Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

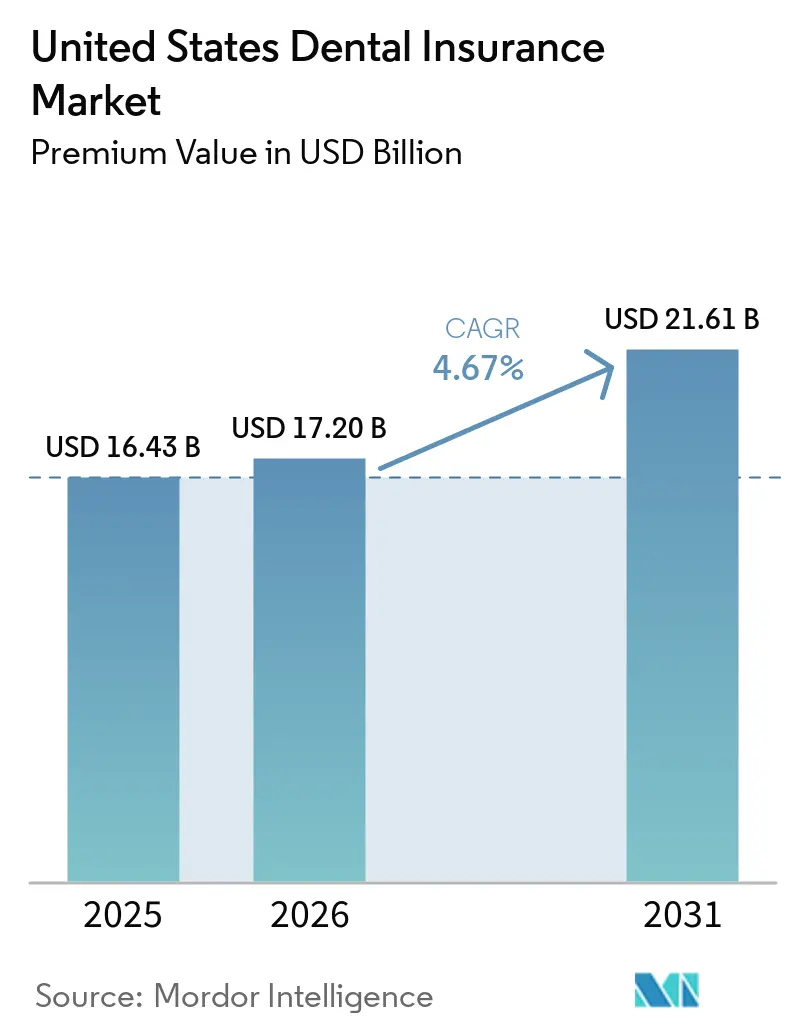

| Base Year Market Size (2025) | USD 16.43 Billion |

| Market Size (2026) | USD 17.20 Billion |

| Market Size (2031) | USD 21.61 Billion |

| Growth Rate (2026 - 2031) | 4.67% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Dental Insurance Market Analysis by Mordor Intelligence

The United States Dental Insurance Market size in terms of premium value was valued at USD 16.43 billion in 2025 and is estimated to grow from USD 17.20 billion in 2026 to reach USD 21.61 billion by 2031, at a CAGR of 4.67% during the forecast period (2026-2031).

Employer-sponsored Dental Preferred Provider Organization plans hold a decisive position, with DPPO formats accounting for a significant share in 2025, reinforcing product standardization and underwriting stability across large groups. Senior-focused demand is expanding as Medicare Advantage plans make dental benefits widely available, yet the breadth of coverage varies and comprehensive benefits remain limited across many offerings. Pediatric dental coverage embedded as an Affordable Care Act Essential Health Benefit, along with ongoing upgrades to adult Medicaid dental benefits in dozens of states, provides a structural base of insured lives that supports utilization and claims volume across both public and commercial books. A wave of state-level dental insurance reforms enacted in 2025, including dental loss ratio reporting and payment transparency, is directing carrier behavior toward clearer value signals and greater alignment with quality metrics. As virtual care infrastructure matures and carriers refine benefit designs for major procedures, the United States dental insurance market is positioned to balance preventive care anchoring with measured growth in higher acuity services.

