Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

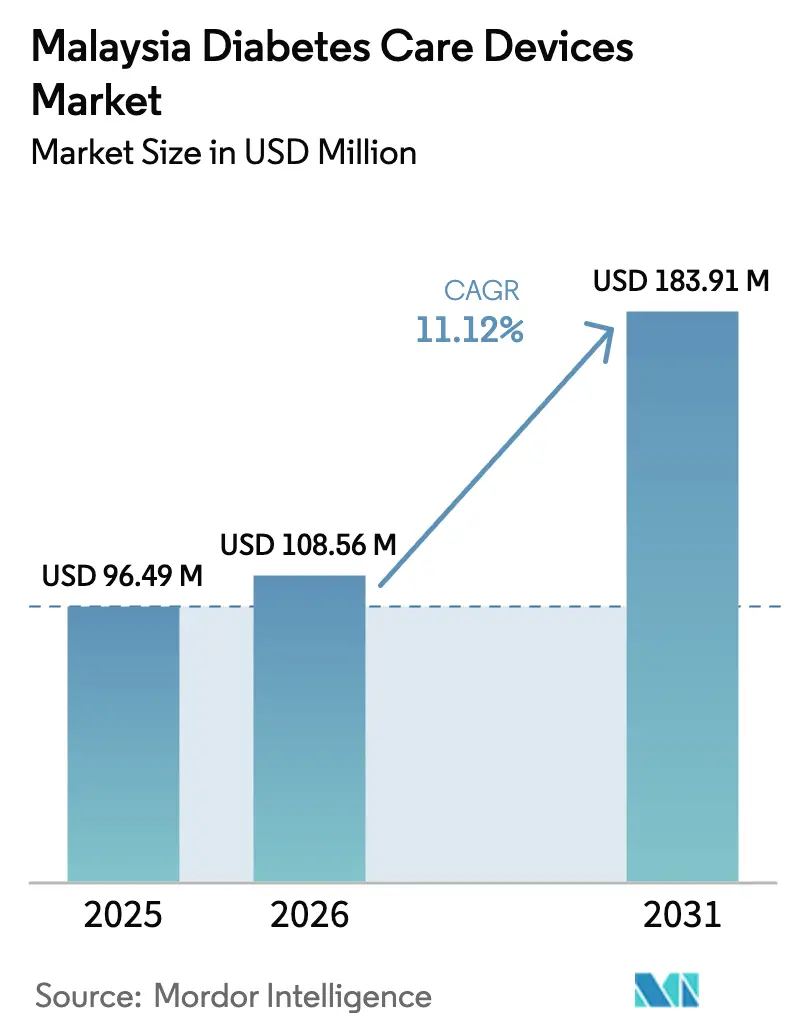

| Base Year Market Size (2025) | USD 96.49 Million |

| Market Size (2026) | USD 108.56 Million |

| Market Size (2031) | USD 183.91 Million |

| Growth Rate (2026 - 2031) | 11.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Diabetes Care Devices Market Analysis by Mordor Intelligence

The Malaysia Diabetes Care Devices Market size is projected to be USD 96.49 million in 2025, USD 108.56 million in 2026, and reach USD 183.91 million by 2031, growing at a CAGR of 11.12% from 2026 to 2031.

Escalating disease prevalence, aggressive foreign direct investment in local manufacturing, and an upshift toward home-based monitoring collectively bolster the Malaysian diabetes care devices market. Public-sector procurement budgets are expanding, yet 40% of adults with diabetes remain undiagnosed, sustaining latent demand for entry-level self-monitoring blood glucose (SMBG) systems. Pharmacy chains have widened point-of-care access, while subscription models package devices, strips, and teleconsultations, lowering behavioral barriers to daily monitoring. Interoperability agreements, such as Abbott’s data-sharing pact with Medtronic, signal a competitive push toward closed-loop ecosystems that integrate continuous glucose monitoring (CGM) with automated insulin delivery, a pairing likely to accelerate the Malaysia diabetes care devices market through 2031.

Key Report Takeaways

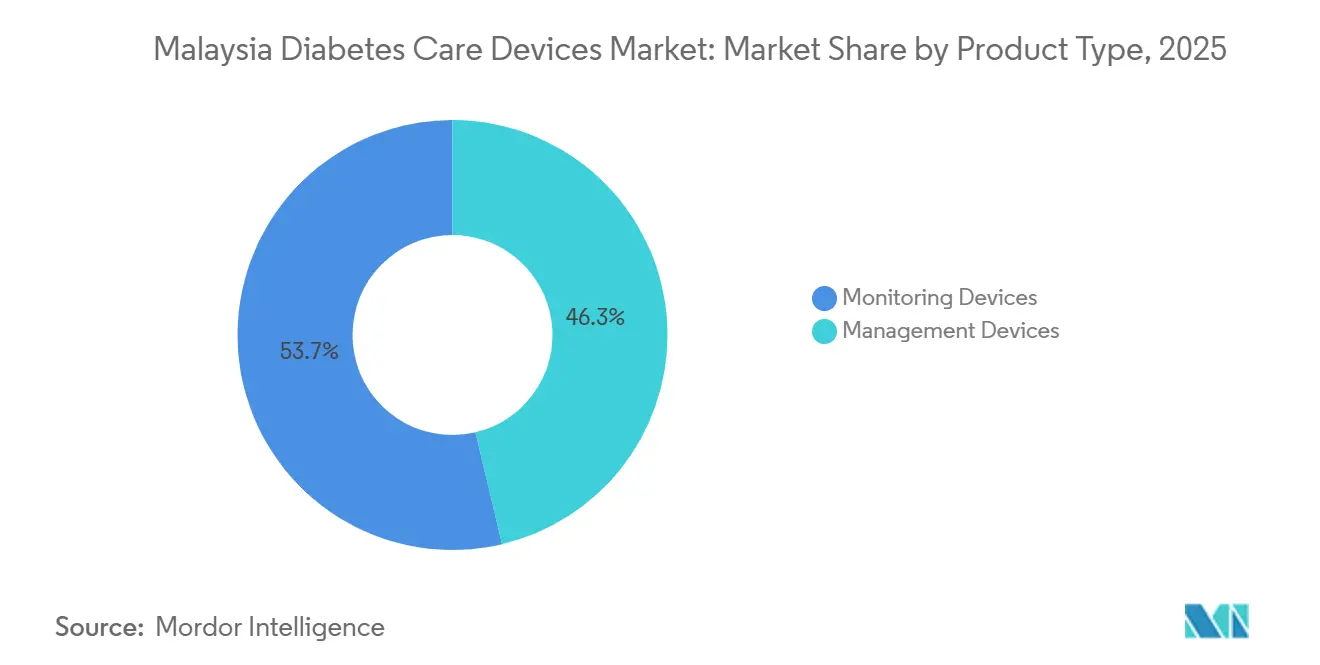

- By product type, monitoring devices accounted for 53.69% of the Malaysia diabetes care devices market share in 2025, whereas management devices are projected to grow at a 13.72% CAGR to 2031.

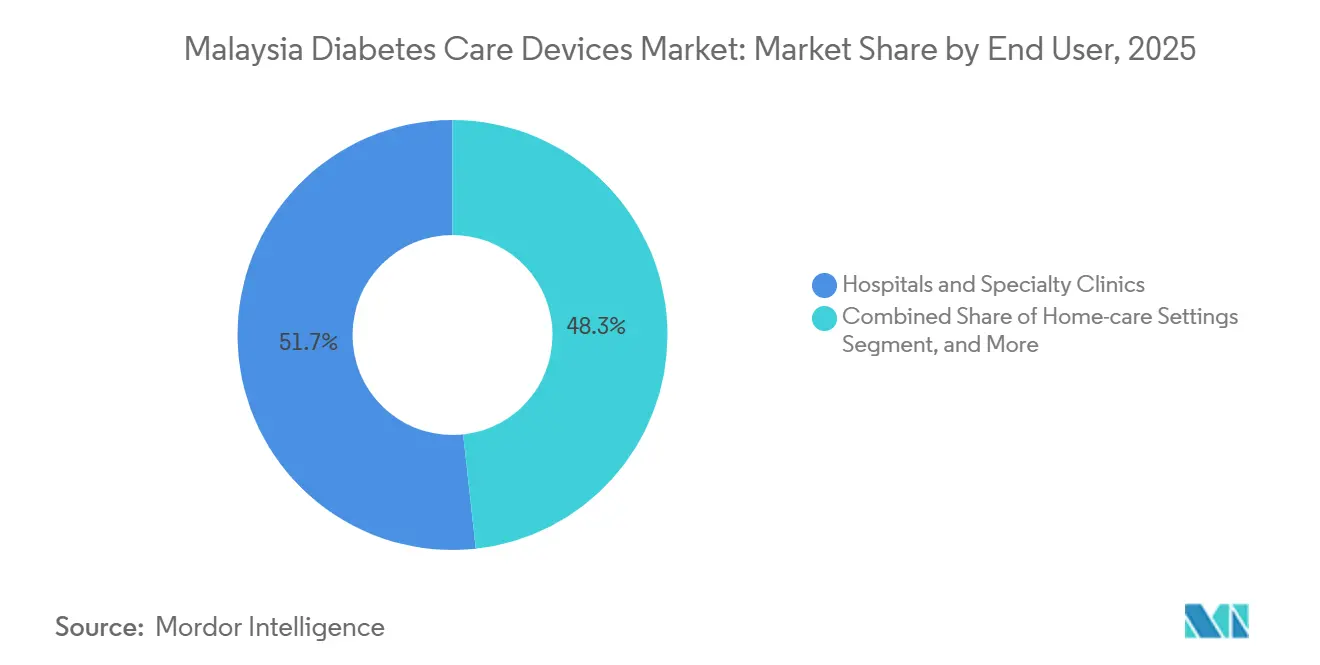

- By end user, hospitals and specialty clinics accounted for 51.73% of revenue in 2025, and the home-care setting segment is forecast to expand at a 14.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia Diabetes Care Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diabetes Prevalence & SMBG Penetration | +2.8% | National, concentrated in Klang Valley, Johor Bahru, Penang urban centers | Medium term (2-4 years) |

| Expanding Public-Health Budget & Device Procurement | +1.9% | National, MOH clinic network across 13 states and 3 federal territories | Short term (≤ 2 years) |

| Home-Healthcare & POC Testing Boom | +2.4% | Urban and peri-urban areas with telemedicine infrastructure | Short term (≤ 2 years) |

| Localised CGM/Insulin-Pump Manufacturing Incentives | +2.1% | Penang, Johor (Iskandar Malaysia), with export spillover to ASEAN | Long term (≥ 4 years) |

| HTA-Driven Push for CGM Reimbursement | +1.5% | National, contingent on MOH and private-insurer policy shifts | Medium term (2-4 years) |

| Medical-Tourism Demand for Advanced Devices | +0.5% | Kuala Lumpur, Penang, Johor medical-tourism hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes Prevalence & SMBG Penetration

Malaysia’s adult diabetes prevalence rose to 15.6% in 2023, yet 44% of diagnosed patients still lack a glucometer at home, underscoring the growth headroom for entry-level SMBG kits. Retail meters sell for RM66–99, while test strips cost RM28–91, a range that aligns with median monthly household incomes and supports recurring consumable demand. National Diabetes Registry data indicate 902,991 active cases in Ministry of Health (MOH) clinics, a figure that excludes the private sector and undiagnosed individuals, thereby widening the total addressable volume. The 2026 budget allocations of RM64 billion (USD 14.2 billion) for metabolic disease management guarantee stable tender volumes for SMBG supplies.[1] Ministry of Health Malaysia, “Budget 2026: Diabetes Interventions,” moh.gov.my Pharmacy majors respond by stocking low-price glucometers such as EASYSURE, offering affordable entry points while securing strip replenishment revenue.[2]Watsons Malaysia, “Diabetes Care Catalog,” watsons.com.my

Localised CGM/Insulin-Pump Manufacturing Incentives

Dexcom’s Penang plant, commissioned in 2024 with an investment of RM2.83 billion (approximately USD 662 million), and Insulet’s Johor facility, which was scaled to five production lines in 2024, anchor Malaysia as ASEAN’s principal manufacturing hub for CGM sensors and tubeless pumps. Tax holidays, streamlined device registration under the ASEAN Medical Device Directive, and ready access to a seasoned electronics workforce lower production costs and shorten time-to-market. Biocon and Novo Nordisk have committed RM2.7 billion and RM1.5 billion, respectively, to insulin facilities, reinforcing a vertically integrated local supply chain for the Malaysian diabetes care devices market. Most output feeds export demand, yet local availability improves logistical resilience and supports rapid product rollouts. Over the long term, cumulative capacity may enable price renegotiations with MOH clinics, narrowing affordability gaps for advanced devices.

HTA-Driven Push for CGM Reimbursement

A 2024 MOH health technology assessment ruled CGM non-cost-effective at retail prices of RM279 (approximately USD 62) per 14-day sensor, thereby curbing immediate public funding. Nonetheless, the review highlighted significant quality-of-life gains for Type 1 patients, signaling a policy window for negotiated discounts or outcomes-based reimbursement. Private insurers now pilot selective CGM coverage within pump therapy bundles at premium hospitals such as Gleneagles Kuala Lumpur, paving a blueprint for future public adoption. Singapore’s RM340 per sensor benchmark indicates that Malaysian retail margins remain flexible, thereby strengthening MOH’s bargaining power. If threshold prices fall, CGM uptake could migrate from the affluent niche to a broader Type 2 cohort, redirecting the Malaysia diabetes care devices market toward routine sensor replacement cycles.

Home-Healthcare & POC Testing Boom

Pandemic-era telemedicine catalyzed remote monitoring platforms like DoctorOnCall’s SIHAT program and Speedoc virtual wards, each integrating glucometer or CGM data into remote consultations. A 2024 IDEAS trial reported modest glycaemic improvement due to low engagement, prompting market entrants to bundle coaching with devices for sustained behavior change. SugO365 offers six-month kits at RM260 (approximately USD 57) that include a meter, strips, and teleconsults, while Ottai Health sells CGM units at RM128–199, 30% below the prices of legacy brands, capturing price-sensitive home-care customers. Point-of-care testing in pharmacies now targets walk-in shoppers, and the MOH clinical guideline endorses SMBG for all insulin users, validating home-based protocols. Together these factors accelerate device diffusion into households, reinforcing the Malaysia diabetes care devices market trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CGM & Pump Cost Burden | -1.8% | National, most acute in rural and lower-income urban segments | Medium term (2-4 years) |

| Import-Dependency & Supply-Chain Risk | -0.9% | National, with vulnerability to USD/MYR exchange-rate volatility | Short term (≤ 2 years) |

| Tropical-Climate Sensor Adhesion Failures | -0.7% | National, exacerbated in coastal and high-humidity zones | Long term (≥ 4 years) |

| Clinician Data-Integration Knowledge Gaps | -0.6% | National, concentrated in primary-care and rural clinics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CGM & Pump Cost Burden

A single 14-day sensor costs RM279 (approximately USD 62), translating to RM7,200 (approximately USD 1,593) annually. In contrast, hybrid pumps exceed RM20,000 (approximately USD 4,425), which is significantly higher than the RM5,873 (approximately USD 1,299) median monthly household income.[3]Department of Statistics Malaysia, “Household Income Survey 2024,” dosm.gov.my The 2024 HTA deemed CGM not cost-effective, which delayed public reimbursement and limited penetration to the top-income quintiles and foreign medical tourists. Private hospitals provide pump packages, yet financing hurdles deter middle-class uptake. Lower-priced alternatives, such as Ottai CGM, reduce hardware expenses by approximately 30%, although the lack of large-scale clinical validation hinders endocrinologist adoption. Unless bulk procurement discounts emerge, high out-of-pocket costs will hinder the diffusion of advanced devices and temper the expansion of the Malaysian diabetes care devices market.

Tropical-Climate Sensor Adhesion Failures

Malaysia’s year-round humidity, typically ranging from 80% to 90%, degrades CGM adhesives, causing premature detachment and forcing users to purchase overlay patches, which adds indirect costs. A 2024 user survey revealed sensor loss rates exceeding 15% per cycle, particularly among outdoor workers. Neither Abbott nor Dexcom has yet commercialized humidity-tuned adhesives for Southeast Asia, compelling clinicians to recommend skin-prep regimens that complicate daily routines. Ascensia’s planned launch of Senseonics’ 180-day implantable Eversense sensor in 2026 could bypass adhesive failures, potentially shifting share in the Malaysia diabetes care devices market. Until then, adhesion breakdown remains a structural deterrent to broader CGM adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automation Drives Management Device Surge

Management Devices are forecast to grow at a 13.72% CAGR through 2031, a rate that will tilt revenue leadership away from monitoring devices despite the latter holding a 53.69% share in 2025. Demand for closed-loop insulin delivery hinges on clinical successes, such as a 22% reduction in hypoglycemia with Medtronic’s MiniMed 780G at Subang Jaya Medical Centre. Insulet’s local Omnipod output enhances supply certainty and shortens replenishment cycles, while pharmacy chains continue to stock high-volume insulin pens priced at RM55–65 per pack. Subscriptions that pair pens with virtual coaching blur the line between durable and consumable sales, broadening the Malaysia diabetes care devices market.

Continuous glucose monitoring (CGM) penetration remains below 5% but is poised to rise as Abbott-Medtronic interoperability integrates Libre data into pump algorithms, thereby increasing sensor value beyond stand-alone readings. Roche’s AI-enabled Accu-Chek SmartGuide, approved in 2024, enters a technology race that can compress upgrade cycles despite saturated meter ownership. Still, price competition is fierce; test-strip commoditization pushes manufacturers toward data-driven services to preserve margins in the Malaysia diabetes care devices market.

By End User: Home-Care Disrupts Hospital Dominance

Home-care settings are projected to expand at a 14.29% CAGR, reflecting consumer preference for remote consultations and the avoidance of clinic queues. DoctorOnCall and Speedoc integrate device data into teleconsultation workflows, while SugO365 monetizes recurring strip sales through six-month packages, converting episodic buyers into subscribers. Ottai Health lowers CGM entry barriers, targeting tech-savvy millennials with pricing 30% lower than legacy brands'. Together, these models transfer demand from tertiary centers to living rooms, growing the Malaysia diabetes care devices market size for at-home solutions.

Hospitals & specialty clinics still own a 51.73% share in 2025 due to exclusivity over pump initiation, professional CGM, and complex comorbidity management. Subang Jaya Medical Centre showcases hybrid closed-loop therapy, while Gleneagles Kuala Lumpur caters to expatriates and high-net-worth locals with bundled endocrinology services. MOH clinics struggle with limited budgets for advanced devices, but procurement of SMBG kits ensures baseline access in rural areas. Continued infrastructural investment might tilt share, yet premium technologies will likely stay hospital-led for the next five years within the Malaysia diabetes care devices market.

Geography Analysis

The Malaysia diabetes care devices market concentrates in Klang Valley, Penang, and Johor Bahru, owing to higher household incomes, dense private-hospital clusters, and manufacturing spillovers. Dexcom’s Penang footprint and Insulet’s Johor lines deepen supply resilience while attracting skilled labor pools. Medical tourism funnels international patients to Kuala Lumpur’s Prince Court Medical Centre and Penang’s Gleneagles, reinforcing the uptake of premium devices and ancillary sensor sales. In contrast, Sabah and Sarawak exhibit lower device penetration due to sparse pharmacy networks and reliance on MOH clinics, where SMBG shortages are common. Rural incomes amplify affordability barriers; an annual CGM regimen equates to more than 10% of average household earnings, muting adoption outside urban cores.

Regional policy integration also shapes geographic trajectories. The ASEAN Medical Device Directive harmonizes certification, enabling Malaysian-made sensors to flow seamlessly into Indonesia, Thailand, and Vietnam, insulating Penang and Johor plants from domestic demand volatility. However, over 90% of component raw materials remain imported, exposing local manufacturers to USD/MYR volatility and shipping disruptions. The MOH 2026 budget prioritizes urban tertiary centers, potentially widening urban-rural gaps unless targeted subsidies extend devices to community clinics. Addressing these disparities is critical for balanced growth across the Malaysia diabetes care devices market.

Competitive Landscape

Roughly 20 sizable competitors populate the Malaysian diabetes care devices market, with Abbott, Dexcom, Medtronic, Roche, and Novo Nordisk leading the premium segments. Abbott’s FreeStyle Libre ecosystem gains new leverage through its integration into Medtronic’s MiniMed 780G pump, fostering stickiness that could consolidate share among interoperability leaders. Dexcom’s RM2.83 billion Penang factory, Malaysia’s largest CGM plant, boosts sensor availability and provides a platform for region-specific product tweaks, though humidity-optimized adhesives remain in development. Insulet’s Johor site lifts Omnipod pump output, supporting Southeast Asian expansion and limiting import lag.

White-space innovation focuses on humidity-resistant adhesives, AI-driven glycaemic prediction, and subscription pricing. Roche’s SmartGuide enters the AI arena, while Ascensia’s future Senseonics implant bypasses adhesive shortcomings, potentially reshaping the Malaysia diabetes care devices market share mix. Domestic disruptors Ottai Health and SugO365 pivot on affordability, yet they lack randomized-controlled trial evidence, a gap that multinational incumbents exploit to retain endocrinologist loyalty. Market fragmentation persists, but ecosystem partnerships signal gradual convergence around integrated data platforms and manufacturing scale.

Malaysia Diabetes Care Devices Industry Leaders

Medtronic

Roche

Dexcom

Abbott Laboratories

Novo Nordisk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Ascensia and Senseonics signed an MoU to introduce the 180-day Eversense implantable CGM in Malaysia, targeting adhesion-related device failures.

- March 2025: Biocon announced a RM1.1 billion (USD 243 million) expansion of its Johor insulin facility, bringing cumulative investment to RM2.7 billion (USD 597 million).

- November 2024: Dexcom inaugurated its 887,510 sq ft Penang factory, investing RM2.83 billion (USD 662 million) and creating 3,000 jobs.

- August 2024: Abbott and Medtronic agreed to integrate FreeStyle Libre sensor data into MiniMed 780G automated insulin delivery systems, enabling closed-loop therapy in Malaysia.

Malaysia Diabetes Care Devices Market Report Scope

There are two primary categories of devices used to measure blood glucose levels. The first type is comprised of blood glucose meters, which require a small sample of blood to determine your current levels. On the other hand, continuous glucose monitors (CGMs) are capable of regularly monitoring your blood glucose throughout the day and night. The Malaysia Diabetes Care Devices Market is segmented into devices. The report offers the market size in value terms in USD and Volume terms in Units for all the abovementioned segments.

By Product Type

| Monitoring Devices | Self-Monitoring Blood Glucose Devices |

| Continuous Glucose Monitoring | |

| Management Devices | Insulin Pumps |

| Insulin Syringes | |

| Insulin Cartridges | |

| Disposable Pens | |

| Other Management Devices |

By End User

| Hospitals & Specialty Clinics |

| Primary Care & Diabetes Centres |

| Home-Care Settings |

| By Product Type | Monitoring Devices | Self-Monitoring Blood Glucose Devices |

| Continuous Glucose Monitoring | ||

| Management Devices | Insulin Pumps | |

| Insulin Syringes | ||

| Insulin Cartridges | ||

| Disposable Pens | ||

| Other Management Devices | ||

| By End User | Hospitals & Specialty Clinics | |

| Primary Care & Diabetes Centres | ||

| Home-Care Settings | ||

Key Questions Answered in the Report

How large is the Malaysia diabetes care devices market in 2026?

The Malaysia diabetes care devices market size is USD 108.56 million in 2026 with a 11.12% CAGR projected through 2031.

Which product segment is expanding fastest?

Management Devices, led by insulin pumps, are forecast to grow at 13.72% CAGR to 2031, outpacing monitoring devices.

What fuels home-care device demand?

Telemedicine adoption, subscription bundles like SugO365, and lower-priced CGM options drive an 14.29% CAGR for home-care settings.

Why is CGM adoption still limited?

High sensor costs of RM279 per 14-day unit and humidity-related adhesion failures constrain widespread use.

How do local factories affect pricing?

Facilities from Dexcom and Insulet enhance supply security and may enable future bulk-procurement discounts, though most output currently targets export markets.

Page last updated on: