United States Industrial Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

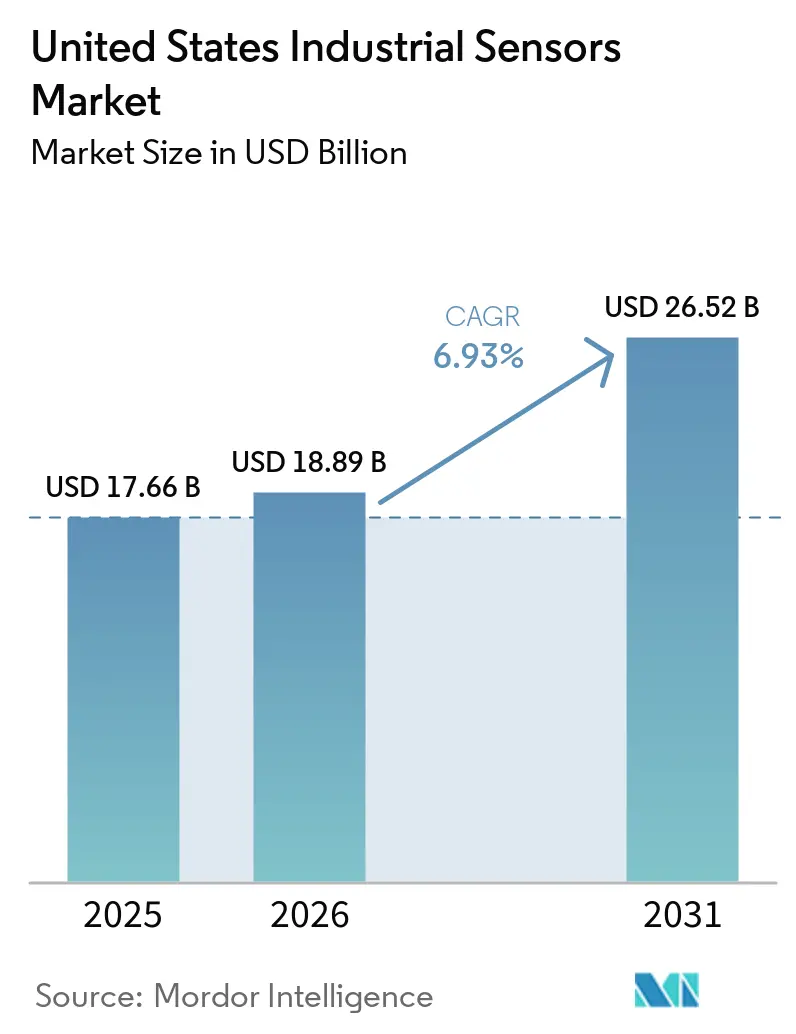

| Base Year Market Size (2025) | USD 17.66 Billion |

| Market Size (2026) | USD 18.89 Billion |

| Market Size (2031) | USD 26.52 Billion |

| Growth Rate (2026 - 2031) | 6.93% CAGR |

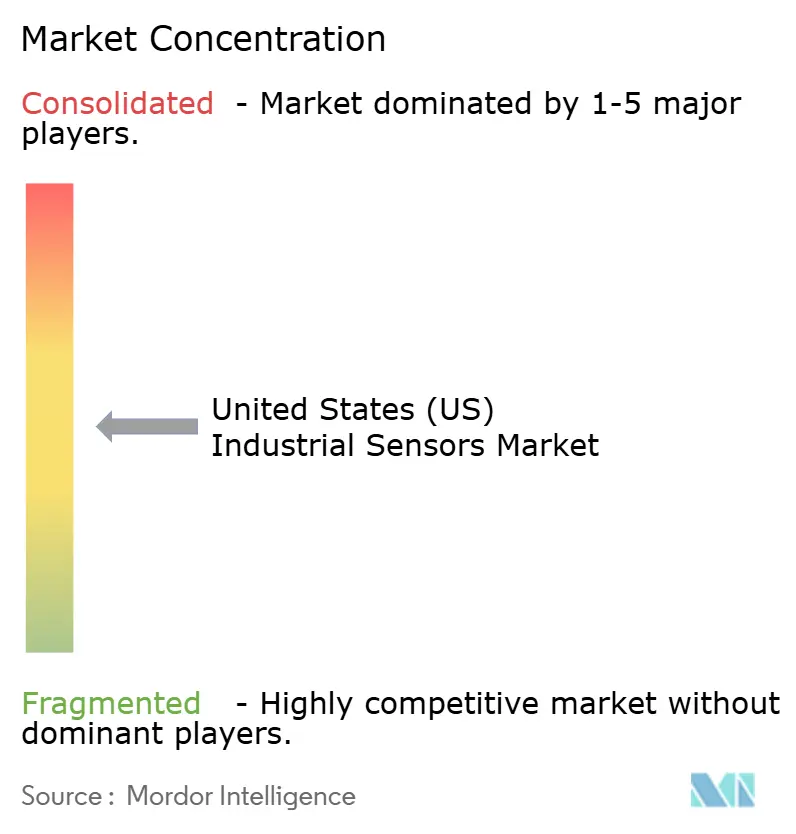

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Industrial Sensors Market Analysis by Mordor Intelligence

The United States industrial sensors market size was valued at USD 17.66 billion in 2025 and is estimated to grow from USD 18.89 billion in 2026 to USD 26.52 billion by 2031, growing at a CAGR of 6.93% from 2026 to 2031. Ongoing retooling of factories toward data-driven optimization, federal incentives for reshoring high-tech supply chains, and a wave of clean-energy projects are widening the addressable base of connected instrumentation. Wired architectures still dominate safety-critical loops, while private 5G and Ethernet-APL are accelerating wireless adoption in greenfield facilities. Demand for ultra-clean, high-accuracy sensors is rising in newly announced semiconductor fabs, while life-science plants require stringent environmental monitoring to comply with 21 CFR Part 11 and 211.110. Vendors are differentiating through longer warranties, factory-calibrated devices, and cybersecurity certifications, signaling a shift from hardware price competition to lifetime cost and digital services.

Key Report Takeaways

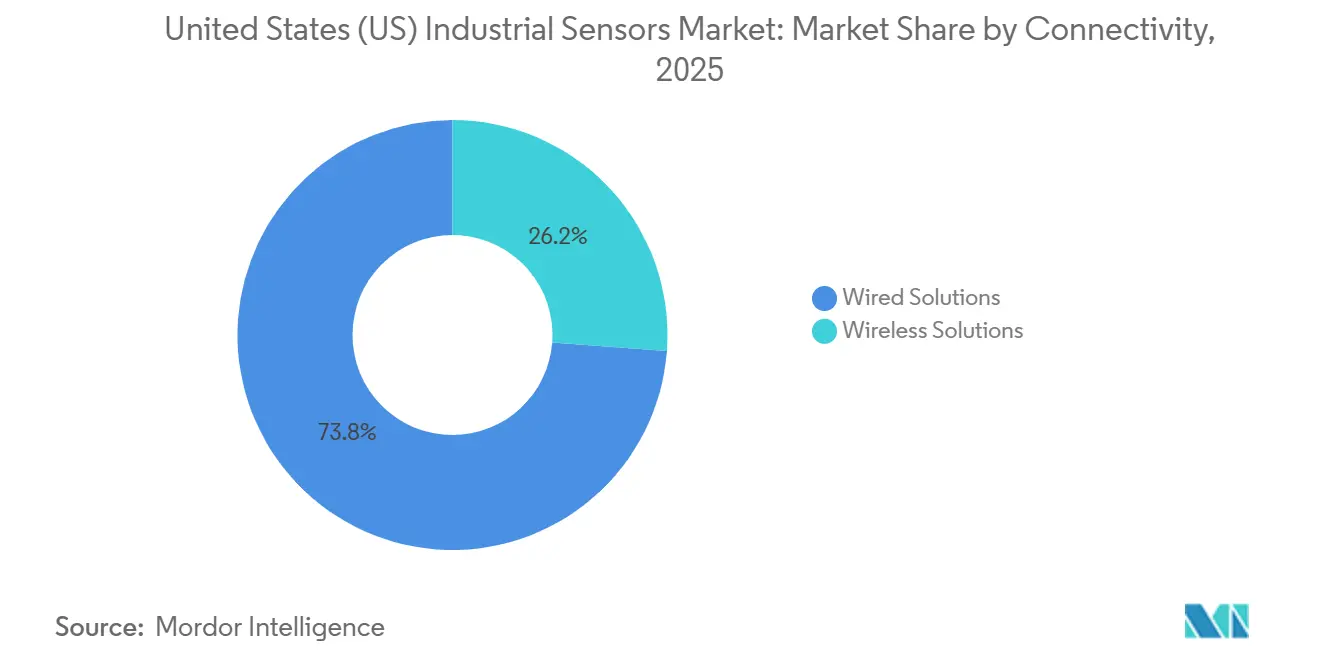

- By connectivity, wired solutions held 73.82% of the United States industrial sensors market share in 2025, whereas wireless solutions are projected to expand at an 8.45% CAGR through 2031.

- By sensor type, pressure devices led with 27.30% share of the US industrial sensors market size in 2025, while gas sensors are forecast to grow at an 8.74% CAGR over 2026-2031.

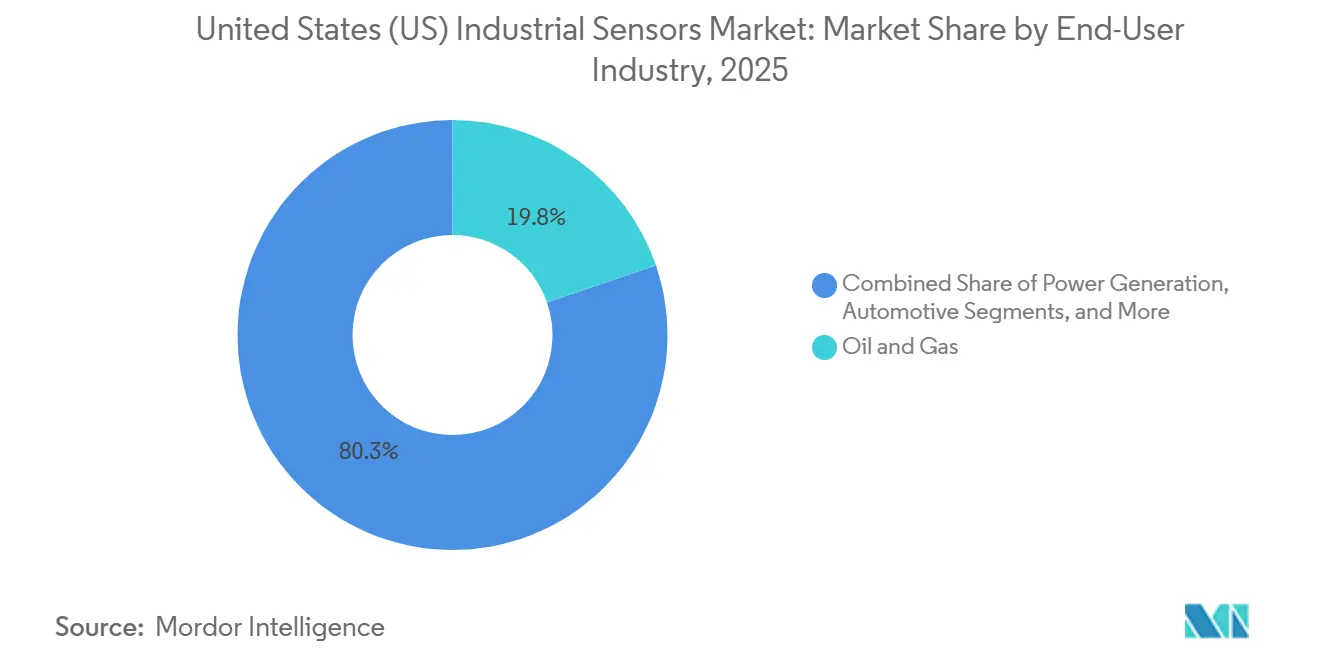

- By end-user industry, the oil and gas sector accounted for 19.75% of the USA industrial sensors market demand in 2025, but the pharmaceutical and life sciences sector is advancing at a 7.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Industrial Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in IIoT Adoption Across Discrete and Process Industries | +1.8% | Midwest manufacturing belt, Gulf Coast clusters | Short term (≤ 2 years) |

| Rising Capital Expenditure on Clean-Energy Infrastructure | +1.5% | Texas, California, offshore wind corridors | Medium term (2–4 years) |

| Expansion of the United States Semiconductor Fabs Driving Sensor Demand in Advanced Manufacturing | +1.2% | Arizona, Ohio, Texas, New York | Medium term (2–4 years) |

| Acceleration of Predictive-Maintenance Programs Post-2025 | +1.0% | Automotive, power generation, heavy industry nationwide | Short term (≤ 2 years) |

| Federal Incentives for Reshoring Critical Industries | +0.8% | Battery, semiconductor, pharmaceutical supply chains | Long term (≥ 4 years) |

| Growth of Hydrogen Economy Requiring Novel Pressure and Gas Sensors | +0.6% | California, Gulf Coast, DOE hydrogen hubs | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surge in IIoT Adoption Across Discrete and Process Industries

Manufacturers are embedding sensors at every production node to enable real-time analytics that minimize unplanned downtime and scrap rates. Private 5G deployments demonstrate sub-10 millisecond latency for vibration, temperature, and vision sensors, validating wireless performance on automotive assembly and CNC machining lines.[1]Verizon Communications, “Private 5G for Smart Manufacturing,” verizon.com Food processors have reduced cabling work by 60% using LoRaWAN gateways to backhaul data from hygienic temperature and flow sensors. Edge gateways now run time-sensitive networking in concert with OPC UA, allowing closed-loop control that was previously limited to wired systems. As a result, the United States industrial sensors market is witnessing denser sensor grids and higher attach rates in both brownfield and greenfield facilities.

Rising Capital Expenditure on Clean-Energy Infrastructure

The Department of Energy’s Speed to Power initiative halves interconnection timelines, spurring demand for differential pressure sensors in wind-turbine pitch systems and current sensors inside grid-tied inverters. A USD 44 million federal outlay in 2025 targeted advanced metering and substation automation, both of which rely on temperature and partial-discharge sensors. Offshore wind developers specify intrinsically safe pressure and flow devices rated for Class I Division 1 environments under NFPA 70 Article 500.[2]National Fire Protection Association, “NFPA 70: National Electrical Code,” nfpa.orgBattery storage projects, which added 15 GW in 2025, mandate thermal-runaway detection to meet UL 9540A standards. Clean-energy growth, therefore, tilts the United States industrial sensors market toward gas, current, and vibration sensing technologies that support asset availability and regulatory compliance.

Expansion of the United States Semiconductor Fabs Driving Sensor Demand

TSMC, Micron, and Intel collectively earmarked more than USD 185 billion for domestic fab construction, with each site requiring thousands of pressure, flow, and particle-count sensors to achieve ISO 14644-1 Class 1 cleanroom certification. The CHIPS Act further encourages local sensor assembly, shortening lead times for MEMS pressure dies and SOI accelerometers. New MEMS lines in Oregon and Pennsylvania broaden supply but are not expected to reach Asian economies of scale until the later part of the decade. Advanced packaging plants also deploy high-precision force sensors for chiplet alignment, supporting the upward trajectory of the USA industrial sensors market.

Acceleration of Predictive-Maintenance Programs Post-2025

Asset-intensive sectors are shifting from time-based maintenance to condition-based maintenance. Vibration and temperature sensors on boiler feed pumps have extended the mean time between failures by eight months in a Midwest power plant, while bearing-health devices detect degradation weeks ahead of catastrophic breakdowns. Banner Engineering’s QM30VT3, launched in 2026, integrates a MEMS accelerometer and RTD element with IO-Link for seamless data streaming to machine-learning models. Edge analytics trigger work orders directly in enterprise asset-management systems, cementing sensors as the cornerstone of reliability-centered maintenance strategies within the US industrial sensors market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Chip-Supply Volatility for Specialty MEMS Dies | -0.9% | Automotive, aerospace, medical devices nationwide | Medium term (2–4 years) |

| Cyber-Security Risks Inhibiting Wireless Sensor Roll-Outs | -0.7% | Critical infrastructure and defense assets | Short term (≤ 2 years) |

| High Total Cost of Ownership for Intrinsically Safe Sensors in Explosive Zones | -0.5% | Oil and gas, chemicals, mining regions | Medium term (2–4 years) |

| Standards Fragmentation Across Industrial Communications Protocols | -0.4% | Brownfield retrofits nationwide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Persistent Chip-Supply Volatility for Specialty MEMS Dies

Lead times for automotive-grade piezoresistive pressure dies and capacitive accelerometers extended beyond 26 weeks in late 2024, delaying retrofit programs. Infineon’s XENSIV and Bosch Sensortec’s BMI families faced the steepest allocation constraints. Domestic foundries funded by the CHIPS Act are ramping up production but are not expected to match Asian manufacturing capacity until at least 2028, keeping supply risks elevated. Dual sourcing and redesigns around SOI and piezoelectric alternatives increase non-recurring engineering costs, tempering near-term growth of the United States industrial sensors market.

Cybersecurity Risks Inhibiting Wireless Sensor Roll-Outs

NIST’s Cybersecurity Framework 2.0 and ISA/IEC 62443 outline security safeguards, yet fewer than 15% of installed wireless gateways currently comply with these standards.[3]National Institute of Standards and Technology, “Cybersecurity Framework 2.0,” nist.gov ICS-CERT advisories continue to flag vulnerabilities in Modbus TCP and EtherNet/IP. Rockwell Automation’s acquisition of Verve Industrial Protection embeds zero-trust architectures at the sensor edge, but critical-infrastructure operators remain cautious. This hesitation slows the migration toward higher-margin wireless devices within the US industrial sensors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Connectivity: Hybrid Topologies Bridge Reliability and Flexibility

Wired solutions captured 73.82% of the United States industrial sensors market share in 2025 due to decades-long investment in 4-20 mA and HART loops. They remain indispensable for sub-5 millisecond shutdown tasks mandated by NFPA 85 and API 670. However, wireless nodes are forecast to grow at an 8.45% CAGR through 2031 on the back of private 5G, LoRaWAN, and Ethernet-APL adoption. Greenfield semiconductor fabs deploy thousands of IO-Link temperature sensors over wireless backhaul to preserve cleanroom flexibility, while Ethernet-APL supports intrinsic-safety compliance in hydrocarbon zones. The USAindustrial sensors market is converging toward hybrid architectures in which wired loops handle safety functions and wireless layers add diagnostics.

Private cellular pilots at automotive plants show that reducing cable pulls can lower installation budgets by 40%, creating a compelling case for wireless deployment in discrete manufacturing. Conversely, brownfield chemical sites often retain wired retrofits because spectrum licenses and gateway hardware dilute the wireless value proposition. Vendors such as Emerson and Honeywell now offer unified asset-management suites that aggregate both wired and wireless data streams, demonstrating how hybrid connectivity will underpin the next growth phase of the US industrial sensors market.

By Sensor Type: Gas and Vibration Lead the Growth Curve

Pressure sensors accounted for 27.30% of the United States industrial sensors market in 2025, anchored by their widespread use across hydraulics, pneumatics, and vessels. Gas sensors represent the fastest-growing category, projected to expand at an 8.74% CAGR through 2031, propelled by EPA methane-monitoring rules and hydrogen safety codes. Emerson’s Rosemount 625IR and Honeywell’s 4-Series NDIR devices are factory-calibrated for life, significantly reducing maintenance costs. Temperature sensors benefit from biologics cold-chain expansion and wafer-fab thermal stability requirements, while flow sensors gain momentum from municipal infrastructure upgrades under the Clean Water Act. Vibration sensing, a key component of predictive maintenance, is gaining traction as IO-Link-enabled devices integrate temperature monitoring and diagnostics, increasing analytical value in the USindustrial sensors market for rotating-equipment health.

Level, proximity, and photoelectric sensors continue to modernize with radar and IO-Link interfaces, replacing mechanical floats and discrete switches. Adoption remains strong in food, beverage, and packaging lines where hygienic and wash-down requirements are critical. Ultrasonic and radar technologies deliver non-contact measurement that improves sanitation compliance, underscoring broad-based diversification across the USA industrial sensors market.

By End-User Industry: Life Sciences Outpaces a Still-Dominant Oil and Gas Base

Oil and gas contributed 19.75% of the United States industrial sensors market demand in 2025, supported by pipeline integrity, refinery automation, and upstream well monitoring. However, the pharmaceutical and life sciences segment is the fastest-growing end-user industry, projected to expand at a 7.92% CAGR as biologics plants proliferate and FDA digital-record mandates gain traction. Emerson’s Rosemount 490A optical dissolved-oxygen sensor and Vaisala’s cleanroom probes exemplify demand for permanently stable, maintenance-free instrumentation.[4]U.S. Food and Drug Administration, “21 CFR Part 11,” fda.gov

Automotive customers operate across both legacy internal combustion engine (ICE) assets and expanding EV battery lines, creating diverse requirements ranging from high-temperature exhaust sensing to cell-pressure monitoring. Water and wastewater utilities are deploying more turbidity and dissolved-oxygen sensors to comply with federal discharge permits, while food and beverage processors are adopting 3-A-certified pressure and level devices for sanitary compliance. Power generators integrate vibration sensors to reduce turbine-failure risks, and chemical plants specify ATEX-certified gas detectors to address flammable environments. The breadth of applications underscores the resilience of the United States industrial sensors market across economic cycles.

Geography Analysis

Manufacturing and process clusters across the Midwest and Gulf Coast anchor a large installed base of wired instrumentation, generating stable replacement revenues for the United States industrial sensors market. Texas hosts extensive refinery and petrochemical activity, driving sustained demand for intrinsically safe pressure and gas sensors. California leads early hydrogen-hub deployments and battery storage installations, increasing demand for advanced leak detectors and state-of-charge monitors.

Arizona and Ohio have emerged as semiconductor manufacturing hubs following major fab announcements, triggering strong demand for ultra-clean pressure, flow, and particle sensors. New York’s memory-fabrication project and the Pacific Northwest’s MEMS foundry expansions shorten lead times for specialty dies, although scale advantages remain modest compared with Asia. These pockets of high-precision demand diversify the regional profile of the United States industrial sensors market.

Offshore wind corridors along the Atlantic coast now specify Class I Division 1 pressure and flow sensors capable of withstanding salt spray and explosive risks, while Midwest automotive plants are experimenting with private 5G vibration sensing to reduce downtime. The Rocky Mountain states are witnessing incremental adoption tied to mining and power-generation facilities, and the Southeast’s expanding EV battery corridor requires temperature and pressure devices for gigafactory quality control. The geographic spread confirms that localized policy incentives and industrial footprints will continue to shape the trajectory of the United States industrial sensors market.

Competitive Landscape

The market demonstrates moderate fragmentation, with the top five suppliers, Emerson, Honeywell, ABB, Rockwell Automation, and Endress+Hauser, controlling an estimated 30-35% share through proprietary protocols and long-term service contracts. Emerson’s Rosemount 4051S pressure transmitter offers a 20-year warranty and 800:1 turndown ratio, strengthening customer loyalty in process industries.[5]Emerson Electric, “Rosemount 4051S Pressure Transmitter,” emerson.com Rockwell Automation’s acquisition of Verve Industrial Protection embeds zero-trust defenses directly at the sensor edge, aligning with evolving customer cybersecurity priorities.

Honeywell and ABB are deepening customer retention by bundling analytics platforms that contextualize multi-vendor sensor data, while Endress+Hauser’s partnership with Sick AG broadens its laser-based gas-analysis offerings. Smaller challengers, including Banner Engineering, IFM Efector, and Pepperl+Fuchs, are expanding within discrete manufacturing through IO-Link sensors that deliver advanced diagnostics without requiring complete control-system replacement. Their agile product-development cycles enable them to address emerging niches such as hydrogen detection more rapidly than larger incumbents.

Component suppliers such as Analog Devices, Infineon, and Texas Instruments focus on MEMS dies, ASICs, and analog-to-digital (A-to-D) converters, capturing value higher in the signal chain. Standards-body leadership by ABB, Emerson, and Siemens within the OPC Foundation and FieldComm Group enables these firms to influence future specifications toward architectures that favor their installed bases. The interplay of hardware innovation, protocol influence, and service bundling is expected to keep competitive intensity moderate in the United States industrial sensors market.

United States Industrial Sensors Industry Leaders

TE Connectivity Ltd

Omega Engineering Inc.

Honeywell International Inc.

Rockwell Automation Inc.

Texas Instruments Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Honeywell introduced the 4-Series NDIR hydrocarbon gas sensor with parts-per-million sensitivity for oil and gas safety.

- February 2026: Banner Engineering launched the QM30VT3 vibration and temperature sensor with IO-Link connectivity.

- April 2025: Emerson launched the Rosemount 490A optical dissolved-oxygen sensor targeting biopharma and water treatment.

- March 2025: Endress+Hauser finalized a strategic partnership, transferring 800 Sick AG personnel to expand gas analysis offerings.

United States Industrial Sensors Market Report Scope

The United States industrial sensors market comprises devices and sensing technologies used to detect, measure, and transmit real-time operational and environmental data for industrial automation, process control, equipment monitoring, predictive maintenance, and safety applications. The market is driven by increasing adoption of IIoT, smart manufacturing, and advanced industrial automation across discrete and process industries.

The United States Industrial Sensors Market Report is segmented by Connectivity (Wired Solutions, and Wireless Solutions), Sensor Type (Pressure Sensors, Flow Sensors, Temperature Sensors, Level Sensors, Gas Sensors, Proximity and Photoelectric Sensors, Vibration Sensors, and Other Types of Sensors), and End-User Industry (Oil and Gas, Chemicals and Petrochemicals, Water and Wastewater, Food and Beverage, Power Generation, Automotive, Pharmaceutical and Life Sciences, Aerospace and Defense, and Other End-User Industries). The market forecasts are provided in terms of value (USD).

| Wired Solutions |

| Wireless Solutions |

| Pressure Sensors |

| Flow Sensors |

| Temperature Sensors |

| Level Sensors |

| Gas Sensors |

| Proximity and Photoelectric Sensors |

| Vibration Sensors |

| Other Types of Sensors |

| Oil and Gas |

| Chemicals and Petrochemicals |

| Water and Wastewater |

| Food and Beverage |

| Power Generation |

| Automotive |

| Pharmaceutical and Life Sciences |

| Aerospace and Defense |

| Other End-User Industries |

| By Connectivity | Wired Solutions |

| Wireless Solutions | |

| By Sensor Type | Pressure Sensors |

| Flow Sensors | |

| Temperature Sensors | |

| Level Sensors | |

| Gas Sensors | |

| Proximity and Photoelectric Sensors | |

| Vibration Sensors | |

| Other Types of Sensors | |

| By End-User Industry | Oil and Gas |

| Chemicals and Petrochemicals | |

| Water and Wastewater | |

| Food and Beverage | |

| Power Generation | |

| Automotive | |

| Pharmaceutical and Life Sciences | |

| Aerospace and Defense | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the United States industrial sensors market?

The United States industrial sensors market size stood at USD 18.89 billion in 2026 and is projected to reach USD 26.52 billion by 2031, reflecting a 6.93% CAGR (Mordor Intelligence).

Which connectivity segment is expanding fastest?

Wireless solutions are forecast to grow at an 8.45% CAGR through 2031 as private 5G and Ethernet-APL gain traction across new factories (Mordor Intelligence).

Which sensor type shows the highest growth rate?

Gas sensors lead with an 8.74% CAGR to 2031, driven by methane-monitoring rules and hydrogen infrastructure investments (Mordor Intelligence).

Which industry vertical is adopting sensors most quickly?

Pharmaceutical and life sciences is the fastest-growing user segment at 7.92% CAGR, supported by biologics manufacturing and FDA electronic record mandates (Mordor Intelligence).

What restraint could slow wireless sensor adoption?

Cyber-security risks remain a major concern, with fewer than 15% of installed gateways compliant with ISA/IEC 62443 and NIST CSF 2.0 standards.

How are companies differentiating their sensor offerings?

Leading vendors emphasize lifetime-calibrated devices, extended warranties, and embedded cybersecurity, shifting competition toward total lifecycle value rather than upfront hardware cost.

Page last updated on: