Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

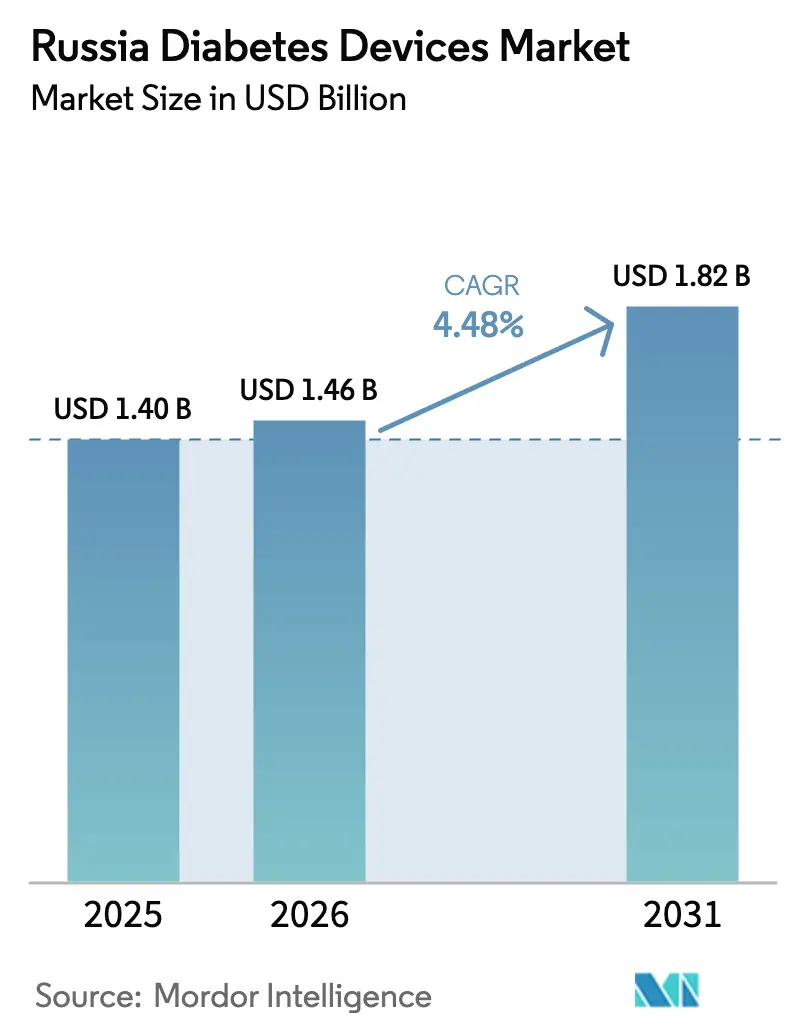

| Base Year Market Size (2025) | USD 1.40 Billion |

| Market Size (2026) | USD 1.46 Billion |

| Market Size (2031) | USD 1.82 Billion |

| Growth Rate (2026 - 2031) | 4.48% CAGR |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Diabetes Devices Market Analysis by Mordor Intelligence

The Russia diabetes devices market size was valued at USD 1.40 billion in 2025 and estimated to grow from USD 1.46 billion in 2026 to reach USD 1.82 billion by 2031, at a CAGR of 4.48% during the forecast period (2026-2031). Consistent public-health funding, rapid localisation of production, and expanding reimbursement for continuous glucose monitoring sustain this steady growth despite sanctions-related headwinds. Domestic manufacturers increasingly fill supply-chain gaps, while urban centres adopt hybrid closed-loop systems that enhance glycaemic control and reduce long-term complications. Procurement reforms that prioritise locally registered devices further accelerate market penetration for sensor-based monitoring, and tele-health integration extends advanced care to rural populations. Intensifying competition, particularly in continuous glucose monitoring sensors and smart insulin delivery, fosters incremental innovation as firms seek accuracy gains, longer wear times, and smartphone connectivity.

Key Report Takeaways

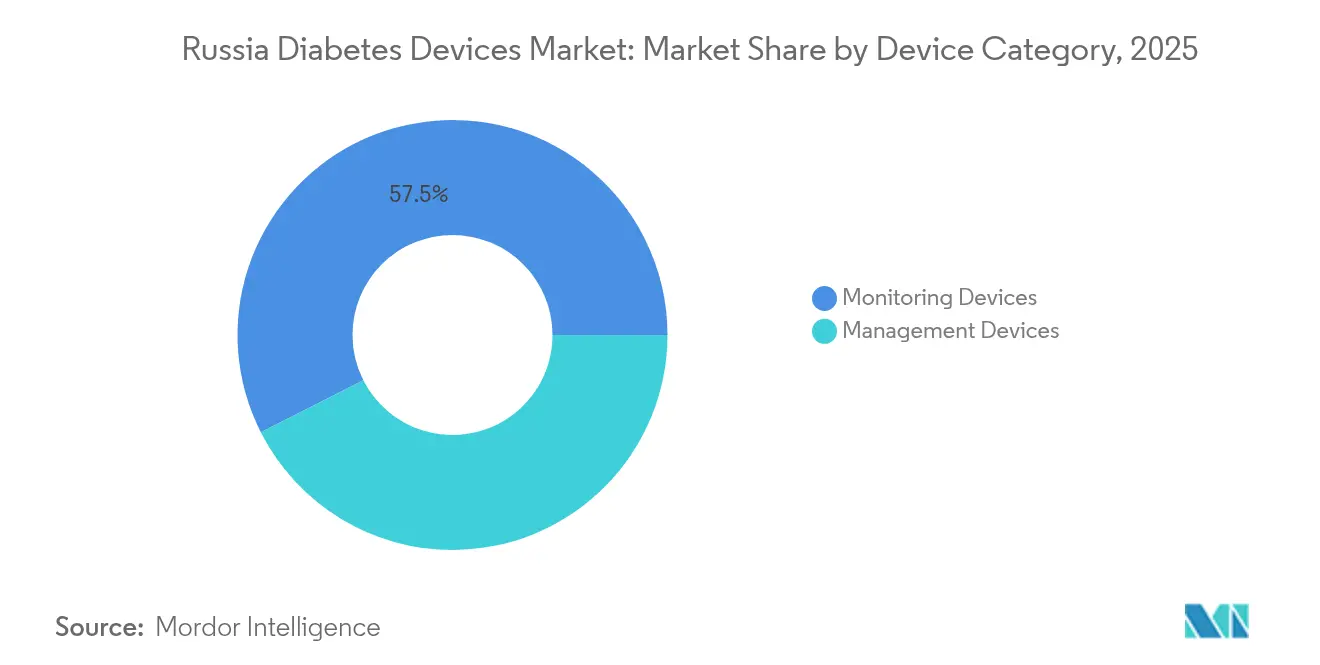

- By device category, monitoring devices led with 57.48% of the Russia diabetes devices market share in 2025, while management devices registered the fastest 5.02% CAGR through 2031.

- By distribution channel, the offline segment retained 67.35% share of the Russia diabetes devices market size in 2025; the online channel is projected to expand at 5.28% CAGR to 2031.

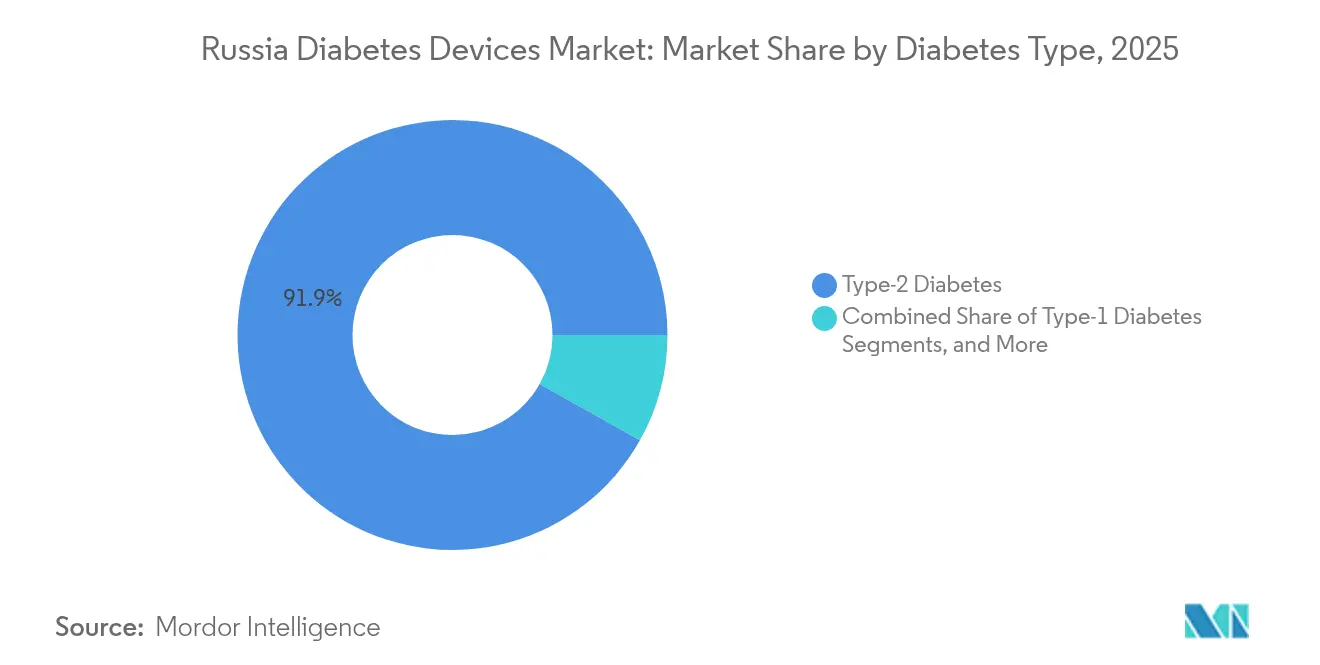

- By diabetes type, Type-2 cases accounted for 91.85% of the Russia diabetes devices market size in 2025 and are forecast to grow at a 5.12% CAGR between 2026 and 2031.

- By end user, home-care settings captured 67.10% Russia diabetes devices market size in 2025, while hospitals and specialty clinics are advancing at a 4.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Diabetes Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diabetes prevalence & earlier diagnosis | +1.2% | National, concentrated in urban centers | Medium term (2-4 years) |

| Expansion of state reimbursement for CGM & SMBG | +0.8% | National, with priority regions receiving enhanced funding | Short term (≤ 2 years) |

| Shift to sensor-based monitoring & hybrid closed-loop pumps | +0.9% | Major metropolitan areas, expanding to regional centers | Medium term (2-4 years) |

| Rising prevalence of obesity among youth increasing earlier onset diabetes | +0.6% | National, with higher impact in developed regions | Long term (≥ 4 years) |

| Remote monitoring integration with national tele-health platforms | +0.7% | National rollout, starting with pilot regions | Medium term (2-4 years) |

| University-led R&D in non-invasive microwave & MIR sensors | +0.4% | Research clusters in Moscow, St. Petersburg, Tomsk | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes Prevalence & Earlier Diagnosis

More than 5 million diagnosed diabetics and an estimated 8–9 million undiagnosed Russians underscore the expanding addressable base for the Russia diabetes devices market. Mobile medical centres such as Diamodul deliver HbA1c screening in regional towns, triggering earlier clinical intervention. The economic burden, equivalent to 1% of GDP, incentivises federal grants for point-of-care systems that shorten diagnostic delays. Urban screening programmes reveal sizeable gaps between actual and registered patient numbers, increasing demand for self-monitoring devices outside traditional hospital settings. Federal diabetes registries now track individual outcomes, enabling targeted subsidies that enhance device uptake.

Expansion of State Reimbursement for CGM & SMBG

The Federal Compulsory Medical Insurance Fund earmarked 4.5 trillion RUB for 2025–2027, widening coverage for continuous glucose monitors and self-monitoring meters. Reimbursement rules classify CGM sensors as technical rehabilitation aids, lowering patient co-pays and raising utilisation in paediatric endocrinology. Preferential procurement for locally produced systems channels demand toward domestic brands, shielding supply chains from import restrictions. Regional health budgets receive supplemental transfers that finance bulk purchases for specialist diabetes centres. As devices become reimbursable within outpatient clinics, adoption curves steepen in secondary cities previously constrained by limited funding.

Shift to Sensor-Based Monitoring & Hybrid Closed-Loop Pumps

Clinical evidence highlights the Glunovo real-time CGM’s 8.89% mean absolute relative difference versus lab standards [1]Marina Solovieva, “Real-Time Continuous Glucose Monitoring Accuracy in Russian Adults With Diabetes,” Frontiers in Endocrinology, frontiersin.org. Success of such products accelerates the migration from finger-stick testing to continuous monitoring in tertiary hospitals. Hybrid closed-loop pumps introduced through international alliances create new benchmarks for automated insulin delivery, although high list prices temper broad adoption. Russian-language marketing emphasises app-based glucose visualisation that aligns with national digital-health targets. Emerging domestic players prototype integrated pump-sensor platforms to meet demand for locally manufactured solutions compatible with state reimbursement.

Remote Monitoring Integration with National Tele-Health Platforms

Pandemic-era regulatory sandboxes allowed diabetes data to feed directly into the federal tele-medicine backbone. AI-enhanced electronic-health-record platforms, exemplified by Webiomed, flag high-risk patients for proactive outreach. Cloud dashboards link CGM feeds with comorbidity indicators, enabling physicians to adjust regimens without in-person visits. Rural dwellers previously travelling long distances for endocrinology consults now receive dosage guidance via secure messaging. Legislative support under the Artificial Intelligence federal project ensures continuing investment in predictive analytics that complement device hardware.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost & partial insurance coverage gaps | -0.9% | National, with higher impact in lower-income regions | Short term (≤ 2 years) |

| Sanctions-driven supply-chain disruptions for imported consumables | -1.1% | National, affecting all import-dependent devices | Short term (≤ 2 years) |

| Lengthy Roszdravnadzor device registration timelines | -0.6% | National regulatory bottleneck | Medium term (2-4 years) |

| Warranty/after-sales issues for grey-market imports | -0.4% | Urban centers with higher grey market activity | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost & Partial Insurance Coverage Gaps

Cost-effectiveness assessments show potential savings of 51.97 million RUB per year from intensive monitoring, yet many Type-2 patients still finance sensors out of pocket [2]Oleg Sokolov, “Cost-Benefit Analysis of Continuous Glucose Monitoring in Russian Type-2 Diabetes Care,” Journal of Diabetes Science and Technology, journals.sagepub.com. Insurance formularies often cover basic meters but exclude CGM for non-insulin users, limiting penetration in provincial regions. Income disparities magnify affordability issues even where reimbursement exists, as co-payments remain material relative to household budgets. Hospitals respond by offering loan programmes for advanced systems, though uptake depends on philanthropic funding. Gradual convergence with Eurasian Economic Union (EAEU) benefit packages could equalise coverage over time, but near-term access gaps persist.

Sanctions-Driven Supply-Chain Disruptions for Imported Consumables

Logistics bottlenecks elevate costs for sensors, infusion sets and strip reagents, particularly those requiring cold-chain transport. Some clinics resort to grey-market imports that arrive without warranty, increasing risk of device failure. Domestic capacity expansion narrows shortages for select categories, yet specialist items like long-wear CGM adhesives remain dependent on foreign inputs. Multinational firms consolidate shipping through Eurasian hubs to bypass direct sanctions, but extended lead times force hospitals to hold higher safety stock. These pressures dampen short-term unit growth until domestic substitutions fully mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Category: Monitoring Devices Dominate, Management Innovations Accelerate

Monitoring devices accounted for 57.48% of the Russia diabetes devices market share in 2025, anchored by widespread adoption of self-monitoring blood glucose meters. The Contour Plus One platform illustrates meter evolution, pairing Bluetooth data sync with dietary logging that elevates patient engagement. Continuous glucose monitoring systems now represent the fastest sub-segment as tertiary centres document improved time-in-range metrics that reduce costly complications. The Russia diabetes devices market size for monitoring will climb in tandem with expanded reimbursement that lowers sensor ownership barriers.

Insulin pumps, smart pens and jet injectors comprise management devices and post a 5.02% CAGR through 2031. Federal paediatric programmes subsidise pump therapy, boosting adherence among children. Yet discontinuation rates hover high due to consumable costs and technical complexity; only 24.2% of adolescents using pumps achieve target HbA1c compared with 43.6% of younger children . The convergence of AI-driven glucose forecasting and adaptive basal algorithms promises to bridge this gap, positioning management devices as the principal innovation frontier within the Russia diabetes devices market.

By Distribution Channel: Offline Scale Meets Online Momentum

Offline channels—hospitals, clinics and retail pharmacies—held 67.35% of the Russia diabetes devices market size in 2025. Their dominance reflects entrenched physician-patient consult patterns and the need for hands-on training during device initiation. Procurement portals such as the state Unified Information System facilitate tendering for high-volume consumables, securing advantageous pricing for public institutions.

Conversely, the online channel expands at 5.28% CAGR as digital marketplaces simplify direct-to-consumer sales. E-pharmacies integrate electronic insurance verification, allowing eligible patients to redeem subsidised devices without brick-and-mortar visits. Remote regions benefit most, cutting travel costs and easing access to specialty sensors unavailable locally. Manufacturers leverage online storefronts to collect user analytics that guide firmware updates, reinforcing data-centric competition within the broader Russia diabetes devices market.

By Diabetes Type: Type-2 Drives Volume, Type-1 Spurs Technology Uptake

Type-2 patients contributed 91.85% of 2025 revenue and will advance at a 5.12% CAGR, underpinning the Russia diabetes devices market size expansion. Rising obesity and sedentary lifestyles push earlier onset, prompting clinicians to prescribe CGM beyond insulin-dependent cohorts.

Type-1 patients, though numerically smaller, adopt advanced pumps and hybrid closed-loop systems faster due to intensive insulin regimens. Gestational and other rare diabetes categories remain niche, yet improved screening during prenatal care increases sensor demand for short-term monitoring. As predictive analytics spread, multi-parameter wearables will likely serve comorbid metabolic disorders, intertwining cardiovascular metrics with glucose data across the Russia diabetes devices market.

By End User: Home-Care Prevails, Hospitals Gain Strategic Importance

Home-care environments captured 67.10% of the Russia diabetes devices market size in 2025 because daily glucose checks suit self-management. Smartphone-linked meters allow instant data uploads, enabling carers to monitor elderly relatives remotely. National broadband subsidies enhance rural connectivity, making cloud dashboards viable outside major cities.

Hospitals and specialist clinics will grow at 4.78% CAGR, reflecting adoption of professional CGM systems for diagnostics and therapeutic adjustments. University-affiliated endocrinology units pilot non-invasive microwave sensors, positioning institutional buyers at the forefront of technology validation. Hospitals also stock pumps and sensors as contingency backups when patients’ personal devices malfunction, reinforcing their integral role in a resilient Russia diabetes devices market.

Geography Analysis

Moscow and St Petersburg anchor demand with high per-capita incomes, robust insurance networks and flagship diabetes centres that trial hybrid closed-loop systems. These cities showcase premium device uptake, serving as early-adopter bellwethers for the wider Russia diabetes devices market. Federal diabetes registries reveal that urban dwellers achieve 15% higher CGM utilisation than the national mean.

The Siberian Federal District emerges as a technological hotbed, led by Tomsk State University research into near-infra-red and microwave non-invasive sensors. Government grants under the Science and Universities national project accelerate prototyping, tightening the feedback loop between academia and device manufacturers. Local start-ups partner with regional hospitals to conduct clinical validation, advancing these alternatives toward Roszdravnadzor approval.

Far-Eastern and Arctic regions grapple with logistical barriers—long supply lines, extreme temperatures and sparse healthcare facilities. Tele-health initiatives mitigate these constraints, streaming CGM data to endocrinologists thousands of kilometres away. The State Programme for Socio-Economic Development of the Far East finances satellite-backed connectivity that improves device data transmission reliability, narrowing the access gap inside the Russia diabetes devices market.

Southern oblasts—Krasnodar, Rostov and Stavropol—report higher diabetes prevalence due to dietary patterns rich in refined carbohydrates. Regional authorities channel dedicated funds from the 519.5 billion RUB federal transfer pool toward screening vans and subsidised sensors. Cross-border cooperation under the EAEU framework simplifies customs clearances for Kazakh- and Belarusian-produced consumables, reducing unit costs for clinics near international frontiers.

Competitive Landscape

The Russia diabetes devices market exhibits moderate fragmentation. Domestic players Geropharm and Promomed leverage local plants and Roszdravnadzor fast-track status to secure state tenders, collectively seizing share from multinationals restricted by sanctions. Geropharm filed patents for polymer-encapsulated CGM sensors that withstand sub-zero conditions, differentiating its hardware for northern territories. Promomed collaborates with Skolkovo-based AI firms to fine-tune basal insulin algorithms powering forthcoming hybrid pumps.

Abbott and Medtronic preserve brand equity through authorised distributors and grey-channel stock replenishment. Their 2023 collaboration enabled Russian clinics to access integrated FreeStyle Libre 3 sensors paired with MiniMed 780G pumps, consolidating a premium product tier. Dexcom’s 2025 roll-out of a generative-AI coaching module—adapted for Cyrillic text—raises the competitive bar on software services layered atop hardware.

Academic institutions act as innovation feeders. University spin-offs negotiate licensing agreements with mid-tier device firms seeking next-gen sensor technology. Venture-capital interest remains cautious but active, focusing on exportable intellectual property that can address neighbouring EAEU markets. Heightened localisation rules combined with rising technical sophistication gradually shift the Russia diabetes devices market toward endogenous innovation and away from dependency on imported solutions.

Russia Diabetes Devices Industry Leaders

Abbott Diabetes Care

Medtronic PLC

Novo Nordisk A/S

Roche Diabetes Care

Lifescan Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2023: Medtronic presented one-year ADAPT study results confirming MiniMed 780G outperformed multiple daily injections plus CGM in adult patients not meeting glycaemic targets.

- April 2022: CamDiab and Ypsomed partnered with Abbott to link FreeStyle Libre 3 sensors, CamAPS FX app and mylife YpsoPump into an integrated automated insulin-delivery system for European markets.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Russia diabetes devices market as turnover from blood-glucose monitoring equipment, meters, strips, lancets, flash and real-time CGM sensors, and their data-management software, and insulin-delivery hardware, including pens, syringes, jet injectors, and pumps with associated disposables, sold to end users inside the Russian Federation.

Scope Exclusion: Cosmetic wellness wearables and laboratory analyzers are not counted.

Segmentation Overview

- By Device Category

- Monitoring Devices

- Self-Monitoring Blood Glucose Devices

- Continuous Glucose Monitoring Devices

- Management Devices

- Insulin Pumps

- Insulin Pens (Disposable & Reusable)

- Jet Injectors

- Monitoring Devices

- By Distribution Channel

- Offline (Hospital & Retail Pharmacy)

- Online (E-commerce & DTC)

- By Diabetes Type

- Type-1 Diabetes

- Type-2 Diabetes

- Gestational & Other Specific Types

- By End User

- Hospitals & Specialty Clinics

- Home-care Settings

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed endocrinologists in Moscow and Novosibirsk, procurement leads at regional clinics, and distributors supplying retail pharmacies. They then followed up with an online survey of adult patients to verify sensor adoption and strip replacement cycles.

Desk Research

We began by extracting patient prevalence and treatment data from the Russian Ministry of Health bulletins, IDF Diabetes Atlas tables, and Rosstat household-expenditure panels, which ground our demand pool. Trade flows from the Federal Customs Service clarified import volumes and average customs-declared prices for strips, sensors, and pumps. Supplementary insight came from peer-reviewed articles in Diabetes Technology & Therapeutics and press releases posted by global and local device makers. Paid intelligence from D&B Hoovers and Dow Jones Factiva provided company revenue splits that helped us stress-test pricing corridors and market shares. The sources listed are illustrative; dozens of additional publications informed data checks and clarifications.

A second pass consolidated national reimbursement rules, tender results, and ruble-dollar FX history so our totals reflect real purchasing power rather than headline list prices.

Market-Sizing & Forecasting

A top-down model converts treated-patient cohorts and incidence growth into annual device demand, which is then balanced with bottom-up snapshots of manufacturer shipments and sampled average selling prices. Five market fingerprints, insulin-treated population, CGM penetration, reimbursement coverage ratio, ruble trajectory, and average strip use per patient, feed a multivariate regression that projects values through 2030. When distributor volumes were incomplete, we applied mean ASP × unit proxies from customs data before final triangulation.

Data Validation & Update Cycle

Variance screens flag outliers for analyst review, after which senior reviewers sign off. The file is refreshed every year, with mid-cycle updates triggered by major currency or regulatory shocks.

Why Mordor's Russia Diabetes Devices Baseline Commands Reliability

Published estimates often vary because each firm chooses different product baskets, patient definitions, or exchange-rate assumptions. Our disciplined scope, multi-side price checks, and annual refresh give decision-makers a dependable anchor.

Key gap drivers include narrower channel coverage, omission of pump consumables, or the use of headline list prices by some publishers, whereas Mordor blends real transaction pricing, verified import data, and cross-checked patient pools.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.40 billion (2025) | Mordor Intelligence | - |

| USD 0.48 billion (2024) | Regional Consultancy A | Excludes CGM and pump disposables; partial retail tracking |

| USD 1.34 billion (2025) | Trade Journal B | Uses list prices, lumps in OTC lancets |

The comparison shows that, by aligning device scope with clinical use and validating prices through multiple channels, Mordor delivers a balanced, transparent baseline that practitioners and investors can retrace and replicate.

Key Questions Answered in the Report

How big is the Russia Diabetes Care Devices Market?

The Russia Diabetes Care Devices Market size is expected to reach USD 1.46 billion in 2026 and grow at a CAGR of 4.48% to reach USD 1.82 billion by 2031.

Which device category dominates sales today?

Monitoring devices lead with 57.48% share, driven by broad use of self-monitoring blood-glucose meters and emerging CGM sensors.

Who are the key players in Russia Diabetes Devices Market?

Abbott Diabetes Care, Medtronic PLC, Novo Nordisk A/S, Roche Diabetes Care and Lifescan Inc. are the major companies operating in the Russia Diabetes Devices Market.

How are sanctions influencing supply chains?

Import restrictions create intermittent shortages of consumables, prompting localisation and the rise of domestic manufacturers protected by preferential procurement.

Page last updated on: