United States Cocoa And Chocolate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

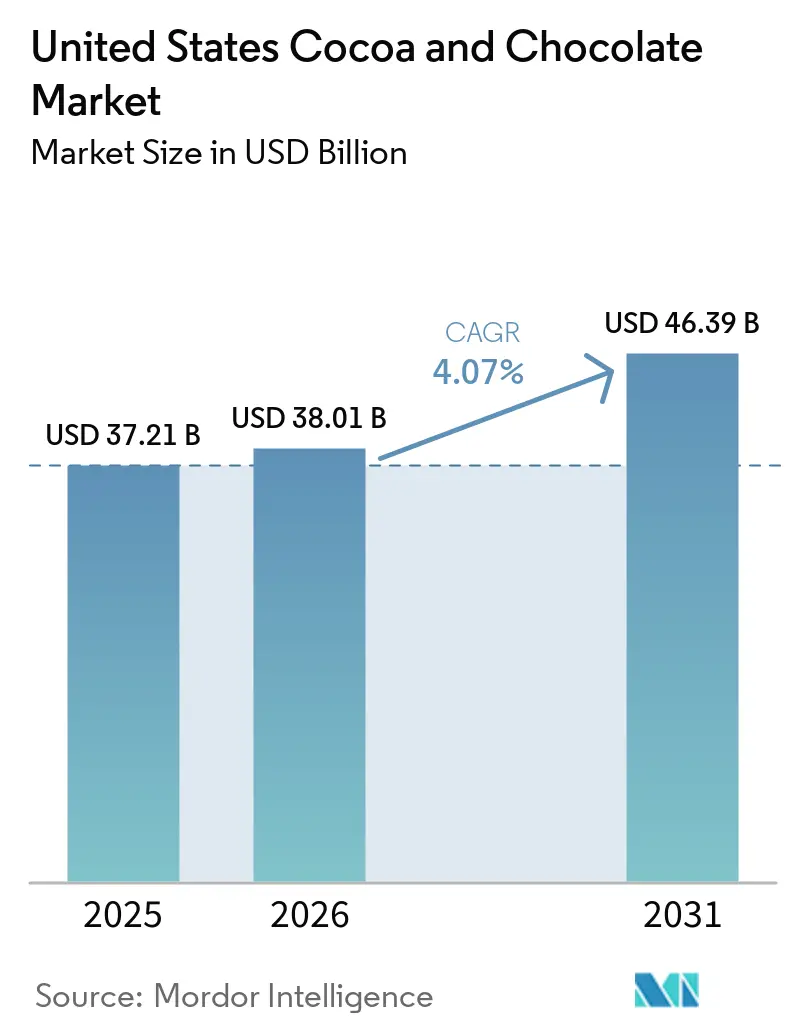

| Base Year Market Size (2025) | USD 37.21 Billion |

| Market Size (2026) | USD 38.01 Billion |

| Market Size (2031) | USD 46.39 Billion |

| Growth Rate (2026 - 2031) | 4.07% CAGR |

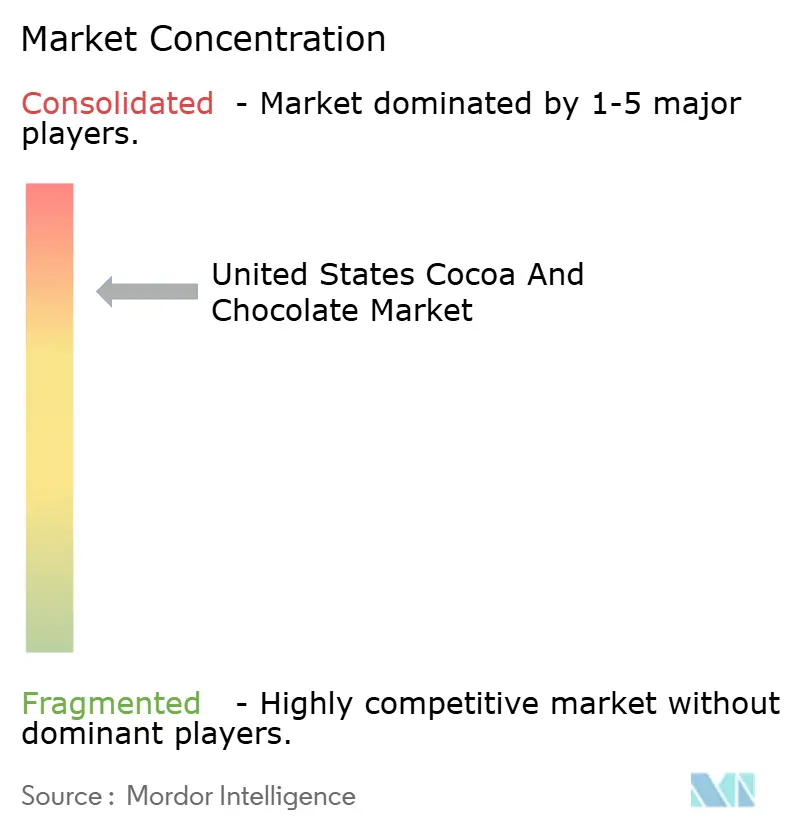

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Cocoa And Chocolate Market Analysis by Mordor Intelligence

The US cocoa and chocolate market was valued at USD 37.2 billion in 2025 and is estimated to grow from USD 38.0 billion in 2026 to reach USD 46.4 billion by 2031, at a CAGR of 4.1% during the forecast period (2026-2031). The United States cocoa and chocolate market is experiencing sustained growth driven by rising premium chocolate consumption, innovation in organic and clean-label cocoa ingredients, and expanding applications across confectionery, bakery, dairy, beverages, cosmetics, and nutraceuticals. The market includes cocoa butter, cocoa powder, cocoa liquor, cocoa nibs, dark chocolate, milk and white chocolate, and compound chocolate distributed through foodservice and retail channels, including supermarkets, convenience stores, online platforms, and specialty stores. According to the United States Department of Agriculture, U.S. imports of cocoa beans and processed cocoa ingredients remained strong through 2025 as manufacturers increased sourcing to support premium confectionery and industrial chocolate production. In 2025, The Hershey Company expanded its Reese Chocolate Processing facility to strengthen production efficiency and chocolate manufacturing capacity in North America. During the same period, Barry Callebaut expanded sustainable and traceable cocoa programs for North American food manufacturers, while Mondelez International accelerated premium chocolate innovation and seasonal product launches across retail channels. In 2026, manufacturers increasingly focused on organic cocoa sourcing partnerships, clean-label chocolate formulations, and capacity optimization strategies to address rising consumer demand for ethically sourced, premium, and functional chocolate products in the United States.

Key Report Takeaways

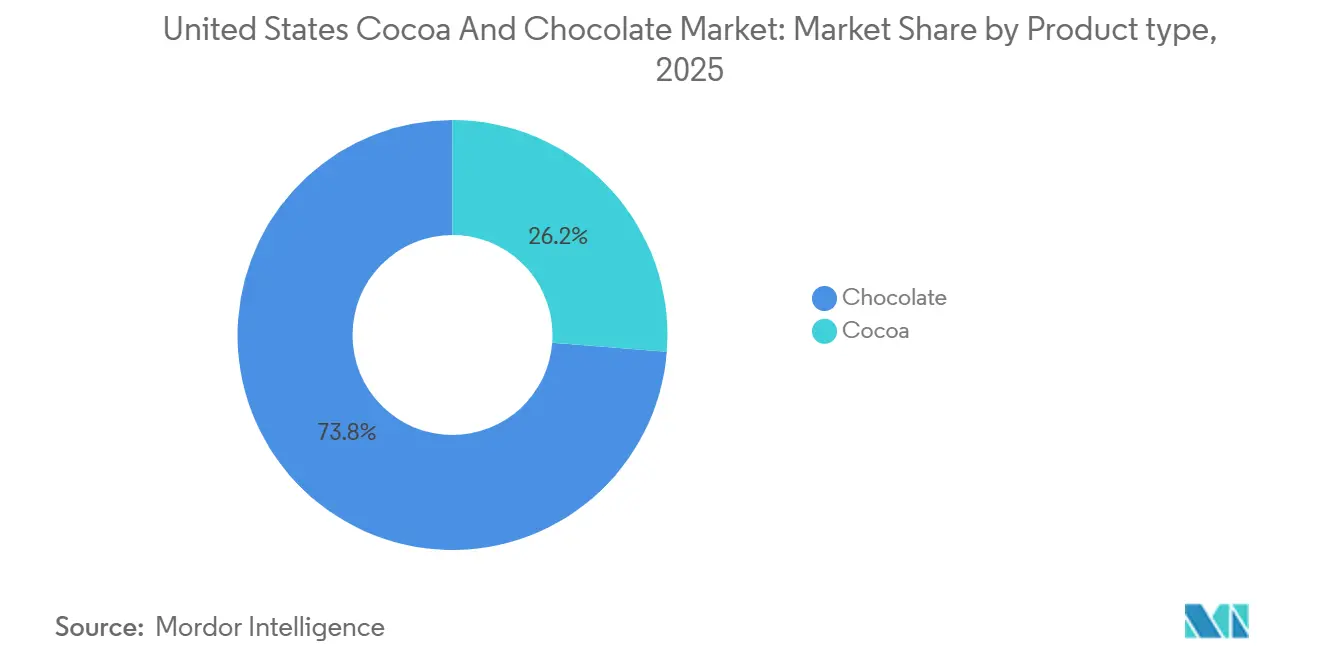

- By product type, chocolate held 73.68% of the US cocoa and chocolate market share in 2025, while cocoa is projected to expand at a 5.81% CAGR from 2026 to 2031.

- By distribution channel, retail accounted for 62.36% of the US cocoa and chocolate market share in 2025, while foodservice is forecast to grow at a 6.08% CAGR through 2031.

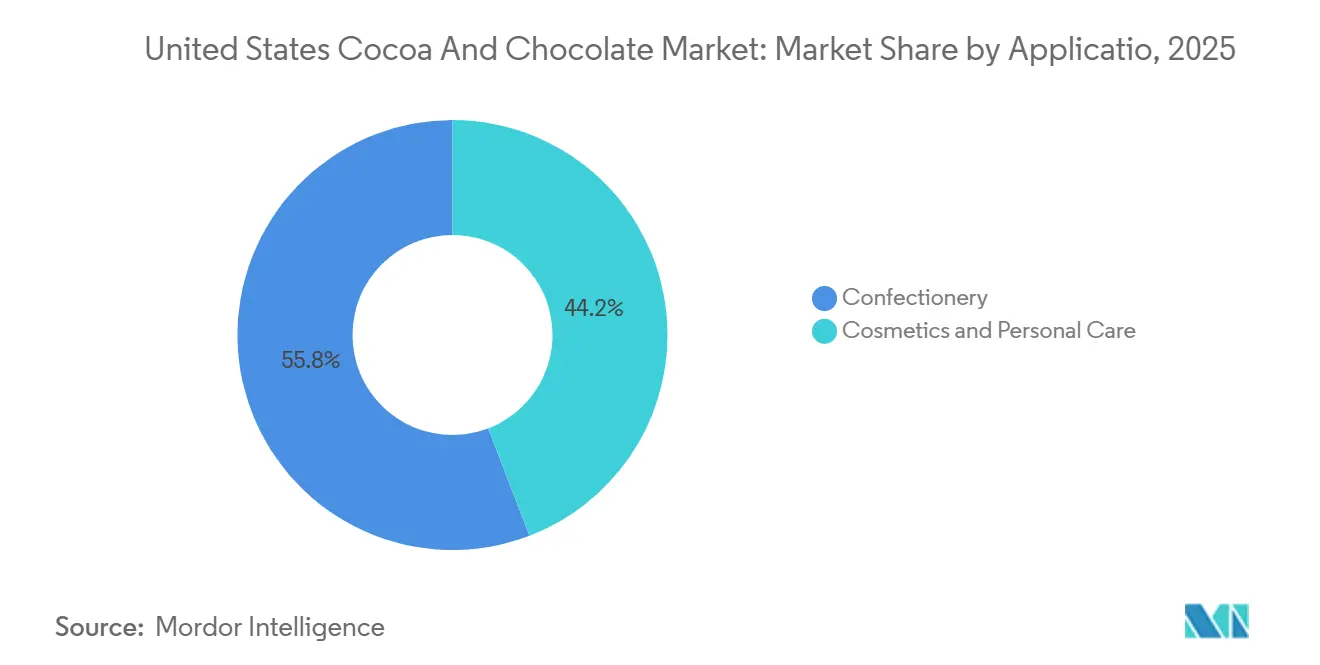

- By application, confectionery captured 55.82% of revenue in 2025, while the cosmetics and personal care segment is projected to record the fastest growth at a 5.92% CAGR through 2031.

- By nature, conventional products represented 91.36% of sales in 2025, while organic products are expected to advance at a 6.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Cocoa And Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Demand for Premium and Dark Chocolate Variants | +1.2% | National, with above-average traction in the Northeast, the Pacific Coast, and major metro markets | Medium term (2–4 years) |

| Growing Popularity of Clean-Label and Organic Chocolate Products | +0.8% | National; concentrated in the Pacific Coast, the Mountain West, and college towns | Long term (≥ 4 years) |

| Increasing Gifting Culture and Seasonal Sales Peaks | +0.7% | National, with a higher absolute contribution from the South and Midwest (the highest seasonal volume) | Short term (≤ 2 years) |

| Innovation in Flavor Profiles and Formats | +0.6% | National: fastest uptake in Northeast and West Coast urban centers | Medium term (2–4 years) |

| Expansion of Craft Bean-to-Bar Micro-Manufacturers Driving Local Sourcing | +0.4% | Pacific Coast, Northeast, and select Sunbelt metro markets | Long term (≥ 4 years) |

| Corporate Wellness Programs Adopting Dark Chocolate as Functional Snacks | +0.3% | National, with early gains in tech-hub metro areas | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Premium and Dark Chocolate Reformulating the Category

Rising consumer demand for premium and dark chocolate variants is significantly driving the United States cocoa and chocolate market by increasing demand for high-cocoa-content ingredients, premium confectionery products, and ethically sourced cocoa formulations. Dark chocolate consumption has accelerated due to growing consumer preference for indulgent products perceived as healthier and richer in cocoa content. According to the National Confectioners Association, U.S. confectionery sales reached a record USD 55 billion in 2025, with premium chocolate remaining one of the strongest-performing categories across retail channels[1]Source: National Confectioners Association, "Confectionery Sales Climb to $55 Billion in 2025", candyusa.com. Additionally, a 2025 U.S. chocolate industry forecast noted that 67% of consumers purchased premium chocolate products, while nearly 30% preferred premium variants over standard offerings. Rising premium demand has encouraged manufacturers to expand dark chocolate portfolios and strengthen cocoa sourcing strategies. In 2024, Lindt & Sprüngli expanded premium dark chocolate assortments in North America, while in 2025, The Hershey Company reformulated selected chocolate products with higher cocoa-content dark chocolate variants following strong premium consumer demand. By 2026, manufacturers, including Barry Callebaut, increased investments in traceable cocoa sourcing and premium chocolate innovation as U.S. retail chocolate prices rose 14% in early 2026, reflecting continued consumer willingness to spend on premium and dark chocolate products despite elevated cocoa costs.

Growing Popularity of Clean-Label and Organic Chocolate Products

The growing popularity of clean-label and organic chocolate products is driving the United States cocoa and chocolate market as consumers increasingly seek chocolates made without artificial flavors, preservatives, synthetic emulsifiers, or genetically modified ingredients. Demand is particularly rising among younger consumers prioritizing sustainability, ingredient transparency, and certified organic sourcing. According to the Organic Trade Association, U.S. organic food sales surpassed USD 70 billion in 2025, with organic snacks and confectionery among the fastest-expanding packaged food categories[2]Source: Organic Trade Association, "Organic Trade Association reports sales of organic products at USD 76.6 billion, with growth rate double that of overall marketplace", ota.com. Additionally, the United States Department of Agriculture reported continued growth in certified organic processed food manufacturing and cocoa ingredient imports, supporting premium chocolate production. In 2024, Theo Chocolate expanded organic and fair-trade chocolate assortments with simplified ingredient formulations targeting health-conscious consumers. During 2025, Alter Eco introduced regenerative organic certified dark chocolate products using traceable cocoa sourcing and compostable packaging solutions to strengthen clean-label positioning in the U.S. retail market. By 2026, chocolate manufacturers increasingly partnered with certified sustainable cocoa cooperatives and invested in transparent sourcing technologies, while retailers expanded shelf space for USDA Organic and non-GMO chocolate products as demand for ethically produced and minimally processed confectionery continued strengthening across the United States.

Innovation in Flavor Profiles and Formats

Innovation in flavor profiles and product formats is significantly driving the United States cocoa and chocolate market as manufacturers introduce globally inspired ingredients, layered textures, seasonal varieties, and snack-oriented formats to attract younger consumers and premium buyers. Consumers are increasingly seeking experiential confectionery products featuring combinations such as sea salt caramel, chili-infused dark chocolate, exotic fruits, matcha, espresso, and nut-based inclusions, alongside formats including bite-sized chocolates, filled bars, chocolate clusters, and portable snack packs. According to the National Confectioners Association, U.S. confectionery sales reached USD 55 billion in 2025, with chocolate accounting for USD 28.4 billion, or 51.7% of total confectionery sales, reflecting strong consumer engagement with innovative chocolate products. In 2024, Blommer Chocolate Company launched “Elevate,” a cocoa butter alternative designed for flexible confectionery formulations during cocoa price volatility, enabling innovation in coatings and compound chocolate applications. During 2025, premium chocolate brands expanded limited-edition seasonal assortments and fusion-flavor collections targeting gifting and indulgence occasions. Furthermore, manufacturers are keen on shifting back toward higher cocoa-content and authentic chocolate recipes as cocoa prices stabilize, supporting renewed investments in premium flavor innovation, artisanal textures, and differentiated chocolate formats across the United States market.

Expansion of Craft Bean-to-Bar Micro-Manufacturers Driving Local Sourcing

The expansion of craft bean-to-bar micro-manufacturers is driving local sourcing trends in the United States cocoa and chocolate market by increasing demand for traceable cocoa beans, small-batch production, and regionally differentiated chocolate products. Consumers are increasingly favoring artisan chocolate brands that emphasize direct trade sourcing, ethical cocoa procurement, transparency, and unique origin-specific flavor profiles. The bean-to-bar movement has also strengthened local manufacturing ecosystems by encouraging domestic roasting, refining, packaging, and specialty retail operations. According to industry estimates highlighted by the Fine Chocolate Industry Association and artisan chocolate producers, the number of small-scale bean-to-bar chocolate makers in North America has continued expanding as consumers shift toward premium handcrafted chocolate products and transparent sourcing practices. In 2024, several independent craft chocolate companies expanded direct sourcing partnerships with cocoa cooperatives in Latin America and Africa to secure traceable cocoa supplies and improve quality consistency. During 2025, Seattle-based craft manufacturers, including Spinnaker Chocolate and Cocoa Legato, expanded production facilities, café concepts, and educational tasting programs following rising demand for artisan bean-to-bar chocolate experiences in the United States. Continued volatility in industrial cocoa supply chains and consumer dissatisfaction with reformulated mass-market chocolate products further accelerated demand for premium bean-to-bar brands using higher cocoa content and authentic ingredient sourcing strategies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Cocoa Bean Prices Affecting Processor Margins | -0.9% | Global supply chain; US processors and mid-tier brands are most exposed | Short term (≤ 2 years), with structural sensitivity persisting long term |

| Health Concerns Over Sugar and Calorie Content | -0.5% | National: highest impact in health-conscious metro markets | Long term (≥ 4 years) |

| ESG Scrutiny Over Supply-Chain Transparency Deterring Large Buyers | -0.4% | National, with spillover to global procurement decisions by US-headquartered MNCs | Medium term (2–4 years) |

| Impending Heavy-Metal (Cd/Pb) Limits Tightening Regulatory Risk | -0.3% | National, California (Prop 65) as a bellwether jurisdiction for federal action | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatility in Cocoa Bean Prices Affecting Processor Margins

Volatility in cocoa bean prices is significantly affecting processor margins and restraining the United States cocoa and chocolate market by increasing raw material procurement costs, reducing production predictability, and pressuring manufacturers to raise retail prices or reformulate products. According to the International Cocoa Organization, world cocoa production declined 12.9% year-over-year to 4.368 million tonnes in 2024/25, while the global cocoa supply deficit widened to 494,000 tonnes and end-of-season stocks fell 28% to 1.27 million tonnes. The ICCO further reported that cocoa prices exceeded USD 10,000 per metric ton during late 2024 and early 2025 due to weather disruptions, disease outbreaks, and lower harvests in Ghana and Côte d’Ivoire. These unprecedented price swings compressed processor margins across the United States, where manufacturers rely heavily on imported cocoa. In 2024, several U.S. chocolate companies introduced smaller pack formats and adjusted cocoa-content formulations to manage input inflation. During 2025, processors increased investments in supply-chain diversification and long-term sourcing contracts as U.S. chocolate prices continued rising. According to CoBank, U.S. retail chocolate prices increased 14.4% in early 2026 compared with 2025 levels as elevated cocoa procurement costs continued affecting manufacturers and consumers. By 2026, companies will have increasingly invested in cocoa-alternative ingredients, automation, and sustainable sourcing partnerships to stabilize margins amid continuing commodity price uncertainty.

Health Concerns Over Sugar and Calorie Content

Health concerns over sugar and calorie content are increasingly restraining the United States cocoa and chocolate market as consumers shift toward reduced-sugar snacks, portion-controlled confectionery, and functional alternatives with cleaner nutritional profiles. According to the “USDA Sugar: World Markets and Trade (May 2025)” report published by the United States Department of Agriculture in May 2025, U.S. sugar consumption reached 11.02 million metric tons in 2024/2025 and is projected to remain at 11.02 million metric tons in 2025/2026, reflecting sustained scrutiny over sugar intake and its impact on processed food categories, including confectionery products[3]Source: United States Department of Agriculture, "Sugar and Sweeteners Outlook: December 2025", ers.usda.gov. Rising public awareness regarding obesity, diabetes, and calorie-dense diets has encouraged consumers to moderate traditional chocolate consumption and prioritize lower-sugar offerings. In 2024, ChocZero expanded monk-fruit-sweetened chocolate products targeting keto and diabetic consumers, while Hu Kitchen strengthened clean-label dark chocolate assortments with simplified ingredient formulations. During 2025, manufacturers increasingly introduced portion-controlled packs, protein-infused chocolate snacks, and low-glycemic chocolate variants across U.S. retail channels. By 2026, chocolate companies accelerated investments in natural sweeteners, reduced-calorie cocoa formulations, and functional confectionery innovations as health-conscious purchasing behavior continued reshaping mainstream chocolate demand in the United States market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chocolate's Scale Masks Cocoa's Faster Structural Growth

Chocolate held a commanding 73.68% share of the US cocoa and chocolate market in 2025, while the cocoa segment is projected to post a 5.81% CAGR over 2026–2031. Chocolate accounts for the largest share in the United States cocoa and chocolate market due to its widespread consumption across confectionery, bakery, seasonal gifting, and snack applications, supported by strong retail penetration and continuous premium product innovation. According to the National Confectioners Association, chocolate represented USD 28.4 billion, or 51.7% of total U.S. confectionery sales in 2025, reflecting sustained consumer demand across dark, milk, filled, and premium chocolate categories. In 2025, Ferrero North America expanded manufacturing capacity and seasonal chocolate product launches in Illinois to strengthen U.S. retail supply, while in 2026, premium brands accelerated limited-edition flavor launches, gifting assortments, and experiential retail concepts to increase chocolate category sales and consumer engagement nationwide.

The cocoa segment is the fastest-growing category due to rising demand for cocoa powder, cocoa butter, and cocoa liquor in beverages, bakery, nutraceuticals, and clean-label food formulations. According to the United States Department of Agriculture, U.S. imports of cocoa beans and semi-processed cocoa ingredients increased during 2025 as domestic processors expanded sourcing to support industrial food and beverage applications. In 2025, Cargill expanded cocoa-processing and sustainable sourcing initiatives supporting North American manufacturers, while 2026 witnessed greater investments in specialty cocoa ingredients, high-flavanol cocoa powders, and traceable cocoa solutions targeting functional beverages, dairy products, and premium health-focused applications across the United States market.

By Distribution Channel: Foodservice Gaining Structural Share from Evolving Consumption Patterns

Retail captured 62.36% of the US cocoa and chocolate market by value in 2025, while foodservice is the fastest-growing distribution channel at a projected 6.08% CAGR over 2026–2031. Retail accounts for the largest share in the United States cocoa and chocolate market due to extensive product availability across supermarkets, convenience stores, specialty retailers, and e-commerce platforms, alongside strong seasonal and impulse-driven chocolate purchasing trends. According to the National Confectioners Association, U.S. confectionery sales reached USD 55 billion in 2025, with supermarkets and mass retail channels contributing the majority of chocolate purchases during seasonal events such as Valentine’s Day, Easter, and Halloween. Moreover, innovative product launches are further supporting the market's growth. In 2025, Lindt & Sprüngli expanded premium Lindor and Excellence retail assortments across U.S. grocery and specialty channels, while during 2026, retailers increased investments in personalized online chocolate gifting, premium seasonal collections, and omnichannel fulfillment capabilities to strengthen direct consumer engagement and premium chocolate accessibility nationwide.

The foodservice segment is the fastest-growing category due to rising demand for premium desserts, café beverages, artisanal bakery products, and chocolate-based menu innovation across restaurants, cafés, and hospitality venues. The National Restaurant Association projected U.S. restaurant industry sales to surpass USD 1.5 trillion in 2025, supported by growing consumer spending on experiential dining and premium indulgence products. In 2024, Guittard Chocolate Company expanded foodservice chocolate offerings for bakeries and specialty cafés, while during 2025–2026 manufacturers introduced barista-focused cocoa beverages, premium baking chocolate formats, and chef collaboration programs targeting hotels, restaurants, and artisan dessert chains across the United States foodservice market.

By Application: Confectionery Anchors Volume as Cosmetics and Nutraceuticals Drive Margin

Confectionery accounted for 55.82% of the US cocoa and chocolate market by application in 2025, while the cosmetics and personal care is the fastest-growing application segment at a projected 5.92% CAGR over 2026–2031. The confectionery segment accounts for the largest share in the United States cocoa and chocolate market due to strong year-round consumer demand for chocolate candies, seasonal gifting products, snack bars, and impulse purchases across mass retail channels. The National Confectioners Association reported in 2025 that chocolate remained the leading confectionery category during major seasonal events, including Halloween, Valentine’s Day, and Easter, which collectively drive billions of dollars in U.S. confectionery sales annually. In 2025, Ferrero expanded Kinder and Ferrero Rocher seasonal assortments and invested in North American manufacturing capabilities, while in 2026, manufacturers accelerated limited-edition flavors, nostalgic confectionery launches, and premium gifting collections to strengthen consumer engagement and increase chocolate confectionery sales across supermarkets, convenience stores, and online retail platforms.

The cosmetics and personal care segment is the fastest-growing application due to the rising use of cocoa butter, cocoa polyphenols, and antioxidant-rich chocolate ingredients in skincare, haircare, and wellness formulations. According to the Personal Care Products Council, demand for plant-based and naturally derived cosmetic ingredients continued increasing across the U.S. beauty industry during 2025 as consumers favored clean-label personal care products. In 2024, Lush Cosmetics expanded cocoa butter-based body care formulations in North America, while during 2025–2026 beauty manufacturers increased partnerships with sustainable cocoa suppliers and launched chocolate-inspired skincare masks, moisturizers, and lip-care products emphasizing natural emollient and antioxidant benefits to capitalize on rising demand for botanical and food-derived cosmetic ingredients in the United States market.

By Nature: Conventional Dominance Intact as Organic Builds a Durable Premium Lane

The conventional cocoa and chocolate segment accounts for the largest share in the United States cocoa and chocolate market due to its broad affordability, large-scale industrial availability, and extensive use across confectionery, bakery, dairy, and beverage applications. Conventional cocoa ingredients dominate mass-market chocolate manufacturing because they provide stable supply volumes and lower production costs compared to certified organic alternatives. According to the United States Department of Agriculture, U.S. imports of cocoa beans, cocoa paste, and cocoa powder continued increasing during 2025 to support large-scale food manufacturing and confectionery production requirements. In 2025, Blommer Chocolate Company expanded industrial chocolate solutions and ingredient supply capabilities for North American food manufacturers, while during 2026, major processors increased automation and production-efficiency investments to strengthen conventional cocoa processing capacity and maintain pricing competitiveness across mainstream retail and foodservice channels.

The organic cocoa and chocolate segment is the fastest-growing category due to rising consumer preference for clean-label, pesticide-free, ethically sourced, and sustainably certified chocolate products. The Organic Trade Association reported in 2025 that U.S. organic food sales surpassed USD 70 billion, with organic snack and confectionery categories continuing to expand as consumers prioritized ingredient transparency and sustainability. In 2024, Equal Exchange expanded organic and fair-trade chocolate offerings sourced from farmer cooperatives, while during 2025–2026, manufacturers introduced USDA Organic dark chocolate bars, regenerative cocoa sourcing partnerships, and eco-friendly packaging initiatives to strengthen premium organic chocolate positioning across specialty retail and online distribution channels in the United States market.

Geography Analysis

The Northeast region leads the United States cocoa and chocolate market due to its dense concentration of premium confectionery brands, specialty retailers, and high consumer spending on artisanal and seasonal chocolates. According to the National Confectioners Association, the Northeast remains one of the country’s strongest premium chocolate consumption regions, driven by urban gifting and specialty retail demand. During 2025, Ferrero North America expanded premium seasonal product distribution across northeastern retail chains, while 2026 witnessed further growth in luxury chocolate boutiques, experiential chocolate cafés, and direct-to-consumer gifting platforms in cities such as New York and Boston.

The Midwest region is a major manufacturing and processing hub for the United States cocoa and chocolate market due to its established food-processing infrastructure, logistics connectivity, and concentration of industrial confectionery operations. The United States Department of Agriculture highlighted continued growth in processed food manufacturing activity across Midwestern states during 2025, supporting confectionery ingredient production and chocolate distribution. In 2025, The Hershey Company expanded operational efficiency investments in manufacturing facilities serving central U.S. markets, while during 2026, regional processors accelerated automation and sustainable packaging initiatives to improve production scalability and supply-chain efficiency across large-volume chocolate operations.

The Western and Southern United States are witnessing faster growth due to rising demand for organic, functional, and premium cocoa products alongside expanding café culture and multicultural flavor innovation. The Organic Trade Association reported continued expansion in organic packaged food sales across Western states during 2025, supporting demand for clean-label chocolate products. In 2025, Theo Chocolate strengthened the distribution of organic and fair-trade chocolate products across Western specialty retailers, while 2026 saw increased investments in plant-based cocoa beverages, Mexican-inspired chocolate flavors, and premium dessert collaborations across hospitality and café chains in California, Texas, and Florida.

Competitive Landscape

The US cocoa and chocolate market is moderately consolidated at the mass tier, with Mars Incorporated, The Hershey Company, and Mondelez International exercising significant control over retail shelf space and seasonal confectionery allocation. Leading players focused on premiumization, clean-label reformulation, and seasonal product innovation to strengthen market positioning amid rising cocoa costs and changing consumer preferences. Mars expanded premium Galaxy and Dove chocolate assortments, while Hershey accelerated investments in supply-chain optimization and reduced-sugar confectionery offerings targeting health-conscious consumers across mass retail and e-commerce channels.

Competition is increasingly centered on sustainability, traceable cocoa sourcing, and operational efficiency as manufacturers respond to cocoa supply volatility and stricter consumer expectations regarding ethical sourcing. The National Confectioners Association highlighted in 2025 that sustainability and ingredient transparency remained among the industry’s most important strategic priorities. During 2025, Mondelez International expanded Cocoa Life sustainability initiatives supporting cocoa-farming communities and traceable sourcing systems, while Barry Callebaut strengthened partnerships with North American food manufacturers through sustainable cocoa ingredient solutions and clean-label chocolate formulations targeting premium applications.

Market participants are also strengthening competitive differentiation through acquisitions, manufacturing modernization, and experiential retail strategies. In 2025, Ferrero Group expanded North American production and distribution capabilities to increase penetration across premium chocolate and seasonal confectionery categories. Furthermore, craft and premium manufacturers, including Theo Chocolate and specialty bean-to-bar producers, increased direct-to-consumer expansion, café-based retail concepts, and organic chocolate innovation to compete through authenticity, ethical sourcing, and premium artisanal positioning within the evolving United States cocoa and chocolate market.

United States Cocoa And Chocolate Industry Leaders

-

Mars, Incorporated

-

The Hershey Company

-

Mondelez International

-

Ferrero Group

-

Lindt & Sprüngli AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Mars announced a USD 2 billion investment in US manufacturing facilities in 2026, as part of a broader global manufacturing expansion coinciding with its December 2025 merger with Kellanova. The US investment signals an intent to absorb Kellanova's snacking manufacturing assets into a unified production platform.

- April 2026: Mondelēz International partnered with Israeli startup Celleste Bio to develop the world's first chocolate bars made with cell-cultivated cocoa butter. The partnership targets regulatory dossier submission in the US, EU, Israel, and the UK, with market readiness aimed for 2027.

- April 2026: Mars and Olam Food Ingredients (ofi) launched a five-year net zero cocoa programme in Ecuador, covering 960+ farmers across six provinces and 9,000+ hectares, with a focus on regenerative agroforestry and low-carbon fertilization.

United States Cocoa And Chocolate Market Report Scope

Cocoa is the raw, processed bean harvested from the cacao tree. Chocolate is the final food product made by combining cocoa solids and butter with sugar and milk. The United States cocoa and chocolate market is segmented by product type, distribution channel, application, and nature. By product type, the market is segmented into cocoa and chocolate. The cocoa segment is further sub-segmented into cocoa butter, cocoa powder, cocoa liquor, and cocoa nibs. The chocolate segment is further sub-segmented into dark chocolate, milk/white chocolate, and filled/compound chocolate. By distribution channel, the market is segmented into foodservice and retail. The retail segment is further sub-segmented into supermarkets/hypermarkets, convenience stores, online retail stores, specialty stores, and others. By application, the market is segmented into confectionery, bakery, dairy, beverages, cosmetics and personal care, pharmaceuticals and nutraceuticals, and other applications. By nature, the market is segmented into conventional and organic.

| Cocoa | Cocoa Butter |

| Cocoa Powder | |

| Cocoa Liquor | |

| Cocoa Nibs | |

| Chocolate | Dark Chocolate |

| Milk/White Chocolate | |

| Filled/Compound Chocolate |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Specialty Stores | |

| Others |

| Confectionery |

| Bakery |

| Dairy |

| Beverages |

| Cosmetics and Personal Care |

| Pharmaceuticals and Nutraceuticals |

| Other Applications |

| Conventional |

| Organic |

| Product Type | Cocoa | Cocoa Butter |

| Cocoa Powder | ||

| Cocoa Liquor | ||

| Cocoa Nibs | ||

| Chocolate | Dark Chocolate | |

| Milk/White Chocolate | ||

| Filled/Compound Chocolate | ||

| Distribution Channel | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Specialty Stores | ||

| Others | ||

| Application | Confectionery | |

| Bakery | ||

| Dairy | ||

| Beverages | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals and Nutraceuticals | ||

| Other Applications | ||

| Nature | Conventional | |

| Organic | ||

Key Questions Answered in the Report

What is the current size of the US cocoa and chocolate market?

The US cocoa and chocolate market was valued at USD 37.21 billion in 2025 and is estimated at USD 38.01 billion in 2026, with a projected value reaching USD 46.39 billion by 2031.

What is driving growth in chocolate demand in the United States?

Growth is being supported by premium and dark chocolate demand, clean-label and organic preference, strong seasonal gifting, and new product formats across retail and foodservice.

Which product segment leads sales in the US cocoa and chocolate space?

Chocolate remained the leading product type with a 73.68% share in 2025, supported by confectionery demand, gifting occasions, and broad retail availability.

Which channel is growing fastest for cocoa and chocolate products in the US?

Foodservice is the fastest-growing channel, with a projected 6.08% CAGR from 2026 to 2031, as restaurants, cafés, and workplace foodservice add more cocoa-based items.

Page last updated on: