Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

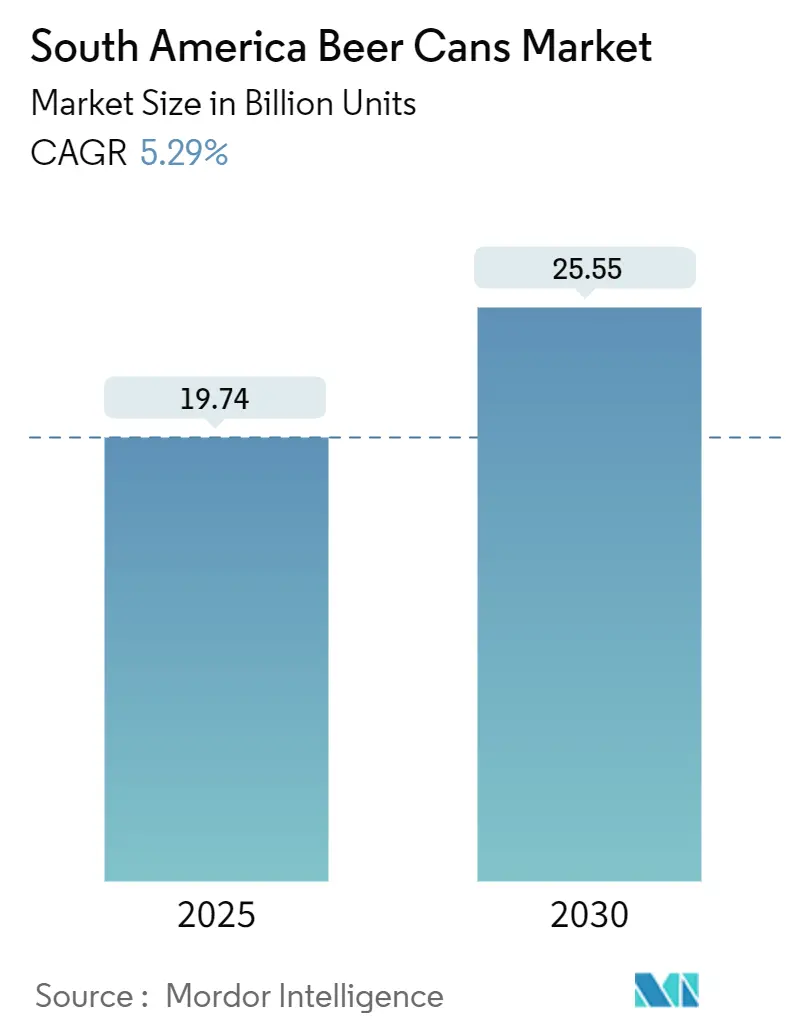

| Market Volume (2025) | 19.74 Billion units |

| Market Volume (2030) | 25.55 Billion units |

| Growth Rate (2025 - 2030) | 5.29% CAGR |

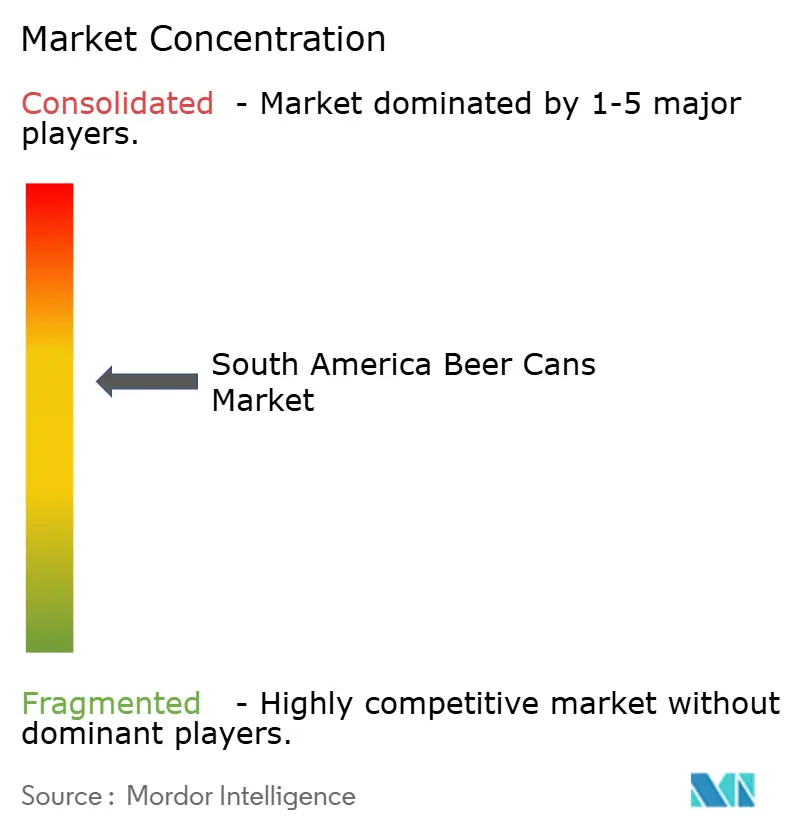

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Beer Cans Market Analysis by Mordor Intelligence

The South America beer cans market size stood at 19.74 billion units in 2025 and is projected to reach 25.55 billion units by 2030, registering a 5.29% CAGR. Rising urban incomes, strong recycling economics and government sustainability mandates continue to pivot brewers toward aluminum cans, while established pass-through contracts with two global sheet suppliers provide price transparency. Brazil’s near-perfect 98-99% collection rate reduces raw-material costs and anchors regional circular-economy advantages. Rapid SKU proliferation in craft beer, the ongoing shift to e-commerce fulfillment and capacity additions that shorten freight distances are further accelerating adoption. Currency volatility remains a profitability risk, yet steady economic recovery supports growing per-capita beer consumption and premium package uptake across major metropolitan areas.

Key Report Takeaways

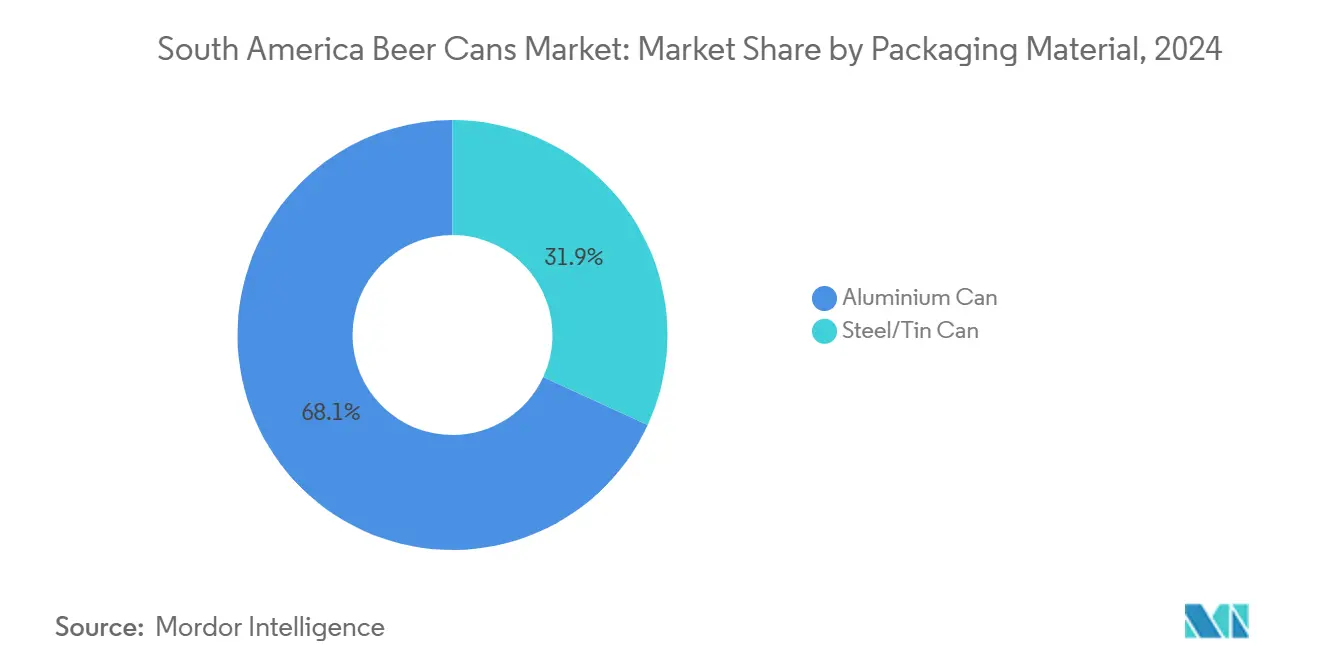

- By packaging material, aluminum cans captured 68.12% of the South America beer cans market share in 2024.

- By can size, South America beer cans market size for the 500 ml and above segment is projected to grow at a 5.89% CAGR between 2025-2030.

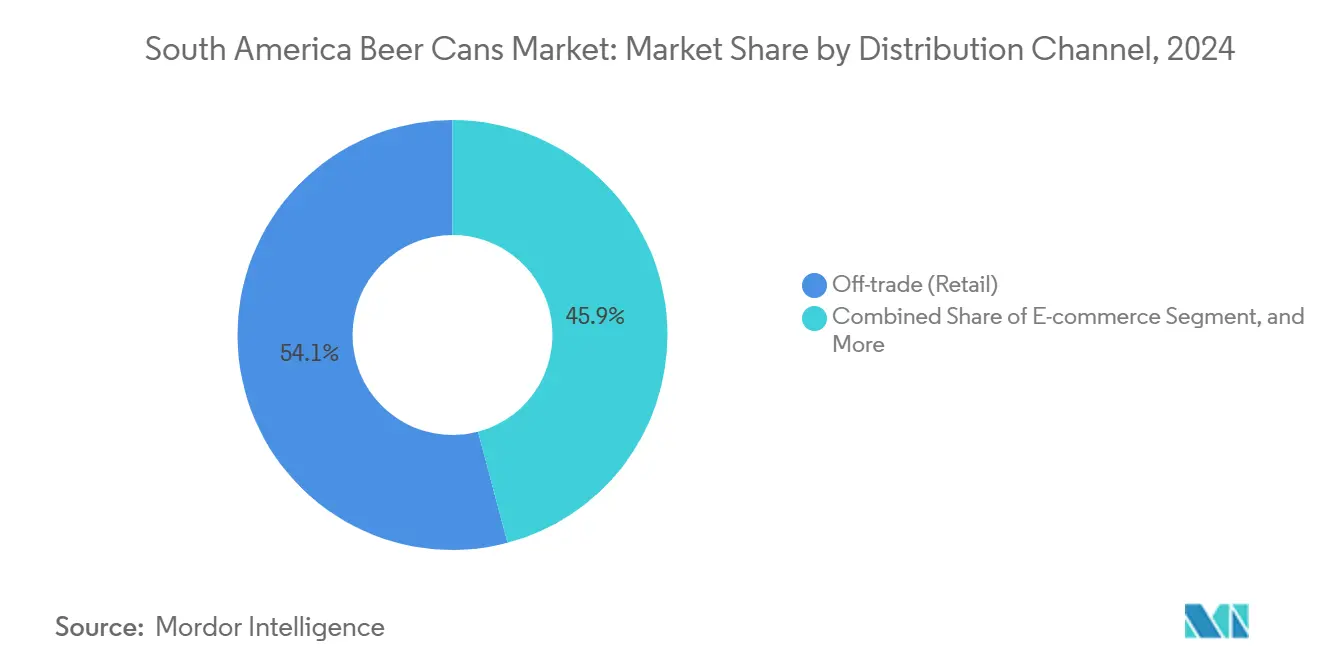

- By distribution channel, off-trade retail captured 54.12% of the South America beer cans market share in 2024.

- By beer type, South America beer cans market size for the craft beer segment is projected to grow at a 6.52% CAGR between 2025-2030.

- By country, Brazil captured 42.31% of the South America beer cans market share in 2024.

South America Beer Cans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability and recyclability appeal of aluminium cans | +1.2% | Brazil strongest impact | Medium term (2-4 years) |

| Growing craft-beer demand and SKU proliferation | +0.9% | Colombia, Argentina | Medium term (2-4 years) |

| Lightweighting drives export cost savings | +0.6% | Brazil hubs | Long term (≥ 4 years) |

| Domestic capacity additions lower freight costs | +0.8% | Brazil, Colombia | Short term (≤ 2 years) |

| Government reverse-logistics schemes accelerate collection rates | +0.7% | Brazil expanding to Colombia | Medium term (2-4 years) |

| E-commerce beer sales boost demand for durable packs | +0.5% | Urban centers region-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sustainability and Recyclability Appeal of Aluminium Cans

Brazil’s 98-99% aluminum can collection enables true can-to-can recycling inside 60 days and uses just 5% of the energy required for primary metal, giving brewers a clear cost and carbon advantage.[1]Ball Corporation, “Recycling Aluminum Cans Is Good Business,” BALL.COM Crown Holdings secured Aluminium Stewardship Initiative certification across plants in Brazil, and Colombia, signaling traceable sourcing commitments. Regional governments embed extended-producer-responsibility rules in packaging law, turning high collection rates into regulatory tailwinds. Brands highlight low embedded carbon and infinite recyclability in marketing, strengthening consumer preference. With global industry targets aiming at 100% circularity by 2050, aluminum cans stand positioned as the default sustainable option for beer in South America.

Growing Craft-Beer Demand and SKU Proliferation

Craft breweries multiplied before consolidation, growing annually and demanding small runs with eye-catching graphics that aluminum cans deliver more economically than glass. Brewers value the can’s light barrier to protect hop-forward styles and its printable surface for brand storytelling. Rapid SKU turnover favors digital printing, enabling seasonal releases without expensive mold changes. Ready-to-drink cocktails and hybrid beverages further widen the use case. As craft culture diffuses into Colombia and Argentina, flexible can suppliers can see rising orders for short-run premium formats.

Lightweighting Drives Export Cost Savings

Ongoing aluminum down-gauging has trimmed average 330 ml body weight by 6.44%, cutting material needs and lowering freight bills for export shipments.[2]Crown Holdings, “2023 Sustainability Report,” CROWNCORK.COMFor Brazil large exporters to North American partners, every gram removed lifts pallet counts and shrinks carbon footprint. Lightweight designs travel better in hot climates as they chill faster, improving cold-chain efficiency. The technology also reduces indirect taxes tied to package weight in several markets, sharpening price competitiveness of canned beer.

Domestic Capacity Additions Lower Freight Costs

Ball Corporation’s 9 Brazilian plants operate close to major filling lines, enabling wall-to-wall delivery that slashes logistics costs and inventory days. Crown’s recent line debottlenecking in Toluca and Ensenada narrows supply gaps, easing previous import dependence. Local production stabilizes lead times during port congestion and bypasses currency swings tied to imported sheet. Brewers benefit from just-in-time deliveries and reduced warehouse space, reinforcing can adoption even in higher-altitude inland markets historically served by glass.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer shift toward wine and spirits | -0.8% | Argentina, Chile and urban Brazil | Medium term (2-4 years) |

| Aluminium price volatility impacts converter margins | -0.6% | Import-reliant markets region-wide | Short term (≤ 2 years) |

| Returnable-glass culture at microbreweries | -0.4% | Colombia craft hotspots | Long term (≥ 4 years) |

| Import tariffs on flat-rolled aluminium sheet | -0.3% | Argentina | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer Shift Toward Wine and Spirits

Premiumization is nudging affluent consumers in Argentina, Chile and Brazil’s largest cities toward wine and aged spirits presented in glass. This moderates beer volume growth and limits can demand, especially during celebratory occasions. Nonetheless, beer remains culturally entrenched and competitively priced, keeping the restraint’s impact moderate.

Aluminium Price Volatility Impacts Converter Margins

London Metal Exchange premiums fluctuated 25-30% through 2024. Two dominant sheet suppliers magnify supply-shock risks, while currency swings such as Argentina’s 55% peso devaluation in Q4 2023 drove USD 22 million in losses for one leading converter.[3]Source: Ball Corporation, “Recycling Aluminum Cans Is Good Business,” BALL.COM Pass-through clauses soften the blow but timing mismatches create working-capital strain, pressuring smaller players and potentially accelerating consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Material: Aluminum Dominance Accelerates

Aluminum cans accounted for 68.12% volume in 2024 and are expanding at a 6.12% CAGR, eclipsing steel alternatives struggling with both weight and recycling limitations. This leadership stems from aluminum’s malleability, allowing intricate embossing and lightweighting that trims freight costs up to 15%. Steel retains niche appeal where rock-bottom cost overrides performance, yet mandated collection targets and consumer awareness keep shifting share toward aluminum. Brewer ESG scorecards increasingly benchmark packaging materials, favoring aluminum’s infinite recyclability and the South America beer cans market’s established collection networks.

Material advances have reduced wall thickness without compromising integrity, letting converters fit more cans per pallet and slash greenhouse-gas intensity. As governments tighten extended-producer-responsibility rules, steel faces higher compliance costs. The South America beer cans market size for aluminum is therefore forecast to widen its advantage, supported by brewer commitments to science-based climate targets.

By Can Size: Premium Formats Drive Growth

Larger 500 ml and above cans are rising at a 5.89% CAGR as brewers chase premium occasions and group consumption. The 355 ml standard still holds 36.14% share, yet consumers willingly trade up for perceived value and fewer trips to the refrigerator. Craft brewers leverage tallboy designs to command 20-30% price premiums per liter, while e-commerce retailers favor bigger packs that maximize shipment value. Tax structures in select markets remain neutral by volume, permitting format experimentation without fiscal penalty.

Standard 330 ml and 473 ml sizes cater to calorie-conscious and on-the-go drinkers respectively but display slower growth. Line flexibility is critical, and converters investing in quick-change tooling are best placed to satisfy the South America beer cans market’s widening size mix. These dynamics ensure that large formats will keep lifting the South America beer cans market share of premium cans through 2030.

By Distribution Channel: E-Commerce Disrupts Traditional Patterns

Off-trade supermarkets and convenience stores generated 54.12% of 2024 volume, yet online beer delivery is scaling at a 6.54% CAGR following pandemic-era habit shifts. Aluminum cans outperform glass in parcel networks, with up to four times more units fitting a pallet and dramatically lower breakage claims. Digital platforms spotlight recyclable packaging, reinforcing consumer perception that cans are the greener choice.

On-trade bars and restaurants still shape brand imagery, particularly for new craft entrants, but macroeconomic pressures and evolving social life have slowed this channel’s recovery. As home consumption normalizes, brewers optimize multi-pack formats designed for courier durability. Combined, these factors underpin steady growth in the South America beer cans market size attributed to e-commerce.

By Beer Type: Craft Premiumization Accelerates

Mainstream lager remained the volume backbone at 46.78% in 2024, but craft beer is advancing 6.52% annually by capitalizing on flavor experimentation and local identity. Aluminum’s light barrier safeguards hop character, vital for hazy IPAs and fruited sours gaining traction among millennials. Seasonal rotations and collaboration brews spark short production runs that cans accommodate deftly without costly bottle molds.

Low- and no-alcohol variants have begun leveraging sleek can designs to appeal to health-minded shoppers, and specialty styles such as barrel-aged stouts use 500 ml formats for higher ticket sales. Altogether, diversified styles are enlarging the South America beer cans market as brands rely on colorful graphics and limited editions to secure shelf visibility.

Geography Analysis

Brazil led the region with 42.31% share in 2024, rooted in unmatched 98-99% recycling and nine localized manufacturing plants that convert scrap back to cans in under two months. Consumers associate cans with cold, portable refreshment, and retailers value their stackability. Recent line upgrades lifted domestic output, mitigating import reliance and protecting margins from freight volatility.

Regulatory reforms ending distributor exclusivity enabled microbreweries to access national shelves using cans instead of the returnable-glass systems historically controlled by incumbents. Sustainability storytelling resonates strongly with young urban drinkers, accelerating premium-can adoption.

Argentina, Colombia and the rest of South America collectively add meaningful volume despite unique challenges. Argentine hyper-inflation poses currency risk yet beer remains an affordable staple. Colombia’s relative macro stability, paired with Crown’s ASI-certified Tocancipá plant, is raising local can usage. In Central America and Caribbean islands, tourism rebounds are boosting resort demand for lightweight, easily chilled cans, broadening the South America beer cans market footprint.

Competitive Landscape

Ball Corporation held 47% share in 2024, leveraging 12 South American plants and wall-to-wall supply contracts with leading brewers. The company’s average 6.44% can lightweighting underscores a culture of incremental process innovation. Crown Holdings remains a formidable challenger, topping Brazilian volumes thanks to sustained capacity investments and ASI certifications that differentiate on sustainability.

Market entry barriers hinge on capital intensity, sheet procurement contracts, and customer technical specifications, pointing to moderate concentration. Yet white-space niches persist: regional independents servicing craft brewers can capitalize on short-run digital printing and agile delivery. Global consolidation continues, as illustrated by large plastics deals that hint at future cross-material competition. Strategic focus across incumbents has pivoted to renewable energy sourcing, water stewardship, and circularity programs, aligning with brewer ESG procurement criteria and cementing cans’ long-term relevance.

South America Beer Cans Industry Leaders

Ball Corporation

Crown Holdings, Inc.

CCL Container Inc.

Nampak Limited

Ardagh Group S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Albéa Group acquired Amfora Packaging in Colombia to deepen its South American footprint in beauty and personal-care packaging.

- July 2025: Nelipak Corporation broke ground on a 60,000 sq ft ISO 13485-ready healthcare packaging plant in Costa Rica’s Green Valley, due mid-2026.

- May 2025: Crown Holdings partnered with San Juan Beverage Company to can Bammarita ready-to-drink cocktails for U.S. distribution.

- April 2025: Crown reported 24% year-over-year beverage can segment income growth for Q1 2025, led by Brazilian demand.

South America Beer Cans Market Report Scope

The South America Beer Cans Market Report is Segmented by Packaging Material (Aluminium Can, and Steel/Tin Can), Can Size (330 ml, 355 ml, 473 ml, and 500 ml and Above), Distribution Channel (Off-Trade Retail, On-Trade HoReCa, and More), Beer Type (Mainstream Lager, Craft Beer, and More), and Geography (Brazil, Argentina, and Colombia). The Market Forecasts are Provided in Terms of Volume (Units).

By Packaging Material

| Aluminium Can |

| Steel/Tin Can |

By Can Size

| 330 ml |

| 355 ml |

| 473 ml |

| 500 ml and above |

By Distribution Channel

| Off-trade (Retail) |

| On-trade (HoReCa) |

| E-commerce |

By Beer Type

| Mainstream Lager |

| Craft Beer |

| Low/No-Alcohol Beer |

| Other Beer Types |

By Country

| Brazil |

| Argentina |

| Colombia |

| Rest of South America |

| By Packaging Material | Aluminium Can |

| Steel/Tin Can | |

| By Can Size | 330 ml |

| 355 ml | |

| 473 ml | |

| 500 ml and above | |

| By Distribution Channel | Off-trade (Retail) |

| On-trade (HoReCa) | |

| E-commerce | |

| By Beer Type | Mainstream Lager |

| Craft Beer | |

| Low/No-Alcohol Beer | |

| Other Beer Types | |

| By Country | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

What is the projected volume of beer cans consumed in South America by 2030?

The South America beer cans market is forecast to reach 25.55 billion units by 2030.

Which material leads packaging choices for brewers in the region?

Aluminum commands 68.12% share, far ahead of steel alternatives, and continues to gain ground.

Why are larger 500 ml and above can sizes growing faster?

Consumers associate the format with premium value and sharing occasions, driving a 5.89% CAGR for these sizes.

How fast is e-commerce beer distribution expanding?

Online sales of canned beer are growing at a 6.54% CAGR, the quickest among all channels.

Which country offers the highest growth potential?

Mexico is expanding at a 6.92% CAGR, supported by craft-beer momentum and tariff-free aluminum trade.

Who dominates regional supply?

Ball Corporation leads with 47% market share and 12 production sites, followed closely by Crown Holdings.

Page last updated on: