Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

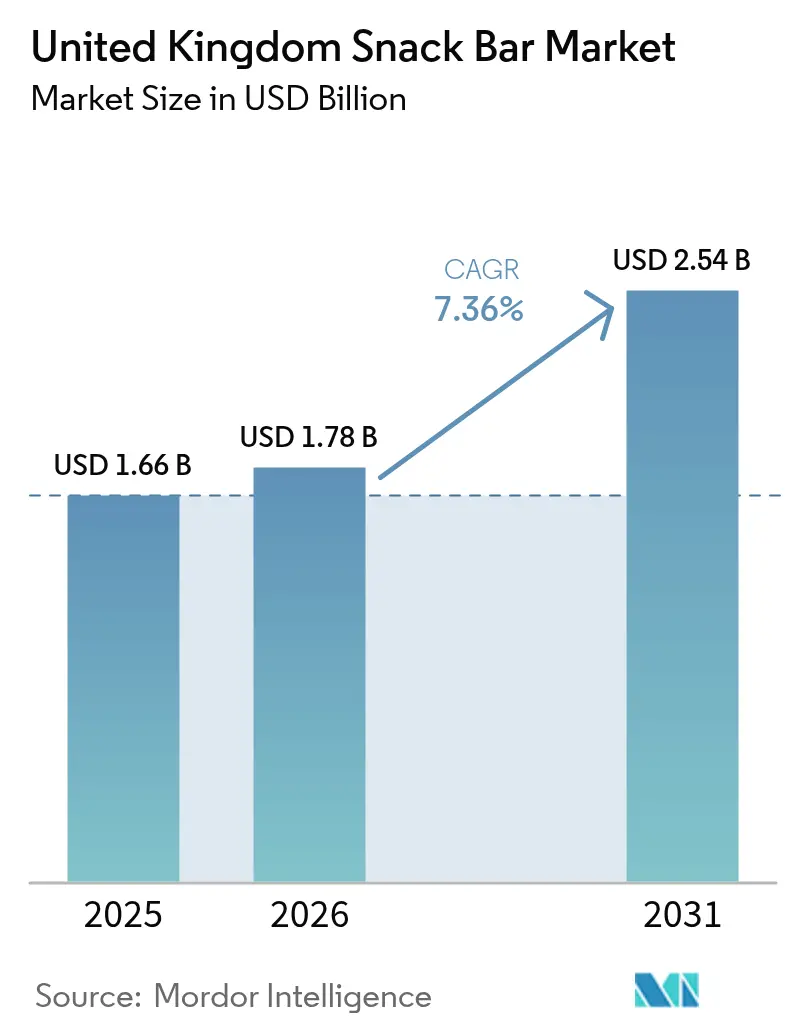

| Base Year Market Size (2025) | USD 1.66 Billion |

| Market Size (2026) | USD 1.78 Billion |

| Market Size (2031) | USD 2.54 Billion |

| Growth Rate (2026 - 2031) | 7.36% CAGR |

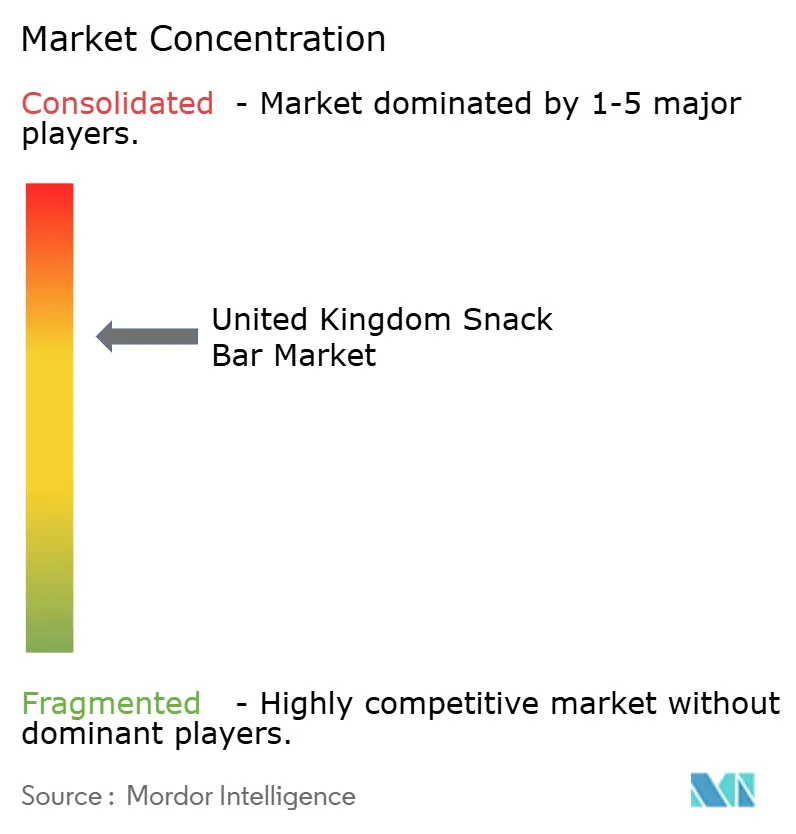

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Snack Bar Market Analysis by Mordor Intelligence

The United Kingdom snack bar market size was valued at USD 1.66 billion in 2025 and estimated to grow from USD 1.78 billion in 2026 to reach USD 2.54 billion by 2031, at a CAGR of 7.36% during the forecast period (2026-2031). Consumers are increasingly breaking traditional mealtimes into multiple snack occasions, seeking functional nutrition that complements hybrid work schedules and busy, on-the-go lifestyles. While cereal-based products remain a staple, there is growing demand for protein-fortified and plant-based options, driven by 23.4% of adults identifying as flexitarian and 66% aiming to reduce meat consumption. Retailers are seeing intensified promotions among mass-market brands, but premium clean-label products are expanding rapidly as consumers associate shorter ingredient lists with health and sustainability benefits. Additionally, the market is witnessing a shift in distribution channels: supermarkets and hypermarkets continue to dominate, but the rapid growth of online sales is enabling direct-to-consumer brands to bypass traditional retailers, gather first-party data, and command higher price points. Overall, the trends of premiumization, product fortification, and e-commerce growth are shaping a positive outlook for the United Kingdom snack bar market.

Key Report Takeaways

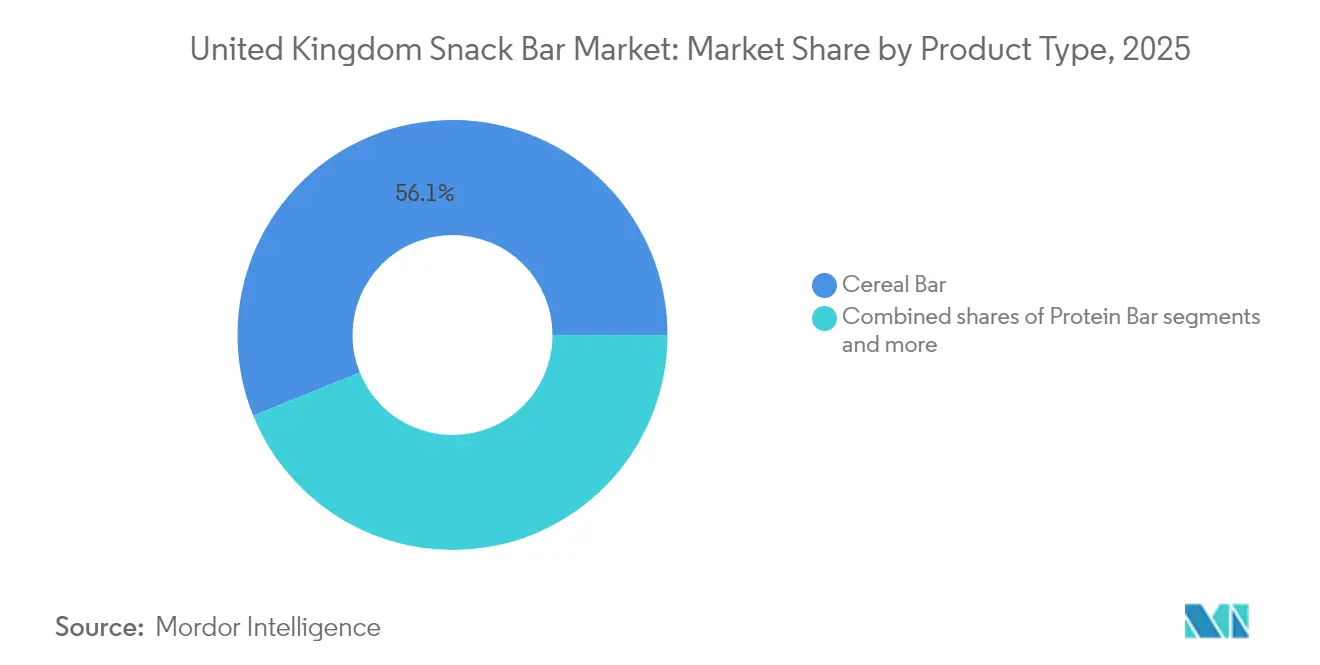

- By product type, cereal bars led with 56.12% of the United Kingdom snack bar market share in 2025; protein bars are forecast to post the highest 8.11% CAGR through 2031.

- By ingredient base, granola and oat formats controlled 35.31% of the United Kingdom snack bar market size in 2025; dairy and protein-based formulations are projected to grow at 8.05% CAGR to 2031.

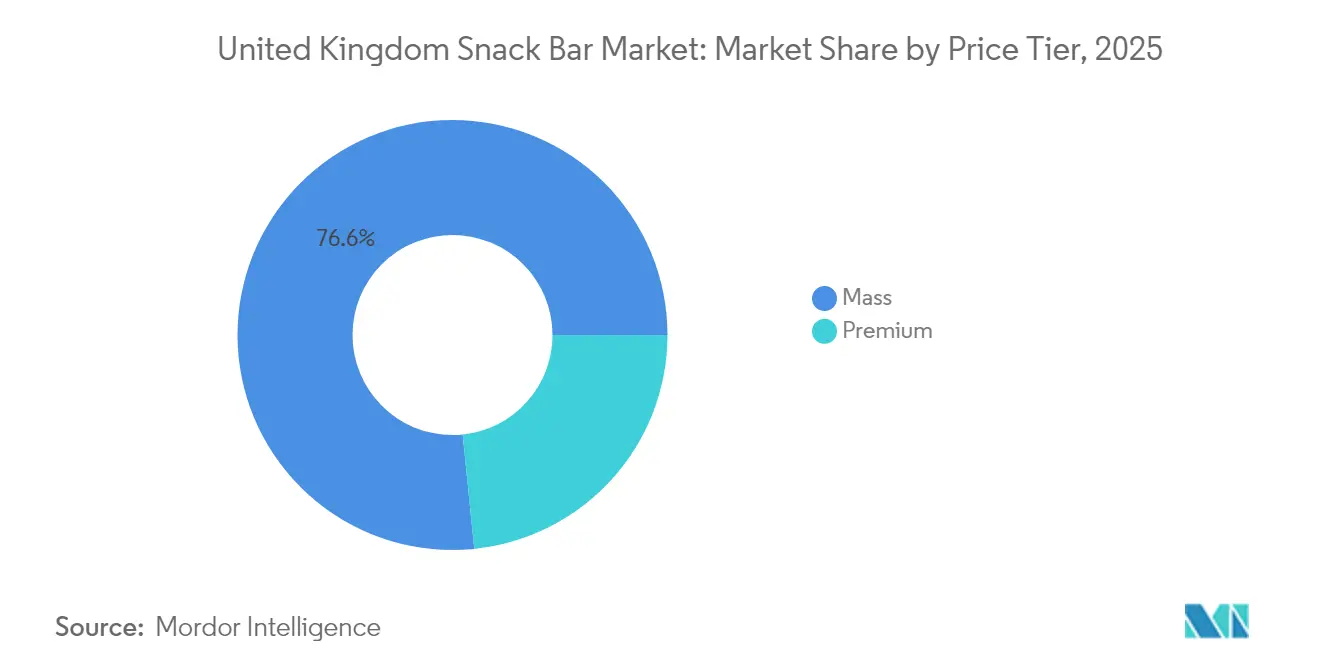

- By price tier, mass offerings captured 76.62% revenue in 2025; the premium segment is set to expand at 8.24% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets retained 54.10% share in 2025; online retail is the fastest-rising outlet with an 8.42% CAGR outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Snack Bar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in protein, vegan, and plant-based bar segments | +1.8% | National, with early gains in London, Manchester, Edinburgh | Medium term (2-4 years) |

| Increasing awareness and adoption of clean-label products | +1.5% | National | Short term (≤ 2 years) |

| Trend towards natural, organic, and non-GMO ingredients | +1.2% | National, stronger in affluent Southeast | Medium term (2-4 years) |

| Popularity of free-from bars | +1.0% | National | Short term (≤ 2 years) |

| Innovations in flavors, textures, and nutritional profiles | +1.3% | National | Short term (≤ 2 years) |

| Rise of flexitarian and active lifestyles | +1.4% | National, concentrated in urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Protein, Vegan, and Plant-Based Bar Segments

In 2024, the plant-based snack bar market in the United Kingdom encountered challenges, reflecting a broader trend of decline in the overall plant-based retail market, amounting to hundreds of millions of pounds. This downturn suggests the category is entering a maturation phase, with price sensitivity becoming more pronounced as inflation-affected households prioritize value over novelty. Protein bars are adapting to this environment by positioning themselves as functional nutrition products rather than solely ethical alternatives. This approach appeals to a significant segment of adults in the United Kingdom identifying as flexitarian, who seek convenient post-workout recovery options without fully committing to plant-based diets. Manufacturers are increasingly incorporating dairy and protein-based formulations, utilizing ingredients such as pea protein isolates and whey concentrates. This strategy not only provides a substantial protein content per serving but also ensures compliance with HFSS regulations. While a majority of adults in the United Kingdom express a willingness to reduce meat consumption, and there is a slight increase in household adoption of plant-based milk, mainstream acceptance appears to hinge more on achieving taste parity and competitive pricing than on ideological motivations. In 2024, consumers in the United Kingdom purchased an average of 9.1 million plant-based products per week from major supermarkets [1]Source: Good Food Institute, “Plant-based meat and milk are now mainstream choices for British consumers,” gfieurope.org.

Increasing Awareness and Adoption of Clean-Label Products

In the United Kingdom, a growing number of consumers are actively avoiding processed foods, driven by increasing awareness and concerns about health implications. Many are particularly critical of the classification that groups protein bars with confectionery under ultra-processed food (UPF) labels, which they feel does not accurately reflect the nutritional value of certain products. This shift in consumer perception presents a strategic challenge for brands, as they are under mounting pressure to simplify ingredient lists and remove synthetic additives to align with consumer preferences. However, achieving shelf stability without the use of preservatives remains a significant hurdle, often resulting in higher production costs and increased waste. Nakd provides a strong example of addressing this challenge with its Fruit & Fibre bars, which are made from dates and chicory fibre, without added sugar. These bars highlight the growing market potential for High Fat, Sugar, and Salt (HFSS)-compliant, clean-label products. When supported by effective digital marketing strategies and endorsements from credible nutritionists, such products can successfully command premium pricing and resonate with health-conscious consumers.

Trend Towards Natural, Organic, and Non-GMO Ingredients

Organic and non-GMO (non-genetically modified organism) certifications are increasingly moving beyond niche health-food stores and entering mainstream supermarket aisles. Despite this broader availability, the 10.4% year-on-year growth observed in barista-style plant milk, a premium subcategory, highlights a contrasting trend when compared to the 4.1% decline in overall plant-based retail sales. This suggests that consumers are placing greater emphasis on functional performance and taste rather than certification labels, especially during periods of financial constraint. Similarly, date-based bars, which leverage dates as a natural binder and sweetener, are gaining traction as manufacturers strive to eliminate the use of refined sugars and synthetic emulsifiers. However, the higher water activity of dates poses challenges by reducing shelf life and complicating ambient distribution logistics. Additionally, pulse and pea protein ingredients are becoming more prevalent as manufacturers reformulate products to increase protein content while maintaining plant-based claims. Yet, the earthy off-notes associated with pea protein isolates require masking through the use of natural flavors and cocoa, which adds further complexity to the formulation process.

Popularity of Free-From Bars

Free-from bars, tailored for consumers with specific dietary requirements such as gluten-free, dairy-free, nut-free, and allergen-free options, are experiencing notable growth as the Food Standards Agency (FSA) strengthens its enforcement of allergen labeling regulations. These efforts are part of the Prepacked for Direct Sale (PPDS) regulations, first introduced in October 2021 and subsequently updated in 2024, aimed at ensuring greater transparency and safety in food labeling [2]Source: Food Standard Agency "Food allergen labelling and information requirements technical guidance: Summary," food.gov.uk. The FSA's 2024 retail surveillance uncovered significant non-compliance in allergen declarations and protein claims across several major retailers. This led to product recalls at Tesco, Sainsbury's, Morrisons, Waitrose, Lidl, and Asda due to undeclared allergens such as milk, soy, and gluten found in cereal and snack bars. While these incidents have damaged consumer trust and increased liability risks for retailers, they also highlight a critical market opportunity for brands that prioritize allergen-controlled manufacturing processes and adopt transparent labeling practices, meeting the growing demand for safe and trustworthy free-from products.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict requirements for nutritional content disclosure | -0.8% | National | Short term (≤ 2 years) |

| Limited shelf life—product stability challenges | -0.6% | National | Medium term (2-4 years) |

| Occasional product recalls due to allergens or contamination | -0.5% | National | Short term (≤ 2 years) |

| Packaging waste and environmental concerns | -0.4% | National, stronger in urban areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strict Requirements for Nutritional Content Disclosure

The Food Standards Agency's High Fat, Salt, and Sugar (HFSS) regulations, designed to promote healthier eating habits, require manufacturers to reformulate their products or risk losing visibility in prominent retail spaces. According to a recent survey conducted by Action on Salt, a significant percentage of snacks in the UK currently fall under the HFSS classification, emphasizing the substantial challenge manufacturers face in meeting these standards. Despite these hurdles, the industry has demonstrated that success is achievable. For instance, the high rate of compliance with salt reduction targets highlights that, with the right investments in advanced ingredient technology and precise process control, manufacturers can identify and implement effective technical solutions. A notable example is PepsiCo, which recently reformulated its Doritos product line to remove its HFSS classification. This strategic move aligns with their broader goal of ensuring a significant portion of their UK snack sales come from healthier options in the near future. Such proactive measures by large companies underscore their ability to adapt and lead in response to regulatory changes. However, smaller brands often encounter significant obstacles, as they may lack the financial resources for research and development or the strong supplier relationships necessary to execute rapid reformulations effectively.

Limited Shelf Life—Product Stability Challenges

Preservative-free, clean-label formulations, which aim to meet consumer demand for natural and minimally processed products, reduce shelf life from 12-18 months to 6-9 months. This shorter shelf life creates challenges such as inventory waste and added supply chain complexity, as retailers prefer longer shelf life to minimize the risk of markdowns. Date-based bars, which incorporate dates as a natural binder and sweetener, present additional hurdles due to their higher water activity levels. This characteristic accelerates microbial growth and texture degradation, necessitating the use of modified-atmosphere packaging or refrigeration. These measures, while essential for maintaining product quality, increase production costs and limit the feasibility of ambient distribution. The Food Standards Agency (FSA) provides general guidance on shelf life, emphasizing microbial safety and sensory quality. However, it does not offer specific standards for snack bars, leaving manufacturers to bear the expense of conducting challenge testing and stability studies to validate their shelf-life claims.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protein Bars Disrupt Cereal Dominance

Cereal bars captured 56.12% of the market share in 2025, underlining their position as a widely preferred, affordable, and convenient snacking option for consumers with busy lifestyles. These bars have become a staple due to their familiarity and accessibility. On the other hand, protein bars are forecasted to grow at a compound annual growth rate (CAGR) of 8.11% through 2031, driven by a noticeable shift in consumer preferences from indulgent snacks to nutrition that supports performance and fitness goals. This trend is particularly evident among the 23.4% of United Kingdom adults who identify as flexitarian, seeking convenient post-workout recovery options without fully committing to plant-based diets. Furthermore, the 66% of consumers who are open to reducing their meat consumption are creating a favorable environment for the development and adoption of protein-rich formulations.

Energy bars, which occupy a middle ground between cereal and protein bars, are designed to meet the needs of active-lifestyle consumers who prioritize sustained energy release over high protein content. These bars cater to individuals looking for a balance between nutrition and energy, making them a practical choice for those with demanding schedules. However, their growth potential is somewhat limited due to competition with sports nutrition products and their lack of clear differentiation from cereal bars in mainstream retail channels. This overlap in positioning has made it challenging for energy bars to carve out a distinct identity in the broader market.

By Ingredient Base: Dairy and Protein Formulations Gain Ground

Granola and oat-based bars held 35.31% of the market share in 2025, largely due to their strong association with wholesome breakfast options and clean-label attributes. On the other hand, dairy and protein-based formulations are growing at a compound annual growth rate (CAGR) of 8.05% through 2031. This growth is driven by manufacturers incorporating whey concentrates and pea protein isolates to deliver 15-20 grams of protein per serving while ensuring compliance with high fat, sugar, and salt (HFSS) regulations. Nut-based bars continue to appeal to premium-tier consumers who prioritize satiety and healthy fats. However, concerns about allergens and the higher cost of ingredients have limited their adoption in mainstream markets.

Date-based bars, which use dates as a natural binder and sweetener, are gaining traction as manufacturers aim to replace refined sugars and synthetic emulsifiers. Despite this, the higher water activity of dates reduces shelf life and complicates ambient distribution. Hybrid blends that combine oats, nuts, dates, and protein sources offer manufacturers the ability to optimize texture, taste, and nutritional profiles. However, these blends come with increased formulation complexity, leading to higher production costs and supply chain risks. Additionally, other varieties, such as rice-based and seed-based bars, serve niche segments by addressing specific dietary preferences or allergen sensitivities.

By Price Tier: Premium Segment Captures Value-Conscious Upgraders

In 2025, mass-market bars held a 76.62% share of the market, underscoring their strong presence in promotional aisles and multi-pack formats that appeal to cost-conscious households. Meanwhile, the premium segment is expanding at a compound annual growth rate (CAGR) of 8.24% through 2031, as consumers increasingly opt for products with clean-label credentials, artisanal formulations, and functional benefits. This shift reflects the preferences of 59% of consumers who prioritize sustainability credentials when buying snacks and the 54% of United Kingdom consumers who favor reduced-sugar options. These trends have created a growing demand for claims such as organic, non-GMO (non-genetically modified organisms), and regenerative agriculture.

However, 49% of United Kingdom consumers purchase snacks on promotion, highlighting a price-quality tension. While shoppers value clean labels, they are often hesitant to pay significantly higher prices, placing pressure on manufacturers to either absorb reformulation costs or risk losing sales volumes. Pip & Nut's July 2024 launch of peanut-butter-stuffed oat bars demonstrates how provenance storytelling and transparent sourcing can help justify premium pricing when compared to mass-market alternatives.

By Distribution Channel: Online Retail Disrupts Traditional Dominance

In 2025, supermarkets and hypermarkets accounted for 54.10% of the market share, benefiting from their scale, promotional activities, and strategic placement of impulse-purchase items at checkouts and end-caps. Meanwhile, online retail is experiencing significant growth, with a projected compound annual growth rate (CAGR) of 8.42% through 2031. This expansion is supported by Ocado's 15.5% year-on-year revenue growth in the third quarter (Q3) of 2024 and the continued adoption of click-and-collect shopping habits established during pandemic lockdowns. Online retail sales in the United Kingdom increased by 2.0% month-on-month and 3.7% year-on-year in July 2025, representing 27.8% of total retail sales during that period .

Convenience stores are facing challenges with margin pressures as consumer footfall patterns evolve and shopping trips become more consolidated. However, their proximity advantage continues to drive demand for single-serve formats. Other distribution channels, including foodservice, vending, and direct-to-consumer (DTC) subscriptions, cater to niche segments. These channels provide brands with opportunities to test new product formats and gather consumer feedback before scaling into mainstream retail. The share of snack bars within total UK snacking revenue, as highlighted by Houlihan Lokey, underscores significant growth potential. Manufacturers can tap into this opportunity by encouraging occasional users to become regular buyers through subscription models and multi-pack promotions.

Geography Analysis

The snack bar market in the United Kingdom demonstrates significant demand concentrated in urban centers such as London, Manchester, Edinburgh, and Birmingham. This trend is largely driven by the rise of hybrid work patterns and the increasing prevalence of compressed meal occasions, which encourage higher per-capita consumption of convenient, portable, and functional snack formats. Additionally, consumer preferences are shifting, with 23.4% of adults in the United Kingdom identifying as flexitarian and 66% expressing openness to reducing their meat consumption. These preferences are particularly prominent in metropolitan areas where higher levels of educational attainment and disposable income are common. As a result, there is a growing demand for premium protein bars and plant-based snack options, which are increasingly occupying shelf space in independent health-food retailers and specialty chains.

Regulatory enforcement across the United Kingdom varies significantly by region, creating challenges for businesses operating nationwide. The Food Standards Agency (FSA) launched retail surveillance in 2024, which has resulted in allergen recalls across major retailers, including Tesco, Sainsbury's, Morrisons, Waitrose, Lidl, and Asda. However, independent retailers in Scotland and Wales face less frequent inspections due to resource constraints, leading to disparities in compliance standards. These regional differences in regulatory enforcement can create operational complexities for manufacturers and retailers, particularly those aiming to maintain consistent standards across all markets.

Looking ahead, the Simpler Recycling legislation, set to take effect in March 2027, will introduce mandatory and consistent collection of plastic films across England. However, this legislation will not extend to Scotland, Wales, or Northern Ireland, resulting in regional disparities in packaging recyclability. For manufacturers and brands operating across the United Kingdom, this creates additional challenges. Companies will need to either produce multiple stock-keeping unit (SKU) variants to meet varying regional requirements or accept reduced sustainability credentials in devolved nations. These complexities highlight the need for strategic planning to navigate the evolving regulatory landscape while addressing consumer expectations for sustainability.

Competitive Landscape

The United Kingdom snack bar market is moderately consolidated, featuring a combination of global companies such as Mars, Nestlé, PepsiCo, Mondelēz, General Mills, and Kellanova, alongside emerging players like Grenade UK, Huel, and Pulsin. These smaller brands often focus on direct-to-consumer channels and emphasize clean-label products to appeal to premium market segments. Mars' USD 36 billion acquisition of Kellanova in August 2024 highlights the strategic need to expand distribution and cross-sell product portfolios across snack categories. This merger allows the combined company to secure better shelf placement and promotional support from United Kingdom retailers. On the other hand, smaller brands are exploring niche opportunities in areas like functional nutrition, allergen-free products, and subscription models, though their limited production capacity and distribution networks remain barriers to wider market reach.

Companies are adopting various strategies to stay competitive, including reformulating products to comply with High Fat, Sugar, and Salt (HFSS) regulations, innovating packaging to meet recyclability standards, and using digital marketing to build direct relationships with consumers. For example, PepsiCo reformulated Doritos in October 2024 to achieve non-HFSS status, aligning with its goal of generating 50% of United Kingdom snack sales from healthier alternatives by 2025. These efforts reflect how established players are proactively addressing regulatory challenges and shifting consumer preferences.

Sustainability is another key focus area for market leaders. Nestlé's £7 million investment in flexible plastic recycling infrastructure demonstrates its long-term commitment to improving sustainability credentials. Such initiatives highlight how companies are not only adapting to regulatory requirements but also responding to growing consumer demand for environmentally responsible practices in the snack bar market.

United Kingdom Snack Bar Industry Leaders

-

Abbott Laboratories

-

Associated British Foods plc

-

August Storck KG

-

Ferrero International SA

-

General Mills Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Pip & Nut has expanded its United Kingdom portfolio with a trio of peanut butter-stuffed snack bars, leveraging British oats and targeting consumers seeking healthy, on-the-go confectionery alternatives within the snack bar market.

- March 2024: The British Snack Co introduced kerbside-recyclable paper crisp packs in partnership with EvoPak, marking progress in sustainable packaging for the United Kingdom snack market. This development supports eco-friendly innovation trends.

- February 2024: Nakd, under Natural Balance Foods, has expanded its United Kingdom snack bar portfolio with new Fruit & Fibre bars, supported by a digital campaign and nutritionist partnership. The launch strengthens Nakd’s functional snack offering in the United Kingdom market.

United Kingdom Snack Bar Market Report Scope

Cereal Bar, Fruit & Nut Bar, Protein Bar are covered as segments by Confectionery Variant. Convenience Store, Online Retail Store, Supermarket/Hypermarket, Others are covered as segments by Distribution Channel.

By Product Type

| Cereal Bar |

| Energy Bar |

| Protein Bar |

| Fruit and Nut Bar |

By Ingredient Base

| Nut-based bars |

| Granola/Oat-based |

| Date-based |

| Dairy/Protein-based |

| Hybrid blends |

| Other Forms |

By Price Tier

| Mass |

| Premium |

By Distribution Channel

| Supermarket/Hypermarket |

| Online Retail Store |

| Convenience Store |

| Other Distribution Channels |

| By Product Type | Cereal Bar |

| Energy Bar | |

| Protein Bar | |

| Fruit and Nut Bar | |

| By Ingredient Base | Nut-based bars |

| Granola/Oat-based | |

| Date-based | |

| Dairy/Protein-based | |

| Hybrid blends | |

| Other Forms | |

| By Price Tier | Mass |

| Premium | |

| By Distribution Channel | Supermarket/Hypermarket |

| Online Retail Store | |

| Convenience Store | |

| Other Distribution Channels |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms