Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

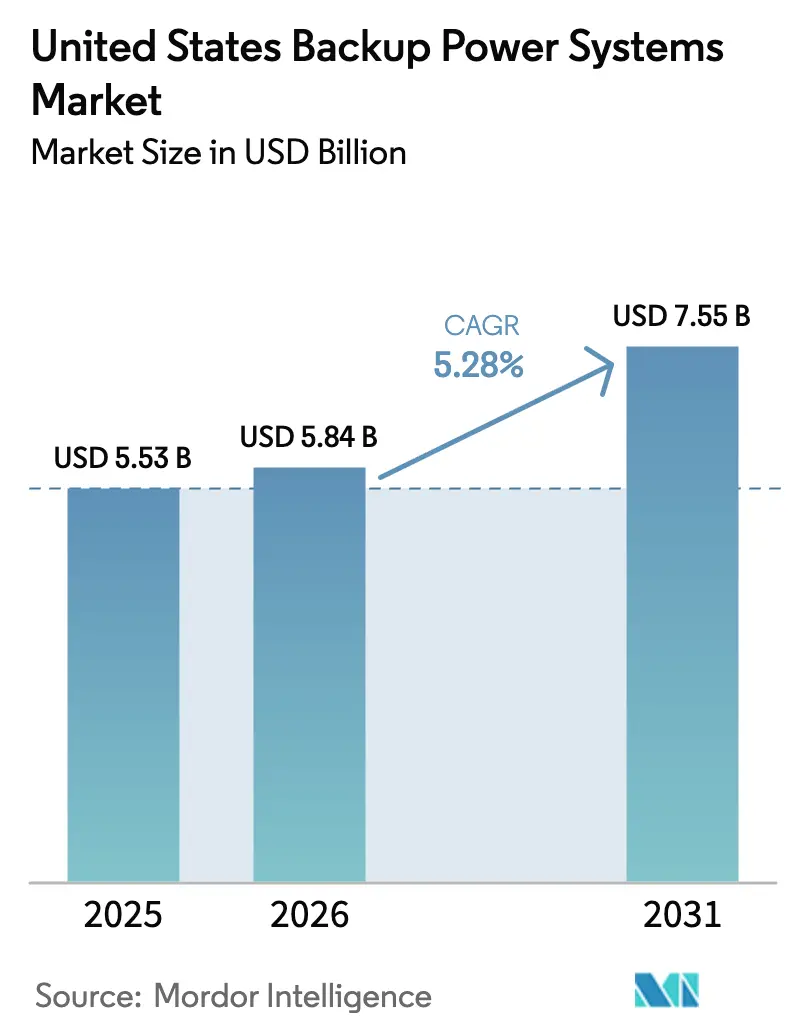

| Base Year Market Size (2025) | USD 5.53 Billion |

| Market Size (2026) | USD 5.84 Billion |

| Market Size (2031) | USD 7.55 Billion |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

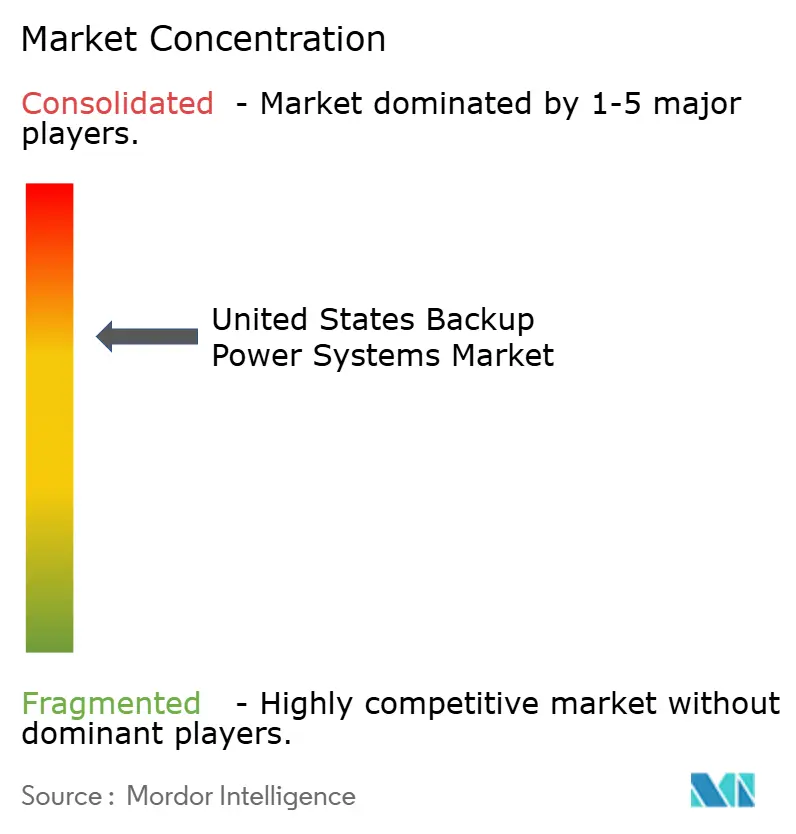

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Backup Power Systems Market Analysis by Mordor Intelligence

The United States Backup Power Systems Market size was valued at USD 5.53 billion in 2025 and is estimated to grow from USD 5.84 billion in 2026 to reach USD 7.55 billion by 2031, at a CAGR of 5.28% during the forecast period (2026-2031).

Aging transmission infrastructure, a 15% rise in sustained outages during 2024, and the commissioning of 23 gigawatts of new data-center standby generation in 2025 collectively underpin resilient demand. Fuel switching is underway as Tier 4 Final diesel‐emission costs lift natural-gas and hydrogen-ready adoption, while predictive-maintenance software is lowering whole-life service costs for fleets exceeding 500 units. Rental genset-as-a-service offerings are compressing margins for OEMs, but the sector continues to rely on standby power’s irreplaceable role in critical facilities where even brief outages can incur multi-million-dollar losses. These forces combine to drive a steady yet diversified growth trajectory for the United States backup power systems market.

Key Report Takeaways

- By technology, gas generators led with 40.2% revenue share in 2025, while fuel-cell backup platforms are forecast to grow at a 9.6% CAGR through 2031.

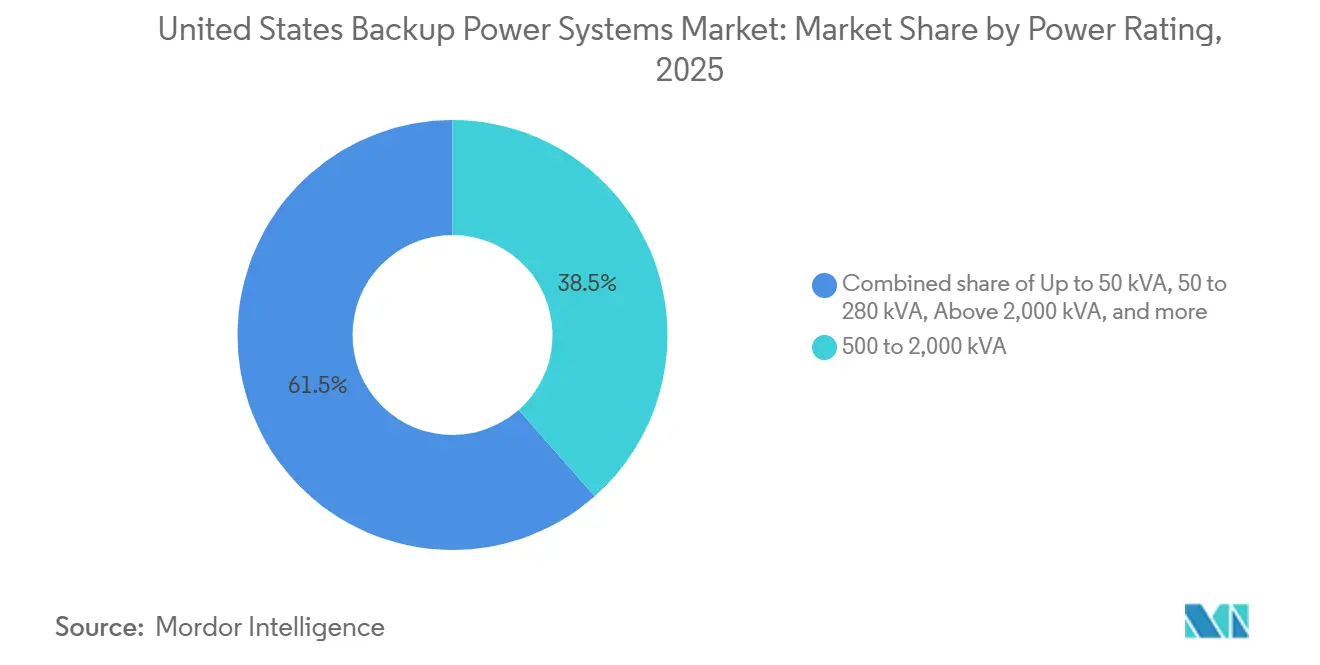

- By power rating, the 500-2,000 kVA segment held 38.5% of the United States backup power systems market share in 2025 and is advancing at a 5.8% CAGR to 2031.

- By application, standby and emergency systems captured a 49.9% share in 2025; off-grid and remote uses are projected to expand at an 8.5% CAGR to 2031.

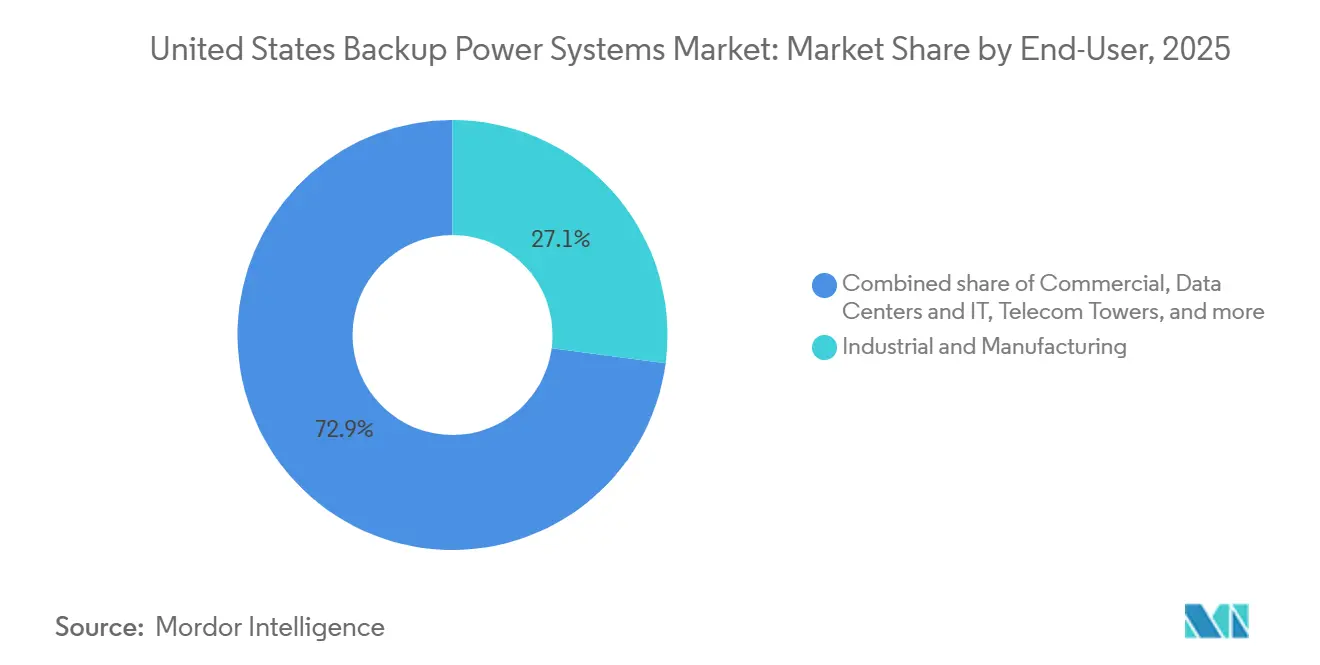

- By end user, industrial and manufacturing sites accounted for 27.1% of the United States backup power systems market size in 2025, while data centers are progressing at a 10.3% CAGR through 2031.

- Generac, Cummins, and Caterpillar together commanded roughly 55-60% of 2025 revenue, yet new entrants in fuel cells and hybrid genset-plus-storage solutions are eroding share through differentiated zero-emission offerings.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Backup Power Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing data-center footprint | 1.8% | National, concentrated in Northern Virginia, Oregon, Texas, Arizona | Medium term (2-4 years) |

| Severe grid-outage frequency & duration | 1.2% | National, acute in Gulf Coast, California wildfire zones, Northeast ice-storm corridors | Short term (≤ 2 years) |

| Growth of AI-enabled manufacturing lines | 0.7% | Midwest industrial belt, Southwest semiconductor clusters | Long term (≥ 4 years) |

| Electrification of critical healthcare assets | 0.5% | National, urban hospital systems and rural critical-access facilities | Medium term (2-4 years) |

| Mandatory resiliency codes for commercial buildings | 0.6% | Coastal states (Florida, North Carolina, New York), California seismic zones | Short term (≤ 2 years) |

| AI-driven predictive-maintenance platforms unlock TCO savings | 0.4% | National, early adoption in large industrial and data-center portfolios | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Data-Center Footprint

Hyperscale operators commissioned 11 gigawatts of additional white-space in 2025, prompting 23 gigawatts of redundant onsite generation to satisfy N+1 and 2N topologies.[1]U.S. Energy Information Administration, “Electric Power Monthly,” eia.gov Loudoun County added 1.2 gigawatts of diesel and gas sets, straining local air-quality compliance and catalyzing battery-assisted runtime pilots.[2]Dominion Energy, “Data Center Infrastructure,” dominionenergy.com Power-density escalation toward 50-60 kilowatts per rack now requires backup systems to stabilize voltage in milliseconds, elevating demand for hybrid UPS paired with quick-start gas turbines. Secondary hubs in Oregon and Texas are scaling because of renewable energy access and land availability, yet transmission congestion heightens the strategic value of onsite standby power.[3]Electric Reliability Council of Texas, “Grid Conditions Report,” ercot.com Collectively, these deployments embed long-term growth for the United States backup power systems market.

Severe Grid-Outage Frequency and Duration

The System Average Interruption Duration Index for investor-owned utilities rose 15% in 2024, reflecting extreme weather and equipment aging.[4]U.S. Energy Information Administration, “Electric Power Monthly,” eia.gov Hurricane events in Florida and Louisiana during the 2025 season caused outages averaging 72 hours, spurring insurers to mandate backup generation for policy renewal. California logged 38 days of Public Safety Power Shutoffs in 2025, with some circuits de-energized for 200-plus hours, thereby shifting backup economics from rarely used assets to frequently dispatched resources. Ice storms in Vermont and Maine triggered week-long blackouts, leading to state bills that offer tax credits on residential units above 10 kilowatts. The persistent nature of outages embeds backup power procurement into capital budgets across every vertical, reinforcing growth in the United States backup power systems market.

Growth of AI-Enabled Manufacturing Lines

Semiconductor fabs and EV battery plants now deploy equipment that fails if voltage sags exceed 5% or frequency drifts 0.1 hertz, necessitating rotary UPS or flywheel bridges for the 8-12 second genset start window. Intel’s Arizona fab added 120 megawatts of standby capacity in late 2025 to protect USD 150 million lithography tools from power anomalies. Domestic content rules in the Inflation Reduction Act accelerated six battery gigafactory groundbreakings in 2025, each specifying 30-45 minutes of full-load backup. Hydrogen fuel cells are in pilot use because they offer zero onsite emissions and share pipeline infrastructure with natural gas after minor retrofits. Continuous investment in AI-driven production environments raises the baseline need for resilient power and widens the addressable base for the United States backup power systems market.

Mandatory Resiliency Codes for Commercial Buildings

Hurricane-exposed states and seismic zones now embed standby power within updated building codes that require elevators, fire pumps, and egress lighting to run for 96 hours during outages. Florida, North Carolina, and New York implemented stricter provisions after the 2025 storm season, creating a compliance-driven surge in medium-sized gensets. Joint Commission standards for hospitals similarly enforce 96-hour runtime, prompting facility managers to renew older diesel fleets with Tier 4 Final or gas alternatives. Urban adoption is also growing as local ordinances limit noise, making low-NOx natural-gas sets and modular fuel cells attractive for downtown buildings. These statutory pressures ensure a predictable installation pipeline, materially benefiting the United States backup power systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening EPA emission caps (Tier 4 Final) | -0.9% | National, enforcement concentrated in non-attainment zones (California, Northeast) | Short term (≤ 2 years) |

| Rising interest-rates inflate capex for large gensets | -0.6% | National, acute impact on capital-intensive industrial and utility projects | Short term (≤ 2 years) |

| Lithium-ion fire-safety concerns in UPS rooms | -0.5% | National, heightened scrutiny in high-rise commercial buildings and legacy data centers | Medium term (2-4 years) |

| Capital-allocation shift toward on-site PV-plus-storage | -0.7% | Sunbelt states (California, Arizona, Texas, Florida), ITC-eligible projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening EPA Emission Caps

Tier 4 Final rules cap particulate matter at 0.03 g/kWh and NOx at 0.4 g/kWh, adding USD 8,000-15,000 per genset for after-treatment hardware. California’s Air Resources Board mandates extra filter regeneration cycles, lifting annual maintenance outlays 12-18%. Best Available Control Technology permitting extends diesel project timelines up to nine months in Los Angeles and the San Joaquin Valley, pushing buyers toward natural-gas and propane units that emit 60% less NOx. Secondary markets for used gensets weaken because non-compliant equipment cannot be resold, raising lifecycle costs. This dynamic trims near-term diesel demand, tempering growth for the United States backup power systems market.

Capital-Allocation Shift Toward On-Site PV-Plus-Storage

The Investment Tax Credit and declining battery prices make photovoltaic-coupled storage arrays financially attractive, diverting capex from large gensets in California, Arizona, Texas, and Florida. Commercial sites can offset 40-60% of annual load with solar, leaving backup duty for shorter durations that smaller gensets or batteries can handle. Rising interest rates added 180 basis points to genset financing between 2024 and 2025, widening the gap versus subsidized solar loans. Insurance incentives also favor carbon-free backup, further challenging diesel deployments. While PV-plus-storage cannot yet replace multi-day runtime in all applications, it constrains some addressable segments of the United States backup power systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Gas Generators Anchor Installations While Fuel Cells Accelerate

Gas generators captured 40.2% of 2025 revenue, reflecting widespread pipeline coverage to 77% of commercial sites and lower selective catalytic reduction costs compared with diesel. Fuel-cell platforms, although smaller today, are growing at a 9.6% CAGR in the United States backup power systems market size through 2031 because corporate net-zero pledges and California’s 2028 zero-emission mandate incentivize hydrogen and solid-oxide systems.

Diesel sets remain economical for code-minimum standby use where annual operation remains below 100 hours, yet Tier 4 compliance outlays and resale limitations are eroding share. Lithium-ion UPS dominates the sub-50 kVA tier that guards sensitive IT loads, while battery energy storage systems monetize demand-charge avoidance and ancillary-services revenue. Hybrid diesel-plus-battery packages are emerging in microgrids for military bases and remote industrial sites, cutting fuel burn by 30-40% and supporting the broader United States backup power systems market.

By Power Rating: Medium-Scale Units Balance Footprint and Redundancy

The 500-2,000 kVA class held 38.5% of the 2025 market and is set to rise 5.8% annually, underscoring its appeal for multi-tenant data halls and mid-sized factories that need N+1 redundancy without oversizing. Modular enclosures allow parallel operation in 500-kW increments, aligning capacity with demand ramps and preserving capital.

Above-2,000 kVA sets serve hyperscale campuses where 3-4 MW singles reduce interconnect complexity, but they face 12-18 month lead times for custom switchgear, tempering uptake. Units up to 50 kVA dominate residential demand and small commercial offices; natural-gas variants command 65% because of automatic transfer and unlimited runtime. The 50-280 kVA cohort protects retail, hospitality, and small clinics by covering refrigeration and life-safety loads, offering a three-to-five-year payback via avoided spoilage. This nuanced mix supports sustained volume in the United States backup power systems market.

By Application: Standby Leads, Off-Grid Gains with Rural 5G

Standby and emergency systems held 49.9% of the United States backup power systems market share in 2025, anchored by building codes and hospital life-safety rules. Off-grid and remote power is the fastest growing application at 8.5% CAGR, propelled by telecom carriers deploying 5G small cells where grid extension costs exceed USD 50,000 per mile.

Prime and continuous duty grows modestly as natural-gas price volatility and renewable incentives tilt economics toward grid-connected operations. Peak-shaving is a high-margin niche: battery arrays and fast-start turbines cut demand charges 15-30% and offer frequency-regulation revenue without jeopardizing standby readiness. Application boundaries blur as operators stack services, enabling a single asset to provide backup, demand response, and energy arbitrage, further broadening the United States backup power systems industry opportunity set.

By End User: Industrial Spending Dominates, Data Centers Expand Rapidly

Industrial and manufacturing facilities contributed 27.1% of 2025 revenue because unplanned shutdowns can cost up to USD 500,000 per hour. Data centers are the fastest-growing vertical at a 10.3% CAGR, reflecting AI training clusters that push rack densities beyond 50 kW and require 99.982% uptime.

Hospitals remain a steady buyer group under Joint Commission mandates for 96-hour runtime, though consolidation tempers absolute growth. Telecom towers need 5-10 kW units as 5G densification adds 15,000-20,000 sites annually, while residential installations now comprise 8% of shipments after multi-day storm outages disrupted remote work in 2025. Utilities and government facilities demand military-grade, multi-fuel sets for control centers and defense bases. These varied use cases diversify revenue streams inside the United States backup power systems market.

Geography Analysis

California's wildfire-related shutoffs and the nation's strictest emissions caps accelerate the adoption of natural-gas gensets, fuel cells, and large battery systems that offset diesel runtime. Texas combines rapid data-center buildout with an isolated grid, making onsite backup indispensable during cold snaps and heatwaves. Florida's hurricane exposure drives residential and commercial uptake, reinforced by insurer requirements following USD 42 billion of 2025 storm losses.

Northern Virginia added 1.2 gigawatts of data-center backup in 2025, challenging air-quality attainment and prompting utility-scale batteries that cut genset runtime. The Northeast grapples with ice storms and aging substations, spurring proposed residential tax credits in Vermont and Maine. Midwest industrial states rely on standby power to hedge against coal retirements and wind curtailments, whereas Arizona and Oregon emerge as secondary data hubs constrained by transmission limits.

Regional divergence in regulation and weather risk makes the United States backup power systems market both geographically balanced and opportunity-rich. Stringent emissions in California and the Northeast steer investment toward gas and zero-emission options, while diesel remains prevalent in cost-sensitive Sunbelt states. Population shifts into the South and West elevate demand where grid capacity lags, sustaining nationwide growth momentum.

Competitive Landscape

The top five suppliers hold roughly 55-60% revenue, giving the United States backup power systems market a moderate concentration yet leaving ample space for innovators. Generac, Cummins, and Caterpillar leverage broad service networks and vertical integration, but fuel-cell specialists and solar-plus-storage integrators are chipping away at legacy diesel strongholds. Generac’s 2025 acquisition of Electriq Power adds solar and batteries to its portfolio, while Cummins partnered with a hydrogen-electrolyzer firm to co-develop zero-carbon backup for data centers.

Smaller firms exploit the 50-280 kVA bracket by offering quiet, modular fuel cells that bypass urban noise ordinances. Rental providers are shifting to genset-as-a-service models enabled by predictive analytics that guarantee uptime and transfer ownership risk. AI-driven maintenance from Schneider Electric cuts unscheduled downtime up to 60%, lowering total cost and reducing churn.

Patent filings in fuel-cell durability and battery thermal management rose 28% to 340 in 2025, underscoring a pivot toward zero-emission architectures. Tesla’s entry with commercial Powerpacks combines backup and peak-shaving, challenging OEMs that lack advanced software and grid interconnection expertise. Competitive intensity is therefore moving from mechanical superiority to integrated energy-as-a-service platforms, reshaping the trajectory of the United States backup power systems market.

United States Backup Power Systems Industry Leaders

Eaton Corporation plc

Generac Holdings Inc.

Caterpillar Inc.

Cummins Inc.

Kohler Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Schneider Electric’s USD 2.3 billion U.S. data centre deals underscore the importance of robust backup power infrastructure, including UPS systems and power modules, to support AI-driven growth. Reliable power distribution and backup solutions are essential for ensuring resilience in U.S. AI and cloud facilities.

- November 2025: Cummins announced a USD 150 million expansion of its Minnesota gas-generator plant to serve hyperscale data-center demand.

- June 2024: Generac Power Systems acquired PowerPlay Battery Energy Storage Systems to expand its U.S. commercial and industrial backup power and energy storage portfolio. The integration of turnkey BESS solutions, with capacities up to 7 MWh, strengthens Generac’s ability to provide resilient on-site power for businesses facing grid instability or outages.

United States Backup Power Systems Market Report Scope

Backup power systems refer to systems that provide electricity when the primary power source fails or is interrupted. These systems are also known as emergency power systems. During power outages, they are designed to provide reliable power to critical loads, such as medical equipment, data centers, and telecommunication systems.

The US backup power systems market is segmented by technology, power rating, application, and end users. The market is segmented by technology into diesel generators, gas generators, UPS, BES, hybrid power, fuel-cell backup, and portable power stations. By power rating, the market is segmented into Up to 50 kVA, 50-280 kVA, 280-500 kVA, 500-2,000 kVA, and Above 2,000 kVA. By application, the market is segmented into standby/emergency, prime/continuous, peak shaving, and off-grid. By end users, the market is segmented into residential, commercial, industrial, data centres, healthcare, telecom, utilities, and government. Market sizing and forecasts have been done for each segment based on revenue (USD).

By Technology

| Diesel Generators |

| Gas Generators |

| Uninterruptible Power Supply (UPS) |

| Battery Energy Storage Systems (BESS) |

| Hybrid Power Solutions |

| Fuel-Cell Backup Systems |

| Portable Power Stations |

By Power Rating

| Up to 50 kVA |

| 50 to 280 kVA |

| 280 to 500 kVA |

| 500 to 2,000 kVA |

| Above 2,000 kVA |

By Application

| Standby/Emergency Power |

| Prime/Continuous Power |

| Peak Shaving and Load Management |

| Off-Grid and Remote Power |

By End-User

| Residential |

| Commercial (Retail, Offices, Hospitality) |

| Industrial and Manufacturing |

| Data Centers and IT |

| Healthcare Facilities |

| Telecom Towers |

| Utilities and Energy |

| Government and Defence |

| By Technology | Diesel Generators |

| Gas Generators | |

| Uninterruptible Power Supply (UPS) | |

| Battery Energy Storage Systems (BESS) | |

| Hybrid Power Solutions | |

| Fuel-Cell Backup Systems | |

| Portable Power Stations | |

| By Power Rating | Up to 50 kVA |

| 50 to 280 kVA | |

| 280 to 500 kVA | |

| 500 to 2,000 kVA | |

| Above 2,000 kVA | |

| By Application | Standby/Emergency Power |

| Prime/Continuous Power | |

| Peak Shaving and Load Management | |

| Off-Grid and Remote Power | |

| By End-User | Residential |

| Commercial (Retail, Offices, Hospitality) | |

| Industrial and Manufacturing | |

| Data Centers and IT | |

| Healthcare Facilities | |

| Telecom Towers | |

| Utilities and Energy | |

| Government and Defence |

Key Questions Answered in the Report

What is the current value of the United States backup power systems market?

The market was valued at USD 5.84 billion in 2026 and is forecast to reach USD 7.55 billion by 2031.

Which technology leads sales in the United States backup power systems market?

Natural-gas generators led with 40.2% revenue share in 2025.

How fast is the fuel-cell segment growing?

Fuel-cell backup systems are advancing at a 9.6% CAGR through 2031.

Why are data centers driving demand for backup power?

AI workloads require 50-60 kW per rack and strict uptime, prompting hyperscale operators to install large redundant generation.

What regulations most impact diesel generators?

EPA Tier 4 Final rules that add USD 8,000-15,000 per unit for after-treatment and extend permitting in non-attainment zones.

Which U.S. regions show the strongest growth?

California, Texas, and Northern Virginia exhibit the highest installation rates because of wildfire shutoffs, grid isolation, and data-center clustering.

Page last updated on: