Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

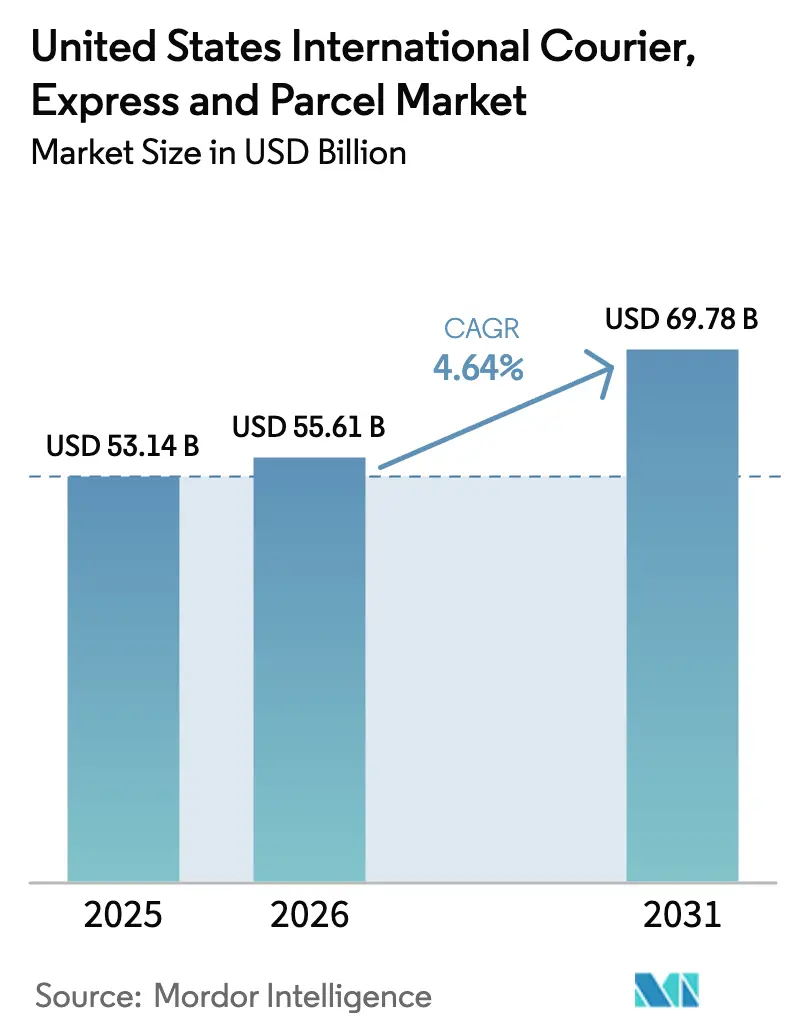

| Base Year Market Size (2025) | USD 53.14 Billion |

| Market Size (2026) | USD 55.61 Billion |

| Market Size (2031) | USD 69.78 Billion |

| Growth Rate (2026 - 2031) | 4.64% CAGR |

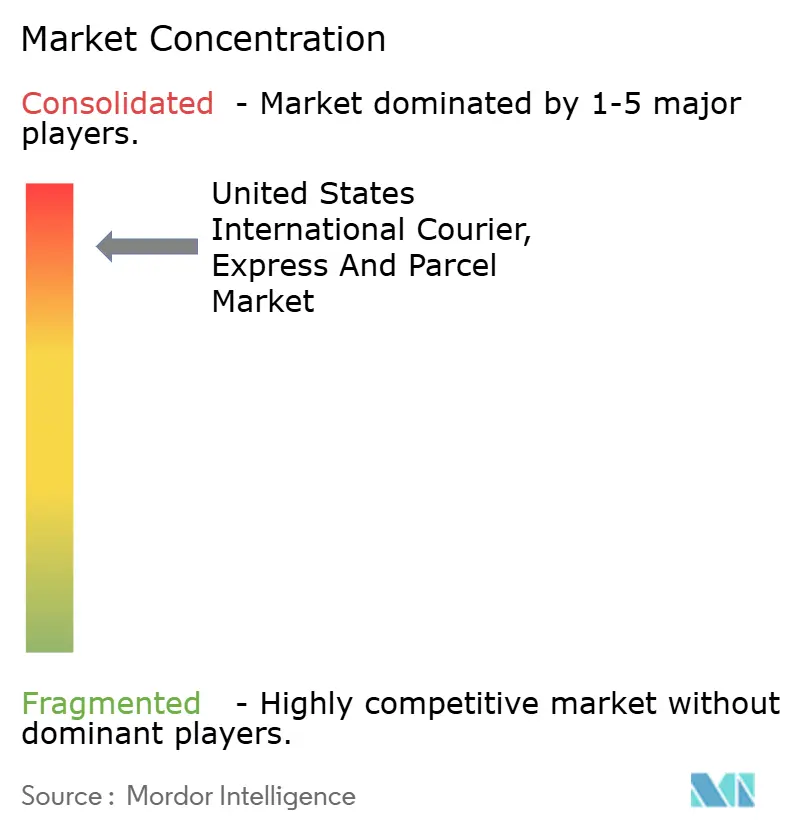

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States International Courier, Express And Parcel Market Analysis by Mordor Intelligence

The United States International Courier, Express And Parcel Market size in 2026 is estimated at USD 55.61 billion, growing from 2025 value of USD 53.14 billion with 2031 projections showing USD 69.78 billion, growing at 4.64% CAGR over 2026-2031.

E-commerce-driven demand for rapid cross-border deliveries, new data-intensive customs rules, and the steady recovery of wide-body belly capacity collectively redefine network design and pricing power. Integrators continue to prioritize technological upgrades that cut clearance time and enhance shipment visibility, while smaller operators pursue niche verticals to offset rising compliance costs. Meanwhile, regulatory attention on the USD 800 de minimis threshold is re-shaping cost structures for ultra-fast fashion platforms and sparking debate over the duty-free treatment of Section 301 goods. Airport slot constraints, especially at Newark Liberty International, amplify the premium placed on operational agility as carriers juggle alternative routings to protect time-definite service guarantees.

Key Report Takeaways

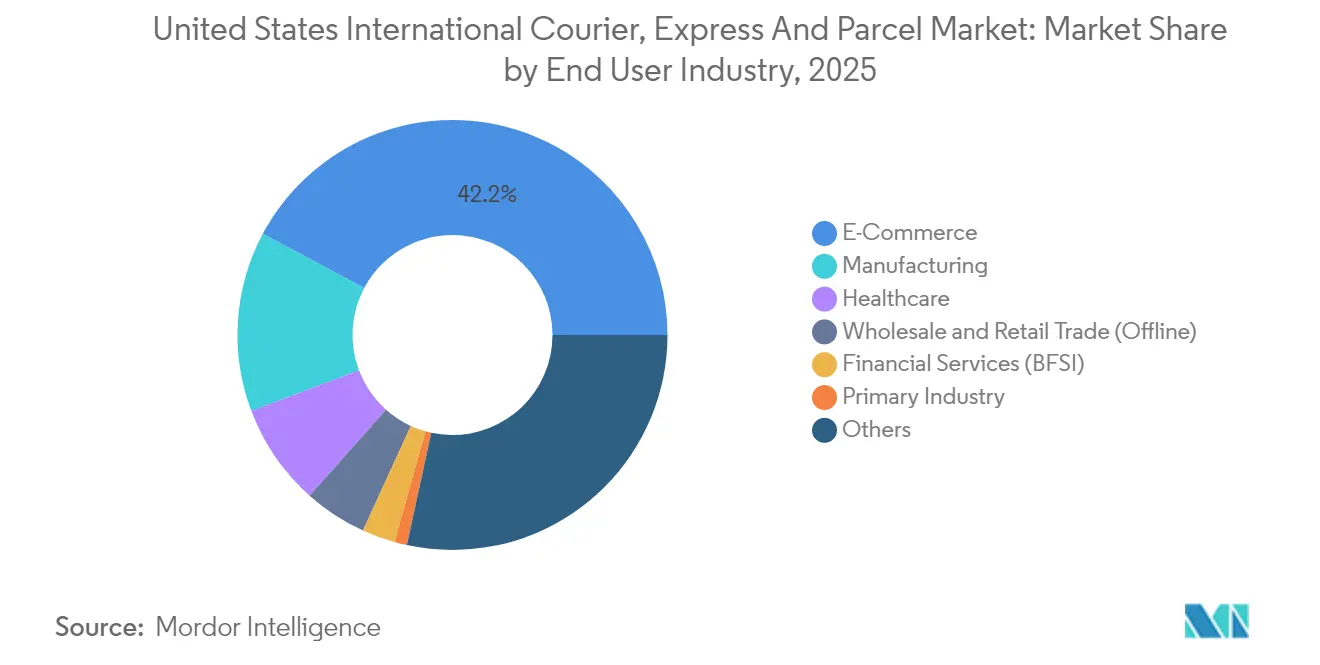

- By end user industry, E-commerce retained a 42.20% revenue share in 2025; wholesale and retail trade (offline) is on track for the highest CAGR at 5.31% between 2026-2031.

- By speed of delivery, express services led with 67.05% of the United States international courier market share in 2025 and are projected to record the fastest segment growth at a 5.88% CAGR between 2026-2031.

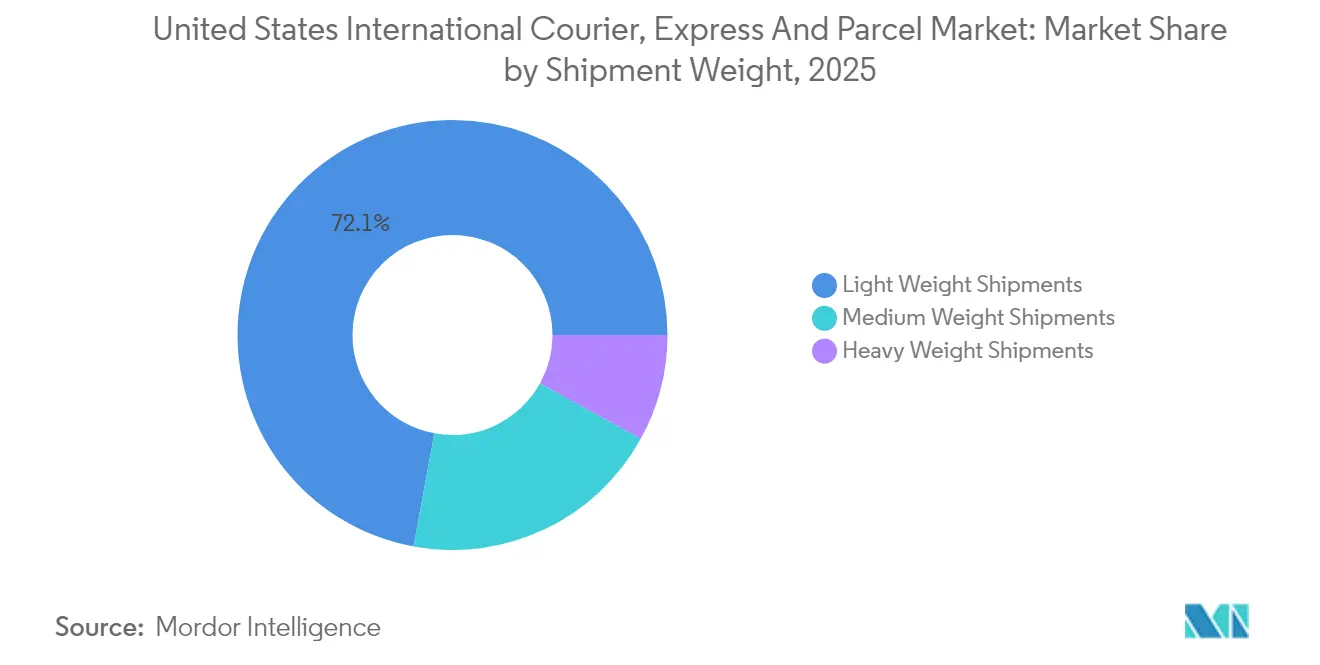

- By shipment weight, light-weight shipments accounted for 72.10% share of the United States international courier market size in 2025, while the medium-weight shipments are projected to expand at a 5.74% CAGR between 2026-2031.

- By model, business-to-business (B2B) shipments held 50.30% revenue share in 2025, whereas business-to-consumer (B2C) flows will outpace at a 4.87% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States International Courier, Express And Parcel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| USMCA-driven growth in SME parcel flows to Canada and Mexico | +0.8% | North America | Medium term (2-4 years) |

| Cross-border DTC imports surge, influenced by USD 800 de-minimis threshold | +1.2% | Asia-Pacific to US | Short term (≤2 years) |

| Ultra-fast fashion platforms like Temu and Shein propel surge in less than 2 kg parcel shipments | +0.9% | China-to-US corridor | Short term (≤2 years) |

| Paperless trade and ACE/ITDS automation reducing clearance time | +0.4% | Major US gateways | Medium term (2-4 years) |

| Wide-body belly capacity recovery cutting international air-freight rates | +0.3% | Transcontinental routes | Short term (≤2 years) |

| ESG-focused contracts favor carbon-accounted green-lane express offerings | +0.2% | North America and EU | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

USMCA-Driven Growth in SME Parcel Flows to Canada and Mexico

CBP regulations that took effect in March 2025 simplified origin certification, enabling blanket declarations that cover multiple shipments and lowering paperwork for frequent traders[1]U.S. Customs and Border Protection, “Electronic Advance Data Requirements for International Mail Shipments,” cbp.gov . Small and medium sellers quickly expanded cross-border catalogs, lifting demand for fast, trackable parcel services. Integrators use enhanced data feeds to pre-clear consignments and shorten door-to-door transit by up to a full day on select lanes. Automakers that reorganized component flows within the USMCA bloc have also turned to express couriers for critical parts, elevating average revenue per shipment. Competitive differentiation now hinges on real-time visibility tools that reassure SMEs about customs compliance.

Cross-Border DTC Imports Surge, Influenced by USD 800 De-Minimis Threshold

CBP processed more than 1 billion de-minimis parcels in 2024, a six-fold jump since 2016. Proposed rules to deny Section 301 goods duty-free status and mandate richer data elements may generate up to USD 7.8 billion in new duties yet could tilt business toward carriers with robust compliance infrastructure. Platforms shipping straight from China ramped up pre-advice filings and SKU-level harmonized codes, pushing courier IT spend higher. Larger integrators view the heavier documentation load as a competitive moat that squeezes smaller rivals. The looming change also nudges online sellers to explore near-shore inventory models, fostering two-way trade within the Americas.

Ultra-Fast Fashion Platforms Propel Surge in Less Than 2 kg Parcel Shipments

Tech-enabled brands like Shein and Temu now dominate fast‐fashion import volumes, routinely dispatching less than 2 kg packages that bypass traditional distribution centers. Their data-rich order management systems feed directly into courier booking APIs, turning round-the-clock order drops into near-continuous uplift demand. Integrators rebalance aircraft mix toward narrow-body feeders to accommodate the skewed weight profile and increase sortation headcount at West Coast gateways. Although pending tariff changes threaten the existing model, platform agility and influencer-led micro-collections support sustained shipment frequency.

Paperless Trade and CE/ITDS Automation Reducing Clearance Time

Full electronic manifesting inside CBP’s ACE platform, covering all modes by 2025, slashes documentation errors and accelerates PGA risk assessments[2]Federal Aviation Administration, “Order Limiting Scheduled Operations at Newark Liberty International Airport,” govinfo.gov . Digital container shipping association analyses show e-bills of lading can shave USD 6.5 billion in annual costs, benefits that cascade into the express parcel ecosystem through shared data standards[3]Digital Container Shipping Association, “The Case for Electronic Bills of Lading,” dcsa.org. Couriers leverage the same data pipes to preload entry summaries and achieve less than 2-hour average release windows at key airports, freeing line-haul capacity for additional rotations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CBP advanced electronic data AED mandate raising compliance costs | -0.6% | All inbound US lanes | Short term (≤2 years) |

| Gateway airport congestion and slot constraints impacting time-definite SLAs | -0.4% | Major US hubs | Medium term (2-4 years) |

| Integrator peak surcharges and jet-fuel volatility compressing SME margins | -0.3% | High-volume corridors | Short term (≤2 years) |

| Return and dispute rates surge due to gaps in destination market postal services | -0.2% | Selected developing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

CBP Advanced Electronic Data Mandate Raising Compliance Costs

Enhanced ACAS requirements obligate carriers to transmit 100% shipment data before wheels-up, driving multi-million-dollar platform upgrades. Penalties for late or inaccurate filings intensify operational risk, especially for smaller couriers with fragmented agent networks. Integrators amortize investment over higher shipment density, widening a cost gap that accelerates consolidation. Parallel USPS inbound mail rules reinforce a shift toward private-sector handlers able to guarantee data integrity.

Gateway Airport Congestion and Slot Constraints Impacting Time-Definite SLAs

Newark Liberty capped movements at 28 per hour during ongoing works through 2025, forcing carriers to re-time wide-body arrivals and build regional truck-air shuttles. Similar slot stewardship programs at JFK and LAX tighten peak-hour flexibility. These constraints boost the strategic value of secondary gateways in Tennessee and Indiana, although ground line-haul distances add cost and erode some express transit advantages. Carriers continue to lobby the FAA for seasonal slot flexibility tied to ecommerce peaks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Offline Retailers Accelerate Digital Sourcing

E-commerce shipments captured 42.20% share in 2025, a figure that grows more modestly as penetration plateaus in affluent zip codes. Merchandise categories diversify beyond electronics into beauty, nutraceuticals, and hobby items, each with unique compliance documents that elevate the expertise premium for couriers. Manufacturing retains second position, benefiting from multi-regional component sourcing that underpins just-in-sequence assembly lines. Temperature-controlled pharmaceuticals spur investment in small active-container fleets fitted with IoT sensors that communicate directly with ACE portals.

Wholesale and retail trade (offline) posts the fastest 5.31% CAGR (2026-2031) as big-box store operators digitize supplier portals and run smaller, more frequent international restocks. Their pivot tightens delivery windows, incentivizing contract clauses that penalize late freight and elevate network reliability. BFSI reliance on physical documents declines in absolute terms, but courier spending per shipment rises as firms choose secure chain-of-custody services to protect sensitive records from cyber risk. Ancillary industries—ranging from aerospace to luxury goods—continue outsourcing critical-item logistics, extending the United States international courier market’s breadth across the real economy.

By Speed of Delivery: Express Services Extend Market Lead

Express services generated 67.05% of the United States international courier market revenue in 2025 as cross-border merchants emphasized checkout promises that mirror domestic standards. Demand elasticity favors premium transit, enabling operators to introduce Saturday cut-offs and late-night pick-ups. The segment’s 5.88% CAGR between 2026-2031 outpaces historical growth, reflecting continued cross-border marketplace expansion and corporate inventory shifts toward near-real-time replenishment. Non-express offerings still carry substantial volume but confront customer migration toward ocean-plus-last-mile hybrids on heavier lanes. FedEx’s Network 2.0 co-locations illustrate how integrators blend express and deferred parcels within a single service envelope, optimizing sort window utilization. Capacity rationalization on medium-haul lanes allows providers to re-deploy aircraft toward Asia-US trunk routes where density rewards higher-priced time guarantees.

Competitive positioning inside the express bracket is moving away from pure speed toward data-rich experience. Carriers embed customs status notifications into merchant dashboards, simplifying customer service by cutting “where-is-my-parcel” queries. The end result is a sharper value proposition that protects yields even as fuel indices fluctuate. Non-express players experiment with value-added evening deliveries and carbon-offset bundles but face difficulty matching the network depth of top-tier integrators. As US-Mexico e-commerce matures, regional express specialists leverage cross-dock hubs at Laredo and El Paso to shorten line-haul and divert volume from coastal air gateways.

By Shipment Weight: Medium Weight Shipments Gain Momentum

Light weight shipments maintained 72.10% of the United States international courier market size in 2025, anchored by consumer gadgets and apparel. Yet the medium weight shipments show the strongest 5.74% CAGR (2026-2031), driven by consolidated consumer orders and inventory top-ups for omnichannel retailers. Sellers combine multiple SKUs into one box to mitigate potential de minimis reform risk, nudging average declared weight higher. Couriers respond with dynamic pricing ladders that reward incremental kilos and defend margins on lighter tiers. Ultra-fast fashion’s emphasis on micro-drops still keeps sub-2 kg density at unprecedented levels, prompting investment in small-package sorters and mobile unload crews at airport warehouses.

Heavy weight shipments remain niche but critical for spare parts and medical-device emergencies where speed trumps mode economics. Airlines reinstating pre-pandemic wide-body frequencies offer discounted freight rates that nibble at courier yield, pushing operators to develop bundling strategies such as timed retrieval, specialized crating, or in-field technician dispatch. The diversity in weight mix encourages network planners to re-engineer cut-off times by lane, giving medium-weight flows priority during afternoon uplifts when volumetric imbalance is lowest.

By Model: Business-to-Consumer (B2C) Momentum Remains Strong

Business-to-business (B2B) consignments still hold 50.30% of market revenue, yet the business-to-consumer (B2C) lane’s 4.87% CAGR (2026-2031) signals persistent rebalancing. Marketplaces integrate artificial-intelligence-driven duty calculators that remove buyer uncertainty, stimulating higher ticket values and heavier multicategory baskets. Couriers earn incremental margin through API-based landed-cost solutions that ensure up-front transparency. The healthcare-focused UPS–Andlauer deal illustrates a counter-trend play: expanding specialized B2B verticals where regulatory oversight and temperature assurance support premium yields.

Consumer-to-consumer (C2C) traffic stays comparatively small; however, social-commerce influencers occasionally trigger bursts that test network elasticity. Operators experiment with locker pickup at destination to lower residential delivery touches and mitigate failed-delivery costs endemic to C2C parcels. Over time, the integration of B2B and B2C flows onto unified aircraft networks promises higher asset utilization, but data-segmentation by model remains a must for customs governance and customer analytics.

Geography Analysis

North American corridors, buoyed by USMCA reforms, are the first to benefit from simplified documentation, driving an uptick in SME-driven two-day services between the Midwest and central Mexico. The region’s lane mix strengthens secondary airports such as Monterrey and Calgary, spreading volumes away from legacy hubs. On Asia-Pacific routes, notably China-US traffic, proposed de-minimis rule revisions create tariff uncertainty that motivates some sellers to pre-position inventory in bonded US warehousing. Gateways on the West Coast absorb this shift yet confront berth and intermodal constraints that compel carriers to revise cut-off times and move partial volumes through Dallas/Fort Worth or Phoenix for onward trucking to coastal distribution centers.

Transatlantic flows remain steady, supported by strong US consumer appetite for European luxury goods and EU demand for tech components. Slot caps at Newark Liberty, JFK, and London Heathrow, however, inject volatility into uplift planning. Express operators increasingly book belly space on evening passenger departures to hedge against morning slot shortages. Intra-Americas trade, particularly perishables and apparel moving from Central America, grows in relevance as brands near-shore production to diversify beyond East Asia. Regulatory realignment in Mexico, where a 19% tax now applies to low-value e-commerce imports from non-FTA nations, alters route selection; couriers reroute via Laredo ground crossings to leverage US pre-clearance processes before southbound final mile.

Within the United States, geographic dispersion of e-commerce demand favors multi-node sort-center footprints. Eastern seaboard congestion encourages integrators to beef up Cincinnati, Louisville, and Greensboro operations, granting faster turnarounds on Europe-origin parcels. Midwest air hub expansion caters to growing automotive and industrial component traffic linked to reshoring. Western gateways like Ontario, California, pick up Asia-origin e-commerce surges but must contend with environmental curfews that cap nighttime sorts. Together, these regional adaptations ensure the United States’ international courier market maintains resilience amid fluctuating global trade currents.

Competitive Landscape

Consolidation defines the strategic backdrop as DSV’s USD 15.78 billion purchase of DB Schenker vaults the Danish group to the top of global freight forwarder rankings[4]DSV, “DSV to Acquire DB Schenker,” dsv.com. Scale empowers the new entity to negotiate better interline rates and invest in unified visibility stacks that integrate courier, forwarding, and contract-logistics workflows. Incumbent integrators respond with targeted vertical plays; UPS’s pending Andlauer takeover reinforces its position in temperature-controlled healthcare, a segment less vulnerable to price commoditization. FedEx accelerates Network 2.0 site mergers to squeeze USD 2 billion in annual efficiencies, funneling savings into its FDX Commerce platform that promises merchants inventory, checkout, and last-mile orchestration in one subscription.

Digital entrants leverage platform economics rather than asset heft. Several e-commerce marketplaces negotiate bulk block-space agreements directly with airlines, then outsource last-mile to regional couriers, fragmenting the traditional integrator monopoly. Yet high regulatory thresholds, particularly for advanced electronic data (AED) compliance, limit how far asset-light models can penetrate without partnering established operators. Private-label retailers such as Amazon continue to expand cross-border air capacity but still rely on third-party customs brokers for statutory filings, preserving a role for legacy couriers.

Price volatility in jet fuel and the seasonal peak surcharge cycle intensify margin pressure on SMEs, nudging them toward multi-carrier shipping software that brokers real-time rates. Carriers counter by bundling returns management and carbon accounting to deepen account stickiness. Investment focus converges on artificial intelligence for demand forecasting, warehouse robotics for small-parcel sortation, and blockchain pilots that tie trade documents to immutable ledgers. The competitive field increasingly rewards integrated data-physical hybrids capable of meeting regulators’ appetite for granular shipment intelligence while sustaining speed and reliability.

United States International Courier, Express And Parcel Industry Leaders

FedEx

United Parcel Service of America, Inc. (UPS)

DHL Group

United States Postal Service (USPS)

SF Express (KEX-SF, KEX Express US LLC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: UPS announced an agreement to acquire Andlauer Healthcare Group for CAD 2.2 billion (USD 1.6 billion), adding 3 million ft² of temperature-controlled space across Canada.

- March 2025: FedEx expanded Network 2.0 to eight more cities and closed six redundant ship centers as part of a USD 350 million cost program.

- February 2025: TFI International abandoned its plan to shift its corporate domicile to the United States, even though nearly 70% of its business is already south of the border, after management concluded that the move less beneficial than initially expected.

- April 2024: UPS replaced FedEx as the U.S. Postal Service’s primary air cargo provider, shifting nearly USD 2 billion in annual postal uplift spend.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study frames the United States international courier, express, and parcel (CEP) market as all revenue generated from cross-border shipments weighing up to 70 kg that originate in, or are destined for, the US and are handled by express or parcel operators through air, road, rail, or combined modes. Services covered span B2B, B2C, and C2C transactions and include timed express, deferred parcel, and return flows. According to Mordor Intelligence, domestic-only deliveries, postal letter mail, and freight consignments above the 70 kg threshold fall outside this scope.

Scope exclusion: purely domestic courier movements are not sized in this study.

Segmentation Overview

- Speed of Delivery

- Express

- By Route

- Inter-Region

- Intra-Region

- By Route

- Non-Express

- Express

- Shipment Weight

- Heavy Weight Shipments

- Light Weight Shipments

- Medium Weight Shipments

- End User Industry

- E-Commerce

- Financial Services (BFSI)

- Healthcare

- Manufacturing

- Primary Industry

- Wholesale and Retail Trade (Offline)

- Others

- Model

- Business-to-Business (B2B)

- Business-to-Consumer (B2C)

- Consumer-to-Consumer (C2C)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed parcel integrators, third-party logistics managers, customs brokers, and e-commerce merchants across coastal gateways and inland hubs. These conversations clarified cross-border service shares, typical surcharge structures, and emerging demand pockets, allowing us to validate secondary patterns and adjust assumptions where volume data were sparse.

Desk Research

We gathered macro inputs from publicly available tier-1 sources such as the US Census Bureau's International Trade data, Bureau of Economic Analysis trade statistics, UN Comtrade shipment records, Universal Postal Union parcel tallies, and e-commerce sales from the US Department of Commerce. Company 10-Ks, investor decks, and industry association notes (for example, the Airforwarders Association) provided operator level clues on average selling prices and parcel mix. Subscription tools from D&B Hoovers and Dow Jones Factiva enriched the competitive picture. This list is indicative; many additional references were consulted for cross-checks and context.

Market-Sizing & Forecasting

We adopted a top-down build that reconstructs international parcel flows from production and trade data, then layers penetration rates for e-commerce and industrial exports. Results are corroborated with selective bottom-up operator roll-ups and sampled ASP-times-volume checks. Key variables feeding the model include outbound merchandise export value, cross-border e-commerce spend, average parcels per online order, fuel surcharges, and currency movements. Forecasts rely on multivariate regression that links parcel volumes to real GDP, online retail growth, and export value; scenario analysis around fuel costs tempers the outlook. Gaps in operator disclosures are bridged with normalized yield curves derived from primary interviews.

Data Validation & Update Cycle

Outputs undergo variance scanning against independent parcel revenue indices; any anomaly prompts a senior review before sign-off. Reports refresh annually, and interim updates are triggered by material events such as new trade pacts or carrier rate hikes. A final analyst pass right before publication ensures clients receive the latest view.

Why Mordor's US International CEP Baseline Earns Trust

Published estimates often diverge because each firm slices the market differently and adopts its own refresh rhythm.

Key gap drivers include whether domestic flows are bundled with international, how mixed-weight shipments are treated, currency conversion points, and the cadence at which price surcharges are rebased. Mordor's model isolates only cross-border parcels, applies weight-specific ASP ladders validated with operators, and is refreshed every twelve months, which curbs legacy bias.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 53.14 B (2025) | Mordor Intelligence | - |

| USD 136.0 B (2024) | Global Consultancy A | Combines domestic and international flows, uses static ASPs |

| USD 183.0 B (2024) | Market Insights B | Includes heavy freight and same-day local services, annualizes 2023 operator revenues without forecast calibration |

| USD 197.9 B (2023) | Industry Statistics C | Revenue figure for all parcel shipping; lacks segmentation or forecast model |

The comparison shows that once domestic parcels, heavy freight, and ancillary services are stripped out, Mordor's disciplined scope selection and yearly update cadence deliver a balanced, transparent baseline that decision-makers can trace back to clearly defined variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the United States international courier market?

The market stands at USD 55.61 billion in 2026 and is projected to reach USD 69.78 billion by 2031.

Which segment is growing fastest by speed of delivery?

Express services are advancing at a 5.88% CAGR (2026-2031) as merchants pay premiums for time-definite cross-border delivery.

How does the USD 800 de-minimis rule affect couriers?

It fuels high parcel volumes but may raise compliance complexity and duty exposure if CBP’s proposed exclusions for Section 301 goods take effect.

Why are medium-weight parcels gaining traction?

Consolidated multi-item orders and just-in-time inventory strategies push more shipments into the >5 kg to ≤31.5 kg band, which is expanding at a 5.74% CAGR (2026-2031).

What impact do airport slot caps have on service reliability?

Restrictions at hubs like Newark Liberty force carriers to reroute flights and add ground legs, potentially lengthening transit times if alternative capacity is unavailable.

How are couriers responding to stricter electronic data mandates?

Leading integrators invest in advanced IT platforms to pre-file detailed shipment information, turning compliance into a competitive advantage while smaller firms may seek partnerships or exit the market.

Page last updated on: