High Voltage Direct Current (HVDC) Cables Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 11.70 Billion |

| Market Size (2031) | USD 17.27 Billion |

| Growth Rate (2026 - 2031) | 8.10% CAGR |

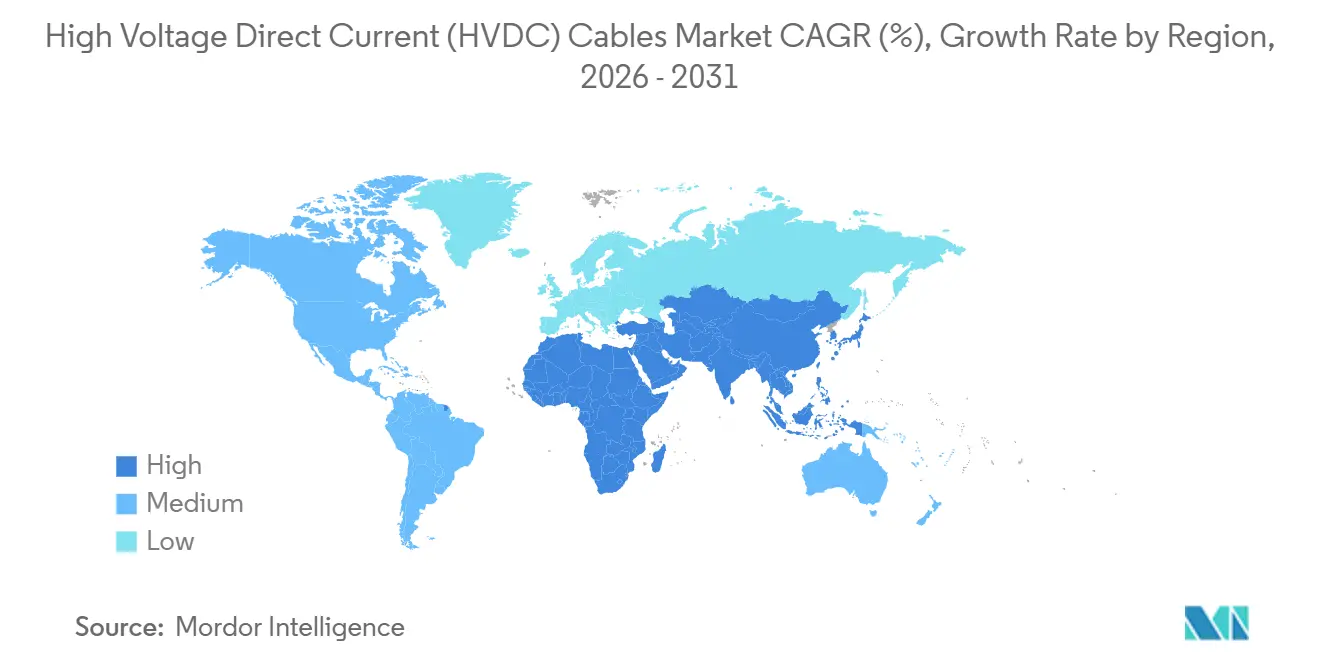

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

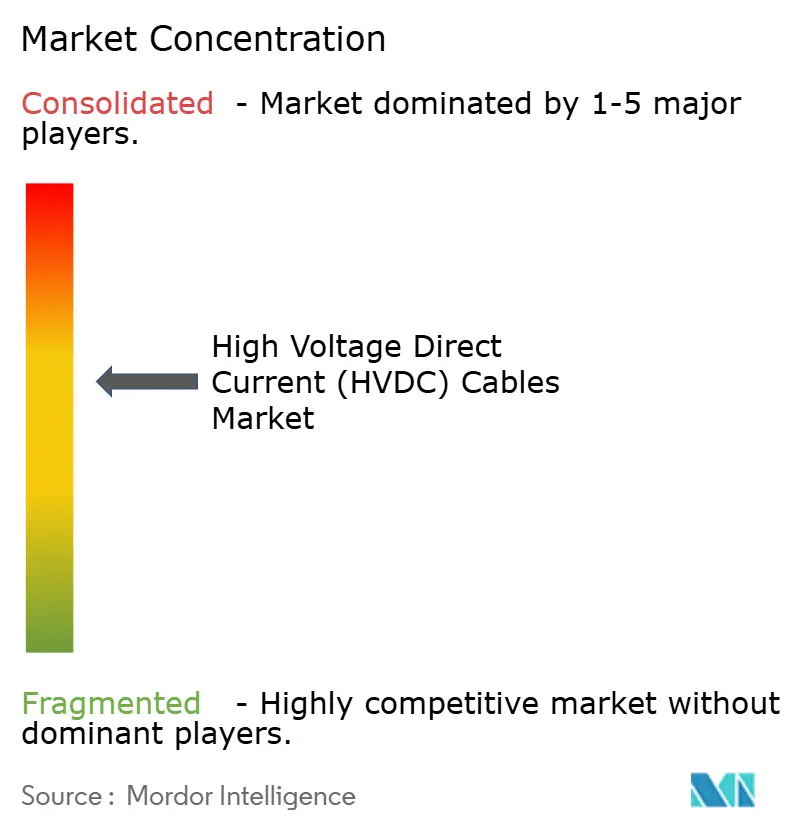

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Voltage Direct Current (HVDC) Cables Market Analysis by Mordor Intelligence

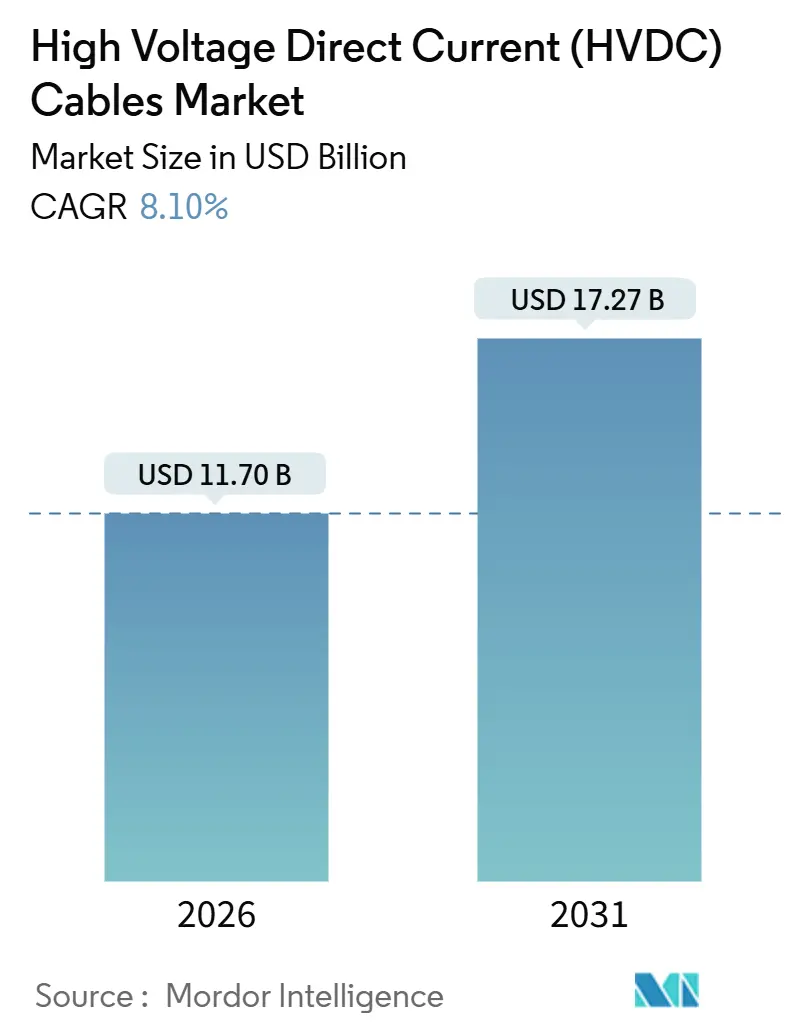

The High Voltage Direct Current (HVDC) Cables Market size is estimated at USD 11.70 billion in 2026, and is expected to reach USD 17.27 billion by 2031, at a CAGR of 8.10% during the forecast period (2026-2031).

Rising offshore wind build-outs in Europe and Asia-Pacific, national super-grid programs in China, India, and the Gulf, and the move toward grid-forming converter stations are jointly pushing demand for long-distance, high-capacity links. Utilities are shifting specifications toward aluminium-core conductors to hedge copper price volatility, while cable makers deepen backward integration into XLPE resin production to secure supply. Turnkey engineering-procurement-construction (EPC) contracts that bundle cable, converter, and installation services are now the preferred procurement route, rewarding scale and vertical integration. At the same time, stricter cybersecurity clauses under IEC 62351 add both cost and competitive barriers, favoring vendors that can certify secure communication protocols.

Key Report Takeaways

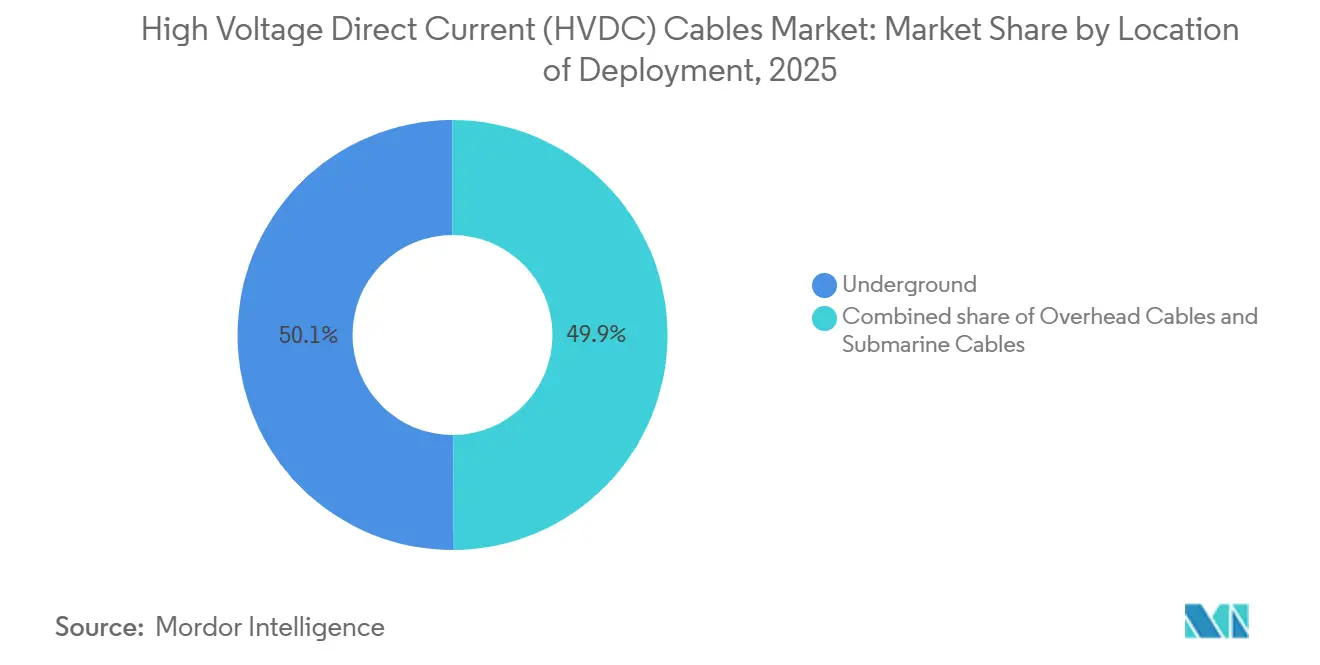

- By location of deployment, underground cables led with 50.1% HVDC cables market share in 2025; submarine cables are the fastest-growing deployment mode at a 10.5% CAGR through 2031.

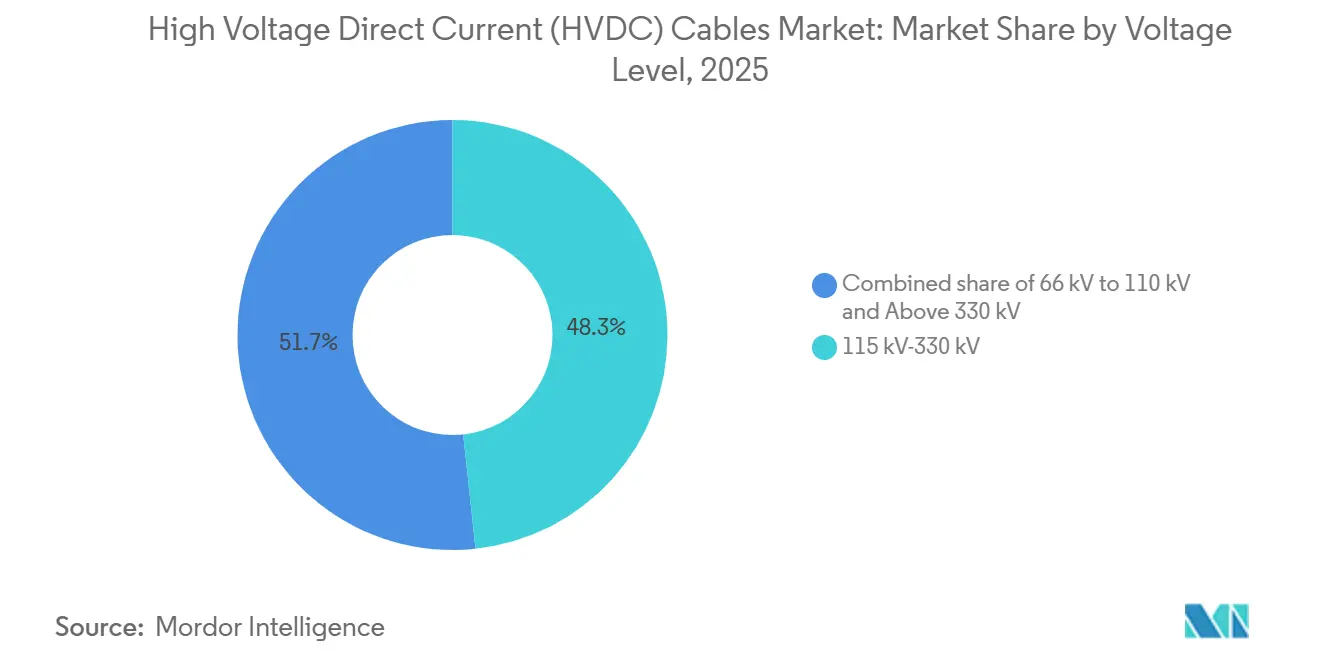

- By voltage level, the 115–330 kV band held 48.3% of the HVDC cables market size in 2025, while systems rated above 330 kV are expanding at a 9.0% CAGR to 2031.

- By geography, Asia-Pacific captured 42.5% revenue in 2025 and is set to remain the largest regional pocket, projected to post a 9.8% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High Voltage Direct Current (HVDC) Cables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated offshore-wind interconnection projects | 2.3% | Europe (North Sea, Baltic), APAC (Taiwan, Japan, Australia) | Medium term (2–4 years) |

| Repowering of ageing AC interconnectors with HVDC links | 1.5% | Europe (UK-Continent, Nordics), North America (US-Canada) | Long term (≥ 4 years) |

| National super-grid initiatives in Asia & MENA | 2.8% | APAC (China, India, ASEAN), Middle East (GCC) | Long term (≥ 4 years) |

| Grid-forming converters enabling hybrid AC/DC grids | 1.2% | Global, early adoption in Europe & Australia | Medium term (2–4 years) |

| Copper price hedging driving aluminium-core HVDC cable demand | 0.9% | Global, concentrated in Asia-Pacific & Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Offshore-Wind Interconnection Projects

Europe and Asia-Pacific are adding offshore wind capacity faster than onshore additions, creating a steady pull-through for submarine links that can move multi-gigawatt blocks over 100 km distances. Denmark’s Bornholm Energy Island hub will use a 3 GW HVDC backbone to export power to Denmark, Germany, and Poland by 2030.[1]Hitachi Energy, “Bornholm Energy Island HVDC Contract,” hitachienergy.com In Australia, the 1.5 GW Marinus Link reached financial close in 2025 and will rely on ±500 kV extruded cable supplied by Prysmian. Ireland’s 700 MW Celtic Interconnector is under construction and will cut peaking fossil output on the island once active in 2027. Each of these projects demonstrates that offshore wind is no longer niche; it now determines vessel fleet sizing, cable-armoring standards, and even crew training.

Repowering of Ageing AC Interconnectors with HVDC Links

Many AC links built in the 1980s and 1990s are nearing end-of-life, and owners are opting for HVDC replacements that slash losses, add capacity, and allow asynchronous operation. National Grid confirmed in 2025 that it will scrap the 2 GW IFA link and replace it with a 3 GW voltage-source-converter system using Nexans 320 kV cables.[2]National Grid, “IFA Repowering Announcement,” nationalgrid.com Norway’s Statnett is evaluating a similar upgrade for the NorNed link, which has faced insulation degradation outages. Repowering carries lower permitting risk as corridors already exist, yet it demands specialist decommissioning and marine coordination. The European Union’s 15% interconnection target for 2030 further accelerates this swap-out wave.

National Super-Grid Initiatives in Asia & MENA

China, India, and the Gulf states are rolling out ultra-high-voltage corridors that connect renewable resource zones with distant load centers. State Grid put three ±800 kV lines in service in 2025, adding 36 GW of transfer capacity.[3]State Grid Corp. of China, “±800 kV UHV Lines Commissioned,” sgcc.com.cn India awarded a 6 GW Ladakh-Punjab link to a consortium in 2025, incorporating aluminium-core overhead conductors and underground entry sections. The Gulf Cooperation Council is progressing a 3 GW backbone that will eventually couple to South Asia and support synthetic-fuel exports. These corridors involve ticket sizes above USD 5 billion, pushing bidders to show balance-sheet strength, EPC depth, and local-content roadmaps.

Copper Price Hedging Driving Aluminium-Core HVDC Cable Demand

Copper futures averaged above USD 9,000 per tonne in late 2025, prompting cable firms to fast-track aluminium conductor lines. LS Cable qualified a ±320 kV aluminium-core cable and booked a 400 MW order for a wind collector in South Korea in 2025.[4]LS Cable & System, “Aluminium-Core HVDC Cable Qualified,” lscns.com Taihan is piloting hybrid aluminium-copper conductors for harsh climates in the Middle East. Aluminium offers 60% weight savings and 40% cost advantage but raises losses and demands tighter manufacturing tolerances. Utilities in price-sensitive Asia-Pacific and Gulf markets are now specifying aluminium in tenders, creating a parallel supply chain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex cross-border permitting for submarine corridors | -1.4% | Europe (North Sea, Mediterranean), ASEAN | Medium term (2–4 years) |

| Volatility in XLPE insulation supply chain | -0.8% | Global, acute in Europe & North America | Short term (≤ 2 years) |

| Rising distributed generation reducing long-haul projects | -0.7% | North America, Western Europe | Long term (≥ 4 years) |

| Cyber-security requirements inflating project CAPEX | -0.5% | Global, stringent in North America & EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Complex Cross-Border Permitting for Submarine Corridors

Subsea projects cross multiple economic zones and need clearances from maritime, environmental, defense, and fisheries bodies, often extending timelines by more than five years. The NeuConnect link from the UK to Germany was pushed to 2028 due to routing debates and fishing-industry objections. LionLink required environmental studies across 14 marine protected areas, which took 18 extra months. A European one-stop-shop concept exists on paper but is not yet harmonized, while the ASEAN Power Grid faces similar hold-ups over transit fees and fault liabilities. These delays raise financing costs and deter merchant-model sponsors.

Volatility in XLPE Insulation Supply Chain

Dow and Borealis dominate high-grade XLPE resin capacity, and each faced force-majeure events in 2024, stretching lead times to 26 weeks in early 2025. Resin prices rose 18% year-on-year, and NKT reported a four-month cable delivery delay for the Baltic Power project. With few qualified dielectric alternatives, cable makers are investing upstream; Prysmian bought into a European compounder in 2025 to lock in feedstock. Qualification for new materials can take up to two years, leaving little short-term relief.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location of Deployment: Submarine Cables Emerge as the Fastest-Growing Segment

Submarine cables accounted for the smallest share in 2025, yet are projected to post a 10.5% CAGR between 2026 and 2031, outpacing underground and overhead lines as offshore wind build-outs multiply. The HVDC cables market size for submarine projects is forecast to widen in tandem with Europe’s North Sea Wind Power Hub plan, which alone will need about 15,000 km of cabling. Prysmian’s new P-Laser vessel, operational since 2024, can lay 525 kV cables in 3,000 m water depths, allowing schemes in the Norwegian Sea and off Japan.

Underground cables retained a 50.1% share in 2025 thanks to urban feeders in Beijing, Shanghai, and Mumbai, where land constraints block overhead lines. Nexans delivered 320 kV cables for the 230 km Delhi–Agra line in 2025. Overhead networks dominate China’s interior ±800 kV backbone because per-kilometer costs run 40% to 60% lower. Growth here is slower as China’s core grid nears saturation, yet Africa and South America still rely on overhead links to unlock remote hydro and solar assets.

By Voltage Level: Above 330 kV Systems Gain Ground

The ultra-high-voltage segment, defined as above 330 kV, is set to grow at 9.0% through 2031, fueled by China’s ±800 kV corridors and India’s planned ±1,100 kV pilot. Hitachi Energy’s modular multilevel converter on the North Sea Link has proven 99.5% availability at ±525 kV since 2024.

The 115–330 kV band still held 48.3% market share in 2025 and remains the workhorse for medium-distance interconnectors such as Germany–Norway’s NordLink. Industrial niches like semiconductor fabs use 66–110 kV point-to-point schemes; LS Cable shipped a ±80 kV system to a Korean fab in 2025. The bifurcation shows utilities embracing ultra-high-voltage for thousand-kilometer corridors while retaining mid-voltage links for incremental upgrades.

Geography Analysis

Asia-Pacific led the HVDC cables market with 42.5% revenue in 2025 and is projected to grow at a 9.8% CAGR to 2031. China commissioned the 2,090 km Baihetan–Jiangsu ±800 kV line in 2025 and plans three more ultra-high-voltage projects by 2031. India’s green-energy corridor tendered 6 GW of capacity in 2025, drawing bids from Prysmian, ZTT, and Hengtong. Japan and South Korea are pushing subsea links to move offshore wind from Hokkaido and the Yellow Sea to demand centers; Sumitomo Electric and LS Cable are front-runners in these awards.

Europe ranks second, driven by offshore wind hubs and repowering of legacy AC corridors. The Bornholm Energy Island, Viking Link, and LionLink schemes together top 10 GW of capacity and more than 2,000 km of cable. Germany’s regulator cleared four north-south HVDC corridors in 2024, with 80% underground routing to placate public resistance. The United Kingdom seeks to replace radial offshore connections with a meshed backbone, aiming for GBP 6 billion savings and 30% less cabling.

North America focuses on cross-border projects that tap Canadian hydro for U.S. load pockets. The 1.25 GW Champlain Hudson Power Express will start service in 2026, bringing power into New York City via a 545 km ±320 kV cable. In the Gulf, a 3 GW spine linking Saudi Arabia, the UAE, and Oman will smooth solar ramp rates and prepare for electricity exports to South Asia. South America and Africa remain early-stage but show proof points such as Brazil’s Belo Monte ±800 kV line and Egypt–Saudi Arabia’s 3 GW interconnection.

Competitive Landscape

The HVDC cables market displays moderate concentration. The top five suppliers, Prysmian, Nexans, NKT, Sumitomo Electric, and Hitachi Energy, captured roughly 60% of submarine and underground revenue in 2025. Their edge lies in vertical integration that spans resin compounding, conductor fabrication, converter stations, and marine installation vessels. Prysmian’s 2025 purchase of a stake in a European XLPE producer secures feedstock and shortens lead times. NKT added a second cable-laying vessel in 2025, enabling multi-route installation on gigawatt-scale offshore hubs.

Asian firms leverage cost advantages and local demand. ZTT and Hengtong expanded ultra-high-voltage conductor capacity by 40% in 2025 and now target Middle East export bids. LS Cable and Taihan are early movers in aluminium-core and hybrid conductors, focusing on Gulf and Asia-Pacific projects sensitive to copper prices.

Technology differentiation centers on grid-forming control algorithms and new cable materials. Hitachi Energy filed a 2024 patent for a modular converter that integrates electrolyzer controls, positioning for corridors that co-locate HVDC cables with hydrogen pipelines. Compliance with IEC 62351 cybersecurity clauses adds cost and deters smaller entrants, pushing utilities toward established brands that can certify secure communication paths.

High Voltage Direct Current (HVDC) Cables Industry Leaders

Sumitomo Electric Industries Ltd

NKT AS

Nexans SA

Prysmian Group

Hitachi Energy Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Nexans clinched a landmark framework deal exceeding EUR 1 billion with Réseau de Transport d’Electricité (RTE). This agreement is set for the design, manufacture, and supply of high-voltage direct current (HVDC) cables, pivotal for offshore wind farms in France.

- March 2025: National Grid has awarded Sumitomo Electric Industries, Ltd. a framework contract for HVDC cables, aimed at upcoming subsea power projects in the UK. Produced in Sumitomo's UK factory, these cables bolster the UK economy, support its employment initiatives, and align with its energy transition objectives.

- March 2025: Hellenic Cables and Jan De Nul clinched a pivotal framework agreement with the UK's National Grid. This positions them as primary contractors for upcoming HVDC cable initiatives across the UK and Europe, bolstering the UK's net-zero ambitions through enhanced offshore wind integration.

- March 2025: National Grid has allocated two segments of a GBP 59 billion High Voltage Direct Current (HVDC) supply chain framework, aiming to equip pivotal energy projects nationwide.

Global High Voltage Direct Current (HVDC) Cables Market Report Scope

High-voltage direct current (HVDC) cables are designed to transmit electrical power at high voltage levels. These cables are typically used to transport electricity over long distances, such as from a power plant to a substation or a substation to a distribution network. High voltage direct current (HVDC) cables are typically insulated with materials such as oil-impregnated paper, cross-linked polyethylene (XLPE), or ethylene propylene rubber (EPR) to prevent electrical breakdown and to ensure that electricity is transmitted efficiently. These can also be shielded to protect against interference from external sources, such as electromagnetic fields.

The Global High Voltage Direct Current (HVDC) Cables Market is segmented by location of deployment, voltage level, and geography. By location of deployment, the market is segmented into overhead, underground, and submarine HVDC cables, reflecting their use across long-distance transmission, urban power corridors, and offshore interconnections. By voltage level, the market is segmented into 66–110 kV, 115–330 kV, and above 330 kV, covering applications ranging from regional grid reinforcement to ultra-high-voltage transmission for cross-border and offshore wind power integration. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, capturing regional demand patterns driven by grid modernization, renewable energy integration, and cross-border interconnections. The report also covers market size and forecasts for the global HVDC cables market across major countries within these regions. For each segment, market sizing and forecasts are provided in terms of value (USD).

| Overhead Cables |

| Underground Cables |

| Submarine Cables |

| 66 kV to 110 kV |

| 115 kV to 330 kV |

| Above 330 kV |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Location of Deployment | Overhead Cables | |

| Underground Cables | ||

| Submarine Cables | ||

| By Voltage Level | 66 kV to 110 kV | |

| 115 kV to 330 kV | ||

| Above 330 kV | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the hvdc cables market by 2031?

The HVDC cables market is projected to reach USD 17.27 billion by 2031.

Which regional block will lead growth through 2031?

Asia-Pacific is expected to post the highest regional CAGR of 9.8% on the back of Chinese and Indian ultra-high-voltage build-outs.

Which deployment mode is expanding the fastest?

Submarine links, driven by offshore wind, show the quickest pace at a 10.5% CAGR between 2026 and 2031.

Which voltage segment is gaining the most traction?

Systems rated above 330 kV are expanding at a 9.0% CAGR as utilities pursue longer, higher-capacity corridors.

Who are the top suppliers by revenue?

Prysmian, Nexans, NKT, Sumitomo Electric, and Hitachi Energy together accounted for about 60% of submarine and underground sales in 2025.

Page last updated on: