Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Industrial Logic Integrated Circuits Market is Segmented by IC Type (Digital Bipolar, MOS Logic), Technology Node (≥ 65 Nm, 40-65 Nm, and More), Industrial Application (Factory Automation and Robotics, Process Control and Distributed Control Systems, and More), End-Use Equipment (PLCs, Industrial PCs and Edge Gateways, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

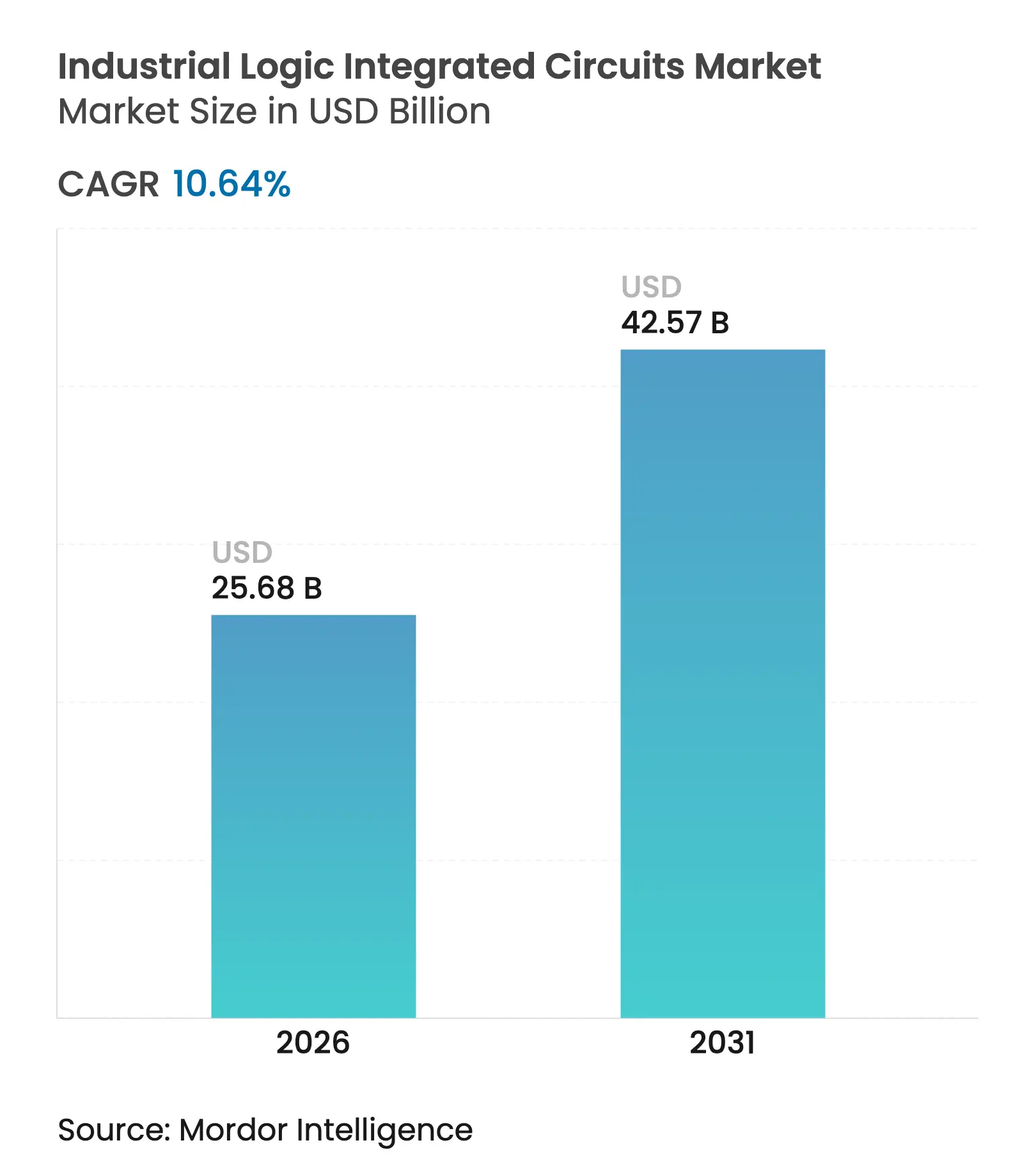

| Market Size (2026) | USD 25.68 Billion |

| Market Size (2031) | USD 42.57 Billion |

| Growth Rate (2026 - 2031) | 10.64 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The industrial logic integrated circuits market size was valued at USD 23.21 billion in 2025 and estimated to grow from USD 25.68 billion in 2026 to reach USD 42.57 billion by 2031, at a CAGR of 10.64% during the forecast period (2026-2031). Growth reflected the fast spread of edge-AI workloads in factory controllers, the migration of automotive production lines to 800 V systems that demand rugged logic components, and widening global fab capacity backed by 18 new facilities that started construction in 2025. Taiwan’s leadership in sub-7 nm manufacturing continued to bolster advanced logic availability. Vendors bundled logic, communication, and security blocks inside integrated modules, shifting buyer preference from discrete chips to system-level products. At the same time, qualification cycles longer than seven years and design-for-reliability constraints at temperatures above 175 °C slowed aggressive node migration.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Demand for Edge-AI-Enabled Industrial Controllers

Accelerating High-Speed Logic IC Adoption

Demand for Edge-AI-Enabled Industrial Controllers

Accelerating High-Speed Logic IC Adoption

| +2.1% | Global, with APAC leading adoption | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+2.1%

|

Geographic Relevance

:

Global, with APAC leading adoption

|

Impact Timeline

:

Medium term (2-4 years)

|

Transition from Discrete PLCs to Integrated

System-on-Module Architectures in Europe

Transition from Discrete PLCs to Integrated

System-on-Module Architectures in Europe

| +1.8% | Europe's core, expanding to North America | Long term (≥ 4 years) | |||

Semiconductor Fab Expansions in Taiwan, South Korea, and the

US CHIPS Act Incentives

Semiconductor Fab Expansions in Taiwan, South Korea, and the

US CHIPS Act Incentives

| +1.5% | APAC core, spill-over to North America | Short term (≤ 2 years) | |||

Migration of Automotive Factories to 800V Architectures

Requiring Rugged Logic ICs

Migration of Automotive Factories to 800V Architectures

Requiring Rugged Logic ICs

| +1.2% | Global, with Europe and China leading | Medium term (2-4 years) | |||

Uptake of GaN/SiC Power Stages Stimulating Companion Logic

Driver IC Demand

Uptake of GaN/SiC Power Stages Stimulating Companion Logic

Driver IC Demand

| +0.9% | North America and EU, expanding to APAC | Medium term (2-4 years) | |||

Cyber-Physical Security Mandates Pushing Secure Logic

Co-Processors in Industrial IoT

Cyber-Physical Security Mandates Pushing Secure Logic

Co-Processors in Industrial IoT

| +0.7% | Global, with a regulatory focus in the EU and North America | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Demand for Edge-AI-Enabled Industrial Controllers Accelerated High-Speed Logic IC Adoption

Manufacturers embedded AI inference directly inside machines to cut latency and raise line throughput. Rockwell Automation’s link-up with NVIDIA to run Isaac robotics software on factory controllers highlighted the need for high-bandwidth logic that handles vision and navigation in real time.[1]Rockwell Automation, “Rockwell Automation to Advance Intelligent Automation…,” rockwellautomation.com 3M production sites that piloted Azure SQL Edge showed how on-device analytics trimmed cloud traffic yet preserved performance. Vendors such as Intel and NXP broadened industrial-grade edge CPUs, which raised demand for FinFET-based logic devices. As inference workloads spread, factory planners specified lower power draw and tighter real-time determinism, steering orders toward advanced nodes below 22 nm. This shift lifted the industrial logic integrated circuits market by expanding the value captured per controller.

Transition from Discrete PLCs to Integrated System-on-Module Architectures in Europe

European OEMs reduced cabinet complexity by combining control, connectivity, and safety blocks on compact modules. Renesas rolled out SMARC-form-factor boards with built-in AI acceleration for industrial use, pointing to a rising need for logic that supports multi-protocol communication in one footprint. Phoenix Contact’s PLCnext partnership with Festo illustrated openness to Linux-based control stacks inside modular hardware. Beckhoff’s MX-System mounted distributed I/O, drives, and logic inside a single IP67 housing, further proving that board-level integration trims wiring and accelerates line reconfiguration. These moves expanded bill-of-materials value for suppliers that shipped high-density logic arrays and custom drivers. The change added momentum to the industrial logic integrated circuits market as customers upgraded legacy PLCs.

Semiconductor Fab Expansions in Taiwan, South Korea, and the US

TSMC, Samsung, and domestic US projects that received CHIPS Act grants widened 300 mm capacity for industrial-grade logic wafers, easing the shortages that plagued 2023-2024. Texas Instruments committed USD 60 billion to new analog and logic fabs across seven US sites, strengthening local supply for automotive and factory customers. STMicroelectronics lifted weekly output in its Agrate 300 mm line to support MCU and logic portfolios. Extra headroom lowered per-wafer costs, made 28 nm and 40 nm nodes more affordable, and underpinned a smoother delivery schedule. The resulting capacity improved buyer confidence and sustained the double-digit growth pace of the industrial logic integrated circuits market.

Migration of Automotive Factories to 800 V Architectures Required Rugged Logic ICs

EV production plants retrofitted lines for faster 800 V charging, forcing motor test rigs, welding robots, and powertrain stations to rely on logic devices rated for high-voltage transients. Infineon’s EiceDRIVER isolated gate driver family is targeted at traction inverter control and meets automotive isolation rules. Navitas launched AEC-Plus qualified SiC MOSFETs with top-side cooling to improve thermal cycling margins in fast-charge and industrial power blocks. As automotive-grade logic trickled into plant equipment, vendors captured cross-segment synergies and expanded lifetime revenue streams in the industrial logic integrated circuits market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Design-for-Reliability

Complexity Beyond 175°C Junction Temperatures

Design-for-Reliability

Complexity Beyond 175°C Junction Temperatures

| -1.2% | Global, particularly affecting harsh environment applications | Long term (≥ 4 years) |

(~) %

Impact on CAGR Forecast

:

-1.2%

|

Geographic

Relevance

:

Global,

particularly affecting harsh environment applications

|

Impact

Timeline

:

Long

term (≥ 4 years)

|

Lengthy

Industrial Qualification Cycles (>7 years) Hindering Node Shrink Adoption

Lengthy

Industrial Qualification Cycles (>7 years) Hindering Node Shrink Adoption

| -0.9% | Global, with stricter requirements in Europe and North America | Long term (≥ 4 years) | |||

Global

Shortage of Specialty Gases and Photoresists for Logic IC Lithography

Global

Shortage of Specialty Gases and Photoresists for Logic IC Lithography

| -0.7% | Global, with acute impact on APAC manufacturing hubs | Short term (≤ 2 years) | |||

Fragmented

Industrial Field-Bus Standards Inflating Verification Costs

Fragmented

Industrial Field-Bus Standards Inflating Verification Costs

| -0.5% | Global, with higher complexity in Europe due to diverse protocols | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Design-for-Reliability Complexity Beyond 175 °C Junction Temperatures

Standards such as JEDEC JESD-22-A100C demanded extended humidity-bias cycling for devices exposed to 175 °C plus ambient levels, pushing packaging, die attach, and metallurgy to their limits. Steel and glass plants that ran furnaces above 1,200 °C needed controllers that survived hot zones where cabinet cooling proved impractical. Infineon’s OPTIREG TLF35585 PMIC, rated to 175 °C, revealed the extra design steps, cost premiums, and elongated qualification plans involved. These hurdles trimmed the pace at which advanced nodes penetrated extreme-temperature niches.

Lengthy Industrial Qualification Cycles Hindering Node Shrink Adoption

AEC-Q100 and AEC-Q101 tests required temperature cycling, mechanical shock, and electromagnetic stress sessions that spanned many quarters, delaying volume release for each mask set. Renesas adhered to IATF16949 and ISO9001 protocols across multiple fabs to secure customer trust for a 20-year equipment life. This conservative culture kept ≥65 nm logic popular in programmable logic controllers and drive inverters, limiting near-term revenue upside from FinFET or GAA nodes in the industrial logic integrated circuits market.

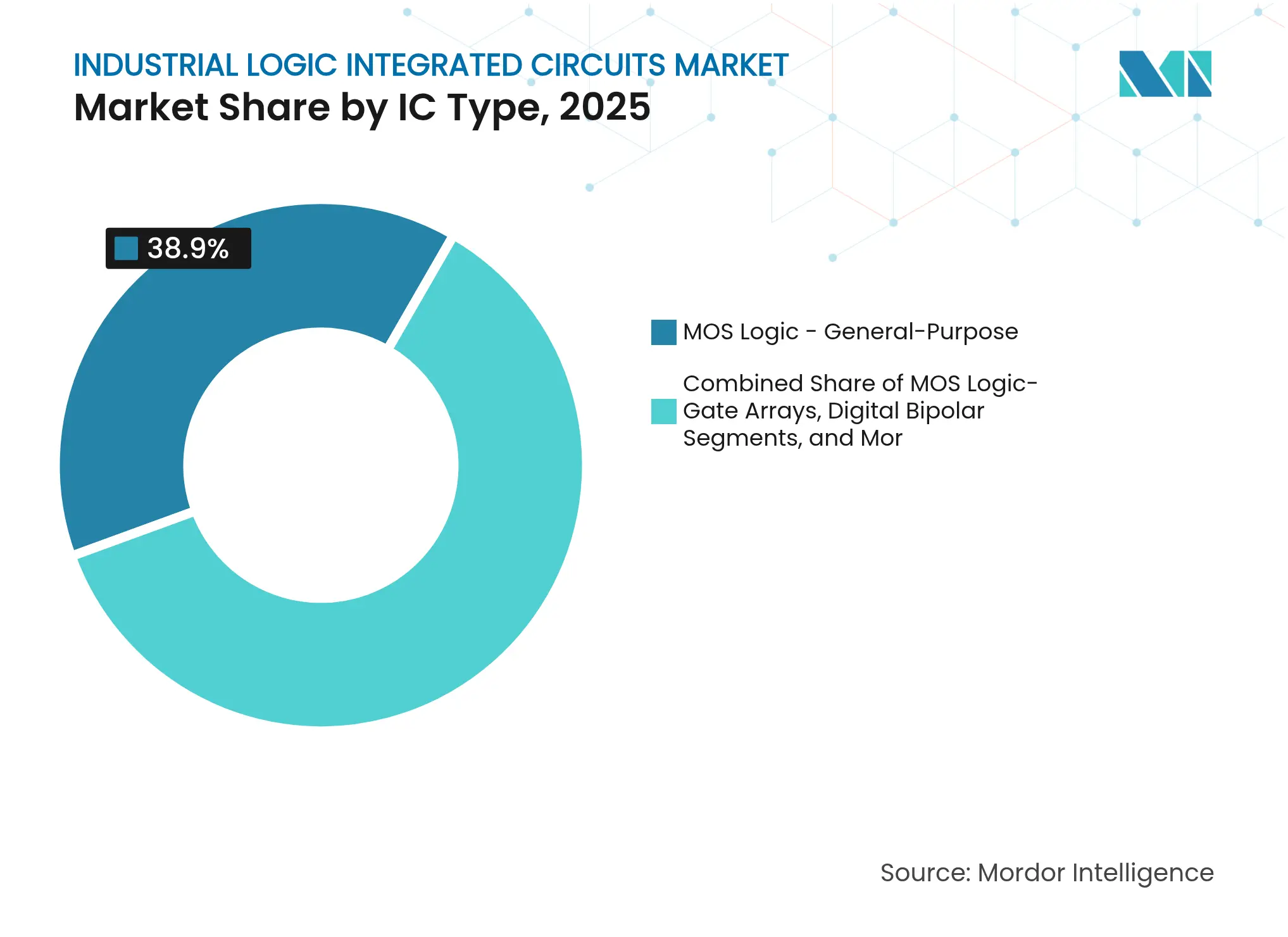

By IC Type: Integration Raises Value per Board

The MOS general-purpose logic segment captured 38.90% of the industrial logic integrated circuits market share in 2025, underlining its ubiquity in basic gating, buffering, and signal translation across disparate control boards. Vendors shipped millions of quad-gate packages for PLC I/O expansion and simple combinatorial tasks. Demand stayed stable as OEMs valued predictable performance and wide temperature coverage.

MOS drivers/controllers posted a 11.7% CAGR and lifted their slice of the industrial logic integrated circuits market size by enabling single-chip motor control, integrated diagnostics, and safety shutdown. Infineon’s MOTIX portfolio showed how embedded current sensing and SPI diagnostics reduced board count in UAV propulsion modules. Gate arrays, standard cells, and special-purpose logic fulfilled niche timing, interface, or protocol duties where off-the-shelf MCUs failed to meet latency or certification needs, while digital bipolar parts kept a foothold in environments rich in electromagnetic noise.

Note: Segment shares of all individual segments available upon report purchase

By Technology Node: Reliability Favored Mature Nodes

Nodes at or above 65 nm held 50.85% of 2025 revenues because buyers trusted their field failure records and valued multi-source wafer capacity. Mature geometries delivered ample logic density for ladder logic, interlocks, and safety relays while offering tolerable soft error rates.

Sub-10 nm FinFET/GAA processes showed an 17.4% CAGR during 2026-2031, driven by edge inference engines and secure co-processors. The 28-32 nm class functioned as a midway step where automotive and industrial chips combined flash, DRAM, and CPU cores within the cost envelope of older lines. 14-22 nm nodes served drive-by-wire and high-value metrology gear that required faster response but accepted slightly higher die costs. These migration patterns indicated that the industrial logic integrated circuits industry balanced reliability with performance instead of chasing the absolute leading edge.

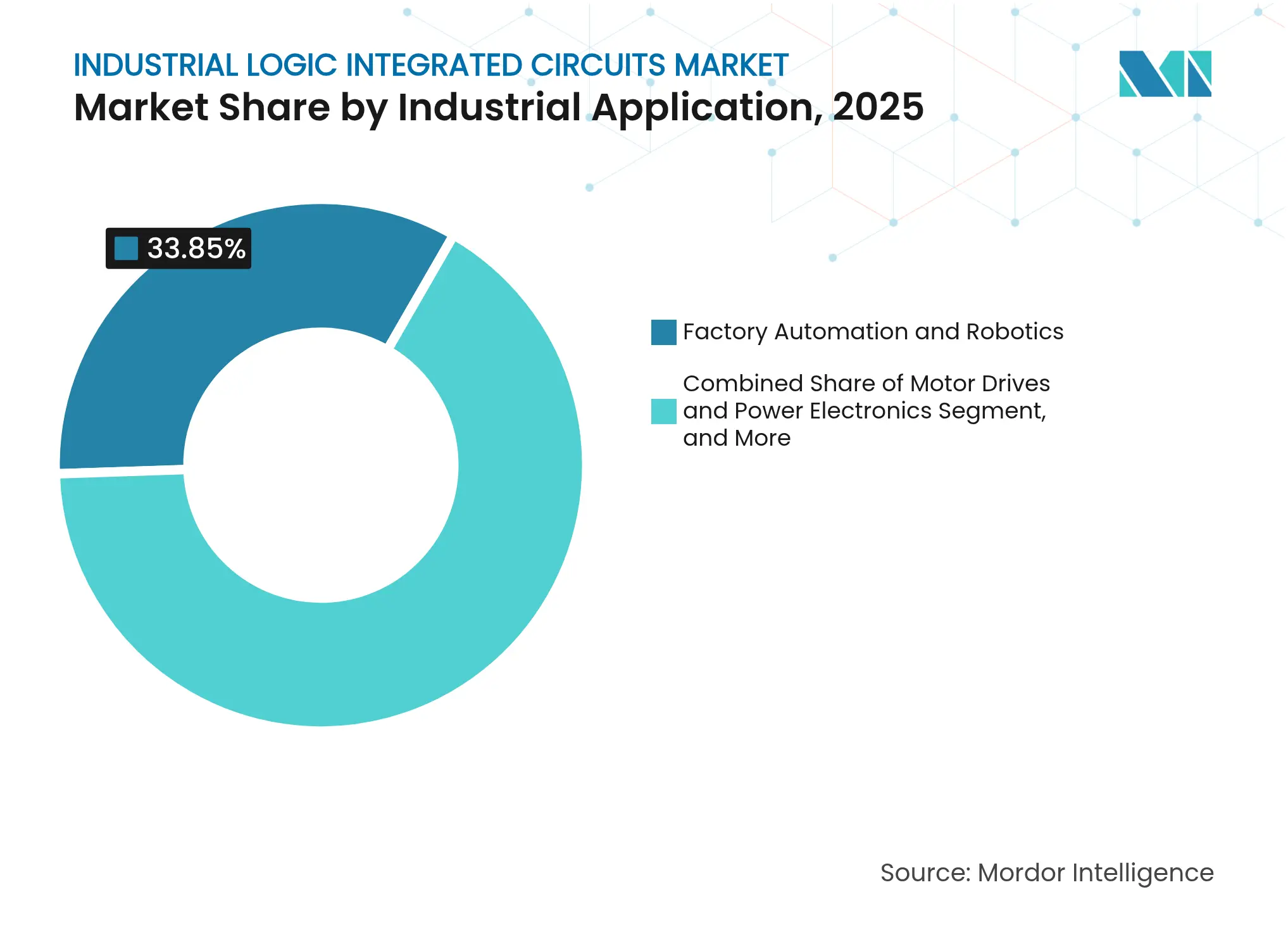

By Industrial Application: Automation Remained the Anchor

Factory automation and robotics commanded 33.85% of 2025 demand, reflecting the centrality of motion control, vision guidance, and pick-and-place coordination in modern assembly plants. Continued Industry 4.0 rollouts kept this base steady.

Smart grid and energy management recorded the fastest 13.6% CAGR as utilities upgraded substations with synchrophasor measurement and distributed energy resource control. Logic ICs paired with high-speed ADCs to manage bidirectional power flows and protect lines from cyber attacks. Process control, motor drives, and precision instrumentation formed resilient demand pillars, each aligned with sector-specific maintenance cycles and capex plans.

Note: Segment shares of all individual segments available upon report purchase

By End-Use Equipment: Edge Gateways Closed the IT-OT Gap

PLCs retained a 28.75% share of the industrial logic integrated circuits market size in 2025, securing sales through decade-long install bases, ladder logic familiarity, and robust enclosure ratings. Vendors refreshed designs with gigabit Ethernet and OPC UA stacks but kept existing instruction sets to protect customer code.

Industrial PCs and edge gateways logged a 14.4% CAGR due to cloud connectivity, containerized workloads, and remote fleet management. Sensors and transducer modules adopted integrated logic for calibration and digital output. Power management modules blended gate drivers, logic, and telemetry in renewable inverters. HMIs demanded low-power graphics controllers to present KPI dashboards on touchscreens. These shifts encouraged suppliers to ship combo devices that bundled CPU, FPGA fabric, memory, and secure boot.

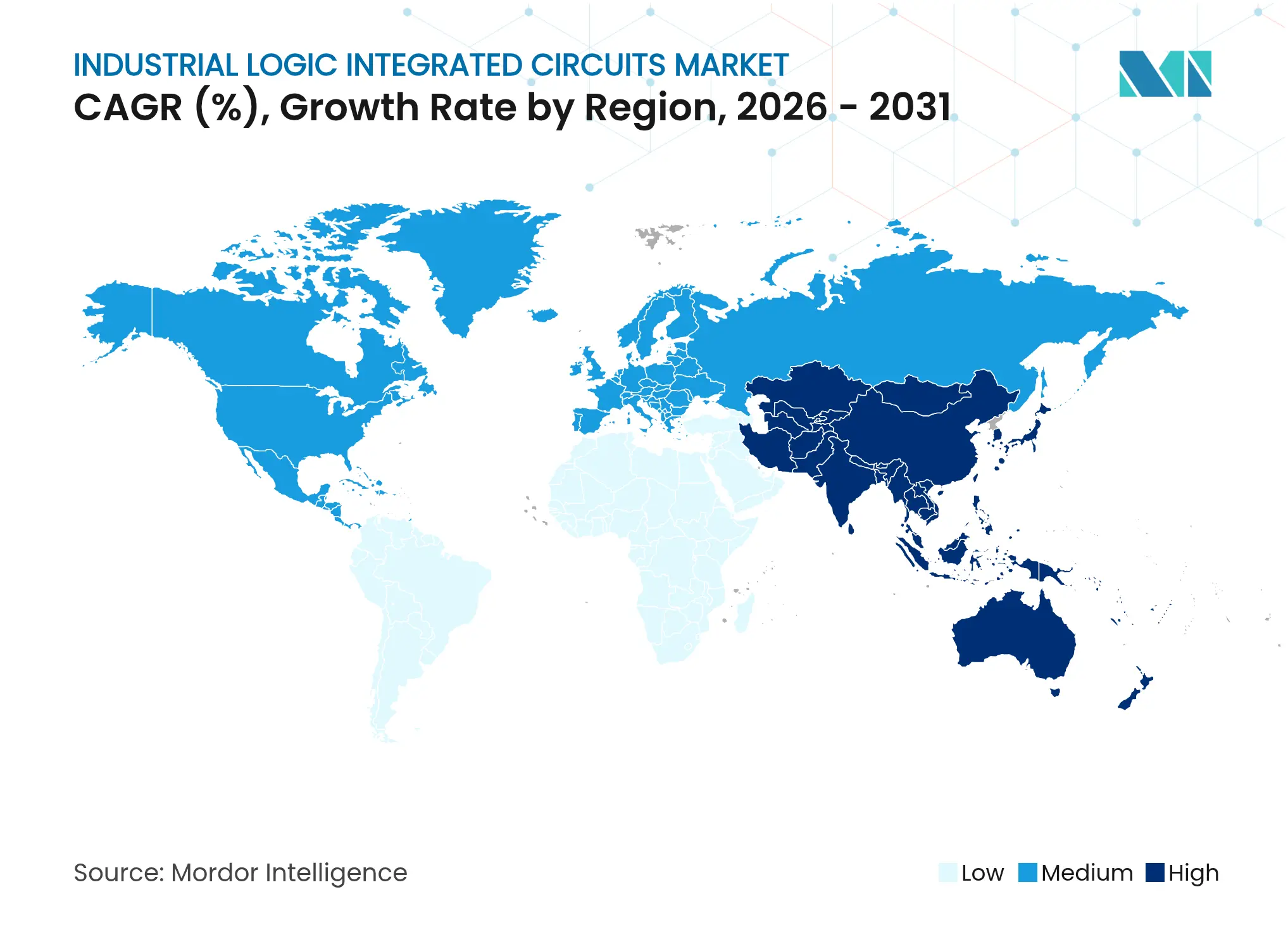

Asia-Pacific secured 57.10% of 2025 revenue and is advancing at 10.95% CAGR, anchored by Taiwan’s 63.8% share of global wafer output and 70% dominance in sub-7 nm chip supply. China accelerated factory automation investments under its Made in China 2025 agenda, while South Korea leveraged Samsung’s and SK hynix’s node expertise to serve domestic EV and battery plants. Japan’s precision robotics sector and India’s fast-growing discrete manufacturing clusters further reinforced demand.

Europe’s industrial logic integrated circuits market leaned on Germany’s automotive plants, France’s aerospace assembly, and the Nordic push for energy-efficient machinery. Stringent IEC 62443 cybersecurity rules spurred the inclusion of hardware root-of-trust modules inside controllers. Regional fab projects in Italy and France aimed to retain sovereignty over strategic semiconductors.

North America benefited from USD 52 billion in CHIPS Act incentives and the reshoring of PCB and drive-inverter lines. Texas Instruments’ USD 60 billion multi-year fab build underscored its intent to shorten supply chains for US aerospace, defense, and oilfield service customers. Canada’s mining automation and Mexico’s growing Tier-1 auto supplier base added downstream pull. However, specialist photoresist and EUV mask blanks still flowed from Asia, leaving room for logistical risk.

Market Concentration

The industrial logic integrated circuits market displayed moderate fragmentation. STMicroelectronics, Texas Instruments, and Infineon delivered broad catalogs spanning 65 nm to 22 nm nodes, while niche vendors served edge-AI or ultra-high-temperature gaps. Barriers included seven-year qualification cycles and the need for factory audits, which protected incumbents.

Players shifted to platform strategies. Renesas bundled MPU, PMIC, and connectivity on SMARC boards to shorten OEM design time.[4]Renesas Electronics, “Quality and Reliability,” renesas.com Phoenix Contact knits logic, fieldbus, and cloud connectors into its PLCnext ecosystem to lock in software developers. Infineon's advanced RISC-V microcontrollers with integrated security IP to answer EU cybersecurity mandates.

Emerging challengers included Navitas, which applied SiC expertise to motor inverter drivers; Imec, whose GaN-on-Si IP attracted RF industrial customers; and system integrators that wrapped open-source stacks around FPGA logic. Competitive intensity remained high, yet the long product lifetimes diluted the probability of any single vendor exceeding a 15% share in the next five years.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Logic integrated circuits (ICs) are specialized semiconductor devices that perform logical operations on digital signals. These operations include fundamental functions such as AND, OR, and NOT, which are the building blocks of digital circuits.

For market estimation, the revenue generated from sales of various types of industrial logic integrated circuits like digital bipolar and MOS logic across a diverse range of geographic regions worldwide is tracked. Market trends are evaluated by analyzing product innovation, diversification, and expansion investments. Enhancements in energy efficiency, artificial intelligence, miniaturization, machine learning, manufacturing process control, embedded & communications systems, etc., are also crucial in determining the growth of the market studied.

The industrial logic integrated circuits market is segmented by IC type (digital bipolar and MOS logic [MOS general purpose, MOS gate arrays, MOS drivers/controllers, MOS standard cells, and MOS special purpose]), and geography (United States, Europe, Japan, China, Korea, Taiwan, and rest of the world). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.