Key Report Takeaways

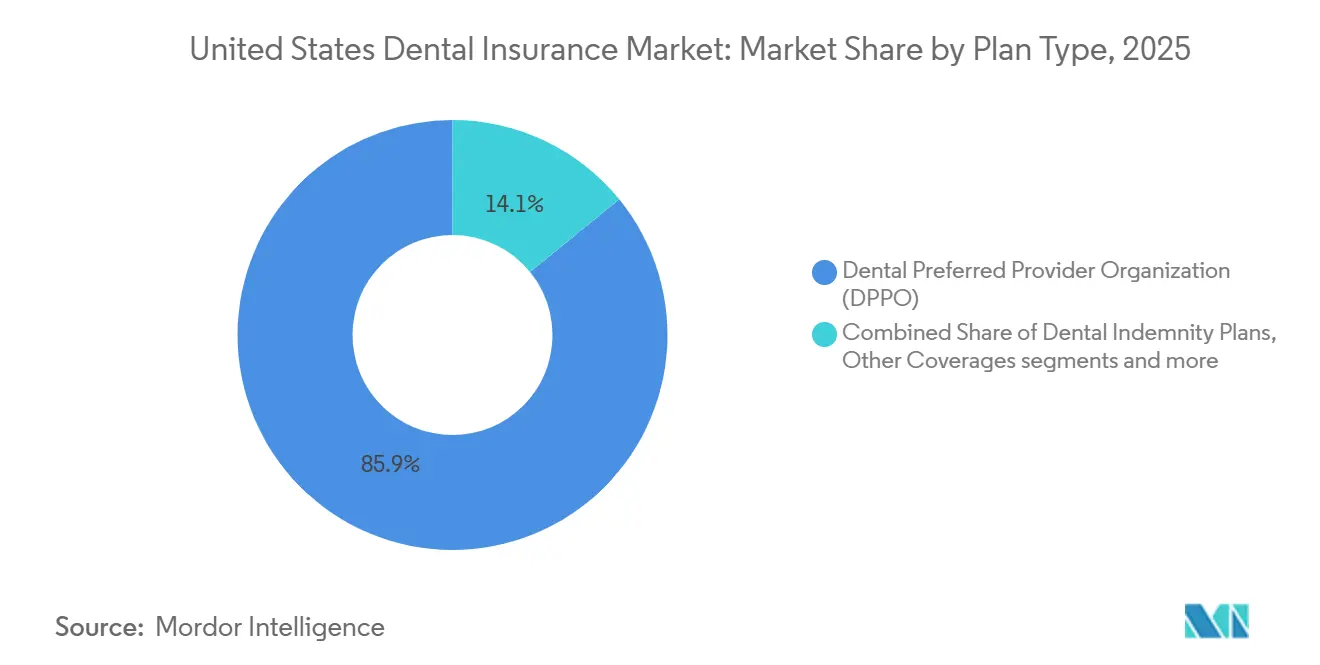

- By plan type, DPPO led with 85.87% of the United States dental insurance market share in 2025, while Other Coverages are projected to post the fastest growth at a 6.33% CAGR through 2031.

- By procedure type, preventive services accounted for 51.88% share of the United States dental insurance market in 2025, while major procedures are forecast to expand at a 6.98% CAGR to 2031.

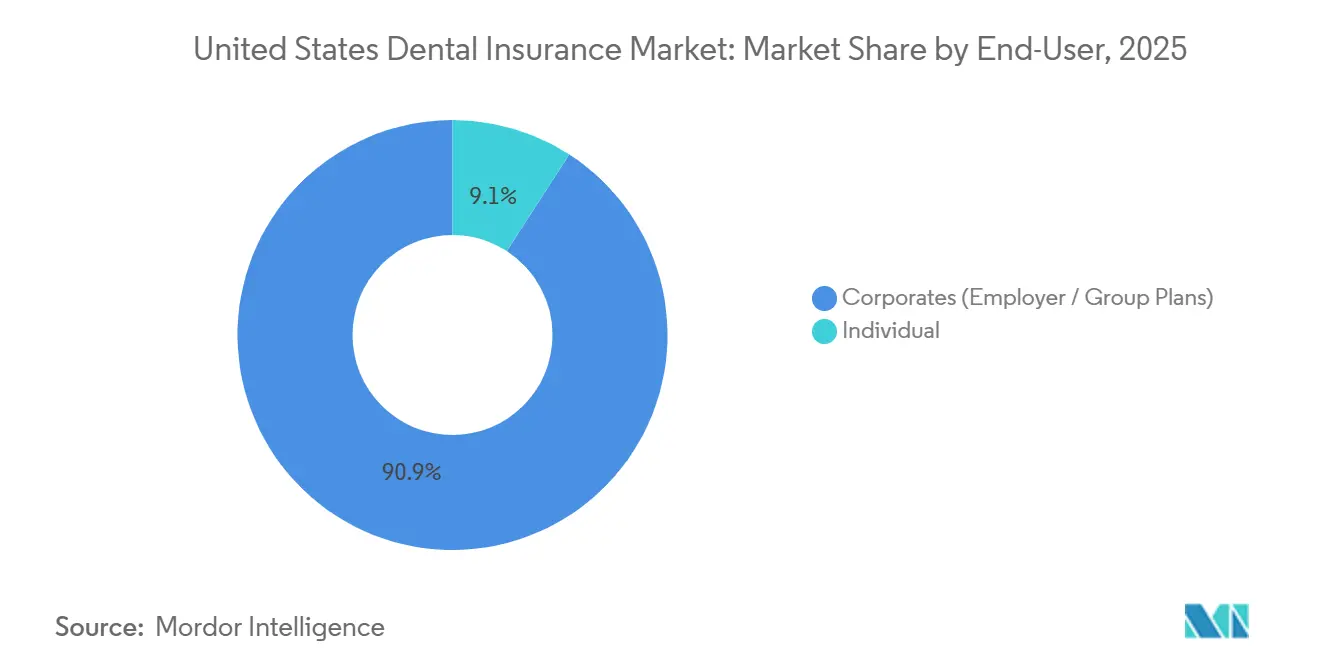

- By end-user, corporates represented 90.87% of total enrolment of the United States dental insurance market in 2025, while individual direct-purchase plans are projected to grow at a 7.18% CAGR through 2031.

- By demographics, adults aged 21-64 comprised 61.24% of insured lives of the United States dental insurance market in 2025, while senior citizens are expected to register the fastest expansion at a 7.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Dental Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DPPO dominance and employer-sponsored coverage sustain enrolments and pricing stability | +1.2% | National, concentrated in employer-dense metros such as Dallas, Atlanta, Minneapolis | Medium term (2-4 years) |

| Medicare Advantage dental benefits near-universal availability expands senior coverage | +0.9% | National, higher penetration in FL, CA, TX, PA, OH | Long term (≥ 4 years) |

| Medicaid adult dental expansions and managed dental programs increase covered lives | +0.7% | 18 expansion states since 2021 including GA, IN, KS, KY, MO, OK, UT; early gains in TN and NY | Medium term (2-4 years) |

| Pediatric dental as ACA Essential Health Benefit underpins minors' coverage | +0.5% | National, with marketplace concentration in CA, FL, TX, NY | Long term (≥ 4 years) |

| Teledentistry adoption and virtual-first benefits lower access frictions | +0.6% | CA, GA, TX; spillover to rural Health Professional Shortage Areas | Short term (≤ 2 years) |

| State Dental Loss Ratio and transparency rules catalyze benefit/value improvements | +0.4% | 18 states enacted 37 reform laws in 2025 with actions on DLR reporting and virtual credit card payments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

DPPO Dominance and Employer-Sponsored Coverage Sustain Enrolment and Pricing Stability

DPPO remains the core architecture of the United States dental insurance market, capturing a significant share in 2025 as large employers favour broad networks and out-of-network flexibility that can support geographically distributed workforces and specialist referrals. Scale advantages for national carriers translate into stable pricing, predictable claims trends, and standardized plan designs that help benefits teams manage renewals across multi-state employee populations. Network breadth continues to be a linchpin, with UnitedHealthcare projecting a large national dentist panel and reporting strong in-network utilization across employer groups. Employers are adopting administrative structures that emphasize steady premiums and utilization management, which helps DPPO offerings maintain their anchor role within the United States dental insurance market. Concentration within corporate enrollment creates sensitivity to macro labor conditions and remote-work dispersion, though national carriers are responding with digital tools and virtual benefits to sustain access continuity inside DPPO frameworks.

Medicare Advantage Dental Benefits Near-Universal Availability Expands Senior Coverage

Medicare Advantage plans widely include dental benefits, but the level of coverage is uneven, with peer-reviewed research showing that 86.6% of MA plans provided any dental benefit in 2024, and only 8.4% offered comprehensive coverage[1]JAMA Editorial Team, “Availability and Comprehensiveness of Dental Benefits in Medicare Advantage Plans,” JAMA, jamanetwork.com . This landscape makes supplemental dental a key differentiator for plan selection, even as plan designs often limit major services through narrower benefit tiers or utilization controls. Carriers continue to compete on preventive benefits and selective major-service coverage enhancements, as seen in Humana’s nationwide 2026 rollout of two annual cleanings, exams, and X-rays across all MA plans and broader inclusion of periodontal services across many offerings. Senior oral health needs are evolving in line with longer retention of natural teeth and reduced edentulism rates in older adults, which aligns benefit design with a heavier emphasis on maintenance and restorative pathways. As the senior population grows and MA penetration remains high, the United States dental insurance market is seeing more plan differentiation in dental coverage, networks, and virtual access features tailored to older adults.

Medicaid Adult Dental Expansions and Managed Dental Programs Increase Covered Lives

Enhanced adult Medicaid dental coverage across 38 states and the District of Columbia as of 2025, including 18 state expansions since 2021, is lifting the covered base and contributing to more consistent utilization patterns in both preventive and restorative care. These policy shifts include upgrades from emergency-only coverage to more robust benefit tiers in multiple states, which helps rebalance care from hospital emergency departments toward in-network dental settings. States are integrating new delivery channels as well, with New York adding continuous coverage for children under age six and including School-Based Health Center dental services in Medicaid managed care packages during 2025, a move that supports early and ongoing access for minors. Benefit design updates and managed dental program capabilities are allowing states to align performance incentives with measures from the Dental Quality Alliance, including those adopted into the federal Child Core Set, which can strengthen outcomes tracking over time. Continued focus on rate adequacy and practitioner participation remains essential to convert expanded eligibility into realized care, yet the structural demand created by these expansions is supportive for the United States dental insurance market.arket.

Pediatric Dental as ACA Essential Health Benefit Underpins Minors’ Coverage

Pediatric dental sits within the Affordable Care Act’s Essential Health Benefits for individual and small-group plans, embedding diagnostic, preventive, restorative, and medically necessary orthodontic services for children through age 19 into core medical plan designs[2]Blue Cross Blue Shield of Alabama, “Essential Health Benefits: Pediatric Dental,” BCBS Alabama, bcbsal.org . This integration aligns pediatric dental coverage with medical plan deductibles and out-of-pocket maximums, improving predictability for families and reducing financial barriers to routine oral care. The federal policy framework is evolving, as the Centers for Medicare & Medicaid Services has signaled pathways for states to add adult dental to Essential Health Benefits in later plan years, which could extend this integration model into the adult market over time. States are also moving to set minimum standards for stand-alone products sold on marketplaces, with New York announcing a 2026 Standard Adult Dental Plan that aims to clarify cost-sharing and scope for hundreds of thousands of individual enrollees. Together, these norms provide a floor for minors’ access and a template that can extend to adults in the coming years, supporting steady utilization flows in the United States dental insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dental HPSA-driven network adequacy gaps constrain access and utilization | -0.8% | National; 65.63% rural designations; notable counts in NY, FL, CA | Long term (≥ 4 years) |

| Low adult Medicaid reimbursement vs private dampens provider participation | -0.6% | National; participation varies widely by state | Long term (≥ 4 years) |

| Annual maximums, waiting periods, and cost-sharing cap uptake of major care | -0.5% | National; PPO caps affect a subset of enrollees | Medium term (2-4 years) |

| Medicare Advantage dental benefit limits (caps/scope) temper realized value | -0.3% | National MA footprint with concentrations in FL, CA, TX, PA, OH | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dental HPSA-Driven Network Adequacy Gaps Constrain Access and Utilization

As of December 31, 2025, there were 7,443 designated dental Health Professional Shortage Areas affecting 63.7 million residents, with only 32.93% of need met and 10,744 additional dentists required to close the gap nationwide[3]Health Resources and Services Administration, “Designated Health Professional Shortage Areas Statistics,” HRSA, data.hrsa.gov . Shortage designations are concentrated in rural communities, which account for 65.63% of all dental HPSAs, elevating the challenge of securing timely care in regions with fewer active providers and longer travel distances. States such as New York, Florida, and California carry large counts of dental HPSAs with millions of residents impacted and persistent deficits in the number of required clinicians, magnifying the importance of accurate directories and time-distance compliance for plan networks. Virtual care is a partial relief valve, with teledentistry modalities now embedded by many carriers and accepted in growing numbers of state programs, although clinical delivery of major services still requires in-person visits. Emerging regulatory models and technology solutions aimed at validating provider participation and reducing phantom listings will matter for network adequacy performance and realized access in the United States dental insurance market.

Low Adult Medicaid Reimbursement Versus Private Dampens Provider Participation

Adult Medicaid dental fee schedules remain well below private reimbursement on average, and national dentist participation in Medicaid and CHIP programs has stayed near long-run plateaus, constraining network capacity even as more states enhance coverage. Comparative research in JAMA Health Forum shows that Medicaid reimbursement averaged 49.8% of private rates across surveyed states, highlighting the margin pressure that discourages broader participation among general dentists and specialists[4]JAMA Health Forum Editorial Team, “Medicaid Reimbursement Rates and Dentist Participation,” JAMA Health Forum, jamanetwork.com . Administrative burdens such as prior authorization delays and inconsistent claims adjudication compound the reimbursement gap for practices that operate with high fixed overhead and lean staffing models. While states are piloting transparency rules for payment practices and credentialing, these reforms have not yet delivered parity with commercial schedules, so access bottlenecks in Medicaid adult dental coverage are likely to persist without rate and process improvements. This supply-side friction tempers the speed at which coverage expansions translate into realized utilization and claim volume inside the United States dental insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Plan Type: DPPO hegemony, with embedded and DHMO models shaping the growth edge

DPPO held 85.87% of the 2025 landscape, the largest single format in the United States dental insurance market, reflecting employer preference for broad provider choice and national network reach that supports distributed workforces. Other Coverages, a composite of embedded Medicare Advantage dental, marketplace stand-alone plans, and direct-to-consumer offerings, is projected to deliver the fastest expansion within the forecast window, supported by rising plan standardization in select states and active product refresh cycles by national carriers. Carriers continue to differentiate through network scale and utilization management, with UnitedHealthcare communicating strong in-network usage and broad national participation by dentists under its employer-focused contracts. DHMO, offered by multiple large carriers, emphasizes fixed copayments and no deductibles, providing predictable out-of-pocket costs and appealing to price-sensitive members who value straightforward cost-sharing. The United States dental insurance market is also seeing carriers refine PPO product details such as frequency limits and procedure coding updates to keep preventive coverage broad while calibrating major services to align costs and outcomes.

The growth edge within Other Coverages is being shaped by teledentistry access embedded in many large-group PPOs, alignment with MA benefit updates, and marketplace initiatives that reduce variability in plan design for individual buyers. UnitedHealthcare’s introduction of level-funded dental and vision options for small employers beginning in 2026 underscores a push to reach underpenetrated segments with bundled benefits that simplify administration and enrollment. DHMO product suites from Delta Dental and Cigna are evolving with broader panels and revised copay schedules, ensuring that closed-panel offerings retain clear positioning for cost control while maintaining adequate access. Indemnity products continue to serve niche needs where unrestricted choice is prioritized over managed costs, though employers rarely select indemnity as the primary format because of claim variability. At a segment level, DPPO concentration provides a stable baseline for the United States dental insurance market while alternative formats attract growth through targeted design, virtual access, and new funding constructs tailored to small groups and individual buyers.

By Procedure Type: Preventive anchors share, while major procedures lead growth

Preventive services commanded 51.88% share in 2025, reflecting long-standing coverage norms that reimburse routine cleanings, exams, and X-rays at high coinsurance levels when members use in-network providers. Major procedures, including crowns, implants, and complex restorative care, are projected to deliver the highest growth among procedure categories through 2031 as carriers update benefit tiers and codes to reflect more granular clinical workloads and to support medically necessary treatments. Basic procedures such as fillings and extractions sit between preventive and major services in plan schedules, and carriers are adjusting replacement and frequency policies to manage costs in high-volume categories. The United States dental insurance market is responding to care pathway shifts by maintaining strong preventive incentives while creating selective on-ramps for major treatments under clearer authorization criteria and revised fee schedules. Virtual dental access has increased for consults and triage, which complements preventive engagement but still directs members toward in-person care for surgical and prosthetic interventions.

Plan updates by major carriers illustrate the trend, including the addition of new CDT codes for implant maintenance and sedation, which supports accurate billing and opens space for value-based pilots targeting outcomes in complex cases. Preventive coverage shows limited geographic variance because of standard plan templates, while the scope of major services is more sensitive to annual maximums and utilization controls that can vary by employer, product, or state rules. Pediatric orthodontics tied to medical necessity remains a defined component inside ACA Essential Health Benefit packages, while many adult orthodontic benefits remain limited to certain DHMO offerings. As carriers calibrate coinsurance and caps, the United States dental insurance market is aligning long-run cost containment with targeted access to high-value major services, supporting measured adoption where clinical needs justify coverage.

By End-User: Corporate enrolment anchors scale, while individual direct-purchase accelerates

Corporate and employer-sponsored plans form the enrolment backbone of the United States dental insurance market, with national carriers like MetLife serving tens of thousands of group customers and millions of covered employees and dependents across the country. Administrative service models and large-network contracts enable employers to sustain comprehensive preventive coverage and streamlined claims processing, which supports strong participation and stable utilization. Individual direct-purchase channels, however, are the fastest-growing end-user segment, propelled by marketplace reforms that seek to standardize stand-alone dental coverage for consumers and by evolving embedded benefits in Medicare Advantage. Federal benefits programs such as FEDVIP also provide a reference point for plan design across a broad population, with a defined set of national carriers and consistent product documentation that facilitates comparison and informed choice.

Employer contributions remain tax-deductible, and employer-provided dental coverage is excluded from employees’ taxable income, which structurally favors group enrollment relative to post-tax individual purchases unless a member qualifies for marketplace subsidies. Carriers are responding to small-business demand with funding constructs such as level-funded options that bundle dental and vision with medical plans to reduce administrative friction and encourage broader adoption among employers with 2-50 employees. The United States dental insurance market is therefore balancing a large, stable corporate base with a rising share of individual and small-group buyers who seek defined benefits, clear pricing, and virtual access, especially in geographies where provider networks are thinner. As these channels evolve, plan designs are converging around more transparent benefits and standardized coding, which should improve comparability and member experience across end-user types.

By Demographics: Adults dominate coverage today, seniors lead growth into the forecast

Adults aged 21-64 represent the largest share of insured lives, sustained by employer-sponsored coverage that embeds preventive care and routine restorative benefits within familiar DPPO formats. Seniors are expected to lead growth through 2031 as Medicare Advantage dental benefits remain prominent in plan offerings and carriers compete on preventive coverage, with Humana’s 2026 enhancements signaling the competitive stakes. Pediatric coverage maintains a stable base under ACA Essential Health Benefits, which require pediatric dental coverage in individual and small-group plans and align dental cost-sharing with medical plan rules for minors. Broader adoption of DQA-aligned measures, including those in the CMS Child Core Set, is also helping public programs and participating carriers track and improve pediatric outcomes.

In older adults, edentulism has trended lower, and more seniors retain natural teeth, which raises the long-run need for maintenance and restorative services that align with comprehensive benefit tiers. Adults face varied access dynamics by coverage type and geographic location, which highlights the importance of network adequacy enforcement and virtual access to bridge gaps for routine care. Pediatric access is reinforced by Medicaid’s EPSDT requirements and state-level program integration in school-based settings that can reduce barriers for low-income families, as seen in New York’s 2025 managed care update. As a result, the United States dental insurance market is anchored by adult coverage today while drawing incremental growth from seniors and maintaining stable pediatric demand through established public and marketplace frameworks.

Geography Analysis

State-level policy choices and workforce availability shape access and plan design across the United States dental insurance market, with enhanced adult Medicaid dental coverage adopted by 38 states and the District of Columbia by 2025 and 18 states upgrading benefits since 2021. Reform momentum continued in 2025 as 18 states enacted 37 dental insurance laws focused on dental loss ratio reporting, assignment of benefits, and virtual credit card payment transparency, increasing regulatory attention to value and administrative process. Marketplace standardization is also emerging at the state level, exemplified by New York’s 2026 Standard Adult Dental Plan to clarify benefits and cost-sharing for stand-alone dental products sold to individual buyers. These public policy trends frame the context in which carriers adapt plan portfolios and distribution across the United States dental insurance market.

Provider availability remains a decisive local factor, with 7,443 dental Health Professional Shortage Areas affecting 63.7 million people nationwide at year-end 2025 and most shortage designations in rural regions. Large states such as New York, Florida, and California each carry hundreds of dental HPSA designations and sizable practitioner deficits, which test plan directory accuracy, member wait times, and compliance with time-distance rules. Policymakers and carriers are deploying virtual modalities to ease access frictions for triage and follow-up, and several state programs have clarified billing codes and coverage conditions for teledentistry, which supports preventive engagement while maintaining in-person delivery for surgical care. The United States dental insurance market continues to see adjustments to benefit scope and network management in HPSA-heavy counties, which influences realized utilization across public and commercial plans.

States are piloting different approaches to dental loss ratio oversight and data transparency, and early experiences indicate that aggressive requirements can lead to product exits while more calibrated models preserve participation and foster incremental value improvements. Carriers use these regulatory signals to recalibrate benefit designs, administrative processes, and network strategies, which in turn affect competitiveness at the regional level. In this environment, the United States dental insurance market size is supported by policy frameworks that expand nominal coverage while network adequacy, virtual access, and plan standardization determine the pace at which coverage converts into realized care across regions.

Competitive Landscape

National carriers including Delta Dental, MetLife, UnitedHealthcare, Cigna, Aetna, Guardian, United Concordia, Humana, and others anchor the competitive core of the United States dental insurance market, competing on group underwriting scale, network breadth, and digital tools that streamline administration. MetLife’s reach across large employers enables product standardization and cross-sell opportunities, while network partners focus on access, scheduling, and throughput to maintain strong in-network utilization. Carriers are also updating benefit details to better capture clinical complexity, as reflected in MetLife’s 2026 revisions that add implant maintenance and sedation codes in federal program offerings. Together, these moves support product clarity and operational consistency at scale in the United States dental insurance market.

The relationship between payers and provider organizations is evolving as Dental Support Organizations expand affiliation networks and as carriers explore deeper partnerships around data, scheduling, and claims accuracy, areas where artificial intelligence tools and quality metrics can reduce friction. The adoption of Dental Quality Alliance measures into the CMS Child Core Set, and the advancement of a pregnancy oral-evaluation metric to mandatory status in 2026, are examples of how outcomes tracking is moving toward consistent national benchmarks. In addition, teledentistry features are now common in large-group PPO plan designs, reinforcing preventive engagement and care navigation across distributed member populations. These shifts point to a competitive dynamic that rewards carriers and provider networks that coordinate efficiently on access, documentation, and quality.

Market structure is also being tested by vertical integration experiments, such as Delta Dental of Wisconsin’s 2025 acquisition of a multi-practice DSO, which prompted a formal opposition letter from the American Dental Association citing concerns about clinical autonomy and potential conflicts of interest. Carriers continue to position around seniors, where Medicare Advantage plans are broadening dental benefits, highlighted by Humana’s 2026 preventive coverage commitments that aim to raise the competitive floor for senior dental benefits. New small-group funding and bundling constructs, such as level-funded dental and vision offerings integrated with medical, are designed to win a greater share of employers with 2-50 employees who value streamlined administration. These strategies show how the United States dental insurance market blends national scale with targeted segment plays across seniors and small businesses to sustain growth and differentiation.

United States Dental Insurance Industry Leaders

Delta Dental

MetLife

Cigna

Aetna

UnitedHealthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Delta Dental has extended its collaboration with Disabled American Veterans (DAV) by committing USD 150,000 to support the organization's initiatives. As part of this renewed partnership, Delta Dental will also contribute to the development of a specialized dental health resource page on DAV's official website.

- February 2026: Aetna, a CVS Health subsidiary, announced a fully digital benefits onboarding platform for four million members during the 2026 welcome season. Utilizing digital tools and Rich Communication Services (RCS) text messaging, the platform enhances navigation and self-service, providing streamlined access to essential information and support at the start of the plan year.

- December 2025: The Dental Quality Alliance launched a State Oral Healthcare Quality Dashboard using T-MSIS data to enable performance benchmarking across Medicaid and CHIP populations.

- October 2025: Humana announced that all 2026 Medicare Advantage plans will include two annual cleanings, exams, and X-rays, with broader periodontal service inclusion across many products.

United States Dental Insurance Market Report Scope

Dental insurance is coverage protection for dental treatments. The United States Dental Insurance Market is segmented by Coverage (Dental health maintenance organizations (DHMO), Dental preferred provider organizations (DPPO), Dental Indemnity plans (DIP), Dental exclusive provider organizations (DEPO), and Dental point of service (DPS)), by Procedure (Preventive, major, and basic), by End-users (Individuals and corporates), by Industries (Chemicals, Refineries, Metal and mining, food and beverages, and others), and by demographics (senior citizens, adults, and minors).

By Plan Type

| Dental Health Maintenance Organization (DHMO) |

| Dental Preferred Provider Organization (DPPO) |

| Dental Indemnity Plans (DIP) |

| Other Coverages |

By Procedure Type

| Preventive |

| Major |

| Basic |

By End-User

| Individual |

| Corporates |

By Demographics

| Senior Citizens |

| Adult |

| Minors |

| By Plan Type | Dental Health Maintenance Organization (DHMO) |

| Dental Preferred Provider Organization (DPPO) | |

| Dental Indemnity Plans (DIP) | |

| Other Coverages | |

| By Procedure Type | Preventive |

| Major | |

| Basic | |

| By End-User | Individual |

| Corporates | |

| By Demographics | Senior Citizens |

| Adult | |

| Minors |

Key Questions Answered in the Report

What is the outlook for the United States dental insurance market through 2031?

The United States dental insurance market size is projected to rise from USD 17.20 billion in 2026 to USD 21.61 billion by 2031 at a 4.67% CAGR, supported by stable DPPO enrolment, MA benefit competition, and state-level reforms that enhance transparency and access.

Which plan format leads in the United States dental insurance market?

DPPO is the leading format with 85.87% share in 2025, favored by employers for nationwide networks and flexible access designs that accommodate distributed workforces.

Which procedure category is growing the fastest through 2031?

Major procedures are forecast to post the highest growth, while preventive services retain the largest share due to strong coverage norms for cleanings, exams, and X-rays across carriers.

How are state policies influencing dental coverage trends?

States have enacted wide-ranging dental insurance reforms and expanded adult Medicaid dental coverage, with 38 states plus DC offering enhanced adult benefits in 2025 and multiple states standardizing marketplace products.

What is changing for seniors in dental coverage?

Medicare Advantage plans widely include dental benefits, but comprehensive offerings remain limited, prompting competitive updates such as Humana’s 2026 nationwide preventive coverage for all MA members.

Where do access gaps remain most significant?

Dental HPSAs cover 63.7 million people nationally with the majority in rural areas, making network adequacy and virtual access strategies critical for closing distance and wait-time barriers.

Page last updated on: