Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

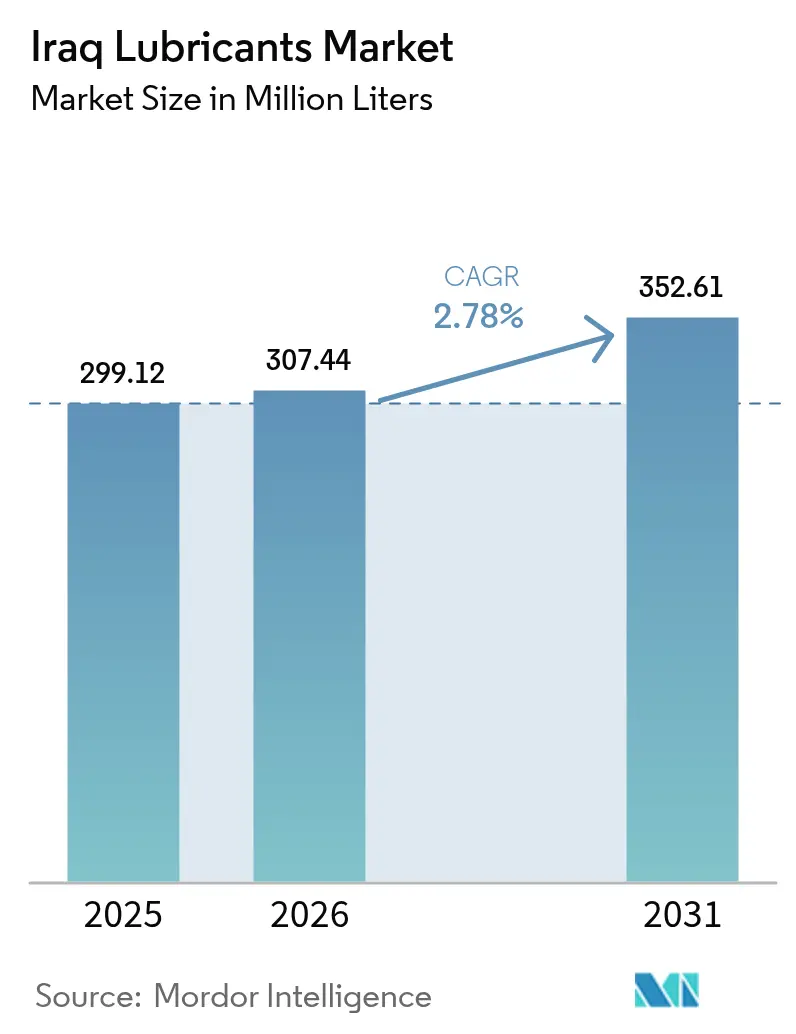

| Base Year Market Size (2025) | 299.12 Million liters |

| Market Volume (2026) | 307.44 Million liters |

| Market Volume (2031) | 352.61 Million liters |

| Growth Rate (2026 - 2031) | 2.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iraq Lubricants Market Analysis by Mordor Intelligence

The Iraq Lubricants Market size was valued at 299.12 Million liters in 2025 and is estimated to grow from 307.44 Million liters in 2026 to reach 352.61 Million liters by 2031, at a CAGR of 2.78% during the forecast period (2026-2031). Reconstruction spending, upstream oil projects exceeding USD 52 billion, and the rapid expansion of authorized workshop networks are driving volume growth, despite challenges from counterfeit products and the early stages of vehicle electrification. Diesel generator usage remains consistently high, as Iraq's power grid supplies only 24-28 GW against a peak demand exceeding 50 GW, sustaining strong demand for high-viscosity engine oils. OEM service-fill agreements are strengthening relationships between global blenders and dealerships, encouraging a consumer shift toward synthetic grades, with retail prices for full synthetics ranging from USD 16-27 per liter. Meanwhile, the rationalization of subsidies on base-oil imports is increasing input costs for local blenders, leading to greater dependence on imported Group I and Group II stocks. Over the next five years, the Iraq lubricants market is expected to be influenced by the addition of 38 GW of combined-cycle capacity, gradually shifting the product mix toward turbine and transformer oils for the power sector.

Key Report Takeaways

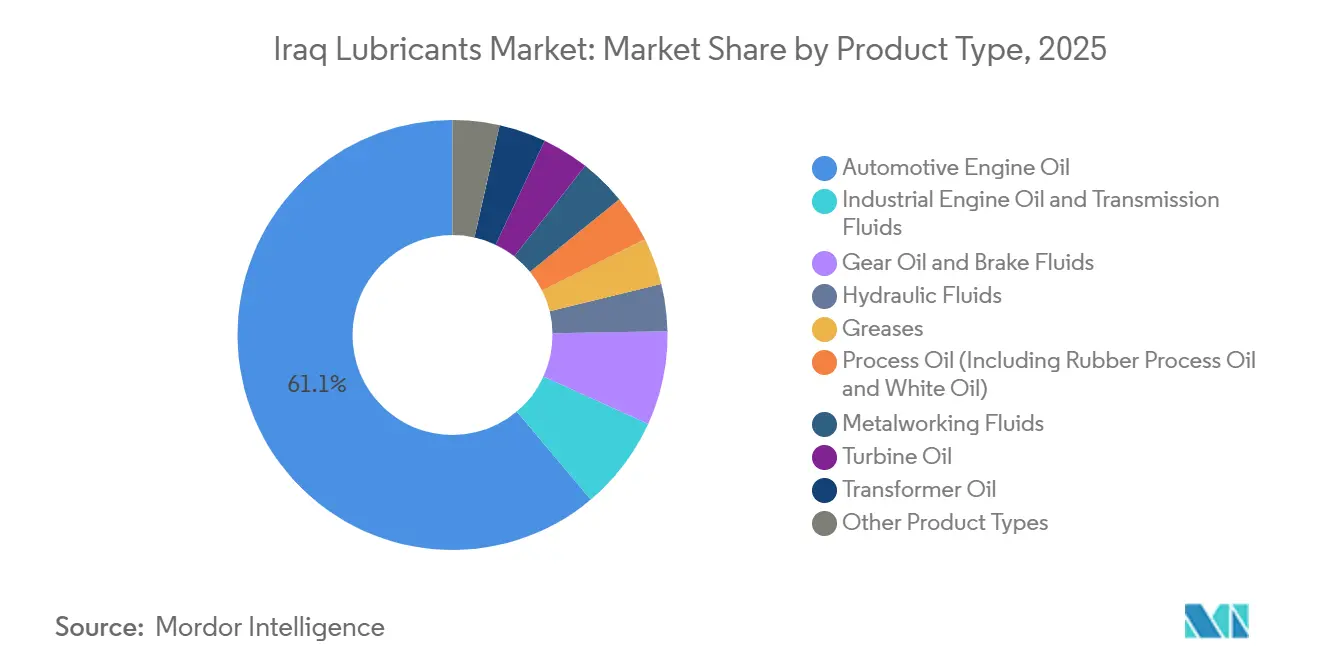

- By product type, automotive engine oil led with 61.12% of Iraq lubricants market share in 2025, while hydraulic fluids are projected to expand at a 3.12% CAGR through 2031.

- By base stock type, mineral oil-based lubricants accounted for 72.12% of the Iraq lubricants market share in 2025, whereas synthetic formulations are forecast to advance at a 4.55% CAGR over 2026-2031.

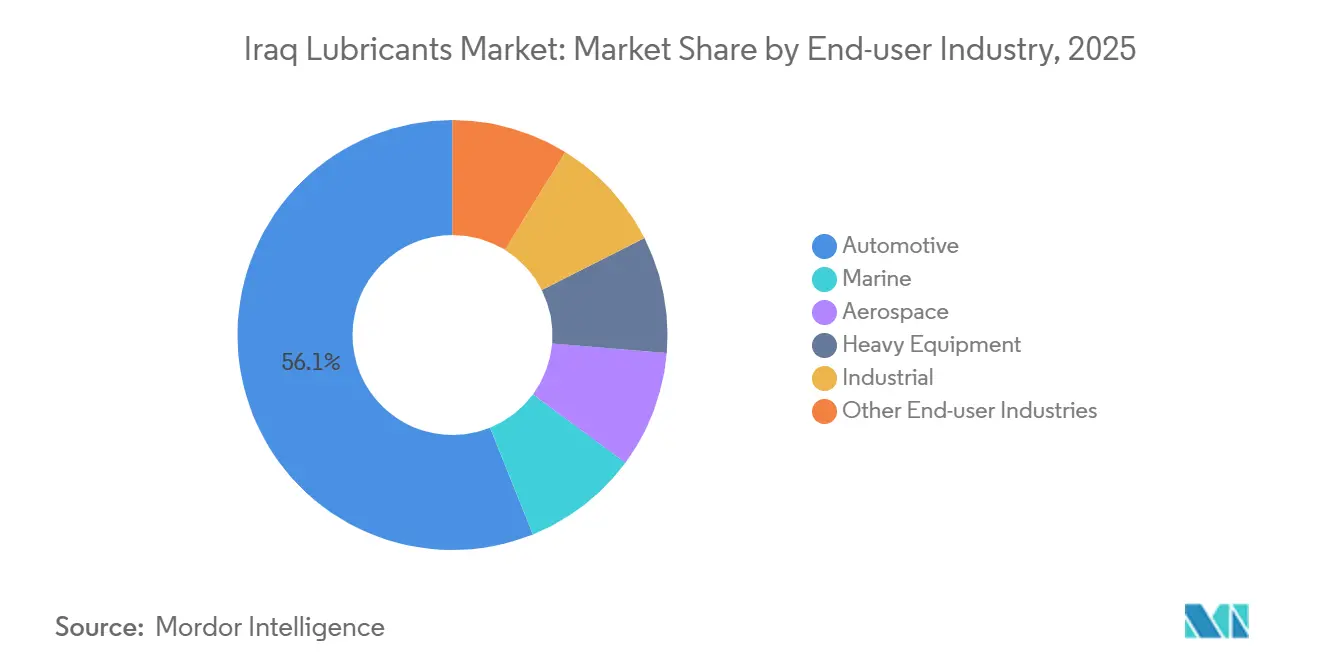

- By end-user industry, the automotive segment held 56.10% of the Iraq lubricants market share in 2025, while the industrial segment is expected to post the fastest growth at 4.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Iraq Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reconstruction-led rise in diesel genset hours | +0.6% | National, with peak demand in Baghdad, Basra, and Kirkuk | Medium term (2-4 years) |

| Up-scaling of upstream and mid-stream oil projects | +0.7% | National, concentrated in Kirkuk, Basra, and Akkas gas field | Long term (≥ 4 years) |

| OEM service-fill tie-ups expanding authorized workshop network | +0.4% | National, early gains in Baghdad, Erbil, Sulaymaniyah, Duhok, Basra | Short term (≤ 2 years) |

| Consumer shift toward synthetic and semi-synthetic grades | +0.3% | National, led by Baghdad and Kurdistan Region | Medium term (2-4 years) |

| United Nation/IFC-backed industrial energy-efficiency lubrication programs | +0.2% | National, with IFC investments in Basra Gas, cement sector, and eco-industrial parks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reconstruction-led Rise in Diesel Genset Hours

Hospitals, malls, and households depend on private generators to address the 20 GW power-supply deficit, reducing engine-oil drain intervals to fewer than 300 running hours in certain applications. Kirkuk General Hospital installed four 2,250 kVA generator sets in February 2025, reflecting a nationwide trend that supports short-cycle lubricant demand. Although 38 GW of combined-cycle capacity from GE Vernova and Siemens Energy is under contract, challenges related to grid connection, pipeline feedstock, and dispatch flexibility mean full operationalization is unlikely before 2028. Until then, the Iraq lubricants market benefits from two opportunities: immediate demand for generator lubricants and, later, turbine-oil demand as large plants become operational. Suppliers offering ISO VG 46 turbine oils and API CF-4 heavy-duty engine oils can bridge current demand with future product requirements.

Up-scaling of Upstream and Mid-stream Oil Projects

BP’s USD 25 billion Kirkuk redevelopment and TotalEnergies’ USD 27 billion Gas Growth Integrated Project are driving increased demand for hydraulic fluids and compressor oils across drilling, gathering, and processing operations. Drilling activities at Akkas commenced in January 2026, with plans to quadruple gas output to 400 MMscfd, boosting demand for high-pressure gear oils and food-grade greases for associated water-treatment units. Iraq aims to increase crude production from 4.47 million barrels per day in 2025 to 6 million barrels per day by 2029, a 34% rise that proportionally expands auxiliary lubricant requirements. Regional clustering in Basra and Kirkuk encourages the establishment of forward-stocking depots, enabling blenders to meet 24-hour delivery timelines for rig sites. Additionally, each new midstream compressor station requires 3-5 metric tons of synthetic turbine oil annually, creating sustained demand for premium products.

OEM Service-fill Tie-ups Expanding Authorized Workshop Network

Toyota Iraq invested IQD 30 billion in a 225,000 m² integrated facility and opened two service centers in Baghdad in February 2026, reinforcing adherence to brand-approved lubricant standards within its growing after-sales network. Similarly, Changan’s 39,000 m² Baghdad showroom with 40 lift stations, BMW’s Retail. Next facility in Sulaymaniyah, and BYD’s December 2025 launch are driving the adoption of ILSAC GF-6 and API SP specifications in routine servicing. Blenders securing first-fill agreements gain multi-year captive demand, as vehicle owners typically remain within authorized service networks during warranty periods. Consequently, the Iraq lubricants market is shifting toward synthetic oils priced at USD 16-27 per liter, reducing the informal sector’s market share. Additionally, digital parts-management systems enhance traceability, limiting the entry of counterfeit oils into authorized dealer networks.

Consumer Shift Toward Synthetic and Semi-synthetic Grades

Shell has identified Iraq, the UAE, and Oman as leading markets in the Middle-East for synthetic lubricant adoption, driven by the increasing prevalence of turbocharged engines requiring low-viscosity, high-temperature-stable oils. Retail shelves now feature a three-tier pricing structure: mineral oils at USD 4-7 per liter, semi-synthetics at USD 8-13, and full synthetics priced above USD 16. With the registered vehicle fleet surpassing 8 million units by December 2025 and projected to reach 9 million by 2030, the growing penetration of modern engines is shifting demand toward higher-grade lubricants. Research by the University of Technology on viscosity-index improvers for Al-Dorah refinery’s SN-500 base oil highlights local ambitions to produce semi-synthetics domestically, though commercial-scale production remains distant. In the meantime, reliance on imports persists, and suppliers offering OEM-approved products with extended drain intervals are gaining market share.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and informal-sector lubricant circulation | -0.4% | National, concentrated in unregulated retail channels | Short term (≤ 2 years) |

| Subsidy rationalization on base-oil imports | -0.3% | National, affecting local blenders and importers | Medium term (2-4 years) |

| Rising EV and hybrid vehicle imports | -0.2% | National, early adoption in Baghdad and Kurdistan Region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Informal-sector Lubricant Circulation

Damage to refineries in Baiji, Daura, and Basra has resulted in a shortage of domestic base stocks, leading to the diversion of 500,000-750,000 tons per month of subsidized heavy fuel oil into off-spec blends that emit sulfur odors and fail API standards[1]Oxford Institute for Energy Studies, “Iraq’s Downstream Challenges,” oxfordenergystudies.org. For example, January 2026 saw the arrest of 19 fuel-smuggling suspects and the seizure of 27 million liters of illicit products, demonstrating enforcement efforts but also exposing regulatory gaps. While COSQC standards are in place, limited field laboratories and porous borders allow substandard imports to bypass scrutiny. Unbranded oils, priced 30-50% lower than branded equivalents, undermine consumer trust and delay the transition to synthetic lubricants. As OEM service networks expand, the informal sector faces increasing challenges, but a comprehensive crackdown remains a medium-term goal for the Iraq lubricants market.

Subsidy Rationalization on Base-oil Imports

Heavy fuel prices rose from USD 70 per ton in early 2024 to over USD 220 per ton by late 2025 due to subsidy rollbacks and regional supply constraints linked to Iranian sanctions. Local blenders, previously reliant on inexpensive feedstocks, now import Group I or Group II base oils at full market prices, squeezing margins and raising concerns about quality compromises. Iraq’s imports are primarily sourced from Kuwait, Saudi Arabia, and the UAE, where supply disruptions quickly affect finished-oil pricing. This polarization is driving budget players out of the market or forcing quality reductions, while premium brands absorb costs through value-added synthetics. Between 2026 and 2031, rationalized pricing is expected to accelerate the shift from mineral to synthetic lubricants, even as the overall Iraq lubricants market continues to grow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automotive Engine Oil Dominates, Hydraulic Fluids Accelerate

Automotive engine oil accounted for 61.12% of Iraq's lubricants market size in 2025, supported by a vehicle fleet exceeding 8 million units. Hydraulic fluids are expected to grow at the fastest rate, with a 3.12% CAGR through 2031, driven by the addition of USD 89.7 million worth of Chinese construction equipment to reconstruction sites in 2024[2]UN Comtrade, “Iraq Import Statistics: Construction Equipment 2024,” un.org. The increased use of excavators, cranes, and loaders is fueling demand for ISO HM and ISO HV hydraulic oils, aligning with Iraq's goal of producing 50 million tons of cement annually by 2030. Industrial engine oils are consumed by auxiliary diesel generators at oilfields, while transmission fluids and gear oils support the 2,156 Japanese trucks imported in 2024. Smaller segments, such as greases and brake fluids, cater to the railway, marine, and aviation industries but collectively hold a smaller share of the Iraq lubricants market.

In the latter half of the decade, turbine oils and transformer oils are expected to gain prominence as 38 GW of gas-turbine capacity is phased in. Each 1 GW plant requires 40-60 kiloliters of ISO VG 32 turbine oil during commissioning and an additional 6-8 kiloliters annually for maintenance. The Central Organization for Standardization and Quality Control (COSQC) relies on API and ISO standards for regulatory guidance, but further market education on varnish formation and oxidation limits is needed. Blenders offering onsite oil-analysis services are positioning themselves as partners in risk management rather than mere suppliers, a strategy gaining traction in Iraq's lubricants market.

By Base Stock Type: Mineral Oils Prevail, Synthetics Gain Traction

Mineral oil-based lubricants held 72.12% of the market volume in 2025. However, synthetic lubricants are expected to grow at a 4.55% CAGR through 2031, outpacing other base-stock categories. Semi-synthetic blends, typically containing 20-30% Group III or PAO, serve as a cost-effective alternative for consumers transitioning to higher-quality products without incurring the full cost of synthetic lubricants, which can reach USD 27 per liter. While Iraq remains dependent on imports, local research and development on viscosity-index improvers may enable partial substitution of Group I stocks by the end of the decade. Bio-based lubricants remain in the early stages of adoption, with niche applications such as marine-environment regulations at the Port of Umm Qasr potentially driving initial demand. This trend mirrors global bio-lubricant revenues, which reached USD 3.06 billion in 2024.

Industrial users value synthetic lubricants for their energy efficiency and extended drain intervals. For example, steel mills transitioning to synthetic gear oils report up to a 3% reduction in power consumption and decreased unplanned downtime, benefits that justify the 2-3 times price premium. These economic advantages are expected to drive a long-term shift in Iraq's lubricants market toward higher-margin products, even as overall consumption levels stabilize.

By End-user Industry: Automotive Leads, Industrial Segment Surges

The automotive industry accounted for 56.10% of Iraq's lubricants market share in 2025, supported by a 24.1% year-on-year increase in Q1 2025 vehicle sales and the import of 18,000 Chinese vehicles in the first half of 2025. Passenger cars dominate the segment, but commercial trucks imported from Japan, with sump capacities exceeding 28 liters, contribute significantly to per-unit lubricant consumption. The industrial sector is expected to grow at the fastest rate, with a 4.56% CAGR through 2031, driven by contracts with GE Vernova and Siemens Energy to add 24 GW and 14 GW of gas turbine capacity, respectively, which require premium-grade turbine oils.

Reconstruction-related heavy equipment drives demand for hydraulic and gear oils, while the marine sector requires greases and cylinder oils for 90 monthly port calls at Umm Qasr. The aerospace industry adheres to strict MIL-PRF standards, with Iraqi Airways' planned delivery of 31 new aircraft by 2027, ensuring demand for high-temperature, low-coking aviation turbine oils. These diverse end-user industries provide stability to Iraq's lubricants market, reducing reliance on any single sector.

Geography Analysis

Baghdad, Basra, and the Kurdistan Region collectively account for the majority of lubricant consumption, reflecting population density and industrial activity. Baghdad leads in automotive after-sales volumes, supported by Toyota's new service centers and Changan's flagship showroom, both of which promote factory-approved synthetic oils during routine maintenance. Chronic power shortages in the capital sustain demand for SAE 15W-40 engine oils for rooftop generators. Basra, home to hydrocarbon megaprojects such as TotalEnergies' USD 27 billion program and IFC-funded gas-capture installations, drives demand for compressor and process oils.

In the Kurdistan Region, cities like Erbil, Sulaymaniyah, and Duhok benefit from relative political stability, encouraging the growth of premium-brand dealerships and faster adoption of synthetic passenger-car motor oils. Kirkuk's redevelopment under BP stimulates local demand for hydraulic and gear oils used in drilling and workover rigs. Port-centric lubricant demand thrives at Umm Qasr, where IFC-funded berth expansions and crane additions in February 2026 are expected to increase turnover of hydraulic fluids and greases.

Secondary cities such as Najaf, Karbala, and Mosul contribute incremental demand. Mosul International Airport, 86% rebuilt by early 2026, resumed operations in January 2026, driving demand for aviation hydraulic fluids for ground-support equipment. While counterfeit products still infiltrate northern governorates, increased COSQC spot-testing and dealership density are gradually tightening market controls. Across all regions, Iraq's lubricants market continues to grow, supported by reconstruction efforts, power generation projects, and a predominantly internal-combustion vehicle fleet.

Competitive Landscape

The Iraq lubricants market is moderately fragmented, with major players such as Shell, TotalEnergies, BP, ExxonMobil, and FUCHS leveraging multinational R&D capabilities and OEM partnerships. However, informal blenders and regional entrants maintain price competition. Shell's promotion of synthetic lubricants aligns with its global "Powering Progress" strategy, securing a strong position in authorized workshops. BP and TotalEnergies benefit from their extensive upstream portfolios, but the lack of disclosed captive supply contracts leaves room for specialty suppliers targeting turbine and process oil niches.

Chinese brands are capitalizing on the import of 18,000 vehicles in H1 2025, offering factory-approved lubricants under their own labels. Thai company PTT Lubricants has entered the market with API SQ and ILSAC GF-7A ranges designed for GCC climate conditions, adding another layer of competition. Digital inventory platforms within dealership networks are improving traceability of lubricant grades and lot numbers, gradually reducing the prevalence of counterfeit products. However, limited COSQC lab capacity highlights the need for collaboration with private blenders to enhance testing infrastructure and accelerate market formalization.

Niche players such as ADDINOL, Carl Bechem, Klüber, and Zeller+Gmelin focus on high-margin segments like food-grade hydraulics and metalworking fluids for steel fabrication at Grand Faw port. Their success depends on providing technical training and oil-analysis services in Arabic and Kurdish. As upstream, power, and maritime projects progress, contract-linked volume opportunities are emerging, favoring suppliers capable of bundling products, logistics, and application engineering within tight project timelines.

Iraq Lubricants Industry Leaders

Behran Oil Company

FUCHS

Petromin Corporation

TotalEnergies

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SAS Trading and Vehicle Services Ltd., authorized by Toyota Iraq, expanded its aftersales network in Baghdad by opening two new service centers. This development is expected to drive the lubricant market by improving accessibility to genuine parts and services.

- October 2025: Iraq awarded a USD 764 million public-private partnership contract to a consortium led by Corporación América Airports (CAAP) and Amwaj International to rehabilitate and operate Baghdad International Airport. This development is expected to drive the lubricant market by increasing demand for aviation-grade lubricants due to enhanced airport operations and infrastructure upgrades.

Iraq Lubricants Market Report Scope

Lubricants are substances made from a combination of base oils and additives. These lubricants are used in various automotive applications such as engines, brakes, gears, and other parts. The base oil composition in the formulation of lubricants is primarily between 75-90%. Lubricants are used to reduce friction between surfaces in contact to minimize energy loss generated from friction.

The Iraq lubricants market is segmented by product type, base stock type, and end-user industry. By product type, the market is segmented into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil (including rubber process oil and white oil), metalworking fluids, turbine oil, transformer oil, and other product types. By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, industrial, and other end-user industries. The automotive segment is further segmented into passenger vehicles, commercial vehicles, and two-wheelers. The heavy equipment segment is further segmented into construction, mining, and agriculture. The industrial segment is further segmented into power generation, metallurgy and metalworking, textiles, and oil and gas. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-user Industries |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

What is the volume of the Iraq lubricants market?

The Iraq lubricants market stands at 307.44 million liters in 2026 and is projected to reach 352.61 million liters by 2031.

Which product type holds the largest share in 2025?

Automotive engine oil led with 61.12% of the total volume in 2025.

Which end-user industry will grow the fastest through 2031?

The industrial segment, including power generation, supported by 38 GW of gas-turbine projects, is expected to post a 4.56% CAGR.

How are tariffs affecting electric-vehicle penetration?

A 15% customs duty introduced in December 2025 has slowed EV import growth, keeping BEV share below 7% by 2031.

Page last updated on: