United States Antacids Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

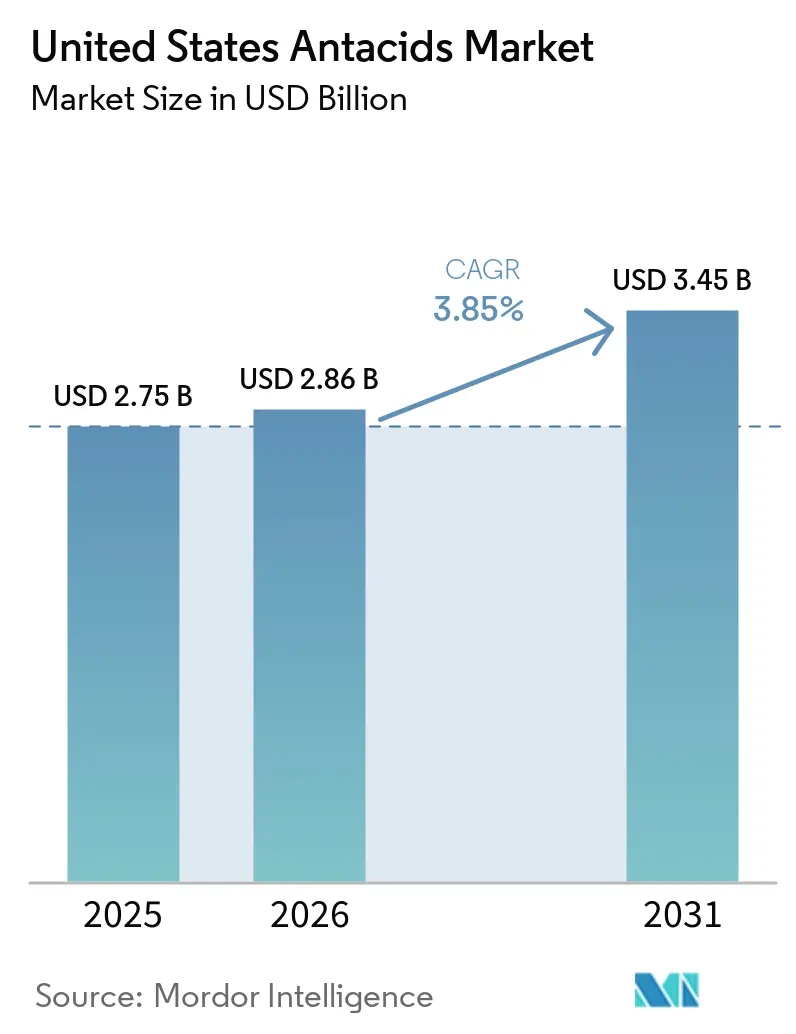

| Base Year Market Size (2025) | USD 2.75 Billion |

| Market Size (2026) | USD 2.86 Billion |

| Market Size (2031) | USD 3.45 Billion |

| Growth Rate (2026 - 2031) | 3.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Antacids Market Analysis by Mordor Intelligence

The United States Antacids Market size is projected to expand from USD 2.75 billion in 2025 and USD 2.86 billion in 2026 to USD 3.45 billion by 2031, registering a CAGR of 3.85% between 2026 to 2031.

The United States (US) antacids market continues to draw steady demand from an aging population, since all baby boomers will be age 65 or older by 2030 and older adults experience reflux conditions at materially higher rates than younger groups. Dietary behavior is adding a second layer of support, as adults in the United States derived 53% of daily calories from ultra-processed foods between 2021 and 2023, which sustains recurring heartburn and acid discomfort across a broad consumer base. These conditions keep baseline demand in the US antacids market resilient even when consumer spending becomes more selective, because heartburn relief remains a low-ticket and need-based purchase. At the same time, the US antacids market is splitting between established formats such as tablets and newer growth pockets such as gummies, alginate formulations, and e-commerce, which requires manufacturers to manage both volume stability and product renewal in parallel. The competitive setting remains moderate rather than tight, with branded leaders defending shelf space, private-label suppliers absorbing value demand, and therapeutic substitution plus safety messaging shaping how companies position products and channel investments.

Key Report Takeaways

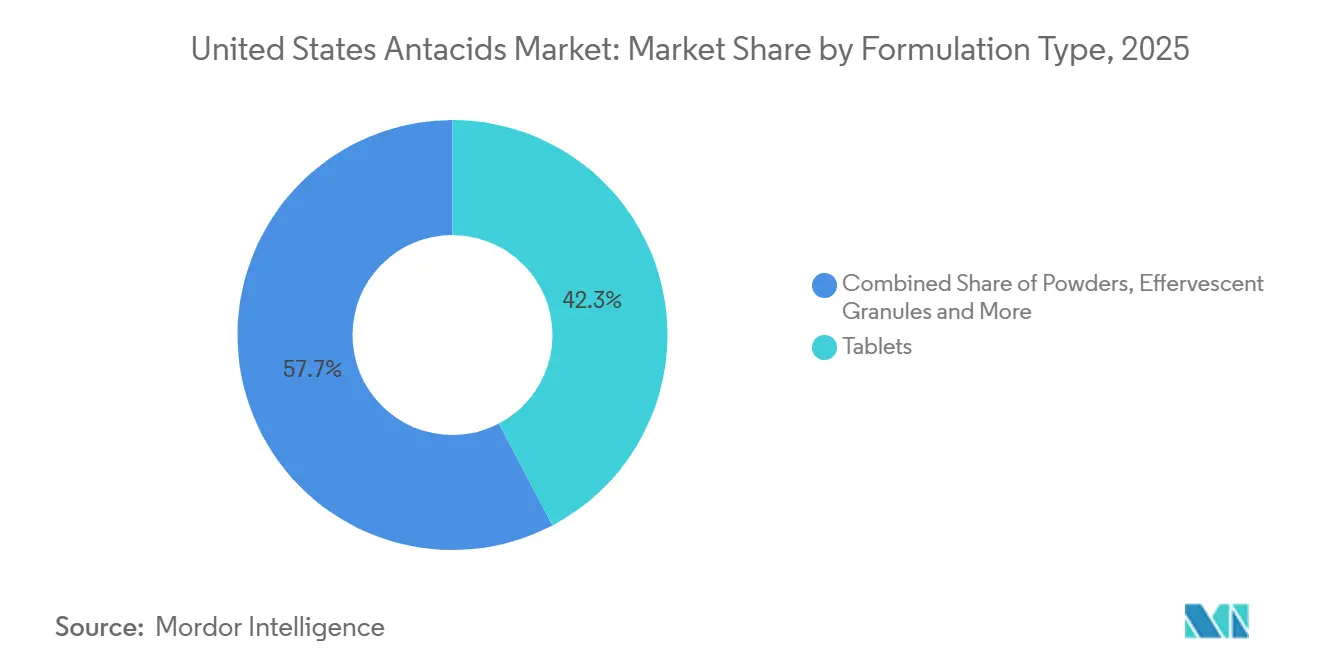

- By formulation type, tablets held 42.31% of the US antacids market share in 2025, while gummies and chewable soft-gels are projected to expand at a 6.38% CAGR through 2031.

- By active ingredient type, calcium carbonate held 35.24% revenue share in 2025, while alginate-based products are forecast to grow at a 7.52% CAGR through 2031.

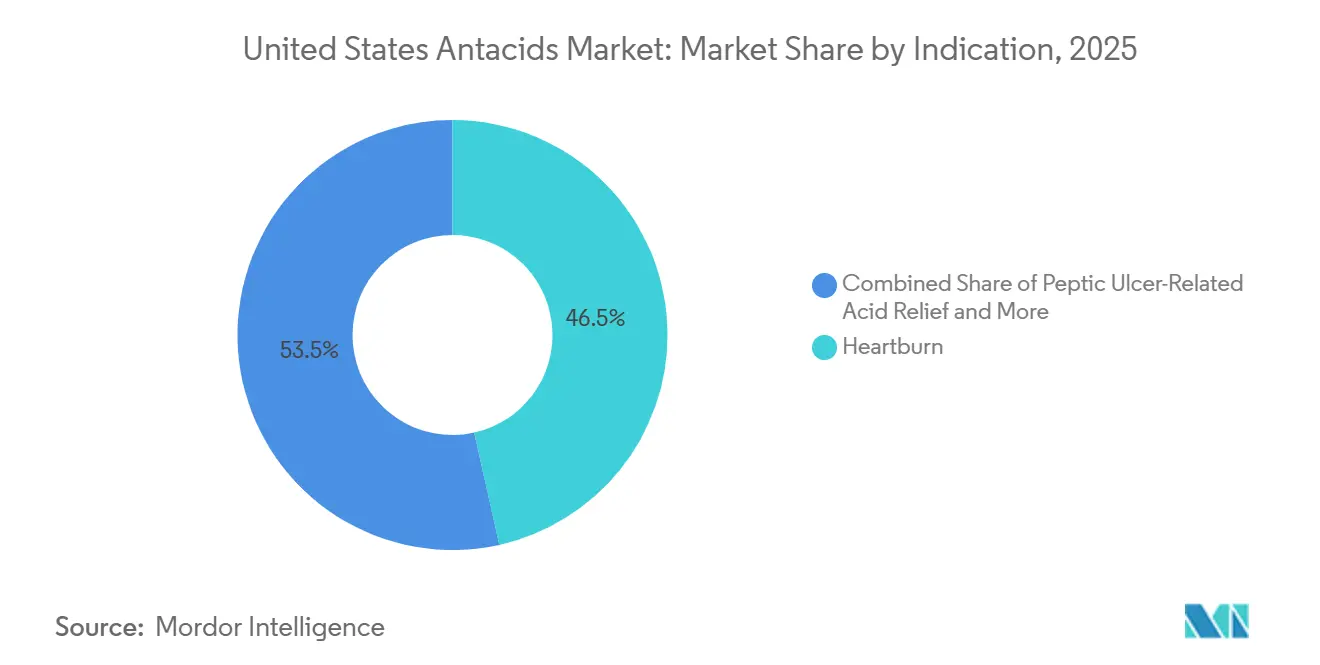

- By indication, heartburn accounted for 46.52% of revenue in 2025, while functional dyspepsia is projected to advance at a 7.25% CAGR through 2031.

- By distribution channel, retail pharmacies and drug stores accounted for 38.24% share of the US antacids market size in 2025, while e-commerce is projected to grow at a 7.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Antacids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population And Sustained Heartburn Prevalence | +1.2% | National, with elevated impact in South and Midwest states | Long term (≥ 4 years) |

| Unhealthy Diets And Episodic Reflux Triggers | +0.8% | National, highest in South and Midwest | Medium term (2-4 years) |

| OTC Accessibility And Self-Medication Behavior | +0.7% | National, accelerating in suburban and rural markets | Medium term (2-4 years) |

| Retail Pharmacy And E-Commerce Expansion | +0.5% | National, accelerating in urban hubs and e-commerce-dense markets | Short term (≤ 2 years) |

| Clean-Label Challenger Brands Broaden Category Appeal | +0.3% | Pacific West, Northeast, and major metropolitan markets | Medium term (2-4 years) |

| Convenience-Led Route-To-Market Expansion | +0.2% | National, with early gains in suburban and on-the-go consumer segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population And Sustained Heartburn Prevalence

The US antacids market is supported by the speed of demographic aging, not only by the size of the older population. All baby boomers will be age 65 or older by 2030, which means the US antacids market will keep drawing demand from an age group with higher exposure to reflux and chronic digestive discomfort. Population studies continue to place GERD prevalence in North America at 18.1% to 27.8%, and reflux oesophagitis incidence peaks between ages 60 and 70. This matters because older users tend to repurchase more regularly, which gives the US antacids market a dependable demand floor that is less exposed to the swings seen in more discretionary consumer categories. Brands that focus too narrowly on younger clean-label buyers risk missing a loyal older customer base that still values familiar relief formats, lower-sodium options, and easy-to-swallow products.

Unhealthy Diets And Episodic Reflux Triggers

The US antacids market also benefits from a dietary pattern that keeps episodic reflux active across income groups and age bands. Adults in the United States derived 53% of daily calories from ultra-processed foods between 2021 and 2023, which is associated with higher body weight, greater intra-abdominal pressure, and more frequent acid reflux triggers. The CDC reported in December 2025 that every state and territory had adult obesity prevalence of at least 25%, with the Midwest at 35.8% and the South at 34.6%[1]Centers for Disease Control and Prevention, “2024 Adult Obesity Prevalence Maps,” Centers for Disease Control and Prevention, cdc.gov. The USDA and HHS dietary guidance also continued to emphasize the health burden linked to ultra-processed food patterns, which reinforces the persistence of reflux-provoking diets rather than a temporary spike in poor eating habits. This keeps the US antacids market supplied with repeat demand from consumers who move from occasional heartburn to more frequent self-treatment over time.

OTC Accessibility And Self-Medication Behavior

The US antacids market remains easy to access because antacid products sit inside the FDA OTC monograph framework and do not require a prescription for routine purchase. This gives consumers a short decision path, since heartburn relief can be purchased directly at retail without a physician visit, prior authorization, or reimbursement process. The result is a market where self-medication behavior supports stable volume and where brand choice is often made at the shelf, on the retailer app, or through repeat purchasing habits. That pattern is especially useful for the US antacids market in suburban and rural areas, where OTC access often fills the gap between symptoms and formal clinical evaluation. For manufacturers, this means visibility, assortment, and simple communication remain central levers because the consumer often controls the full purchase cycle from symptom recognition to product selection.

Retail Pharmacy And E-Commerce Expansion

Distribution change is becoming one of the clearest structural shifts in the US antacids market. E-commerce is the fastest-growing channel in the US antacids market with a 7.83% CAGR through 2031, while retail pharmacies still carry the largest revenue share and remain central to impulse and refill purchases. The October 2025 closure of all remaining Rite Aid stores redistributed significant OTC shelf space toward CVS, Walgreens, Kroger, and Albertsons, which increased the influence of the largest pharmacy and food retail chains over category placement. This shift strengthens the hand of retailers with large private-label programs and puts more pressure on branded players to defend placement, pricing, and visibility across both physical and digital shelves. The US antacids market therefore faces a dual channel reality, with store presence still shaping immediate purchases and e-commerce gaining importance for planned replenishment, subscription ordering, and broader assortment discovery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Switching To PPIs And H2 Blockers | -0.6% | National, concentrated among chronic GERD patients aged 45+ | Long term (≥ 4 years) |

| Safety Concerns With Chronic Antacid Use | -0.4% | National, amplified by FDA-mandated label disclosures | Medium term (2-4 years) |

| Private-Label Price Transparency And Margin Pressure | -0.3% | National, most pronounced in mass retail and club store channels | Short term (≤ 2 years) |

| Ingredient-Transparency Scrutiny On Dyes And Excipients | -0.2% | Pacific West, Northeast, and health-conscious urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Switching To PPIs And H2 Blockers

Therapeutic substitution remains the primary restraint on the US antacids market because chronic heartburn sufferers often look for longer-lasting acid suppression than a standard antacid provides. PPIs are positioned around 24-hour suppression and H2 blockers around longer relief windows than antacids, so frequent sufferers can move up the treatment ladder when symptoms become more regular. This creates a real retention challenge for the US antacids market, especially among consumers who experience heartburn several times each week and begin to see rapid relief as less important than duration. At the same time, clinical discussion around PPI use has become more active, and step-down treatment remains part of the conversation for appropriate patients who do not need continuous high-intensity suppression. That means the US antacids market is not facing a one-way exit into other therapies, but brands still need to explain where antacids fit in a broader symptom-management pathway if they want to retain users over time.

Safety Concerns With Chronic Antacid Use

Safety messaging is the second meaningful restraint on the US antacids market, especially for products used too frequently or at the maximum labeled dose. FDA labeling under the OTC antacid framework states that consumers should not use the maximum dosage for more than 2 weeks without physician supervision. This has particular relevance for calcium carbonate products, which lead the category and also carry clinician concern around hypercalcaemia and milk-alkali syndrome when used chronically at high doses[2]DailyMed, “Calcium Carbonate (Antacid) Chewable Tablet,” U.S. National Library of Medicine, dailymed.nlm.nih.gov. The warning language makes it harder for the US antacids market to stretch into an everyday wellness position, because the label clearly frames these products as short-term symptom relief rather than long-term routine use. It also gives non-calcium and differentiated formulations a chance to position around a different safety conversation, even if the overall category still operates under the same regulatory baseline.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Formulation Type: Tablets Lead, Gummies Reshape the Format Calculus

Tablets accounted for 42.31% of the US antacids market share in 2025, and that lead came from long-standing consumer familiarity, broad shelf placement, and manufacturing scale that supports competitive pricing. Chewable tablet products from established brands remain embedded across pharmacy planograms and mass retail aisles, which keeps the format highly visible for both planned and impulse purchases. Liquids and suspensions continue to serve older adults and consumers with swallowing difficulty, which gives them a stable role despite the dominance of solid formats. Powders and effervescent granules still address a smaller convenience-oriented need state for users who want portability or fast mixing.

Gummies and chewable soft-gels are the fastest-growing formulation segment, with a 6.38% CAGR expected through 2031. Their rise reflects a broader format shift that has already reshaped vitamins and supplements, where consumers increasingly prefer easier taste profiles and more approachable dosage forms. Younger adults, especially those aged 18 to 45, show higher trial rates for gummy-style products because they reduce the chalky texture associated with traditional antacid tablets. Quest Products reinforced that direction in May 2026 with the launch of OraHealth Antacid Melts, a stick-on product for nighttime heartburn relief that extends the US antacids market beyond the long-established tablet and liquid format set.

By Active Ingredient Type: Calcium Carbonate Anchors Volume, Alginate Captures Clinical Interest

Calcium carbonate held 35.24% of active ingredient revenue in 2025, which kept it at the center of the US antacids industry because of low production cost, a familiar safety profile under labeled use, and well-established monograph compliance. Magnesium-based products held the next important position, supported by consumer recognition of their digestive effect at higher doses. Aluminium compounds remained less favored because long-running concern around tolerability and perception has weakened consumer appeal, even where the underlying discussion remains contested. Combination products such as calcium carbonate plus magnesium hydroxide continue to benefit from a broader buffering profile, but alginate-based products stand out as the fastest-growing group with a 7.52% CAGR through 2031.

Alginate products are gaining attention because they do not rely only on neutralizing acid, but also form a physical raft barrier above gastric contents. A 2025 Scientific Reports study found comparable efficacy between generic and original alginate formulations in PPI-refractory GERD patients, which gives the US antacids industry a stronger clinical basis for differentiated positioning. That distinction matters because brands can speak to a different mechanism of action without leaving the OTC channel or requiring a prescription step. Haleon is well placed in this part of the US antacids market through its global exposure to both TUMS and Gaviscon, yet the domestic opportunity remains open enough for specialists and direct-to-consumer brands to move first if larger players stay measured in their rollout[3]Haleon plc, “2025 Full Year Results,” Haleon plc, haleon.com.

By Indication: Heartburn Dominates, Functional Dyspepsia Emerges as the Volume Frontier

Heartburn accounted for 46.52% of revenue in 2025, which confirms that the US antacids market is still anchored in fast relief for post-meal or trigger-related discomfort. GERD remains the next important indication, but it is harder to capture fully because many chronic sufferers are moved toward longer-duration therapies as symptoms become more severe or more frequent. That leaves occasional and intermittent users as the core volume engine, especially in OTC channels where the first response to symptoms is often self-treatment rather than a physician visit. Functional dyspepsia, however, is emerging as the fastest-growing indication in the US antacids market, with a projected 7.25% CAGR through 2031.

The commercial appeal of functional dyspepsia comes from underdiagnosis as much as from symptom prevalence. A population study published in The Lancet Gastroenterology & Hepatology found that 10% to 12% of adults in the United States meet Rome IV symptom criteria for functional dyspepsia. Many of these consumers self-medicate without receiving a formal diagnosis, which routes purchasing behavior toward antacids by default rather than through a prescription pathway. The US antacids market also has a smaller emerging pocket tied to gastric discomfort linked with GLP-1 receptor agonist use, and while this demand is not yet formally carved out in most indication frameworks, it is widening the set of occasions in which consumers reach for OTC acid relief.

By Distribution Channel: Retail Pharmacy Leads, E-Commerce Restructures the Purchase Journey

Retail pharmacies and drug stores accounted for 38.24% share of the US antacids market size in 2025, which kept them as the largest distribution route for the category. Their strength comes from high trip frequency, trusted placement in healthcare-oriented stores, and the habit of picking up digestive relief alongside prescriptions or other OTC products. Hospital pharmacies still serve a steady institutional role, especially for liquid formulations used around inpatient acid-related care and related co-morbidities. The October 2025 exit of Rite Aid from the remaining store base shifted category volume toward CVS, Walgreens, Kroger, and Albertsons, which increased retailer leverage and supported stronger private-label positioning in the US antacids market.

E-commerce is the fastest-growing distribution channel, with a 7.83% CAGR expected through 2031. That pattern fits how antacids are purchased, because some orders happen after symptoms begin while others are made in advance of travel, known trigger foods, or regular replenishment cycles. Subscription and auto-replenishment models are especially suited to the planned side of demand, where consumers want to avoid running out of a familiar relief product. Amazon Basic Care and other store-brand listings also intensify price comparison and reduce the advantage branded products once enjoyed from physical shelf visibility alone. The practical result is that the US antacids market now treats digital storefronts as a primary route to repeat demand rather than a secondary extension of brick-and-mortar distribution.

Geography Analysis

The US antacids market covers a single country, yet consumption patterns differ meaningfully across regions inside the United States. The South and Midwest support some of the strongest underlying demand conditions, since adult obesity prevalence reached 34.6% in the South and 35.8% in the Midwest in the CDC’s December 2025 maps. Those regions tend to favor tablets and liquids, and they remain important demand zones for private-label products supplied by Perrigo and contract manufacturers serving value-oriented retail channels. The Northeast presents a different profile, with higher household incomes, stronger brand loyalty, and a greater willingness to pay for premium tablet and gummy products within the US antacids market.

The Western United States, especially California, Washington, and Oregon, carries stronger demand for ingredient transparency and cleaner label positioning in the US antacids market. That consumer stance aligns with the continued policy focus on limiting ultra-processed food intake and with a retail environment where label reading plays a larger role in purchase decisions. California adds another layer because Proposition 65 warning expectations and a more active regulatory climate raise sensitivity around dyes, titanium dioxide, talc, and other excipients. Wonderbelly’s formulation style fits that regional backdrop, and its later acquisition by Procter & Gamble gives a larger company a clearer route into this part of the market. The Mountain West and Southwest, with younger population profiles and continuing population growth, are also opening room for convenience-led products such as gummies and stick-on melts.

Rural parts of the Midwest and South present a separate opportunity set for the US antacids market because product use is high by volume while e-commerce adoption remains less central to the purchase path. In these areas, pharmacy shelf presence still matters more than elaborate digital merchandising, especially for value-tier brands and familiar tablets. Rite Aid’s disappearance removed a visible brick-and-mortar option in some communities and temporarily altered local OTC access where the chain had maintained a stronger footprint. As prescription files and store traffic shift toward CVS, Walgreens, independent pharmacies, and dollar stores, the US antacids market gains an unconventional opening for private-label and lower-priced brands that can secure replacement shelf space quickly.

Competitive Landscape

The US antacids market shows moderate concentration in branded products and much broader fragmentation in the private-label layer. Haleon holds the strongest branded position through TUMS and also benefits from Nexium 24HR in OTC reflux care, while digestive health contributed 17.7% of Haleon’s global revenue in 2025. Procter & Gamble has built a wide digestive health presence across Pepto-Bismol, Rolaids, and Prilosec OTC, and it widened that reach in January 2026 by acquiring Wonderbelly, a clean-label antacid brand. Infirst Healthcare with Mylanta, Bayer with Alka-Seltzer, and Perrigo in store-brand supply all hold meaningful roles, and Perrigo reported store-brand share gains in 2025 even as broader category demand softened.

A clear gap remains where clinical credibility meets ingredient transparency in the US antacids market. Alginate products have a stronger clinical story than many consumers recognize, and the 2025 Scientific Reports evidence around efficacy in PPI-refractory GERD suggests a differentiated growth lane that remains underdeveloped in the United States. That leaves room for direct-to-consumer and digitally native brands to compete on mechanism and label simplicity at the same time. It also means established players cannot rely only on brand history, because format, ingredient messaging, and digital repeat ordering are steadily becoming more important in how the US antacids market allocates growth.

Strategic activity is already reshaping the field. Procter & Gamble’s Wonderbelly acquisition added a cleaner-label platform to an already broad digestive health portfolio, and Quest Products’ May 2026 launch of OraHealth Antacid Melts showed that differentiated delivery formats can still open new usage occasions in the US antacids market. Kimberly-Clark’s planned acquisition of Kenvue, expected to close in the second half of 2026, may also change how digestive health investment is prioritized across adjacent brands and categories. At the same time, FDA monograph compliance remains the shared operating baseline for all competitors. Companies that move earlier on excipient transparency and cleaner formulations will likely face lower reformulation friction if regulatory expectations tighten, while brands that stay dependent on price alone will remain vulnerable to retailer power and private-label competition.

United States Antacids Industry Leaders

Haleon plc

Bayer AG

Perrigo Company plc

Procter & Gamble Co.

Infirst Healthcare USA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Quest Products launched OraHealth Antacid Melts, the first stick-on antacid for nighttime heartburn relief, using proprietary Stick-On Melt technology. The product entered CVS in 40-count packs at the May 18 reset, extending the antacid format innovation beyond traditional tablets and liquids and targeting the underserved nocturnal heartburn occasion.

- January 2026: Procter & Gamble completed the acquisition of Wonderbelly, a clean-label OTC antacid brand founded in Austin, Texas, for an undisclosed sum. The deal added a dye-free, talc-free, non-GMO antacid platform to P&G's digestive health portfolio alongside Pepto-Bismol, Rolaids, and Prilosec OTC, accelerating the company's reach into ingredient-conscious consumer segments.

United States Antacids Market Report Scope

As per the scope of the report, antacids are substances that neutralize stomach acid, helping to relieve symptoms of indigestion, heartburn, and acid reflux. They work by directly counteracting stomach acidity to provide relief from discomfort.

The United States antacids market is segmented by formulation type, active ingredient type, indication, and distribution channel. By formulation type, the market includes tablets, liquids/suspensions, powders, gummies/chewable soft-gels, effervescent granules, and other formulations. By active ingredient type, the segmentation covers calcium carbonate, magnesium compounds, aluminum compounds, sodium bicarbonate, alginate-based, and combination preparations. By indication, the market is categorized into heartburn, gastroesophageal reflux disease (GERD), peptic ulcer-related acid relief, functional dyspepsia, and other indications. By distribution channel, the segmentation includes retail pharmacies and drug stores, e-commerce, hospital pharmacies, and other distribution channels. For each segment, the market size and forecast are provided in terms of value (USD).

| Tablets |

| Liquids / Suspensions |

| Powders |

| Gummies / Chewable Soft-Gels |

| Effervescent Granules |

| Other Formulations |

| Calcium Carbonate |

| Magnesium Compounds |

| Aluminium Compounds |

| Sodium Bicarbonate |

| Alginate-Based |

| Combination Preparations |

| Heartburn |

| Gastroesophageal Reflux Disease (GERD) |

| Peptic Ulcer-Related Acid Relief |

| Functional Dyspepsia |

| Other Indications |

| Retail Pharmacies & Drug Stores |

| E-Commerce |

| Hospital Pharmacies |

| Other Distribution Channels |

| By Formulation Type | Tablets |

| Liquids / Suspensions | |

| Powders | |

| Gummies / Chewable Soft-Gels | |

| Effervescent Granules | |

| Other Formulations | |

| By Active Ingredient Type | Calcium Carbonate |

| Magnesium Compounds | |

| Aluminium Compounds | |

| Sodium Bicarbonate | |

| Alginate-Based | |

| Combination Preparations | |

| By Indication | Heartburn |

| Gastroesophageal Reflux Disease (GERD) | |

| Peptic Ulcer-Related Acid Relief | |

| Functional Dyspepsia | |

| Other Indications | |

| By Distribution Channel | Retail Pharmacies & Drug Stores |

| E-Commerce | |

| Hospital Pharmacies | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is driving demand for antacid products in the United States?

Demand is being supported by population aging and dietary patterns that keep reflux and heartburn common. The market was valued at USD 2.75 billion in 2025 and is projected to reach USD 3.45 billion by 2031 at a 3.85% CAGR.

Which formulation leads sales in the United States?

Tablets led with 42.31% of revenue in 2025 because they remain familiar, widely stocked, and price competitive across pharmacy and mass retail channels.

Which product formats are growing the fastest?

Gummies and chewable soft-gels are forecast to grow at a 6.38% CAGR through 2031, helped by better taste acceptance and broader trial among younger adults.

Why are alginate-based products gaining attention?

Alginate-based products are projected to expand at a 7.52% CAGR through 2031 because they offer a different mechanism of action by forming a physical barrier above gastric contents.

Which indication generates the most revenue?

Heartburn remained the largest indication with 46.52% of revenue in 2025, while functional dyspepsia is the faster-growing pocket at a 7.25% CAGR through 2031.

How is distribution changing for antacid brands?

Retail pharmacies and drug stores still led with 38.24% of revenue in 2025, but e-commerce is growing faster at a 7.83% CAGR through 2031 as consumers increasingly use planned replenishment and subscription models.

Page last updated on: