United States Multi-Tenant (Colocation) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

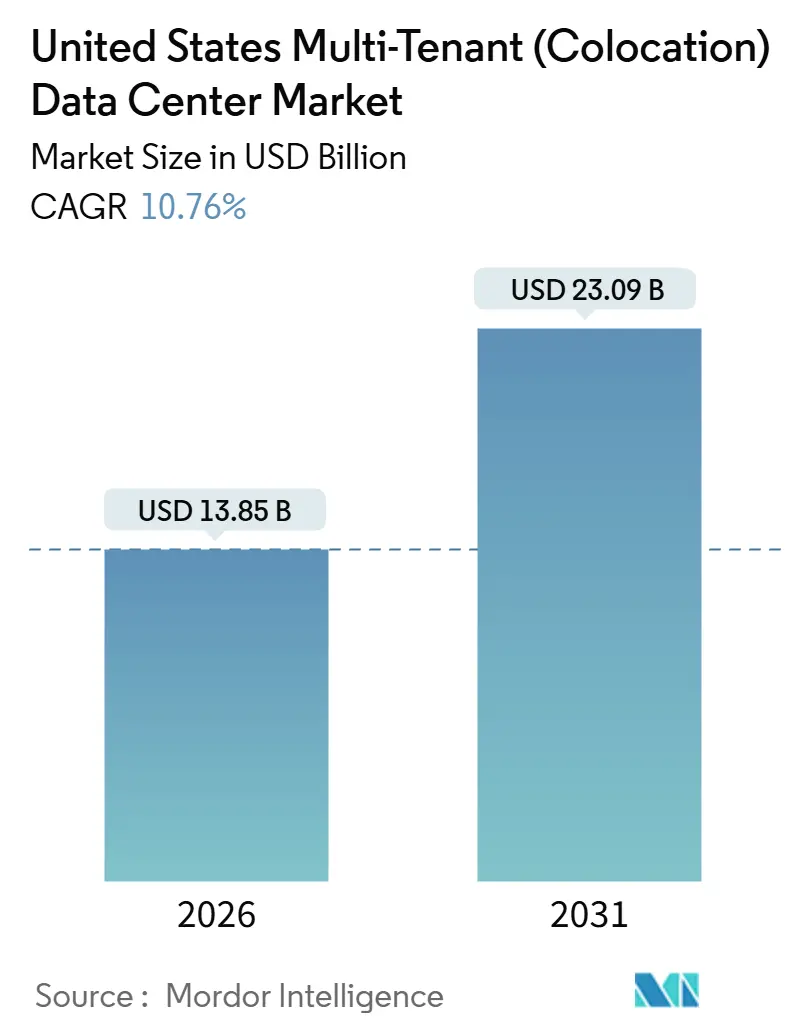

| Market Size (2026) | USD 13.85 Billion |

| Market Size (2031) | USD 23.09 Billion |

| Growth Rate (2026 - 2031) | 10.76% CAGR |

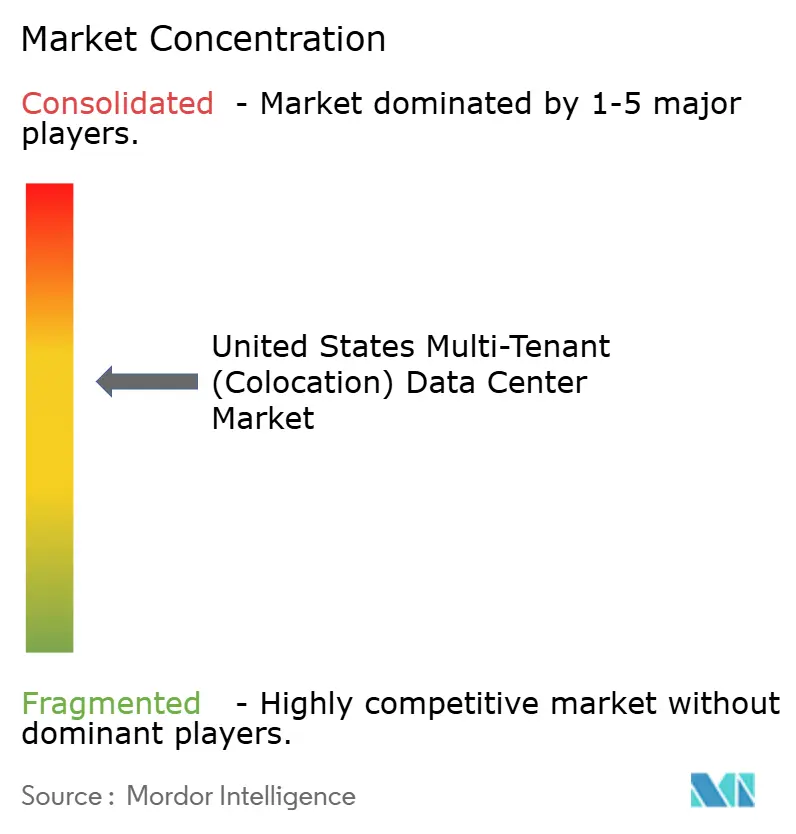

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Multi-Tenant (Colocation) Data Center Market Analysis by Mordor Intelligence

The United States multi-tenant (colocation) data center market size is estimated at USD 13.85 billion in 2026, and is expected to reach USD 23.09 billion by 2031, at a CAGR of 10.76% during the forecast period 2026-2031. Current expansion is rooted in three converging forces: hyperscaler migration to wholesale colocation in Tier-2 metros, accelerated artificial intelligence training that demands liquid-cooled racks, and enterprise adoption of hybrid-cloud strategies that elevate interconnection revenue. A generous federal tax-credit regime, introduced under the Inflation Reduction Act, lowers the levelized cost of capacity and encourages groundbreakings in Dallas, Atlanta, and Chicago. Power purchase agreements tied to low-cost solar and wind generation now underwrite 15-year hedge contracts, improving cost visibility for operators while satisfying sustainability clauses embedded in 78% of Fortune 500 supplier questionnaires. Competitive intensity remains moderate because the five largest operators hold 48% of installed capacity, yet fragmentation persists beneath that tier as edge-focused specialists pursue latency-sensitive workloads from autonomous vehicles and real-time analytics.

Key Report Takeaways

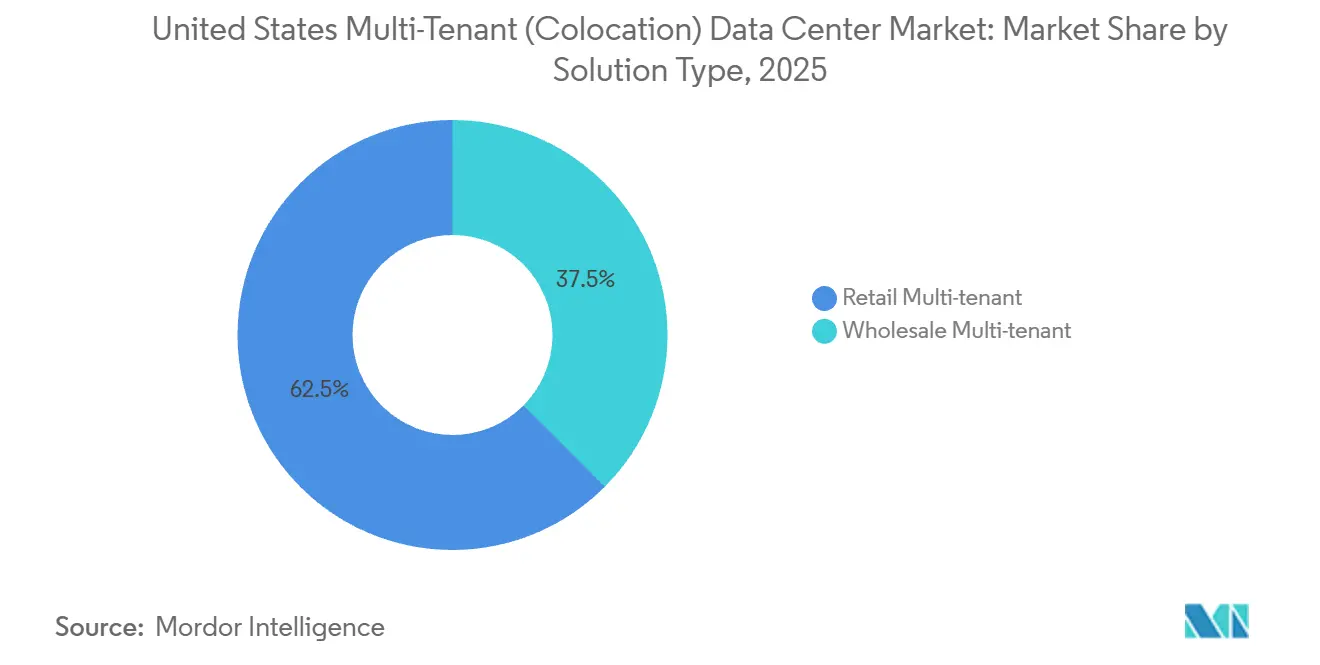

- By solution type, retail colocation led with 62.53% revenue share in 2025, while wholesale colocation is forecast to expand at an 11.32% CAGR through 2031.

- By tier classification, Tier 3 held 47.43% of the United States multi-tenant (colocation) data center market share in 2025, whereas Tier 4 deployments are projected to register an 11.66% CAGR through 2031.

- By facility size, large data centers captured 49.21% of the United States multi-tenant (colocation) data center market in 2025, but hyperscale campuses are advancing at an 11.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Multi-Tenant (Colocation) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Proliferation of AI and ML Workloads | +2.8% | National, Northern Virginia, Silicon Valley, Dallas | Short term (≤ 2 years) |

| Accelerating Adoption of Hybrid Cloud and Edge Computing | +2.3% | National, Atlanta, Chicago, Phoenix | Medium term (2-4 years) |

| Hyperscaler Preference for Build-to-Suit Wholesale Colocation | +1.9% | Dallas, Atlanta, Chicago, Denver | Medium term (2-4 years) |

| Growing Availability of Renewable Energy Purchase Agreements | +1.5% | Texas, Southwest, Pacific Northwest | Long term (≥ 4 years) |

| Surging Demand for Interconnection Hubs | +1.3% | Ashburn, Los Angeles, Chicago, New York | Short term (≤ 2 years) |

| Federal and State Tax Incentives | +1.0% | National, Virginia, Texas, Ohio, Georgia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Proliferation of AI and ML Workloads Requiring High-Density Colocation

Nvidia H100 clusters that underpin large-language-model training routinely exceed 100 kW per cabinet, a density that only 18% of US colocation halls could support in December 2025.[1]Uptime Institute, “Data Center Tier Standards and Certifications,” uptimeinstitute.com Hyperscalers therefore reserve wholesale suites of 5-10 MW to secure liquid-cooling readiness before the next GPU allocation cycle. CyrusOne disclosed that AI customers represented 42% of all bookings during the first three quarters of 2025. Operators that invest in rear-door heat exchangers report 30-40% pricing premiums relative to legacy deployments, compressing payback periods to under four years. National Fire Protection Association is revising NFPA 75 to clarify lithium-ion battery suppression protocols for such high-density clusters.

Accelerating Adoption of Hybrid Cloud and Edge Computing Architectures

Flexential recorded a jump from 51% to 63% of enterprise customers running hybrid deployments between 2024 and 2025. Enterprises distribute workloads across on-premises racks, public-cloud regions, and colocation cages to satisfy latency and data-sovereignty mandates. EdgeConneX expanded to 42 edge locations by focusing on Omaha, Boise, and Raleigh, cities overlooked by national platforms. Analysts expect 800-1,000 MW of new edge colocation demand by 2028. Regulatory strictures such as HIPAA continue to favor hybrid cloud alliances with carrier-neutral operators.

Hyperscaler Preference for Build-to-Suit Wholesale Colocation in Tier-2 US Metros

Digital Realty’s xScale platform added 120 MW in Dallas and Atlanta during 2025, all pre-leased to cloud platforms that seek faster energization timelines than Northern Virginia can offer. Ohio extends a 75% sales-tax exemption on data-center equipment, and Georgia offers investment-tax credits up to 5% for qualifying builds.[2]State of Ohio Department of Development, “Data Center Tax Incentives,” development.ohio.gov Wholesale tenants value 18- to 24-month utility interconnection versus 36- to 48-month waits in primary hubs. Operators in Tier-1 metros now differentiate by cultivating dense peering fabrics that edge-only facilities cannot match.

Growing Availability of Renewable Energy Purchase Agreements in US Power Markets

Equinix reached 96% renewable coverage of its US footprint by December 2025. Solar PPAs in Texas clear below USD 30 per MWh, a price that undercuts fossil-fuel alternatives. Switch operates its Nevada campus on 100% renewable supply and markets carbon-free hosting at premium rates. The Inflation Reduction Act should deliver an incremental 15-20 GW of renewable capacity by 2028, deepening PPA liquidity.[3]U.S. Energy Information Administration, “Renewable Energy Market Data,” eia.gov

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Power Grid Constraints | -1.8% | Northern Virginia, Phoenix, Silicon Valley, Dallas | Short term (≤ 2 years) |

| Rising Land Acquisition and Construction Costs | -1.2% | Ashburn, Chandler, Santa Clara | Medium term (2-4 years) |

| Intensifying Sustainability Reporting Requirements | -0.6% | National | Long term (≥ 4 years) |

| Competition from Hyperscaler Self-Builds | -0.9% | Northern Virginia, Oregon, Iowa, South Carolina | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Power Grid Constraints and Utility Lead Times

Pending interconnection requests in Northern Virginia exceed 4.2 GW, representing nearly three years of backlog. Dominion Energy froze new large-load hookups in portions of Loudoun County during 2025, compelling builders to self-fund substations or postpone energization. Arizona Public Service faces a similar strain in Phoenix, where data-center applications surpassed 1.8 GW in 2025. The Federal Energy Regulatory Commission may prioritize projects with firm site control and completed environmental reviews to clear queues faster. Operators have begun colocating adjacent to generation assets or installing on-site natural-gas peakers at an added USD 50-80 million per 50-MW hall.

Rising Land Acquisition and Construction Costs in Core Hubs

Land in Ashburn appreciated 28% between January 2024 and December 2025 as developers compete for utility-adjacent parcels. Construction outlays for hyperscale halls climbed to USD 12-15 million per MW in 2025, up from USD 9-11 million in 2023, driven by steel inflation and switchgear shortages. Builders respond by adopting modular electrical rooms that cut on-site labor 30-40% and compress schedules by up to six months. Smaller developers without balance-sheet resilience are exiting through asset sales to REITs and infrastructure funds.[4]CBRE, “Data Center Development Trends,” cbre.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Wholesale Momentum Builds on Hyperscaler Reservations

Retail colocation held 62.53% share of the United States multi-tenant (colocation) data center market in 2025, reflecting the appeal of turnkey rack-level leasing to small and midsized enterprises that avoid capital expenditure. Operators bundle power, cooling, and physical security so customers can scale workloads a single rack at a time. Wholesale leases of 5 MW or more are growing faster, at an 11.32% CAGR, as hyperscalers reserve contiguous capacity to bypass uncertainty in utility queues. The wholesale segment benefits from AI and hybrid-cloud workloads that demand bespoke electrical topologies, liquid-cooling loops, and dedicated meet-me rooms.

CyrusOne’s Massively Modular builds allowed tenants to specify up to 30 kW per rack in 2025, capturing wholesale demand at premium rates. Digital Realty pre-leased 85% of its 240-MW 2025 pipeline before first power, signaling that supply still trails demand. Retail colocation will remain resilient because enterprises value geographic diversity and disaster-recovery options across multiple metros, yet wholesale’s faster expansion ensures it will capture the majority of incremental megawatts commissioned during the forecast window. As a result, the United States multi-tenant (colocation) data center market will see a gradual rebalancing toward wholesale without eroding the entrenched retail installed base.

By Tier Type: Tier 4 Certifications Gain Traction Under Insurance Scrutiny

Tier 3 sites commanded 47.43% of United States multi-tenant (colocation) data center market share in 2025 because concurrent maintainability satisfies most service-level agreements at an attractive cost point. Tier 4 halls, however, are growing at an 11.66% CAGR, powered by insurance carriers that now require fault-tolerant designs before underwriting cyber-risk policies above USD 50 million.

Uptime Institute logged a 14% rise in domestic Tier 4 certifications during 2025, with financial services absorbing 38% of new certificates and healthcare 22%. Capital overhead of Tier 4 construction has narrowed from 40% in 2023 to 25-30% in 2025 due to economies of scale in dual-fed switchgear and redundant chillers. Blockchain and real-time payments need zero downtime, further shifting demand to Tier 4. Conversely, Tier 1 and Tier 2 facilities continue to lose relevance as enterprises consolidate into higher-tier campuses to simplify compliance with frameworks such as FedRAMP and PCI-DSS. The United States multi-tenant (colocation) data center market size tied to Tier 4 will therefore accelerate, though Tier 3 will remain the dominant installed base through 2031 because its performance-to-cost ratio still aligns with mainstream enterprise workloads.

By Data Center Size: Hyperscale Campuses Lead Next-Generation Workloads

Large halls between 10 MW and 50 MW accounted for 49.21% of the United States multi-tenant (colocation) data center market share in 2025, a legacy of enterprise consolidation. Hyperscale campuses above 50 MW now post an 11.75% CAGR as generative AI and public-cloud capacity additions co-locate GPU clusters that demand contiguous power blocks.

Operators retrofitting legacy halls for liquid cooling often sacrifice rentable square footage, while purpose-built hyperscale shells integrate cold-plate or rear-door heat-exchanger loops from day one. Switch, for example, deploys direct-to-chip cooling across its Nevada and Michigan campuses, enabling 120 kW racks without breaching 1.2 PUE. Edge-oriented small facilities under 5 MW continue to thrive in secondary metros where 10-20 ms latency is mission-critical for autonomous vehicle telemetry. DataBank’s 65-site edge network illustrates how small-to-medium halls can capture regional analytics and content caching. Nevertheless, the United States multi-tenant (colocation) data center market size devoted to hyperscale will expand the fastest as the top 10 cloud and AI providers consolidate procurement, compelling operators to pour capital into mega-campuses that can scale beyond 200 MW.

Geography Analysis

Northern Virginia remains the single largest hub, hosting more than 2 GW of installed capacity; however, interconnection moratoria and escalating land prices restrain short-term supply. Silicon Valley encounters similar constraints because available transmission capacity has flatlined, while Phoenix faces rising transmission queue times that now exceed 30 months. These limitations redirect capital to Tier-2 metros where power availability and tax incentives are more favorable, thereby reshaping the geographic spread of new builds.

Dallas leads the Tier-2 surge, recording 280 MW of net absorption in 2025 thanks to deregulated power markets and abundant solar resources that support competitively priced PPAs. Atlanta follows closely; Georgia Power maintains reserve-margin headroom, and the state offers investment tax credits that reduce upfront capital outlays. Chicago benefits from a unique combination of low-carbon nuclear baseload and five transcontinental fiber corridors, making it a strategic site for latency-sensitive trading and media workloads. Denver and Salt Lake City are also capturing overflow demand, with developers citing 18- to 24-month interconnection timelines compared with 36-plus months in Northern Virginia.

Emerging metros such as Columbus, Kansas City, and Reno attract edge deployments that require sub-20 ms latency to reach Midwest and Mountain-West consumers. Operators choose these cities to hedge against power price volatility while securing water rights unavailable in coastal hubs. Exurban parcels remain plentiful, yet builders must invest in new fiber backhaul and water infrastructure, which can extend project schedules by up to 9 months. Over the forecast period, geographic diversification will temper land and power inflation in legacy hubs while sustaining aggregate growth across the broader United States multi-tenant (colocation) data center market.

Competitive Landscape

Market concentration is moderate, with Equinix, Digital Realty, CyrusOne, CoreSite, and Switch together holding 48% of installed capacity. Equinix monetizes dense interconnection fabrics, where cross-connect and on-ramp services deliver gross margins above 65% and represent 20% of group revenue. Digital Realty relies on PlatformDIGITAL to simplify hybrid-cloud orchestration, which deepens customer lock-in and reduces churn across 34 domestic campuses.

CyrusOne differentiates through Massively Modular builds that compress construction schedules by prefabricating electrical and mechanical rooms, enabling 20% quicker deliveries than stick-built halls. CoreSite focuses on software-defined interconnection via its Open Cloud Exchange, shrinking provisioning from weeks to minutes and capturing growing network-automation demand. Switch leverages 100% renewable supply and liquid-cooled designs to win AI-heavy tenants that prioritize carbon-neutral capacity paired with 120 kW rack densities.

Below the top tier, STACK Infrastructure, Compass Datacenters, EdgeConneX, and DataBank target Tier-2 and edge metros with build-to-suit or distributed footprints designed for latency-critical workloads. Schneider Electric’s EcoStruxure AI platform helps many operators cut unplanned downtime by 35% and reduce energy waste by up to 12%, making technology partnerships a competitive necessity. Patent filings for immersion-cooling modules and modular DC-in-a-box solutions rose 22% in 2025, signaling a race to meet next-generation density benchmarks while controlling total cost of ownership.

United States Multi-Tenant (Colocation) Data Center Industry Leaders

Digital Reality Trust, Inc.

Equinix, Inc.

CyrusOne LLC

Quality Technology Services (QTS Realty Trust)

CoreSite Realty Corporation (American Tower)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Digital Realty finished a 72 MW hyperscale hall in Dallas with direct-to-chip cooling designed for 120 kW racks and signed a 15-year pre-lease with a cloud provider.

- December 2025: Equinix acquired three carrier-neutral sites in Chicago for USD 420 million, adding 18 MW of capacity to its Midwest interconnection hub.

- November 2025: CyrusOne secured USD 1.2 billion in project financing to build 180 MW across Phoenix and Northern Virginia, with interest-rate incentives linked to Science Based Targets validation.

- October 2025: STACK Infrastructure partnered with a solar developer to install 200 MW of on-site generation and battery storage, targeting 80% renewable coverage by 2028.

United States Multi-Tenant (Colocation) Data Center Market Report Scope

A multi-tenant (colocation) data center is a facility where businesses can rent space for servers and other computing hardware. These centers provide shared infrastructure, including power, cooling, and security, enabling cost efficiency and scalability for tenants.

The United States Multi-Tenant (Colocation) Data Center Market Report is Segmented by Solution Type (Wholesale Multi-tenant, Retail Multi-tenant), Tier Type (Tier 1 and 2, Tier 3, Tier 4), and Data Center Size (Small Data Center, Medium Data Center, Large Data Center, Hyperscale Data Center). The Market Forecasts are Provided in Terms of Value (USD).

| Wholesale Multi-tenant |

| Retail Multi-tenant |

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Small Data Center |

| Medium Data Center |

| Large Data Center |

| Hyperscale Data Center |

| By Solution Type | Wholesale Multi-tenant |

| Retail Multi-tenant | |

| By Tier Type | Tier 1 and 2 |

| Tier 3 | |

| Tier 4 | |

| By Data Center Size | Small Data Center |

| Medium Data Center | |

| Large Data Center | |

| Hyperscale Data Center |

Key Questions Answered in the Report

How large is the US multi-tenant data center market in 2026?

The market stands at USD 13.85 billion and is projected to expand to USD 23.09 billion by 2031.

What is driving wholesale colocation growth?

Hyperscalers reserve multi-megawatt blocks to secure liquid-cooled halls and bypass utility queue delays, producing an 11.32% CAGR for wholesale space.

Why are Tier 4 facilities gaining share?

Cyber-insurance carriers and regulators now demand fault-tolerant designs, pushing Tier 4 deployments to an 11.66% CAGR through 2031.

Which metros attract new hyperscale builds?

Dallas, Atlanta, Chicago, and Denver draw investment because they combine faster utility interconnections with generous state tax incentives.

How are operators meeting sustainability mandates?

They lock in long-term renewable PPAs, deploy on-site solar and battery storage, and use AI-driven energy-management systems to cut waste by up to 12%.

What is the main constraint on new supply?

Power-grid congestion in primary hubs such as Northern Virginia and Phoenix extends substation lead times, delaying energization of additional capacity.

Page last updated on: