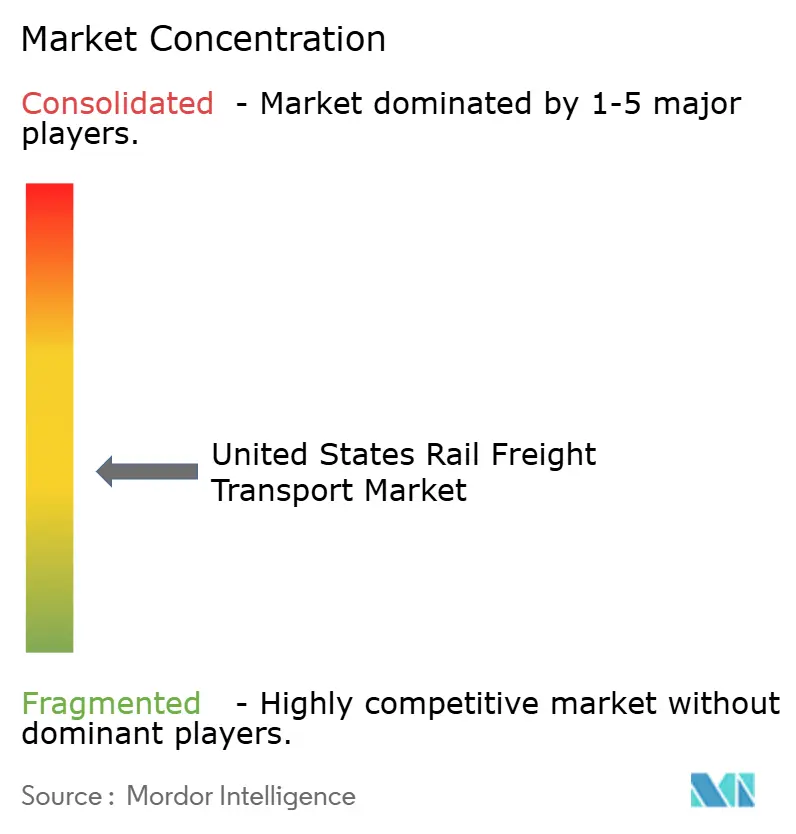

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Rail Freight Transport Market Analysis by Mordor Intelligence

The United States Rail Freight Transport Market size market size in 2026 is estimated at USD 74.17 billion, growing from 2025 value of USD 71.77 billion with 2031 projections showing USD 87.42 billion, growing at 3.34% CAGR over 2026-2031.

Intermodal traffic remains the engine of top-line expansion as retailers strengthen e-commerce supply chains and shift more import boxes from coast-side terminals onto inland trains. Carriers are funding larger intermodal ramps, siding extensions, and double-tracking projects that ease bottlenecks and add turn-time flexibility, helping them protect pricing in lanes where trucking still offers speed advantages. Bulk flows are changing too: grain has stepped up to fill part of the coal shortfall, while Gulf Coast petrochemical output is nudging tank-car demand higher and encouraging railroads to commit capital to hazmat-certified equipment. Persistent federal investment especially through Infrastructure Investment and Jobs Act grants lowers the cost of modernisation and supports advanced train-handling technologies that can lift asset productivity even as headcount stabilises. Competitive focus is shifting from pure cost control to service dependability; operators that blend Precision Scheduled Railroading discipline with customer-facing visibility tools appear better positioned to win discretionary freight over the next five years.

Key Report Takeaways

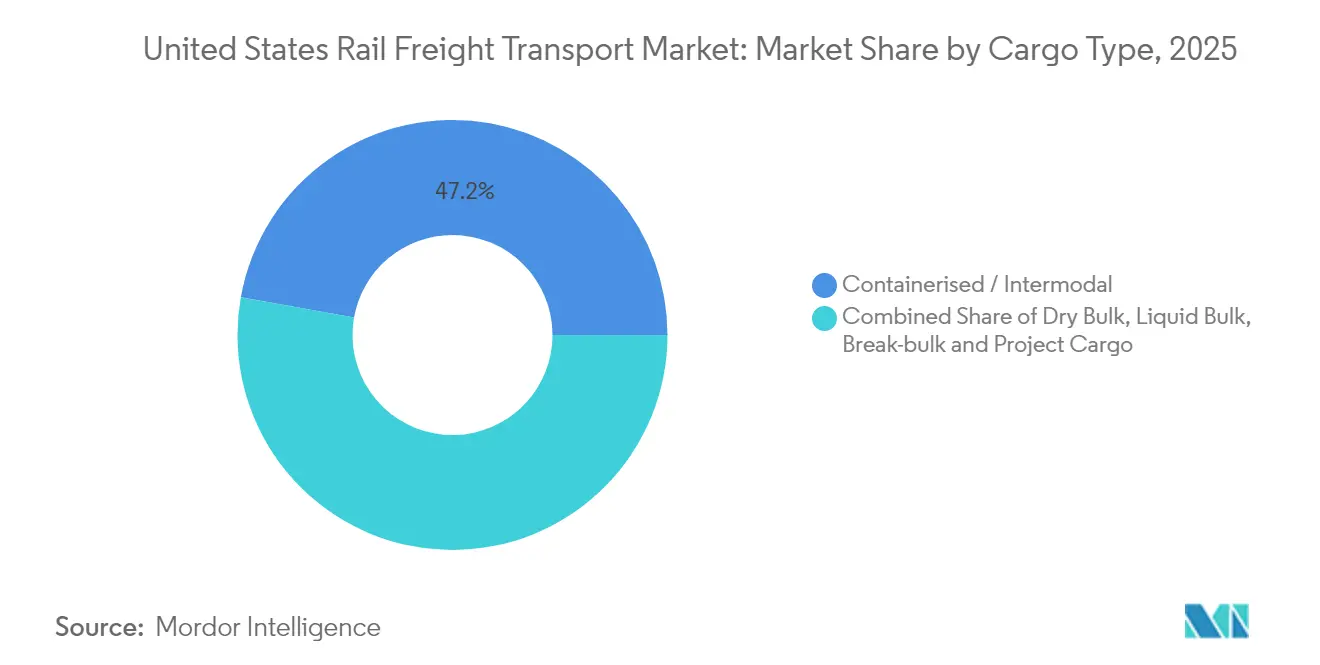

- By cargo type, Intermodal captured 47.20 % of the United States Rail Freight Transport market share in 2025, while break-bulk and project cargo within the United States Rail Freight Transport market size is expected to expand at a 6.82 % CAGR through 2031.

- By service type, core Transportation services generated 88.40 % of the United States Rail Freight Transport market share in 2025, whereas the United States Rail Freight Transport market size tied to Allied services is forecast to grow at a 7.02 % CAGR to 2031.

- By end-user industry, Mining & Minerals held 21.60 % of the United States Rail Freight Transport market share in 2025, and the United States Rail Freight Transport market size linked to Retail & FMCG is projected to advance at an 7.88 % CAGR over the same horizon.

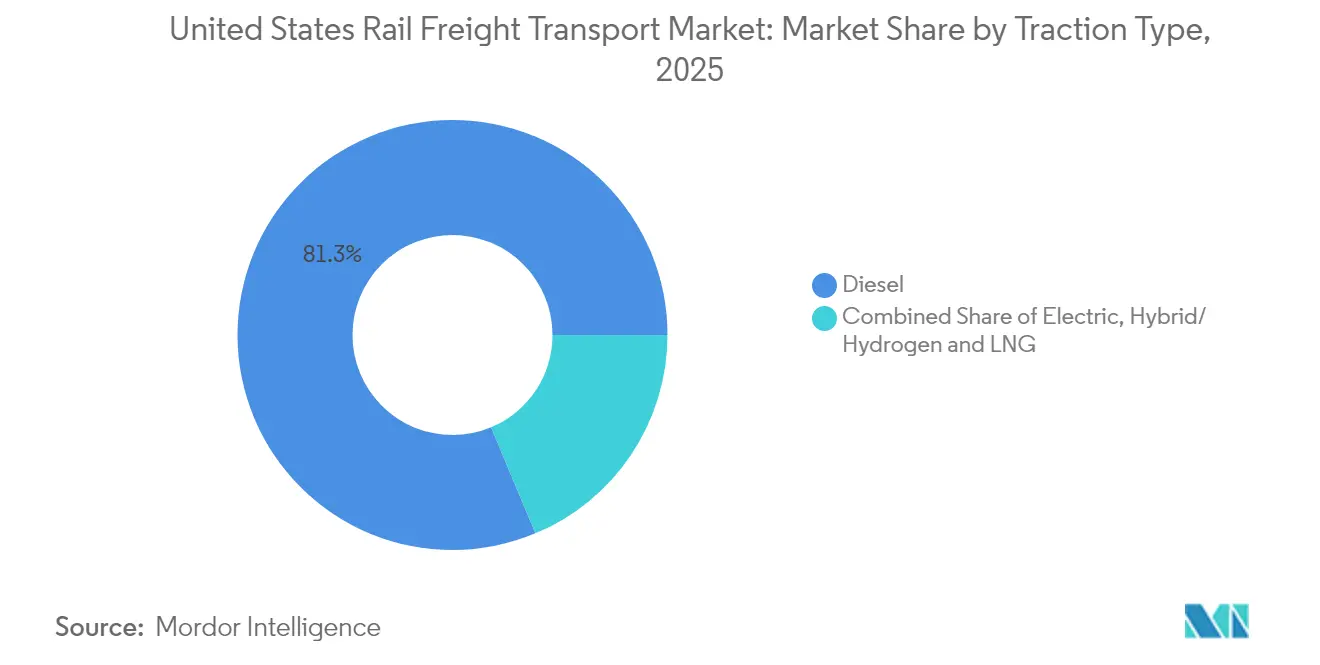

- By traction type, Diesel locomotives accounted for 81.30 % of the United States Rail Freight Transport market share in 2025, yet the United States Rail Freight Transport market size for Hybrid/Hydrogen & LNG locomotion is set to rise at a 10.05 % CAGR through 2031.

- By destination, Domestic movements represented 80.70 % of the United States Rail Freight Transport market share in 2025, while the United States Rail Freight Transport market size for cross-border traffic is anticipated to climb at a 8.25 % CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Rail Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in E-commerce-led Intermodal Volumes | +0.8% | West Coast, Southwest, inland hubs | Medium term (3-4 yrs) |

| Gulf Coast Petrochemical Boom | +0.4% | Texas and Louisiana Gulf Coast | Medium term (3-4 yrs) |

| IIJA-Funded Corridor Upgrades | +0.6% | Nationwide; emphasis on Northeast Corridor and key freight routes | Long term (≥ 5 yrs) |

| Cross-border Grain Flows from Canada | +0.3% | Northern border states, Upper Midwest | Short term (≤ 2 yrs) |

| Resurgence of Domestic Coal under High Gas Prices | +0.2% | Powder River Basin, Appalachia | Short term (≤ 2 yrs) |

| Precision Scheduled Railroading Cost Efficiencies | +0.5% | National | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

Surge in E-commerce-Led Intermodal Volumes

Containerised freight remains the United States rail freight transport market’s growth engine, with total intermodal units up 8.5 % year over year in 2024. Class I carriers have accelerated pop-up ramp initiatives and inland-port developments to capture e-commerce imports flowing through West Coast and Southwest gateways. Because omnichannel retailers schedule inventory replenishment in daily windows, on-time performance is becoming as vital as price. A clear outgrowth is the placement of new distribution centres on rail-served sites in secondary urban rings, which lengthens the dray leg and tilts the cost equation toward rail line-haul.

Gulf Coast Petrochemical Boom Boosting Tank-Car Traffic

Petrochemical complexes along the Texas-Louisiana coastline recorded a 4.2 % production increase in 2024, and rail shipments of chemicals rose roughly 3.5 % year over year, outpacing overall freight growth. ExxonMobil’s USD 2 billion Baytown expansion alone is raising specialty-chemical output by 40 %, driving additional inbound feedstock and outbound product moves. The planned deep-water Sea Port Oil Terminal at Freeport, Texas, approved by the Maritime Administration, will further reshape tank-car corridors by adding capacity to load 2 million barrels of crude daily. Growing traffic density is prompting carriers to invest in double-tracking and yard expansions to avoid pinch points.

Cross-Border Grain Flows from Canada to the United States

Canadian National’s grain and fertiliser revenue climbed 9 % in Q3 2024 thanks to a robust U.S. harvest. Rail grain movements from Canada to the U.S. exceeded 6.9 million metric tonnes that year, reinforcing rail’s role in cross-border trade. The single-line network created by Canadian Pacific Kansas City (CPKC) is poised to add further capacity, with a winter contingency plan targeting 685 000 tonnes weekly when Thunder Bay is ice-free [1]Canadian Pacific Kansas City, “Strengthening Resiliency: 2024–2025 Winter Contingency Report,” Canadian Pacific Kansas City, cpkcr.com. Increased throughput tightens supply-chain integration between Prairie grain elevators and Midwest processors, boosting car utilisation for carriers.

Resurgence of Domestic Coal under High Gas Prices

Temporary spikes in natural-gas prices drove a 3.2 % winter-over-winter increase in coal burn at power plants, and about 70 % of that coal moves by rail [2]U.S. Energy Information Administration, “U.S. coal shipments increased slightly in 2022 as power plants replenished stockpiles,” U.S. Energy Information Administration, eia.gov. Railroads chose to keep capacity active in the Powder River Basin, valuing optionality over immediate cost cuts. The upturn supports network economics because coal routes often subsidise mixed-freight lanes, although operators remain cautious about investing new capital in declining corridors. This behaviour suggests that cash-flow resilience, rather than long-term growth, motivates carriers to maintain coal capability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural Decline in Coal-Fired Power | -0.7% | Coal-producing regions | Long term (≥ 5 yrs) |

| Service Reliability Issues | -0.6% | Congested corridors nationwide | Medium term (3-4 yrs) |

| Labor Contract Disputes & Wage Inflation | -0.4% | National | Medium term (3-4 yrs) |

| Tightened Hazmat Regulations on Flammable Liquids | -0.3% | Gulf Coast, major energy corridors | Medium to long term (3-5 yrs) |

| Source: Mordor Intelligence | |||

Structural Decline in U.S. Coal-Fired Power

Coal shipments fell 13.6 % in 2024, reaching their lowest volume since 1988, and the Energy Information Administration sees coal’s share of generation sliding to 15 % by 2030. Class I carriers manage the downturn by allowing specialised coal cars to retire through attrition while redirecting capital toward diversified bulk and intermodal projects. Because coal routes historically subsidised network maintenance, their decline requires rate adjustments across other commodities, subtly affecting overall pricing power.

Service Reliability Issues Driving Mode Shift to Trucking

Journal of Commerce surveys show that many rail customers remained dissatisfied with H2 2024 performance, citing missed pick-ups and erratic transit times. Shippers warned regulators that weak rail service threatens the broader economy, prompting congressional hearings and calls for Surface Transportation Board action. Some cargo has migrated to trucking despite higher freight rates, underscoring the premium shippers place on dependability. Carriers have begun posting real-time dashboards and rehiring crews to stabilise key terminals, indicating a more proactive stance on service recovery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Cargo Type: Intermodal Leads Growth Amid Evolving Commodity Mix

Intermodal holds a 47.20 % market share of the United States rail freight transport market size in 2025, reflecting the segment’s dominance as e-commerce and global sourcing reshape supply chains. Volume growth of 8.5 % in 2024 confirms that container traffic remains the primary engine of car-load expansion. Terminal productivity, rather than mainline speed, is emerging as the constraint; BNSF and Union Pacific have therefore prioritised new ramp capacity in Chicago and Phoenix to keep stack-train velocity intact.

Dry bulk is the next-largest segment, yet coal’s 13.6 % decline has shifted its internal mix toward grains and aggregates. Grain carloads rose year over year, cushioning revenue loss from coal and highlighting the importance of agricultural flows reported by the Agricultural Marketing Service . Liquid bulk benefits from petrochemical output gains, while break-bulk and project cargo, though the smallest, show the fastest forecast CAGR at 6.82 % as renewable-energy components move by rail. The evolving commodity mix signals that railroads must maintain a flexible wagon fleet to manage diverse loading needs across cargo types.

Service Type: Allied Services Gain Momentum in Integrated Logistics

Transportation services account for roughly 88.40 % of 2025 market size, but allied services are forecast to grow at a 7.02 % CAGR through 2031. Growth in storage, transloading, and wagon maintenance reflects shippers’ demand for one-stop logistics solutions that reduce hand-offs. By bundling these services, carriers create stickier revenue streams and improve car utilisation, indirectly lifting margins.

BNSF’s Shortline Select partnership with Genesee & Wyoming demonstrates how main-line carriers leverage network reach to support smaller railroads and expand transload offerings. Railroads are also investing in predictive-maintenance software to cut repair cycle-time, freeing assets for higher-yield traffic. Together, these trends imply that allied services will outpace core haulage in revenue growth, enhancing overall industry resilience.

End-user Industry: Retail & FMCG Disrupts Traditional Dominance

Mining & Minerals commands a 21.60 % market share of 2025 rail freight volumes, anchored by residual coal traffic and rising shipments of critical minerals. Agriculture & Food retains a significant slice, supported by grain unit-train configurations that deliver low cost per tonne. Notably, cross-border grain expansions have strengthened this segment’s outlook.

Retail & Fast-Moving Consumer Goods is forecast to post an 7.88 % CAGR through 2031, making it the fastest-growing end-user category. Oil, Gas & Chemicals is buoyed by Gulf Coast investments, while Manufacturing & Automotive shows corridor-specific variability linked to plant schedules. This diversified demand mosaic reduces cyclicality and supports steady capital spending across the rail network.

Traction Type: Hybrid/Hydrogen & LNG Accelerates Amid Decarbonization Push

Diesel traction maintains an 81.30 % market share, but Hybrid / Hydrogen & LNG is projected to grow at a 10.05 % CAGR between 2026 and 2031. CSX’s prototype hydrogen locomotive, developed with CPKC, showcases the industry’s move toward lower-emission motive power.

Union Pacific’s battery-electric hybrid demonstrator targets up to 80 % fuel-efficiency gains in yard service. Early results suggest that hybridisation will scale first in switching roles before moving to mainline assignments, potentially stimulating domestic battery and hydrogen supply chains.

Destination: International Cross-border Growth Outpaces Domestic

Domestic movements represent 80.70 % of 2025 market size, yet cross-border traffic is forecast to expand at a 8.25 % CAGR through 2031. The CPKC network provides the only single-line rail service connecting Canada, the United States, and Mexico, trimming transit times and border delays.

A joint CPKC-CSX corridor linking Mexico, Texas, and the Southeast will add optionality for exporters and tighten service schedules. Growth in refrigerated agricultural exports and automotive near-shoring supports sustained international volume gains, implying that carriers will continue investing in customs-compliant gateways and temperature-controlled equipment.

Competitive Landscape

Seven Class I railroads account for 94 % of industry freight revenue, reflecting a consolidated structure backed by extensive track mileage. Recent mergers, notably Canadian Pacific and Kansas City Southern’s formation of CPKC, demonstrate carriers’ intent to secure contiguous networks that reduce interchange hand-offs and maximise asset turns. Canadian National’s 2025 purchase of Iowa Northern Railway further highlights targeted regional acquisitions as a cost-efficient growth vehicle.

Competition increasingly revolves around service reliability and digital transparency rather than price alone. Railroads with robust customer portals that provide real-time tracing are winning discretionary freight, particularly in short-haul lanes where trucking remains a viable option. PSR-driven cost advantages endow incumbents with pricing power, yet any lapse in on-time performance can trigger rapid mode shifts, motivating carriers to reinvest in yards and crews.

Technological differentiation is a rising competitive lever. Operators equipping wagons with smart sensors for predictive maintenance report higher asset availability, which they market as a guarantee to shippers demanding tight delivery windows. Alternative traction pilots—hydrogen, battery electric, blended LNG—offer shippers measurable Scope 3 emissions reductions, potentially influencing modal choices for carbon-conscious cargo owners. Smaller regionals and short lines respond by specialising in first- and last-mile services that feed into Class I networks, creating a collaborative ecosystem where technology and service complement geography.

United States Rail Freight Transport Industry Leaders

Union Pacific Railroad

BNSF Railway

CSX Transportation

Norfolk Southern Railway

Canadian Pacific Kansas City

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BNSF unveiled a USD 3.8 billion capital plan for network maintenance and expansion, including a new Phoenix intermodal facility and land purchases for the Barstow International Gateway. The plan underscores confidence in long-term intermodal growth

- January 2025: Canadian National completed its acquisition of Iowa Northern Railway, adding 175 route miles and enhancing grain and renewable-fuel service in the Midwest.

- November 2024: Norfolk Southern launched a hybrid-locomotive program with Alstom through a federal CRISI grant. The initiative will convert two engines, cutting emissions 90 % and boosting pulling power 30 % compared with traditional diesel units.

- September 2024: BNSF introduced the Shortline Select program with Genesee & Wyoming’s AGR, offering joint marketing and operational support to improve service and expand transload capacity

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States rail freight transport market as the revenue earned by common-carrier railroads for hauling bulk, break-bulk, intermodal, and tank cargo over the national network; terminal handling, wagon leasing, and in-plant switching billed by third-party contractors are also counted because shippers pay for them as part of the rail move. Passenger, tourist, and metro rail services, as well as private captive spurs that never interchange, are outside this market's financial boundary.

Scope exclusions: rolling-stock manufacturing, passenger fares, and purely intrafacility industrial rail operations are excluded.

Segmentation Overview

- By Cargo Type

- Containerised / Intermodal

- Dry Bulk (Coal, Ores, Grains)

- Liquid Bulk (Crude, Chemicals)

- Break-bulk & Project Cargo

- By Service Type

- Transportation

- Services Allied to Transportation (Maintenance of Railcars and Rail Tracks, Switching of Cargo, and Storage)

- By End-user Industry

- Mining & Minerals

- Oil, Gas & Chemicals

- Agriculture & Food

- Manufacturing & Automotive

- Retail & FMCG

- Construction Materials & Others

- By Traction Type

- Diesel

- Electric

- Hybrid / Hydrogen & LNG

- By Destination

- Domestic

- International / Cross-border

Detailed Research Methodology and Data Validation

Desk Research

We built the base dataset from publicly available tier-1 sources such as the Surface Transportation Board Waybill Sample, Association of American Railroads ton-mile statistics, Bureau of Transportation Statistics revenue filings, Federal Railroad Administration grant records, and U.S. Energy Information Administration commodity flow tables. Company 10-Ks, investor decks, and trade-press loadings reports fleshed out quarterly shifts. Where deeper firm-level splits were required, analysts tapped D&B Hoovers and Dow Jones Factiva for segmented revenue clues. This list is illustrative; many additional open and paid references supported fact-checking and gap filling.

Primary Research

Mordor analysts interviewed Class I marketing managers, regional short-line executives, intermodal marketing associations, port drayage brokers, and bulk-commodity shippers across the Midwest, Gulf Coast, and Pacific gateways. These discussions clarified price escalators, equipment cycle times, and the realistic penetration of precision scheduled railroading, allowing us to reconcile secondary data with on-ground sentiment.

Market-Sizing & Forecasting

A top-down build starts with national ton-miles, average yield per ton-mile, and distance elasticities, which are then corroborated with bottom-up checks such as sampled average selling price times loaded units for key lanes. Variables fed into the model include e-commerce parcel imports, industrial production index, coal burn in power generation, Class I capital-expenditure ratios, diesel-to-alternative traction mix, and weekly intermodal container counts. A multivariate regression with ARIMA overlays projects each driver, after which scenario tests from primary interviews adjust for policy or fuel shocks. Gaps in bottom-up counts, common for grain shuttle volumes, are back-cast using USDA export certificates and STB tariff filings.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated anomaly flags, peer analyst cross-checks, and a senior sign-off. We revisit models annually, and interim refreshes trigger when quarterly revenues deviate by >=5% or new federal funding materially alters capacity.

Why Mordor's United States Rail Freight Transport Baseline Commands Reliability

Published numbers often diverge because firms pick different service buckets, revenue recognition points, and refresh cadences.

Key gap drivers include whether passenger or private in-plant moves are blended, how ancillary fees are mapped, and the frequency with which fuel-surcharge resets are rebased. Our work reports the service wallet actually paid by shippers, uses 2024 currency conversions, and is refreshed every twelve months, whereas some peers retain older exchange rates or forecast off global proxies.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 71.77 B (2025) | Mordor Intelligence | - |

| USD 19.6 B (2024) | Global Consultancy A | Counts freight alone within mixed passenger-freight filings, excludes terminal and switching fees |

| USD 77.6 B (2023) | Industry Association B | Combines shipper revenue and carrier fuel surcharges without inflation adjustment |

| USD 117.23 B (2024) | Regional Consultancy C | Bundles rail logistics services such as warehousing and last-mile drayage |

Taken together, the comparison shows that once common scope and currency filters are applied, Mordor's disciplined, annually refreshed baseline offers decision-makers the most transparent and repeatable view of the U.S. rail freight opportunity.

Key Questions Answered in the Report

What is the current United States rail freight transport market size?

The market size is USD 74.17 billion in 2026.

How fast is the market expected to grow through 2031?

It is forecast to expand at a 3.34 % CAGR from 2026 to 2031.

Which cargo type commands the largest market share?

Intermodal containers lead with a 47.20 % share of total rail freight volumes.

How will the Infrastructure Investment and Jobs Act affect rail freight?

IIJA grants are funding track upgrades, grade separations, and siding extensions that will increase capacity and enhance reliability across national corridors.

Which end-user industry is projected to grow fastest?

Retail & Fast-Moving Consumer Goods is expected to register the highest CAGR through 2030 due to e-commerce-driven demand.

What technologies are Class I railroads adopting to cut emissions?

Carriers are piloting hydrogen-fuel locomotives, battery-electric hybrids, and LNG-capable engines to reduce greenhouse-gas output and improve fuel efficiency.

Page last updated on: