Germany Defense Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.61 Billion |

| Market Size (2026) | USD 4.86 Billion |

| Market Size (2031) | USD 6.27 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Defense Logistics Market Analysis by Mordor Intelligence

The Germany defense logistics market size is projected to expand from USD 4.61 billion in 2025 and USD 4.86 billion in 2026 to USD 6.27 billion by 2031, registering a CAGR of 5.21% between 2026 to 2031.

The Germany defense logistics market is moving away from lean peacetime inventory planning and toward a readiness model built on faster deployment, deeper stock positions, and more reliable in-theater support. Germany’s 2026 defense allocation reached EUR 108.2 billion (USD 125.4 billion), including EUR 25.5 billion (USD 29.6 billion) from the Sondervermogen Bundeswehr special fund, which provides logistics operators with a firmer demand base across transport, support, and sustainment activities. Germany’s latest OPLAN DEU also reinforces this shift by positioning the country as the main staging hub for allied troops and vehicles in a crisis, which raises long-run requirements for throughput capacity, depot support, and multimodal movement planning. The Germany defense logistics market is also being shaped by faster procurement, digital integration in depots, and a wider use of performance-based support models, while competitive pressure is rising as OEMs, government-linked operators, and major freight groups all move into overlapping service areas. At the same time, capacity bottlenecks in maintenance facilities, strict defense cloud onboarding rules, and long approval cycles for storage infrastructure continue to slow the pace at which the Germany defense logistics market can absorb new demand.

Key Report Takeaways

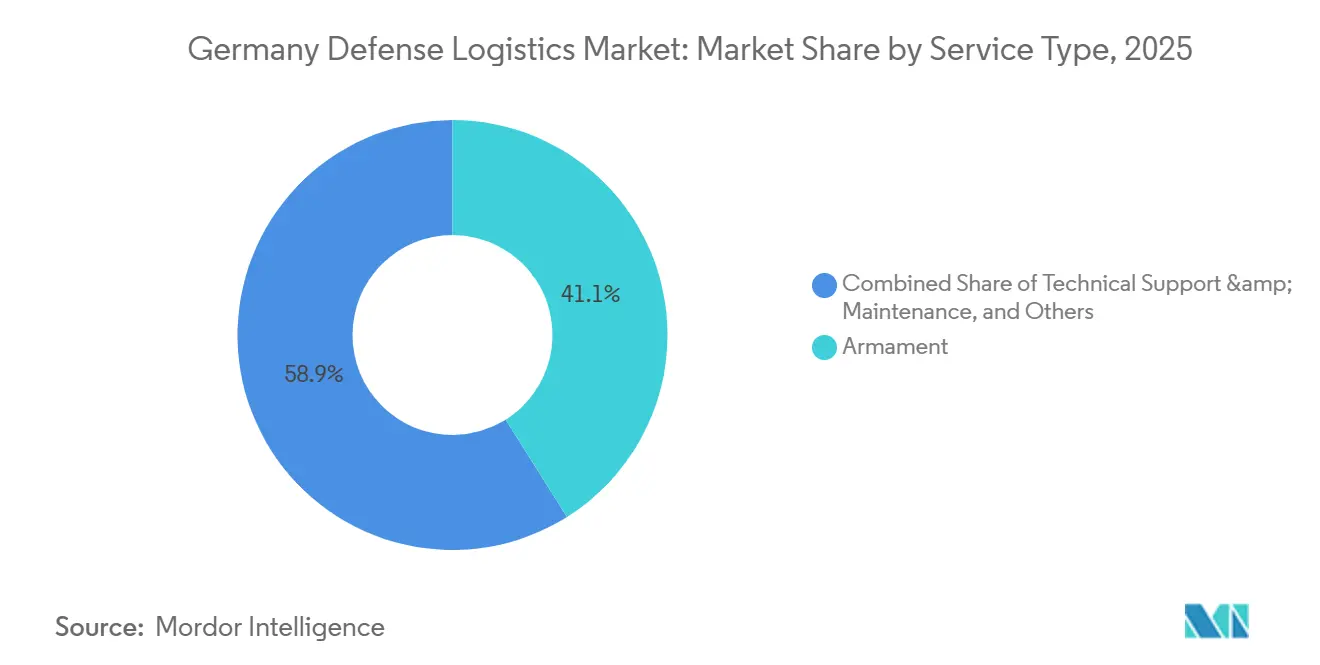

- By service type, armament led with 41.07% of the Germany defense logistics market share in 2025, while technical support and maintenance are projected to expand at an 8.05% CAGR through 2031.

- By logistics function, transportation accounted for 56.93% of the Germany defense logistics market size in 2025, while value-added services are forecast to grow at 7.22% CAGR through 2031.

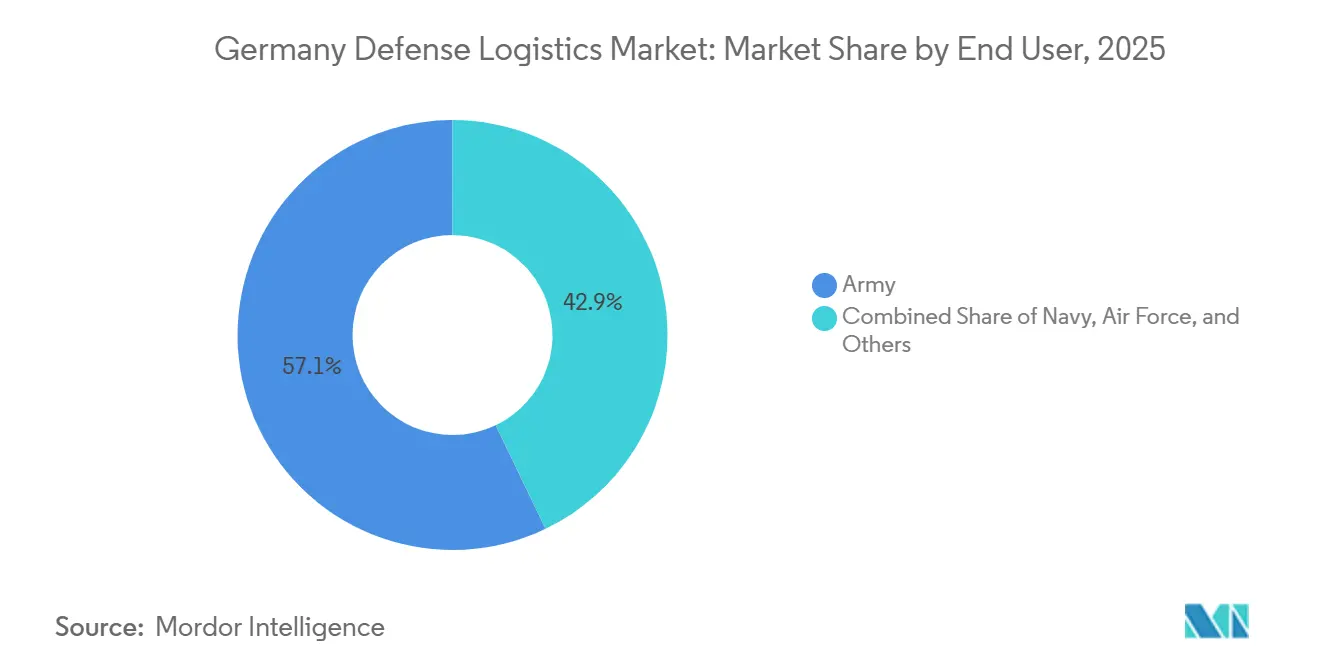

- By end user, the army accounted for 57.12% of market demand in 2025, while the air force is projected to record the highest CAGR of 8.35% through 2031.

- By region, North Rhine-Westphalia captured 34.84% of regional revenue in 2025, while Baden-Wurttemberg is expected to advance at a 6.59% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Defense Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bundeswehr Special Fund Accelerates Multi-Modal Logistics Modernization | +2.0% | National, concentrated in North Rhine-Westphalia, Bavaria, and Baden-Württemberg. | Short term (≤ 2 years) |

| NATO Deterrence Requirements Raise Rapid-Deployment Stockpiles Along the Rhine Corridor | +0.8% | North Rhine-Westphalia, Rhineland-Palatinate, North Germany | Medium term (2-4 years) |

| Digital Twin Rollout for Military Depots Improves Inventory Lead Times | +0.6% | National, with depot concentration in North Rhine-Westphalia and Saxony | Medium term (2-4 years) |

| Civil and Military Logistics Integration with DB Cargo Expands Rail Capacity | +0.5% | National, with key nodes in North Rhine-Westphalia and Baden-Württemberg | Short term (≤ 2 years) |

| Hydrogen Tactical Vehicle Pilots Create New Fuel-Chain Service Needs | +0.2% | Bavaria and Baden-Württemberg | Long term (≥ 4 years) |

| EU Military Mobility Funding Supports Cross-Border Corridor Upgrades | +0.4% | National, with spillover to the Netherlands and Poland corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Bundeswehr's EUR 100 Billion (USD 116.0 billion) Sondervermogen Accelerates Multi-Modal Logistics Modernization.

Germany’s defense budget structure now works through both the regular budget and the special fund, which has materially increased the scale and visibility of logistics demand in Germany's defense logistics market. The combined 2026 defense budget of EUR 108.2 billion (USD 125.4 billion), including EUR 25.5 billion (USD 29.6 billion) from the Sondervermogen fund, is the clearest sign that logistics planning is now tied to sustained military readiness rather than limited replacement cycles. One of the strongest signals came from the call-off for more than 2,000 RMMV HX military transport vehicles under the broader framework agreement, which sharply lifts Germany’s organic movement capacity for fuel, ammunition, and engineering equipment. The vehicle mix matters because the heavier variants support pre-positioning and force sustainment rather than just routine domestic movement. The Bundestag’s accelerated planning and procurement law, effective from January 2026, also reduces earlier bottlenecks in defense contracting, thereby supporting faster execution of logistics infrastructure, fleet support, and related services. As a result, the Germany defense logistics market is seeing a stronger pipeline of contracts that link procurement volumes directly to transport readiness, depot activity, and maintenance support.

NATO Deterrence Requirements Drive Rapid-Deployment Stockpiles Along the Rhine Corridor

Germany’s role inside NATO logistics has become more central as alliance planning increasingly depends on the country’s rail, road, port, and staging infrastructure. OPLAN DEU identifies Germany as the hub for moving up to 800,000 allied troops and 200,000 vehicles within 6 months of crisis activation, thereby lifting baseline demand for stockpiling, convoy support, and transit coordination in the German defense logistics market. This demand is not limited to state-owned capacity because commercial contracts alone cannot absorb a surge of that scale without added integration across service providers and military planners. Rheinmetall’s February 2025 framework agreement for force redeployment support shows how broader logistics tasks, such as convoy services, housing, catering, refueling, and waste management, are increasingly being bundled into larger contracts[1]Rheinmetall AG, “Rheinmetall Wins Order for Logistical Support of the Armed Forces,” Rheinmetall, rheinmetall.com. That shift favors operators that can manage field support and movement services together rather than compete only as freight carriers. The Germany defense logistics market therefore benefits not only from higher military traffic volumes, but also from a wider transfer of operational responsibilities into integrated logistics contracts.

Digital-Twin Roll-Out for Military Depots Cuts Inventory Lead-Times

Digital modeling is becoming a practical planning tool in the Germany defense logistics market because the Bundeswehr now manages a much broader and more dynamic inventory burden than in earlier years. This matters because the Germany defense logistics market is no longer judged only by physical capacity, and contract performance increasingly depends on better visibility into parts availability, maintenance cycles, and depot throughput. IABG has also highlighted that configurable digital twin solutions are better suited to the Bundeswehr than rigid standard models because fleet structures and mission profiles vary widely across platforms[2]IABG, “Digital Twin,” IABG, iabg.de. That creates a clear divide between operators that can interface with defense data environments and those that still rely on basic transactional systems. Over time, the Germany defense logistics market is likely to reward interoperability, simulation capability, and digital traceability as strongly as it rewards warehouse space or vehicle fleets.

Civil–Military Logistics Integration with DB Cargo Unlocks Rail Capacity

Rail remains one of the most important support layers in the Germany defense logistics market because it connects military movement planning with the country’s civilian freight infrastructure. Germany’s Vorhaltevertrag Schine gives the Bundeswehr access to the national rail network for force-projection needs, preserving rail as a core mobility channel during large-scale deployments. The April 2025 sale of DB Schenker to DSV has introduced another structural change by concentrating a large share of commercial freight capacity within a single combined operator. This consolidation improves network reach and can support larger defense contracts that depend on dense rail and road links across Germany. It also raises concentration risk because a greater share of high-volume military movement work may flow through fewer commercial hands. In that setting, the Germany defense logistics market gains scale and coordination benefits from civil and military integration. Still, it also becomes more sensitive to capacity concentration among top-tier freight groups.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slower Puma IFV Retrofit Cycle Uses Warehouse and Workshop Capacity | -0.3% | North Rhine-Westphalia and Bavaria | Medium term (2-4 years) |

| Tight Defense Cybersecurity Rules Slow Third-Party Cloud Onboarding | -0.2% | National | Short term (≤ 2 years) |

| Skilled Logistics Personnel Shortage in Bundeswehr Civilian Corps | -0.3% | National, especially the eastern German states | Medium term (2-4 years) |

| Environmental Approval Delays for New Ammunition Storage Sites | -0.2% | Rhineland-Palatinate, Schleswig-Holstein, Lower Saxony | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Slower Puma IFV Retrofit Cycle Ties Up Warehouse Capacity

The Puma modernization cycle is constraining operational flexibility in the Germany defense logistics market because maintenance space and spare parts handling capacity remain tied up for long periods. The S1-standard upgrade of 297 Puma vehicles has a completion target of 2029, ensuring key depot and workshop resources remain committed while other land systems also require support. The upgrade scope includes missile integration, improved sensors, and digital radio equipment, and each layer adds testing and acceptance work that extends normal throughput times. The December 2025 agreement for 200 additional Puma vehicles also lengthens the period during which the most capable maintenance cells remain heavily focused on this platform. This creates a sequencing problem because fleet expansion and fleet support are rising simultaneously across the Army portion of the Germany defense logistics market. Commercial contractors can absorb part of that pressure, but current footprints limit how much overflow work can move out of the core network.

Tight MoD Cyber-Security Rules Delay Third-Party Cloud Onboarding

Digital modernization in the Germany defense logistics market is moving more slowly than planned because defense software has to comply with strict sovereignty and security requirements. The Bundeswehr’s pCloudBw architecture requires external applications to operate in an air-gapped environment, and the Google Cloud Air-Gapped integration is not expected to be completed until the end of 2027. Until that system is fully in place, many operators must run older and newer platforms together, which adds administrative work and slows the use of unified data in logistics planning. The delay matters because the Germany defense logistics market is increasingly dependent on live inventory views, predictive support tools, and secure information exchange across contractors and public agencies. Stringent certification rules also tend to favor incumbent providers that already understand classified system requirements and documentation routines. This leaves newer software vendors at a disadvantage and slows the pace at which the Germany defense logistics market can adopt AI-assisted forecasting and more integrated digital workflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Armament Dominates, Maintenance Services Accelerate

Armament accounted for 41.07% of revenue in 2025, making it the largest service segment in the German defense logistics market. This segment remains the core demand center because it covers munitions handling, weapons-related storage, specialized transport, procurement coordination, and documentation under strict military compliance rules. The January 2026 IRIS-T contracts signed by Diehl Defense and BAAINBw reinforce this pattern because missile production growth directly increases the need for secure warehousing, controlled handling, and tightly managed supply chains[3]Diehl Defense, “Contracts for IRIS-T Guided Missiles Signed with BAAINBw,” Diehl Defense, diehl.com.

Technical support and maintenance is the fastest-growing service area, and the segment is projected to expand at 8.05% CAGR from 2026 to 2031. Growth comes from larger fleets, longer sustainment cycles, and the steady spread of outsourced or performance-linked support models across land and air systems. Rolls-Royce Power Systems’ March 2026 contract for around 200 MTU Powerpacks for Puma vehicles shows how propulsion support is becoming a larger part of the aftermarket workload.

By Logistics Function: Transportation Commands Scale, Value-added Services Drive Margin

Transportation accounted for 56.93% of revenue in 2025, so it remains the largest functional block in the Germany defense logistics market size. Germany’s position as both a force contributor and a NATO transit hub keeps movement services at the center of logistics planning, especially for road and rail corridors that connect western depots to forward support routes. The Germany defense logistics market share held by transportation reflects not only the volume of shipments, but also the need for route coordination, convoy planning, and multimodal handoff across civilian and military networks.

Value-added services is the fastest-growing logistics function, and is set to rise at 7.22% CAGR through 2031. Demand is growing because military logistics now requires more digital kitting, labeling, codification, consulting, reverse logistics, and configuration control than a basic freight model can provide. These services become even more important when multinational procurement, electronic documentation, and interoperability standards are applied across multiple programs simultaneously. The Germany defense logistics industry is therefore seeing margin expansion in areas where operators can combine physical handling with systems knowledge and process support.

By End User: Army Anchors Demand, Air Force Surges

The Army represented 57.12% of the Germany defense logistics market share in 2025, which made it the largest consumer in the market. This position reflects the Army’s large vehicle fleet, heavy equipment needs, forward support structure, and broad reliance on transport, armament handling, and depot activities. Orders tied to logistics trucks and the ongoing Puma vehicle program create multi-year work across several functions simultaneously, including distribution, sustainment, and support services. Army demand is also more storage-intensive than other categories because it requires deeper spare parts pools, ammunition handling, and more dispersed readiness planning. For that reason, the Army remains the anchor customer group in the Germany defense logistics market even as growth is starting to accelerate in other services.

The Air Force is forecast to record the highest end-user CAGR at 8.35% through 2031, which makes it the most dynamic expansion area in the Germany defense logistics market. Simultaneous aircraft modernization, new propulsion support needs, and a rising volume of high-value component handling are driving the shift. The Germany defense logistics market also gains new complexity from naval aviation support, as Lufthansa Technik Defense is already performing maintenance work for the German Navy’s P-8A Poseidon fleet in Hambur. Air domain growth raises the need for tightly controlled spares flows, engine support, avionics handling, and specialized maintenance planning that differs sharply from land-system logistics. That is why the Germany defense logistics market is becoming more balanced over time, with the Army still dominant in scale and the Air Force contributing the fastest pace of new demand.

Geography Analysis

North Rhine-Westphalia held 34.84% of regional revenue in 2025, so it remained the largest geography in the Germany defense logistics market. The state benefits from a dense mix of military support infrastructure, strong commercial logistics networks, and direct access to the Rhine corridor that underpins domestic and allied movement planning. Its role is strengthened further by Germany’s staging function under OPLAN DEU, which pulls transport coordination, stock positioning, and transit services toward the country’s western logistics spine. This makes North Rhine-Westphalia the most immediate beneficiary when the Germany defense logistics market expands through force movement, redeployment support, or multimodal throughput upgrades. The region also provides a practical base for combined civil and military contracting because major freight networks already intersect with defense movement routes.

Baden-Wurttemberg is the fastest-growing regional segment and is expected to grow at a 6.59% CAGR through 2031, reflecting expanding activity in sensors, electronics, and missile-related production. Diehl Defense also opened a new missile integration center in Nonnweiler in January 2026 as part of a wider expansion program, strengthening the regional support chain for armament logistics and related storage and handling services. These developments keep southern Germany central to the growth profile of the Germany defense logistics market.

The rest of Germany is gaining relevance as infrastructure reactivation broadens the national support network beyond the traditional western and southern triangle. Schleswig-Holstein, Lower Saxony, Rhineland-Palatinate, Saxony, and several eastern states are becoming more important as storage, support, and resilience capacity is spread more widely across the country. This shift matters because the Germany defense logistics market needs redundancy as well as scale, especially when depot activation, stockpiling, and surge support must operate at the same time. Regional growth outside the core hubs is therefore less about displacing North Rhine-Westphalia or Bavaria and more about reducing concentration risk across the national network. Over the forecast period, that wider geographic spread should make the Germany defense logistics market more resilient to throughput bottlenecks, maintenance congestion, and site-specific approval delays.

Competitive Landscape

The Germany defense logistics market is moderately concentrated at the top tier, with a mix of OEM-led support providers, government-linked maintenance operators, and large commercial freight companies competing across adjacent service spaces. Rheinmetall is expanding beyond its traditional manufacturing role and is positioning itself as an integrated logistics partner through redeployment support, vehicle supply, and unmanned systems-related activity. The February 2025 Bundeswehr framework agreement for redeployment logistics support is a clear example because it covers housing, catering, refueling, waste management, and convoy support under a single contract structure. Government-owned HIL also remains central in land-system sustainment, while commercial groups such as DHL, Kuehne+Nagel, and DSV compete in larger freight-heavy portions of the Germany defense logistics market. This creates a competitive landscape where no single operator dominates every function, but scale and integration are becoming increasingly important for winning higher-value work.

The DSV acquisition of DB Schenker, completed in April 2025, is one of the most important structural changes in the Germany defense logistics market because it combines extensive network density with strong multimodal reach. That matters for Bundeswehr frameworks where rail access, domestic coverage, and contract execution scale are decisive. A second strategic move came in March 2026, when Rheinmetall partnered with Boeing Australia on the MQ-28 Ghost Bat program, demonstrating how OEMs are increasingly bundling integration, maintenance, and logistics support within broader system offers. A third example is HENSOLDT’s continued expansion in armored vehicle optronics and other electronics support chains, which strengthens the position of specialized suppliers in segments that general freight firms cannot easily serve[4]HENSOLDT AG, “HENSOLDT Receives Major Order for Digital Armored Vehicle Optronics,” HENSOLDT, hensoldt.net. Together, these moves show that competition in the Germany defense logistics market is increasingly shaped by system knowledge and program access, not only by transport scale.

Strategy is now splitting between full-service defense integrators and focused providers with niche technical capability. Full-service players aim to control a greater share of the contract scope, from transport and warehousing to field support and sustainment planning. Niche players instead compete where standards compliance, secure handling, or platform-specific expertise matters more than broad network reach. This is especially visible in parts of the Germany defense logistics market tied to missiles, sensors, propulsion, and aircraft support, where entry barriers are higher and customer switching is slower. The result is a market where scale helps secure large frameworks, but specialization still protects margins in tightly regulated service lines. Competitive pressure in the Germany defense logistics market is therefore rising, though it remains balanced enough to support both large national operators and targeted technical support providers.

Germany Defense Logistics Industry Leaders

Rheinmetall AG

HIL Heeresinstandsetzungslogistik GmbH

DHL Group

Kuehne+Nagel

DSV (incl. DB Schenker)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Rheinmetall received a multi-billion EUR framework contract from the Bundeswehr for FV-014 loitering munition, autonomous reconnaissance and strike drones, with the first call-off valued at EUR 300 million (USD 348.0 million) gross. Qualification is underway in 2026 with deliveries from the first half of 2027.

- March 2026: Rheinmetall and Boeing Australia entered a strategic partnership to offer the MQ-28 Ghost Bat collaborative combat aircraft to the Bundeswehr, targeting deployment by 2029. Rheinmetall will serve as German system manager, overseeing integration, maintenance, and logistical support, directly extending its defense logistics portfolio into unmanned combat systems.

- February 2026: Diehl Defense and BAAINBw signed multiple contracts for the IRIS-T family of guided missiles, including air-to-air IRIS-T and ground-based IRIS-T SLM and SLS variants, as part of a delivery framework that extends through 2030. Diehl is investing EUR 1.5 billion (USD 1.74 billion) company-wide in production expansion across all German facilities.

- November 2025: Boeing and Lufthansa Technik Defense signed a multi-year Performance-Based Logistics contract covering MRO services, aircraft maintenance, engine support, component supply, operations management, and technical training for the German Navy's fleet of 8 P-8A Poseidon maritime patrol aircraft. This is the first weapon-bearing aircraft system in Lufthansa Technik Defense's military MRO portfolio.

Germany Defense Logistics Market Report Scope

| Armament |

| Military Troops Movement Support |

| Technical Support & Maintenance |

| Medical Aid & Health Services |

| Fire-fighting Protection |

| Other Services |

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing & Distribution | |

| Value-added Services (Labelling, Kitting, Consulting) |

| Army |

| Navy |

| Air Force |

| Others |

| North Rhine-Westphalia |

| Bavaria (Bayern) |

| Baden-Wurttemberg |

| Rest of States |

| By Service Type | Armament | |

| Military Troops Movement Support | ||

| Technical Support & Maintenance | ||

| Medical Aid & Health Services | ||

| Fire-fighting Protection | ||

| Other Services | ||

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing & Distribution | ||

| Value-added Services (Labelling, Kitting, Consulting) | ||

| By End User | Army | |

| Navy | ||

| Air Force | ||

| Others | ||

| By Region | North Rhine-Westphalia | |

| Bavaria (Bayern) | ||

| Baden-Wurttemberg | ||

| Rest of States | ||

Key Questions Answered in the Report

What is the 2031 value forecast for Germany defense logistics?

The Germany defense logistics market is forecast to reach USD 6.27 billion by 2031, up from USD 4.86 billion in 2026, at a 5.21% CAGR from 2026 to 2031.

Which service area leads revenue in Germany defense logistics?

Armament is the largest service segment, accounting for 41.07% of revenue in 2025, supported by munitions handling, secure transport, and weapons-related supply chain activities.

Which logistics function is growing fastest in Germany?

Value-added services are the fastest-growing logistics function, with a projected 7.22% CAGR through 2031, driven by digital kitting, codification, and configuration support needs.

Why is North Rhine-Westphalia so important for defense logistics in Germany?

North Rhine-Westphalia accounted for 34.84% of regional revenue in 2025, thanks to its military support infrastructure and dense commercial transport links along the Rhine corridor.

Which end user is expanding fastest in this sector?

The Air Force is the fastest-growing end user, with an 8.35% CAGR through 2031, reflecting higher demand for aircraft spares, engine support, and technical maintenance logistics.

What are the main constraints slowing adoption and capacity growth?

The biggest limits are Puma retrofit-related workshop congestion, strict cloud and cybersecurity requirements, staffing gaps in logistics, and slow environmental approvals for new storage facilities.

Page last updated on: