Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 12.76 Billion |

| Market Size (2026) | USD 13.24 Billion |

| Market Size (2031) | USD 15.95 Billion |

| Growth Rate (2026 - 2031) | 3.79% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Travel Retail Market Analysis by Mordor Intelligence

The North America travel retail market size was valued at USD 12.76 billion in 2025 and estimated to grow from USD 13.24 billion in 2026 to reach USD 15.95 billion by 2031, at a CAGR of 3.79% during the forecast period (2026-2031). Operators are transitioning from simple post-pandemic volume recovery to experience-led differentiation that persuades travellers to spend more on each trip, a strategic pivot validated by the finding that four out of five passengers will boost their spending when airports enhance the overall journey. International enplanements climbed to 23.234 million in December 2024, 7% above the prior year, providing a solid traffic base that underpins steady retail receipts [1]International Trade Administration, “December 2024 Air Passenger Travel,” trade.gov. This resilient demand enables concessionaires to test higher-margin assortments, deploy cashier-less technologies, and negotiate longer-term space rights in redeveloped terminals. As a result, the North America travel retail market continues to mature into a data-driven, passenger-centric ecosystem where experience quality outweighs simple product availability.

Key Report Takeaways

- By product category, Fragrances & Cosmetics captured 32.05% of the North America travel retail market share in 2025 and is expanding at a 11.92% CAGR through 2031.

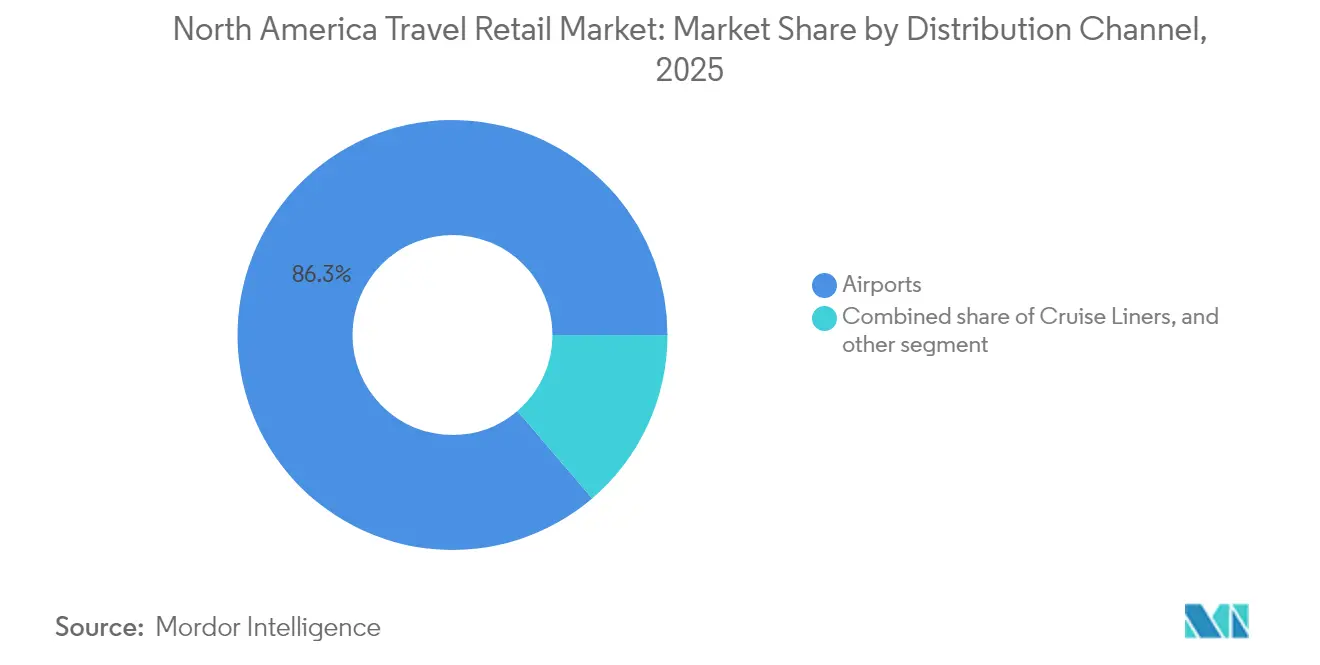

- By distribution channel, airports commanded 86.25% of the North America travel retail market size in 2025, while cruise liners are projected to log the fastest 8.96% CAGR toward 2031.

- By traveller demographic, leisure travellers accounted for 56.10% of the North America travel retail market share in 2025, whereas medical & wellness tourists are rising at a 13.04% CAGR to 2031.

- By geography, the United States held 70.88% of the North America travel retail market share in 2025, yet Mexico is forecast to grow at a 9.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Travel Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rebound in international air passenger traffic | +1.2% | U.S.–Mexico corridors, pan-regional hubs | Short term (≤ 2 years) |

| Expansion of airport retail footprints & concession upgrades | +0.8% | JFK, DFW, YYZ, YVR | Medium term (2-4 years) |

| Rising spend per passenger via premiumization | +0.9% | Long-haul business routes | Long term (≥ 4 years) |

| Strong performance of fragrances & cosmetics | +0.7% | International departure concourses | Medium term (2-4 years) |

| Growth of private jet & FBO duty-free | +0.3% | U.S. domestic network, selective Canadian bases | Long term (≥ 4 years) |

| Contactless checkout technologies | +0.4% | Major U.S. hubs, pilot rollouts across Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rebound in International Air Passenger Traffic

North American carriers recorded a 28.3% jump in traffic during 2023 compared with 2022, regaining 84.6% of 2023 volumes and restoring the essential passenger base that drives the North America travel retail market [2]International Air Transport Association, “Global Air Travel Demand Continued Its Bounce Back in 2023,” iata.org . International travellers typically out-spend domestic flyers by a factor of three to four, so the rebound instantly translates into stronger retail cash flow. Leisure traffic already surpasses pre-pandemic highs, while business travel remains lower; nevertheless, business travellers still generate premium category sales that cushion overall yields. Mexico contributed 4.002 million international passengers in December 2024, underscoring its emergence as a pivotal growth node linked to upgraded tourism infrastructure and new air-service agreements. Looking forward, Boeing’s 20-year outlook for 43,975 aircraft deliveries ensures adequate lift to sustain volume expansion, reinforcing the long-range health of the North America travel retail market [3]Boeing, “2024 Commercial Market Outlook,” boeing.com .

Expansion of Airport Retail Footprints & Concession Redevelopments

Massive infrastructure programs are redefining commercial space inside major hubs. JFK’s USD 19 billion transformation adds a retail boulevard designed to anchor luxury, dining, and experiential activations, redefining shopping from a convenience add-on into a destination in its own right [4]TRBusiness, “Hudson and Dufry to Run Retail at JFK Terminal 6,” trbusiness.com. Research shows that every 10% rise in passenger dwell time boosts non-aeronautical revenues by roughly 5%, validating airport authority priorities that extend seating, power outlets, and entertainment features to keep travellers engaged. Operators with the financial capability to invest in white-box build-outs, leverage integrated digital engagement strategies, and implement rapid assortment rotations are well-positioned to unlock incremental value within the North American travel retail market. These strategic capabilities allow businesses to respond effectively to evolving consumer preferences, optimize operational efficiency, and strengthen their competitive positioning in a highly dynamic and competitive market landscape.

Rising Spend Per Passenger via Premiumization

Travelers have begun to treat the terminal as the opening chapter of their trip rather than a waiting room. In 2024, 64% of passengers chose to dine during dwell time, eclipsing traditional retail for the very first time and signalling a wider pivot toward experience-oriented consumption. Luxury brands capitalize by launching airport-exclusive capsules and concierge-style services: Byredo’s flagship boutique at LAX demonstrates the magnetic power of high-end fragrances in a captive environment. The monetization of lounge access reflects a strategic shift in consumer spending behaviour, with an increasing number of travellers opting to pay for entry. This trend underscores a growing preference for integrated service-product offerings over standalone products, indicating a transformation in value perception within the travel industry. Generation Z and Millennials, who together will make up the majority of flyers beyond 2026, elevate authenticity and share-worthy moments, forcing retailers to embed storytelling, live demonstrations, and social-media backdrops within the physical store footprint. These dynamics sustain a higher average ticket and solidify premiumization as a multi-year driver of the North America travel retail market.

Strong Performance of Fragrances & Cosmetics Category

Fragrances & Cosmetics enjoy unique advantages that e-commerce cannot easily replicate. Estée Lauder continues to champion travel retail despite macro headwinds, while L’Oréal broadened Armani Beauty counters across top North American airports, signalling brand confidence in the channel’s premium positioning capacity. Margins outshine alcohol and tobacco because beauty products face fewer regulatory hurdles, and product spoilage is minimal. Ultra-premium initiatives, such as Dufry’s haute-perfumeries concept featuring USD 800 SKUs, target affluent flyers who equate scarcity with status. By marrying exclusivity with personalized service, beauty counters amplify conversion and strengthen the overall revenue mix within the North America travel retail market.

Restraints Impact Analysis*

| Restraint | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent customs limits on tobacco & alcohol | -0.6% | U.S.–Canada land crossings, international arrivals | Long term (≥ 4 years) |

| Competition from downtown duty-free & e-commerce | -0.4% | Major metropolitan cores, cross-border shopping districts | Medium term (2-4 years) |

| Slot-constrained U.S. gateway airports | -0.3% | JFK, Newark, LaGuardia | Short term (≤ 2 years) |

| Wellness shift curbing alcohol demand | -0.5% | North America, most acute among younger cohorts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Customs Limits on Tobacco & Alcohol Allowances

Regulatory restrictions are limiting growth opportunities in the high-margin liquor and tobacco markets. Canadian regulations impose strict limits on the quantities of alcohol that residents can bring back after trips lasting at least 48 hours. These limits include 1.5 liters of wine, 1.14 liters of spirits, or 8.5 liters of beer. Such constraints significantly restrict consumer purchase volumes, thereby impacting overall market expansion potential. Comparable U.S. restrictions similarly limit duty-free uptake, particularly at land-border outlets. Although USMCA raised Canada’s courier de minimis threshold to CAD 150, the benefit flows mainly to e-commerce rather than bricks-and-mortar travel retail. Retailers respond by reallocating shelf space to beauty, fashion, and local gourmet lines that face lighter regulatory drag but yield comparable margins.

Competition from Downtown Duty-Free & E-Commerce

Online transparency erodes the airport’s historical price advantage. City-centre duty-free stores now mirror airport assortments without the time pressure of final boarding, while digital storefronts deliver tax-advantaged goods directly to consumers’ homes. Only 15% of younger travellers bypass airport digital channels altogether, underscoring the need for seamless online-to-offline engagement strategies. Reserve-and-collect services attempt to bridge convenience gaps yet demand real-time inventory visibility and last-mile logistics that smaller concessionaires find capital-intensive. The incentive, therefore, is to elevate in-store sensory experiences, tastings, product personalization, and interactive demonstrations that cannot be replicated through a smartphone screen.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Beauty Leadership Reshapes Category Mix

Fragrances & Cosmetics dominated with 32.05% of the North America travel retail market share in 2025, and the sub-segment will add revenue at a 11.92% CAGR through 2031, underscoring its pivotal role in sustaining premiumization. Wine & Spirits holds strong average receipt value but labours under duty caps and wellness-driven moderation trends. Tobacco’s structural decline continues, but it still drives footfall among committed smokers who also cross-shop high-margin snacks and accessories. Fashion & Accessories capture impulse luxury purchases through limited-edition drops timed with seasonal travel peaks. Food & Confectionery enjoys a stable gifting and souvenir niche, boosted by Mars Wrigley’s refreshed M&M’s and Maltesers lines geared toward premium flavour profiles. Other product types, including electronics, watches, and jewellery, retain relevance via hands-on testing and instant ownership satisfaction that online channels cannot match.

Retailers allocate prime post-security real estate to beauty because conversion spikes when passengers exit screening. Digital testers, augmented-reality mirrors, and expert-led curation speed shopper decision-making, vital when boarding time looms. Liquor brands shrink bottle sizes for compliance and highlight gift sets priced to align with customs allowances. Confectionery labels invest in storytelling around origin and sustainability, targeting ethically minded flyers. The net effect balances the North America travel retail market portfolio, reducing reliance on any single category and insulating revenue from regulatory swings.

By Distribution Channel: Airport Dominance Meets Efficiency Mandate

Airports generated 86.25% of the North America travel retail market size in 2025, and while expected growth sits at 8.15% CAGR, physical expansion remains constrained by slot-controlled capacity at legacy hubs. Hudson's implementation of Amazon-powered Just Walk Out technology at JFK and Dulles airports has significantly enhanced operational efficiency by reducing average checkout times to under 30 seconds. This technological advancement enables the company to optimize turnover rates per square foot, demonstrating that operational efficiency, rather than merely increasing physical store size, is a critical driver of revenue growth and profitability.

Cruise liners represent a comparatively small slice but benefit from multi-day dwell periods where relaxed vacationers engage deeply with onboard boutique assortments. Railway stations lag, reflecting North America’s limited intercity rail network relative to Europe or Japan. Border and downtown duty-free stores fight ecommerce headwinds but gain share among cross-border bargain hunters and city tourists. Private terminal duty-free remains nascent yet lucrative, catering to affluent travellers willing to pay premiums for bespoke assortments.

By Traveler Demographics: Wellness Tourists Outpace Leisure Core

Leisure travellers comprised 56.10% of the North America travel retail market in 2025, powered by pent-up vacation demand and flexible remote-work policies that extend trip lengths. Business travellers, while representing a smaller segment in terms of volume, consistently generate the highest average expenditure per trip. Their spending patterns are heavily skewed towards premium categories such as high-end liquor, advanced tech accessories, and health supplements. This segment's purchasing behaviour reflects a preference for quality and convenience, making them a lucrative target for retailers. In contrast, the visiting friends and relatives (VFR) segment provides a stable and counter-cyclical demand base, driven by strong immigration and diaspora connections. This segment ensures consistent travel flows, even during periods of economic uncertainty, offering retailers a dependable revenue stream.

Additionally, student travellers contribute significantly to travel frequency but exhibit a strong inclination towards cost-effective products, particularly in electronics and fashion categories, highlighting their price-sensitive nature. Retailers strategically align their offerings to cater to the specific needs and preferences of these diverse traveller segments. For wellness-focused visitors, curated "recovery kits" address their health and relaxation needs, while leisure travellers are drawn to sense-of-place memorabilia that enhances their travel experience. For time-constrained business executives, retailers prioritize efficiency by offering time-saving mobile checkout solutions. By tailoring their strategies to the unique demands of each segment, retailers aim to optimize conversion rates and maximize revenue opportunities across the travel retail market.

Geography Analysis

In 2025, the United States accounted for 70.88% of the North America travel retail market share. This dominance can be attributed to the presence of the continent's most extensive network of international gateways, coupled with a consistently high monthly volume of foreign passenger traffic. JFK’s USD 19 billion redevelopment alone adds 28,000 sq ft of new retail, illustrating how even mature nodes can unlock incremental value through design overhauls and experiential layering. Yet capacity caps at coastal hubs create scarcity that pushes operators to hone revenue-per-square-foot metrics through AI-driven planograms, dynamic pricing models, and cross-trained staff who fluidly move between categories. Contactless payment adoption hits critical mass, shortening dwell time at the point of sale and improving customer flow.

Canada remains smaller but strategically important, serving as a Pacific and trans-Atlantic bridge. Regulatory friction on alcohol and tobacco compresses category mix, so operators emphasize beauty, fashion, and local artisanal goods with lighter duty constraints. Toronto Pearson and Vancouver International spearhead digital engagement by piloting reserve-and-collect kiosks and biometric payments that reduce queue time. Duty-free stores also benefit from a rebound in Asia-Pacific arrivals, who display a robust appetite for luxury SKUs despite currency volatility.

Mexico delivers the fastest path at 9.92% CAGR through 2031, propelled by rising middle-class tourism, upgraded airports, and cross-border shopping synergies. Cancun, Mexico City, and Guadalajara airports are rolling out expansions via public-private partnerships that embed modern retail formats from day one. Currency arbitrage against the USD stimulates discretionary spending among U.S. visitors, while Mexican outbound shoppers gravitate toward beauty and fashion categories that still offer price advantages compared to domestic channels. Hybrid cross-border terminals, such as Tijuana–San Diego, pioneer dual-country duty-free models that exploit differing regulatory regimes to widen assortment breadth. The net result is a more diversified North America travel retail market revenue mix, reducing over-reliance on U.S. gateway performance.

Competitive Landscape

The North America travel retail market exhibits a moderately concentrated structure, with a significant portion of the market controlled by leading operators such as Avolta (a merger of Hudson and Dufry), HMSHost, Paradies Lagardère, WHSmith North America, and 3Sixty Duty Free. These dominant players collectively hold a substantial market share, yet the market dynamics continue to present opportunities for niche players to enter and establish a foothold. Technology is the decisive competitive lever: Hudson’s cashier-less outlets powered by Amazon’s Just Walk Out algorithms cut transaction times and raise conversion, while Paradies Lagardère pilots Scan-Pay-Go mobile checkout lines that shorten queuing without sacrificing basket size.

WHSmith’s 2025 migration to a cloud-native retail platform enables unified inventory and CRM analytics across what will be 500 U.S. stores by 2028. Avolta pushes premium beauty environments and exclusive boutique collaborations, while HMSHost combines food & beverage with curated retail to extend dwell-time monetization. Emerging white-space includes private-jet duty-free, wellness-centric concepts, and omnichannel tie-ins that merge downtown flagship stores with airport collection points. Smaller regional specialists exploit local-culture storytelling to secure ACDBE-compliant contracts, keeping competitive pressure high despite the scale advantages of incumbents.

North America Travel Retail Industry Leaders

Dufry (Hudson)

Duty Free Americas

Paradies Lagardère

WH Smith (InMotion)

WH Smith (InMotion)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: HMSHost expanded its Dallas-Fort Worth partnership under a 10-year contract, unveiling Velvet Taco, La La Land Kind Café, and Nékter Juice Bar within the airport’s USD 12 billion capital plan.

- May 2025: HMSHost secured a 10-year deal to revitalize JFK Terminal 5 dining, introducing local favorites like Eataly and Dos Toros with self-order kiosks and digital waitlists.

- April 2025: URW selected Duty Free Americas to run duty-free in JFK’s new Terminal One, strengthening DFA’s premium-gateway positioning.

- January 2025: Puig and DFS launched the first West Coast Byredo travel retail boutique at LAX, deepening luxury fragrance penetration on high-yield routes.

North America Travel Retail Market Report Scope

'Travel retail' is a term that commonly refers to sales made in travel environments where customers require proof of travel to access the commercial area, but which are subject to taxes and duties.A complete background analysis of the North America carpet tile market, which includes an assessment of the emerging trends by segments and regional markets, significant changes in market dynamics, and market overview, is covered in the report. North America Travel Retail Market is Segmented By Product Type (Fashion and Accessories, Jewelry and Watches, Wine & Spirits, Food & Confectionery, Fragrances and Cosmetics, Tobacco, Others (Stationery, Electronics, etc.)), By Distribution Channel (Airports, Airlines, Ferries, Other(Railway Stations, Border, Downtown)) and By Geography (United States and Canada).

By Product Type

| Fashion and Accessories |

| Wine and Spirits |

| Tobacco |

| Food and Confectionery |

| Fragrances and Cosmetics |

| Other Product Types (Stationery, Electronics, Watches, Jewelry, etc.) |

By Distribution Channel

| Airports |

| Cruise Liners |

| Railway Stations |

| Other Distribution Channels |

By Traveler Demographics

| Business Travelers |

| Leisure Travelers |

| Visiting Friends and Relatives (VFR) |

| Medical and Wellness Tourists |

| Student Travelers |

By Geography

| Canada |

| United States |

| Mexico |

| By Product Type | Fashion and Accessories |

| Wine and Spirits | |

| Tobacco | |

| Food and Confectionery | |

| Fragrances and Cosmetics | |

| Other Product Types (Stationery, Electronics, Watches, Jewelry, etc.) | |

| By Distribution Channel | Airports |

| Cruise Liners | |

| Railway Stations | |

| Other Distribution Channels | |

| By Traveler Demographics | Business Travelers |

| Leisure Travelers | |

| Visiting Friends and Relatives (VFR) | |

| Medical and Wellness Tourists | |

| Student Travelers | |

| By Geography | Canada |

| United States | |

| Mexico |

Key Questions Answered in the Report

How large is the North America travel retail in 2026?

Sales reached USD 13.24 billion in 2026.

Which product category leads duty-free sales in the region?

Fragrances & Cosmetics command 32.05% share and post the quickest 11.92% CAGR through 2031.

What is the projected CAGR for the sector between 2026 and 2031?

Spending is forecast to rise at a 3.79% CAGR over the period.

Which traveler demographic is expanding the fastest?

Medical & wellness tourists are advancing at a 13.04% CAGR to 2031.

Why do airports remain the dominant retail channel?

Airports hold 86.25% share thanks to captive footfall, duty-free pricing and sustained infrastructure investment.

Which country shows the fastest growth through 2031?

Mexico is projected to progress at a 9.92% CAGR as tourism infrastructure and cross-border travel expand.

Page last updated on: