Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

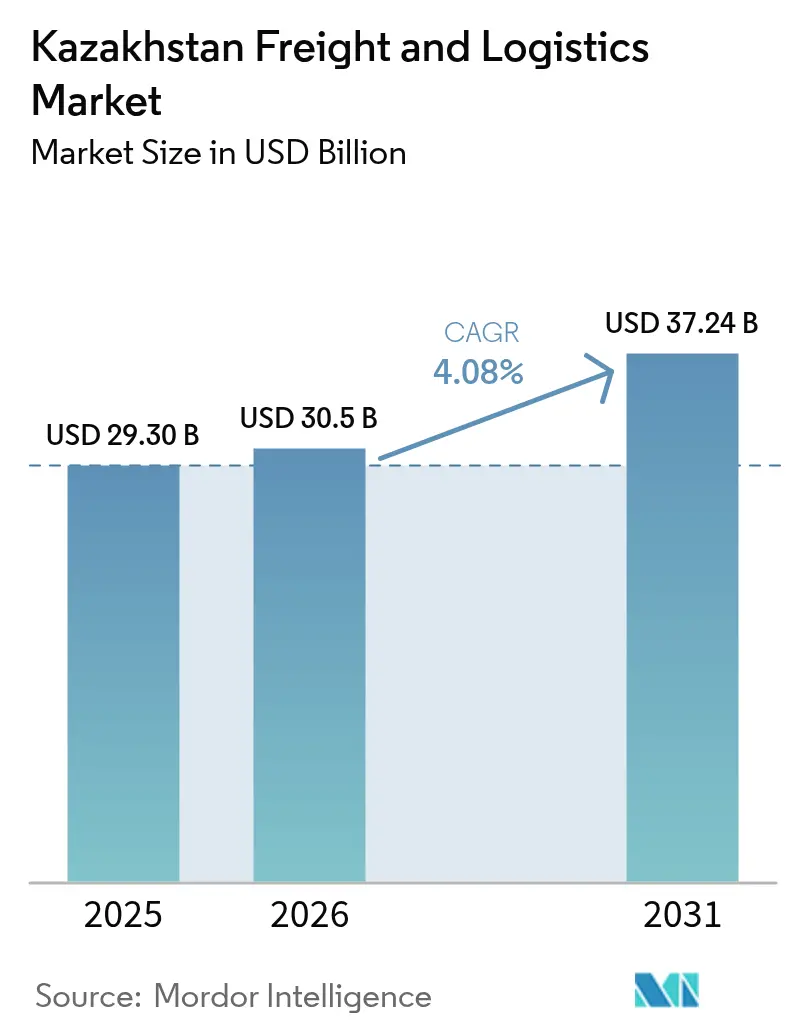

| Base Year Market Size (2025) | USD 29.30 Billion |

| Market Size (2026) | USD 30.5 Billion |

| Market Size (2031) | USD 37.24 Billion |

| Growth Rate (2026 - 2031) | 4.08% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kazakhstan Freight And Logistics Market Analysis by Mordor Intelligence

The Kazakhstan Freight And Logistics Market size was valued at USD 29.30 billion in 2025 and estimated to grow from USD 30.5 billion in 2026 to reach USD 37.24 billion by 2031, at a CAGR of 4.08% during the forecast period (2026-2031).

The growth trajectory is underpinned by Kazakhstan’s role in the Belt and Road Initiative, accelerating public–private infrastructure spending, and the steady diversification of export routes through the Trans-Caspian International Transport Route. Rising e-commerce volumes, free-zone incentives, and near-shoring by automotive OEMs further widen demand for multimodal services, while digital customs reforms compress dwell times at key borders. Capacity constraints at Aktau seaport and the Khorgos dry port create attractive investment openings for operators capable of scaling rail, road, and cold-chain assets. Meanwhile, volatile fuel prices and fragmented trucking fleets temper operating margins but accelerate the modal shift toward rail and pipeline options.

Key Report Takeaways

- By logistics function, freight transport led with 73.65% Kazakhstan freight and logistics market share in 2025, while Courier, Express, and Parcel (CEP) registered the fastest 4.32% CAGR through 2031.

- By CEP sub-segment, domestic parcels captured 66.60% of the Kazakhstan freight and logistics market size in 2025; international parcels are forecast to expand at a 4.45% CAGR to 2031.

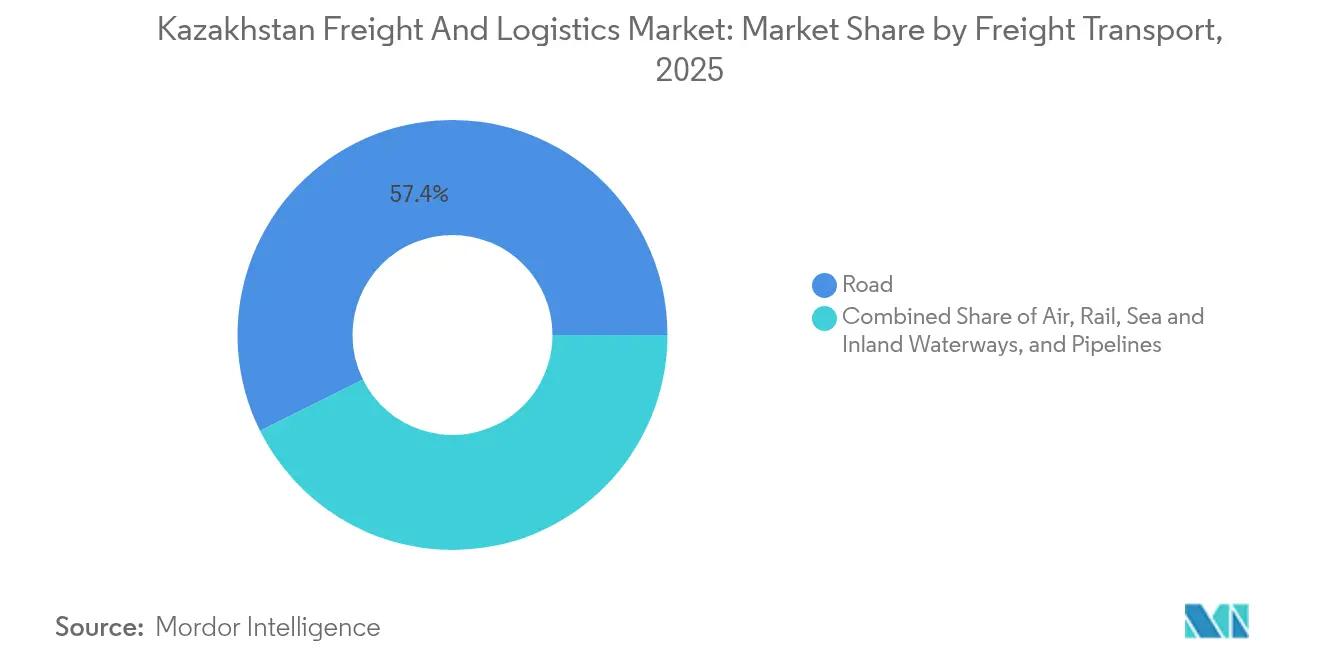

- By freight forwarding mode, sea and inland waterways commanded a 57.76% share of the Kazakhstan freight and logistics market size in 2025, whereas air forwarding is advancing at a 4.27% CAGR through 2031. By freight transport mode, road retained a 57.35% share in 2025, yet air freight is projected to post a 4.18% CAGR between 2026-2031.

- By warehousing type, non-temperature-controlled facilities held a 90.12% share in 2025; temperature-controlled space is set to grow at a 4.16% CAGR.

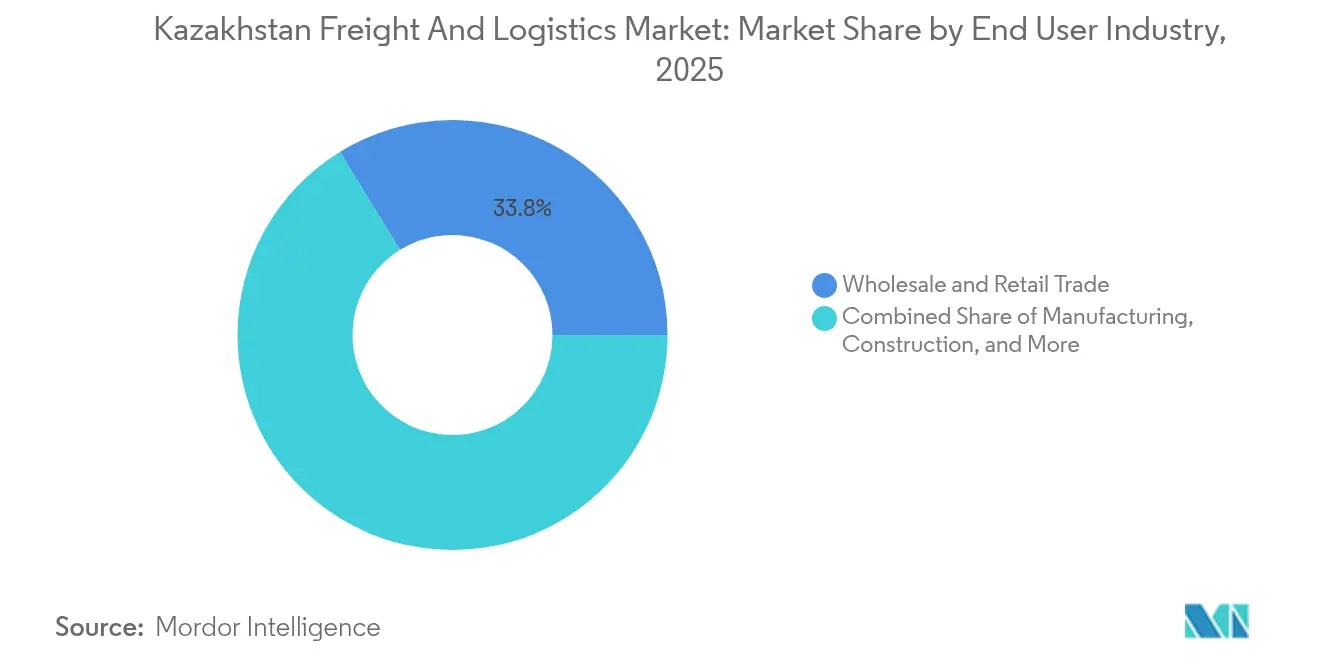

- By end user, Wholesale and Retail Trade accounted for 33.78% Kazakhstan freight and logistics market share in 2025, while Manufacturing is on track for a 4.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kazakhstan Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strategic Eurasian Transit Hub and Middle Corridor Expansion | +1.0% | Trans-Caspian corridor, Aktau & Kuryk ports, Khorgos dry port | Long term (≥ 4 years) |

| State-led Infrastructure Modernization Across Rail, Roads, and Dry Ports | +0.8% | National, focused on Almaty, Astana, and border regions | Medium term (2-4 years) |

| Growth in Industrial Production and Extractive Exports Requiring Bulk and Project Logistics | +0.7% | Western oil & gas basins, mining areas, industrial zones | Medium term (2-4 years) |

| Rising Domestic and Cross-Border E-commerce Stimulating CEP and Fulfillment Demand | +0.6% | National, Almaty & Astana urban centers | Short term (≤ 2 years) |

| Digitalization of Customs, Border, and Transport Documentation Processes | +0.4% | Border checkpoints with China, Uzbekistan, Turkmenistan | Short term (≤ 2 years) |

| Entry and Expansion of International Logistics Operators and 3PL Platforms | +0.3% | Major cities & strategic corridors, Khorgos, Aktau | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strategic Eurasian Transit Hub and Middle Corridor Expansion

Kazakhstan’s role as the land bridge of the Trans-Caspian International Transport Route reshapes regional trade lanes by shortening Asia-Europe transit times and reducing geopolitical risk away from northern corridors. Bilateral accords signed with Georgia in February 2025 target capacity coordination, underpinning long-range capital flows into port cranes, rail wagons, and digital tracking layers [1]“Kazakh, Georgian PMs Discuss Key Initiatives to Boost Bilateral Relations,” Astana Times, astanatimes.com.. While extensive broad-gauge rail mileage gives the country scale advantages, chokepoints at Aktau and Khorgos expose investment gaps that private 3PLs can monetize through integrated intermodal solutions. In the long run, the corridor elevates revenue streams beyond transit fees toward higher-margin consolidation, customs brokerage, and regional fulfillment services.

State-led Infrastructure Modernization Across Rail, Roads, and Dry Ports

The National Infrastructure Plan 2024-2029 funnels resources into 59 transport projects and anchors an unprecedented USD 4.2 billion locomotive framework plus the USD 405 million Wabtec order secured in October 2024 [2]“The Government Of Kazakhstan Has Approved The National Infrastructure Plan Until 2029,” Conventus Law, conventuslaw.com. Parallel rail projects, from Darbaza-Maktaaral to the Ayagoz-Tachen route, knit the network to Uzbekistan and a third China border gate, while AD Ports Group’s USD 775 million pledge lifts Aktau’s container throughput. High-capacity roads such as the Big Almaty Ring Road ease urban distribution friction. Each asset stimulates clustered demand for warehouses, cranes, telecom systems, and workforce reskilling, magnifying growth multipliers across the Kazakhstan freight and logistics market.

Growth in Industrial Production and Extractive Exports Requiring Bulk and Project Logistics

Oil, mining, and new-energy projects drive complex transport tasks, from heavy-lift rig modules to time-critical spare parts. CPC shipped 54.9 million tons of crude in 2024, and September 2025 saw KazMunayGas redirect volumes through the Baku-Tbilisi-Ceyhan line, diversifying haulage lanes [3]“Kazakhstan’s Oil Exports Uninterrupted Despite Caspian Pipeline Consortium Berth Suspensions,” The Times of Central Asia, timesca.com. Korean interest in East Kazakhstan lithium and nine renewable-energy builds totaling 455.5 MW commissioned in 2025, intensifies demand for project freight and specialized handling.

Rising Domestic and Cross-Border E-commerce Stimulating CEP and Fulfillment Demand

More than 300,000 e-commerce jobs and a significant number of Kaspi.kz orders routed via proprietary couriers showcase a nationwide shift toward integrated payment-logistics ecosystems [4]“Kazakhstan Sees Job Growth Driven by E-Commerce Boom,” Trend.az, trend.az. Government directives to scale Kazpost complement locker rollouts and rural service expansion, while single-window customs modules streamline B2C imports. Operators that combine fulfillment, brokerage, and last-mile data visibility capture the lion’s share of the fast-moving Kazakhstan freight and logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Border Transshipment, Gauge / Modal-break Inefficiencies at China-Europe Interfaces | -0.6% | Khorgos dry port, China-Kazakhstan border | Medium term (2-4 years) |

| Tariff, Regulatory, and Administrative Inefficiencies Raising Transit Costs and Dwell Times | -0.5% | Customs checkpoints nationwide | Short term (≤ 2 years) |

| Capacity Bottlenecks and Terminal Congestion along the Middle Corridor and Caspian Segment | -0.4% | Aktau, Kuryk, Khorgos, Caspian ferry routes | Medium term (2-4 years) |

| Fragmented SME Logistics Base with Low Digital Maturity and Skilled-Labor Gaps | -0.3% | Rural and secondary cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Border Transshipment, Gauge / Modal-break Inefficiencies at China-Europe Interfaces

Standard-gauge Chinese trains meet broad-gauge Kazakh tracks, forcing costly bogie swaps and up to 48-hour delays. Although Khorgos’ capacity rose to 18,000 TEU, congestion and IT outages undermine schedule reliability. The planned Ayagoz-Tachen line adds volume headroom but not gauge parity, so container damage risk and perishable spoilage persist, dampening high-value traffic potential.

Tariff, Regulatory, and Administrative Inefficiencies Raising Transit Costs and Dwell Times

Despite single-window advances, multi-agency documentation and fluid tariff rules inflate compliance burdens. January 2025 reforms to cut border times at nine crossings are promising but hinge on cross-border coordination and staff reskilling. Cumbersome permit regimes still weigh on small forwarders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Wholesale Trade Leadership Amid Manufacturing Acceleration

Wholesale and Retail Trade generated 33.78% of the Kazakhstan freight and logistics market revenue in 2025, underpinned by imported consumer goods and nationwide hypermarket expansion. Omnichannel strategies demand regional DC networks, interactive voice-picking, and returns processing.

Manufacturing posts the swiftest 4.42% CAGR (2026-2031), courtesy of industrial diversification into autos, renewables, and processing. Korean investors in lithium mining and battery packs amplify inbound flows of chemicals and export-ready cathode materials. As plants synchronize with JIT dashboards, logistics providers deploy milk-run shuttles and line-side feed solutions to minimize WIP inventories.

By Logistics Function: Freight Transport Dominance Drives Market Evolution

Freight Transport captured 73.65% of the Kazakhstan freight and logistics market in 2025, owing to bulk commodities and transit shipments that rely on road, rail, and pipeline assets. Road preserved a 57.35% slice, but investment in Wabtec locomotives in late-2024 raises rail capacity, improving competitiveness on east-west corridors. The Kazakhstan freight and logistics market size for Freight Transport is projected to expand in tandem with multimodal corridor upgrades linking China to the Caspian.

Growth momentum tilts toward CEP, advancing at a 4.32% CAGR (2026-2031). Domestic parcels dominate today, yet cross-border orders rise in double digits as digital customs slash processing times. Warehousing demand mirrors this shift: temperature-controlled space, just 9.88% of capacity, records a brisk 4.16% CAGR (2026-2031) as pharma and fresh-food exports multiply. Providers with automation, pick-to-light technology, and micro-fulfillment centers secure long-term contracts from retailers pivoting to omnichannel models.

By Courier, Express, and Parcel (CEP): Domestic Dominance Amid International Acceleration

Domestic CEP held 66.60% of the Kazakhstan freight and logistics market size in 2025, backed by nationwide locker rollouts and same-day delivery promises in Almaty and Astana. Astana-1’s automated risk-profiling clears 90% of parcels via the green channel, raising throughput for domestic e-tailers.

International CEP is the fastest-rising slice at a 4.45% CAGR (2026-2031) as merchants tap Chinese suppliers for electronics and fashion. Khorgos dry port’s revamped crane yard lifts daily parcel handling, while new scheduled freighters in Almaty funnel outbound returns to Europe within 48 hours. Temperature-controlled CEP emerges for insulin, vaccines, and gourmet foods, bolstering demand for GDP-compliant packaging and data loggers.

By Warehousing and Storage Temperature Control: Cold-Chain Expansion Accelerates

Non-temperature-controlled facilities ruled at 90.12% in 2025, serving FMCG, machinery, and bulk mineral stockpiles. The Kazakhstan freight and logistics market size for temperature-controlled warehousing is climbing on a 4.16% CAGR (2026-2031), spurred by 16.1 million tons of agri-exports and mounting pharma imports.

Modern Grade-A stock faces a shortage: Almaty registers 95% occupancy, and speculative projects such as Griffin Park’s 106,000 m² hub pre-lease over half their space before completion. IoT sensors, lithium-battery back-ups, and WMS integration become baseline requirements as shippers enforce GDP and HACCP standards.

By Freight Transport Mode: Road Supremacy Challenged by Modal Diversification

Road transport retained a 57.35% share in 2025, thanks to last-mile reach and flexible scheduling. However, air freight’s 4.18% CAGR (2026-2031) reflects time-sensitive cargo trends, especially pharma and high-tech components. Kazakhstan's freight and logistics market share is gradually rebalancing as rail garners subsidies for China-EU block trains, and pipeline throughput remains pivotal, moving 54.9 million tons of crude through CPC in 2024.

Sea shipments hinge on Caspian weather windows, yet ferry expansions diversify routing. Environmental policies encourage modal shifts from road to rail, but wagon shortages and gauge breaks at Khorgos still cap achievable volumes. Hybrid solutions-truck-rail-sea chains managed via a single waybill-gain traction for fast-fashion apparel headed to Western Europe.

By Freight Forwarding: Sea Routes Lead Amid Air Growth Acceleration

Sea and inland waterways forwarding commanded 57.76% of the Kazakhstan freight and logistics market in 2025, reflecting crude exports via the Caspian and growing container traffic on feeder services to Baku. The Kazakhstan freight and logistics market size for forwarding is expected to widen as the USD 775 million Aktau upgrade lifts box capacity and embeds IoT-enabled yard management.

Air forwarding, posting a 4.27% CAGR (2026-2031), benefits from electronics, perishables, and urgent automotive spares. Transit incentives at Almaty International Airport halve warehousing charges for re-exported cargo, luring regional consolidations. Forwarders embed API links with the Digital Trade Corridor platform to deliver real-time milestone updates, strengthening value propositions for multinational shippers.

Geography Analysis

Kazakhstan’s vast landmass mandates multimodal arteries that link mineral-rich regions with demand centers. The Trans-Kazakhstan Railway carries the bulk of east-west trade, while federal road upgrades improve feeder access to rural silos. Border reforms in early 2025 shaved average crossing delays by 40% at nine checkpoints, accelerating cross-border truck and rail throughput.

The Caspian littoral anchors maritime logistics. Aktau managed 3.6 million tons of oil in 2024 and will soon feature a green customs lane and reefer plugs to handle fruit transshipments from Central Asia to the Gulf. Western regions reliant on oil pipelines simultaneously welcome wind-farm components, creating backhaul opportunities for project carriers.

Competitive Landscape

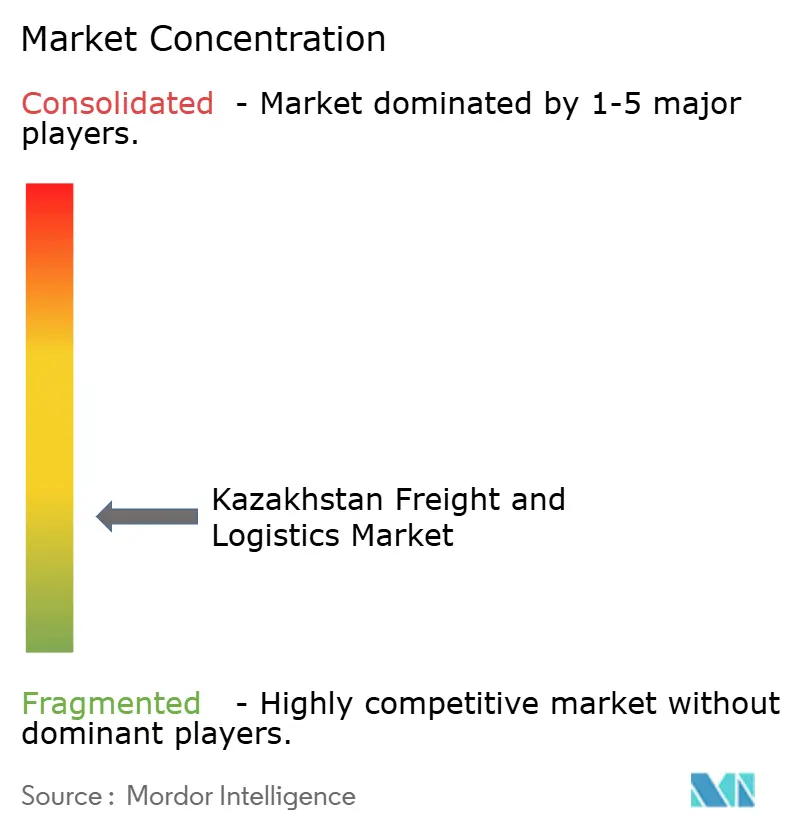

The market remains moderately fragmented. State-owned KTZ subsidiaries dominate rail haulage and terminal operations, benefiting from infrastructure ownership and policy alignment. Kazpost leverages an unrivaled postal network to secure CEP volume spikes linked to domestic e-tailing. International 3PLs such as Rhenus Logistics and CJ Logistics deploy joint ventures to gain know-how on local regulations while injecting global SOPs and IT platforms.

Capacity around critical nodes—including Khorgos dry port and Aktau seaport—drives localized concentration where early movers negotiate preferential slots and long concessions. Digital differentiation is accelerating: KTZ’s blockchain pilot for wagon tracking and Prometeo’s smart-contract platform enhance transparency for shippers wary of transit disruptions.

White-space remains in temperature-controlled logistics, heavy-lift project cargo, and integrated rail-truck services linking SEZ factories to Caspian ports. Consolidation trends emerge as larger 3PLs absorb owner-operators unable to finance Euro-6 truck upgrades or comply with GDP standards. Overall, intense competition on line-haul rates coexists with premium niches commanding double-digit margins.

Kazakhstan Freight And Logistics Industry Leaders

KTZ-Freight Transportation LLC

Kazpost JSC

KTZ Express JSC

Pandora Logistics

KM Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Rhenus Logistics outlined plans for a multimodal terminal in Aktau, targeting cold-chain cargo and project logistics.

- February 2025: QAZTECH and Kazpost commenced talks to embed AI route optimization and drone pilot projects within the national postal network.

- November 2024: Kazakhstan Temir Zholy and Russian Railways agreed to modernize nine border stations and deploy unified digital systems for cross-border freight.

- October 2024: LX Pantos signed an MOU with PTC Group to co-develop TITR-based freight services and optimize shared assets.

Kazakhstan Freight And Logistics Market Report Scope

Freight and logistics refer to the transportation of goods in the domestic and international markets via various modes, including air, rail, and roadways. A complete background analysis of the Kazakhstan freight and logistics market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact is included in the report.

The Kazakhstan Freight and Logistics Market is segmented by Function (Freight Transport, Freight Forwarding, Warehousing, Value-added Services, Cold Chain Logistics, Last-mile Logistics, Return Logistics, and Other Emerging Areas) and End User (Construction, Oil and Gas and Quarrying, Agriculture, Fishing, and Forestry, Manufacturing and Automotive, Distributive Trade, Telecommunications, and Other End Users). The report offers market size and forecast values (USD billion) for all the above segments.

By Logistics Function

| Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | ||

| Freight Forwarding | By Mode of Transport | Air |

| Sea and Inland Waterways | ||

| Others | ||

| Freight Transport | By Mode of Transport | Air |

| Rail | ||

| Road | ||

| Sea and Inland Waterways | ||

| Pipelines | ||

| Warehousing and Storage | By Temperature Control | Non-Temperatured Control |

| Temperatured Control | ||

| Other Services | ||

By End User Industry

| Agriculture, Fishing, and Forestry |

| Construction |

| Manufacturing |

| Oil and Gas, Mining and Quarrying |

| Wholesale and Retail Trade |

| Others |

| By Logistics Function | Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | |||

| Freight Forwarding | By Mode of Transport | Air | |

| Sea and Inland Waterways | |||

| Others | |||

| Freight Transport | By Mode of Transport | Air | |

| Rail | |||

| Road | |||

| Sea and Inland Waterways | |||

| Pipelines | |||

| Warehousing and Storage | By Temperature Control | Non-Temperatured Control | |

| Temperatured Control | |||

| Other Services | |||

| By End User Industry | Agriculture, Fishing, and Forestry | ||

| Construction | |||

| Manufacturing | |||

| Oil and Gas, Mining and Quarrying | |||

| Wholesale and Retail Trade | |||

| Others | |||

Key Questions Answered in the Report

What is the current value of the Kazakhstan freight and logistics market?

The sector is valued at USD 30.5 billion in 2026 and is projected to reach USD 37.24 billion by 2031.

Which logistics function generates the most revenue?

Freight Transport accounts for 73.65% of total revenue thanks to bulk commodity shipments and transit trade.

Which segment is growing the fastest?

The Courier, Express, and Parcel segment shows the quickest expansion with a 4.32% CAGR through 2031.

What role does the Trans-Caspian corridor play?

It channels rising China-Europe volumes, with cargo on the route targeted to double to 10 million tons by 2027.

How will port investments affect capacity?

A USD 775 million upgrade at Aktau is set to lift container handling and embed digital customs, easing bottlenecks.

What is the biggest operational challenge for trucking companies?

Volatile fuel prices and fleet fragmentation drive up costs and complicate service standardization.

Page last updated on: