United States Air Freight Ancillary Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

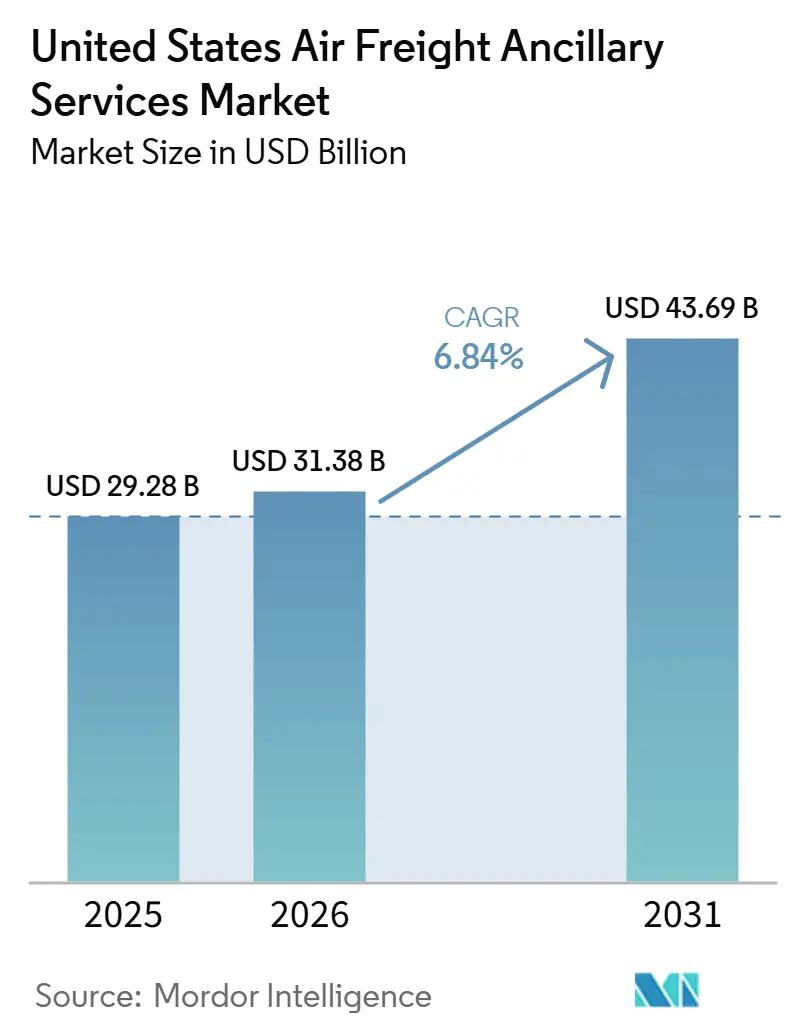

| Base Year Market Size (2025) | USD 29.28 Billion |

| Market Size (2026) | USD 31.38 Billion |

| Market Size (2031) | USD 43.69 Billion |

| Growth Rate (2026 - 2031) | 6.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Air Freight Ancillary Services Market Analysis by Mordor Intelligence

The United States air freight ancillary services market was valued at USD 29.28 billion in 2025 and is estimated to grow from USD 31.38 billion in 2026 to reach USD 43.69 billion by 2031, at a CAGR of 6.84% during the forecast period 2026-2031.

The United States air freight ancillary services market is being shaped by tighter pharmaceutical handling requirements, deeper shipper demand for integrated door-to-door execution, and a broader shift toward bundled logistics services rather than stand-alone freight moves. Services such as temperature-controlled handling, cargo consolidation, packaging, customs support, and real-time visibility now sit closer to the center of contract value, which is changing how providers compete and how customers evaluate service depth. Policy changes affecting low-value parcel flows are also pushing more volume into customs-cleared and consolidated air freight channels, which increases the need for documentation, packaging, and handling support. Competition in the United States air freight ancillary services market is increasingly tied to certified cold-chain assets, controlled capacity, digital booking systems, and the ability to manage regulated cargo without service breaks. Margin pressure remains present, but it is also creating room for operators that can pair compliance capability with network reach and steady execution on high-value trade lanes.

Key Report Takeaways

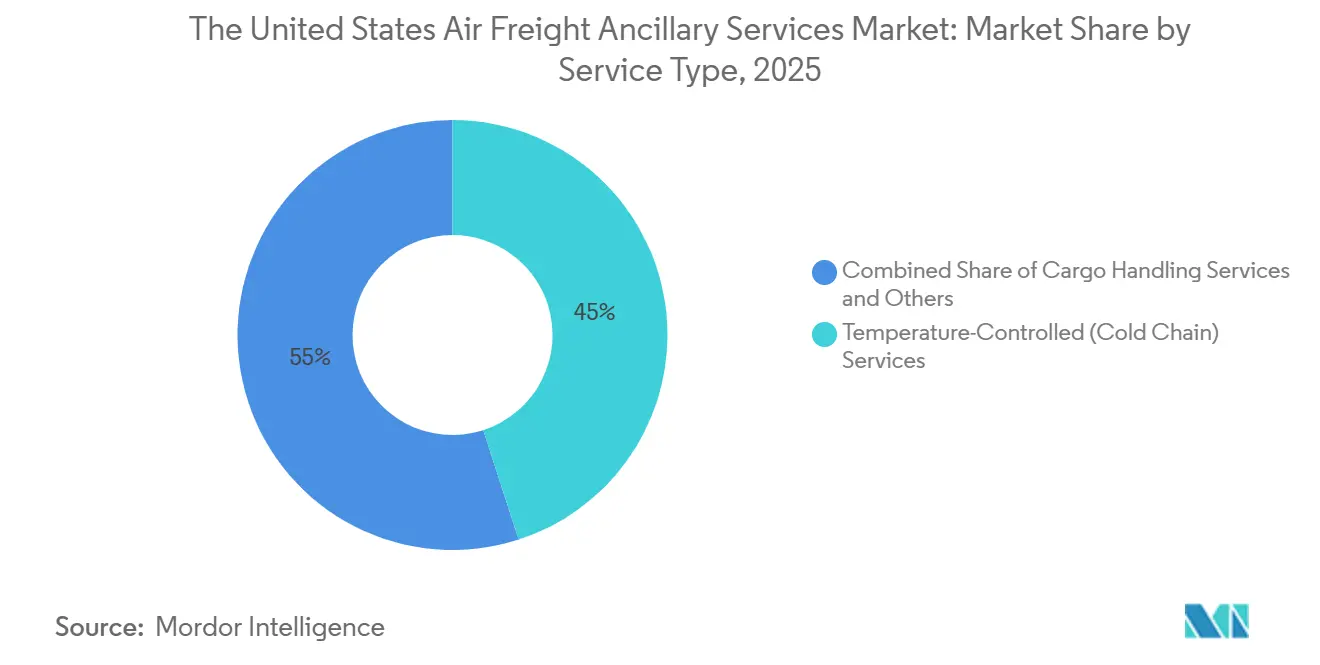

- By service type, temperature-controlled services held 45.02% of the United States air freight ancillary services market share in 2025 and are forecast to expand at 8.21% CAGR through 2031.

- By shipment type, international shipments accounted for 48.27% of the United States air freight ancillary services market size in 2025 and are forecast to expand at a 7.14% CAGR through 2031.

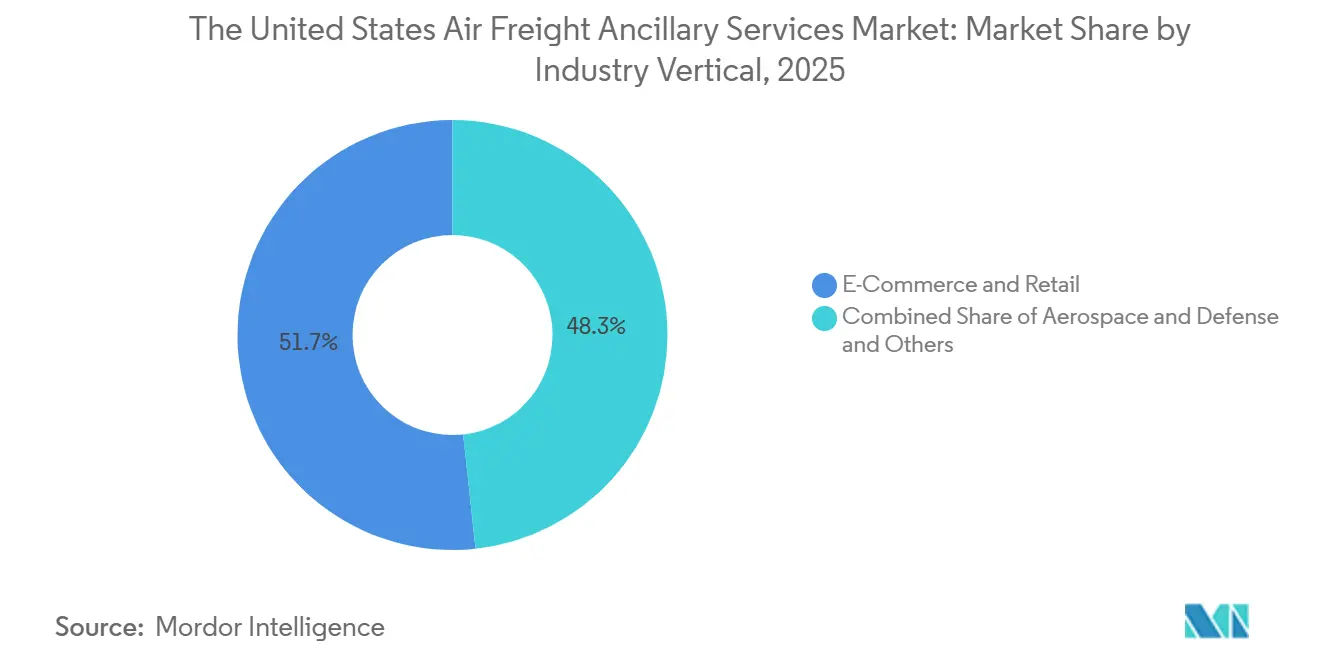

- By industry vertical, e-commerce and retail held 51.71% of the United States air freight ancillary services market share in 2025, while healthcare and technology are forecast to expand at a 10.15% CAGR through 2031.

- By region, the West accounted for 40.11% of the United States air freight ancillary services market size in 2025, while the Southeast is forecast to expand at a 8.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Air Freight Ancillary Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Parcel Consolidation Demand | +1.6% | Global, concentrated in the United States domestic and transpacific lanes | Short term (≤ 2 years) |

| Pharmaceutical Cold Chain Compliance Needs | +1.9% | North America and Europe, with spillover to Asia-originating biologics lanes | Medium term (2-4 years) |

| Higher Demand for Single-Invoice Door-to-Door Solutions | +0.8% | Global, strongest on international trade lanes | Medium term (2-4 years) |

| Real-Time Cargo Visibility and Chain-of-Custody Expectations | +0.9% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Nearshoring-Led United States-Mexico Air Cargo Reconfiguration | +1.1% | North America, especially the United States Southwest, and border corridors | Short term (≤ 2 years) |

| Specialized Handling Demand for High-Value Electronics and Batteries | +0.7% | Global, with strong relevance in transpacific and intra-North America lanes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pharmaceutical Cold Chain Compliance Reshapes Ancillary Revenue Structures

The United States air freight ancillary services market is seeing cold-chain compliance move from a specialist function to a core operating requirement for providers serving healthcare cargo. FDA good distribution requirements and IATA CEIV Pharma standards are pushing operators to maintain documented temperature integrity at each transfer point, turning handling, packaging, and monitoring into contract-critical service lines. This shift matters because the value of the shipment is now tied not only to speed, but also to proof that conditions remained within approved ranges throughout the warehouse, ramp, and handoff activities. GEODIS reinforced this direction in October 2025, when it opened a dedicated healthcare cold-chain cross-docking facility in Chicago with dual-zone, temperature-controlled storage near O'Hare International Airport[1]Source: GEODIS, “GEODIS Unveils First Cold Chain Cross-Dock Facility in the Americas,” PR Newswire, prnewswire.com. As a result, the United States air freight ancillary services market is directing a larger share of premium revenue toward operators with certified facilities, documented processes, and stronger temperature-control discipline.

E-Commerce Parcel Consolidation Demand Drives New Ancillary Bundling Models

The United States air freight ancillary services market is also supported by a shift away from simpler, low-value parcel structures toward more consolidated, document-heavy shipment flows. That shift is increasing the value of packaging, labeling, customs support, cargo handling, and consolidated forwarding because these steps now determine whether parcel-heavy cargo can move without delay. The operational result is that providers are trying to bundle more tasks into one managed transaction rather than leaving packaging, customs, and forwarding to separate specialists. This favors platforms and forwarders that can reduce handoffs, maintain invoice clarity, and support faster exception handling across international lanes. In the United States air freight ancillary services market, this trend is elevating the role of bundled parcel handling, even as freight growth is not evenly distributed across all shipment categories.

Nearshoring-Led United States-Mexico Corridor Reconfiguration Creates New Ancillary Demand Pools

The United States air freight ancillary services market is gaining new demand from the restructuring of North American manufacturing and the tighter logistics connection between the United States and Mexico. Nearshoring is changing the service mix because manufacturers need customs brokerage, cross-border warehousing, time-definite ground-to-air transfers, and origin documentation alongside core freight execution. C.H. Robinson highlighted the expansion of industrial parks linked to Mexico's manufacturing program in its April 2026 cross-border update, which shows that new demand nodes are forming across major production states and border-linked corridors. UPS responded in May 2026 with a USD 50 million investment in its North American Air Freight network to add time-definite heavy air freight service to and from Mexico, while bundling transportation, customs brokerage, and warehousing into a single offering[2]Source: UPS Supply Chain Solutions, “UPS Invests $50 Million to Transform Logistics for North American Automotive and Industrial Manufacturers,” UPS Newsroom, about.ups.com. This means the United States air freight ancillary services market is not only adding corridor volume, but is also increasing the value of integrated border-facing services that many legacy operators were not built to provide.

Real-Time Cargo Visibility and Chain-of-Custody Expectations Accelerate Technology Investment

The United States air freight ancillary services market is also moving toward greater digital control, as shippers in pharmaceuticals, semiconductors, and aerospace now treat visibility as a basic service requirement. IATA's ONE Record framework is pushing the sector toward interoperable data exchange, making real-time cargo information part of everyday operations rather than a premium feature. When customers can track location, timing, and handoff status with less delay, ancillary services such as exception management, compliance reporting, and chain-of-custody support become more valuable and easier to defend in pricing. The practical effect is that digital capability now supports retention just as much as physical network scale does. In the United States air freight ancillary services market, providers that cannot provide auditable shipment data across the full movement are becoming less relevant in higher-value, more regulated verticals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fuel Surcharges and Rate Volatility in Time-Critical Shipments | -1.4% | Global, most acute on transpacific and United States-Middle East lanes | Short term (≤ 2 years) |

| Capacity Constraints in Peak-Lane and Belly-Hold Networks | -1.0% | North America and transpacific lanes, with spillover to Atlantic routes | Medium term (2-4 years) |

| High Compliance Burden for Temperature-Controlled and Dangerous Goods Flows | -0.8% | Global, the highest in the United States, domestic, and EU import lanes | Medium term (2-4 years) |

| Labor Dependence and Facility Throughput Bottlenecks at Major Cargo Hubs | -0.6% | United States domestic express hubs and international gateways | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fuel Surcharges and Rate Volatility Erode Ancillary Margin Predictability

The United States air freight ancillary services market remains exposed to fuel-linked pricing swings because ancillary contracts often sit atop transport costs that change faster than service fees can be reset. Time-critical shipments usually depend on packaging, handling, insurance, and documentation bundles sold under service commitments, but the transport leg can be subject to weekly surcharge changes. That mismatch makes forward pricing harder and weakens margin visibility for providers supporting healthcare, aerospace, and premium electronics cargo. C.H. Robinson noted in April 2026 that tankering remained a scenario risk on selected long-haul routes, which means aircraft may carry extra fuel to avoid costly stops and leave less room for paying cargo. In the United States air freight ancillary services market, that combination of unstable transport cost and reduced payload can disrupt both contracted volumes and labor planning on sensitive lanes.

Capacity Constraints in Peak-Lane and Belly-Hold Networks Limit Ancillary Throughput

The United States air freight ancillary services market also faces a structural limit when dedicated freighter space or belly-hold availability tightens during peak periods. C.H. Robinson stated in March 2026 that dedicated freighter availability remained constrained across North America, limiting the system's ability to absorb sudden demand spikes and weakening routing flexibility during disruptions. When capacity is tight, ancillary providers have less room to recover from service failures, rework bookings, or protect high-value cargo with preferred handling windows. The Cargo Airline Association also warned in May 2026 that potential CBP staffing actions at Newark, Los Angeles, Chicago, and San Francisco could disrupt predictable international processing at major United States gateways. In the United States air freight ancillary services market, providers with controlled capacity, diversified gateways, and stronger customs coordination will remain better positioned as throughput pressure rises.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Cold Chain Emerges as the Market's Defining Revenue Layer

Temperature-controlled services held 45.02% of the United States air freight ancillary services market share in 2025, and this segment is also projected to expand at 8.21% CAGR through 2031. That lead reflects the way healthcare cargo has shifted service value away from basic uplift and toward validated handling, monitored storage, and documented handoffs. In the United States air freight ancillary services market, cold-chain services now have greater pricing power because the operational risk of a temperature break is far higher than that associated with standard general cargo. This makes certified rooms, trained staff, packaging controls, and transfer discipline more important than simple warehouse space.

Cargo handling and cargo consolidation services remain the next-largest revenue streams because large parcel and retail flows still require sorting, build-up, unitization, and export preparation before uplift. Packaging and labeling also remain stable contributors, but the work is becoming more demanding in sensitive categories such as batteries and regulated electronics. IATA's 2026 lithium battery guidance increased the documentation and labeling burden for battery-powered goods, which supports the pricing of specialized packaging and acceptance support[3]Source: International Air Transport Association, “Lithium Battery Guidance Document, IATA Dangerous Goods Regulations 67th Edition,” IATA, iata.org.

By Shipment Type: International Cargo Complexity Fuels Ancillary Service Depth

International shipments accounted for 48.27% in 2025, and this segment is projected to expand at a 7.14% CAGR through 2031. Cross-border air cargo requires additional layers of support because customs brokerage, cargo insurance, documentation review, labeling, visibility, and compliance checks are more difficult to avoid on international lanes. That makes international freight the deeper ancillary revenue pool on a per-shipment basis, even when not every cross-border lane grows at the same speed. DSV also expanded its Shanghai Star route in November 2025 to connect Asia with the Americas via Chicago Rockford, underscoring the same preference for controlled international capacity on high-touch lanes.

Domestic shipments account for the remaining share, and their demand pattern is shaped more by urgent healthcare distribution, express replenishment, and time-definite business moves within the United States. The domestic side of the United States air freight ancillary services market still needs support for packaging, handling, and visibility. Still, customs-related complexity is usually lighter than for international cargo. This keeps the ancillary stack narrower on average, even when domestic networks are critical for premium same-day and next-day flows. The gap does not mean domestic work is simple, because biologics and urgent components still require strict handoff discipline, fast exception management, and dependable airport-to-facility coordination. The result is that international freight remains the heavier ancillary segment by value, while domestic freight remains important for service density, repeat customer relationships, and network utilization.

By Industry Vertical: Healthcare Disrupts E-Commerce's Revenue Supremacy

E-commerce and retail accounted for 51.71% of the United States air freight ancillary services market size in 2025, underscoring the extent to which the United States air freight ancillary services market still relies on parcel consolidation, documentation support, labeling, and fulfillment-linked handling for consumer goods flows. Retail volumes continue to matter because high shipment frequency creates repeat demand for standardized ancillary tasks, especially in consolidated channels where large numbers of parcels must move.

Healthcare and technology are projected to expand at a 10.15% CAGR through 2031, indicating a faster shift toward compliance-heavy, higher-margin cargo. That difference matters because healthcare shipments usually require stricter temperature control, stronger chain-of-custody discipline, and more intensive exception management than general retail freight does. The vertical structure, therefore, shows a shift in value concentration, even if retail remains the largest-volume anchor.

Geography Analysis

The West accounted for 40.11% of the United States air freight ancillary services market share in 2025, making it the largest regional base for ancillary revenue. This position reflects the region's long-standing role in transpacific trade, its dense fulfillment activity, and the concentration of technology and retail cargo that require frequent consolidation and handling support. The West also benefits from the fact that large import gateways continue to attract operators that can combine air freight with customs coordination, warehousing, and inland distribution.

The Southeast is forecast to grow at 8.11% CAGR through 2031, making it the fastest-growing region in the United States air freight ancillary services market. The region benefits from pharmaceutical logistics activity, strong access to Latin American trade, and broader cross-modal links that support urgent air cargo with trucking and warehousing support. That combination increases demand for temperature-controlled handoffs, compliance documentation, and customs-heavy execution, rather than just basic freight uplift.

The Northeast remains important because its pharmaceutical and biotechnology corridor supports high-value cargo that requires strict handling controls and reliable airport processing. The Southwest is gaining relevance as nearshoring deepens and cross-border production networks create greater demand for customs brokerage, staging, and time-definite transfers. At the same time, the Cargo Airline Association's May 2026 warning on potential CBP staffing actions at Newark, Los Angeles, Chicago, and San Francisco shows that gateway performance remains a real risk across multiple regions. That means regional growth in the United States air freight ancillary services market will depend not only on cargo demand but also on whether airports and border processing nodes can sustain consistent throughput for high-touch shipments.

Competitive Landscape

The United States air freight ancillary services market is moderately consolidated at the top and fragmented across the middle and lower tiers. Large global integrators and major freight forwarders hold a structural advantage because they can spread compliance costs across larger volumes, invest in certified facilities, and support customers across more trade lanes. Smaller operators remain active, but they are more exposed when customers ask for temperature control, customs support, digital tracking, and unified billing within the same shipment program. This is why scale is becoming a stronger competitive filter in the United States air freight ancillary services market, even though fragmentation remains visible across specialist providers. The result is a market where a few large operators shape standards, while many smaller participants compete in selected verticals or corridor-specific roles.

Recent strategy moves show how leading players are trying to deepen control rather than rely only on transactional forwarding. AIT Worldwide Logistics announced a strategic partnership with Greenbriar Equity Group in February 2026 to support expansion through organic growth and acquisitions, which signals that capital scale remains important in this market. Kuehne+Nagel added Frankfurt to its Inspire aircraft rotation in June 2026, creating a weekly Chicago-Frankfurt-Atlanta routing under long-term charter to support pharmaceuticals, aerospace, semiconductors, and other high-value flows. UPS also expanded its Mexico-facing air freight service in 2026, adding integrated brokerage and warehousing, indicating that cross-border depth is becoming part of competitive positioning rather than a separate support function. GEODIS's Chicago healthcare cross-dock is another example of targeted specialization, where facility design itself becomes part of the value proposition for shippers with sensitive cargo.

Digital capability is another clear line of competition in the United States air freight ancillary services market. IATA's data standard work is raising the baseline for shipment information exchange, making visibility tools increasingly central to service quality over time. SEKO Logistics expanded its Freightos partnership in July 2025 to unify air and ground rate management and booking across its worldwide operations, which shows how mid-market providers are standardizing digital execution to stay relevant. FedEx's June 2026 agreement with China Southern Air Logistics also included digitalization within the scope of cooperation, indicating that major network players are pairing capacity coordination with digital process alignment[4]Source: Federal Express Corporation, “FedEx and China Southern Air Logistics Sign Memorandum of Understanding on Strategic Cooperation,” FedEx Newsroom, newsroom.fedex.com. In practical terms, the strongest competitors are those that combine network reach, certified compliance capabilities, and better data control without creating extra handoffs for the customer.

United States Air Freight Ancillary Services Industry Leaders

Expeditors International of Washington, Inc.

C.H. Robinson Worldwide, Inc.

UPS

FedEx

AIT Worldwide Logistics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: FedEx Corporation signed a Strategic Memorandum of Understanding with China Southern Air Logistics, formally establishing a strategic relationship covering capacity sharing, route coordination, hub connections, network planning, fleet resources, ground operations, and digitalization.

- June 2026: Kuehne+Nagel added Frankfurt Airport to its Inspire aircraft rotation, creating a weekly Chicago-Frankfurt-Atlanta routing operated by Atlas Air under long-term charter. The service targets shipments of pharmaceuticals, aerospace, high-tech, semiconductors, and cloud infrastructure, strengthening transatlantic ancillary connectivity for high-value United States trade flows.

- February 2026: AIT Worldwide Logistics entered a definitive agreement to partner with Greenbriar Equity Group, L.P., in a transaction described as one of the largest private acquisitions in global freight forwarding. Greenbriar brings more than USD 15 billion in cumulative capital commitments and over 25 years of experience in transportation and logistics investment.

- December 2025: GEODIS signed a strategic interline agreement with Atlas Air and MAS (Martinair Cargo/AV) to expand its air freight network across South America, strengthening connections in Colombia, Brazil, Panama, Chile, and Costa Rica. The agreement provides GEODIS with direct air connections from the Asia-Pacific region, including Hong Kong, via Mexico, with freight demand from Central and South America reported to have grown 30% in the preceding period.

United States Air Freight Ancillary Services Market Report Scope

| Cargo Handling Services |

| Cargo Consolidation Services |

| Packaging and Labeling Services |

| Cargo Insurance Services |

| Temperature-Controlled (Cold Chain) Services |

| Other Services |

| Domestic Shipments |

| International Shipments |

| Aerospace and Defense |

| Consumer Electronics |

| Automotive and Industrial Manufacturing |

| E-commerce and Retail |

| Healthcare and Technology |

| Food and Beverage (Perishables) |

| Chemicals and Hazardous Materials |

| Fashion and Luxury Goods |

| Others |

| Northeast |

| Southeast |

| Midwest |

| Southwest |

| West |

| By Service Type | Cargo Handling Services |

| Cargo Consolidation Services | |

| Packaging and Labeling Services | |

| Cargo Insurance Services | |

| Temperature-Controlled (Cold Chain) Services | |

| Other Services | |

| By Shipment Type | Domestic Shipments |

| International Shipments | |

| By Industry Vertical | Aerospace and Defense |

| Consumer Electronics | |

| Automotive and Industrial Manufacturing | |

| E-commerce and Retail | |

| Healthcare and Technology | |

| Food and Beverage (Perishables) | |

| Chemicals and Hazardous Materials | |

| Fashion and Luxury Goods | |

| Others | |

| By Region | Northeast |

| Southeast | |

| Midwest | |

| Southwest | |

| West |

Key Questions Answered in the Report

What is driving growth in the United States air freight ancillary services through 2031?

Growth is being supported by pharmaceutical cold-chain requirements, integrated door-to-door logistics demand, nearshoring-linked United States-Mexico cargo shifts, and stronger demand for shipment visibility and compliance support.

How large is this business expected to become by 2031?

The United States air freight ancillary services market is projected to reach USD 43.69 billion by 2031 from USD 31.38 billion in 2026, at a 6.84% CAGR over 2026-2031.

Which service type leads revenue today?

Temperature-controlled services lead with 45.02% share in 2025 and also post the fastest service-type growth at 8.21% CAGR through 2031.

Why are international shipments more valuable for ancillary providers?

International shipments held a 48.27% share in 2025 and bring greater ancillary depth, as they require customs brokerage, labeling, insurance, documentation, and broader compliance support.

Which customer group is growing fastest?

Healthcare and technology are growing at the fastest 10.15% CAGR through 2031 because these shipments require tighter temperature control, chain-of-custody discipline, and real-time visibility.

Which United States region is strongest for future expansion?

The West remained the largest region with a 40.11% share in 2025, while the Southeast is the fastest-growing region at an 8.11% CAGR through 2031, driven by pharmaceutical and nearshoring-related cargo activity.

Page last updated on: