United States Analog Integrated Circuits Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

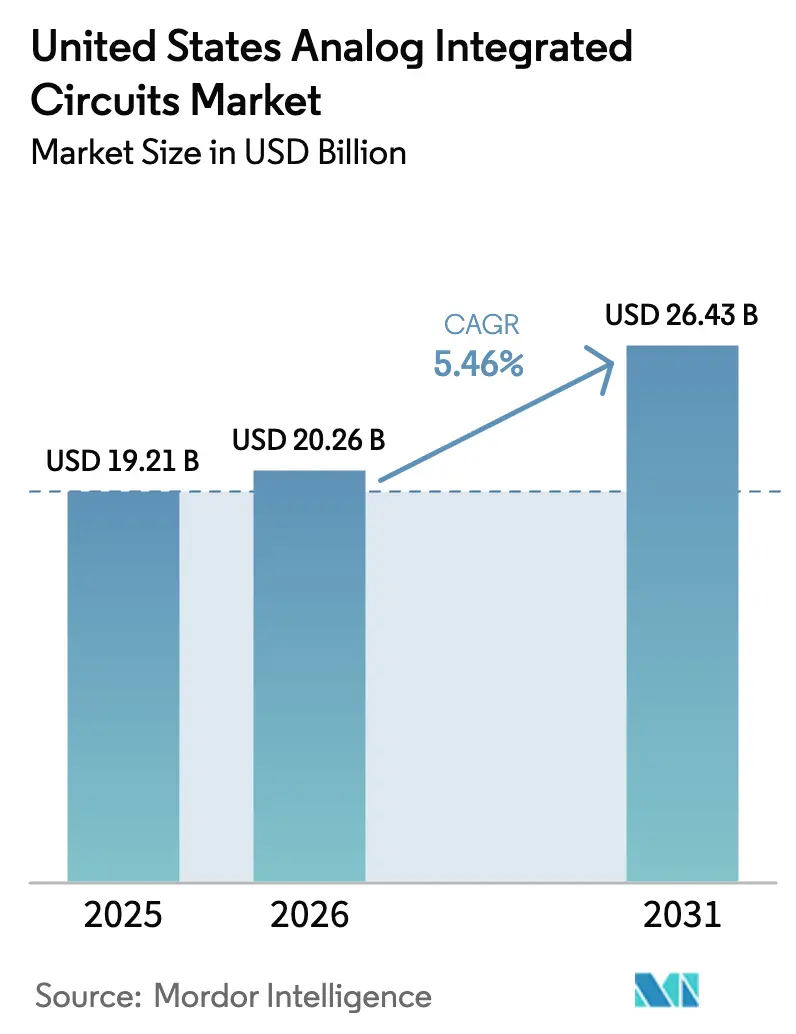

| Base Year Market Size (2025) | USD 19.21 Billion |

| Market Size (2026) | USD 20.26 Billion |

| Market Size (2031) | USD 26.43 Billion |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Analog Integrated Circuits Market Analysis by Mordor Intelligence

The United States analog integrated circuits market size is expected to grow from USD 19.21 billion in 2025 to USD 20.26 billion in 2026 and is forecast to reach USD 26.43 billion by 2031 at 5.46% CAGR over 2026-2031. Solid growth reflects resilient domestic demand in automotive electrification, 5G infrastructure densification, and industrial automation, all amplified by CHIPS and Science Act incentives that have spurred more than USD 30 billion in new fabs and tool upgrades. Integrated device manufacturers (IDMs) are adding 300 mm capacity to reduce die cost, while fabless vendors leverage expanding foundry ecosystems to accelerate design cycles. Mature-node processes above 180 nm remain dominant because they balance voltage headroom, passive component density, and cost, yet mixed-signal nodes under 28 nm are gaining share where system-on-chip integration is critical. In parallel, the acute shortage of seasoned analog engineers and persistent 200 mm capacity tightness temper the longer-term growth profile.

Key Report Takeaways

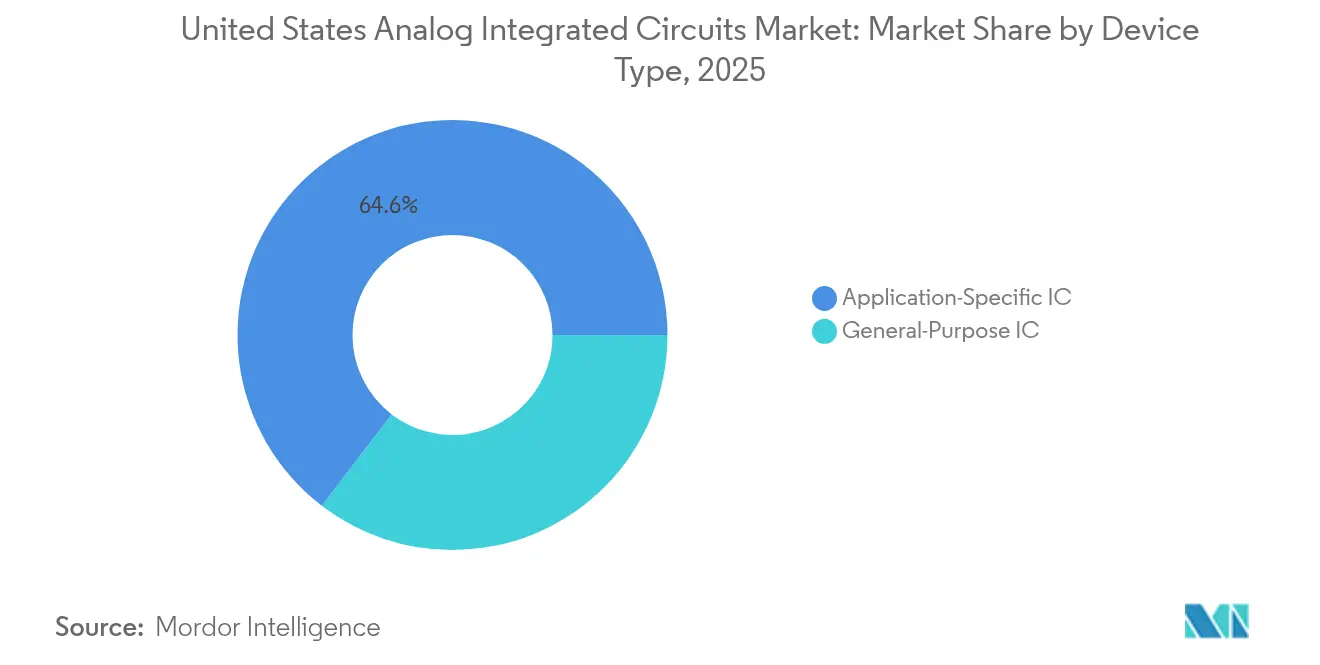

- By device type, application-specific analog ICs held 64.60% of the United States analog integrated circuits market share in 2025, and the segment is on track for a 6.53% CAGR to 2031.

- By wafer size, 200-300 mm substrates commanded 50.20% revenue in 2025, while 300 mm wafers are expanding at a 8.78% CAGR through 2031.

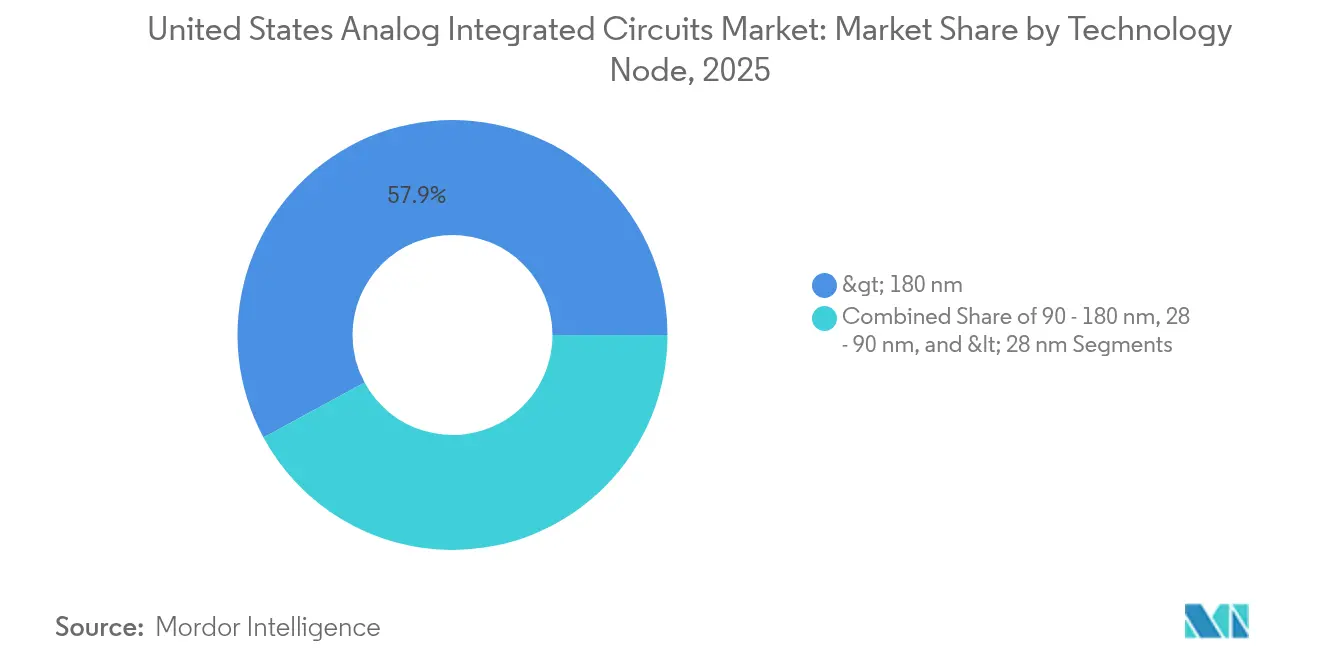

- By technology node, processes above 180 nm accounted for 57.90% of the United States analog integrated circuits market size in 2025; nodes below 28 nm are the fastest-growing at 7.62% CAGR.

- By business model, IDMs controlled 65.10% revenue in 2025, whereas fabless vendors recorded an 8.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United states representing one among them. The global report on analog integrated circuit market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

United States Analog Integrated Circuits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CHIPS and Science Act Incentives Accelerating U.S. Analog Fab Expansions | +1.2% | National, with concentrations in Texas, Utah, Arizona, Oregon | Medium term (2-4 years) |

| Electrification of U.S. Automotive Fleet Boosting Power Management IC Demand | +1.8% | National, with automotive hubs in Michigan, Texas, California | Long term (≥ 4 years) |

| 5G Infrastructure Densification: Creating High-Performance RF Analog IC Needs | +0.9% | National, with early deployments in major metropolitan areas | Short term (≤ 2 years) |

| Industrial Reshoring and IIoT Adoption Driving High-Reliability Analog Sensor IC Consumption | +0.7% | National, with manufacturing belt concentration | Medium term (2-4 years) |

| Wearable and Medical Device Proliferation Leveraging Ultra-Low-Power Analog Front-Ends | +0.6% | National, with medtech clusters in Massachusetts, California | Long term (≥ 4 years) |

| Space and Defense Programs Requiring Radiation-Hardened Analog ICs | +0.4% | National, with a defense contractor concentration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CHIPS and Science Act incentives accelerating U.S. analog fab expansions

Federal incentives have triggered the largest domestic analog capacity build-out since the 1980s. Texas Instruments secured USD 1.6 billion in grants for its Utah expansion, enabling 300 mm production that will triple output by 2030. GlobalFoundries committed USD 16 billion to new analog-focused lines, further strengthening the United States' analog integrated circuits market.[1]GlobalFoundries, “GlobalFoundries Announces $16B U.S. Investment to Reshore Essential Chip Manufacturing and Accelerate AI Growth,” gf.com Investments shorten lead times that reached 18 months during the pandemic and reinforce supply assurance for commercial and defense customers.

Electrification of U.S. automotive fleet boosting power-management IC demand

Electric vehicles embed up to five times more analog content than internal-combustion models because high-voltage systems, battery management, and thermal control all rely on precision power ICs. Partnerships such as Ford’s wafer-allocation deal with GlobalFoundries anchor long-term supply and underscore the United States' analog integrated circuits market’s strategic role in automotive competitiveness. With content per vehicle projected to exceed USD 1,000 by 2030, automotive remains the largest single growth engine.

5G infrastructure densification creating high-performance RF analog IC needs

Nationwide 5G roll-out demands millimeter-wave beamforming ICs able to operate beyond 28 GHz. Foundry moves to gallium-arsenide and silicon-germanium processes to improve noise figures and power efficiency. Qorvo’s 2025 integration of Anokiwave broadens beamforming portfolios and captures small-cell deployment momentum, supporting revenue gains above 15% in infrastructure analog products.

Industrial reshoring and IIoT adoption driving high-reliability sensor IC consumption

Post-pandemic supply-chain redesign led manufacturers to deploy smart factories domestically. IIoT nodes require rugged analog front-ends that survive temperature cycling, vibration, and electromagnetic interference for decades. Analog Devices responded by doubling Beaverton's output of condition-monitoring ICs, ensuring the United States' analog integrated circuits market can meet accelerated factory-automation schedules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Shortage of Experienced Analog Design Engineers in the U.S. | -1.1% | National, with acute shortages in Silicon Valley, Austin, Boston | Long term (≥ 4 years) |

| Capacity Tightness at Domestic 200 mm Mature-Node Fabs | -0.8% | National, affecting all analog IC segments | Medium term (2-4 years) |

| Export Controls Constraining Cross-Border EDA Collaboration | -0.5% | National, with particular impact on advanced mixed-signal designs | Short term (≤ 2 years) |

| Rising Verification Complexity and Costs in Mixed-Signal SoC Designs | -0.3% | National, affecting fabless and IDM companies equally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute shortage of experienced analog design engineers in the U.S.

Industry surveys indicated 67,000 unfilled semiconductor roles by 2030, with analog posts hardest to recruit. Salaries for senior designers topped USD 200,000 in 2025, yet universities continued prioritizing digital curricula, widening the skills gap. Companies are endowing professorships and accelerating apprenticeships, but talent pipelines will remain constrained through the decade.

Capacity tightness at domestic 200 mm mature-node fabs

Analog ICs still rely heavily on 200 mm tools optimized for >180 nm nodes. U.S. capacity rationalization in the 2000s left a shortfall that CHIPS grants can only partly reverse. Lead times near 12 months persisted in early 2025 despite new fabs under construction, limiting rapid ramp-ups for medical and industrial programs.[2]Mark LaPedus, “Legacy Process Nodes Going Strong,” Semiconductor Engineering, semiengineering.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Custom Application-Specific ICs Sustain Leadership

Application-specific devices commanded 64.60% of the United States analog integrated circuits market in 2025 and maintained a 6.53% projected CAGR. Automotive electrification alone drove multi-rail power-management and battery-monitor IC demand, while 5G base-station suppliers specified beamforming front-ends with bespoke gain and phase control. Consumer audio codecs and imaging interfaces also migrated to single-chip analog solutions that trimmed board area and bill-of-materials cost. Adoption is encouraged by IDMs’ ability to marry process tweaks with circuit design, yielding superior noise performance for radar, lidar, and sensor-fusion subsystems. On the other hand, high development costs and lengthy qualification cycles can delay revenue realization for smaller design houses.

General-purpose analog ICs, which include amplifiers, data converters, and interface transceivers, remain indispensable for cost-sensitive consumer and industrial products. Interface chips that withstand ±15 kV ESD are critical in factory automation, while ultralow-power converters enable battery-powered IoT nodes. Although the category’s CAGR trails that of application-specific solutions, standardized pinouts shorten design-in times and sustain a broad catalog approach. Vendors differentiate through quiescent-current reductions and digital calibration hooks that meet new energy-efficiency mandates. Together, both device categories underpin the continued diversification of the United States' analog integrated circuits market across end markets.

By Wafer Size: 300 mm Adoption Cuts Die Cost

The 200-300 mm class held 50.20% revenue in 2025, reflecting entrenched 200 mm dominance for voltage-tolerant analog processes. Yet 300 mm fabs recorded a 8.78% CAGR as IDMs added larger substrates for cost leverage. Texas Instruments confirmed a 40% die-cost reduction after migrating select power-management families to Utah’s 300 mm line. Photolithography modules were re-qualified for thicker copper and high-voltage LDMOS devices, proving that cost savings do not compromise analog performance.

At the same time, legacy 150 mm and 200 mm lines remain critical for rad-hard and medical implant devices, where process re-qualification costs outweigh economies of scale. Prototype volumes, military demand, and niche technologies—such as silicon-on-insulator—continue to run on smaller wafers. Pilot evaluations of ≥450 mm analog remain academic because tool sets are scarce, and device dimensions render most cost advantages moot. The mixed production landscape ensures that the United States' analog integrated circuits market can service high-volume automotive parts and low-volume specialty runs simultaneously.

By Technology Node: Mature Processes Anchor Reliability

Nodes above 180 nm retained 57.90% of the United States analog integrated circuits market size in 2025 due to their superior voltage headroom and matching characteristics. Automotive and industrial buyers prefer 5 V and 40 V device options that are impractical at advanced geometries. Moreover, extensive field reliability data accelerates functional safety qualification, a decisive factor in traction inverters, battery management, and factory automation.

Conversely, mixed-signal nodes below 28 nm, advancing at 7.62% CAGR, enable tighter integration of analog front-ends with digital signal processing. High-speed data converters in lidar and radar modules benefit from sub-28 nm transistors that switch faster and support embedded calibration. Designers mitigate substrate noise with deep-n-well isolation, while foundries offer enhanced passive component libraries. These innovations illustrate how the United States' analog integrated circuits market meets concurrent demands for precision analog and machine-learning acceleration on the same die.

By Business Model: Vertical Integration vs. Asset-Light Flexibility

IDMs accounted for 65.10% revenue in 2025 by exploiting tight design-process coupling to optimize flicker-noise, drift, and avalanche robustness. Device-specific process modules—such as thick-gate oxide variants—give IDMs a defensible advantage, particularly in safety-critical automotive zones. Their wafer ownership also guarantees supply continuity, an attribute OEMs value after pandemic shortages.

Fabless vendors, expanding at 8.05% CAGR, harness open-access PDKs and multi-project wafer shuttles to launch differentiated parts quickly. Compound-semiconductor foundry offerings unlock millimeter-wave 5G and satellite-communications opportunities. Ecosystem support for digital calibration IP and cloud-based EDA tools helps small teams deliver production-ready silicon. The dual-model environment enriches innovation and keeps the United States' analog integrated circuits market adaptive to emerging niches.

Geography Analysis

Regional investment patterns mirror established semiconductor corridors. Texas attracted multi-billion-dollar analog fabs through tax incentives, ample land, and proximity to automotive customers. Oregon’s Silicon Forest focused on precision data converters and sensor interfaces, leveraging an experienced workforce and university collaborations. Arizona gained momentum as TSMC ramped advanced packaging and mixed-signal wafers in 2025, widening the manufacturing footprint. California, while high-cost, maintained design dominance via Silicon Valley’s IP, EDA, and venture networks.

Demand concentration also follows end-market hubs. Michigan’s electrification push anchors automotive analog consumption, while Massachusetts’ medtech cluster favors ultra-low-power sensor ASICs. Defense procurement pipelines in Virginia and California require radiation-hardened power devices, reinforcing in-country sourcing mandates. Supply-chain resilience initiatives further redistribute procurement to domestic suppliers, insulating OEMs from cross-border logistics disruptions.

Public funding through the CHIPS and Science Act earmarked USD 39 billion for U.S. fabs, with priority on mature-node analog capacity. The incentives offset steep capital costs—often exceeding USD 4 billion per 300 mm line—and shorten payback periods. Combined with state-level tax abatements, the policy framework consolidates the United States' analog integrated circuits market as a cornerstone of national industrial strategy.

Mordor Intelligence provides coverage of the analog integrated circuit market across other key regional markets. Detailed country-level analysis extends to Taiwan and South Korea incorporating local coverage and market participation, as required.

Competitive Landscape

The five largest suppliers controlled majority of the United States' analog integrated circuits revenue in 2024, signalling moderate consolidation. Texas Instruments scaled proprietary BCDMOS platforms, cloaking cost and performance gains from pure-play foundry competitors. Analog Devices doubled Oregon's output of low-noise amplifiers to defend industrial leadership, while GlobalFoundries secured long-term wafer purchase agreements with automotive OEMs to underpin fab utilization.

Fabless challengers concentrate on niche-performance vectors instead of breadth. Silicon-germanium startups target 40 GHz phased-array modules, and power-conversion specialists exploit wide-bandgap devices for 800 V battery packs. Strategic alliances allow these firms to access specialty process nodes without owning capital assets, eroding IDM's share in emerging segments. M&A activity—such as Qorvo’s purchase of Anokiwave—reflects a race to acquire scarce RF system knowledge and speed portfolio build-out.

Over the outlook period, competitive differentiation will pivot on integrated solutions that merge precision analog, edge AI, and functional safety certification. Vendors combining circuit innovation, domain-specific software, and robust supply logistics will capture outsize value. Talent scarcity and verification complexity, however, raise entry barriers and favor players with deep engineering benches and automated design flows, preserving the United States' analog integrated circuits market’s medium concentration profile.

United States Analog Integrated Circuits Industry Leaders

-

Analog Devices Inc.

-

Infineon Technologies AG

-

STMicroelectronics N.V.

-

Texas Instruments Inc.

-

NXP Semiconductors N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: GlobalFoundries announced a USD 16 billion plan to expand U.S. analog capacity, adding 200 mm and 300 mm lines for automotive and industrial applications.

- April 2025: Nvidia began Blackwell AI chip production at TSMC’s Arizona site, validating advanced mixed-signal manufacturing in the U.S.

- March 2025: Texas Instruments allocated USD 11 billion to its Utah complex, enabling 300 mm analog output that will triple capacity by 2030.

- February 2025: Analog Devices finished doubling the Beaverton output of precision amplifiers and converters.

United States Analog Integrated Circuits Market Report Scope

For market estimation, the revenue generated from sales of various types of analog integrated circuits used in a diverse range of industries, such as consumer, automotive, communication, computer, industrial, etc., is tracked. Market trends are evaluated by analyzing investments made in product innovation, diversification, and expansion. Enhancements in 5G, IoT, AI, energy efficiency, artificial intelligence, autonomous systems, electric vehicles, and biomedical devices are also crucial in determining the growth of the market studied.

The analog integrated circuits market in the United States is segmented by type (general-purpose IC (interface, power management, signal conversion, and amplifiers/comparators), application-specific IC (consumer (audio/video and digital still camera & camcorder, and other consumers), automotive (infotainment and other automotive application ICs), communication (cell phone, infrastructure, wired communication, short range, and other wireless), computer (computer system & display, computer periphery, storage, and other computers), and industrial and other analog IC types)). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| General-Purpose IC | Interface | |

| Power Management | ||

| Signal Conversion | ||

| Amplifiers / Comparators | ||

| Application-Specific IC | Consumer Electronics | Audio / Video |

| Digital Still Camera and Camcorder | ||

| Other Consumer | ||

| Automotive | Infotainment | |

| Other Automotive Applications | ||

| Communication | Cell Phone | |

| Infrastructure | ||

| Wired Communication | ||

| Short Range Wireless | ||

| Other Wireless | ||

| Computer | System and Display | |

| Peripherals | ||

| Storage | ||

| Other Computer | ||

| Industrial and Others | ||

| ≤ 200 mm |

| 200–300 mm |

| 300 mm |

| ≥ 450 mm |

| > 180 nm |

| 90 – 180 nm |

| 28 – 90 nm |

| < 28 nm (mixed-signal) |

| Integrated Device Manufacturer (IDM) |

| Design/ Fabless Vendor |

| By Device Type | General-Purpose IC | Interface | |

| Power Management | |||

| Signal Conversion | |||

| Amplifiers / Comparators | |||

| Application-Specific IC | Consumer Electronics | Audio / Video | |

| Digital Still Camera and Camcorder | |||

| Other Consumer | |||

| Automotive | Infotainment | ||

| Other Automotive Applications | |||

| Communication | Cell Phone | ||

| Infrastructure | |||

| Wired Communication | |||

| Short Range Wireless | |||

| Other Wireless | |||

| Computer | System and Display | ||

| Peripherals | |||

| Storage | |||

| Other Computer | |||

| Industrial and Others | |||

| By Wafer Size | ≤ 200 mm | ||

| 200–300 mm | |||

| 300 mm | |||

| ≥ 450 mm | |||

| By Technology Node | > 180 nm | ||

| 90 – 180 nm | |||

| 28 – 90 nm | |||

| < 28 nm (mixed-signal) | |||

| By Business Model | Integrated Device Manufacturer (IDM) | ||

| Design/ Fabless Vendor | |||

Key Questions Answered in the Report

What is the projected value of the United States' analog integrated circuits market by 2031?

The market is forecast to reach USD 26.43 billion by 2031, up from USD 20.26 billion in 2026.

How does the CHIPS and Science Act influence the analog IC supply?

The Act offers USD 39 billion in incentives that finance new 200 mm and 300 mm fabs, shortening lead times and encouraging on-shore production.

Why are 300 mm wafers important for analog ICs?

Moving select analog families to 300 mm substrates can lower die cost by roughly 40% while maintaining mature-node device characteristics.

Which device segment leads the market?

Application-specific analog ICs hold 64.60% revenue share and are growing at 6.53% CAGR through 2031 due to customization for automotive and 5G applications.

What is the main challenge limiting market growth?

A national shortage of experienced analog design engineers is the top structural restraint, reducing the pace at which new products can be developed.

Page last updated on: