Market Overview

| Study Period | 2020 - 2031 |

|---|---|

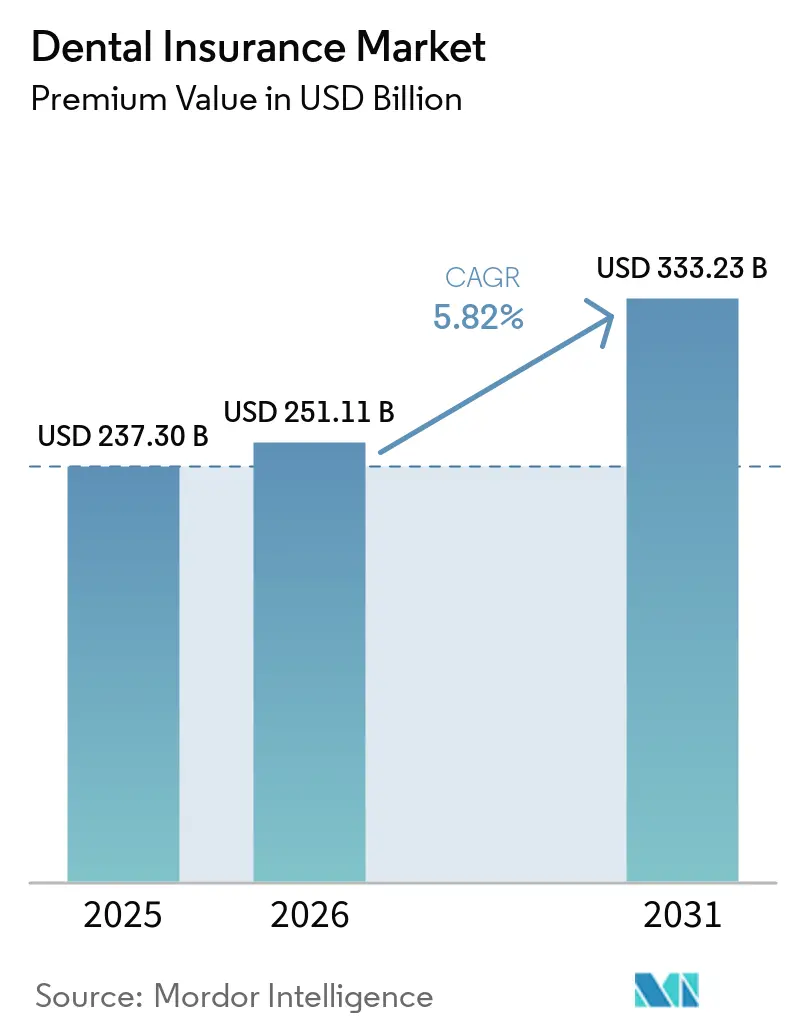

| Market Size (2026) | USD 251.11 Billion |

| Market Size (2031) | USD 333.23 Billion |

| Growth Rate (2026 - 2031) | 5.82% CAGR |

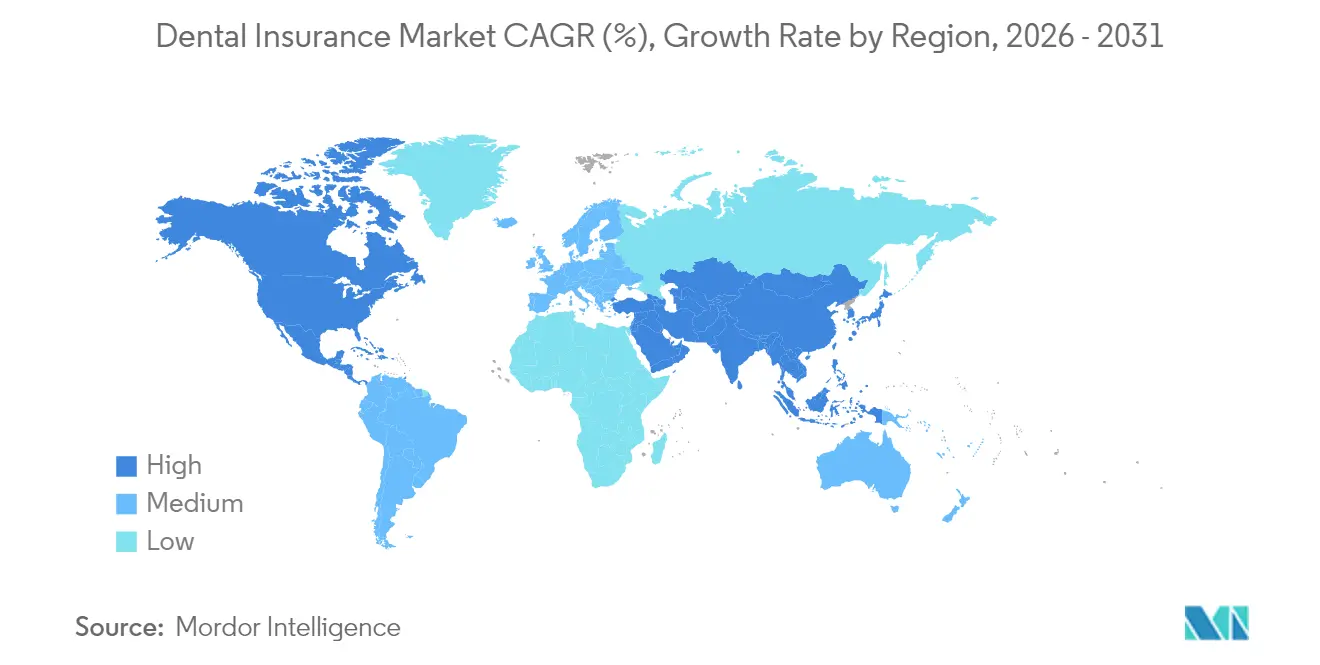

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Insurance Market Analysis by Mordor Intelligence

The Dental Insurance Market size in terms of premium value is projected to expand from USD 237.30 billion in 2025 and USD 251.11 billion in 2026 to USD 333.23 billion by 2031, registering a CAGR of 5.82% between 2026 to 2031.

Demand pivots toward preventive care as employers and public programs eliminate cost-sharing for routine services, while tele-dentistry makes coverage attractive to remote populations. Employer-sponsored benefit expansion among small and medium enterprises in Asia-Pacific, regulatory mandates that embed pediatric dental benefits in essential health packages, and artificial intelligence adoption in claims processing combine to accelerate the uptake of dental policies. Preferred Provider Organization (PPO) products maintain leadership because they balance provider choice and cost containment, yet discount dental plans record the fastest growth as consumers seek budget-friendly options during inflationary periods. Investors also favor insurers that digitize workflows and partner with tele-dentistry platforms to reduce administrative expenses, improve member engagement, and reach underserved areas.

Key Report Takeaways

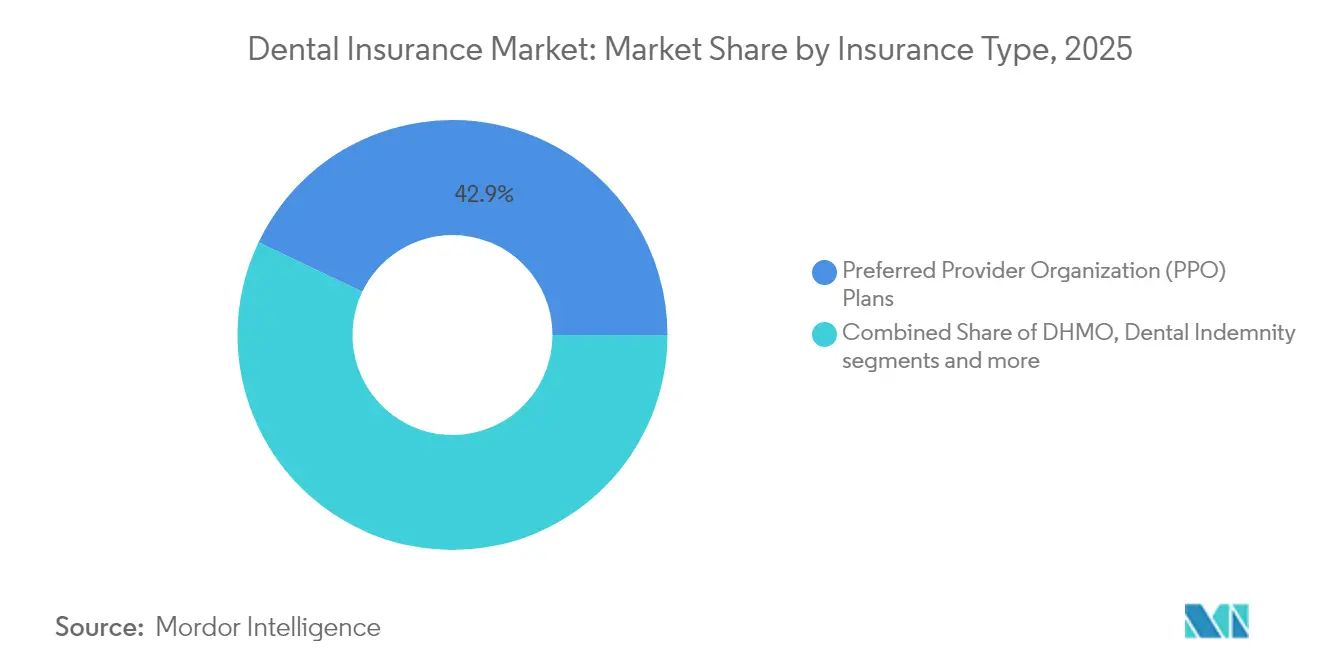

- By insurance type, Preferred Provider Organization plans held 42.90% of the dental insurance market share in 2025, while discount dental plans are projected to expand at a 9.02% CAGR to 2031.

- By coverage, preventive care accounted for 41.70% of the dental insurance market size in 2025; orthodontic and cosmetic coverage is forecast to advance at a 9.85% CAGR through 2031.

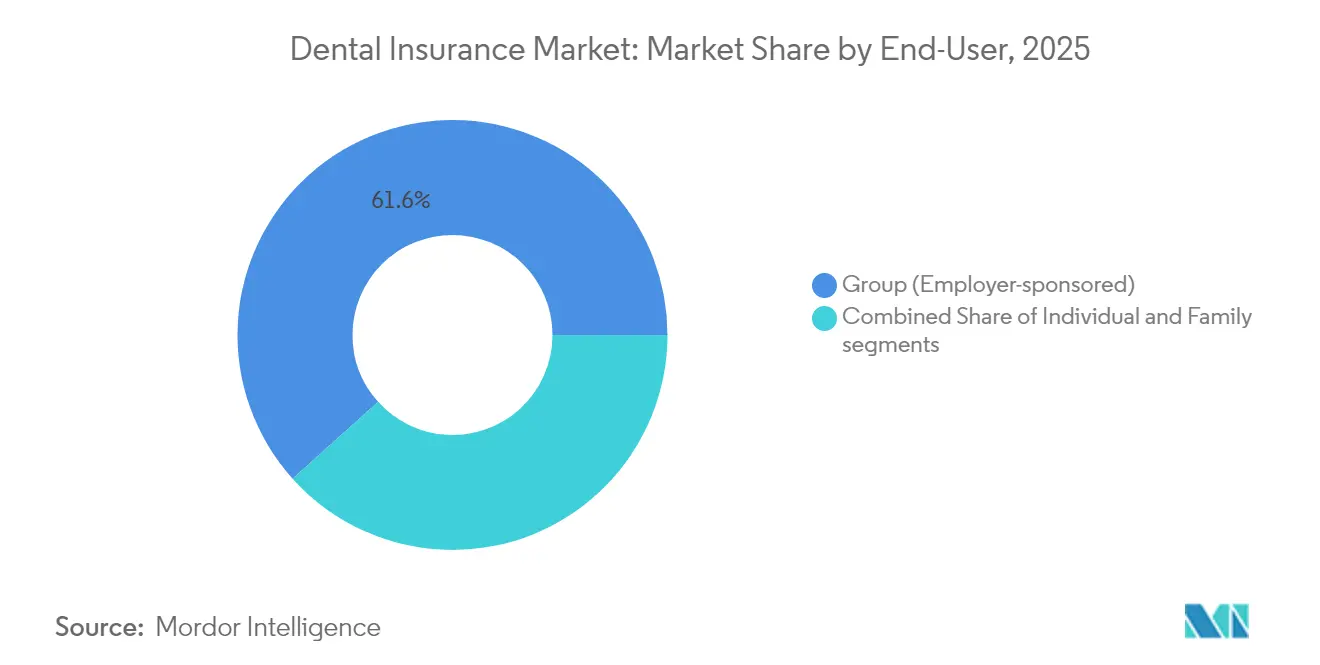

- By end-user, group employer-sponsored policies captured 61.65% revenue share in 2025, whereas the family segment is set to grow at a 9.05% CAGR to 2031.

- By geography, North America commanded 35.10% of 2025 revenue in the dental insurance market, yet Asia-Pacific is expected to post a 10.20% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Dental Insurance Market*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of preventive dental care under value-based insurance models | +2.1% | North America, Europe | Medium term (2–4 years) |

| Employer-sponsored dental benefits expansion among SMEs | +1.8% | Asia-Pacific, Latin America | Long term (≥ 4 years) |

| Integration of teledentistry services into dental plans | +1.4% | Europe, North America | Short term (≤ 2 years) |

| Aging population driving prosthodontic demand | +1.2% | Japan, Western Europe | Long term (≥ 4 years) |

| Rising disposable income enabling voluntary coverage | +0.9% | Latin America, Southeast Asia | Medium term (2–4 years) |

| Government mandates for pediatric dental coverage | +0.8% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Preventive Dental Care Under Value-Based Insurance Models

Value-based plan designs waive cost-sharing for routine cleanings, examinations, and fluoride treatments, encouraging members to seek care earlier and avoid expensive restorative work[1]Delta Dental Plans Association, “2025 Adult Oral Health & Wellness Survey,” deltadental.com. Delta Dental reports that 65% of U.S. adults now maintain dental coverage, while 91% view oral check-ups as vital as annual physicals. Preventive visits rise and emergency visits decline, trimming claim costs and boosting satisfaction. Employers highlight dental benefits to win talent, and regulators in nine American states now apply medical-loss-ratio-style rules to dental plans to ensure consumers receive value. The emphasis on prevention underpins sustained expansion of the dental insurance market.

Employer-Sponsored Dental Benefits Expansion Among SMEs in Asia

More small and medium enterprises in Asia-Pacific add dental insurance to retain skilled workers amid tight labor conditions. Flexible benefit menus, digital enrollment portals, and premium subsidies encourage take-up in countries such as India, Vietnam, and Indonesia. Insurers capitalize on relaxed foreign-ownership caps to launch co-branded products that bundle dental with health or accident cover, unlocking scale across fragmented employer groups. Advanced data analytics assist carriers in tailoring premiums to each firm’s risk profile, reducing adverse selection and stimulating broader coverage penetration.

Integration of Teledentistry Services into Dental Plans

Teledentistry's integration into dental plans is becoming a pivotal force in the global dental insurance market, bolstering accessibility and preventive care. Insurers are now covering virtual consultations, diagnostics, and follow-ups, aiming to cut treatment costs and boost patient engagement. This digital transition allows for real-time monitoring of oral health and timely interventions, which could lead to a decrease in claim frequency over time. With healthcare systems adopting telehealth infrastructures, collaborations among insurers, dental networks, and digital platforms are broadening coverage and enhancing convenience for policyholders globally.

Aging Population Driving Prosthodontic Procedure Coverage Demand

Japan’s median age now exceeds 49 years. Seniors require crowns, bridges, and implant-supported restorations to maintain nutrition and life quality. European insurers also offer enhanced major-procedure tiers that reimburse a larger share of prosthodontic fees. Product innovation includes lifetime maximums indexed to inflation, age-banded premium tables, and care-coordination services that guide members to accredited oral surgeons. Insurers partner with dental service organizations to negotiate bundled implant pricing, containing costs as utilization climbs.

Restraints Impact Analysis of Dental Insurance Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited provider networks in rural Africa & MEA | -1.6% | Africa, Middle East | Long term (≥ 4 years) |

| High loss ratios from restorative cost inflation | -1.3% | United States | Short term (≤ 2 years) |

| Consumer perception of low value vs out-of-pocket costs | -0.8% | Europe, APAC | Medium term (2–4 years) |

| Regulatory caps on premium increases in select APAC markets | -0.7% | China, select ASEAN | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Limited Dental Service Provider Networks in Rural Africa & MEA Reducing Claim Utilization

Average dentist density across 27 low-income countries remains well below World Health Organization benchmarks, and only nine have formal oral health policies[2]Global Health Research and Policy, “Dentist Density and National Oral Health Policies in Low-Income Countries,” biomedcentral.com. Sparse provider networks lower claim utilization and weaken the value proposition of the dental insurance market in these regions. In Saudi Arabia, only 11.5% of adults undertake routine check-ups, and non-insured populations visit even less often. Low penetration deters investment in new clinics, perpetuating a cycle of limited supply and muted demand.

High Loss Ratios from Inflation in Restorative Procedure Costs in the United States

Nine states require public reporting of dental loss ratios, and Massachusetts mandates that at least 83% of premium revenue fund patient care[3]Amwins Connect, “Massachusetts Dental Loss Ratio Implementation Guide,” amwins.com. Inflation pushes the average fee for a crown toward USD 1,500, squeezing insurer margins. Carriers respond by raising annual maximum limits slowly, encouraging network dentists to adopt lower-cost materials, and investing in artificial intelligence that flags claim anomalies. Some underwriters pivot toward value-based payment models that reward providers for outcome metrics instead of volume.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Dental Insurance Market Segment Analysis

By Insurance Type:

PPO Plans Sustain Leadership While Discount Products AccelerateThe dental insurance market size for PPO policies totaled 42.90% of global revenue. Discount dental plans expanded briskly at a 9.02% CAGR, signaling an appetite for predictable flat-fee memberships that sidestep complex claim forms. PPOs outperform alternatives by locking in negotiated fees and still letting policyholders choose among thousands of dentists. Providers tolerate lower reimbursement because high patient volumes remain attractive. Meanwhile, Health Maintenance Organization (DHMO) and indemnity formats maintain niche roles, appealing to members who prefer capitation or unrestricted access, respectively. Competitive tension among plan types widens the overall dental insurance market by catering to diverse affordability thresholds and care preferences.

PPO network depth provides negotiating leverage that restrains fee inflation for basic procedures, favorably affecting overall dental insurance market share distribution. Discount plans thrive among younger workers and gig-economy participants whose employers rarely subsidize coverage. Many insurers bundle discount cards with telehealth for virtual triage and prescription refills, enhancing perceived value. As inflation continues, employers may tilt toward lower-premium designs, but regulatory focus on transparency will ensure consumer awareness of service limitations particularly on major restorative benefits.

By Coverage:

Preventive Care Dominates While Cosmetic Demand GrowsPreventive policies accounted for 41.70% of the 2025 dental insurance market share, buoyed by scientific evidence tying oral hygiene to chronic disease reduction. Carriers fully cover two cleanings per year plus fluoride varnish for children, positioning prevention as the foundation of overall wellness. Orthodontic and cosmetic riders grow fastest at a 9.85% CAGR, favored by demographics with heightened aesthetic expectations such as Gen Z. Many employers now reimburse a portion of clear aligner programs during open enrollment, signaling mainstream acceptance of cosmetic treatments within benefit budgets.

Basic restorative coverage still anchors the proposition for risk pooling, funding fillings and extractions that are statistically common. Major prosthodontics represent a smaller but high-ticket pool, which insurers manage through waiting periods and shared costs. Teledentistry platforms improve claims efficiency for preventive and basic categories by differentiating urgent from elective needs in real time. Over the forecast period, wider deployment of artificial-intelligence radiograph analysis could shift underwriting models toward more personalized premium tiers, further segmenting the dental insurance industry landscape.

By End-User:

Employers Lead but Family Policies Gain MomentumGroup contracts generated 61.65% of 2025 premium volume, cementing corporate payroll deduction as the most efficient distribution route. Many U.S. employers pay 70% or more of employee premiums, lowering after-tax costs and reducing turnover. However, dual-income households increasingly purchase stand-alone family plans that bundle pediatric orthodontia and accident riders. The dental insurance industry size for family policies is projected to rise at a 9.05% CAGR as urban middle-class populations grow in Asia and Latin America.

Gig-economy growth erodes access to employer plans in mature economies, prompting insurers to craft portable, app-based policies with monthly billing. Medicare Advantage and Medicaid managed-care programs in the United States also offer embedded dental benefits. Humana reported that 79% of its Medicare Advantage membership received major service coverage in 2025, illustrating the blurring boundary between traditional group and public segments. As value-based reimbursement gains traction, family plans may incorporate preventive-visit incentives that rebate premium credits for timely check-ups.

Geography Analysis

North America Dental Insurance Market

North America accounts for 35.10% of global revenue contributed by entrenched private insurance, robust employer participation, and public-sector mandates that guarantee pediatric coverage. Nine U.S. states limit administrative spending via dental loss ratio rules, protecting consumers and sustaining trust in the dental insurance market. Canada’s National Dental Care Plan now covers 2.1 million seniors and extends benefits to 1.2 million additional children and disabled adults, creating spill-over opportunities for supplemental private policies.

APAC Dental Insurance Market

Asia-Pacific records the fastest CAGR at 10.20% through 2031 as disposable incomes rise and governments liberalize foreign ownership. Regional regulators introduce IFRS-17-aligned solvency rules, pressing carriers to refine risk pricing. Japan integrates dental care into universal health care for seniors, while China caps premium increases and subsidizes rural clinic construction. These dynamics expand the dental insurance market without compromising affordability.

Europe Dental Insurance Market

Europe presents steady but varied growth. Universal systems in Denmark and Germany offer free school-age dentistry, limiting private demand, whereas targeted systems in Spain or Ireland leave gaps that insurers fill. Pandemic-era tele dentistry adoption remains high; insurers reimburse video assessments and mail-in aligner programs that cut travel for rural residents.

LATAM Dental Insurance Market

Latin American insurers capture new voluntary buyers as annual household incomes surpass USD 10,000. Odontoprev’s debt-free model and 23% net-income CAGR reflect this momentum, and rivals emulate its nationwide dentist network to achieve scale. Government subsidies remain limited, but public awareness campaigns stress oral health links to cardiovascular disease, boosting policy uptake.

MEA Dental Insurance Market

Middle East and Africa lag due to sparse dentist density—often below one dentist per 10,000 inhabitants—and limited public funding. Ghana and Kenya pilot mobile-clinic programs and micro-insurance, yet premium volume stays modest. Market expansion hinges on training more professionals, subsidizing rural clinics, and forming public-private partnerships that guarantee baseline preventive services.

Competitive Landscape

Moderate consolidation defines the dental insurance industry. UnitedHealth Group served 54 million dental members through Optum-linked networks, sustaining an 85.5% medical care ratio. MetLife rolled out its Dental Hub with Skygen to automate credentialing for 50 million members, cutting administrative cycle time by 40%. Cigna divested its Medicare Advantage unit to sharpen its focus on core health and dental lines, reallocating USD 3.3 billion of sale proceeds toward digital consumer platforms.

Private equity continued its appetite for dental assets, highlighted by Patient Square Capital’s USD 4.1 billion purchase of Patterson Cos., a supply distributor diversifying into insurance adjuncts. Many carriers deploy artificial intelligence to flag duplicate X-rays and autofill claim fields, reducing adjudication times to under five days. Teledentistry partnerships extend provider reach into rural zones and differentiate product portfolios. Competitive intensity centers on technology maturity and network breadth rather than price alone, preserving underwriting discipline even as discount plans gain share.

Strategic moves also target underserved demographics. Guardian Life expands in the gig-economy segment with on-demand policies linked to ride-sharing platforms. Sun Life Financial pilots wellness wallets that reward preventive visits with contribution credits redeemable against major procedures. International giants like Allianz and AXA scale dental bancassurance via regional bank tie-ups in Southeast Asia, leveraging branch penetration to cross-sell policies.

Dental Insurance Industry Leaders

Delta Dental

UnitedHealth Group

Cigna Group

CVS Health / Aetna

MetLife Inc.

- *Disclaimer: Major Players sorted in no particular order

Dental Insurance Market Companies Covered in this Report

- Delta Dental

- UnitedHealth Group

- Cigna Group

- CVS Health / Aetna

- MetLife Inc.

- Humana Inc.

- Guardian Life Insurance Company of America

- Sun Life Financial Inc.

- AXA SA

- Allianz SE

- Zurich Insurance Group

- Bupa

- Anthem Blue Cross Blue Shield

- Assicurazioni Generali S.p.A.

- DentaQuest (Elevance Health)

- Renaissance Dental

- Nippon Life Insurance

- Dai-ichi Life Holdings

- Ping An Insurance

- Discovery Health (South Africa)

- Medibank Private (Australia)

- Pacific Blue Cross (Canada)

- Liberty Dental Plan

Recent Industry Developments in Dental Insurance Market

- January 2025: Welsh, Carson, Anderson & Stowe bought a majority stake in LIBERTY Dental Plan, which manages 5.8 million members, to broaden Medicare and Medicaid reach.

- April 2025: MetLife launched Dental Hub with Skygen to streamline credentialing and improve access for 50 million members.

- June 2024: Nine U.S. states have introduced dental loss ratio regulations to ensure a higher share of premiums go toward patient care. Massachusetts led the way by mandating that at least 83% of dental insurance premiums be spent on care services.

- January 2024: Cigna agreed to sell its Medicare Advantage business to HCSC for USD 3.3 billion, enhancing focus on core dental and medical lines

Global Dental Insurance Market Report Scope

The report offers a complete background analysis of the Dental Insurance Market, which includes an assessment of the emerging market trends by segments, significant changes in the market dynamics, and the market overview. Global Dental Insurance Market is segmented by Coverage (Dental health maintenance organizations (DHMO), Dental preferred provider organizations (DPPO), Dental Indemnity plans (DIP), Dental exclusive provider organizations (DEPO), and Dental point of service (DPS)), by Procedure (Preventive, major, and basic), by End-users (Individuals and corporates), by demographics (senior citizens, adults, and minors) and by Geography (North America, South America, Asia-Pacific, Europe, and Middle-East and Africa). The report offers market size and forecast values for the Dental Insurance Market in USD billion for the above segments.

Segmentation Overview

By Insurance Type

| Preferred Provider Organization (PPO) Plans |

| Health Maintenance Organization (DHMO) Plans |

| Dental Indemnity / Fee-for-Service Plans |

| Discount Dental Plans |

By Coverage

| Preventive Coverage |

| Basic (Restorative) Coverage |

| Major (Prosthodontic) Coverage |

| Orthodontic & Cosmetic Coverage |

By End-User

| Group (Employer-Sponsored) |

| Individual |

| Family |

By Region

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Switzerland | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East & Africa |

| By Insurance Type | Preferred Provider Organization (PPO) Plans | |

| Health Maintenance Organization (DHMO) Plans | ||

| Dental Indemnity / Fee-for-Service Plans | ||

| Discount Dental Plans | ||

| By Coverage | Preventive Coverage | |

| Basic (Restorative) Coverage | ||

| Major (Prosthodontic) Coverage | ||

| Orthodontic & Cosmetic Coverage | ||

| By End-User | Group (Employer-Sponsored) | |

| Individual | ||

| Family | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Switzerland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size of the dental insurance market?

The dental insurance market reached USD 251.11 billion in 2026 and is on track to hit USD 333.23 billion by 2031.

Which region holds the largest dental insurance market share?

North America leads with 35.10% of global revenue because of mature employer benefits and regulatory mandates.

Which coverage type generates the most revenue?

Preventive care policies dominate, capturing 41.70% of 2025 global revenue thanks to value-based designs that waive cost-sharing for routine visits.

What is the fastest-growing geographic market for dental insurance?

Asia-Pacific is projected to grow at a 10.20% CAGR through 2031, driven by rising incomes and relaxed ownership rules.

Page last updated on: