Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

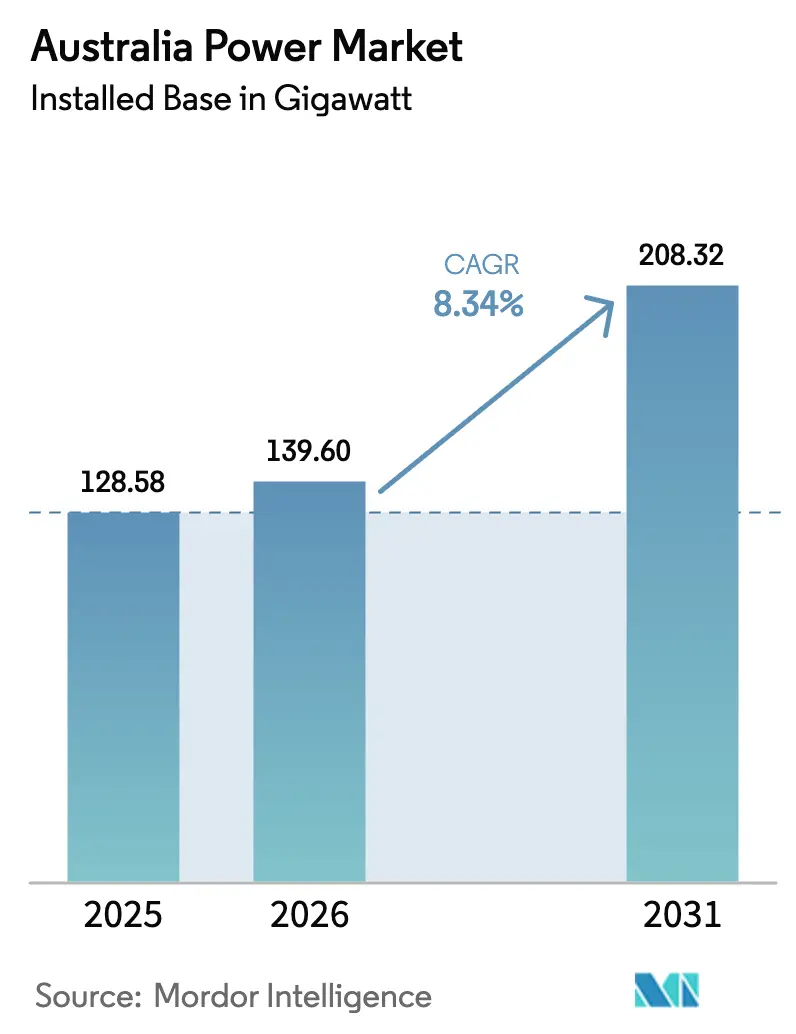

| Base Year Market Size (2025) | 128.58 gigawatt |

| Market Volume (2026) | 139.60 gigawatt |

| Market Volume (2031) | 208.32 gigawatt |

| Growth Rate (2026 - 2031) | 8.34% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Power Market Analysis by Mordor Intelligence

The Australia Power Market size in terms of installed base is expected to increase from 128.58 gigawatt in 2025 to 139.60 gigawatt in 2026 and reach 208.32 gigawatt by 2031, growing at a CAGR of 8.34% over 2026-2031.

Rapid utility-scale solar and wind additions, paired with 4-hour batteries tendered under the Capacity Investment Scheme, underpin the expansion while coal retires on an accelerated schedule. Corporate power-purchase agreements from miners and data-center operators are now underwriting more contracted capacity each year than the Large-scale Renewable Energy Target, shifting demand anchors toward industrial electrification. Transmission investment led by the AUD 20 billion Rewiring the Nation program supports renewable energy zones, although cost inflation of 25-55% for overhead lines threatens to exhaust funding before later-stage links reach financial close. Growing negative wholesale price intervals, especially the 40% share of spring 2024 midday trading periods in South Australia, create arbitrage room for batteries while eroding merchant revenues for solar and wind. Integrated generators are replacing coal baseload with grid-scale batteries and hydrogen-ready peakers to preserve market share and capture dispatchable margins.

Key Report Takeaways

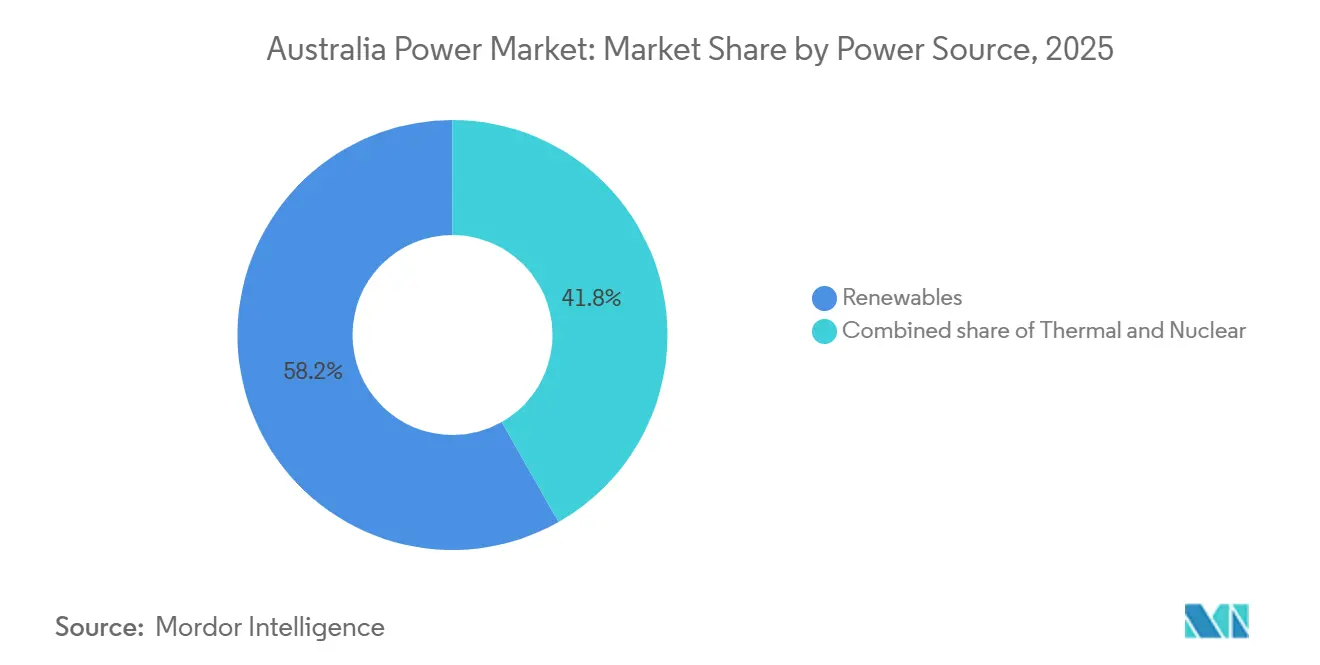

- By power source, renewables held a 58.2% share of the Australian power market size in 2025 and are forecast to expand at a 13.9% CAGR through 2031.

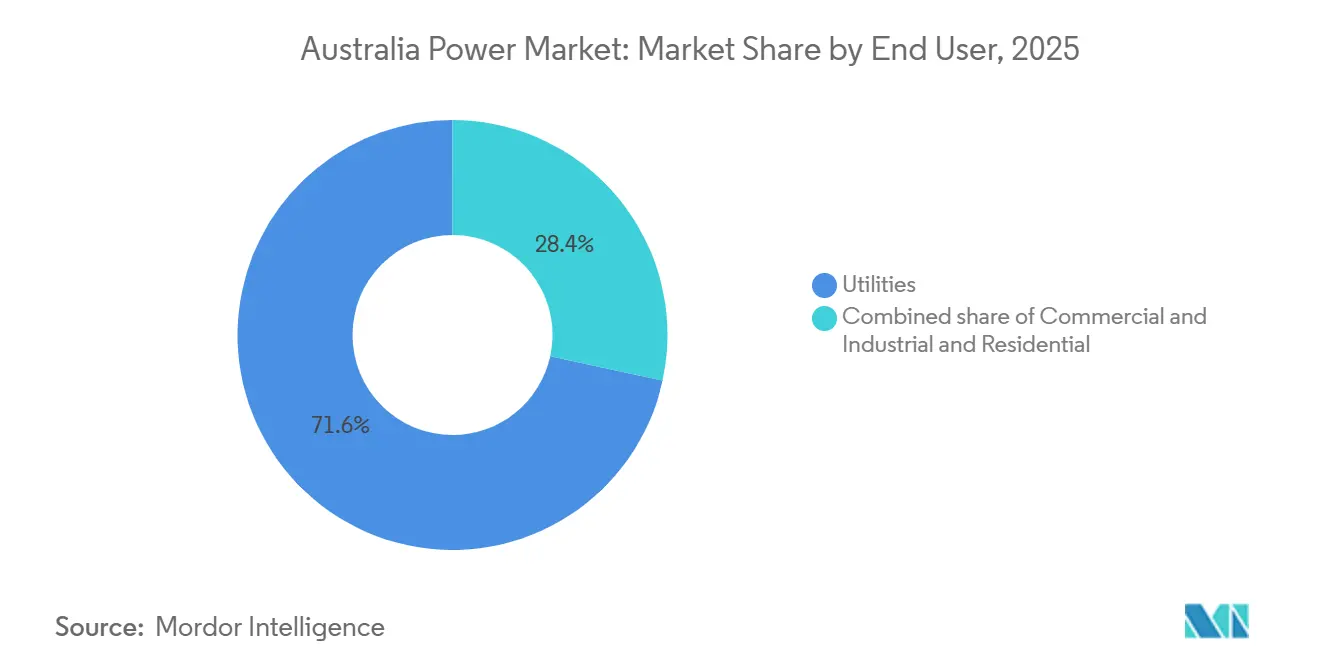

- By end user, utilities controlled 71.6% of Australia's power market share in 2025, yet the residential segment records the fastest growth at a 10.0% CAGR to 2031 as rooftop solar and home batteries proliferate.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Utility-scale Solar PV Deployment under Large-scale Renewable Energy Target | +2.1% | NSW Central-West Orana, QLD Darling Downs, VIC Murray River zones | Medium term (2-4 years) |

| Surge in Corporate PPAs from Mining & Data-Center Operators | +1.4% | WA Pilbara and Goldfields, spillover to QLD coal regions | Medium term (2-4 years) |

| Grid-scale Battery & Pumped-Hydro Investments Accelerated by CIS | +1.8% | NEM states NSW, VIC, QLD, SA | Short term (≤ 2 years) |

| Federal “Rewiring the Nation” Transmission Funding | +1.3% | Priority corridors NSW-VIC, TAS-VIC | Long term (≥ 4 years) |

| Hydrogen-ready Gas-Turbine Projects | +0.7% | NSW Hunter Valley, VIC Latrobe Valley, SA Port Augusta | Medium term (2-4 years) |

| Electrification of Homes & EV Uptake | +1.0% | Eastern states urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Utility-scale Solar PV Deployment under Large-scale Renewable Energy Target (LRET)

The LRET achieved its 33,000 GWh target in 2024, yet certificate oversupply pushed prices down to AUD 25-35/MWh, prompting developers to secure 10-15 year corporate PPAs for revenue certainty.[1]Clean Energy Regulator, “Large-scale Generation Certificates Quarterly Report Q4 2025,” cleanenergyregulator.gov.au Snowy Hydro’s 1,200 MW New South Wales solar portfolio illustrates integrated gentailer hedging that combines generation with retail load. Lightsource bp and ACEN Australia both closed 400 MW solar farms in 2025 after locking in industrial off-takers, a model now standard as wholesale price volatility rises. Eku Energy’s 1,000 MW Riverland Solar project includes co-located storage to monetize energy otherwise curtailed in high-congestion zones. Falling cost curves for bifacial modules and single-axis trackers sustain sub-AUD 50/MWh levelized costs, enabling solar to out-compete new thermal projects without subsidies.

Surge in Corporate PPAs from Mining & Data-Center Operators in Western Australia

BHP’s 100% renewable PPA covering Queensland coal operations from 2027 removes more than 1,000 GWh of annual grid demand and signals board-level alignment on climate targets.[2]BHP Group, “Climate Transition Action Plan 2025,” bhp.com Fortescue is building a 2-3 GW solar-wind-battery pipeline that will commission 500-700 MW each year to reach complete Scope 1 and 2 decarbonization by 2030. Western Australia’s isolated grid expedites renewable penetration because the state solves inertia and firming challenges locally, accelerating battery roll-outs. Hyperscale data-center operators, led by Microsoft and Equinix, signed 24/7 renewable contracts totaling 526 MW in 2025, reflecting AI-driven compute demand that requires continuous power quality. ACCC’s 2025 inquiry found corporate PPA strike prices AUD 10-20/MWh below wholesale averages when contract terms exceed 15 years, transferring volume risk to developers.[3]Australian Competition and Consumer Commission, “Inquiry into Corporate PPA Pricing Transparency 2025,” accc.gov.au

Federal “Rewiring The Nation” Funding For Super-Grid Transmission To Renewable Energy Zones

The AUD 20 billion Rewiring the Nation program has allocated AUD 3.5 billion so far, concentrating on the 360 km HumeLink 500 kV interconnector that will move Snowy Hydro output toward Sydney load centers. Cost inflation of 25-55% for overhead lines and 10-35% for substations relative to the 2024 Integrated System Plan baseline threatens to consume the fund before later-stage links, such as the AUD 7.6 billion VNI West and the Western Renewables Link, secure finance. TransGrid’s AUD 15 billion transmission pipeline for 2024-2034, which includes Central-West Orana renewable energy zone upgrades, is running about two years late on average across 11 projects, prolonging renewable curtailment while waiting for new circuits. Powerlink Queensland’s CopperString 2.0 line obtained AUD 5 billion in combined state and federal funding in 2025, opening North Queensland renewable resources to the National Electricity Market and underpinning new mining electrification demand. Australian Energy Regulator revenue rulings for 2024-2029 granted networks a 5.5-6.0% weighted average cost of capital, below the 6.5-7.0% they sought, signaling that additional concessional loans may be needed to close financing gaps for super-grid corridors.

Grid-scale Battery & Pumped-Hydro Investments Accelerated by Capacity Investment Scheme (CIS)

CIS Tender 3 awarded 4.13 GW of batteries and 15.37 GWh of storage across 16 projects, led by Origin’s 700 MW / 2.8 GWh Eraring unit that became the world’s largest battery in December 2025. Neoen’s 900 MW Collie Battery under construction for 2026 will anchor Western Australia’s coal exit despite its limited multi-day duration. AGL’s 250 MW Torrens Island battery, co-located with a gas plant, cut interconnection costs by 15-20%, illustrating brownfield advantages. Snowy 2.0’s 2,200 MW pumped-hydro slips to 2028-2029 but will offer 175 hours of discharge, tackling long-duration gaps that 4-hour lithium-ion systems cannot fill. AEMO analysis indicates grid-forming inverters add 15-20% capex but supply synthetic inertia comparable to synchronous condensers, supporting system security in a coal-free grid.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transmission bottlenecks causing curtailment in Queensland & New South Wales REZs | −0.9% | Queensland, New South Wales REZs | Short term (≤2 years) |

| Community opposition delaying wind farms & HV interconnector routes | −0.6% | Victoria, New South Wales, Tasmania | Medium term (2-4 years) |

| Rising natural-gas feedstock prices eroding peaker competitiveness | −0.6% | National, acute in South Australia, Victoria | Short term (≤2 years) |

| Policy uncertainty around 2030 coal-exit pathways deterring capital allocation | −1.1% | National, divergent signals across states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Transmission Bottlenecks Causing Curtailment in Queensland & NSW REZs

New South Wales produced 66% of the National Electricity Market congestion in 2024 as 7.15 GW of generation access was granted before network upgrades, forcing curtailment during high solar output. Molong Solar Farm recorded a 53.8% curtailment rate, highlighting the mismatch between 12-18 month generation builds and 3-5 year transmission timelines. Curtailment reached 33% in NSW and 27% in Victoria during spring 2024 when mild demand collided with peak renewable production. AEMO projects that 2-4 year delays could waste 214-456 TWh of renewable energy by 2040, costing up to AUD 20 billion. HumeLink, now targeting 2028-2029 after landholder disputes, extends congestion for southern NSW projects, prompting developers to add onsite batteries to time-shift output.[4]TransGrid, “HumeLink Project Update September 2025,” transgrid.com.au

Community Opposition Delaying Wind Farms & HV Interconnector Routes

VNI West’s 190 km route through Victoria’s Western District faces organized resistance over visual and land-use impacts, extending environmental approvals by 18 months. Western Renewables Link has slipped by 6 years as councils demand underground cabling that would triple project costs under current regulatory settings. HumeLink encountered disputes with 70 landholders, forcing compulsory acquisitions and legal challenges that added 12-18 months to schedules. The Clean Energy Council introduced a voluntary developer rating scheme in 2024, yet limited enforcement constrains its ability to resolve local opposition. AER’s 2025 cost review shows community conflict now adds 25-55% to overhead line budgets, making social licence costs comparable with commodity inflation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Source: Renewables Capture 58% Share as Coal Retirements Accelerate

Renewables held 58.2% of Australia's power market share in 2025 and are expanding at a 13.9% CAGR, adding 3-4 GW of solar and 1-2 GW of wind annually, while grid-scale batteries reach 4 GW under CIS awards. Solar PV dominates additions through Snowy Hydro's 1,200 MW portfolio and Lightsource bp's 400 MW Riverina project, both secured by long-term corporate PPAs. Wind growth concentrates in Neoen's 460 MW Goyder South Stage 2, CleanCo's 1,026 MW MacIntyre precinct, and the proposed 2,200 MW Star of the South offshore wind farm, which will broaden resource diversity if port bottlenecks are resolved. Hydro remains steady near 8 GW, with Snowy 2.0's 2,200 MW pumped-hydro and Tasmania's Battery of the Nation representing the few large additions. Gas peakers such as Kurri Kurri and Tallawarra B supply flexibility but face fuel prices averaging AUD 10-14/GJ in 2024-2025, lowering dispatchability economics compared with batteries charging at negative midday prices.

Long-term emission policies continue to tilt investment toward zero-carbon technologies, yet firming requirements compel hybridization. The Australian power market size allocated to batteries is forecast to rise from 5 GW in 2026 to 27 GW by 2050, while coal capacity retires in 1-2 GW chunks as Eraring, Yallourn, and Collie exit. Hybrid solar-battery complexes like EkEnergy's Silverland project are becoming standard to manage curtailment and capture frequency control revenues. Offshore wind may add up to 10 GW post-2033, diversifying the generation mix once supply chain and transmission hurdles clear. Biomass, geothermal, and tidal remain below 1% of capacity due to limited resources and higher costs. Nuclear remains prohibited, and even if policy shifts, small modular reactors would not arrive before the late 2030s.

By End User: Utilities Dominate but Residential Segment Grows Fastest

Utilities commanded 71.6% of Australia's power market size in 2025 by virtue of owning large-scale generation and retail portfolios, with AGL, Origin, and EnergyAustralia capturing 70% of residential and small business customers. Integrated generators hedge positions by adding 500-700 MW batteries at retired coal sites to protect dispatchable market share. The residential segment expands at a 10.0% CAGR as rooftop solar climbs from 25 GW in 2025 toward 87 GW by 2050, supported by 1.4 GW home batteries that participate in virtual power plants targeting 1,000 MW by 2030. Commercial and industrial users deploy behind-the-meter assets through energy-as-a-service contracts from Zen Energy and Flow Power, lowering bills by 10-15% while avoiding capex outlay.

Mining companies are now significant self-generators; Fortescue’s 2-3 GW pipeline and BHP Nickel West’s solar-battery microgrid show how on-site renewables hedge against carbon and fuel price risk. Data centers drove 526 MW of new contracted load in 2025, a figure expected to triple by 2030 if AI workload forecasts hold. Utilities respond by aggregating distributed resources into VPPs that provide frequency response and wholesale demand reduction, blending centralized and distributed assets. AEMO’s Wholesale Demand Response Mechanism, with 200 MW enrolled, lets large cold-storage and manufacturing plants monetize flexibility in place of generation, reinforcing end-use diversification.

Geography Analysis

New South Wales hosts the largest slice of Australia's power market size at 35% in 2025 on the back of its legacy coal fleet and 7.15 GW renewable access rights, yet faces the highest curtailment until HumeLink and VNI West enter service. Victoria follows with a 24% share, leveraging abundant onshore wind and the planned 2,200 MW Star of the South offshore project that could supply 9% of the National Electricity Market generation by 2050 once built. Queensland commands 23% capacity and leads rooftop solar uptake, while the CopperString 2.0 transmission line connecting North Queensland resources to the NEM unlocks additional utility-scale solar and wind.

South Australia exemplifies high renewable penetration, sourcing 70% daytime demand from rooftop solar in 2024 and registering negative prices in 40% of spring midday intervals, encouraging 4-hour batteries and synchronous condensers to stabilize frequency. Western Australia operates an isolated grid where Synergy's coal retirement schedule and Neoen's 900 MW Collie Battery set a roadmap for rapid decarbonization. Tasmania, already hydro-dominant, positions as a battery of the nation through the Marinus Link and new pumped-hydro arrays, exporting firmed renewable power to mainland states.

Regional renewable energy zones concentrate investment: Central-West Orana in NSW, Darling Downs in Queensland, and Murray River in Victoria each award multi-GW access. However, transmission lags by 2-4 years, causing curtailment until super-grid corridors reach commissioning. Offshore wind areas off Gippsland and the Hunter are in feasibility, promising geographic diversification away from inland congestion. Overall, geographic decarbonization advances unevenly, with eastern states aligned on targets while Western Australia independently tackles firming challenges through large batteries and synchronous condensers.

Competitive Landscape

The top three generators control roughly 60% of generation capacity and 70% of retail customers, placing Australia's power market concentration at a moderate level. Merchant renewable developers such as Neoen and Lightsource bp erode incumbent shares by signing long-term PPAs before construction, insulating returns from wholesale volatility. State-owned entities, including CleanCo Queensland and Snowy Hydro, expand renewable portfolios guided by policy rather than quarterly profit goals.

Strategic repositioning is evident. AGL retired Liddell coal in 2023 and installed a 500 MW battery on the site to arbitrage negative midday and positive evening prices. Origin’s AUD 18.7 billion acquisition by Brookfield aligns global infrastructure capital with a multi-decade transition, enabling accelerated battery investments outside public-market constraints. EnergyAustralia commissioned the 316 MW Tallawarra B hydrogen-ready peaker, demonstrating flexible backup while planning the 350 MW Wooreen battery to balance rising renewables.

Disruptors adopt asset-light models. Zen Energy bundles rooftop solar, batteries, and demand-response software for commercial customers, keeping capex off balance sheets and adding grid-service revenue. Flow Power enables real-time wholesale pass-through pricing matched with behind-the-meter assets, delivering 10-15% savings. White-space opportunities center on long-duration storage beyond 8 hours, offshore wind, and VPP aggregation. Investors eye 8-12 hour iron-flow and pumped-hydro projects to address multi-day calm periods that 4-hour lithium batteries cannot firm.

Australia Power Industry Leaders

AGL Energy Ltd.

Origin Energy Ltd.

EnergyAustralia Holdings

Snowy Hydro Ltd.

Alinta Energy Pty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Vestas Wind Systems A/S, a Danish wind turbine manufacturer, has secured an order from Tilt Renewables. The order pertains to the 108-MW Waddi Wind Farm located in Western Australia's Wheatbelt. As part of the agreement, Vestas will supply and install 18 units of its V162-6.0 MW EnVentus platform turbines.

- December 2025: SPIE, a prominent European player in multi-technical services spanning energy infrastructure and communications, has inked a deal to acquire Worley Power Services, a division of Worley Group.

- December 2025: Samsung C&T, the construction division of the Samsung Group, announced that its partnership with Australia's DT Infrastructure clinched a deal worth 940 million won (approximately USD 635.7 million) to construct high-voltage power transmission facilities in Australia.

- December 2025: Canadian Solar Inc. has revealed that its majority-owned subsidiary, CSI Solar Co., Ltd., through its business unit e-STORAGE, will provide a significant battery energy storage system to Vena Energy.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Australia power market as the total grid-connected electricity generation capacity, coal, natural gas, oil, hydro, solar PV, wind, biomass, and other minor sources, expressed in gigawatts and available to serve industrial, commercial, residential, or storage loads.

Scope exclusion: stand-alone diesel gensets that supply isolated mining or construction sites without exporting to the public grid are outside this boundary.

Segmentation Overview

- By Power Source

- Thermal (Coal, Natural Gas, Oil and Diesel)

- Nuclear

- Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal)

- By End User

- Utilities

- Commercial and Industrial

- Residential

- By T&D Voltage Level (Qualitative Analysis only)

- High-Voltage Transmission (Above 230 kV)

- Sub-Transmission (69 to 161 kV)

- Medium-Voltage Distribution (13.2 to 34.5 kV)

- Low-Voltage Distribution (Up to 1 kV)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with grid planners, network service providers, equipment suppliers, renewable project developers, and leading rooftop-solar installers across New South Wales, Queensland, Victoria, and Western Australia. Insights on realistic ramp-up calendars, average capacity factors, and reserve-margin expectations sharpened assumptions drawn from desk work.

Desk Research

Initial fact-finding drew on public datasets from the Department of Climate Change, Energy, the Environment and Water, the Australian Energy Market Operator, and the Clean Energy Council, which list fleet composition, retirements, and planned additions. According to Mordor Intelligence, these baselines were cross-checked with International Energy Agency statistics and plant announcements captured through Dow Jones Factiva.

A second sweep tapped D&B Hoovers for company filings, customs shipment records on Volza for turbine and panel inflows, and parliamentary papers that clarify policy timelines.

These examples show the open-source backbone supporting our numbers; many further documents were reviewed before figures were locked.

Market-Sizing & Forecasting

A top-down construct converts AEMO demand outlooks into capacity needs; then sampled project lists provide a bottom-up sense-check that tunes totals. Five market fingerprints, coal retirement schedule, annual renewable auction volume, capacity-weighted plant factors, GDP-linked demand growth, and required system reserve margin feed a multivariate regression that projects each driver to 2030. Results are reconciled with supplier roll-ups before Mordor finalizes the baseline.

Data Validation & Update Cycle

Outputs pass two layers of analyst review; variance flags prompt fresh calls with market contacts, and any material policy shift triggers an interim refresh. Reports rebuild every twelve months, and an analyst re-runs the model just before release so clients receive our latest view.

Why Our Australia Power Baseline Commands Confidence

Published estimates often diverge because firms track different metrics, apply varied scope boundaries, or refresh models on contrasting timetables.

Mordor's disciplined scope, driver-based projections, and annual rebuild narrow such gaps for decision-makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 121.79 GW (2025) | Mordor Intelligence | - |

| 277.10 TWh (2024) | Regional Consultancy A | Measures electricity generated, not installed capacity; limited behind-the-meter inclusion |

| USD 41.6 bn (2024) | Industry Publisher B | Values electricity sales, mixes generation and fuel revenue |

| 51.41 GW (2024) | Trade Journal C | Counts renewable assets only, excludes coal and gas plants |

Taken together, the comparison shows that our transparent variables, frequent refresh cadence, and blended top-down plus bottom-up checks deliver a balanced, traceable baseline buyers can rely on.

Key Questions Answered in the Report

How large is the Australia power market in 2026and what growth is expected by 2031?

How large is the Australia power market in 2026 and what growth is expected by 2031?

What share of generation does rooftop solar supply at midday in South Australia?

Rooftop systems met 70% of state demand during spring 2024 midday intervals.

Which storage technology fills multi-day firming gaps beyond 2030?

Pumped hydro such as the 2,200 MW Snowy 2.0 project offers 175 hours of discharge, surpassing 4 hour battery limits.

Why are corporate PPAs priced below wholesale averages?

Miners and data-centers lock in 15-20 year contracts, trading volume risk for AUD 10-20/MWh price discounts.

What is the outlook for coal capacity in Australia after 2029?

Major plants Eraring, Yallourn and Collie are scheduled to retire, reducing coal capacity by 1-2 GW each year.

How fast is utility-scale solar capacity expanding in the Australia power market?

Solar additions average 3-4 GW each year to 2031, driven by corporate PPAs and LRET incentives.

Page last updated on: