Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

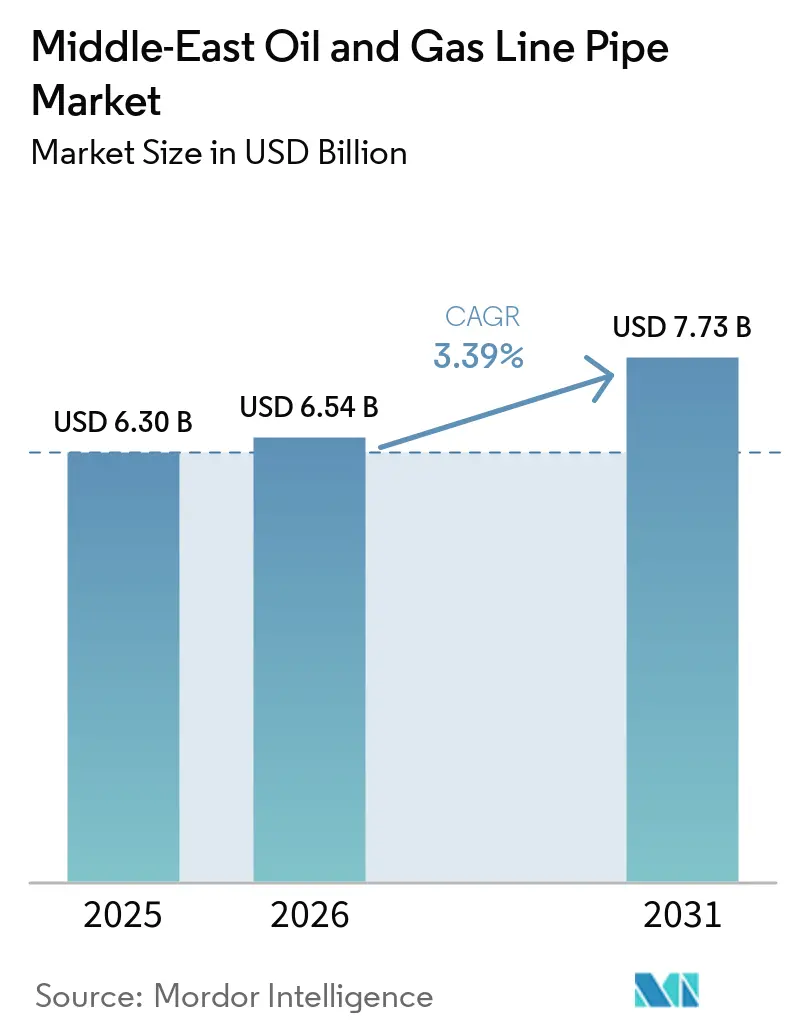

| Base Year Market Size (2025) | USD 6.30 Billion |

| Market Size (2026) | USD 6.54 Billion |

| Market Size (2031) | USD 7.73 Billion |

| Growth Rate (2026 - 2031) | 3.39% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle-East Oil And Gas Line Pipe Market Analysis by Mordor Intelligence

The Middle-East Oil And Gas Line Pipe Market size was valued at USD 6.30 billion in 2025 and is estimated to grow from USD 6.54 billion in 2026 to reach USD 7.73 billion by 2031, at a CAGR of 3.39% during the forecast period (2026-2031).

National oil companies are channeling capital toward gas transmission networks that secure domestic power supply and blue-hydrogen feedstock, even as crude export corridors remain vulnerable to oil-price swings. Cost-optimized welded pipe dominates large-diameter projects, while duplex and super-duplex alloys are gaining importance in sour-gas and hydrogen pilots.[1]ADNOC, “Hail and Ghasha Project Details,” adnoc.ae Localization schemes such as Saudi Arabia’s IKTVA and the UAE’s ICV tilt procurement toward regional mills with in-country facilities.[2]Argus Media, “SeAH Steel Clad Pipe Supply,” argusmedia.com Policy headwinds include the EU Carbon Border Adjustment Mechanism, which will raise delivered costs for Gulf steel makers exporting into Europe.[3]International Monetary Fund, “Impact of the EU Carbon Adjustment Mechanism,” imf.org

Key Report Takeaways

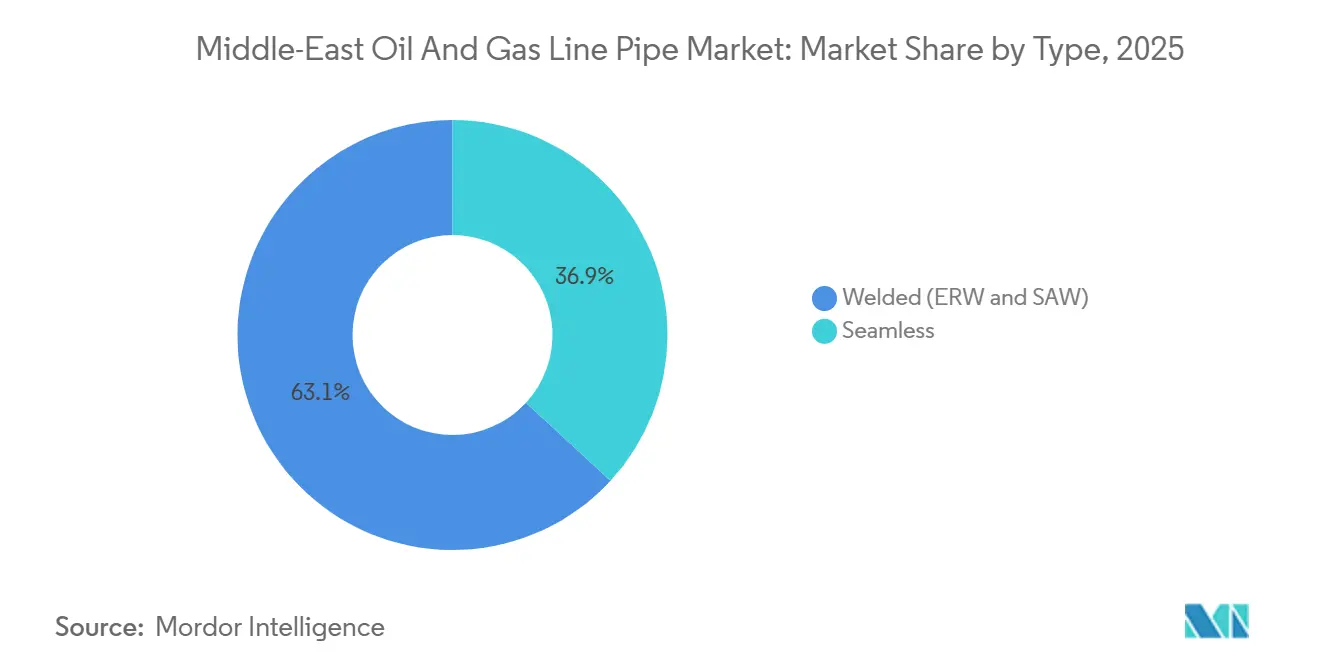

- By type, welded pipe led with a 63.15% share of the Middle-East oil and gas line pipe market in 2025 and is expected to expand at a 3.58% CAGR through 2031.

- By material, carbon steel accounted for a 64.88% share of the Middle East oil and gas line pipe market in 2025, while the duplex/super-duplex segment is projected to grow at a CAGR of 6.12% through 2031.

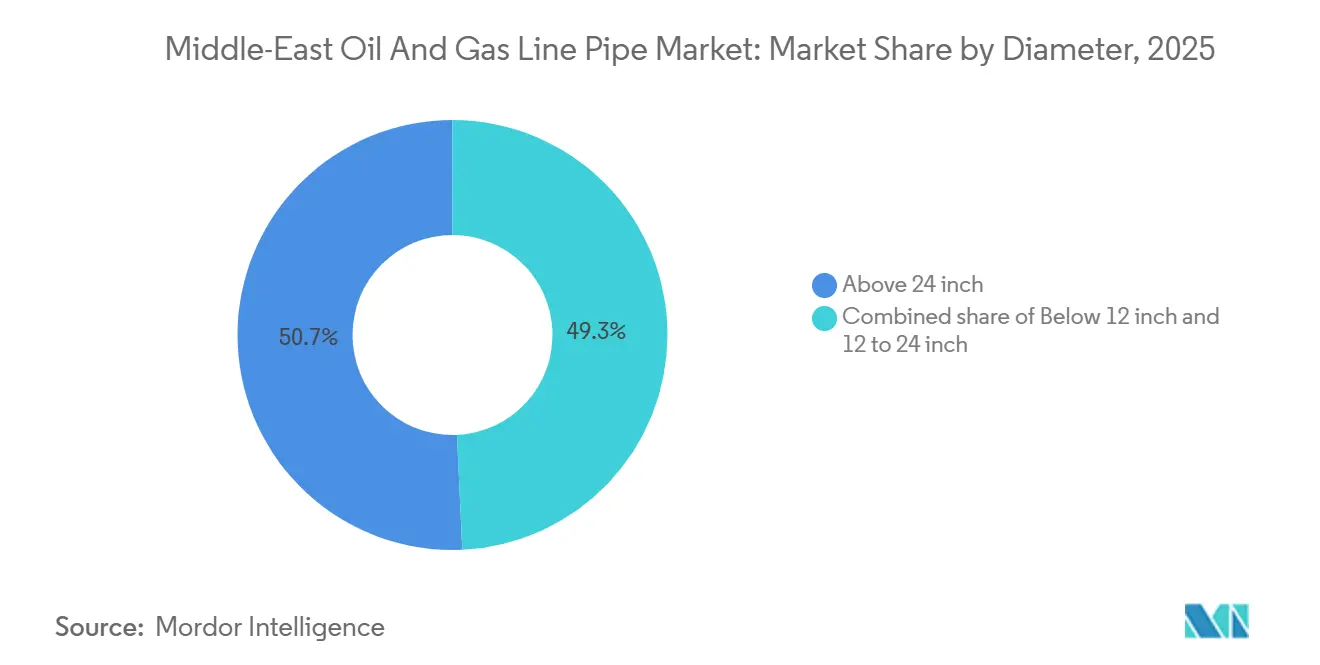

- By diameter, pipe above 24-inch outer diameter captured 50.72% of the 2025 Middle-East oil and gas line pipe market share and is projected to grow at a 4.16% CAGR.

- By application, transmission accounted for 57.44% of the 2025 market, outpacing all other applications and is expected to grow at a 4.44% CAGR to 2031.

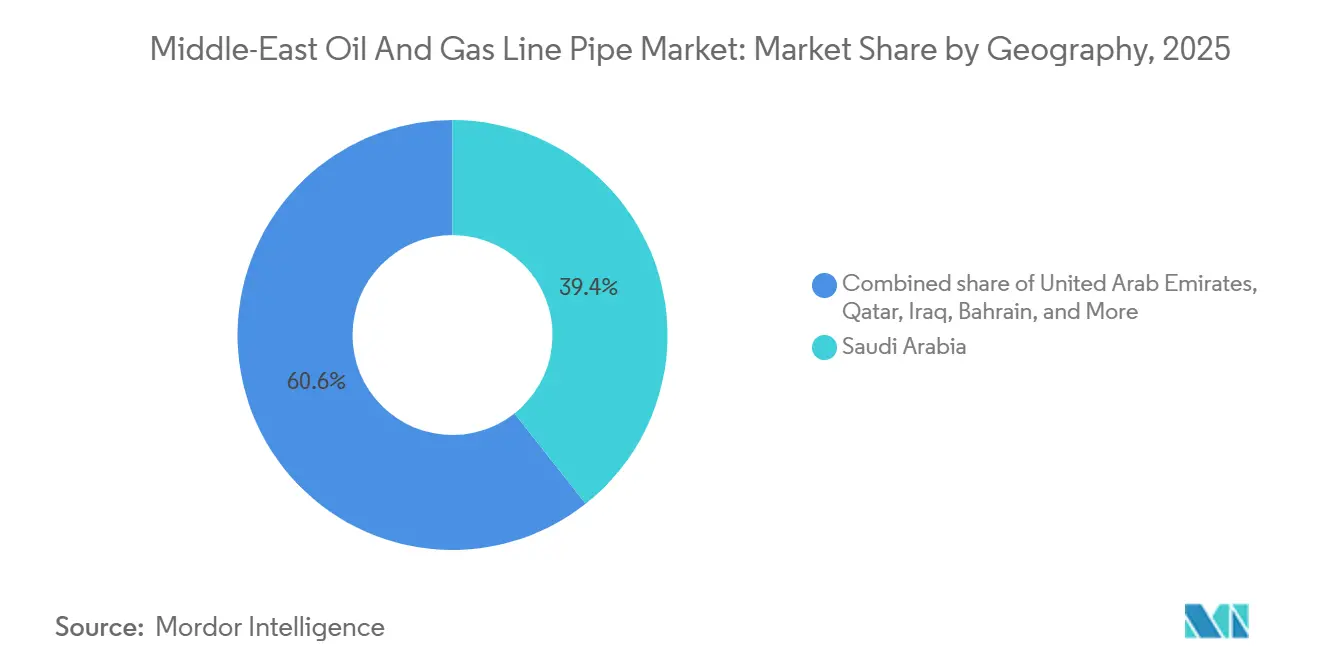

- By geography, Iraq is the fastest expanding geography at a 5.35% CAGR, whereas Saudi Arabia remained the largest market with 39.36% demand in 2025.

- Tenaris, Vallourec, Arabian Pipes, National Pipe Company, and Jindal SAW collectively controlled about 40% of 2025 revenues.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle-East Oil And Gas Line Pipe Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising upstream investment in Arabian Gulf offshore gas fields | +0.9% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Expansion of cross-border crude export trunk lines | +0.7% | Iraq, Saudi Arabia, Oman | Long term (≥ 4 years) |

| Aging pipeline network replacement demand | +0.6% | Saudi Arabia, UAE, Kuwait | Medium term (2-4 years) |

| Hydrogen-ready line-pipe pilots by ADNOC & Aramco | +0.4% | UAE, Saudi Arabia | Long term (≥ 4 years) |

| Localization mandates under IKTVA & ICV programs | +0.8% | Saudi Arabia, UAE | Short term (≤ 2 years) |

| GTL & blue-ammonia projects needing low-temperature alloys | +0.5% | Qatar, Oman, UAE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Upstream Investment in Arabian Gulf Offshore Gas Fields

ADNOC has earmarked USD 150 billion for 2026-2030, prioritizing offshore gas monetization, with Hail and Ghasha alone attracting USD 11 billion in financing to add 1.5 billion cubic feet per day of gas capacity. QatarEnergy’s North Field expansion will lift LNG capability to 126 million tons per year by 2028 and requires more than 500 kilometers of new offshore line pipe. Sour-gas environments drive demand for duplex and clad pipe with high pitting resistance, illustrated by SeAH Steel’s 14,000-ton delivery to Hail and Ghasha. Orders for premium OCTG from Nippon Steel underscore the link between gas growth and decarbonization infrastructure. Collectively, these programs secure long-dated steel demand and partially decouple pipeline activity from oil-price volatility.

Expansion of Cross-Border Crude Export Trunk Lines

Iraq’s USD 4.56 billion Basrah-Haditha line is sized for 2.25 million bpd and exemplifies renewed interest in multi-country corridors. Negotiations with Oman for a Duqm terminal would bypass the Strait of Hormuz and introduce 10 million barrels of storage. Saudi Arabia is studying a regional gas grid that would interconnect with the UAE and Kuwait. These megaprojects require API 5L X65 or X70 grades above 24 inches to reduce the number of pumping stations. Sanction risk in Iran and Iraq could lengthen decision cycles, but route-diversification economics continue to favor large-diameter steel over alternative modes.

Aging Pipeline Network Replacement Demand

More than 700 offshore structures in the region are candidates for retirement, and that figure may top 1,000 by 2038 at an estimated USD 30–50 billion cost. Kuwait Petroleum Corporation awarded USD 1.5 billion of replacement pipeline work in February 2026 to sustain its 4 million bpd production goal. Saudi Aramco’s Master Gas System Phase 3 involves 4,000 kilometers of new pipe to modernize infrastructure commissioned in the early 1980s. ADNOC is extending its ESTIDAMA network beyond 3,500 kilometers under USD 2.1 billion of contracts. Replacement cycles create a predictable backbone of demand regardless of new-field sanctioning trends.

Hydrogen-Ready Line-Pipe Pilots by ADNOC & Aramco

ADNOC’s H2GO and Aramco’s eREACT pilots evaluate steels resistant to hydrogen embrittlement, favoring duplex alloys and modified carbon steels with low sulfur and phosphorus. The UAE’s Supreme Steel now offers UNS S32760 locally, compliant with NACE MR0175, indicating early supply-chain adaptation. Oman plans a 400-kilometer green-hydrogen network that would introduce fresh demand for low-temperature pipe grades. If hydrogen blending exceeds 10 % of gas volume, sections of legacy carbon-steel transmission lines may require replacement or internal cladding. Pilot learnings will guide future material specifications across the Middle-East oil and gas line pipe industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil-price volatility postponing EPC awards | -0.5% | Global, with acute impact in Qatar, UAE | Short term (≤ 2 years) |

| Shift toward composite flexible pipe in shallow offshore | -0.3% | UAE, Oman, Egypt | Medium term (2-4 years) |

| Sanctions-driven funding limits in Iran & Iraq | -0.4% | Iran, Iraq | Medium term (2-4 years) |

| EU CBAM raising cost for GCC steel pipe exports | -0.2% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Oil-Price Volatility Postponing EPC Awards

Brent prices vacillated between USD 70 and USD 85 per barrel during 2025, prompting Qatar to defer Offshore Package 4 and forcing ADNOC to delay several gas awards. Aramco slowed second-half 2025 tendering to reassess capital priorities. In lower-visibility windows, national oil companies channel funds into short-cycle drilling rather than multi-year pipelines. Kuwait is exploring lease-leaseback financing up to USD 7 billion to mitigate price-cycle exposure. The restraint especially affects discretionary export projects, while domestic power-linked gas networks stay relatively insulated.

Shift Toward Composite Flexible Pipe in Shallow Offshore

Egypt’s West Bakr field replaced 25,000 meters of steel with Flexpipe HT, cutting installation time in half and costs by up to 40%. Flexible pipe also avoids cathodic-protection systems and tolerates dynamic fatigue. ADNOC and Aramco have begun controlled trials in satellite developments but have not yet placed large-scale orders. Composite solutions remain limited to depths under 200 meters and diameters below 10 inches, leaving trunk lines and high-pressure sour service solidly in steel’s domain. Nonetheless, margin pressure is mounting in the shallow-water segment of the Middle-East oil and gas line pipe market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Welded Pipe Maintains Cost Leadership

Welded pipe accounted for 63.15% of 2025 demand and will grow at a 3.58% CAGR as operators favor longitudinal submerged arc welded products for 52–56 inch gas lines. TenarisGPC’s LSAW mill in Jubail and East Pipes’ HSAW capacity expansion highlight supply-side confidence. Seamless pipe remains indispensable for high-pressure sour service; Jindal SAW and ArcelorMittal added 900,000 tons of regional seamless capacity scheduled for commissioning by 2029. Automated welding helped L&T Energy Hydrocarbon finish a 120-kilometer 56-inch project with only 0.6% field repairs, underscoring productivity gains.

The Middle-East oil and gas line pipe market size for welded products is expected to climb steadily as trunk-line projects advance, whereas seamless demand tracks drilling cycles and specialty alloy uptake. Welded pipe also benefits from localization mandates that reward regional mills meeting IKTVA or ICV scorecards, reinforcing its dominant market share position.

By Material: Duplex Alloys Show Rapid Uptake

Carbon steel retained a 64.88% share in 2025, given its cost advantage in sweet service, but duplex and super-duplex categories posted the highest growth at 6.12% CAGR. SeAH Steel’s 14,000-ton clad-pipe delivery and Tubacex’s USD 100 million CRA OCTG plant in Abu Dhabi affirm this trajectory. Hydrogen pilots and CO2 transport projects introduce new corrosion vectors that conventional grades cannot withstand.

Within the Middle-East oil and gas line pipe industry, duplex alloys will increasingly substitute for carbon steel in offshore gas and hydrogen infrastructure. The Middle-East oil and gas line pipe market share of carbon steel is therefore set to erode marginally, although absolute tonnage still rises alongside total network length.

By Diameter: Above 24 Inch Dominates Growth

Pipe above 24-inch outer diameter held 50.72% of 2025 revenue and is forecast to post a 4.16% CAGR through 2031. Master Gas System Package 8 and ADNOC’s ESTIDAMA call for 52-inch specifications to move large gas volumes efficiently. OQGN’s Fahud-Suhar award to Jindal SAW adds 193 kilometers of 42-inch line by 2027.

Large diameters drive the Middle-East oil and gas line pipe market size by weight because wall thickness scales with diameter and operating pressure. Smaller diameters below 12 inches continue to serve down-hole and distribution roles, yet contribute less value growth.

By Application: Transmission Secures Budget Priority

Transmission represented 57.44% of 2025 shipment volume and will expand at 4.44% CAGR as gas monetization climbs the policy agenda. Saudi Arabia’s USD 8.8 billion Master Gas System Phase 3 and Qatar’s North Field pipelines exemplify this tilt. Carbon-capture transport projects such as Aramco’s 9 million t CO₂ hub in Jubail add another demand layer.

Gathering and down-hole casing fluctuate with drilling intensity, explaining their slower growth compared with transmission. Still, the Middle-East oil and gas line pipe market share of transmission implies a stable base-load demand insulated from near-term oil-price gyrations.

Geography Analysis

Saudi Arabia contributed 39.36% of 2025 sales, propelled by Master Gas System Phase 3 and the Jafurah unconventional program. Aramco reached 70% local content under IKTVA and signed USD 11 billion of long-term procurement agreements in February 2026. Arabian Pipes collected more than SAR 550 million in orders between 2024 and 2025.

The UAE follows, anchored by ADNOC’s ESTIDAMA expansion and Hail and Ghasha sour-gas project. The ICV framework has recycled AED 242 billion into the domestic economy since 2018. Seamless and clad-pipe capacity is scaling through Jindal SAW, SeAH, and Tubacex investments.

Iraq exhibits the fastest trajectory at a 5.35% CAGR through 2031, yet funding pressure from sanctions and negotiations on route options could delay execution. Kuwait’s USD 1.5 billion replacement program and Oman’s 4,623 kilometer gas-grid build support steady regional demand. Bahrain and Iran remain smaller players, the latter constrained by U.S. Treasury advisories on illicit funding flows.[4]FinCEN, “Advisory on Iranian Petroleum,” fincen.gov

Competitive Landscape

The competitive field is moderately concentrated. The five largest suppliers control about 40–45% of revenue, producing a market concentration score of 6. Localization policies reward mills with domestic plants, prompting global groups to form joint ventures rather than export finished pipe. Welspun’s 350,000 t LSAW project in Dammam and Interpipe’s 250,000 t seamless venture in Abu Dhabi illustrate the trend.

Technology upgrades revolve around automated welding, digital traceability, and alloy design. L&T’s 0.6% repair rate on a 56-inch Saudi gas line demonstrates cost savings from automation. Composite-pipe specialists are emerging challengers in shallow offshore work but have yet to penetrate high-pressure trunk lines. Incumbents respond by offering turnkey coating, logistics, and field-welding services to preserve margin in the Middle-East oil and gas line pipe market.

Middle-East Oil And Gas Line Pipe Industry Leaders

Arabian Pipes Company

Rezayat Group

Vallourec S.A.

Tenaris SA

Jindal SAW Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Kuwait plans a USD 7 billion pipeline infrastructure deal, opening its national pipeline network to foreign investors to finance midstream expansion. The initiative aims to ease budget pressure, expand capacity toward 4 mb/d, and reduce transport bottlenecks, strengthening the Middle East’s broader pipeline investment trend.

- September 2025: ONEOK opened an open season for its proposed Sun Belt Connector, a 440-mile multi-product line. Although U.S.-based, the project illustrates global pipeline-market expansion trends driven by refinery shifts and demand growth, relevant to Middle East operators monitoring line-pipe demand cycles.

- August 2025: Nabors sold Quail Tools, a major downhole tubular supplier, to Superior Energy for $600 million, improving financial flexibility and consolidating tubular supply capabilities. While U.S.-focused, the deal affects Middle East line-pipe activity through Nabors’ retained tubular running services in the region.

- May 2025: I Squared, MPLX, and Enbridge agreed to acquire interests in the Matterhorn Express natural-gas pipeline (2.5 Bcf/d capacity). Though U.S.-centered, the deal reflects continued investment appetite in large-diameter transmission systems, informing Middle Eastern line-pipe market dynamics through global capital flows.

Middle-East Oil And Gas Line Pipe Market Report Scope

Line pipe is a form of steel pipe that is used to move goods across the country via pipelines. Petroleum, natural gas, oil, and water can all be transported via line pipes. Line pipes are connected to form a pipeline.

The market is segmented by type and geography. By type, the market is segmented into seamless and welded. By material, the market is divided into carbon steel, alloy steel, stainless/CRA, and duplex/super-duplex. By diameter, the market is segmented into below 12 inches, 12 to 24 inches, and above 24 inches. By application, the market is divided into transmission (onshore and offshore), down-hole casing and tubing, oil and gas gathering, and water/gas injection. The report also covers the market size and forecasts for the Middle-East Oil and Gas Line Pipe Market across the major countries in the region. For each segment, market sizing and forecasts have been done based on revenue (USD billion).

By Type

| Seamless |

| Welded (ERW and SAW) |

By Material

| Carbon Steel |

| Alloy Steel |

| Stainless/CRA |

| Duplex/Super-Duplex |

By Diameter

| Below 12 inch |

| 12 to 24 inch |

| Above 24 inch |

By Application

| Transmission (Onshore and Offshore) |

| Down-hole Casing and Tubing |

| Oil and Gas Gathering |

| Water/Gas Injection |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| Iraq |

| Iran |

| Rest of Middle East |

| By Type | Seamless |

| Welded (ERW and SAW) | |

| By Material | Carbon Steel |

| Alloy Steel | |

| Stainless/CRA | |

| Duplex/Super-Duplex | |

| By Diameter | Below 12 inch |

| 12 to 24 inch | |

| Above 24 inch | |

| By Application | Transmission (Onshore and Offshore) |

| Down-hole Casing and Tubing | |

| Oil and Gas Gathering | |

| Water/Gas Injection | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Iraq | |

| Iran | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the projected value of Middle-East oil and gas line pipe demand by 2031?

The market is forecast to reach USD 7.73 billion by 2031.

Which diameter class adds the most value over 2026-2031?

Pipe above 24 inch, supported by cross-border gas and crude trunk lines, advances at a 4.16% CAGR.

Why are duplex and super-duplex alloys gaining share?

Sour-gas fields and hydrogen pilot lines need enhanced corrosion and embrittlement resistance that these alloys provide.

How do localization mandates influence supplier selection?

Programs such as IKTVA and ICV award higher scores to bidders with in-country manufacturing, steering orders toward regional mills.

What is the main restraint on near-term project sanctioning?

Oil-price volatility has postponed several EPC awards, especially for discretionary export pipelines.

Are composite flexible pipes a long-term substitute for steel lines?

They offer cost and installation benefits in shallow water under 200 m depth but are not viable for high-pressure or large-diameter transmission.

Page last updated on: