United States Oil And Gas Pipeline Maintenance, Repair, And Overhaul (MRO) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.03 Billion |

| Market Size (2026) | USD 6.33 Billion |

| Market Size (2031) | USD 8.07 Billion |

| Growth Rate (2026 - 2031) | 4.98% CAGR |

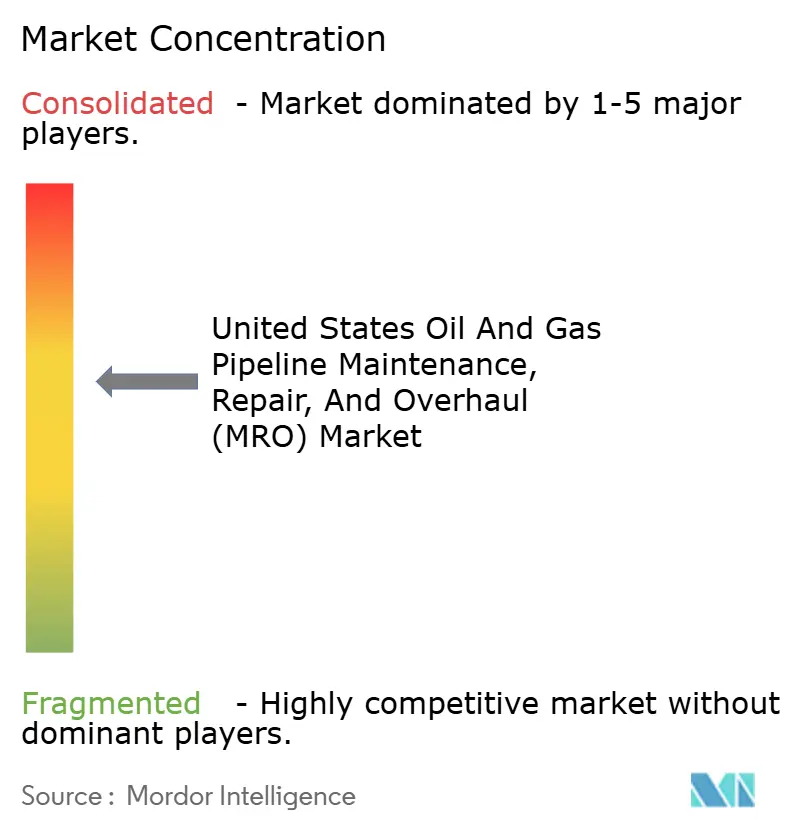

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Oil And Gas Pipeline Maintenance, Repair, And Overhaul (MRO) Market Analysis by Mordor Intelligence

The United States Oil And Gas Pipeline Maintenance, Repair, And Overhaul Market size in 2026 is estimated at USD 6.33 billion, growing from 2025 value of USD 6.03 billion with 2031 projections showing USD 8.07 billion, growing at 4.98% CAGR over 2026-2031.

Robust growth stems from the convergence of aging transmission mileage, intensifying integrity mandates under the PHMSA “Mega Rule,” and the rapid digitalization of inspection workflows, collectively de-risking downtime and environmental incidents.[1]Pipeline Hazardous Materials Safety Administration, “Gas Transmission & Gathering Annual Report Mileage,” phmsa.dot.gov Operators are prioritizing condition-based maintenance enabled by smart-pigging data, while composite repair technologies reduce replacement costs and extend asset life. Federal grants worth USD 196 million, awarded in 2024, are accelerating safety-driven upgrades, particularly across rural gas distribution networks. Competitive intensity is rising as technology specialists leverage IoT sensors and predictive analytics that can trim unplanned outages by as much as 70% and reshape pricing models toward outcome-based contracts.[2]Pipeline & Gas Journal Staff, “Digital Twins Cut Unplanned Downtime by 70%,” pipeline-gasjournal.com

Key Report Takeaways

- By service type, maintenance led with a 35.72% revenue share in 2025, and is projected to expand at a 5.62% CAGR through 2031.

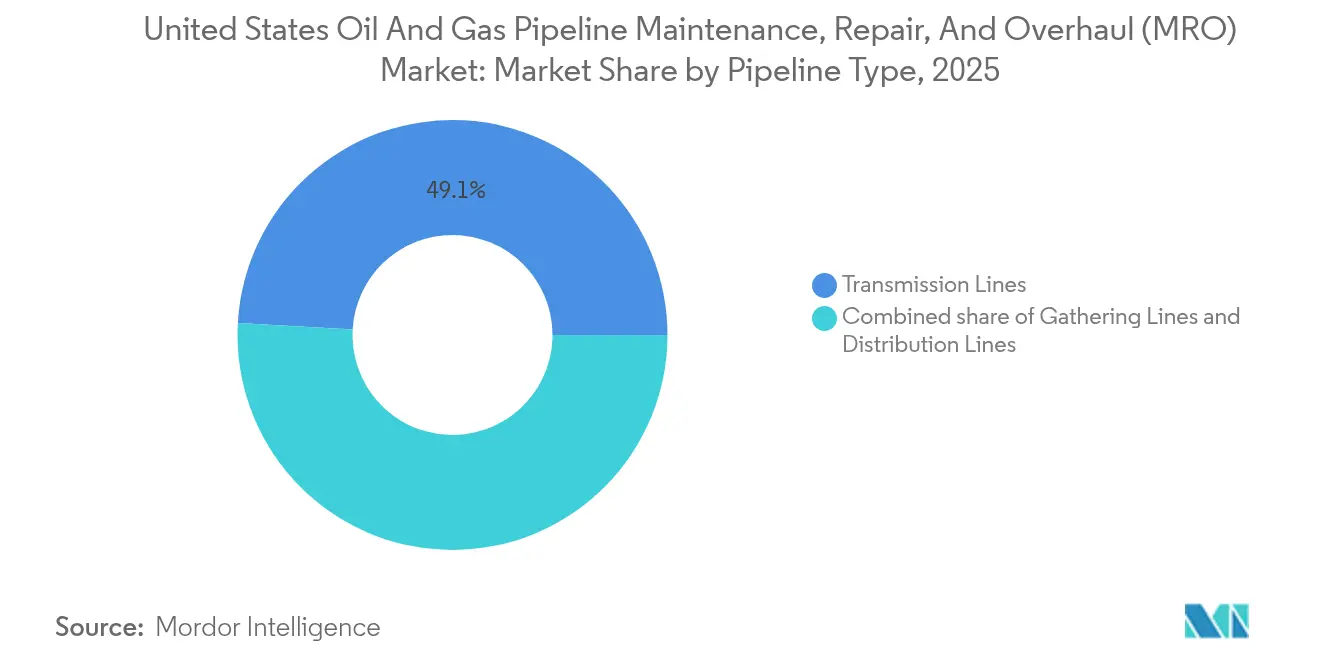

- By pipeline type, transmission lines held 49.12% of the US oil and gas pipeline MRO market share in 2025 and are expected to represent the fastest-growing pipeline class at a 5.18% CAGR through 2031.

- By location of deployment, onshore assets commanded 76.65% of value in 2025; offshore operations, however, deliver the highest growth at a 6.05% CAGR through the forecast window.

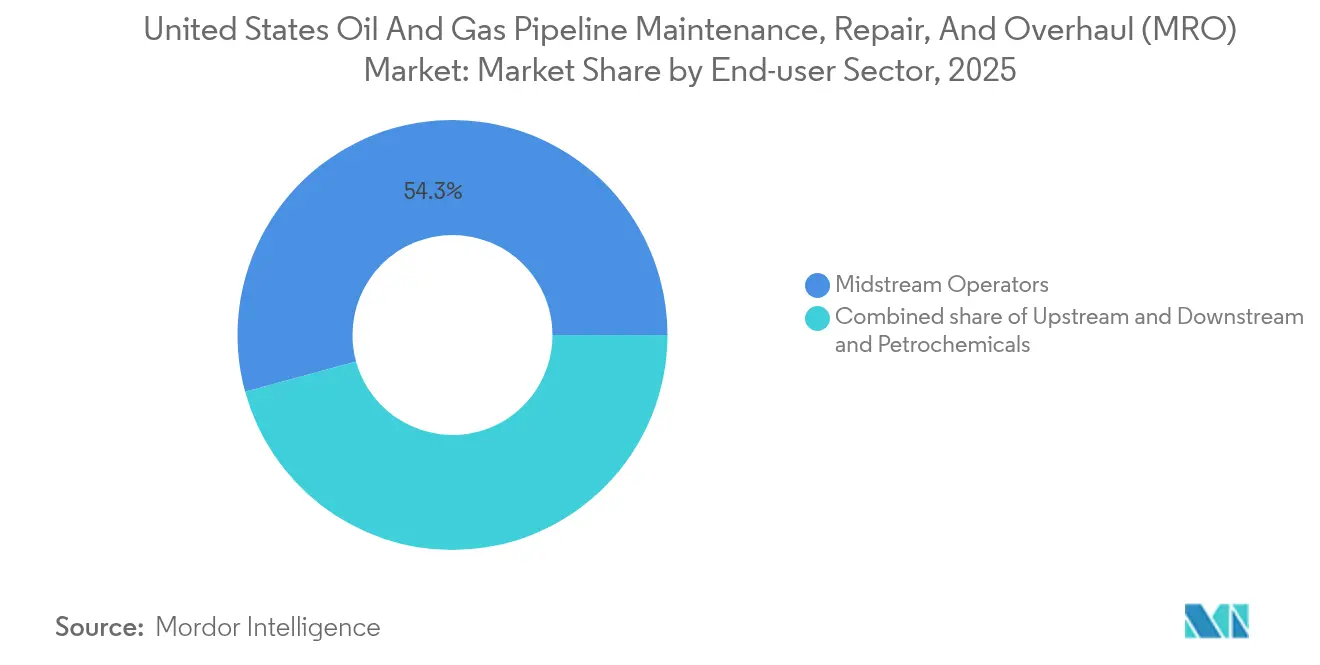

- By end-user sector, midstream operators accounted for 54.25% of revenues in 2025 and continue to register a resilient 5.12% CAGR, given their fee-based business models, which are insulated from crude price swings.

- By geography, the Gulf Coast contributed roughly 34.62% of 2025 spending, underpinned by the nation’s densest pipeline grid and steady petrochemical capacity additions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Oil And Gas Pipeline Maintenance, Repair, And Overhaul (MRO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging pipeline infrastructure & integrity mandates | 1.20% | Gulf Coast, Midwest | Long term (≥ 4 years) |

| Shale output growth raising throughput stress | 0.90% | Permian, Appalachian, Bakken | Medium term (2-4 years) |

| Adoption of smart pigging & IoT sensors | 0.80% | National | Medium term (2-4 years) |

| Federal funding for infrastructure modernization | 0.70% | National | Short term (≤ 2 years) |

| Emergence of composite repair technologies | 0.60% | National | Long term (≥ 4 years) |

| Regulatory compliance requirements | 0.80% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Pipeline Infrastructure & Integrity Mandates

Roughly 67% of US natural-gas transmission mileage predates 1970 standards, necessitating sustained inspection, recoating, and valve replacement schedules.[3]Pipeline Hazardous Materials Safety Administration, “Mega Rule Final Rulemaking,” phmsa.dot.gov Operators now earmark 15-20% of annual capex for compliance-driven MRO, an allocation that underpins the long-run visibility of the US oil and gas pipeline MRO market. The 2025 Mega Rule deadline intensifies demand for Engineering Critical Assessments, a process that service providers monetize via multi-year master service agreements. Long-cycle integrity programs insulate maintenance budgets from commodity price fluctuations, supporting predictable order backlogs even during periods of reduced upstream spending. As regulatory scrutiny intensifies, suppliers offering bundled inspection-plus-repair packages gain market share by streamlining workflow handoffs and reducing permitting timelines.

Shale Output Growth Raising Throughput Stress

Permian Basin oil output at 5.7 million bpd in 2024 strains trunk lines originally engineered for lower volumes, elevating vibration loads and corrosion rates.[4]U.S. Energy Information Administration, “Drilling Productivity Report—Permian Output,” eia.gov Parallel gas surges from Appalachia push multi-decade steel to its fatigue limits, spurring compressor station retrofits and pipe reinforcement campaigns. Because greenfield projects face permitting headwinds, midstream firms are maximizing existing corridors, thereby expanding the opportunity pool for flow-optimization and integrity services within the US oil and gas pipeline MRO market. Accelerated wear profiles result in higher call-out frequencies for weld overlays, sleeve installations, and cathodic protection tune-ups. Vendors versed in predictive analytics win contracts by demonstrating their ability to extend the intervals between digs while maintaining throughput.

Adoption of Smart Pigging & IoT Sensors

High-resolution magnetic-flux-leakage pigs now pinpoint sub-millimeter defects, and when paired with IoT pressure sensors, feed digital twins that forecast failure probability with machine-learning precision. Operators deploying these systems report up to a 70% reduction in unscheduled shutdowns, validating the ROI of condition-based maintenance. The pivot from calendar to risk-ranked maintenance reshapes service mix toward data analytics, firmware updates, and cloud infrastructure support, expanding revenue channels beyond traditional field labor. Early adopters in interstate transmission corridors set best-practice benchmarks that distribution utilities and gathering networks increasingly emulate, widening overall addressable spending in the US oil and gas pipeline MRO market.

Federal Funding for Infrastructure Modernization

PHMSA’s Natural Gas Distribution Infrastructure Safety and Modernization grants released USD 196 million in 2024, the first tranche of nearly USD 1 billion earmarked through 2028. Funds target leak-prone cast-iron and bare-steel segments in disadvantaged communities, accelerating work scopes for distribution contractors. The Infrastructure Investment and Jobs Act further channels money toward methane emissions reduction, boosting demand for advanced leak-detection equipment and low-bleed pneumatic replacements within the US oil and gas pipeline MRO market. Public dollars not only de-risk project finance but also impose performance metrics that favor technology-rich bidders capable of transparent reporting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-price volatility curbing O&M budgets | -0.80% | Permian, Bakken | Short term (≤ 2 years) |

| Environmental opposition to work permits | -0.60% | Northeast, West Coast | Medium term (2-4 years) |

| Skilled labor shortage for specialty MRO | -0.70% | Rural corridors | Long term (≥ 4 years) |

| Cyber-risk in pipeline SCADA systems | -0.40% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Crude-Price Volatility Curbing O&M Budgets

WTI prices swung between USD 70 and USD 85 per barrel in 2024, prompting exploration firms to defer non-critical work and renegotiate service scopes. Although fee-based midstream revenue softens the blow, upstream austerity can ripple into gathering-line maintenance call-outs, dampening near-term order books across the US oil and gas pipeline MRO market. Suppliers counter volatility by diversifying into long-cycle compliance projects and offering subscription-style inspection services that flatten revenue variability.

Environmental Opposition to Work Permits

Legal interventions under NEPA and state-level reviews can stretch routine maintenance permits by 12-18 months, complicating crew scheduling and fragmenting mobilization efficiencies. In regions like the Northeast, public hearings and litigation risk add cost premiums, as contractors factor standby time into their bids. The uncertainty deters smaller firms and reinforces the role of large providers with in-house environmental-compliance teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Maintenance Dominance Reflects Proactive Asset Management

Maintenance captured 35.72% of the US oil and gas pipeline MRO market in 2025 and is projected to grow at a 5.62% CAGR, highlighting the industry’s shift from reactive repairs to predictive maintenance tied to integrity analytics. The segment benefits from grant-funded safety programs and PHMSA inspection cycles, ensuring recurring demand even during commodity downturns. Inspection and monitoring form the backbone of this proactive stance, driving cross-sales into chemical cleaning, valve lubrication, and cathodic protection tuning. Vendors that combine smart-pig analytics with field execution cut client downtime and are rewarded with multi-year blanket purchase agreements. Repair and rehabilitation remain a substantial tail, especially for legacy steel that fails hydro tests; nonetheless, composite wraps are steadily cannibalizing cut-and-replace work. Decommissioning, although still niche, is gaining visibility as operators retire redundant assets in line with methane-reduction pledges, thereby fostering a long-term layer of project work within the US oil and gas pipeline MRO market.

Second-order effects come from digital twins that sequence maintenance tasks into outage-centered clusters, squeezing greater output from limited crew capacity. Overhaul activities tend to focus on critical compressor stations, where centrifugal blades and gearboxes require OEM-grade rebuilds every five to seven years. As uptime metrics increasingly influence pipeline tariffs, service contractors with KPI-linked payment clauses capture premium margins. The rising use of autonomous inline inspection tools also shifts revenue toward data interpretation and software support retainers, further blurring lines between pure maintenance and tech services in the US oil and gas pipeline MRO industry.

By Pipeline Type: Transmission Networks Drive Infrastructure Investment

Transmission lines accounted for 49.12% of expenditure in 2025 and are expected to advance at a 5.18% CAGR, reflecting heavy-diameter, high-pressure assets where failure risk and regulatory scrutiny are highest. These arteries, often spanning state borders, are early adopters of machine-learning corrosion prediction and deploy multi-sensor pigs capable of measuring axial strain, reinforcing their centrality to the US oil and gas pipeline MRO market. Gathering networks, conversely, face rapid lateral expansion in shale plays; while individual diameters are smaller, the aggregate mileage fuels a sizeable maintenance sub-segment. Distribution pipelines focus on urban leak mitigation; grant flows accelerate plastic-pipe replacement, thereby boosting localized MRO spending. The emergence of hydrogen blending pilots inside gas distribution grids could expand material compatibility testing, adding an incremental revenue stream.

As interstate capacity utilization exceeds 90% on certain corridors, operators push deferred maintenance into accelerated schedules. Transmission owners prefer turnkey contractors who can mobilize composite wraps, hot taps, and hydrostatic testing fleets under a single umbrella. By contrast, gathering customers prize low-cost mobilization and quick-hit repairs. This segmentation splits competitive dynamics, yet the high-value transmission slice ultimately steers technology roadmaps and standard-setting within the US oil and gas pipeline MRO market.

By Location of Deployment: Offshore Growth Outpaces Onshore Maturity

Onshore corridors still account for 76.65% of 2025 revenue, sustained by 2.6 million miles of existing pipeline. Even so, offshore assets log the strongest 6.05% CAGR thanks to the Gulf of Mexico’s deepwater tie-backs and increasing subsea compression pilots. Subsea MRO demands ROV-deployed ultrasound and hyperbaric welding capabilities, as well as specialized composite sleeves rated for hydrostatic pressure, all of which carry service premiums two to four times those of onshore equivalents. Remote work scopes linked by digital twins and satellite communications help mitigate weather-related downtime, boosting crew productivity and data capture in harsh environments.

Onshore projects increasingly deploy drones and crawler robots for right-of-way surveillance, freeing scarce technicians for higher-value tasks. Meanwhile, ESG reporting is pushing green-field maintenance yards to electrify their fleets, initiating another capital expenditure stream for tool providers. Although offshore’s absolute spend is smaller, its technology intensity makes it disproportionately influential in shaping innovation paths across the broader US oil and gas pipeline MRO market.

By End-User Sector: Midstream Leadership Reflects Infrastructure Criticality

Midstream entities represented 54.25% of 2025 spending and continue to outpace other sectors with a 5.12% CAGR. Their fee-based revenue insulates budgets, enabling consistent multi-year asset-integrity programs. Transmission-focused midstream operators also have larger right-of-way footprints, which translates into economies of scale for bundled inspection, maintenance, and repair frameworks. Upstream companies fluctuate with drilling cycles, but unconventional output volumes compel them to sustain gathering-line maintenance despite price dips, thereby anchoring a baseline revenue stream. Downstream and petrochemical players maintain steady, albeit slower, growth due to established turnaround calendars synchronized with plant outages.

Integrated majors blur sectoral lines by operating upstream wells, trunk lines, and export terminals, creating demand for end-to-end service contracts that span the full lifecycle. Suppliers familiar with multiple PHMSA sub-parts (B, O, W) gain a competitive edge by offering regulatory expertise across asset classes, thereby bolstering retention in the US oil and gas pipeline MRO market.

Geography Analysis

The Gulf Coast accounted for nearly 34.62% of 2025 expenditures and is expected to maintain robust growth as petrochemical expansions and LNG export terminals reinforce infrastructure complexity. Over 58,000 miles of interstate pipe in Texas alone require discernible maintenance cadences to satisfy both PHMSA and Railroad Commission oversight. High humidity accelerates external corrosion, pushing demand for advanced coatings and real-time cathodic monitoring. Frequent hurricane exposure prompts operators to stage rapid-response repair teams, a logistical niche that contractors with storm-hardening playbooks effectively capture. Digital surveillance via aerial LiDAR and near-real-time SCADA updates enhances anomaly triage, embedding software subscriptions into every new maintenance award in the region.

Midwest states collectively command roughly 25.18% of the US oil and gas pipeline MRO market. Illinois hubs funnel Canadian crude southward, while Ohio’s core role in NGL supply to chemical clusters drives sustained compressor overhauls and metering-station upgrades. Winter freeze cycles induce thermal stress, justifying the installation of seasonal sleeves and pipe supports rated for sub-zero brittleness thresholds. Regulatory coordination between PHMSA and state public utility commissions influences inspection windows, favoring regional service providers who are fluent in both federal and state codes. Planned renewable-diesel conversions at certain refineries could amplify pipeline cleaning jobs to ensure contamination-free flow paths.

The Northeast accounts for nearly 19.74% of MRO outlays, but growth lags due to contentious permitting climates. Dense population corridors impose stringent class-location standards, increasing record-keeping rigor and dig verification frequencies. Appalachian shale gas continues to drive expansions, yet environmental litigation extends project horizons and raises insurance costs. Operators proactively integrate leak-detection fiber optics to appease regulators, which in turn opens up specialist service niches in fiber splicing and sensor calibration. The region’s hilly terrain complicates the sourcing of water for hydrostatic tests, promoting the adoption of inert-gas pressure testing as an alternative method.

Rocky Mountain and West Coast corridors split the remaining share. Colorado’s regulatory restructuring has increased baseline inspection cycles, while California’s carbon-reduction targets accelerate the decommissioning and repurposing of legacy lines toward hydrogen blends. Seismic resilience retrofits on the West Coast generate bespoke MRO scopes, including slip-lining and flexible joint installation. Mountainous topography drives the delivery of helicopter-borne equipment, a sub-service that commands premium rates while ensuring compliance in remote zones.

Competitive Landscape

The US oil and gas pipeline MRO market is moderately fragmented, with the five largest contractors capturing an estimated 28-30% combined share. Baker Hughes leverages its Panametrics sensor suite and Cordant software to lock in multi-year integrity management deals that bundle diagnostics with responsive repair crews. Oceaneering International, rooted in offshore robotics, now cross-sells ROV-deployed smart-pig retrieval and composite sleeve placement services, giving it an edge in deepwater assignments. MISTRAS Group differentiates itself with embedded acoustic-emission monitoring systems installed during overhauls, which shift revenue toward recurring data analytics subscriptions.

Consolidation momentum continues: ONEOK’s 2024 acquisition of EnLink Midstream enlarged a combined pipeline footprint exceeding 30,000 miles, which is now subject to network-wide maintenance harmonization—opportunities that integrated service houses are already pursuing. Technology entrants specializing in artificial-intelligence defect-classification algorithms form joint ventures with established mechanical contractors to penetrate operator preference lists. Barriers to entry remain high in composite repair, where ASME PCC-2 certification requires stringent performance proofs and audited quality manuals, effectively limiting competition to a dozen nationwide licensees.

Cybersecurity consultants are the newest competitive cohort, winning a share of OPEX that previously flowed exclusively to mechanical work. Firms offering turnkey compliance with TSA Security Directive Pipeline-2021-02 now bundle network hardening, anomaly detection, and incident-response playbooks into MRO contracts, creating cross-sell prospects for traditional service incumbents that partner rather than build capabilities in-house. Overall, price competition is intensifying in routine activities such as coating recoats and valve lube runs, whereas differentiated offerings in data analytics, deepwater robotics, and composite wraps maintain margin resilience.

United States Oil And Gas Pipeline Maintenance, Repair, And Overhaul (MRO) Industry Leaders

Oceaneering International, Inc.

Baker Hughes Company

Kinder Morgan Inc.

Aegion Corporation

T.D. Williamson Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: ONEOK closed its USD 4.3 billion takeover of EnLink Midstream, triggering large-scale asset-integration maintenance programs across Texas, Oklahoma, and Louisiana.

- September 2024: DT Midstream finalized a USD 1.2 billion purchase of three natural-gas systems, expanding Midwest mileage that will undergo integrity baseline assessments in 2025.

- August 2024: PHMSA moved the Mega Rule Engineering Critical Assessment deadline to Aug 2025, extending high-value inspection order books for specialty service firms.

- July 2024: Summit Midstream Partners acquired Tall Oak Midstream for USD 450 million, consolidating Permian gathering lines and standardizing maintenance KPIs.

United States Oil And Gas Pipeline Maintenance, Repair, And Overhaul (MRO) Market Report Scope

The United States oil and gas pipeline maintenance, repair, overhaul (MRO) market includes:

| Inspection and Monitoring |

| Maintenance |

| Repair and Rehabilitation |

| Overhaul and Replacement |

| Decommissioning |

| Gathering Lines |

| Transmission Lines |

| Distribution Lines |

| Onshore |

| Offshore |

| Upstream (E&P) |

| Midstream Operators |

| Downstream & Petrochemicals |

| By Service Type | Inspection and Monitoring |

| Maintenance | |

| Repair and Rehabilitation | |

| Overhaul and Replacement | |

| Decommissioning | |

| By Pipeline Type | Gathering Lines |

| Transmission Lines | |

| Distribution Lines | |

| By Location of Deployment | Onshore |

| Offshore | |

| By End-user Sector | Upstream (E&P) |

| Midstream Operators | |

| Downstream & Petrochemicals |

Key Questions Answered in the Report

How large is U.S. spending on pipeline maintenance today?

The US oil and gas pipeline MRO market size stood at USD 6.33 billion in 2026 and is projected to reach USD 8.07 billion by 2031.

Which service area grows fastest through 2031?

Maintenance services lead, expanding at a 5.62% CAGR as operators favor proactive, analytics-driven upkeep.

Why are transmission pipelines the biggest spending category?

They operate under high pressure across long distances, require sophisticated inspection tools, and face strict PHMSA oversight, resulting in 49.12% of 2025 outlays.

What role do federal grants play in future activity?

Programs such as PHMSA’s USD 196 million safety grants accelerate leak-prone pipe replacement and drive short-term MRO spend in distribution networks.

How does labor availability influence project timelines?

A looming retirement wave for certified technicians elevates wage costs and can delay specialty work, adding pressure to adopt automation and remote monitoring.

Page last updated on: