Hydroxyapatite Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.9 Billion |

| Market Size (2031) | USD 3.96 Billion |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

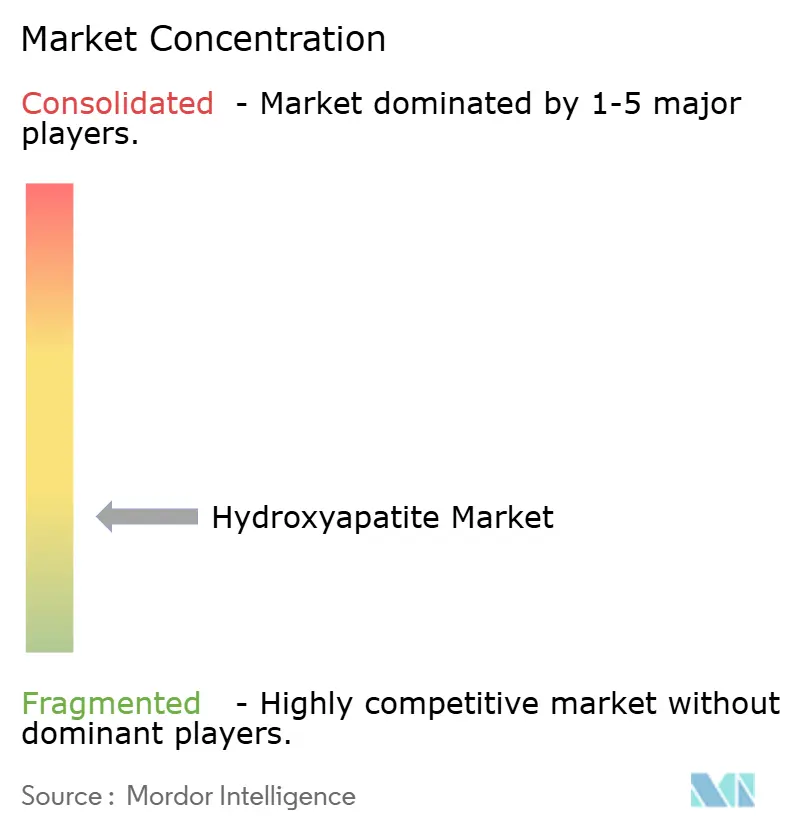

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydroxyapatite Market Analysis by Mordor Intelligence

The Hydroxyapatite Market size is projected to be USD 2.73 billion in 2025, USD 2.9 billion in 2026, and reach USD 3.96 billion by 2031, growing at a CAGR of 6.39% from 2026 to 2031. Aging populations in North America, Europe, and Japan are reshaping demand for osseointegrated dental and orthopedic implants that rely on hydroxyapatite’s biocompatibility, while regulators on both sides of the Atlantic are phasing out nickel- and cobalt-containing alloys in favor of calcium-phosphate ceramics. In craniofacial reconstruction, additive-manufacturing platforms are now producing patient-specific HA scaffolds with high porosity and compressive strength. This advancement has led to a significant reduction in theater time. Meanwhile, capacity expansions in China and Japan are broadening the global feedstock pool. However, premium margins continue to be concentrated in Europe and the United States. Here, factors such as ISO 13485 compliance, proprietary plasma-spray lines, and surgeon-education programs bolster pricing power.

Key Report Takeaways

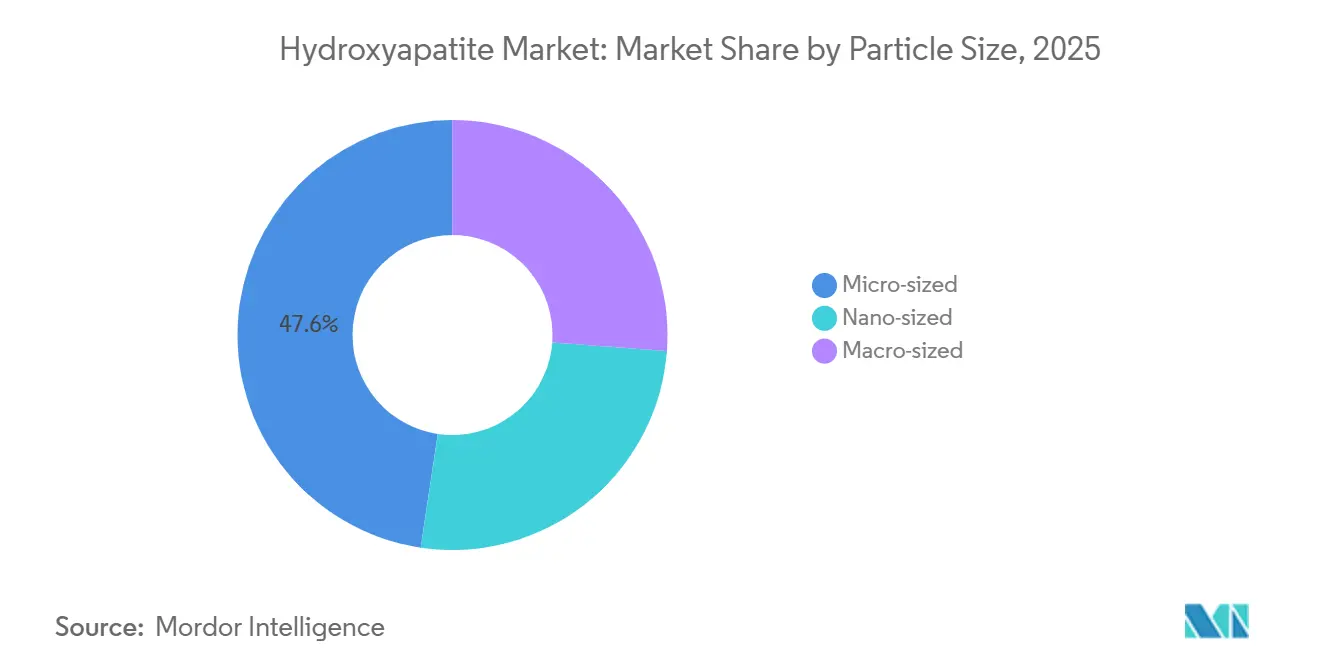

- By particle size, micro-sized grades held 47.65% of 2025 revenue, while nano-sized powders are projected to expand at a 7.09% CAGR between 2026 and 2031.

- By source, synthetic grades commanded 71.85% of the 2025 hydroxyapatite market size, and bio-derived alternatives are set to advance at a 6.83% CAGR over the same horizon.

- By form, powders represented 54.78% of 2025 demand, and coatings and pastes are on track for a 6.62% CAGR to 2031.

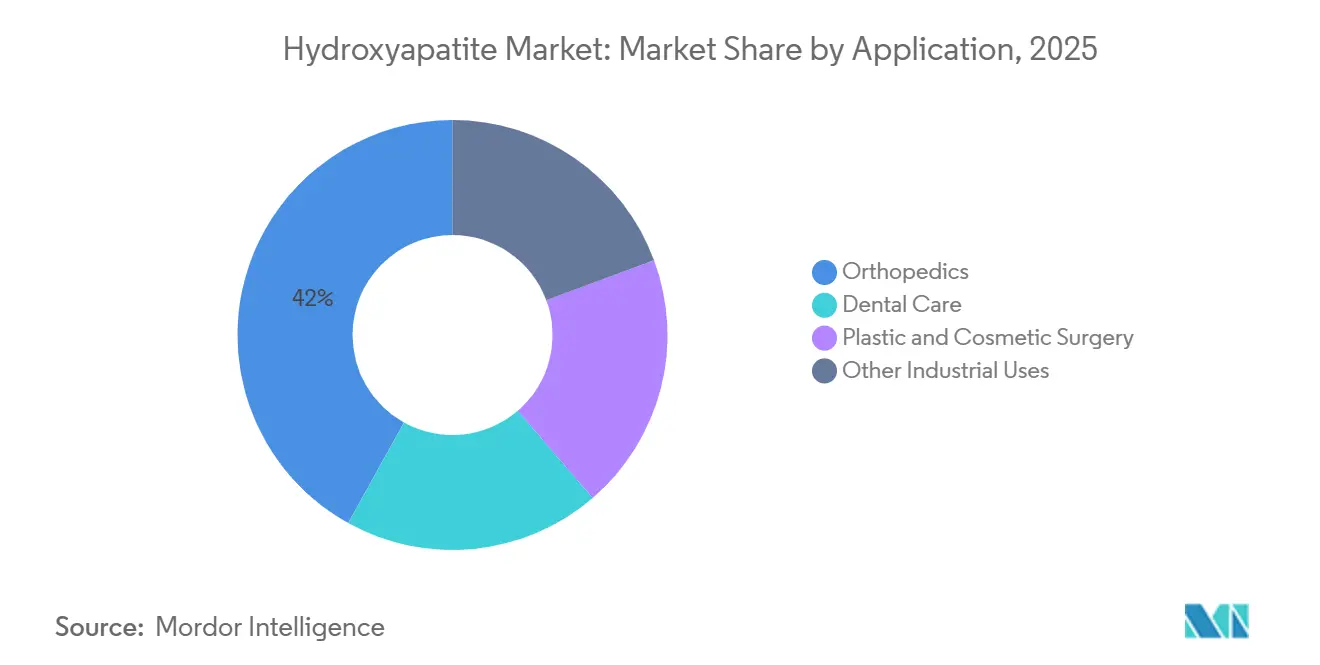

- By application, orthopedics retained 41.95% of the hydroxyapatite market share in 2025, whereas plastic and cosmetic surgery is forecast to deliver a 6.98% CAGR through 2031.

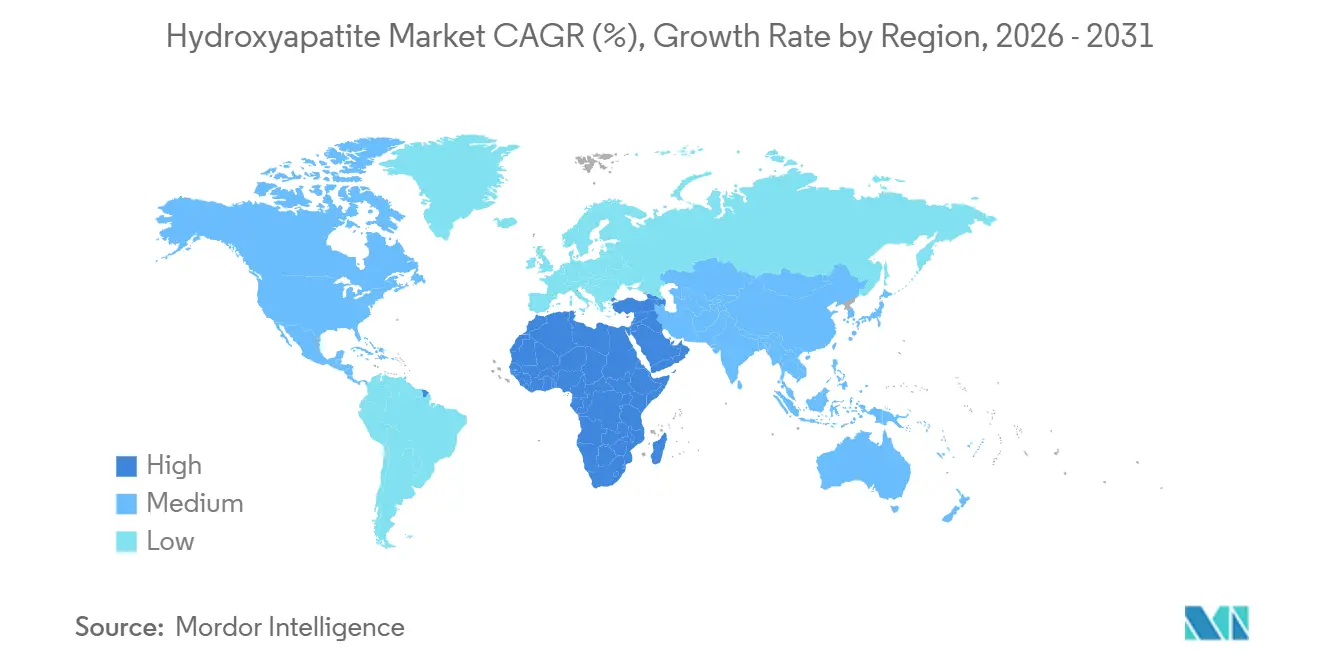

- By geography, Asia-Pacific captured 39.25% of the 2025 value; the Middle-East and Africa region shows the highest forecast CAGR at 6.47% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydroxyapatite Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dental-implant boom in aging economies | +1.8% | North America, Europe, Japan | Medium term (2-4 years) |

| Orthopedic implant volume growth | +2.1% | Global, with concentration in APAC and North America | Long term (≥4 years) |

| Biocompatibility advantage over metallic substitutes | +1.3% | Global, regulatory-driven in EU and North America | Medium term (2-4 years) |

| Government push for safer biomaterials | +0.9% | EU, North America, Japan | Long term (≥4 years) |

| 3D printing enabling patient-specific HA implants | +1.2% | North America, Europe, South Korea | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Dental-Implant Boom in Aging Economies

By 2027, over one-fifth of residents in Japan, Germany, and Italy will be aged 65 and older, spurring a demand for tooth replacements that leans towards HA-coated fixtures instead of removable dentures. Clinical studies indicate that HA-coated posts reduce healing time compared to their uncoated titanium counterparts[1]World Health Organization, “Global Health Observatory,” who.int. This advantage helps maintain their premium pricing in markets backed by reimbursements. Dental-device companies are now aiming for comparable success with mandibular implants. In April 2025, Japan expanded its insurance coverage for HA-coated dental fixtures, projecting an addition of procedures annually starting in 2028. Proactive clinics are now integrating HA coatings with digital dentistry processes, leading to reduced chair time and increased patient turnover. These trends bolster the Hydroxyapatite market, ensuring steady demand in affluent economies.

Orthopedic Implant Volume Growth

In 2025, the global count for hip and knee arthroplasties saw significant growth, with revisions constituting a notable portion of the total. Surgeons are increasingly opting for HA-integrated cages in spinal fusions, steering clear of iliac crest autografts. This choice not only slashes operating time by nearly 40 minutes but also diminishes the risk of infections. Injectable HA-collagen putties, such as moldable scaffolds for posterolateral fusion, have gained clinical trust. The Asia-Pacific region witnessed substantial growth in orthopedic device revenue, largely driven by a rise in elective procedures in China and India. This consistent growth in surgical volumes, paired with payers' growing acceptance of premium coatings, propels the Hydroxyapatite market forward.

Biocompatibility Advantage Over Metallic Substitutes

Calcium-phosphate ceramics dissolve at a pace synchronized with bone remodeling, bypassing the stress-shielding that afflicts titanium and cobalt-chrome implants. ISO 10993 panels repeatedly show lower cytotoxicity and sensitization for HA than for allergy-prone metals. Europe’s MDR 2017/745 requires enhanced surveillance of nickel- and cobalt-based devices, inadvertently steering hospitals toward HA-coated stems that present no hypersensitivity risk. Pediatric orthopedics is another beneficiary, as resorbable HA avoids long-term foreign-body retention around growth plates. With regulators intensifying scrutiny of metal allergens, the Hydroxyapatite market gains a durable advantage rooted in chemistry rather than branding.

3D Printing Enabling Patient-Specific HA Implants

With advancements in vat photopolymerization, direct-ink writing, and robocasting, HA scaffolds now boast controlled pore sizes and an ideal porosity for osteoblast migration. Custom craniofacial plates, crafted from CT data, have been shown to cut surgical time and reduce revision rates associated with poor fitment. South Korea’s Ministry of Food and Drug Safety approved patient-specific HA implants, highlighting growing regulatory confidence in layer-wise manufacturing. As the costs of printers decline, even mid-tier hospitals are embracing chairside planning for trauma reconstructions. This shift in workflow is poised to boost volumes in the Hydroxyapatite market, particularly for anatomically intricate cases where standard hardware falls short.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implant procedure cost | -0.8% | Global, acute in emerging markets without reimbursement | Medium term (2-4 years) |

| Stringent FDA and CE approvals | -0.6% | North America, Europe | Long term (≥4 years) |

| Toxicology debate on nano-HA in oral-care cosmetics | -0.4% | EU, North America, Japan | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Implant Procedure Cost and Regulatory Hurdles

In the U.S., single-tooth implants are expensive. Adding HA coatings further increases the component cost. This pricing structure often sidelines many Medicare beneficiaries, as routine dental care isn't federally covered. In orthopedics, revisions using HA grafts can significantly inflate hospital bills. Private insurers, however, closely monitor these costs, especially under bundled-payment models that target 90-day readmissions. Manufacturers face a hefty price tag for each 510(k) submission. This cost covers mechanical tests, biocompatibility panels, and sterility validations. Europe's MDR has extended CE-mark timelines, pushing back cash flows from product launches. These factors, combined with high surgical costs and extensive regulatory requirements, are dampening the short-term growth of the Hydroxyapatite market.

Toxicology Debate on Nano-Hydroxyapatite

In 2024, the EU Regulation 2024/858 set limits on nano-HA in toothpaste and mouthwash[2]EUR-Lex, “Regulation (EU) 2024/858,” europa.eu . Meanwhile, other jurisdictions have remained silent, leading to fragmented batch-segregation requirements. The SCCS raised concerns about aerosolized nano-HA, citing it as a potential inhalation hazard. In North America, consumer advocates are pushing for nano-labeling, which could unfairly tarnish certain oral-care products. In 2025, two European startups abandoned their nano-HA initiatives after insurers refused liability coverage, highlighting the stifling effect on innovation. Should upcoming toxicology studies validate concerns over pulmonary risks, we might see a tightening of medical-grade standards, which could modestly dampen the Hydroxyapatite market's outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Particle Size: Nano-Sized Powders Advance in Regenerative Surgery

Nano-sized powders are on track for a 7.09% CAGR through 2031, outpacing the average growth of the Hydroxyapatite market. This accelerated growth is attributed to their surface area, which enhances protein adsorption within just 48 hours. Periodontal surgeons utilize these powders in guided-tissue membranes, ensuring a bony fill instead of a fibrotic repair. Micro-sized grades, still dominant with 47.65% hydroxyapatite market share in 2025. Their packing densities enable them to achieve a compressive strength, making them ideal for hip stems and spinal cages.

Wet-precipitation plants, optimized for micro-powders, face challenges in maintaining nucleation. This limitation drives suppliers to invest in more expensive sol-gel or hydrothermal reactors. While ISO 13779-3 provides guidelines on particle-size assays, it falls short on performance thresholds, leaving buyers to establish their own specifications. Notably, nano-HA derived from Japanese scallop shells demonstrates impressive antimicrobial efficacy against Streptococcus mutans, suggesting its potential dual role in promoting bone growth and combating bacteria. Although the EU has imposed cosmetic caps, these regulations haven't yet extended to implants. However, ongoing studies on chronic inhalation could influence future regulations. As a result, there's a pronounced trend of adoption in specialized surgical channels, with expectations of a broader rollout in mainstream dental applications.

By Source: Synthetic Routes Hold Sway, Bio-Derived Grades Gain Momentum

Synthetic production claimed 71.85% of 2025 volume, reflecting the stringent control over the Ca/P ratio, all under the watchful eye of ISO 13485 quality systems. The wet precipitation method, operating between 60-90 °C, adeptly transforms calcium nitrate and diammonium phosphate. The resulting commodity grades are priced at FOB China. Meanwhile, sol-gel batches, boasting higher purity, cater to craniofacial markets where radiographic clarity is paramount.

Bio-derived hydroxyapatite is growing at a 6.83% CAGR. This growth is largely attributed to mandates promoting a circular economy and the osteogenic advantages of trace strontium and magnesium, both sourced from marine feeds. When calcined between 900-1,000 °C, eggshell waste produces a porous form of HA. On the other hand, coral-based variants, while boasting interconnected channels that expedite vascular ingrowth, grapple with supply constraints due to CITES regulations. Shell Apatite, a powder derived from Japanese scallops, made its debut in local dental clinics in 2025 and is now pursuing CE certification. However, the variability in mineral trace elements poses challenges in lot release, prompting innovators to turn to blockchain-style provenance logs for solutions. In summary, as sustainability credentials gain prominence, bio-routes are transitioning from being mere novelties to becoming foundational pillars in the Hydroxyapatite market.

By Form: Coatings and Pastes Outpace Commodity Powders

Plasma-sprayed coatings and injectable pastes are set for a 6.62% CAGR to 2031, riding orthopedic migration toward cementless fixation. Plasma deposition techniques produce HA layers with strong bond strength. This strength is underscored by the Oxford Cementless Partial Knee's impressive survival rate over a decade. Notably, pastes like NOVOSIS PUTTY achieved a higher fusion rate at the 12-month mark, surpassing the benchmark set by autografts.

Powders, though still 54.78% of 2025 sales, grapple with price pressures from Chinese exporters. Granules, positioned as tactile fillers for metaphyseal voids, strike a balance between free-flowing powders and thicker pastes. However, the industry faces capital hurdles: with plasma guns and heat-treat ovens priced significantly, it's clear why established players maintain a competitive edge. Electrophoretic deposition, while reducing temperature exposure, falls short on adhesion metrics. Furthermore, regulatory frameworks like ISO 13779-2 are expediting approvals for coatings, paving the way for broader adoption in revision arthroplasty and trauma hardware, thereby expanding the Hydroxyapatite market size.

By Application: Cosmetic Surgery Segment Accelerates

Plastic and cosmetic surgery is projected at a 6.98% CAGR through 2031. This growth is driven by the efficacy of calcium hydroxyapatite fillers, which not only maintain a volumetric lift for up to 24 months but also stimulate neocollagenesis. This feature effectively doubles the aesthetic durability compared to hyaluronic acid. In the realm of mid-face augmentation, Radiesse stands out as a dominant choice. Furthermore, clinics across the Asia-Pacific region are increasingly favoring combination therapy, especially when paired with micro-focused ultrasound.

Orthopedics, with 41.95% of 2025 revenue, remains the backbone of the Hydroxyapatite market size, supported by spinal fusion and revision arthroplasty where HA reduces aseptic loosening rates. Following closely is the dental care sector, which is poised to benefit from an estimated significant number of implant placements in 2025. These placements are divided between premium HA-coated screws and uncoated titanium options. While industrial niches like heavy-metal adsorption and chromatography command only single-digit market shares, they play a pivotal role in diversifying revenue streams, especially in light of medical pricing challenges.

Geography Analysis

Asia-Pacific contributed 39.25% of the 2025 share of global sales. China's wet-precipitation capacity offers commodity powders at prices significantly lower than their Western counterparts, making inroads into budget-conscious clinics in Southeast Asia. An insurance expansion in April 2025 for HA-coated dental implants in Japan is set to boost annual cases, benefiting domestic sol-gel suppliers like Matsumoto Koshou. In 2025, South Korea's regulators doubled the approvals for 3D-printed HA implants, showcasing their confidence in additive manufacturing. Meanwhile, India, despite witnessing growth in orthopedic devices in 2025, continues to prefer autografts in public hospitals, posing a challenge for HA vendors.

North America sees steady mid-single-digit growth, driven by innovations like patient-specific 3D prints, HA-collagen putties, and CaHA dermal fillers. Zimmer Biomet’s FDA-approved Oxford knee has set a new standard for coating durability, pushing competitors to enhance their offerings. While CMS's exclusion of routine dental implants limits their adoption among seniors, pilot bundled-payments might pave the way for reimbursing HA-coated fixtures, provided they maintain a complication rate within 90 days. In Canada, urban private clinics lean towards premium HA products, but rural hospitals often stick to uncoated metals, highlighting a divide in the provincial healthcare system. Mexico's push for near-shoring saw two multinationals establish HA-coating facilities in Monterrey in 2025.

Europe grapples with extended approvals under MDR 2017/745, yet its emphasis on biocompatibility resonates with HA's inherent advantages. High arthroplasty rates in Germany, the UK, and France account for a significant portion of Europe's HA demand. The Middle East and Africa, buoyed by Saudi Vision 2030's healthcare investment, is witnessing 6.47% CAGR growth. This financial push is motivating orthopedic OEMs to establish hubs in Riyadh, with public-private partnerships facilitating the creation of new hospitals that are keen on premium HA implants. South America, despite grappling with currency fluctuations, sees Brazil's sizable population as a potential market, especially once reimbursement models find stability.

Competitive Landscape

The hydroxyapatite market is fragmented. Regulatory barriers remain effective moats: newcomers must replicate multi-year ISO 13779 and ISO 10993 testing to secure 510(k) or CE marks. The EU’s nano-HA cosmetic cap spurred implant makers to commission inhalation studies, pre-emptively safeguarding latitude in particle-size specs. Overall, technology bifurcation—plasma lines versus additive printers—produces stratified rivalry, with large firms defending coating franchises and smaller innovators colonizing patient-specific and bio-circular sub-segments.

Hydroxyapatite Industry Leaders

Zimmer Biomet

KYOCERA Corporation

Medtronic

CAM Bioceramics

Fluidinova

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The Scientific Committee on Consumer Safety approved higher nano-hydroxyapatite concentration limits in cosmetics, removing regulatory barriers and enabling market growth in the European Union. Manufacturers can now use up to 29.5% in toothpaste and 10% in mouthwash, expanding premium oral care and skincare applications.

- November 2024: Zimmer Biomet's Oxford Cementless Partial Knee with hydroxyapatite coating has received FDA approval, marking a key advancement in cementless implant technology. The device ensures secure fixation without bone cement, simplifying surgery and enhancing patient outcomes.

Global Hydroxyapatite Market Report Scope

Hydroxyapatite (HAp) is a calcium phosphate similar to the human hard tissues in morphology and composition. It is a bioactive material that will support bone ingrowth and osseointegration. It has been used in orthopedic, dental, and maxillofacial applications and can be replaced with bone formation via osteoconduction.

The hydroxyapatite market is segmented by particle size, source, form, application, and geography. By particle size, the market is segmented into nano-sized, micro-sized, and macro-sized (greater than 1 µm). By source, the market is segmented into synthetic (wet, sol-gel, hydrothermal) and bio-derived (egg-shell, coral, bovine, fish-scale). By form, the market is segmented into powder, granules, and coatings and pastes. By application, the market is segmented into dental care, orthopedics, plastic and cosmetic surgery, and other industrial uses (catalysts, chromatography, water-treatment). The report also covers the market sizes and forecasts for the hydroxyapatite market in 18 countries across the globe. Each segment's market sizing and forecasts are based on value (USD).

| Nano-sized |

| Micro-sized |

| Macro-sized (greater than 1 µm) |

| Synthetic (wet, sol-gel, hydrothermal) |

| Bio-derived (egg-shell, coral, bovine, fish-scale) |

| Powder |

| Granules |

| Coatings and Pastes |

| Dental Care |

| Orthopedics |

| Plastic and Cosmetic Surgery |

| Other Industrial Uses (catalysts, chromatography, water-treatment) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Particle Size | Nano-sized | |

| Micro-sized | ||

| Macro-sized (greater than 1 µm) | ||

| By Source | Synthetic (wet, sol-gel, hydrothermal) | |

| Bio-derived (egg-shell, coral, bovine, fish-scale) | ||

| By Form | Powder | |

| Granules | ||

| Coatings and Pastes | ||

| By Application | Dental Care | |

| Orthopedics | ||

| Plastic and Cosmetic Surgery | ||

| Other Industrial Uses (catalysts, chromatography, water-treatment) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How big will the Hydroxyapatite market be by 2031?

It is projected to reach USD 3.96 billion by 2031, reflecting a 6.39% CAGR from USD 2.90 billion.

Which Hydroxyapatite form is growing the fastest?

Coatings and pastes lead growth at 6.62% CAGR, buoyed by plasma-spray adoption in cementless orthopedic implants.

Why are nano-sized Hydroxyapatite powders important?

Their more than 100 m²/g surface area speeds osteoblast adhesion, enabling 7.09% CAGR and widening use in periodontal and craniofacial repair.

Which region currently dominates sales?

Asia-Pacific held 39.25% of 2025 revenue thanks to China’s low-cost capacity and Japan’s sol-gel expertise.

What restrains wider Hydroxyapatite uptake in emerging markets?

High implant costs and complex 510(k)/CE approval pathways raise prices, curbing accessibility where reimbursement is absent.

Page last updated on: