Type 2 Diabetes Drugs And Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

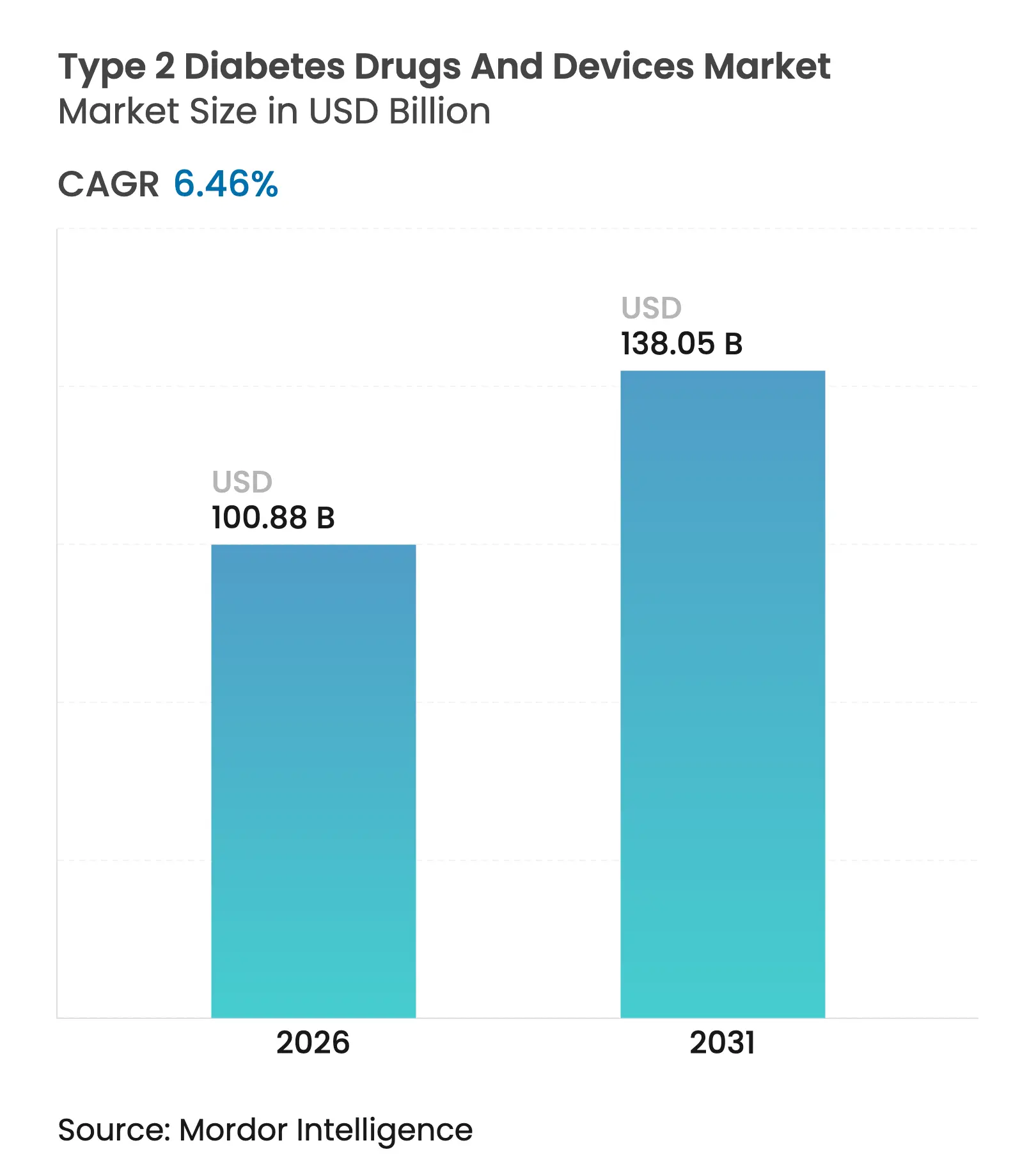

| Market Size (2026) | USD 100.88 Billion |

| Market Size (2031) | USD 138.05 Billion |

| Growth Rate (2026 - 2031) | 6.46 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

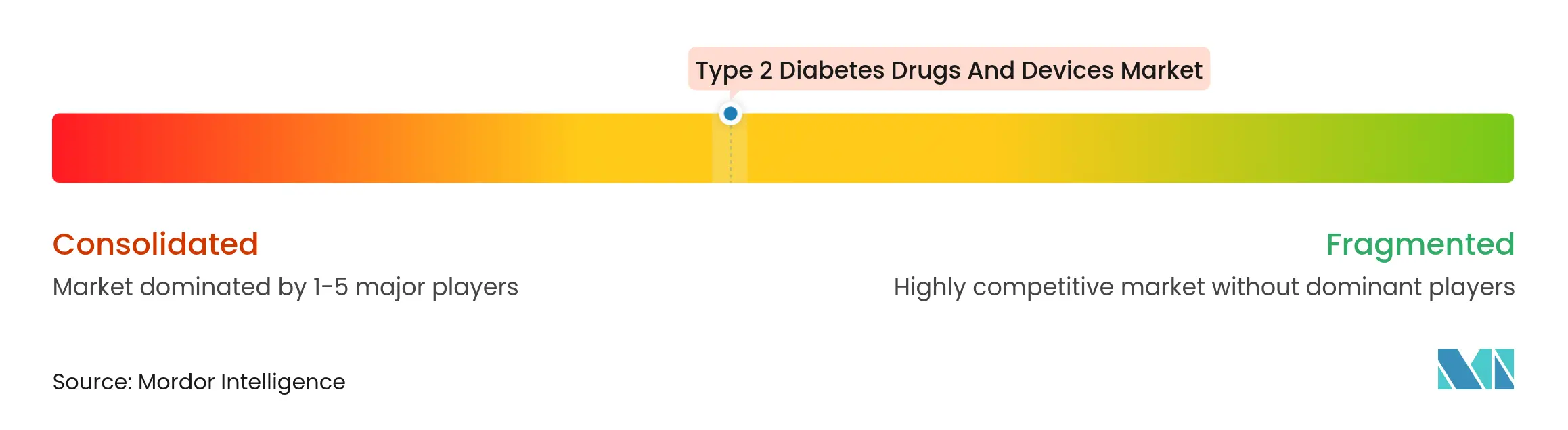

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Type 2 Diabetes Drugs And Devices Market Analysis by Mordor Intelligence

Type 2 diabetes drugs and devices market size in 2026 is estimated at USD 100.88 billion, growing from 2025 value of USD 94.77 billion with 2031 projections showing USD 138.05 billion, growing at 6.46% CAGR over 2026-2031. Growth reflects the rapid clinical shift toward GLP-1 receptor agonists, broader reimbursement for continuous glucose monitoring (CGM), and sustained investment in digital-first distribution models. Demand also rises in tandem with the escalating prevalence of obesity and sedentary lifestyles, while manufacturers re-engineer supply chains to prioritize high-value injectables over legacy human insulin lines. Intensifying competition from technology firms and consumer electronics brands accelerates device innovation, and regulatory focus on cybersecurity pushes connected-pump developers to harden software architectures.

Key Report Takeaways

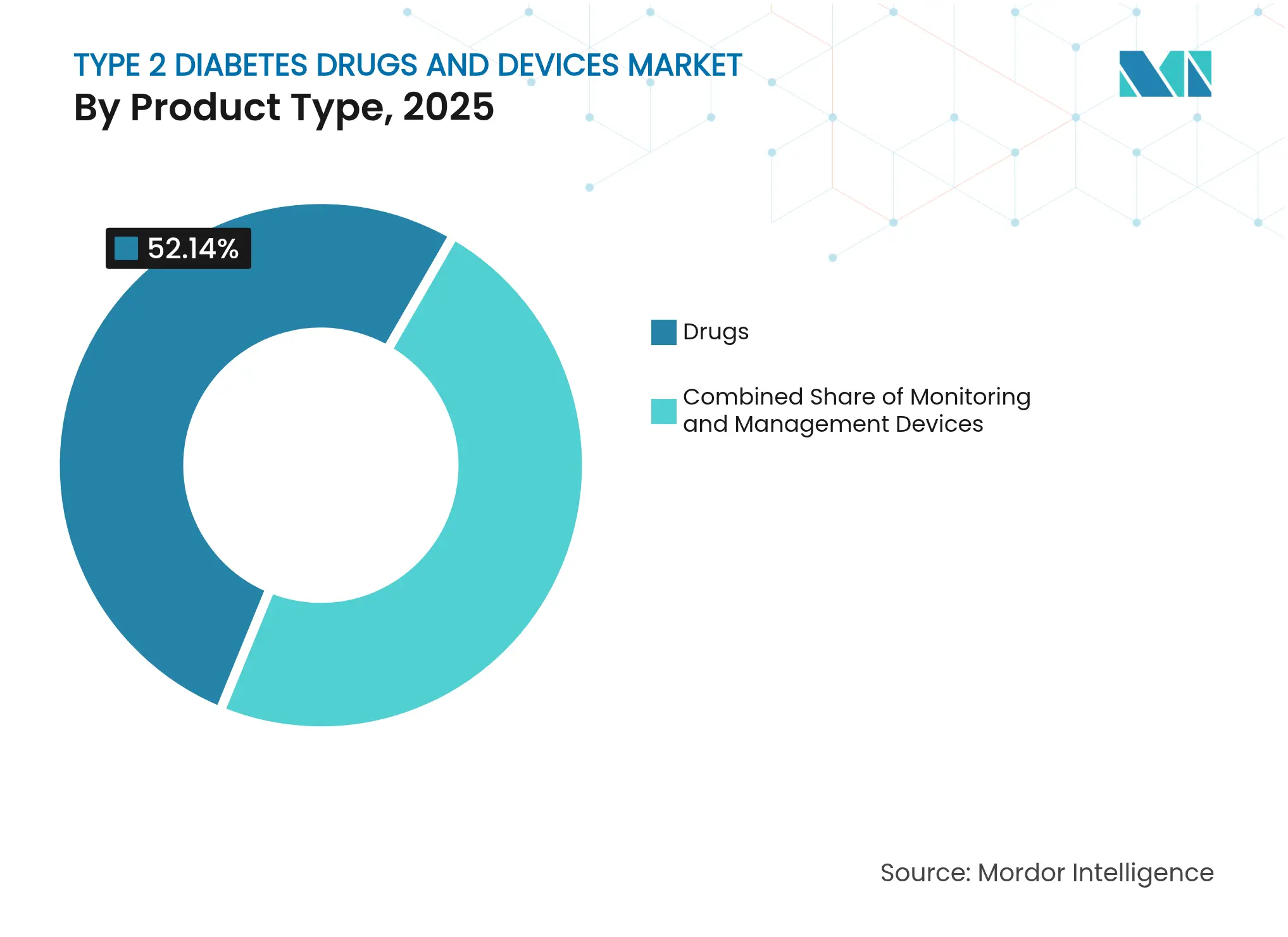

- By product category, drugs led with 52.14% revenue share in 2025; monitoring devices are forecast to expand at a 10.01% CAGR to 2031.

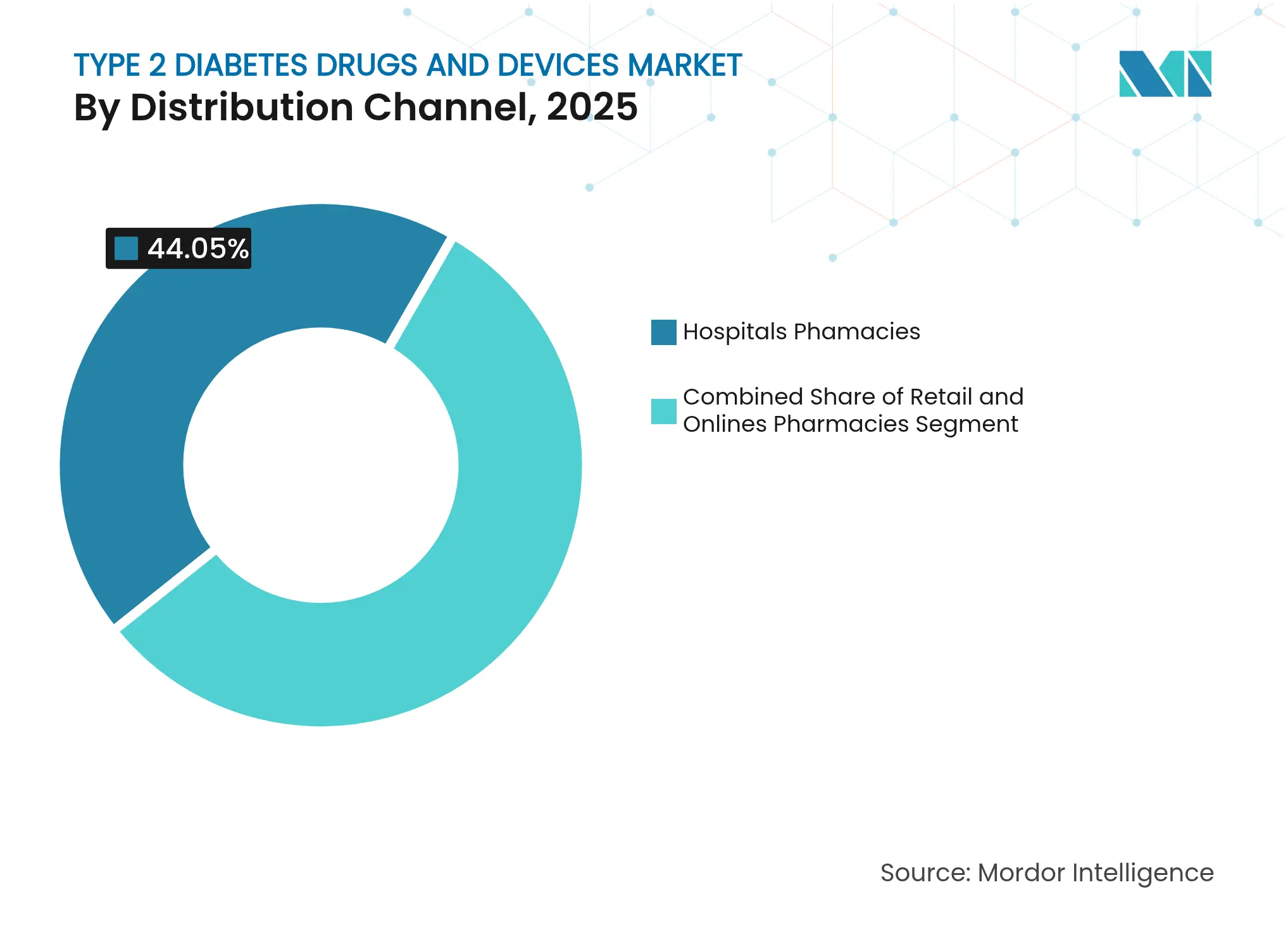

- By distribution channel, hospital pharmacies held 44.05% of the Type 2 diabetes drugs and devices market share in 2025, while online pharmacies record the highest projected CAGR at 10.43% through 2031.

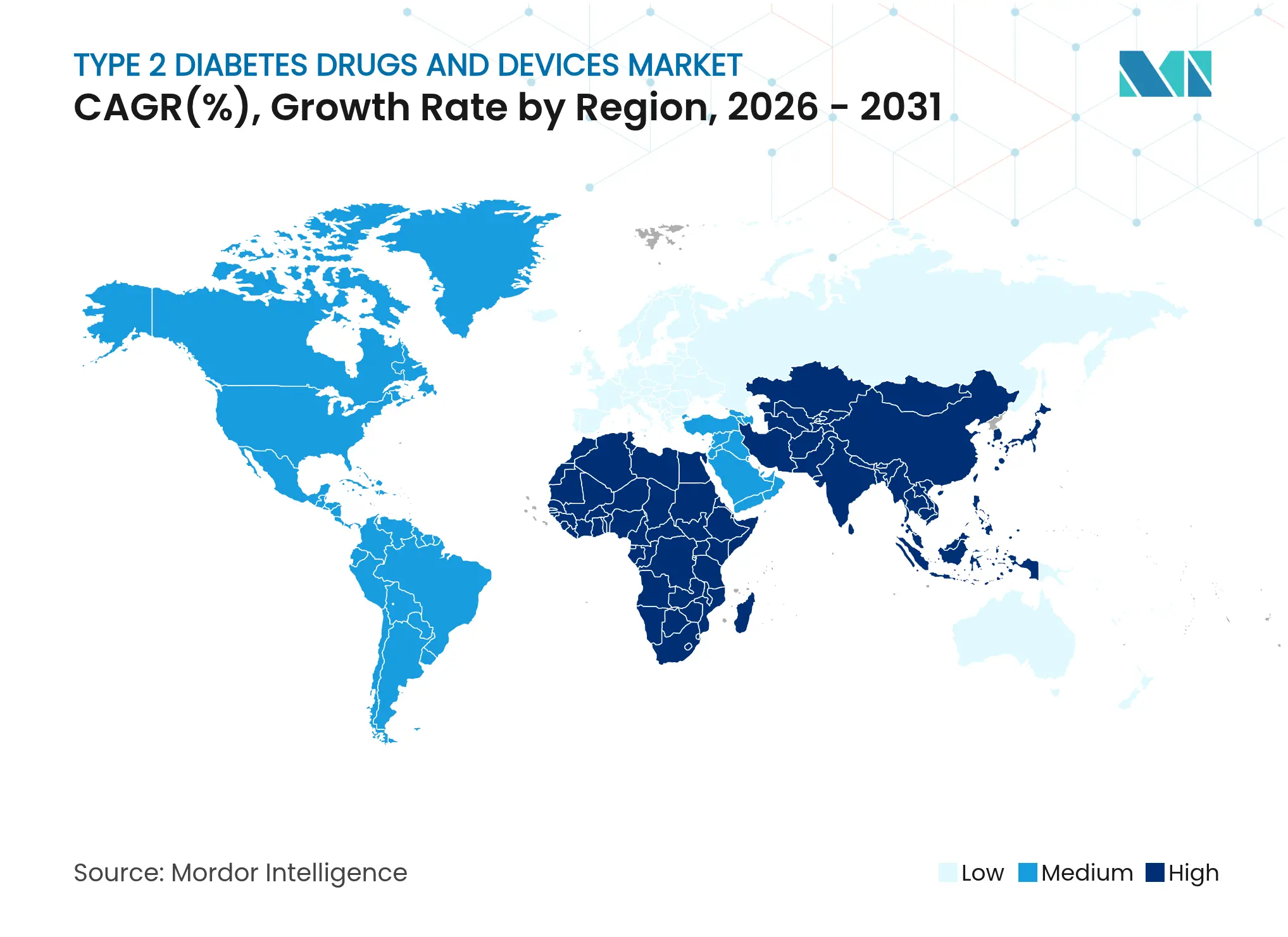

- By geography, North America commanded 39.32% of the Type 2 diabetes drugs and devices market in 2025; Asia-Pacific is poised for the fastest regional expansion at 9.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Type 2 Diabetes Drugs And Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Prevalence Of Diabetes

Type-2, Obesity & Sedentary Lifestyles

Rising Prevalence Of Diabetes

Type-2, Obesity & Sedentary Lifestyles

| 1.4% | Global, with highest impact in APAC and MENA regions | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

1.4%

|

Geographic Relevance

:

Global, with highest impact in APAC

and MENA regions

|

Impact Timeline

:

Long term (≥ 4 years)

|

Rapid Uptake Of GLP-1 Receptor

Agonists

Rapid Uptake Of GLP-1 Receptor

Agonists

| 1.8% | Global, led by North America and Europe | Medium term (2-4 years) | |||

Expansion Of Reimbursement For

Continuous Glucose Monitoring

Expansion Of Reimbursement For

Continuous Glucose Monitoring

| 1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) | |||

Pharma–Tech Data-Sharing

Partnerships Lowering Time-To-Market For Combo Devices

Pharma–Tech Data-Sharing

Partnerships Lowering Time-To-Market For Combo Devices

| 0.9% | Global, concentrated in developed markets | Short term (≤ 2 years) | |||

Government And Public Initiatives

Taken To Improve Health And Support Of Employers To Curb Diabetes

Government And Public Initiatives

Taken To Improve Health And Support Of Employers To Curb Diabetes

| 0.7% | Global, with stronger impact in developed economies | Long term (≥ 4 years) | |||

Integration Of Closed-Loop Insulin

Delivery Into Consumer Wearables

Integration Of Closed-Loop Insulin

Delivery Into Consumer Wearables

| 0.5% | North America & EU, early adoption phase | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising prevalence of Type 2 diabetes and obesity

Global diabetes prevalence continues to climb, with China alone reporting 233 million adults living with the disease in 2023 and a 15.88% prevalence rate[1]Ying Li, “Prevalence of Diabetes in China 2023: National Survey,” Military Medical Research, militarymedicalresearch.biomedcentral.com. Projections indicate Chinese prevalence could rise to 29.1% by 2050, forcing national health systems to reallocate resources toward earlier screening and combination therapy. Prescription data show GLP-1 receptor agonists moving from 4.4% of Type 2 diabetes scripts in 2018 to 19.8% by 2023, while the average drug count per patient rose from 1.58 to 1.65, signaling mounting treatment complexity. The United States already bears USD 413 billion in total annual diabetes-related costs. Asian populations develop Type 2 diabetes at lower BMI thresholds, propelling early adoption of novel therapies. Brazil mirrors these dynamics, with prevalence forecast to triple to 27.0% by 2036 alongside obesity rates topping 31.1% for men and 29.1% for women.[2]Eduardo Silva, “Projected Diabetes and Obesity Trends in Brazil to 2036,” Frontiers in Public Health, frontiersin.org

Rapid uptake of GLP-1 receptor agonists

Semaglutide earned European Commission approval for cardiovascular risk reduction in June 2025, broadening its utility beyond glucose control. Novo Nordisk’s Q3 2024 sales illustrate the pivot: 29.8 billion Danish kroner from semaglutide versus 12.5 billion kroner from insulin, prompting capacity reallocation away from human insulin pens. Combination therapy with SGLT2 inhibitors shows superior renal and cardiovascular outcomes, reinforcing guideline inclusion.[3]Steven E. Kahn, “Cardiovascular and Renal Effects of GLP-1 Receptor Agonists and SGLT2 Inhibitors,” PubMed Central, ncbi.nlm.nih.gov Patent expirations for first-generation GLP-1 agents start in 2026, paving the way for biosimilars that could temper pricing while enlarging the treated population.[4]Anil Kumar, “The Road Toward GLP-1 Biosimilars: Patent Expiry Timelines and Market Outlook,” National Center for Biotechnology Information, ncbi.nlm.nih.gov

Expansion of reimbursement for CGM

Medicare removed finger-stick calibration requirements in April 2023, immediately opening CGM coverage to millions of non-insulin-using Type 2 diabetes beneficiaries. Dexcom capitalized with its G7 system, gaining 15-day sensor coverage for seniors. UnitedHealthcare responded by layering prior authorization on CGMs for non-Type 1 users in September 2024, underscoring payer scrutiny. CMS formalized local coverage for implantable CGMs in May 2025, spurring interest in longer-wear devices.

Pharma–tech data-sharing partnerships

Abbott allied with Medtronic to link FreeStyle Libre sensors to automated insulin delivery (AID) platforms, granting Medtronic access to 6 million Libre users and projecting USD 100 million in annual incremental revenue for Abbott. Dexcom invested USD 75 million in Oura to marry glucose, sleep, and activity datasets, while launching a generative-AI decision-support suite on Google Cloud’s Vertex AI. Tandem signed an R&D pact with Abbott for glucose-ketone sensors that mitigate diabetic ketoacidosis risk in AID systems. These alliances shrink development timelines for combo devices and sharpen personalized-care capabilities.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Cost Of Novel GLP-1 Drugs &

Smart Pumps

High Cost Of Novel GLP-1 Drugs &

Smart Pumps

| -1.1% | Global, most pronounced in emerging markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-1.1%

|

Geographic Relevance

:

Global, most pronounced in emerging

markets

|

Impact Timeline

:

Medium term (2-4 years)

|

Stringent Regulatory Safety

Monitoring For SGLT2 Inhibitors

Stringent Regulatory Safety

Monitoring For SGLT2 Inhibitors

| -0.8% | Global, led by FDA and EMA oversight | Short term (≤ 2 years) | |||

Global Glass-Vial Shortage Delaying

Injectable Launches

Global Glass-Vial Shortage Delaying

Injectable Launches

| -0.6% | Global, acute in supply-constrained regions | Short term (≤ 2 years) | |||

Cyber-Security Vulnerabilities In

Connected Insulin Pumps

Cyber-Security Vulnerabilities In

Connected Insulin Pumps

| -0.4% | North America & EU, expanding globally | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High cost of novel GLP-1 drugs and smart pumps

A four-week supply of tirzepatide (Zepbound) is priced between USD 399 and USD 549, challenging affordability in markets lacking robust reimbursement. Many payers apply prior-authorization hurdles that delay initiation. The discontinuation of Victoza in the United Kingdom because of supply and portfolio reprioritization narrows therapeutic options for patients. In South Africa, shortages of insulin pens have emerged as manufacturers divert capacity to higher-margin GLP-1 production, exemplifying cost-driven access inequities. Patch pumps likewise struggle with affordability; devices carrying 300-unit reservoirs must achieve three-day wear to offset consumable costs for high-dose Type 2 diabetes regimens.

Cyber-security vulnerabilities in connected insulin pumps

The FDA issued a May 2025 safety alert after phone-notification settings caused some patients to miss critical warnings from smartphone-linked pumps. Tandem’s Class I recall of the Mobi device, triggered by firmware errors that could miscalculate doses, underscores the stakes. Academic reverse-engineering of the Tandem t:slim X2 firmware revealed exploits capable of malicious control. Germany’s ManiMed project further spotlighted systemic vulnerabilities in networked medical devices. Recalls of mobile apps for Tandem t:connect and Insulet Omnipod 5 demonstrate the ongoing challenge of securing multi-platform ecosystems.

Segment Analysis

By Product Type: Drugs Sustain Dominance

Drugs controlled 52.14% of the Type 2 diabetes drugs and devices market in 2025. GLP-1 receptor agonists and dual-incretin compounds, such as tirzepatide, have redrawn competitive lines by delivering glycemic, cardiovascular, and renal benefits in a single weekly injection. Insulin innovation continues as Eli Lilly pursues once-weekly formulations, a shift designed to ease adherence burdens. SGLT2 inhibitors complement GLP-1 therapies in combination regimens that aim to delay renal decline. Meanwhile, biosimilar entrants preparing for post-2026 patent expiries are expected to widen access and temper prices. Pharmaceutical R&D increasingly targets triple-agonist profiles, seeking still broader metabolic control windows. Despite device advances, clinician preference for proven drug classes maintains elevated demand, securing the segment’s lead through the forecast horizon.

Management Devices Gain Ground Insulin-delivery technologies evolve toward low-burden formats. CeQur’s three-day wearable patch exemplifies simplified dosing for Type 2 diabetes patients requiring multiple daily injections. Insulet secured FDA clearance in August 2024 for SmartAdjust, the first automated insulin-delivery algorithm explicitly indicated for Type 2 diabetes. Medtronic’s Simplera Sync CGM, paired with MiniMed 780G, also won FDA approval, fusing disposable sensors with adaptive pumps. Such closed-loop ecosystems address glycemic variability while reducing finger-stick dependence. Device makers court payer support by evidencing reduced hospitalization costs from hypoglycemia or diabetic ketoacidosis events. Although cost remains a barrier, device innovation is set to expand its addressable base beyond intensive Type 1 therapy.

Monitoring Devices: CGM Outpaces Finger-Stick Testing CGM advances drive a double-digit CAGR, positioning monitoring technologies as the fastest-growing component of the Type 2 diabetes drugs and devices market. Medicare’s 2023 policy eliminated restrictive calibration rules, enabling Dexcom, Abbott, and Medtronic to target millions of insulin-naïve users. Dexcom’s over-the-counter Stelo is expected to trigger retail-channel expansion once commercially launched. Implantable sensors with six-month wear times are now under CMS coverage review, potentially redefining convenience benchmarks. Meanwhile, consumer-wearable players seek noninvasive optical approaches, though accuracy hurdles persist. Widespread CGM adoption feeds data back to AI-powered decision dashboards, which fine-tune dose recommendations and alert clinicians to early-stage complications.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Transformation Accelerates Online Growth

Hospital pharmacies accounted for 44.05% of the Type 2 diabetes drugs and devices market share in 2025, bolstered by established physician networks and prior-authorization expertise. Online pharmacies, however, post a 10.43% CAGR through 2031 as telehealth scripts migrate to mail-order fulfillment. LillyDirect illustrates the model, linking independent telehealth providers with home delivery and medication counseling. Retail chains respond by layering clinical services—HbA1c testing, nutrition coaching, and virtual endocrinology visits—to safeguard foot traffic. Regulatory bodies monitor direct-to-consumer dispensing for continuity-of-care risks, yet broader digital health acceptance suggests online channels will capture an increasing slice of routine refills.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America commanded 39.32% of the Type 2 diabetes drugs and devices market in 2025, benefiting from broad insurance coverage and a proactive regulatory stance. Medicare’s CGM expansion and FDA clearances for over-the-counter sensors and AID systems sustain regional technology leadership. Novo Nordisk allotted USD 4.1 billion to new North Carolina capacity, while Eli Lilly earmarked USD 5.3 billion for Indiana facilities, ensuring supply lines for GLP-1 injectables. The FDA’s cybersecurity advisories also guide device design, reinforcing patient safety standards.

Asia-Pacific delivers the fastest regional CAGR at 9.12% through 2031 as urbanization, dietary shifts, and lower BMI diagnostic thresholds fuel demand. China’s 233 million patients and three-tier treatment architecture highlight systemic urgency. Local guidelines increasingly endorse GLP-1/SGLT2 combination therapy and CGM for high-risk cohorts, fostering rapid uptake. Multinationals align with domestic manufacturers to navigate volume-based procurement rules—Novo Nordisk secured streamlined approval for semaglutide in 2024, affirming this approach.

Europe leverages centralized purchasing and robust clinical guidelines to maintain substantial market presence. The European Medicines Agency’s January 2024 clinical trial update foregrounded personalized cardiometabolic endpoints, steering R&D pipelines accordingly. Coordinated responses to GLP-1 shortages, including distribution caps, demonstrate advanced demand-management capabilities. Sanofi’s EUR 1.3 billion Frankfurt insulin expansion, slated for 2029, underscores continued investment in injectable drug security across the continent.

Competitive Landscape

Market Concentration

Competition is moderate yet intensifying as traditional pharmaceutical incumbents diversify into data-rich digital services while tech firms angle for noninvasive monitoring niches. Medtronic’s decision to spin off its USD 2.76 billion diabetes arm signals a push toward focused AID innovation with a workforce exceeding 8,000 specialists. Novo Nordisk’s reprioritization away from human insulin pens confirms the market’s pivot to GLP-1 dominance, whereas Dexcom’s generative-AI advisory engine—built on Google Cloud’s Vertex AI—illustrates the race to convert glucose data into actionable insights.

Abbott’s Libre platform remains pivotal, with the Medtronic tie-up promising to connect 6 million Libre users to pump networks. Embecta targets underserved high-dose Type 2 diabetes patients with 300-unit patch pumps, challenging pump incumbents on reservoir capacity. Consumer-electronics giants eye the space: Apple’s optical-sensor patents and Samsung’s millimeter-wave prototypes hint at future noninvasive entrants, although regulatory clearance remains distant. Compliance lapses carry reputational risk, as exemplified by FDA warning letters to CGM manufacturers; firms with robust quality systems may gain a credibility edge.

Type 2 Diabetes Drugs And Devices Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Tandem Diabetes Care and Abbott agree to integrate AID platforms with glucose-ketone sensors, aiming to curb diabetic ketoacidosis in closed-loop systems.

- June 2025: Eli Lilly files for approval of once-weekly insulin after favorable phase 3 data, seeking to improve adherence for basal therapy.

- May 2025: Medtronic announces intent to spin off its diabetes unit into a USD 2.76 billion standalone company focused on AID and smart MDI systems.

- April 2025: FDA approves pairing of Medtronic Simplera Sync CGM with MiniMed 780G pump, forming an integrated, finger-stick-free AID solution.

Table of Contents for Type 2 Diabetes Drugs And Devices Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence Of Diabetes Type -2, Obesity & Sedentary Lifestyles

- 4.2.2Rapid Uptake Of GLP-1 Receptor Agonists

- 4.2.3Expansion Of Reimbursement For Continuous Glucose Monitoring

- 4.2.4Pharma–Tech Data-Sharing Partnerships Lowering Time-To-Market For Combo Devices

- 4.2.5Government And Public Initiatives Taken To Improve Health And Support Of Employers To Curb Diabetes

- 4.2.6Integration Of Closed-Loop Insulin Delivery Into Consumer Wearables

- 4.3Market Restraints

- 4.3.1High Cost Of Novel GLP-1 Drugs & Smart Pumps

- 4.3.2Stringent Regulatory Safety Monitoring For SGLT2 Inhibitors

- 4.3.3Global Glass-Vial Shortage Delaying Injectable Launches

- 4.3.4Cyber-Security Vulnerabilities In Connected Insulin Pumps

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Product Type

- 5.1.1Management Devices

- 5.1.1.1Insulin Pumps

- 5.1.1.2Insulin Syringes

- 5.1.1.3Insulin Cartridges

- 5.1.1.4Disposable Pens

- 5.1.1.5Jet Injectors

- 5.1.2Monitoring Devices

- 5.1.2.1Self-Monitoring Blood Glucose (SMBG)

- 5.1.2.2Continuous Glucose Monitoring (CGM)

- 5.1.3Drugs

- 5.1.3.1Oral Anti-Diabetics

- 5.1.3.1.1Biguanides

- 5.1.3.1.2SGLT2 Inhibitors

- 5.1.3.1.3DPP-4 Inhibitors

- 5.1.3.2Insulins

- 5.1.3.2.1Basal (Long-acting)

- 5.1.3.2.2Bolus (Rapid/Short-acting)

- 5.1.3.3Non-Insulin Injectables

- 5.1.3.3.1GLP-1 Receptor Agonists

- 5.1.3.4Combination Drugs

- 5.2By Distribution Channel

- 5.2.1Hospital Pharmacies

- 5.2.2Retail Pharmacies

- 5.2.3Online Pharmacies

- 5.3By Geography

- 5.3.1North America

- 5.3.1.1United States

- 5.3.1.2Canada

- 5.3.1.3Mexico

- 5.3.2Europe

- 5.3.2.1Germany

- 5.3.2.2United Kingdom

- 5.3.2.3France

- 5.3.2.4Italy

- 5.3.2.5Spain

- 5.3.2.6Rest of Europe

- 5.3.3Asia-Pacific

- 5.3.3.1China

- 5.3.3.2Japan

- 5.3.3.3India

- 5.3.3.4Australia

- 5.3.3.5South Korea

- 5.3.3.6Rest of Asia-Pacific

- 5.3.4Middle East and Africa

- 5.3.4.1GCC

- 5.3.4.2South Africa

- 5.3.4.3Rest of Middle East and Africa

- 5.3.5South America

- 5.3.5.1Brazil

- 5.3.5.2Argentina

- 5.3.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1Novo Nordisk A/S

- 6.4.2Eli Lilly and Company

- 6.4.3Sanofi

- 6.4.4Abbott Laboratories

- 6.4.5Medtronic plc

- 6.4.6Roche Holding AG

- 6.4.7Pfizer Inc.

- 6.4.8Takeda Pharmaceutical Co.

- 6.4.9AstraZeneca plc

- 6.4.10Merck & Co., Inc.

- 6.4.11Boehringer Ingelheim GmbH

- 6.4.12Bristol Myers Squibb Co.

- 6.4.13Novartis AG

- 6.4.14Janssen Pharmaceuticals (J&J)

- 6.4.15Astellas Pharma Inc.

- 6.4.16Dexcom Inc.

- 6.4.17Insulet Corporation

- 6.4.18Tandem Diabetes Care Inc.

- 6.4.19Becton, Dickinson and Company (BD)

- 6.4.20Ypsomed AG

7. Market Opportunities and Future Outlook

- 7.1White-Space and Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global Type 2 diabetes drugs and devices market as every prescription medicine, oral agents, non-insulin injectables, and all insulin formats, and every patient, direct monitoring or delivery device (CGM, SMBG meters and strips, pumps, pens, syringes) sold through retail, hospital, or online channels to manage glycemic control in diagnosed Type 2 adults.

Scope exclusion: wellness wearables, bariatric tools, and education services fall outside this remit.

Segmentation Overview

- By Product Type

- Management Devices

- Insulin Pumps

- Insulin Syringes

- Insulin Cartridges

- Disposable Pens

- Jet Injectors

- Insulin Pumps

- Monitoring Devices

- Self-Monitoring Blood Glucose (SMBG)

- Continuous Glucose Monitoring (CGM)

- Self-Monitoring Blood Glucose (SMBG)

- Drugs

- Oral Anti-Diabetics

- Biguanides

- SGLT2 Inhibitors

- DPP-4 Inhibitors

- Biguanides

- Insulins

- Basal (Long-acting)

- Bolus (Rapid/Short-acting)

- Basal (Long-acting)

- Non-Insulin Injectables

- GLP-1 Receptor Agonists

- GLP-1 Receptor Agonists

- Combination Drugs

- Oral Anti-Diabetics

- Management Devices

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Hospital Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- China

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed endocrinologists, hospital pharmacy buyers, payer officials, and distribution executives across North America, Europe, and Asia-Pacific. The conversations validated GLP-1 uptake, CGM reimbursement timing, and real-world average selling prices that desk work could only approximate.

Desk Research

We pulled prevalence, diagnosis, and therapy data from the IDF Diabetes Atlas, WHO Global Health Observatory, CDC National Diabetes Statistics, OECD health datasets, and EMA safety alerts. Company 10-Ks, investor decks, and UN Comtrade trade codes added pipeline, pricing, and shipment clues, while paid checkpoints from D&B Hoovers and Dow Jones Factiva helped reconcile supplier splits. These sources illustrate, not exhaust, the material reviewed.

Market-Sizing & Forecasting

A top-down build starts with adult prevalence, diagnosed share, and treated share to size the patient pool, which is multiplied by annual drug-dose intensity and device penetration to obtain global spend. Target totals are cross-checked via selective bottom-up roll-ups of leading manufacturer revenues and channel ASP checks. Key inputs, obesity prevalence, fresh therapy approvals, insulin ASP trends, CGM adoption, and reimbursement caps, feed a multivariate regression that projects demand to 2030, while scenario analysis tests upside from oral GLP-1 launches. Regional data holes are bridged with analog markets agreed in expert calls.

Data Validation & Update Cycle

Outputs pass peer review, anomaly screens against historical spend, and variance triggers. We refresh the model each year and issue interim updates for material approvals or policy shifts, so clients always receive the latest view.

Why Mordor's Type 2 Diabetes Drugs And Devices Baseline Commands Reliability

Benchmark comparison

Published values often diverge because firms slice therapies, devices, channels, and rebates differently or refresh on uneven cadences. By aligning scope up front, blending dual-path modeling, and updating annually, Mordor keeps variance tight and transparency high.

The comparison shows that narrower scopes or rebate deductions shrink totals, whereas our inclusive yet patient-grounded frame delivers the balanced baseline decision-makers need.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 94.77 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 84.07 B (2025) | Global Consultancy A | drugs only | ||

USD 61.5 B (2024) | Industry Research Firm B | excludes devices, net rebates |