Cold Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

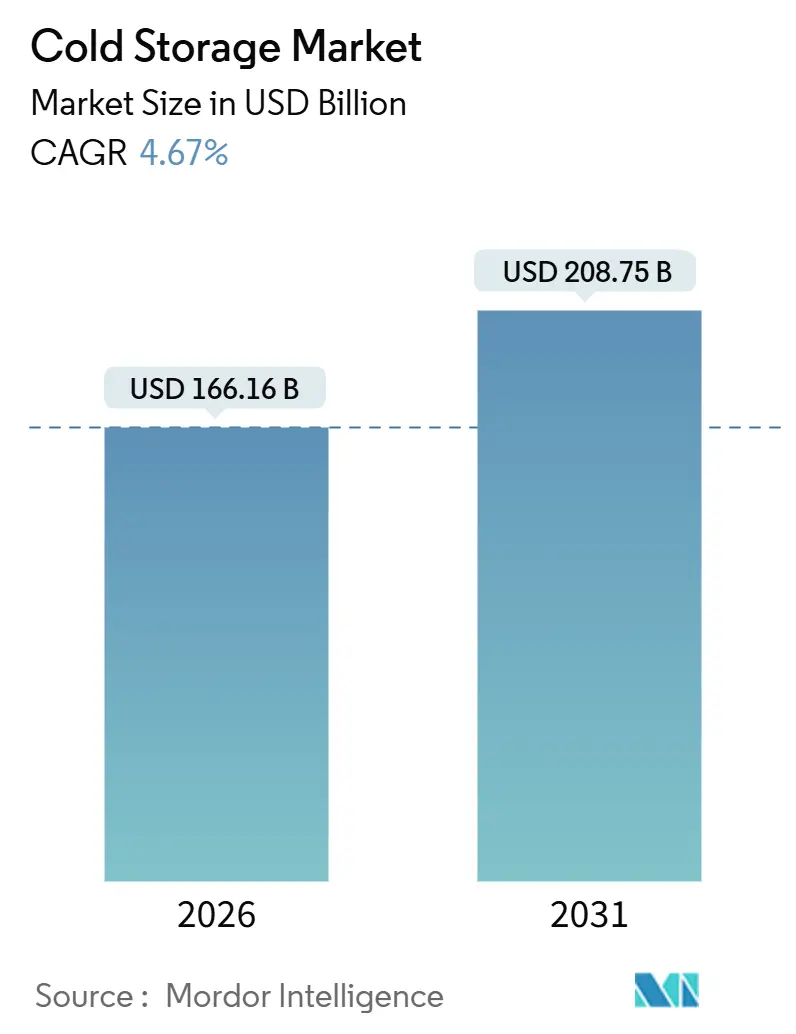

| Market Size (2026) | USD 166.16 Billion |

| Market Size (2031) | USD 208.75 Billion |

| Growth Rate (2026 - 2031) | 4.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cold Storage Market Analysis by Mordor Intelligence

The Cold Storage Market size is estimated at USD 166.16 billion in 2026, and is expected to reach USD 208.75 billion by 2031, at a CAGR of 4.67% during the forecast period (2026-2031).

The expansion is driven less by headline capacity additions and more by structural shifts in consumer behavior, pharmaceutical supply chains, and retail distribution models. Organized retail and e-grocery are demanding urban micro-fulfillment facilities, biologics and cell therapies are pushing temperature thresholds below -20 °C, and automation is becoming a prerequisite for cost control where skilled labor is scarce. Operators able to combine scale, technology, and regulatory expertise are capturing higher-margin niches, while smaller facilities risk obsolescence as energy costs escalate and compliance rules tighten.

Key Report Takeaways

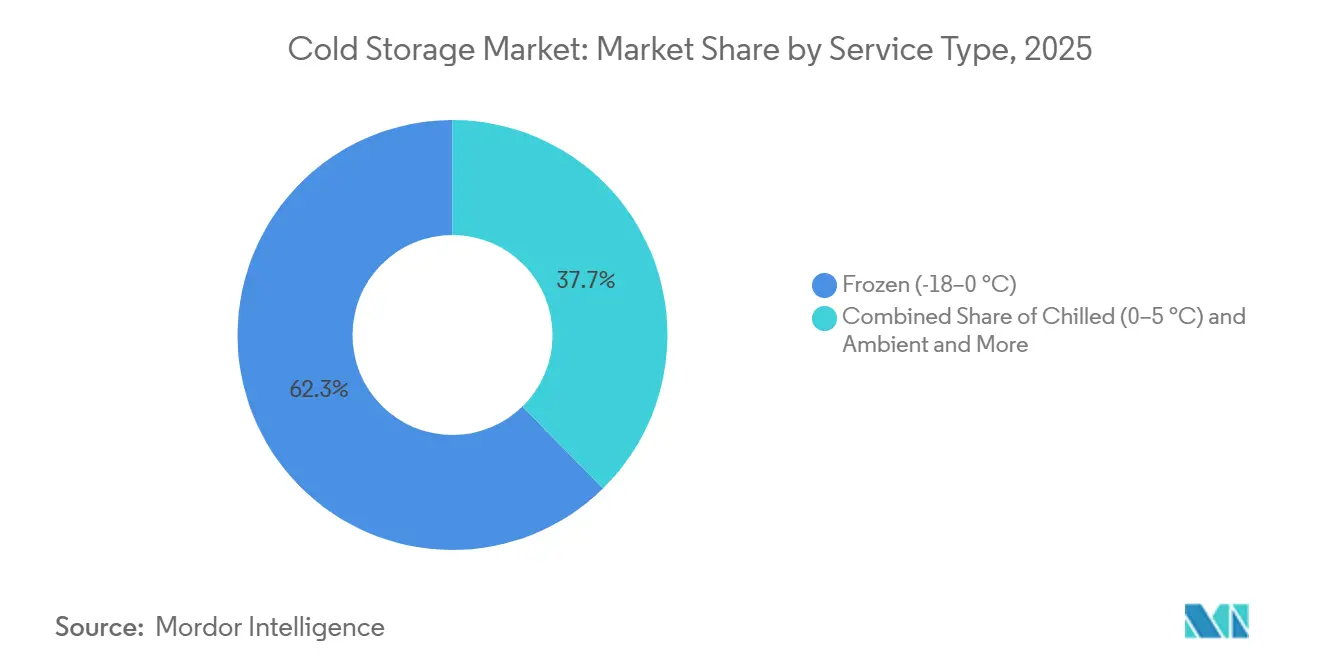

- By temperature type, frozen storage held 62.34% of the cold storage market share in 2025, while deep-frozen and ultra-low facilities are projected to expand at a 13.01% CAGR through 2031.

- By application, fish and seafood led with 17.35% revenue share in 2025; pharmaceuticals and biologics are forecast to advance at an 11.93% CAGR to 2031.

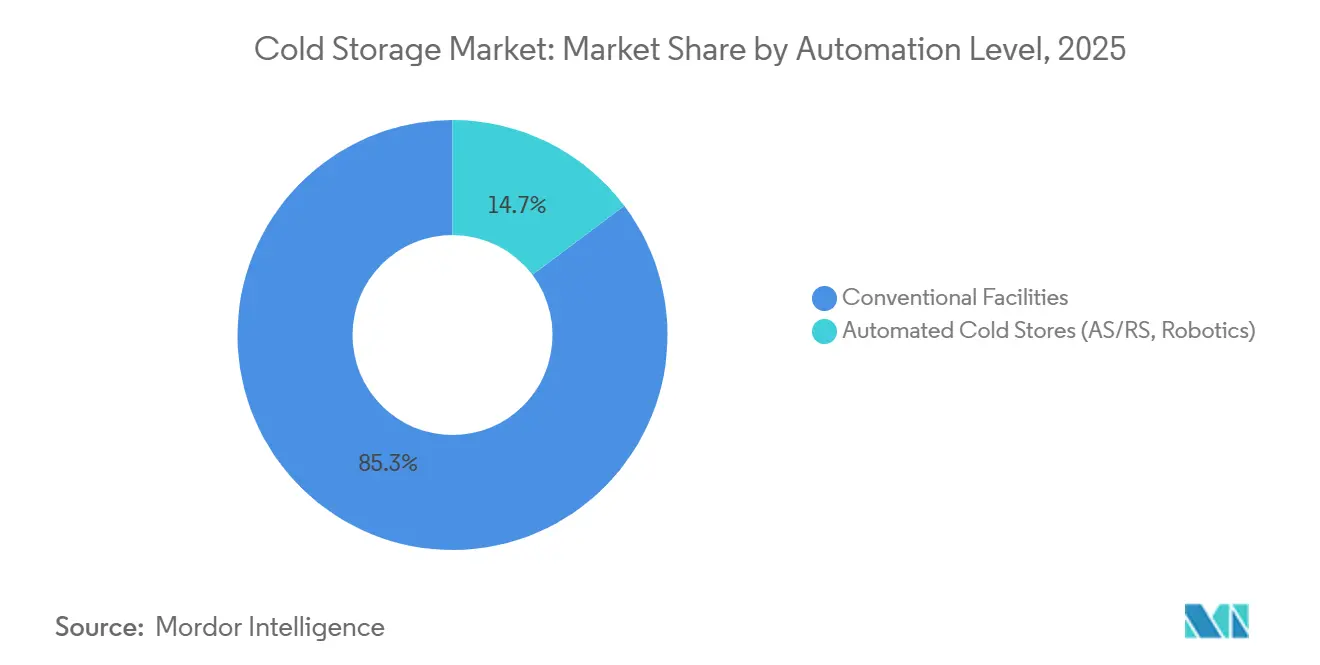

- By automation level, conventional facilities held 85.27% of the cold storage market size in 2025, whereas automated cold stores are expected to grow at a 16.72% CAGR through 2031.

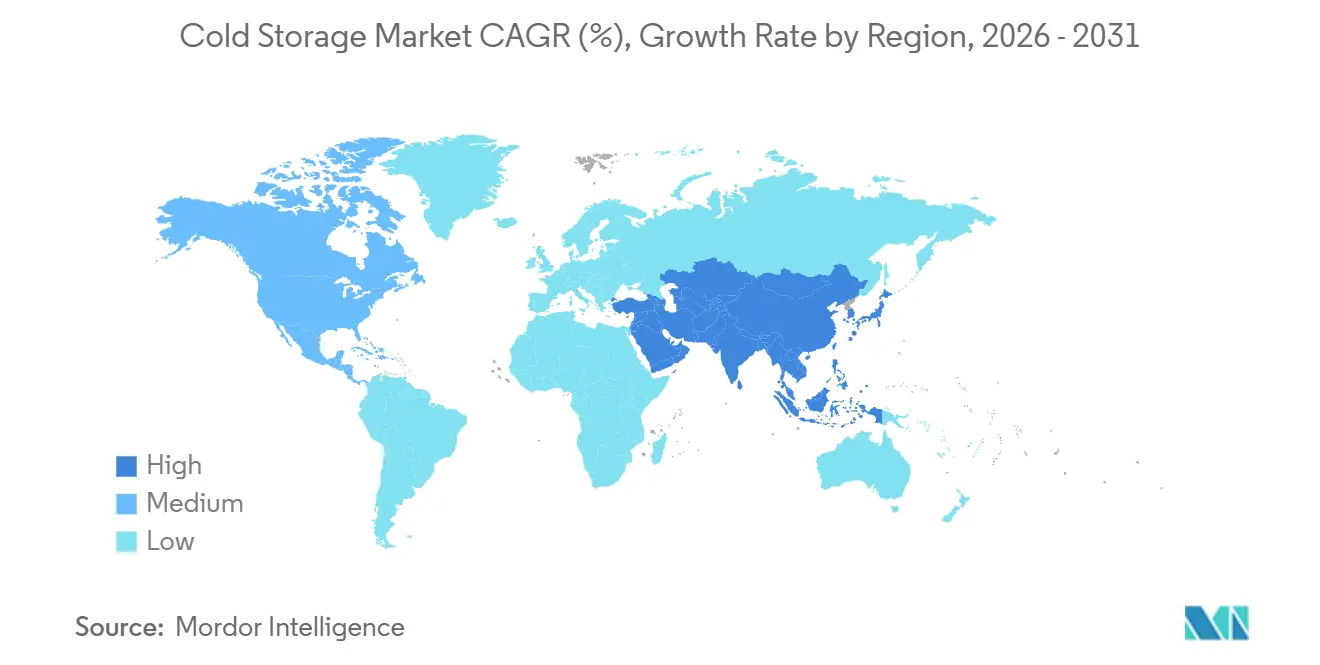

- By region, Asia-Pacific commanded 36.61% of the cold storage market share in 2025 and is poised for the fastest expansion at a 12.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cold Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of Organized Retail & E-grocery | +1.3% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Expansion of Pharmaceutical Cold Chains | +1.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising Demand for Frozen & Convenience Foods | +0.9% | Global | Medium term (2-4 years) |

| Government Incentives for Cold-Chain Infra | +0.7% | India, China, Southeast Asia, Africa | Long term (≥ 4 years) |

| Solar-Powered Refrigeration | +0.5% | Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Warehouse Automation Adoption | +0.4% | North America, Europe, East Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth of Organized Retail & E-grocery

Online grocery is on track to capture 21.5% of total U.S. grocery sales by 2025, reaching the critical mass that justifies purpose-built urban cold stores positioned within 10-15 miles of large population centers. Modern trade formats in India alone are set to rise from USD 790 billion in 2024 to USD 850 billion in 2025, and these outlets require temperature-controlled back-end logistics that legacy wholesale networks cannot supply. Micro-fulfillment designs maximize cubic utilization, often serving more than 100,000 households with a 30-minute delivery window while cutting last-mile costs by up to 50%. The upside is balanced by forecasting challenges: stockouts or spoilage in high-rent urban nodes rapidly erode margin advantages, pushing operators toward sophisticated demand-planning software and advanced analytics.

Expansion of Pharmaceutical Cold Chains

Biologics, cell therapies, and gene therapies now demand storage from -40 °C down to -196 °C, a range far beyond traditional vaccine requirements. SCHOTT Pharma’s polymer syringe validated to -180 °C, launched in 2025, underscores the pace of packaging innovation. GDP certification, automated temperature monitoring, and validated chain-of-custody protocols have raised compliance costs but also created durable barriers to entry, allowing certified facilities to charge 30–50% pricing premiums. Geography is diversifying as manufacturers establish regional depots for resilience, opening opportunities for cold storage operators in secondary markets previously overlooked by pharmaceutical logistics[1].SCHOTT Pharma, “Polymer Syringe for Ultra-Low Temperature Storage,” schott-pharma.com.

Rising Demand for Frozen & Convenience Foods

Per-capita consumption of frozen meals is climbing in mature economies despite stable populations, reflecting improved freezing technologies and changing household time budgets. In the United States, the cold chain logistics value linked to frozen products is projected to move from USD 97.13 billion in 2026 to USD 133.87 billion by 2031 at a 6.63% CAGR. Ready-to-eat meals require rapid blast freezing for texture retention, lengthening dwell times, and tying up warehouse capacity. Operators are responding with hybrid contract models blending dedicated and shared space to smooth utilization curves and secure predictable revenue flows.

Government Incentives for Cold-Chain Infrastructure

India’s PMKSY program has earmarked INR 4,600 crore (USD 550 million) for integrated cold chains through March 2026, already delivering more than 838,000 metric tons of capacity. Provinces in China provide tax holidays and land-use concessions for energy-efficient projects, while the Asian Development Bank’s 2025 integration report lists cold storage as a priority for technical assistance. These incentives now emphasize end-to-end networks over isolated depots, nudging private developers toward hub-and-spoke configurations that link farm gates to city centers[2].Invest India, “Cold Chain Infrastructure and Its Future Potential,” investindia.gov.in

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Energy Consumption & Electricity Costs | -0.8% | Global, acute in regions with high tariffs | Short term (≤ 2 years) |

| Heavy Upfront CapEx & Regulatory Compliance | -0.6% | Global, especially in emerging markets | Long term (≥ 4 years) |

| Shortage of Skilled Refrigeration Technicians | -0.5% | Global, severe in secondary cities | Medium term (2-4 years) |

| Rising Insurance Premiums for Ammonia Systems | -0.3% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Energy Consumption & Electricity Costs

Energy accounts for 50-70% of operating expense in a typical cold store, leaving profitability highly sensitive to tariff swings. In parts of Sub-Saharan Africa, grid unreliability forces diesel backup that can raise operating costs by 25%. Facilities are upgrading building envelopes, installing variable-speed drives, and adopting low-GWP refrigerants such as Honeywell’s Solstice ze, reported to cut energy use by 46%. Capital outlays, however, range from USD 1 million to USD 3 million per 100,000 ft2, slowing adoption in lower-margin facilities[3]Honeywell, “Energy Efficiency Standards in Cold Storage,” honeywell.com.

Heavy Upfront CapEx & Regulatory Compliance

A pharmaceutical-grade warehouse can cost more than USD 200 per ft2, compared with USD 70 for ambient space. Capital intensity is compounded by the EU’s revised F-gas Regulation 2024/573, which bans self-contained units with a GWP above 150 from January 2025, forcing retrofits or replacement. Natural refrigerants such as CO₂ and ammonia meet environmental rules but require new safety protocols, additional sensors, and higher insurance premiums, creating a two-tier market where well-funded operators pull ahead[4].Laird Thermal Systems, “Decline of F-Gases and Impact on Refrigeration Equipment,” lairdthermal.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Temperature Type: Ultra-Low Demand Reshapes Capacity Mix

Frozen storage continues to anchor 62.34% of the cold storage market in 2025 by value. Yet the deep-frozen and ultra-low segment, defined as below -20 °C, is climbing at a 13.01% CAGR to 2031, nearly triple the overall cold storage market growth. Ultra-low freezers operating between -40 °C and -86 °C are indispensable for cell and gene therapies, and demand for cryogenic liquid nitrogen storage below -150 °C is emerging. This high-specification space commands rental rates two to three times higher than standard frozen rooms, cushioning capital costs and supporting premium margins.

Operators investing early enjoy durable advantages. Ultra-low rooms require redundant compressors, backup generators sized for extended outages, stainless-steel racks compatible with cryogenic exposure, and continuous monitoring that integrates with validated laboratory information systems. Upfront capex per pallet slot can exceed USD 1,500, but high utilization and multi-year take-or-pay contracts common in pharma logistics provide revenue certainty. Conversely, the chilled 0-5 °C band retains steady demand for dairy, produce, and non-frozen pharmaceuticals. Pricing pressure is more acute in chilled rooms, prompting consolidation as operators seek scale to spread fixed energy and compliance costs. Hybrid facilities that flex zones among chilled, frozen, and ambient conditions are gaining traction, maximizing cubic throughput and diversifying revenue streams within a single site.

By Automation Level: Robotics reshape throughput economics

Automated stores featuring AS/RS, shuttle systems, and palletizing robots are projected to expand at a 16.72% CAGR through 2031, outstripping the cold storage market overall. The capital requirement of USD 50-100 million per facility favours operators with access to low-cost funding and large anchor tenants willing to commit volume.

Automated palletizers and layer depalletizers reduce dock dwell times by 40%, expanding ship-cum-receive windows. Modern facilities integrate digital twins that model energy draw, labor flow, and inventory turns, enabling operators to tweak algorithms for real-time gains. Cold storage market share captured by automated facilities is forecast to climb as returns on invested capital improve and financing structures mature.

Insurance premiums for automated sites often fall due to lower human exposure risks, partly offsetting capex. In addition, predictive maintenance sensors lower unplanned downtime, a critical metric when handling high-value biologics. Regulatory bodies increasingly accept electronic batch records and automated condition monitoring, streamlining compliance for heavily regulated products.

By Application: Pharma demand outpaces legacy food segments

Fish and seafood retained 17.35% of the cold storage market share in 2025, underpinned by stringent temperature requirements from catch to retail. Pharmaceuticals and biologics, though representing a smaller absolute volume, are on course for an 11.93% CAGR to 2031, making them the principal growth engine. Premium pricing reflects the need for stringent chain-of-custody records, continuous monitoring, and GDP certification.

Meat and poultry volumes remain substantial but exhibit seasonal surges tied to production cycles and holiday demand, necessitating flexible contracts. Fruits and vegetables drive regional dynamics in export-oriented economies, particularly in South America and Southeast Asia. Dairy, frozen desserts, and ready-to-eat meals benefit from improved freezing technology that preserves texture and taste, extending shelf life and global reach. Specialty chemicals and clinical trial materials round out a diverse portfolio that keeps capacity utilization high but demands tailored handling protocols. Successful operators craft mix management strategies that favor year-round, high-margin tenants while allocating shoulder periods to lower-rate, seasonal commodities, thereby smoothing revenue volatility.

Geography Analysis

Asia-Pacific held 36.61% of the cold storage market value in 2025 and is set to outpace all other regions with a 12.02% CAGR to 2031. China’s provincial subsidies and mandatory green-design codes spur investment in energy-efficient warehouses, while India’s government programs underwrite integrated networks from farmgate to megacity. Southeast Asia is maturing into a regional transshipment hub, channeling seafood and pharmaceuticals through Singapore’s and Malaysia’s temperature-controlled ports. Fragmented regulatory frameworks and skills gaps persist, yet savvy operators leverage joint ventures with local partners to navigate permitting and land acquisition hurdles.

North America exhibits a mature yet dynamic landscape. The United States alone controls roughly 3.7 billion cubic feet of refrigerated storage, but average facility age exceeds 40 years, prompting a modernization wave. E-grocery penetration and pharmaceutical growth are redirecting investment toward urban micro-fulfillment nodes and automated mega-warehouses near intermodal corridors. Land scarcity in Tier-1 coastal markets inflates ground rents, pushing development inland along rail-served logistics parks. Canada and Mexico are expanding capacity to support export-oriented agriculture and near-shoring trends, respectively, cementing the region’s integrated supply networks.

South America, Europe, and the Middle East-Africa offer contrasting profiles. Brazil and Peru expand capacity for meat and fruit exports, though currency volatility and high borrowing costs limit smaller projects. Europe’s cold storage market is undergoing a regulatory-driven overhaul as the F-gas ban accelerates adoption of natural refrigerants. Germany, the BENELUX, and the Nordics lead in automation and renewable integration, while Southern Europe deploys hybrid solar-powered plants to offset high electricity tariffs. In the Middle East, the UAE and Saudi Arabia position themselves as regional hubs, while Sub-Saharan Africa experiments with solar-linked micro-storage to cut post-harvest losses, highlighting diverse pathways toward cold chain maturity.

Competitive Landscape

Market concentration is accelerating in developed regions. Lineage Logistics and Americold Realty Trust together control more than 70% of North American capacity, leveraging scale for procurement advantages, proprietary software, and cross-regional service offerings that smaller rivals struggle to match. Lineage’s USD 4.2 billion IPO in 2024 funded further acquisitions and automation rollouts. Americold pursues joint ventures, such as its USD 130 million Kansas City rail-connected site, to expand without over-stretching its balance sheet.

Despite consolidation, fragmentation persists in emerging markets where local knowledge and relationship-based business models still confer advantages. Regional champions in India, China, and Brazil defend their share through deep customer intimacy and agile decision-making, even as global players enter via minority stakes and partnerships. Technology adoption is the fault line: leaders deploy IoT sensors, AI-driven predictive maintenance, and advanced warehouse management systems that compress costs and raise service levels. Smaller facilities lacking capital for upgrades risk relegation to low-margin commodity storage or exit altogether.

White-space opportunities center on pharmaceutical-grade depots, automated micro-fulfillment centers, and solar-powered rural hubs. Specialized providers offering Cooling-as-a-Service, zero-carbon refrigeration, or GDP-certified storage are attracting private equity interest. Competitive intensity is expected to tighten as sustainability disclosures become mandatory and customers prioritize partners able to document carbon footprints and compliance credentials.

Cold Storage Industry Leaders

Lineage Logistics

Americold Logistics

Nichirei Logistics Group

Swire Cold Storage

Burris Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: AGRO Merchants Group announced expansion of Southeast U.S. operations, adding robotics and advanced monitoring to serve pharmaceutical and food-service customers.

- April 2025: NewCold completed installation of automated guided vehicles and robotic picking systems across several European sites, enhancing throughput and reducing labor exposure.

- March 2025: Lineage Logistics agreed to acquire Bellingham Cold Storage, adding four campuses in Washington and Illinois and widening its producer-focused service offering

- February 2025: Americold Realty Trust formalized a USD 130 million Kansas City build-to-suit with Canadian Pacific and a USD 35 million Dubai distribution center with DP World, extending intermodal reach and geographic diversity.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the cold storage market as every purpose-built warehouse that keeps goods between -25 °C and +5 °C, ranging from single-story chiller rooms to high-bay automated sites that move pallets with cranes and robots. We, the analysts at Mordor Intelligence, treat public facilities operated by third-party logistics firms and private captive stores in equal measure, provided the space is revenue-earning.

Scope Exclusions: The model leaves out refrigerated transport fleets, on-premise retail coolers, and the construction value of new greenfield projects.

Segmentation Overview

- By Temperature Type

- Chilled (0–5 °C)

- Frozen (-18–0 °C)

- Ambient

- Deep-Frozen / Ultra-Low (<-20 °C)

- By Automation Level (Storage)

- Conventional Facilities

- Automated Cold Stores (AS/RS, Robotics)

- By Application

- Fruits & Vegetables

- Meat & Poultry

- Fish & Seafood

- Dairy & Frozen Desserts

- Bakery & Confectionery

- Ready-to-Eat Meals

- Pharmaceuticals & Biologics

- Vaccines & Clinical Trial Materials

- Chemicals & Specialty Materials

- Other Perishables

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor's team interviewed warehouse managers across North America, Europe, and Asia Pacific, along with equipment vendors and cold-chain auditors, to verify utilization rates, automation premiums, and energy-efficiency upgrade costs. These discussions closed data gaps and grounded our model assumptions in day-to-day operating realities.

Desk Research

We began with publicly available datasets, USDA refrigerated capacity surveys, FAO perishables output, UN Comtrade trade tonnage, and Eurostat energy indices, which gave us foundational volume and cost signals. Regulation notes from the Montreal Protocol updates, plus guidance papers from the International Association of Refrigerated Warehouses, clarified compliance-driven retrofit needs. Analysts next mined company 10-Ks, investor decks, and D&B Hoovers profiles to extract occupied cubic-foot metrics and lease revenues. Dow Jones Factiva and major trade journals were scanned to cross-check expansion announcements. The sources listed illustrate, not exhaust, the wider pool reviewed.

Market-Sizing & Forecasting

A top-down capacity-reconstruct approach converted national refrigerated cubic feet into addressable revenue using sampled average storage tariffs, which are then validated through selective bottom-up roll-ups of major operators' disclosed earnings. Key inputs include pallet turnover ratios, e-grocery penetration, frozen food export volumes, pharmaceutical biologics output, energy price trends, and F-gas phase-down timelines. Forecasts to 2030 rely on a multivariate regression that links tariff growth to energy costs, automation uptake, and commodity throughput, while scenario checks adjust for policy or supply-chain shocks.

Data Validation & Update Cycle

Outputs pass a multi-tier review where separate analysts audit formulas, compare results with satellite indicators such as compressor sales, and re-interview sources when anomalies exceed preset thresholds. Our dashboard refreshes annually, with interim revisions triggered by material capacity additions or regulatory shifts, ensuring clients always receive an up-to-date baseline.

Why Mordor's Cold Storage Baseline Commands Reliability

Published estimates often vary because firms count different assets, apply divergent tariff assumptions, and refresh at uneven intervals. Our disciplined scope selection and yearly recalibration narrow that spread for decision-makers.

Key gap drivers include whether land and building construction values are bundled, the aggressiveness of demand multipliers, and the depth of occupancy cross-checks. Mordor reports stick to revenue-earning floor space only, adopt balanced growth scenarios, and validate tariffs through direct operator interviews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 158.67 billion | Mordor Intelligence | - |

| USD 185.75 billion | Global Consultancy A | Counts refrigeration equipment sales and land appraisal values, inflating totals |

| USD 179.58 billion | Industry Association B | Applies single frozen-food CAGR without verifying warehouse occupancy or tariff variation |

These comparisons show that Mordor's numbers rest on a traceable chain of capacity data, tariff evidence, and routine validation, giving users a stable, transparent starting point for strategy and investment.

Key Questions Answered in the Report

What is the 2026 value of the cold storage market?

The cold storage market size is valued at USD 166.16 billion in 2026.

How fast will demand for ultra-low temperature storage grow?

Deep-frozen and ultra-low facilities are projected to expand at a 13.01% CAGR through 2031.

Which region is expected to lead growth to 2031?

Asia-Pacific combines the largest share with the fastest growth, advancing at a 12.02% CAGR.

Who are the dominant players in North America?

Lineage Logistics and Americold Realty Trust together control more than 70% of North American capacity.

What share did frozen storage hold in 2025?

Frozen rooms accounted for 62.34% of cold storage market share in 2025.

Which application segment is growing quickest?

Pharmaceuticals and biologics are forecast to grow at an 11.93% CAGR through 2031 due to rising biologics and gene therapy volumes.

Page last updated on: