Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

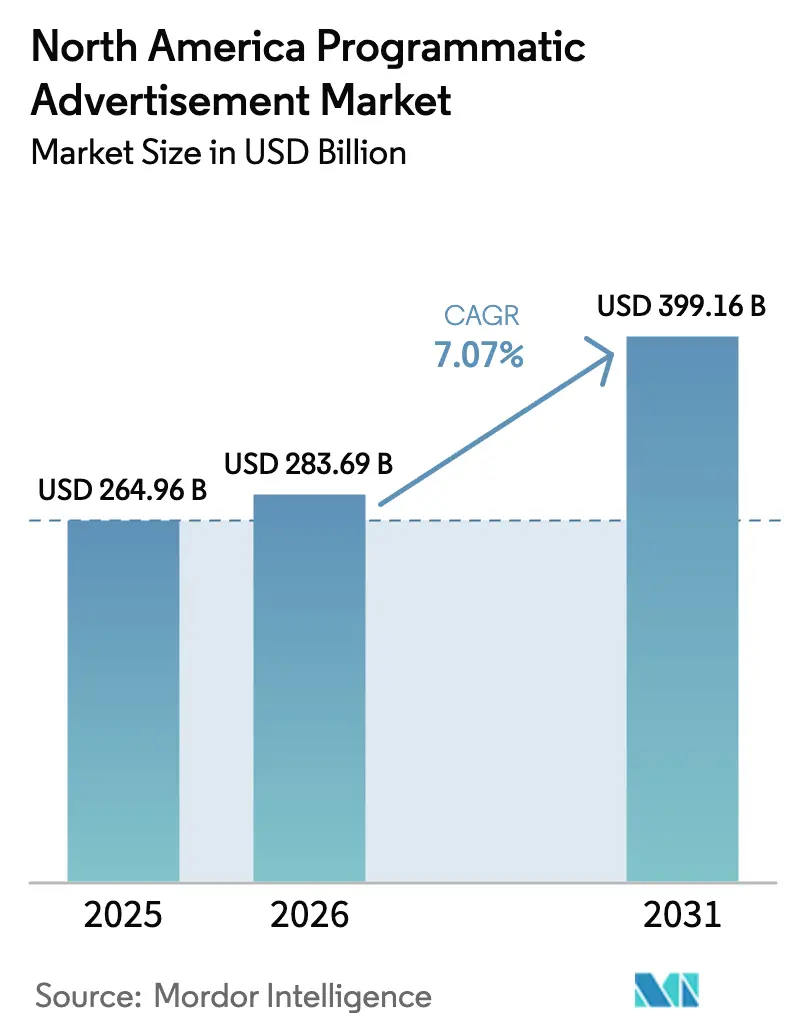

| Base Year Market Size (2025) | USD 264.96 Billion |

| Market Size (2026) | USD 283.69 Billion |

| Market Size (2031) | USD 399.16 Billion |

| Growth Rate (2026 - 2031) | 7.07% CAGR |

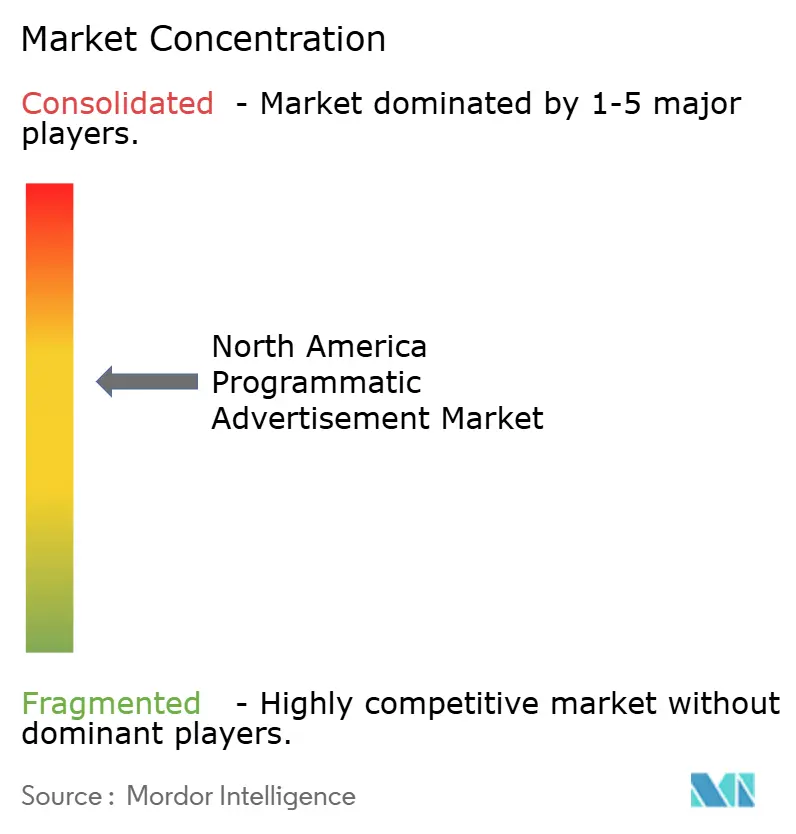

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Programmatic Advertisement Market Analysis by Mordor Intelligence

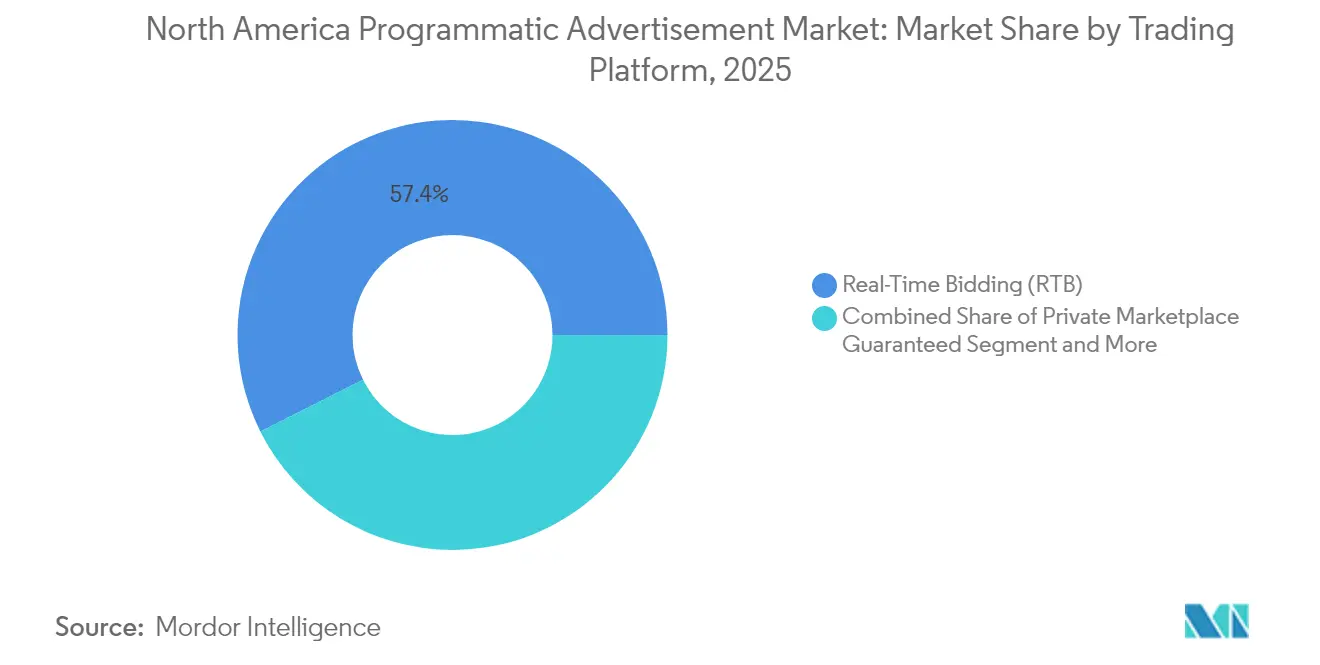

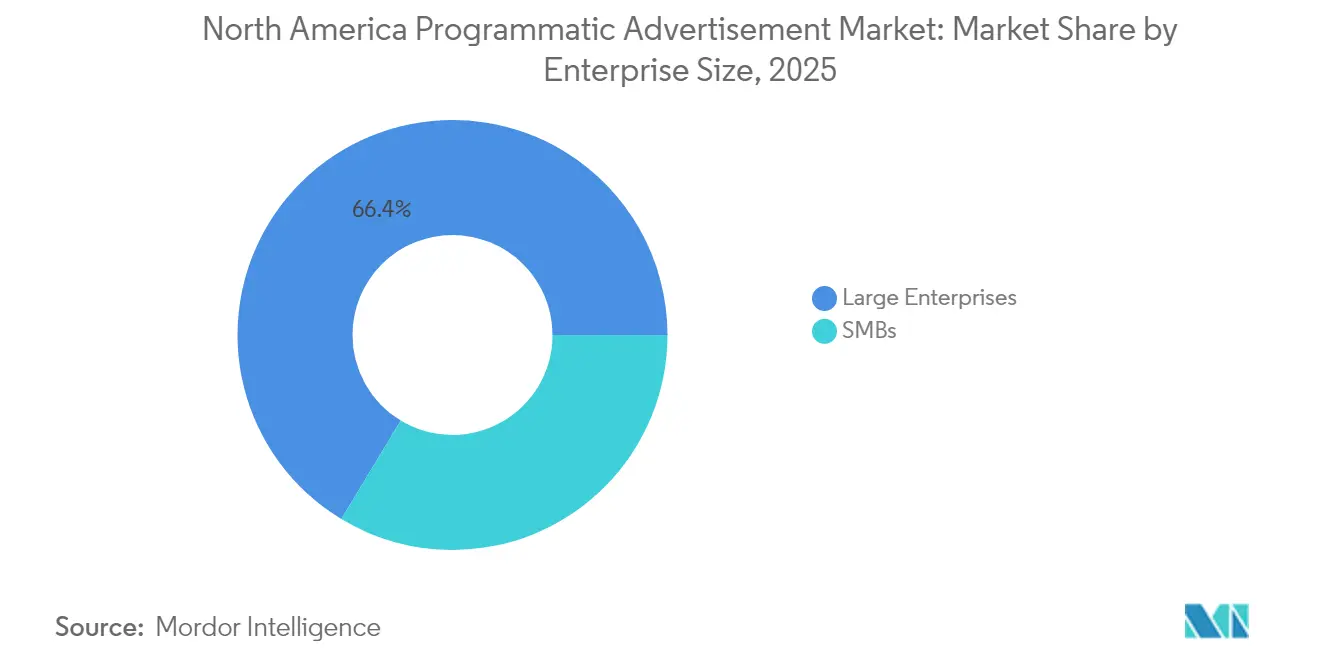

The North America programmatic advertisement market size was valued at USD 264.96 billion in 2025 and estimated to grow from USD 283.69 billion in 2026 to reach USD 399.16 billion by 2031, at a CAGR of 7.07% during the forecast period (2026-2031). Real-time data signals, artificial intelligence, and machine learning now guide automated bidding, turning programmatic from a cost-saving tool into a growth engine that maximizes revenue across screens.[1]Adobe For Business Team, “What Is Programmatic Advertising?,” Adobe, adobe.com Cookie deprecation has spurred a USD 150 billion wave of retail media networks that cultivate first-party data advantages. Connected TV is the fastest-growing medium, supported by identity solutions such as Unified ID 2.0 that help buyers measure households at scale. Real-time bidding (RTB) still leads with 58% of spend, while private marketplace (PMP) guaranteed deals expand briskly as advertisers seek brand-safe, premium inventory. Large enterprises secure 67.1% of regional spend, yet small and medium businesses (SMBs) show the fastest acceleration thanks to self-service interfaces that use AI to boost return on ad spend.

Key Report Takeaways

- By trading platform, real-time bidding led with 57.40% of the North America programmatic advertisement market share in 2025; private marketplace guaranteed transactions are projected to grow at a 9.36% CAGR through 2031.

- By advertising media, mobile display captured 45.85% revenue share in 2025, while connected TV is advancing at a 12.21% CAGR to 2031.

- By enterprise size, large enterprises held 66.35% of the North America programmatic advertisement market size in 2025 and SMBs are expanding at an 8.77% CAGR through 2031.

- By end-user industry, retail and e-commerce accounted for 24.15% share of the North America programmatic advertisement market size in 2025; healthcare and pharmaceuticals are growing at a 10.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Programmatic Advertisement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging CTV ad-spend led by U.S. streaming platforms | +1.80% | United States, spillover to Canada | Medium term (2-4 years) |

| Retail media networks’ first-party data advantage | +1.50% | North America, concentrated in urban markets | Short term (≤ 2 years) |

| AI-optimised real-time bidding enhancing ROAS for SMBs | +1.20% | North America, tech-forward metros | Medium term (2-4 years) |

| De-precation of third-party cookies accelerating PMPs | +0.90% | Global, early implementation in North America | Short term (≤ 2 years) |

| 5G roll-out boosting mobile video impressions | +0.70% | Major North American metropolitan areas | Long term (≥ 4 years) |

| Telco-led cloud gaming bundles stimulating ARPDAU | +0.50% | High-speed coverage areas across North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging CTV Ad-Spend Led by U.S. Streaming Platforms

Connected TV investment reached USD 21.45 billion in 2024 after a 16.2% jump tied to political campaigns and major sports broadcasts. Programmatic execution now accounts for 75% of CTV transactions as Disney, Roku, and Amazon expand real-time exchanges. Disney’s decision to open its exchange to Amazon DSP combines contextual and purchase data, improving performance metrics for cross-screen campaigns. Advertiser confidence is evident, with 95% planning to sustain or lift CTV budgets in 2025. The Trade Desk’s Ventura operating system aims to streamline the CTV supply chain, promising fewer intermediaries and better measurement

Retail Media Networks’ First-Party Data Advantage

Retail media has become the third-largest channel worldwide and is forecast to exceed USD 233.89 billion in 2027. Amazon holds 75% of U.S. retail media ad revenue, but Walmart Connect grew 60% in 2024 as buyers diversify. Their closed-loop attribution links ad exposure to purchase outcomes, a capability traditional programmatic exchanges cannot match in a cookieless. Walmart’s exploration of acquiring Vizio and its offsite push shows how retailers now compete head-on with demand-side platforms. The result is a structural rebalancing that pushes the North America programmatic advertisement market toward deeper data partnerships to defend share.

AI-Optimised Real-Time Bidding Enhancing ROAS for SMBs

AI-driven campaigns deliver 76% higher ROI and cut customer acquisition costs by 30% versus legacy tactics. The Trade Desk’s Kokai provides predictive clearing and KPI scoring at the bid level, simplifying decision-making for SMBs. PubMatic and GroupM deploy AI-generated cohort modeling that respects privacy without sacrificing scale MiQ’s Sigma ingests 700 trillion digital signals, illustrating how machine learning converts reactive auctions into predictive marketing systems. These improvements help SMBs tap advanced optimization once reserved for large advertisers, broadening the spending base within the North America programmatic advertisement market.

Deprecation of Third-Party Cookies Accelerating Adoption of PMPs

Google’s tests show revenue dropped 34% for Ad Manager without cookies, yet Privacy Sandbox APIs trimmed declines to 20% . Advertisers now rely on PMP deals that pair first-party data with direct publisher supply, boosting brand safety and measurement. The Trade Desk’s Deal Desk simplifies PMP execution, addressing the 90% failure rate of legacy Deal ID. Microsoft’s embrace of Privacy Sandbox APIs shows the industry prefers common standards over fragmented proprietary IDs. Elevated PMP pricing is offset by gains in verification, driving more spend into curated, high-quality exchanges inside the North America programmatic advertisement market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SPO fees compressing publisher margins | -1.10% | North America, high impact on mid-tier sites | Short term (≤ 2 years) |

| Fragmented CTV identity graphs limiting reach | -0.80% | United States and Canada | Medium term (2-4 years) |

| Data-privacy litigation risk (CCPA and Bill-64) | -0.60% | California and Quebec | Medium term (2-4 years) |

| Ad-fraud inflation in open exchanges | -0.40% | North America, lower-tier inventory | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

SPO Fees Compressing Publisher Margins

Complex supply chains allow intermediaries to capture up to 98% of a bid, leaving premium publishers with only 2% of spend in extreme cases. Fee variability often fails to correlate with content quality, straining sustainability for niche publishers. Buyers concentrate demand through preferred paths, further reducing competition and widening fee spreads. As revenues shrink, publishers pivot to direct sales and PMPs, accelerating consolidation within the North America programmatic advertisement market. Smaller outlets risk displacement if infrastructure cost reductions do not keep pace with rising take rates.

Fragmented CTV Identity Graphs Limiting Reach Extension

Each major streaming platform maintains its own identity graph, preventing marketers from managing frequency across Samsung, Roku, Fire TV, and Google TV ecosystems. Reliance on household-level IP data leads to duplication and wasted impressions, undermining the premium paid for CTV inventory Advertisers aiming to complement linear TV cannot accurately measure incremental reach, reducing campaign efficiency. Industry guidelines released by the IAB seek to unify metrics, but inconsistent adoption stalls progress. Until cross-platform identity becomes routine, the North America programmatic advertisement market must tolerate elevated frequency capping errors in CTV budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Trading Platform: RTB Dominance Faces PMP Challenge

Real-time bidding contributed 57.40% of spend in 2025, underscoring its central role in the North America programmatic advertisement market. Private marketplace guaranteed deals are rising at 9.36% CAGR as brands seek verified, high-quality environments that mitigate fraud risk. The shift elevates data quality and viewability over pure cost efficiency, pressing open exchanges to refine inventory vetting. Automated guaranteed agreements serve advertisers that need both flexibility and certainty, while unreserved fixed-rate transactions give publishers predictable yields during auction volatility. This blend of models positions PMPs as the premium growth engine even as RTB retains unmatched scale for long-tail inventory.

The migration to PMPs stems from advertisers’ perception that brand safety, measurement, and transparency now outweigh bid-price savings. OpenX pioneered real-time guaranteed to fuse RTB speed with the certainty of guaranteed inventory. That hybrid design reflects a market need to reconcile efficiency with accountability. As a result, the North America programmatic advertisement market continues to perfect trading mechanics that combine scale, speed, and premium content stewardship.

By Advertising Media: Mobile Display Leadership Meets CTV Acceleration

Mobile display retained 45.85% share in 2025 because 5G coverage supports rich video and interactive formats that engage users on the go. Connected TV, while smaller, posts the fastest 12.21% CAGR thanks to programmatic infrastructure maturity across streaming platforms. Desktop display, digital audio, and digital out-of-home (DOOH) complement omnichannel plans by filling contextual gaps in home, commute, and public spaces. Programmatic video ad spend reached USD 19.93 billion, with 87.1% of mobile video already transacted through automated auctions. Integration of 5G and AI-driven creative makes immersive experiences viable, expanding the North America programmatic advertisement market into gaming and social ecosystems.

T-Mobile’s USD 600 million purchase of DOOH specialist Vistar Media confirms telecom giants’ ambitions in screen-agnostic advertising. The deal connects location data, 5G, and a network of 1.1 million screens, underscoring DOOH’s revival. As convergence proceeds, planners allocate budgets fluidly across mobile, CTV, and DOOH to maximize incremental reach and frequency. These trends cement the North America programmatic advertisement market as a fully omnichannel discipline.

By Enterprise Size: Large Enterprise Stability Enables SMB Innovation

Large companies delivered 66.35% of 2025 spend, underpinning infrastructure investments across the North America programmatic advertisement market. Their budgets fund data platforms, attribution models, and verification layers that set standards later adopted elsewhere. SMBs, though smaller, expand at 8.77% CAGR because self-service consoles and AI automation lower operational barriers. The Trade Desk’s integration of retail data from Instacart and Ocado equips smaller advertisers with product-level targeting once exclusive to enterprise partnerships.

PubMatic reports 25% higher eCPMs for publishers working with curated SMB demand, showing that emerging advertisers can deliver quality revenue. These dynamics foster a feedback loop where enterprise spend funds innovation that then benefits SMBs, broadening the North America programmatic advertisement market’s advertiser base and stabilizing growth.

By End-User Industry: Retail Leadership Drives Healthcare Expansion

Retail and e-commerce held 24.15% share in 2025 due to deterministic data that links ad exposure to sales, producing superior ROI metrics. Healthcare and pharmaceuticals lead growth at a 10.05% CAGR, benefiting from privacy-compliant measurement frameworks and the surge in telemedicine. Automotive, BFSI, media and entertainment, and travel round out demand by leveraging location targeting, privacy-safe modeling, and immersive formats. Pharmacy chains’ investment in on-site media hubs illustrates how healthcare overlaps with retail media, widening first-party data pools.

IAB notes that healthcare spend increases as direct-to-consumer pharma marketing seeks precision while meeting stringent consent rules. The confluence of regulatory rigor and data-driven targeting makes healthcare a proving ground for privacy-preserving innovation. Lessons learned here will echo across other verticals, enriching the North America programmatic advertisement market’s compliance toolset.

Geography Analysis

The United States commanded 81.75% of the North America programmatic advertisement market in 2025, supported by advanced infrastructure, early adoption, and a privacy framework that pairs innovation with accountability. High 5G penetration—projected to reach 90% of mobile subscriptions by 2029—enables sophisticated mobile and CTV executions. California’s Consumer Privacy Act, along with federal sandbox pilots, provides a laboratory for cookieless experimentation that shapes global standards.

Canada accounts for 9.05% of spending and enjoys tailwinds from regulatory alignment with U.S. privacy norms, vast broadband coverage, and publisher adoption of programmatic sales models. Quebec’s Law 25 initially created compliance hurdles but also accelerated contextual targeting innovations suited to bilingual audiences. Canadian platforms thus refine solutions for cultural nuance that later scale southward, enriching the North America programmatic advertisement market overall.

Mexico, while representing a smaller slice, shows high future potential as rising digital penetration and cross-border commerce drive advertisers to automated buying. Automotive, consumer goods, and tourism brands already use programmatic to address bilingual and bicultural audiences across the region. Continued infrastructure investment and regulatory modernization will position Mexico as the next high-growth node within the regional ecosystem.

Regulatory Landscape

North America programmatic advertising operates under tightening privacy, consumer-protection, and competition scrutiny across federal and state regimes, with elevated focus on data used for targeted advertising and real-time bidding. In the United States, the Federal Trade Commission (FTC) continues to frame online advertising and marketing practices around deception, unfairness, and substantiation expectations, increasing compliance exposure for data sourcing, audience modeling, and measurement claims across DSPs, SSPs, and retail media networks.

Policy activity during 2025-2026 added uncertainty and compliance workstreams for ad tech and advertisers. In March 2026, the IAB updated its Multi-State Privacy Agreement (MSPA) to refine obligations for first parties and downstream participants supporting state privacy law compliance. Congress also introduced proposals such as S. 4211 (Consumer Data Privacy and Security Act of 2026) to establish a federal privacy framework, and S. 3774 to address fraudulent or deceptive commercial advertisements on online platforms. Sector-specific proposals also appeared, including the May 2026 GAME Act targeting targeted sports-gambling advertising to minors, reinforcing the need for stronger consent, age-gating, and audience governance in programmatic supply paths.

Competitive Landscape

The market’s consolidation accelerated in 2024 with USD 14.8 billion worth of mergers, including Omnicom’s USD 13.3 billion acquisition of IPG and Mediaocean’s USD 500 million purchase of Innovid. These deals merge creative, data, and media activation into unified stacks that serve omnichannel strategies. Retail media networks and streaming platforms intensify competition by forging direct advertiser ties, pressuring traditional demand-side platforms to deepen data partnerships or risk share erosion.

Strategy now revolves around vertical integration. The Trade Desk’s Ventura aims to control the CTV stack from smart-TV operating system to demand-side execution, reducing intermediaries and improving transparency. [2]The Trade Desk, “The Trade Desk Announces Ventura,” thetradedesk.comTelecommunications entrants such as T-Mobile leverage location intelligence and 5G to expand into DOOH and advanced mobile, widening the field of rivals. [3] T-Mobile US, “T-Mobile to Acquire Vistar Media,” t-mobile.comTechnology differentiation centers on machine learning engines that process trillions of signals per day, enabling predictive optimization that trims waste and lifts outcomes across the North America programmatic advertisement market.

Emerging disruptors include retail giants offering off-site programmatic buys, independent CTV platforms consolidating niche streamers, and AI-first creative optimization firms. As privacy and transparency become non-negotiable, platforms that blend deterministic data, predictive modeling, and fraud mitigation will gain strategic advantage. Competitive intensity thus remains high even as ownership concentration increases, indicating a dynamic yet consolidating North America programmatic advertisement market.

North America Programmatic Advertisement Industry Leaders

Alphabet Inc.

The Trade Desk Inc.

PubMatic Inc.

Xandr (Microsoft Corp.)

Amazon Advertising (Amazon .com Inc.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Auction transparency and standardization are a near-term whitespace for platforms and intermediaries as buyers push harder on fee visibility, auction mechanics, and supply-path governance. In January 2026, the Media Rating Council (MRC) issued final Digital Advertising Auction Transparency Standards covering disclosure expectations across display, CTV, and retail media auctions. This creates a concrete implementation opportunity for verification, reporting, and workflow tooling that DSPs, SSPs, and publishers can adopt to differentiate on trust and accountability.

Retail media and CTV data interoperability is another active opportunity area, particularly where first-party purchase data can be applied beyond on-site placements into programmatic CTV and omnichannel planning. In May 2026, Walmart Connect launched Connect Select, a curated programmatic CTV marketplace with partners including Magnite, PubMatic, FreeWheel, and Index Exchange, signaling demand for retailer-led, privacy-managed offsite activation. The March 2026 IAB MSPA update also reinforces a compliance-driven push toward standardized contractual controls and auditable data processing across multi-state privacy requirements, supporting investment in consent management, privacy-safe measurement, and curated deal infrastructure that reduces exposure versus open-exchange buying.

Recent Industry Developments

- April 2026: IAB Tech Lab formed the Programmatic Governance Council (April 21, 2026) with founding members including Amazon Ads, The Trade Desk, Omnicom, WPP, Dentsu, and Disney. The council targets standard-setting for emerging programmatic operating models, including AI-driven and agent-led transactions, which directly affects interoperability and governance across buy-side and sell-side workflows in North America.

- June 2025: The Trade Desk added Instacart and Ocado as SKU-level retail data sellers for self-serve advertisers. The move broadened access to deterministic retail signals for programmatic optimization, helping smaller advertisers use commerce data without negotiating bespoke enterprise data partnerships.

- June 2024: Omnicom announced an agreement to acquire Interpublic Group (IPG) in a USD 13.3 billion deal. The consolidation tightened integration between creative, data, and media activation, increasing pressure on independent ad tech to prove differentiated performance and transparency as large holding companies build more unified buying stacks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers spending on automated buying and selling of digital ad inventory across North America, where bids, deals, and delivery are executed through programmatic platforms and workflows. We size only the value tied to programmatic transactions across common digital media types.

Scope exclusions: We exclude offline advertising, non-ad marketing services, and pure creative production fees that are not directly linked to programmatic media buying.

Segmentation Overview

- By Trading Platform

- Real-Time Bidding (RTB)

- Private Marketplace Guaranteed

- Automated Guaranteed

- Unreserved Fixed-Rate

- By Advertising Media

- Mobile Display

- Desktop Display

- Connected TV (CTV)

- Digital Audio

- Digital Out-of-Home (DOOH)

- By Enterprise Size

- Large Enterprises

- Small and Mid-sized Businesses (SMBs)

- By End-user Industry

- Retail and E-commerce

- Automotive

- BFSI

- Media and Entertainment

- Healthcare and Pharma

- Travel and Hospitality

- By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with grounding the addressable ad economy and the rules that shape it. We lean on public sources such as the US Census Bureau, Bureau of Economic Analysis, and Federal Communications Commission for baseline digital activity and media signals, and we also review IAB publications and North America advertising association releases for definitions and ecosystem context.

After that, numbers are cross-checked using company filings, earnings call transcripts, investor presentations, and reputable business press coverage that discuss pricing, auction dynamics, and demand shifts. We also use paid subscriptions for company financials and intelligence, news and financials, patent databases, and tender tracking when it helps validate platform investments and buying patterns. These examples are illustrative rather than exhaustive, and many other public and proprietary sources are also referred to for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focuses on translating broad digital ad signals into programmatic-specific assumptions that hold up in real buying cycles. We speak with demand-side and supply-side stakeholders, agencies, publishers, ad operations teams, and category marketers across the United States, Canada, and Mexico to validate deal mix, pricing direction, and budget allocation shifts.

Feedback is used to fill gaps that desk sources do not fully explain, such as the share of spend in real-time bidding versus private marketplaces and automated guaranteed pipelines, and how measurement and identity changes are affecting buying choices.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 20% | |

| Mid tier: 47% | Functional/Unit leaders: 29% | |

| Smaller Players: 21% | Managers: 51% |

Market-Sizing & Forecasting

The core model starts from a top-down build where digital advertising activity is reconstructed into a programmatic demand pool by applying trading and media adoption rates across North America. These rates are then mapped to spend by trading platform types and major digital media, before being reconciled with country-level patterns.

To keep the totals realistic, we corroborate the outputs with selective bottom-up checks such as sampled pricing by format, informed volume proxies (like impression supply trends and inventory availability), and channel checks on how budgets are split between open auction and curated deals. In practice, the most influential inputs include RTB versus private marketplace and automated guaranteed mix, average pricing direction by media type (including connected TV versus display), identity and measurement readiness after cookie changes, enterprise size buying patterns, and vertical-level demand shifts (for example retail and e-commerce seasonality versus travel recovery).

For forecasting, scenario analysis is used around a central case, since pricing and deal mix can change quickly when inventory tightens or measurement rules shift. Assumptions are reviewed with primary respondents to keep variables like CPM movement, deal share, and media-type growth aligned with what buyers and sellers are actually planning. Where bottom-up signals are incomplete, gaps are handled by applying conservative ranges and then tightening them using cross-country consistency checks and platform-level benchmarks.

Data Validation & Update Cycle

Outputs are validated through triangulation across multiple independent checks, including country splits, media mix sanity checks, and implied pricing movement versus observed buying behavior. When an outlier shows up, the driver is traced back to the assumption level, then reviewed again through follow-up outreach or additional document checks before it is allowed into the final model.

A multi-step analyst review is used so the logic, math, and scope alignment are verified separately, and only then is the estimate signed off. Reports are refreshed annually, with interim updates when a material event impacts pricing or trading structure, and a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's North America Programmatic Advertisement Market Size Compared With Other Published Estimates

Published market values for programmatic advertising in North America often diverge because the same ad dollars can be counted under different transaction definitions, media boundaries, and timing choices. Differences also come from how each publisher treats pricing movements, deal mix changes, and what gets included when adjacent ad tech services are bundled into the number.

When quarterly pricing moves and mix shifts are refreshed close to the currency conversion timing (instead of being carried forward from an older snapshot), the annual spend total can change materially, and that update cadence plus re-contacts to validate CPM direction is the reason Mordor Intelligence often lands at a different 2025 value versus other sources.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 264.96 B (2025) | |

| Industry Association A | USD 245.00 B (2025) | Uses a narrower programmatic definition that leans toward open auction and excludes parts of private marketplace and automated guaranteed flows, which can reduce the counted spend in higher-priced inventory. |

| Trade Journal B | USD 305.00 B (2025) | Rolls some adjacent ad tech and managed-service fees into the spend total and applies a more aggressive pricing progression for high-growth media such as connected TV, which lifts the estimate. |

Looking across the table, the gap is mostly explained by what is treated as in-scope programmatic spend and how pricing is carried through the year when media mix is shifting. By keeping the steps traceable to deal types, media-level pricing direction, and country checks, we aim to provide a balanced number that can be repeated and stress-tested.

Key Questions Answered in the Report

What is driving growth in the North America programmatic advertisement market?

Advances in AI bidding, the rise of retail media first-party data, and surging CTV budgets are key forces pushing the market’s 7.07% CAGR.

How will cookie deprecation influence programmatic buying?

As third-party cookies disappear, advertisers are shifting spend into private marketplace deals that rely on publisher or retailer first-party data for targeting and measurement.

Which advertising medium is expanding the fastest?

Connected TV leads with a 12.21% CAGR as streaming platforms deepen programmatic infrastructure and identity solutions.

Why are small and medium businesses adopting programmatic now?

Self-service dashboards and AI optimisation reduce complexity and cost, enabling SMBs to achieve higher ROI without large internal trading teams.

Which industry vertical shows the highest forecast growth?

Healthcare and pharmaceuticals are forecast to grow at a 10.05% CAGR due to privacy-compliant targeting that supports telemedicine and direct-to-consumer drug marketing.

What challenges could restrain market expansion?

High supply-path optimisation fees, fragmented CTV identity graphs, and evolving privacy litigation in California and Quebec threaten to slow growth if left unresolved.

Page last updated on: