Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.23 Billion |

| Market Size (2026) | USD 2.34 Billion |

| Market Size (2031) | USD 2.97 Billion |

| Growth Rate (2026 - 2031) | 4.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Fuel Additives Market Analysis by Mordor Intelligence

The North America Fuel Additives Market size is expected to grow from USD 2.23 billion in 2025 to USD 2.34 billion in 2026 and is forecast to reach USD 2.97 billion by 2031 at a 4.88% CAGR over 2026-2031. Greater enforcement of ultra-low sulfur diesel (ULSD) and gasoline direct injection (GDI) cleanliness standards, the rapid penetration of renewable diesel, and real-time dosing technologies are redefining formulation priorities. Deposit control additives already dominate the North America fuel additives market, and the stricter TOP TIER+ revision G limits published in 2025. Diesel applications are catching up as heavy-duty fleets age, driving stronger demand for cetane and lubricity packages. Meanwhile, OEM warranty clauses that reference additive compliance are widening the premium between certified and generic products. Competitive intensity sits at a moderate level, yet mid-tier blenders are exploiting AI-enabled treat-rate optimization to carve out high-margin niches.

Key Report Takeaways

- By product type, deposit control additives led with 33.11% of the North America fuel additives market share in 2025. Antiknock agents are forecast to expand at a 5.32% CAGR through 2031.

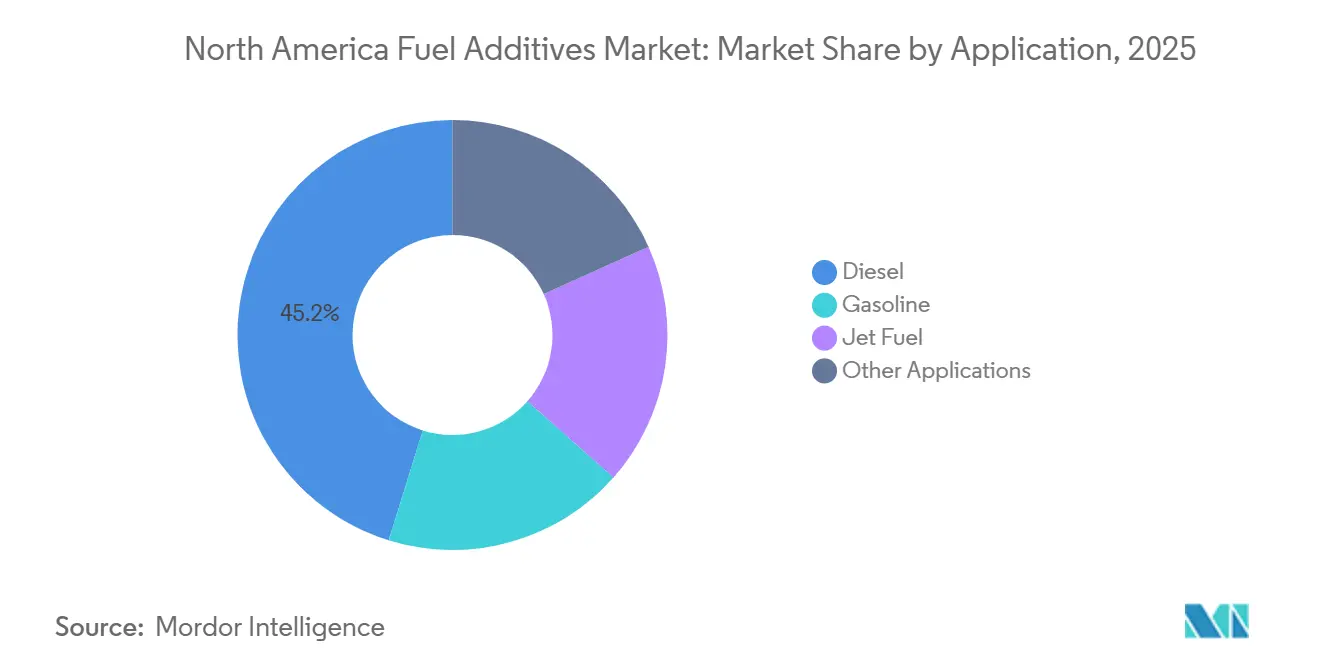

- By application, gasoline accounted for 45.21% of demand in 2025, while diesel is projected to expand at a 4.96% CAGR through 2031.

- By geography, the United States held 85.59% revenue share in 2025 and is projected to expand at a CAGR of 4.88% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Fuel Additives Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ULSD and GDI cleanliness standard upgrades | +1.20% | United States, Canada | Short term (≤ 2 years) |

| After-market demand from aging ICE fleet | +1.50% | United States, Canada, Mexico | Medium term (2-4 years) |

| Renewable diesel/SAF drop-in compatibility | +0.90% | United States (California, Pacific Northwest) | Medium term (2-4 years) |

| OEM warranty-linked additive packages | +0.70% | United States, Canada | Long term (≥ 4 years) |

| AI-enabled real-time dosing systems at retail pumps | +0.40% | United States (pilot regions) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ULSD and GDI Cleanliness Standard Upgrades

Tighter ULSD and GDI guidelines are reshaping additive chemistry. In 2025, the TOP TIER+ revision G took effect, reducing the allowable intake-valve deposits for gasoline engines tuned to a GM LHU turbo platform. Afton Chemical’s HiTEC 65522 GPA, launched in August 2025, demonstrated a significant reduction in deposits during 10,000-mile tests, showcasing the superiority of polyetheramine backbones over traditional polyisobutylene amines[1]Afton Chemical, “HiTEC 65522 GPA Bulletin,” aftonchemical.com . ASTM D6201 has been revised to better simulate stop-start duty cycles. Chevron Oronite’s OLOA 55520 has already met the draft method's requirements, combining friction modifiers with detergents that endure elevated EGR rates. These advancements are shortening additive life cycles, prompting formulators to invest in adaptive detergent packages that ensure consistent performance in blended renewable fuels. Suppliers who navigate these stringent tests successfully are reaping the rewards, securing early volume with OEM-approved service networks and bolstering brand loyalty among downstream distributors.

After-Market Demand from Aging ICE Fleet

As vehicles age, the U.S. light-duty fleet has reached a median age of over 12 years. This aging trend has resulted in a significant base of engines operating without built-in fuel-system protection. Retail and e-commerce channels for consumer-packaged fuel additives have grown steadily. Notably, owners of diesel pickups have shown a marked preference for single-dose blends that enhance cetane and lubricity. Heavy-duty Class 8 tractors, averaging over eight years in age, have spurred a heightened demand for cold-flow improvers, essential for ensuring ultra-low sulfur diesel (ULSD) remains functional during frigid winters. Canada showcases an even more pronounced seasonal trend; in its western provinces, more than 85 percent of winter diesel is treated with pour-point depressants. The rise of do-it-yourself channels, coupled with delayed equipment replacement cycles, positions the North American fuel additives market on a trajectory for sustained aftermarket growth.

Renewable Diesel and SAF Drop-In Compatibility

Legacy additive performance often faces disruption from blends of hydrotreated vegetable oil (HVO) and sustainable aviation fuel (SAF). HVO’s reduced aromaticity diminishes detergent solvency, leading to increased precipitate formation in storage tanks at temperatures below 10 degrees Celsius. BASF’s Kerojet 5000 introduced phenolic antioxidants, extending jet fuel's shelf life to meet airlines' extended inventory cycles. United Airlines is committed to an annual procurement of SAF by 2030, dependent on certification of ASTM D7566 Annex A7 and A8 compatibility by additive suppliers. Additives for static dissipation, now required under ASTM D1655, present a lucrative annual revenue opportunity for certified producers. Consequently, the increasing use of renewable blends broadens the market potential for specialty antioxidants, lubricity enhancers, and conductivity modifiers.

AI-Enabled Real-Time Dosing Systems at Retail Pumps

Artificial intelligence is making its mark on retail forecourts. In 2025, Veeder-Root tested real-time dosing at truck stops across Texas and Oklahoma, achieving a reduction in additive over-treatment. Meanwhile, Additech secured funding to leverage machine learning, allowing them to deduce engine types from payment-card metadata and dynamically adjust detergent dosing. However, a significant challenge looms: the EPA still operates under the assumption of fixed treat rates, making regulatory approval elusive. Should dosing flexibility receive the green light, annual additive consumption might see a decline. Yet those suppliers who can license the algorithms stand to boost their contribution margins. This evolution presents both a volume risk and a potential profitability surge in the North American fuel additives market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High validation and treat-rate Research and Development costs | -0.80% | United States, Canada | Medium term (2-4 years) |

| Specialty-chemical supply-chain shocks | -0.60% | United States, Canada, Mexico | Short term (≤ 2 years) |

| LCFS-driven sulfur-free synthetic fuels cannibalizing additives | -0.50% | United States (California) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Validation and Treat-Rate Research and Development Costs

Bringing a new additive to market demands 18-36 months of scrutiny from OEMs and the EPA, often racking up significant expenses. Smaller players feel the pinch, as TOP TIER certification mandates 10,000-mile engine tests across three platforms, in addition to fleet trials, a feat straining their resources. Backlogs arise from limited test-rig availability under ASTM D6201, pushing commercialization timelines by as much as nine months. In 2024, Dorf Ketal pulled back a deposit-control initiative in North America after it couldn't secure GM's nod, leading to a substantial write-off. Each minor dose reduction triggers a cycle of reformulations, effectively doubling research and development timelines and dampening growth prospects for the North American fuel additives market.

LCFS-Driven Sulfur-Free Synthetic Fuels Cannibalizing Additives

California's Low Carbon Fuel Standard (LCFS) is fast-tracking the adoption of e-diesel, which requires minimal additives. Porsche's pilot project in Chile is producing Fischer-Tropsch diesel, boasting a cetane rating above 70 and natural lubricity within ASTM D975 limits, thus negating the need for conventional enhancers. With LCFS credit multipliers having increased in 2025, synthetic fuels have become cost-competitive[2]California Air Resources Board, “LCFS Program,” arb.ca.gov . The adoption of e-fuels is expected to significantly impact the diesel market in California and neighboring regions. In light of these shifts, suppliers are urged to transition towards value-added antioxidants and static dissipators for Sustainable Aviation Fuel (SAF) to counterbalance the dwindling demand for traditional additives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Deposit Control Leads, Antiknock Agents Surge

Deposit control additives captured 33.11% of the North America fuel additives market in 2025. The expansion of this segment in North America's fuel additives market is attributed to a larger GDI fleet and the enforcement of stricter TOP TIER+ thresholds. Advanced polyetheramine detergents, capable of resisting thermal breakdown at high EGR temperatures, play a pivotal role in preventing piston-crown carbon formation. Cetane improvers, benefiting from Mexico’s upgraded diesel specifications mandating 2-ethylhexyl nitrate dosing, secure the second spot in revenue. On the other hand, while lubricity additives experience treat-rate compression due to HVO's superior baseline wear protection, the overall gallonage continues to rise in tandem with renewable blending targets.

Antiknock agents are expected to register the fastest 5.32% CAGR through 2031. Independent refiners, lacking alkylation or isomerization capacity, are increasingly turning to non-metallic boosters. For instance, quaternary ammonium salts can elevate research octane numbers by a notable margin at low doses. The demand for antioxidants is also on the rise, particularly in biodiesel blends exceeding B20. Packages like phenolic-aminic formulations now extend storage life significantly. In western Canada, cold-flow improvers command premium pricing. Polymers known for reducing pour points by substantial margins achieve this at modest treat rates.

By Application: Gasoline Dominates, Diesel Accelerates

Gasoline applications retained a 45.21% share of the North America fuel additives market in 2025, buoyed by a fleet of light-duty vehicles. However, diesel applications are on track to register the highest 4.96% CAGR through 2031. This surge is fuelled by the aging Class 8 fleets and the rising penetration of Hydrotreated Vegetable Oil (HVO), which are driving new chemistry demands. By 2031, the North American fuel additives market, specifically tied to diesel, is projected to grow. This growth is largely attributed to the demand for lubricity and cetane boosters, ensuring compliance with Ultra-Low Sulfur Diesel (ULSD) standards. While neat HVO poses challenges with ASTM D975 wear-scar limits, Infineum's R655 has carved out a notable segment share in 2025, thanks to its performance guarantee across the full spectrum of renewable blends.

Jet fuel, despite accounting for a smaller portion of revenue, is reaping benefits from airlines' commitments to Sustainable Aviation Fuel (SAF). For instance, United Airlines is projected to need static dissipators and icing inhibitors annually by 2030. Meanwhile, other sectors like marine and off-road applications have stagnated, largely due to the electrification trend in small engines. In a broader perspective, as the adoption of renewables widens, there's a noticeable shift in the product mix. The emphasis is moving away from volume-driven lubricity towards more value-rich packages, focusing on antioxidants and conductivity.

Geography Analysis

The United States leads North America's fuel additives market, contributing 85.59% of the region's revenue in 2025 and is projected to grow at a CAGR of 4.88% through 2031. In 2025, California's LCFS generated significant credits, with most stemming from renewable diesel blends, necessitating tailored antioxidant and lubricity packages. In 2024, EPA reforms expedited additive approvals, as highlighted by Chevron Oronite's OLOA 55520 receiving clearance in a shorter timeframe. Gulf Coast refineries, pivotal to the U.S. landscape, cater to a significant portion of the national demand, while BASF's Geismar plant stands out, supplying a large share of the nation's polyisobutylene succinimide.

Canada, holding a notable market share, has primarily expanded through cold-flow improvers and renewable-diesel stabilizers. Under Clean Fuel Regulations, Canada mandates a reduction in CO₂e per megajoule by 2030. This push towards hydrotreated vegetable oil blends has led to an increase in antioxidant doses compared to petroleum diesel. In 2024, Braya Renewable Fuels commenced operations in Newfoundland, producing hydrotreated vegetable oil, all treated with Clariant DODIFLOW to ensure operability in extremely low temperatures. Due to Arctic weather, Western provinces account for the majority of Canada's cold-flow volume.

Mexico, while holding a smaller market share, has shown the fastest growth rate. In 2024, PEMEX raised cetane minima, leading to widespread additive dosing. Aligning sulfur limits with U.S. ULSD standards further expanded the local lubricity-additive market. In 2025, concerns over inconsistent gasoline quality in Mexico City and Monterrey spurred a rise in single-dose aftermarket sales.

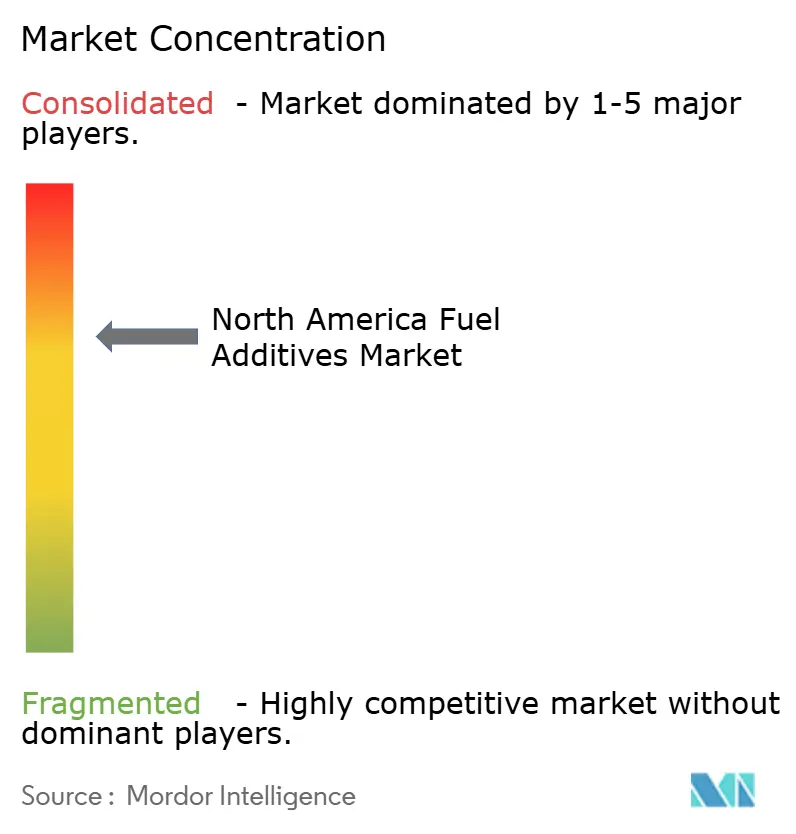

Competitive Landscape

The North America fuel additives market is moderately consolidated. This leaves a significant share for regional blenders. In March 2025, Chevron Oronite bolstered its supply reliability by inaugurating a warehouse in France, effectively shortening Atlantic lead times. Meanwhile, BASF's declaration of force majeure on detergent shipments in January 2025 underscored the fragility of the supply chain, leading some of its customers to divert partial volumes to competitors Innospec and Lubrizol. Patent activity is increasingly favoring non-metallic octane boosters and bio-based lubricity agents. Notably, SABIC lodged patents related to RON-enhancement between 2024 and 2025, while Croda clinched rights to rapeseed-derived lubricity additives, boasting treat rates that are halved compared to conventional ones.

AI-driven dosing and compatibility with Sustainable Aviation Fuel (SAF) are emerging as potential growth areas. Veeder-Root's pilot program achieved a reduction in additive waste, hinting at the profit-boosting potential of software innovations. Presently, only a few suppliers have secured ASTM D1655 approvals for static dissipators, positioning them advantageously as the demand for SAF surges. In a testament to targeted marketing, niche player Hot Shot's Secret registered growth in 2025 by catering to diesel pickup owners via truck-stop chains. However, challenges persist; the TOP TIER certification, priced significantly, acts as a formidable barrier, safeguarding the positions of established players.

North America Fuel Additives Industry Leaders

AFTON CHEMICAL

BASF

Chevron Oronite Company LLC

Innospec

The Lubrizol Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Lubrizol announced certification of its GA9100 Series gasoline fuel additives meeting the updated TOP TIER+ performance threshold, underlining higher detergency and advanced engine-cleanliness targets.

- March 2025: Innospec Inc. expanded drag-reducing-agent capacity in Pleasanton, Texas, targeting pipeline operators seeking throughput gains without major capital upgrades.

North America Fuel Additives Market Report Scope

Fuel additives are compounds that are designed to improve the quality and efficiency of fuels. Fuel additives are added to improve performance, flowability, corrosion resistance, clean burning, and many other properties.

The fuel additives market is segmented by product type, application, and geography. By product type, the market is segmented into deposit control, cetane improvers, lubricity additives, antioxidants, anticorrosion, cold flow improvers, antiknock agents, and other product types. By application, the market is segmented into diesel, gasoline, jet fuel, and other applications. The report also covers the market sizes and forecasts for fuel additives in 3 countries across major North American region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Product Type

| Deposit Control |

| Cetane Improvers |

| Lubricity Additives |

| Antioxidants |

| Anticorrosion |

| Cold Flow Improvers |

| Antiknock Agents |

| Other Product Types |

By Application

| Diesel |

| Gasoline |

| Jet Fuel |

| Other Applications |

By Geography

| United States |

| Canada |

| Mexico |

| By Product Type | Deposit Control |

| Cetane Improvers | |

| Lubricity Additives | |

| Antioxidants | |

| Anticorrosion | |

| Cold Flow Improvers | |

| Antiknock Agents | |

| Other Product Types | |

| By Application | Diesel |

| Gasoline | |

| Jet Fuel | |

| Other Applications | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large will the North America fuel additives market be by 2031?

The market is expected to register USD 2.34 billion in 2026 and is forecast to reach USD 2.97 billion by 2031 on a 4.88% CAGR trajectory.

Which product category leads revenue?

Deposit control additives held 33.11% share in 2025 and keep the top position through 2031.

Why is diesel the fastest-growing application?

Aging heavy-duty fleets and higher renewable-diesel blending demand extra cetane and lubricity packages, lifting diesel additives at a 4.96% CAGR.

What is driving antiknock-agent growth?

Smaller refiners adopt non-metallic octane boosters that meet ASTM D4814 specs without new alkylation units, generating a 5.32% CAGR.

Page last updated on: