United States Aluminum Beverage Cans Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

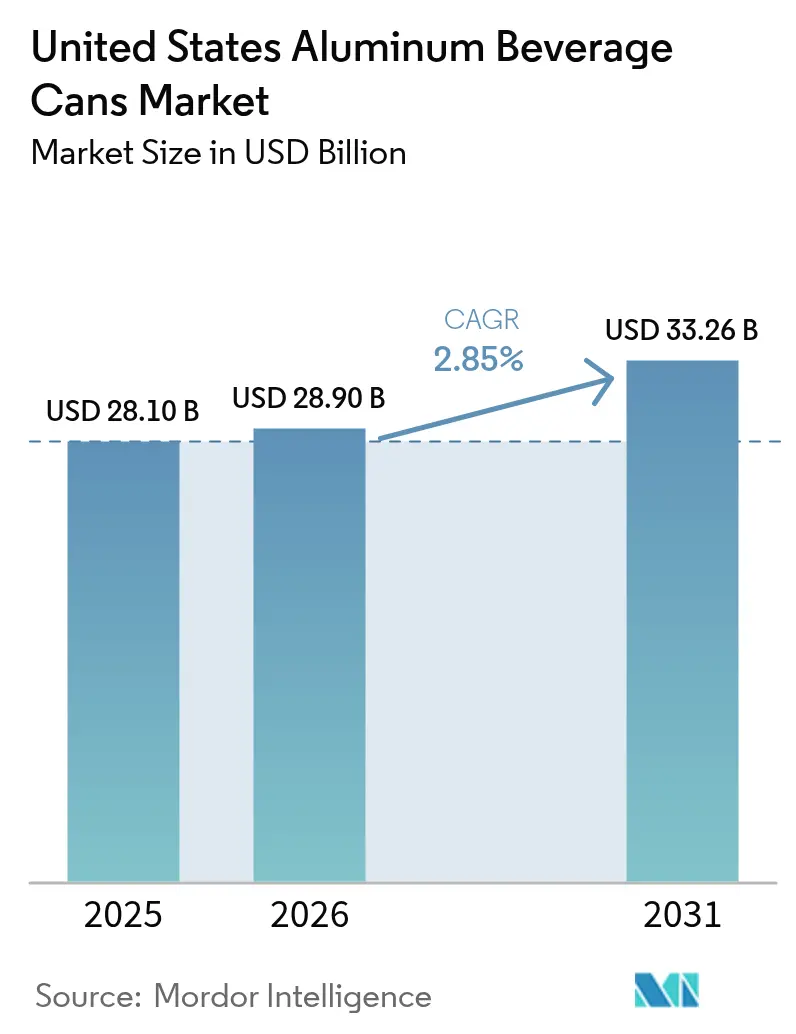

| Base Year Market Size (2025) | USD 28.10 Billion |

| Market Size (2026) | USD 28.9 Billion |

| Market Size (2031) | USD 33.26 Billion |

| Growth Rate (2026 - 2031) | 2.85% CAGR |

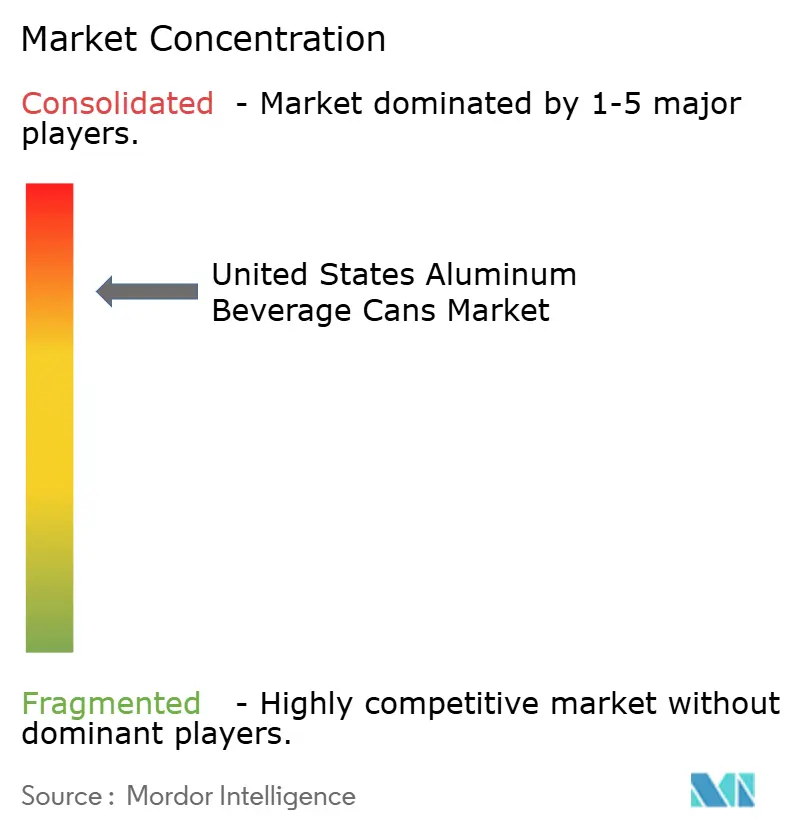

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Aluminum Beverage Cans Market Analysis by Mordor Intelligence

The United States aluminum beverage cans market size in 2026 is estimated at USD 28.9 billion, growing from 2025 value of USD 28.10 billion with 2031 projections showing USD 33.26 billion, growing at 2.85% CAGR over 2026-2031. Demand remains resilient as large beverage brand owners tighten sustainability targets, while two-piece draw-and-iron technology keeps production costs in check despite aluminum tariffs that inflate domestic metal prices by about 10%. Capacity additions such as Novelis’s Bay Minette rolling mill are expected to ease sheet shortages from 2026, but lead times for non-contract buyers still extend to 12-16 weeks. Equipment upgrades that integrate IoT sensors cut change-over losses by 8-12%, helping fillers offset higher material costs. Ongoing FDA restrictions on PFAS will require full coating reformulations by 2026, creating short-term compliance costs but long-term competitive advantage for first move.

Key Report Takeaways

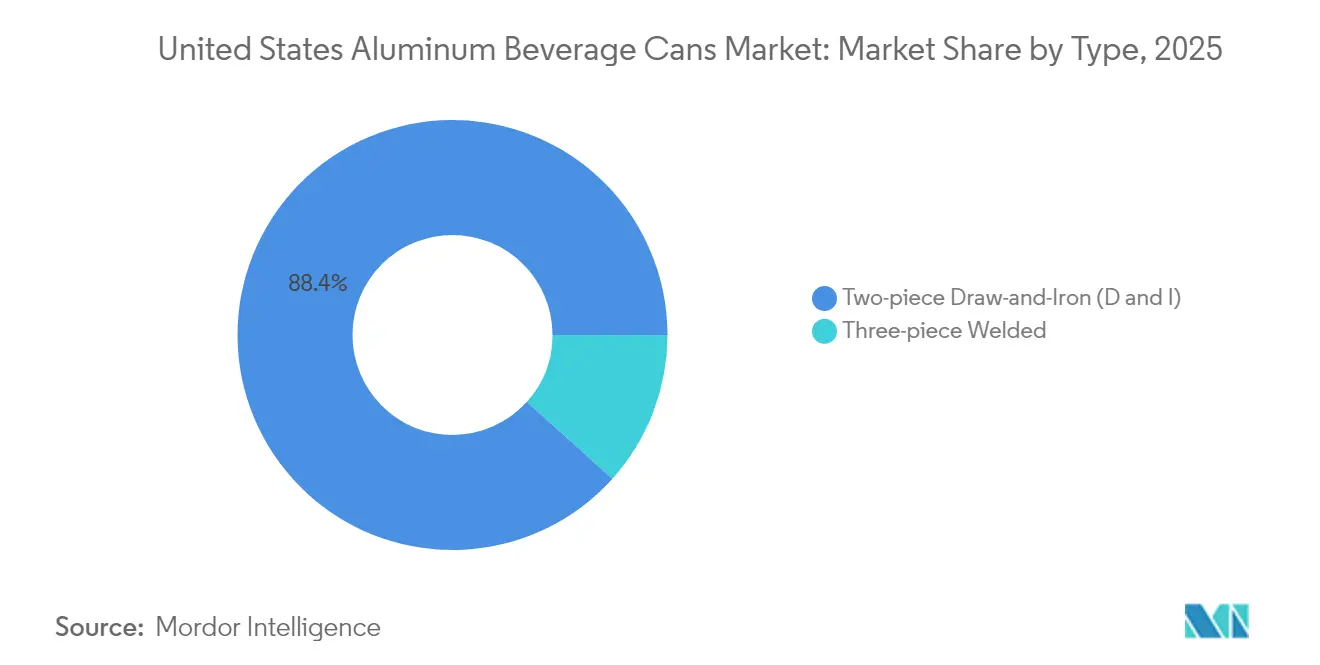

- By type, two-piece draw-and-iron technology held 88.35% of the United States aluminum beverage cans market share in 2025 and is projected to expand at a 3.58% CAGR through 2031.

- By beverage type, flavored alcoholic drinks led growth and are set to record a 3.95% CAGR between 2026 and 2031, while beer retained 31.05% revenue share in 2025.

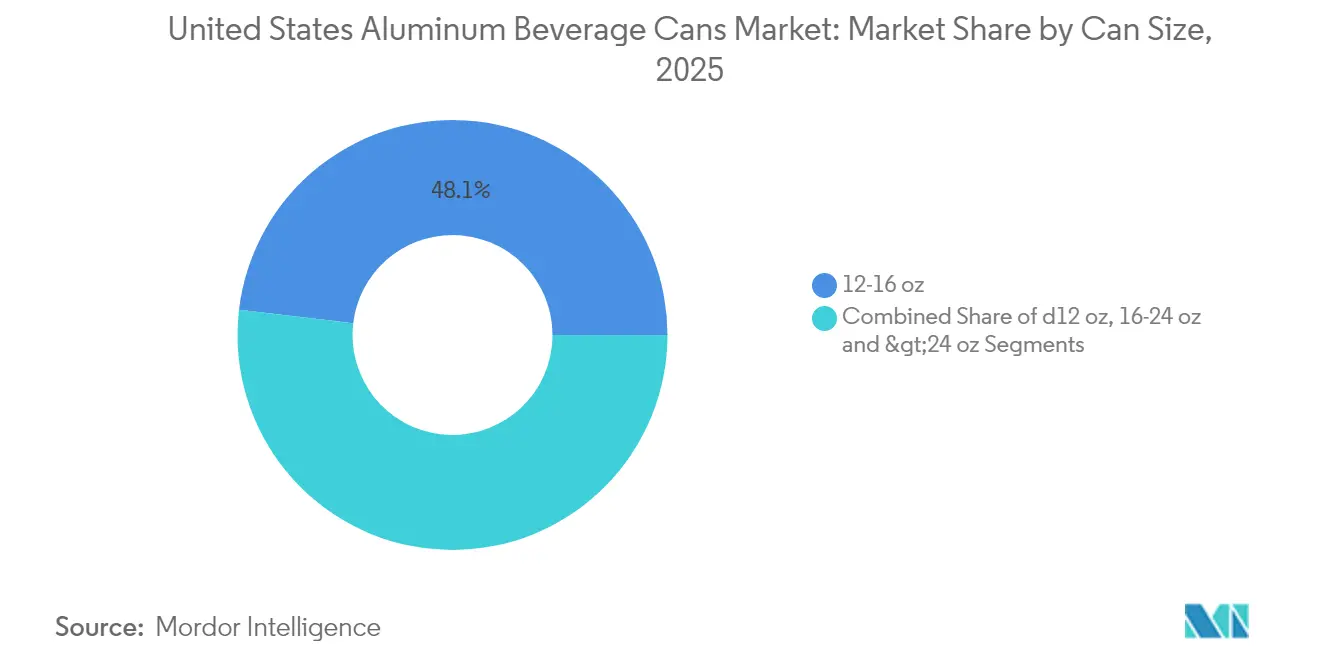

- By can size, the ≤12-oz segment captured 3.39% CAGR potential through 2031, whereas 12-16 oz formats maintained 48.12% share of the United States aluminum beverage cans market size in 2025.

- By distribution channel, direct sales accounted for 64.10% of the United States aluminum beverage cans market share in 2025, while indirect channels are forecast to rise at a 4.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Aluminum Beverage Cans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from non-alcoholic beverage producers | +0.8% | National – Southeast and West Coast | Medium term (2-4 years) |

| Surge in craft beer and hard seltzer launches | +0.9% | National – Colorado, California, North Carolina | Short term (≤ 2 years) |

| Corporate ESG targets favoring infinitely recyclable packaging | +0.6% | National – led by Fortune 500 beverage companies | Long term (≥ 4 years) |

| Aluminum smelter capacity expansions in North America | +0.4% | Gulf Coast and Pacific Northwest | Long term (≥ 4 years) |

| IoT-enabled filling lines | +0.3% | Major metropolitan hubs | Medium term (2-4 years) |

| Blockchain traceability pilots | +0.2% | Premium beverage segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Non-Alcoholic Beverage Producers

Energy drink and ready-to-drink coffee brands favor aluminum formats to boost shelf life and brand differentiation. Red Bull’s Phoenix complex runs a through-the-wall setup that merges can making with beverage filling, trimming logistics costs, and protecting its proprietary 250 ml format. National retailers report that aluminum containers lift premium shelf pricing by 6-8%, allowing functional beverage makers to maintain margins despite stiff competition. RTD tea producers similarly leverage aluminum’s light barrier to save 25% in cold-chain expenses compared with PET. These format advantages are translating into firm purchase commitments that lock in rolled sheet contracts through 2027. As demand widens beyond energy drinks into sports nutrition beverages, small fillers expect can volumes to rise another 5% annually.

Surge in Craft Beer and Hard Seltzer Launches

Hard seltzer’s sleek 12 oz profile became a packaging standard after multiple brands captured double-digit share in flavored alcohol sales during 2024. Craft breweries that once relied on bottles migrated to cans as large converters like Ball offered short-run graphics and lighter gauge material. However, spot buyers paid up to 60% premiums in 2024 when contract volumes were fully allocated, forcing many small breweries to secure distributor-managed inventory buffers. With capacity additions coming online, price gaps are narrowing, yet sleek and 16 oz formats continue to dominate new product launches as consumers associate cans with freshness and recyclability. The trend is likely to persist as alcoholic sparkling teas and spirit-based RTDs replicate hard seltzer’s marketing playbook.

Corporate ESG Targets Favoring Infinitely Recyclable Packaging

Ball’s Perfect Circle roadmap aims for 90% global collection rates and 85% recycled content by 2030, aligning with beverage brand pledges for fully recyclable packaging. [1]Ball Corporation, “Resource Efficiency,” ball.comThese commitments elevate demand for can-sheet that carries ≥70% recycled aluminum, prompting premium fees of 12–15 USD per tonne. Novelis committed USD 2.5 billion to rolling and recycling upgrades that support higher post-consumer content. CPGs are inserting minimum recycled-content clauses into multiyear supply contracts, effectively locking in demand growth for closed-loop can material even as overall beverage volumes plateau.

Aluminum Smelter Capacity Expansions in North America

The 600,000-tonne Bay Minette plant remains the single largest addition planned for U.S. beverage can sheet, though commissioning slipped to late 2025 due to equipment delays. Additional debottlenecking projects in the Pacific Northwest aim to leverage renewable hydroelectric power to reduce scope-2 emissions for can-sheet. Once operational, fresh capacity should shave freight costs for West Coast fillers by roughly USD 80 per tonne. In the interim, converters are maintaining higher inventory days to mitigate sheet shortages during seasonal demand spikes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PET lightweighting and tethered-cap compliance | -0.4% | Regions with active EPR programs | Medium term (2-4 years) |

| Domestic aluminum price volatility from Section 232 tariffs | -0.6% | Nationwide – highest for non-integrated fillers | Short term (≤ 2 years) |

| Can-sheet coil bottlenecks | -0.5% | Areas distant from Gulf Coast mills | Medium term (2-4 years) |

| High capex for 3-piece to Dand I conversion | -0.3% | Small regional producers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PET Lightweighting and Tethered-Cap Compliance

Competing PET bottle suppliers trimmed resin by up to 10% per unit in 2024, narrowing the delivered-cost gap with cans. European tethered-cap mandates inspired a pipeline of universal lid systems that global beverage multinationals could adopt across regions, threatening can volumes if consumer acceptance grows. State-level extended producer responsibility legislation will add further compliance costs to all packaging materials, though aluminum’s 30-day average recycling loop remains an advantage. To counter PET’s advances, can makers are testing even thinner gauges and exploring printable embossing to maintain brand shelf impact without extra weight.

Domestic Aluminum Price Volatility from Section 232 Tariffs

Section 232 duties keep Midwest Transaction Prices 15–20% above LME trends, pressuring converters that lack vertical integration and forcing quarterly surcharge pass-throughs to beverage customers. Spot price swings of up to 5 cents per pound in 2024 compelled some small fillers to hedge through distributor pools, raising working capital needs. If tariff relief does not emerge, continued cost uncertainty could dampen can adoption among emerging beverage brands with thin margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Production Efficiency Anchors D and I Dominance

Two-piece draw-and-iron cans accounted for 88.35% of the United States aluminum beverage cans market share in 2025, and performance gains should lift this segment at a 3.58% CAGR to 2031. Ball’s STARcan family already delivers up to 8% weight savings versus legacy D and I designs, reinforcing margins as metal premiums rise. Incremental lightweighting through base compression and alloy refinements reduces material consumption while preserving the top-load strength required for high-speed filling. Embedded vision systems now inspect every formed shell, cutting defect rates below 50 parts per million and minimizing scrap.

Three-piece welded cans remain a niche for specialty beverages that favor distinctive shapes, yet the FDA’s PFAS phase-out will drive coating redesign and could accelerate their decline. Production cycle times for welded formats remain roughly 30% slower than high-speed D and I lines, discouraging volume beverages from adopting them. Nonetheless, select craft producers opt for three-piece to create retro branding cues, and aerospace-grade coatings under development may extend shelf life for acidic juice blends. Capital requirements for D and I presses, however, still deter small fillers, leaving limited pockets of demand for welded cans.

By Beverage Types: Flavored Alcoholic Drinks Sustain Outperformance

Flavored alcoholic beverages, led by hard seltzer line extensions, are forecast to post a 3.95% CAGR and will continue outpacing core beer volumes through 2031. Sleek 12-oz formats deliver strong visual differentiation at retail while catering to calorie-conscious consumers who prefer smaller serving sizes. Carbonated soft drinks retain a broad consumption base, but growth trails functional beverage categories that promise energy, immunity, or hydration benefits.

RTD coffee and tea exploit aluminum’s barrier to oxygen and light, allowing ambient shipping for products that once required costly refrigeration. As nitro coffee grows, pressurized aluminum containers provide consistent crema, sparking partnerships between independent roasters and regional canners. Energy drinks sustain volume growth in 16 oz sizes, cementing aluminum’s role in high-impact branding with matte and textured finishes. Innovations in can lining chemistry now tolerate low-pH citrus mixes, opening potential for canned juice cocktails.

By Can Size: Premiumization Moves to Smaller Profiles

The ≤12 oz category is projected to rise at 3.39% CAGR through 2031, reflecting consumer appetite for portion control and premium positioning. Specialty coffee, hard kombucha, and craft beer brands often select 8-10 oz cans to justify higher unit pricing while managing alcohol or caffeine thresholds.

In contrast, the 12-16 oz bracket captured 48.12% of the United States aluminum beverage cans market size during 2025 and continues as the mainstream option for carbonated beverages and energy drinks. Larger 19.2 oz and 24 oz cans serve convenience-store multipacks and value beer offerings, but face cooler-space limitations. Manufacturer R and D now focuses on necked sleek variants that maintain shelf standout while enabling easier stacking for downstream logistics.

By Distribution Channel: Service Levels Drive Channel Choices

Direct contracts constituted 64.10% of the United States aluminum beverage cans market share in 2025, with brand owners valuing assured supply and joint innovation programs. Multi-year agreements allow converters to dedicate specific line time, stabilizing utilization rates above 90%.

Indirect channels, growing at 4.55% CAGR, cater to craft breweries and start-ups that lack volume scale. Specialist distributors aggregate orders, provide graphic design support, and finance working capital, but premiums range from 40% to 60% over direct pricing. Some intermediaries are installing small-batch digital printers to shorten lead times for limited-edition runs, helping emerging brands launch seasonal SKUs without committing to large minimums.

Geography Analysis

The Southeast ranks as the largest regional contributor, benefiting from proximity to Gulf Coast smelters and the Atlanta beverage corridor, where multiple fillers and brand headquarters cluster. Integrated supply chains shorten freight lanes, letting converters pass through lower delivered metal costs to local brand owners. Continued inward manufacturing investment in Alabama and Georgia could further entrench the region’s dominance once Novelis’s Bay Minette mill reaches full ramp in 2026.

The West Coast forms the second-largest consumption node but faces higher sheet freight surcharges, spurring can makers to hold larger local inventories. Craft beer density in California, Oregon, and Washington keeps demand buoyant, and container deposit laws enhance aluminum recovery rates that feed a closed-loop supply. However, periodic smelter curtailments in the Pacific Northwest, triggered by power price spikes, tighten alloy availability and inject price volatility.

Midwestern demand remains stable thanks to long-established soft-drink bottling hubs, though older equipment fleets require modernization to match the high-speed throughput of newer Southeast plants. The Northeast maintains niche premium beverage growth, leveraging dense urban markets but relying heavily on inbound sheet from Gulf producers. Emerging extended producer responsibility legislation could alter recycling economics across states, providing advantages to regions that already hit high collection benchmarks.

Competitive Landscape

Ball Corporation and Crown Holdings jointly control roughly 60–65% of United States aluminum beverage cans market share, reflecting a moderately consolidated structure. Ball’s acquisitions of Alucan in October 2024 and Florida Can Manufacturing in February 2025 added 1.2 billion-can annual capacity, securing slots for craft beverage growth. Crown’s capacity extensions in Virginia and Nevada bolster service to Western independents, raising its geographic balance.

Second-tier players Silgan Holdings, Ardagh Metal Packaging, and Independent Can Company pursue regional specialization or custom formats to sidestep head-on volume competition. Many invest in IoT-ready vision modules that lift line utilization and furnish real-time quality data to brand owners. Patent filings show heightened activity in PFAS-free coatings and alloy blends optimized for additive manufacturing, fields where smaller innovators could license technology to majors.[3]U.S. Patent Office, “Aluminum Alloy,” uspto.gov

Regulatory compliance costs favor scale operators able to spread R and D spending across multiple plants, yet white-space opportunities persist in shaped cans, tactile inks, and resealable end technology. Partnerships between coaters and converters accelerate qualification cycles as the 2026 PFAS deadline approaches, with early adopters likely to win premium beverage contracts seeking greener credentials.

United States Aluminum Beverage Cans Industry Leaders

Crown Holdings Inc.

Ball Corporation

Silgan Holdings Inc.

Ardagh Group S.A.

Envases Universales de México S.A. de C.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Ball Corporation completed the acquisition of Florida Can Manufacturing, adding two Southeastern plants with 1.2 billion-can capacity.

- January 2025: Constellium commercialized Aeral™ lightweight aluminum bottle technology, achieving 30% weight reduction versus impact-extruded designs.

- November 2024: Novelis launched its 3×30 circularity program to raise recycled content and cut carbon intensity across beverage can sheet.

- October 2024: Ball Corporation acquired Alucan to enhance premium can forming and specialty coating capabilities.

United States Aluminum Beverage Cans Market Report Scope

Aluminum beverage cans hold and dispense beverages like soft drinks, beer, and energy drinks. They are made from a thin sheet of aluminum that has been molded into the shape of a cylindrical can with a top and bottom cover. Aluminum cans are lightweight, durable, and transportable, making them a popular choice for beverage packaging. Furthermore, using aluminum cans protects the beverage's taste and freshness from light, air, and other external factors that can cause spoiling.

The US aluminum beverage cans market is segmented by type (2-piece and 3-piece) and application (carbonated soft drinks, beer, water, energy drinks, and other applications). The report offers market forecasts and size in value (USD) for all the above segments.

| Aluminium |

| Steel |

| Two-Piece |

| Three-Piece |

| Monobloc Aerosol |

| ≤12 oz |

| 250-500 ml |

| 500-1,000 ml |

| >1,000 ml |

| Drawn and Ironed (DandI) |

| Drawn and Redrawn (DRD) |

| Impact Extrusion |

| Food |

| Beverage |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| Paints and Industrial Chemicals |

| Automotive Fluids and Lubricants |

| Other End-User Industry |

| By Material Type | Aluminium |

| Steel | |

| By Can Structure | Two-Piece |

| Three-Piece | |

| Monobloc Aerosol | |

| By Capacity / Size | ≤12 oz |

| 250-500 ml | |

| 500-1,000 ml | |

| >1,000 ml | |

| By Manufacturing Process | Drawn and Ironed (DandI) |

| Drawn and Redrawn (DRD) | |

| Impact Extrusion | |

| By End-User Industry | Food |

| Beverage | |

| Personal Care and Cosmetics | |

| Pharmaceuticals | |

| Paints and Industrial Chemicals | |

| Automotive Fluids and Lubricants | |

| Other End-User Industry |

Key Questions Answered in the Report

How large is the United States aluminum beverage cans market in 2026?

The market stands at USD 28.9 billion in 2026 and is on track to reach USD 33.26 billion by 2031.

What is the forecast CAGR for aluminum beverage cans through 2031?

The market is projected to expand at a 2.85% CAGR over the 2026-2031 period.

Which can technology holds the biggest share?

Two-piece draw-and-iron cans dominate with 88.35% share in 2025 and continue to grow.

Why are indirect sales channels becoming more popular?

Craft breweries and emerging beverage brands rely on distributors to aggregate volumes and provide just-in-time inventory despite higher pricing.

How will FDA’s PFAS ban affect can manufacturers?

Companies must reformulate interior coatings by 2026, incurring short-term R and D costs but ultimately strengthening sustainability credentials.

Page last updated on: