Vehicle Intercom System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

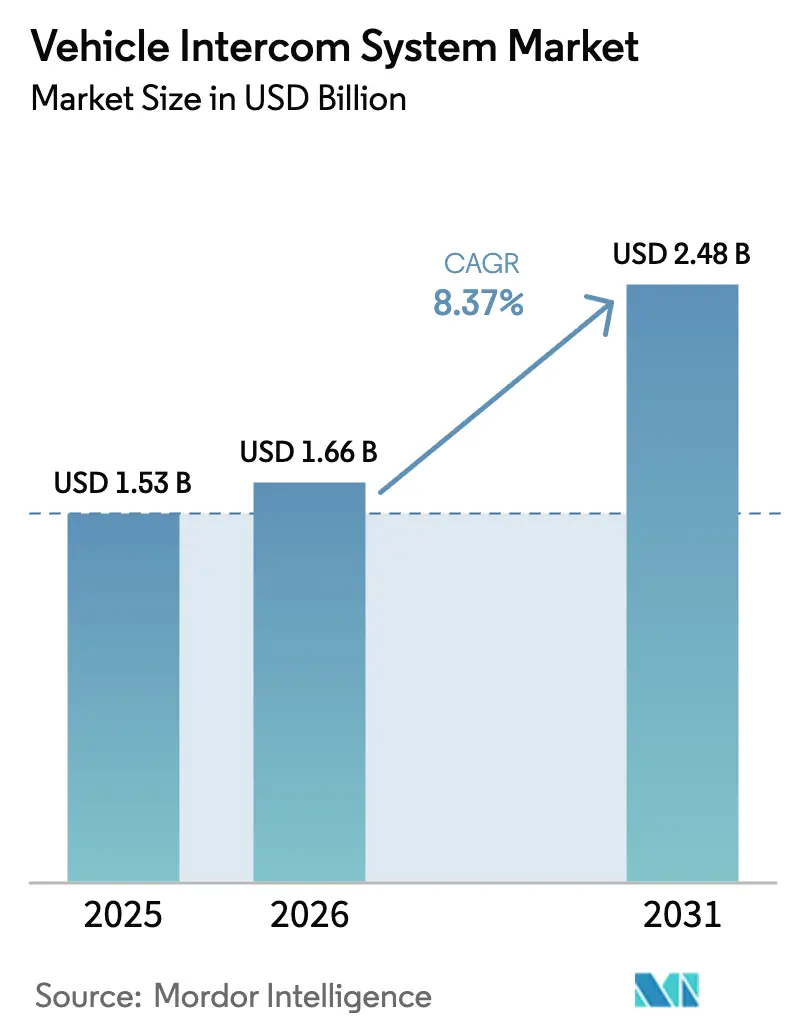

| Market Size (2026) | USD 1.66 Billion |

| Market Size (2031) | USD 2.48 Billion |

| Growth Rate (2026 - 2031) | 8.37% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vehicle Intercom System Market Analysis by Mordor Intelligence

The vehicle intercom system market size was valued at USD 1.53 billion in 2025 and estimated to grow from USD 1.66 billion in 2026 to reach USD 2.48 billion by 2031, at a CAGR of 8.37% during the forecast period (2026-2031). The surge reflects militaries and emergency fleets shifting from analog radios toward fully networked, IP-based voice and data platforms that plug directly into broader tactical and public-safety networks. Sustained modernization budgets across Asia-Pacific and the Middle East, reinforced by Japan’s record USD 54.8 billion defense allocation for 2025, keep procurement pipelines active while fueling competition for lightweight, cyber-hardened designs.[1]Source: Corey Dickstein, “Japan in 2025 to Continue Record-Breaking Run of Increased Defense Spending,” Stars and Stripes, stripes.com Artificial intelligence (AI) enabled audio processing, rising crew mobility needs, and multi-domain operations are redefining system specifications, opening white-space for specialist suppliers. Simultaneously, emergency services accelerate refresh cycles to match 5G adoption, demonstrated by the USD 6.3 billion FirstNet upgrade that mandates vehicle intercom compatibility with broadband applications.

Key Report Takeaways

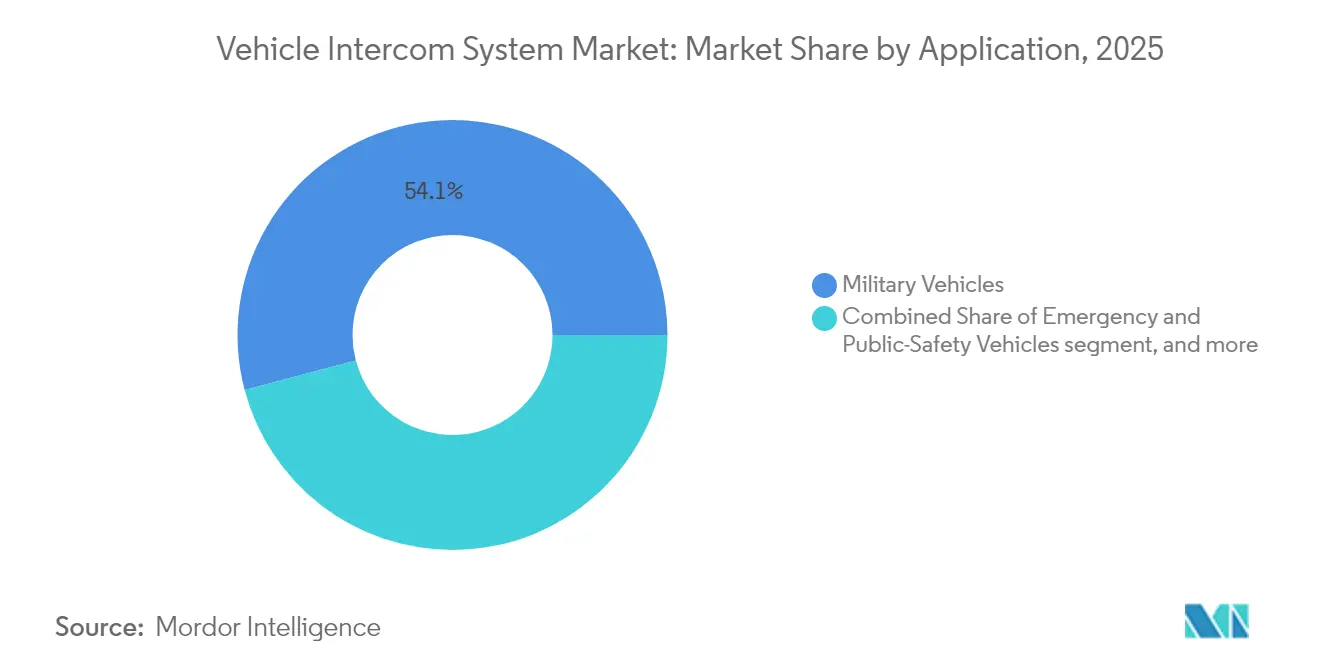

- By application, military vehicles led with 54.12% of vehicle intercom system market share in 2025, whereas emergency and public-safety vehicles are poised to expand at an 11.23% CAGR to 2031.

- By component, crew and control stations accounted for 41.65% of the vehicle intercom system market size in 2025, while headsets and handsets posted the fastest 9.73% CAGR through 2031.

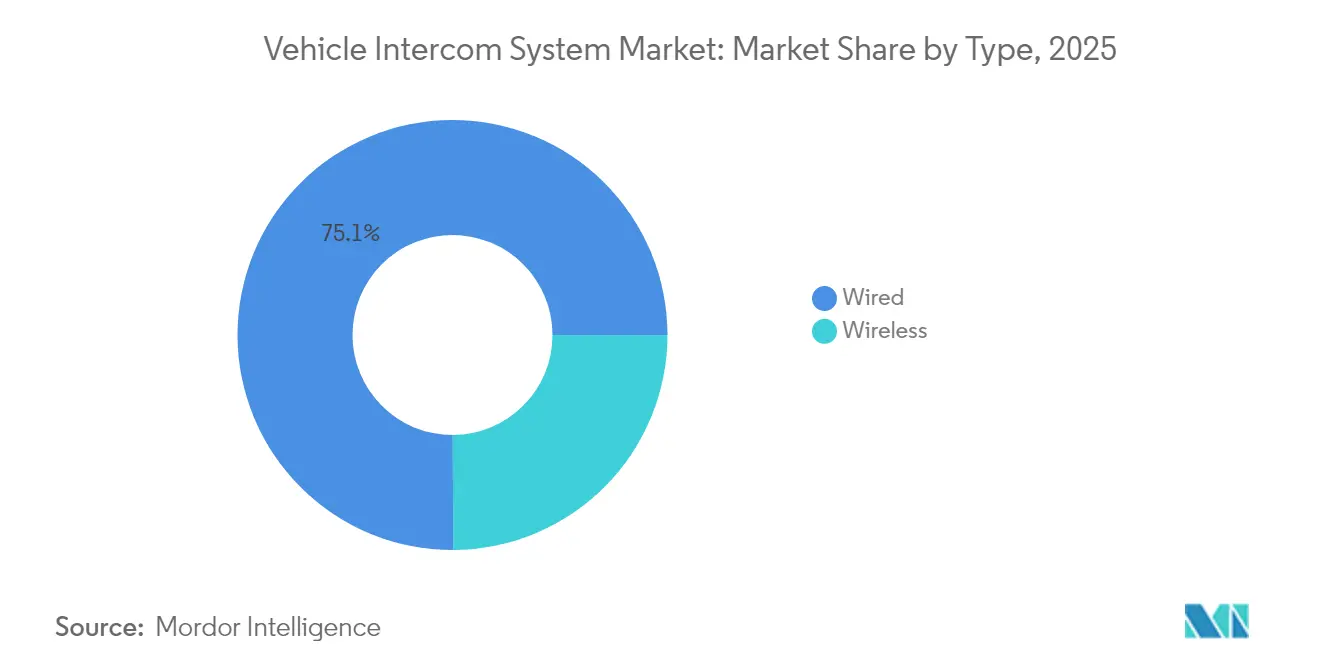

- By type, wired platforms retained 75.05% share of the vehicle intercom system market in 2025; wireless solutions registered the highest 10.59% CAGR over the forecast window.

- By technology, digital systems commanded 64.22% of the vehicle intercom system market in 2025 and are advancing at an 11.28% CAGR to 2031.

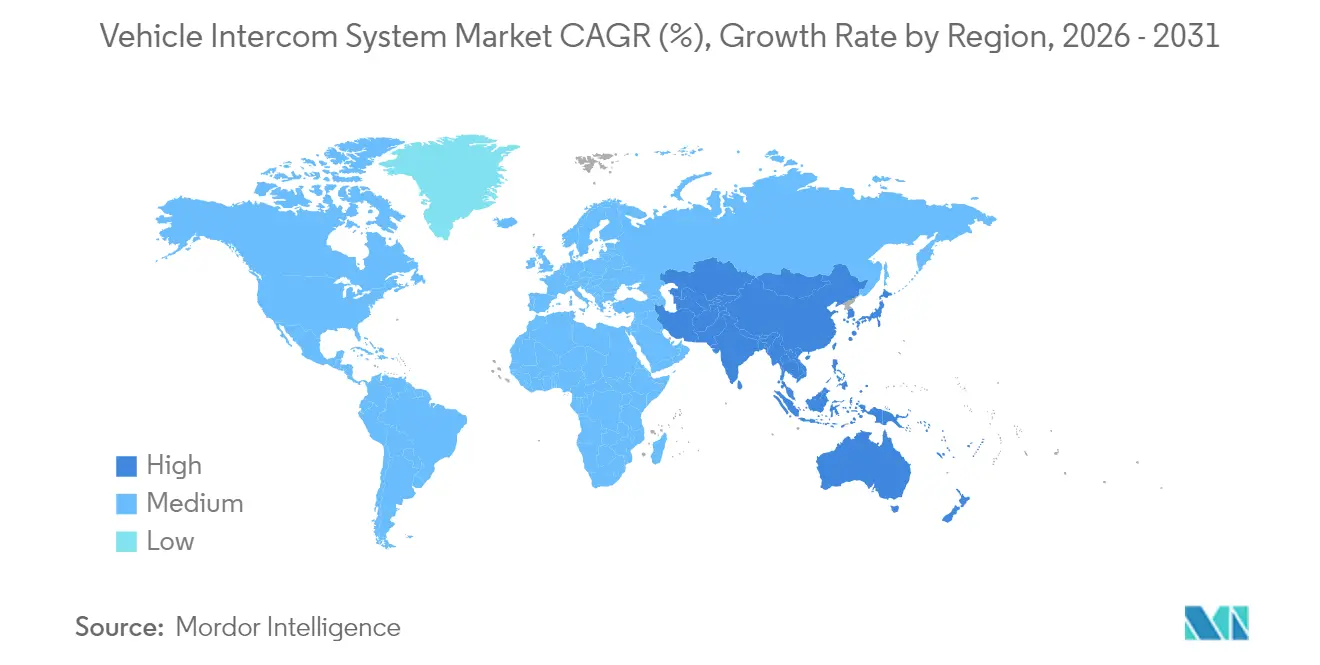

- By geography, North America dominated with 39.05% revenue share in 2025; Asia-Pacific secures the quickest 9.71% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vehicle Intercom System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of network-centric warfare doctrines | +2.1% | NATO members and allies | Medium term (2-4 years) |

| Rising defense modernization budgets in APAC and MENA | +1.8% | Asia-Pacific core, spill-over to Middle East | Short term (≤ 2 years) |

| Shift from analog to IP-based digital intercoms | +1.5% | Global | Medium term (2-4 years) |

| Growing demand for wireless crew-mobility solutions | +1.2% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Need for low-SWaP intercoms for unmanned ground vehicles | +0.9% | North America, EU, selective APAC | Long term (≥ 4 years) |

| Adoption of AI-enabled noise-cancellation and voice analytics | +0.8% | Global tech-forward markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Network-Centric Warfare Doctrines

The US Army’s Armored Formation Network On The Move pilot shows how vehicles turn into rolling nodes that pass high-capacity voice, video, and sensor feeds during maneuvers. Intercom systems must connect seamlessly to satellite, terrestrial, and mesh networks while supporting encryption, quality of service, and real-time data fusion. NATO interoperability guidelines push vendors toward open architectures and common waveforms, which favors software-defined audio gateways. As multi-domain operations expand, crews expect the same interface to switch between voice, data, and AI-driven analytics without hardware swap-outs, accelerating demand for scalable digital platforms. This shift keeps the vehicle intercom system market on a steady upgrade cycle as allied forces standardize a new battlefield communications doctrine.

Rising Defense Modernization Budgets in APAC and MENA

Japan’s FY 2025 budget earmarks sizable funds for unmanned platforms and long-range precision fires, each requiring resilient onboard communications. Parallel programs in the UAE, highlighted by the EDGE–Thales radio partnership, show regional governments blending local manufacturing with imported technology to build sovereign command-and-control capacity.[2]Source: Thales Group, “EDGE and Thales Announce a Strategic Partnership for Radio Communications Development and Manufacturing in the UAE,” thalesgroup.com Procurement timelines are tied to broader force-structure plans, giving suppliers predictable order books. Commercial off-the-shelf sub-systems are gaining acceptance when certified to military EMC and cyber standards, trimming integration risk. Consequently, the vehicle intercom system market benefits from recurring retrofit work and new-build vehicle contracts across armored, logistics, and border-patrol fleets.

Shift from Analog to IP-Based Digital Intercoms

L3Harris’s RF-7800I, with 80% of its capability delivered through software, illustrates how IP migration slashes hardware swaps while allowing field upgrades over the air.[3]Source: L3Harris Technologies, “RF-7800I Tactical Networking Intercom Brochure,” l3harris.com Digital backbones integrate with IPv6 networks, support remote diagnostics, and run advanced voice codecs that squeeze bandwidth without sacrificing clarity. Cyber vulnerabilities remain a concern, pushing manufacturers to embed certified encryption modules and zero-trust architectures by design. Despite these added safeguards, lifecycle costs drop because firmware patches replace board redesigns. As analog inventories retire, armed forces and first-responder agencies pivot almost entirely to software-defined systems, lifting the vehicle intercom system market toward double-digit growth until digital saturation.

Growing Demand for Wireless Crew-Mobility Solutions

Dismounted operations inside dense urban zones need uninterrupted voice links as soldiers exit vehicles to clear buildings. Axnes’s PNG wireless intercom meets this requirement by building a self-healing mesh that covers extended ranges without a fixed base station. Battery endurance improvements and channel-hopping encryption alleviate historical reliability and security concerns. Wireless kits simplify fleet retrofits by bypassing complex hull penetrations on legacy platforms. As 5G and beyond-5G technologies mature under Navy SBIR experiments, bandwidth will rise to video-grade levels, fostering adoption within the vehicle intercom system market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain exposure to rare-earth electronic components | -1.4% | Global, acute in North America and EU | Short term (≤ 2 years) |

| Electromagnetic-interference compliance burden | -0.8% | Global, stricter in EU and North America | Medium term (2-4 years) |

| Cyber-hardening costs for IP intercoms in tactical networks | -0.7% | Tech-advanced militaries worldwide | Medium term (2-4 years) |

| Proprietary interface lock-in slowing multi-vendor integration | -0.5% | North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Exposure to Rare-Earth Electronic Components

Rare-earth magnets and specialty semiconductors underpin secure voice modules yet remain concentrated in a handful of Chinese refineries. The US Department of Defense admitted existing stockpiles cannot cover wartime demand, making cost-plus contracts vulnerable to sudden price spikes. Vendors explore substitution with ferrite materials or domestic recycling streams, but military-grade purity complicates quick fixes. After lengthy environmental testing, intercom producers often qualify single-source electronic boards; relocating production repeats the process and delays deliveries. This bottleneck tempers the otherwise robust expansion of the vehicle intercom system market.

Electromagnetic-Interference Compliance Burden

Standards such as MIL-STD-461G and CISPR-25 force exhaustive testing regimes to verify that intercoms neither radiate harmful emissions nor succumb to external jamming. Engineers must add shielding and filters that increase weight and cost as vehicles integrate high-power electric drives and multiple RF subsystems. Small manufacturers feel the pinch because outsourced test labs charge premium rates and slots are booked months in advance. Compliance remains non-negotiable, particularly when electronic-warfare threats escalate in contested theaters, making EMI management an unavoidable cost of participation in the vehicle intercom system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Military Dominance Drives Emergency Modernization

Military vehicles generated the bulk of 2025 revenues, accounting for 54.12% of the vehicle intercom system market. Emergency and public-safety vehicles, however, are tracking an 11.23% CAGR that positions them as the next major value pool. Many police, fire, and ambulance fleets run century-old analog radios that cannot support multimedia situational awareness or meet cyber mandates set by national broadband programs like FirstNet. Agencies now replace static consoles with ruggedized, IP-native intercom hubs that integrate LTE, 5G, and satellite backhauls.

The widening adoption of body-worn cameras and sensor-rich wearables also stimulates demand for low-latency voice paths and edge analytics. In contrast, the defense segment seeks deeper network integration for unmanned ground vehicles, necessitating intercoms orchestrating human and robotic teammates. Commercial truck and airport ground-support niches post mid-single-digit expansion as safety regulations tighten, yet they remain comparatively small slices of the vehicle intercom system market. Military upgrade cycles will continue to fund the baseline volume, while emergency services deliver the highest incremental growth through 2031.

By Component Type: Headsets Lead Wireless Revolution

Crew and control stations represented 41.65% of 2025 sales, reflecting their centrality within armored, logistics, and rescue vehicles. Nonetheless, advanced headsets and handsets rise at a 9.73% CAGR because crews demand untethered movement and adaptive noise cancellation inside loud cabins. The vehicle intercom system market size for portable audio devices is projected to expand steadily as wireless headsets replace traditional lanyard-based talk-backs.

Honeywell’s QUIETPRO QP400, featuring active protection and multiple channels, typifies next-generation wearables that combine hearing protection with command-net access. Supporting hardware like radio gateways and central processors shift toward modular plug-ins, aligning with the US Army’s SAVE initiative that standardizes mounting envelopes. Software content keeps rising, giving vendors a recurring revenue stream through capability upgrades even after the physical install is complete. These dynamics strengthen the aftermarket within the vehicle intercom system market.

By Type: Wireless Gains Despite Wired Dominance

Wired architectures retained 75.05% revenue in 2025 because armor plating presents a natural conduit for shielded cabling that guarantees security and uptime. Still, the wireless slice of the vehicle intercom system market is growing 10.59% annually as encryption, frequency agility, and battery density improve. Wireless eliminates hull penetrations, shortens installation windows, and allows rapid redeployments in humanitarian missions and pop-up command posts.

Hybrid topologies are emerging where a wired backbone supplies power and bulk data, while local wireless nodes cover turret baskets or dismounted squads. General Dynamics’ GVR5 Dual-Band Wave Relay MANET offers one blueprint, providing seamless roaming between vehicular and on-foot roles. As tactical 5G pilots demonstrate higher throughput, confidence rises that wireless can shoulder mission-critical voice. That said, spectrum-management policies and operational-security rules still limit blanket cut-overs, keeping wired systems entrenched in the vehicle intercom system market.

By Technology: Digital Transformation Accelerates

Digital platforms captured 64.22% share in 2025 and will outpace analog at an 11.28% CAGR to 2031, cementing the new normal for the vehicle intercom system market. IP packets permit quality of service tagging, AES-256 encryption, and API-based integration with battle-management applications, none of which analog circuits can match. Software-defined audio engines let operators field-upgrade acoustics, beam-forming, and language translation within minutes, slashing through-life cost.

Analog products still serve extreme radiation or EMP environments because they lack semiconductors that could fry under pulse events. Yet most fleets now run mixed architectures as they phase out analog sets during depot maintenance cycles. Interoperability gateways smooth the transition, though they add latency and cost. Ultimately, the inexorable shift to digital unlocks AI services such as speech-to-text transcription and command-net summarization, creating new revenue layers inside the vehicle intercom system market.

Geography Analysis

North America generated 39.05% of 2025 revenues, anchored by the US Army’s Command Post Integrated Infrastructure program and Canada’s NATO commitments. The region boasts a mature defense industrial base that fields cutting-edge AI noise-reduction modules and cyber-secure waveforms. Supply-chain exposure to overseas rare-earth processing remains a strategic vulnerability, prompting on-shoring initiatives that may shift component sourcing patterns yet keep spending elevated.

Asia-Pacific is the fastest-growing region, rising at 9.71% CAGR as regional militaries hedge against geopolitical tension. Japan’s standoff-capability push and Australia’s trilateral security pact drive next-generation command-and-control investment. Indigenous production mandates encourage technology-transfer deals, creating joint-venture channels for Western suppliers. China’s modernization spurs neighboring countries to accelerate vehicle programs, indirectly bolstering the vehicle intercom system market across South Korea, India, and Southeast Asia.

Europe delivers steady, mid-single-digit growth under NATO standardization, with the UK’s Emergency Services Network and Germany’s Bundeswehr upgrades setting procurement precedence. Eastern members prioritize rapid fielding of interoperable radios in response to regional security shifts, underscoring sustained demand. Gulf Cooperation Council states in the Middle East continue selective high-ticket buys, as seen in the UAE-Thales software-defined-radio plant that localizes production. Africa remains nascent, yet peacekeeping and border-security funds generate sporadic orders, ensuring the geographic footprint of the vehicle intercom system market remains diverse.

Competitive Landscape

The vehicle intercom system market is moderately fragmented. Thales, L3Harris Technologies, and Elbit Systems anchor the top tier through complete portfolios that cover vehicle, airborne, and soldier comms, reinforced by global support centers. Thales reinforced cockpit and ground dominance with the 2024 acquisition of Cobham Aerospace Communications, adding safety-critical audio lines. L3Harris pushes software-defined differentiation, seen in the 2025 launch of Vapor and Vanguard wideband waveforms for its Falcon III family, which promise resilient performance in dense threat environments. Elbit leverages ISR drone contracts to cross-sell intercom modules tailored for unmanned teaming scenarios.

Mid-tier challengers focus on wireless, AI, or low-SWaP niches. Norway’s Axnes capitalizes on its PNG mesh for special operations and SAR aircraft, reflecting how small firms win contracts by addressing rugged mission sets. US startups partner with cloud-AI providers to embed voice analytics that triage radio chatter, easing cognitive load on crews. Meanwhile, tier-one players adopt open-architecture roadmaps like the US SAVE standard to lock in hardware, then upsell software-only enhancements over time.

Barriers to entry remain high due to stringent EMI and security certifications and the long qualification cycles embedded in defense contracting. Demand for quick-fit wireless kits in emergency vehicles opens doors for commercial electronics vendors. Strategic alliances such as the EDGE–Thales JV in the UAE show incumbents using local partnerships to secure offset credits while seeding future upgrade revenue. Across the board, AI-based noise reduction, mesh networking, and software-centric business models will shape next-round competitive dynamics.

Vehicle Intercom System Industry Leaders

L3Harris Technologies, Inc.

Thales Group

Chelton Limited

David Clark Company

Elbit Systems Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: INVISIO, a tactical communications expert, enhanced its market-leading intercom system, which is designed for customized user and radio communication. The INVISIO Link™, scheduled for shipment in the coming months, introduces wireless access to the system by integrating a body-worn dongle and a base station, improving mobility, flexibility, interoperability, and functionality for mission-critical users.

- October 2024: L3Harris unveiled the Diamondback autonomous reconnaissance vehicle, featuring modular open architecture for integrated mission communication.

Global Vehicle Intercom System Market Report Scope

Vehicle intercom systems are the new generation intercom systems used by emergency vehicles such as military vehicles and ambulances. This communication system can be used in high noise, various environmental conditions, and emergency situations providing clear communication without affecting the hearing of end users.

The vehicle intercom system market is segmented by application, by component, by technology, and by geography. By application, the market is segmented into military vehicles, commercial vehicles, airport ground support vehicles, and emergency vehicles. By component, the market is segmented into wired, and wireless. By technology, the market is segmented into analog, and digital. By geography, the market is segmented into north America, Europe, Asia-pacific, Latin America, and the middle east and Africa.

| Military Vehicles |

| Emergency and Public Safety Vehicles |

| Commercial and Industrial Trucks |

| Airport Ground-Support Equipment |

| Construction and Mining Equipment |

| Headsets and Handsets |

| Crew and Control Stations |

| Radio Interface/Gateway Units |

| Central Processing Units and Networking Hubs |

| Cables, Ancillaries and Software |

| Wired |

| Wireless |

| Analog |

| Digital |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Application | Military Vehicles | ||

| Emergency and Public Safety Vehicles | |||

| Commercial and Industrial Trucks | |||

| Airport Ground-Support Equipment | |||

| Construction and Mining Equipment | |||

| By Component Type | Headsets and Handsets | ||

| Crew and Control Stations | |||

| Radio Interface/Gateway Units | |||

| Central Processing Units and Networking Hubs | |||

| Cables, Ancillaries and Software | |||

| By Type | Wired | ||

| Wireless | |||

| By Technology | Analog | ||

| Digital | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the vehicle intercom system market?

The market is valued at USD 1.66 billion in 2026 and is on course to reach USD 2.48 billion by 2031, delivering an 8.37% CAGR.

Which application segment is expanding the fastest?

Emergency and public-safety vehicles recorded the quickest 11.23% CAGR as agencies replace aging analog systems with IP-enabled intercoms.

How quickly is wireless technology growing within the vehicle intercom system market?

Wireless platforms are increasing at a 10.59% CAGR, outpacing wired systems due to crew-mobility requirements and easier retrofits.

Why are digital intercoms overtaking analog solutions?

Digital systems support software updates, advanced encryption, and AI-driven audio features, delivering an 11.28% CAGR compared with declining analog demand.

Which region offers the highest growth potential by 2031?

Asia-Pacific leads with a 9.71% CAGR, propelled by record defense budgets and a push for indigenous manufacturing capability.

Page last updated on: