Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

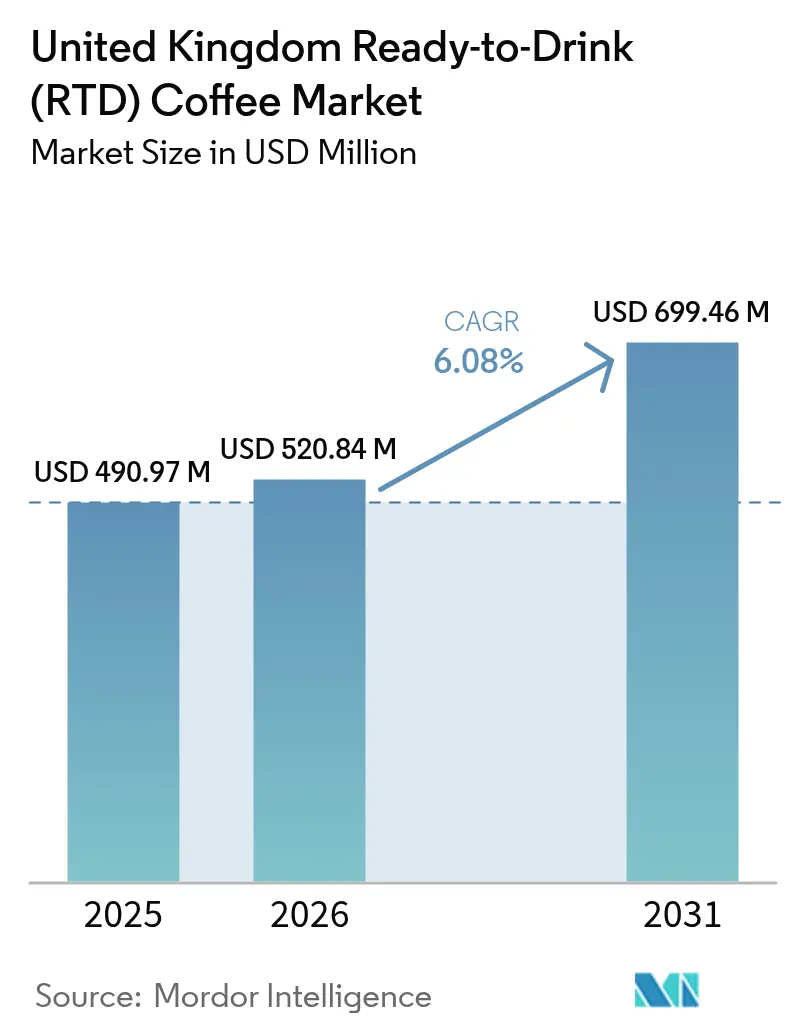

| Base Year Market Size (2025) | USD 490.97 Million |

| Market Size (2026) | USD 520.84 Million |

| Market Size (2031) | USD 699.46 Million |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

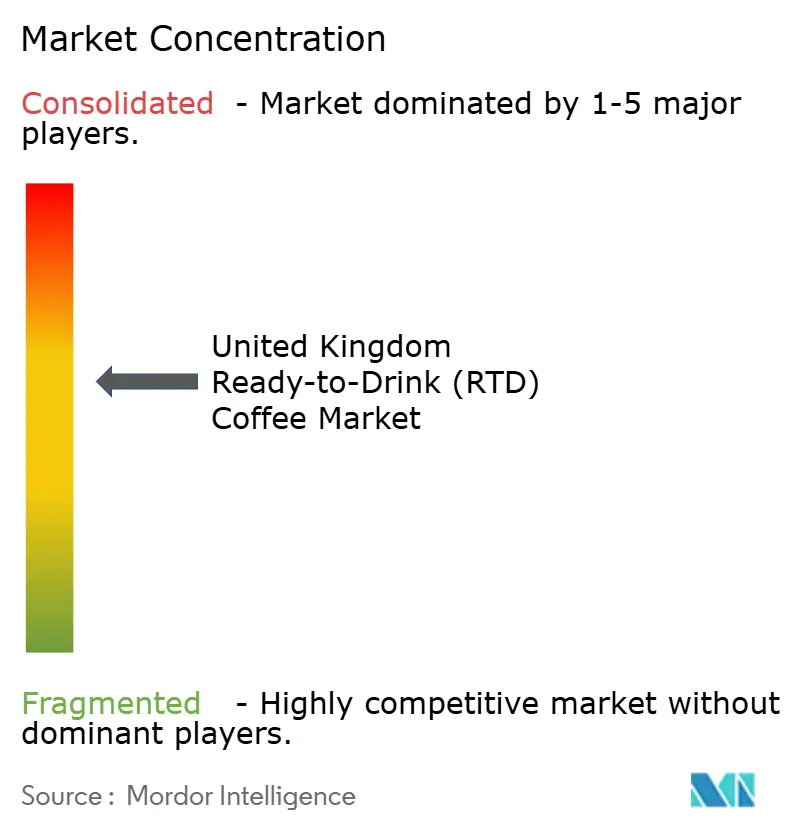

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Ready-to-Drink (RTD) Coffee Market Analysis by Mordor Intelligence

United Kingdom Ready-to-Drink (RTD) coffee market size in 2026 is estimated at USD 520.84 million, growing from 2025 value of USD 490.97 million with 2031 projections showing USD 699.46 million, growing at 6.08% CAGR over 2026-2031. The market expansion is attributed to the increasing consumer preference for convenient, health-conscious, and premium portable beverages. The primary market drivers are Millennial and Generation Z consumers, who demonstrate significant demand for efficient, functional products aligned with contemporary urban lifestyles. The Ready-to-Drink (RTD) coffee segment continues to acquire substantial market share from traditional carbonated beverages and hot brewed coffee through the incorporation of functional elements, including energy-enhancing ingredients, plant-based formulations, and reduced-sugar alternatives. Market advancement is further facilitated by product development initiatives in flavor diversification and health-oriented formulations, implementation of sustainable packaging solutions, and expansion of e-commerce distribution channels.

Key Report Takeaways

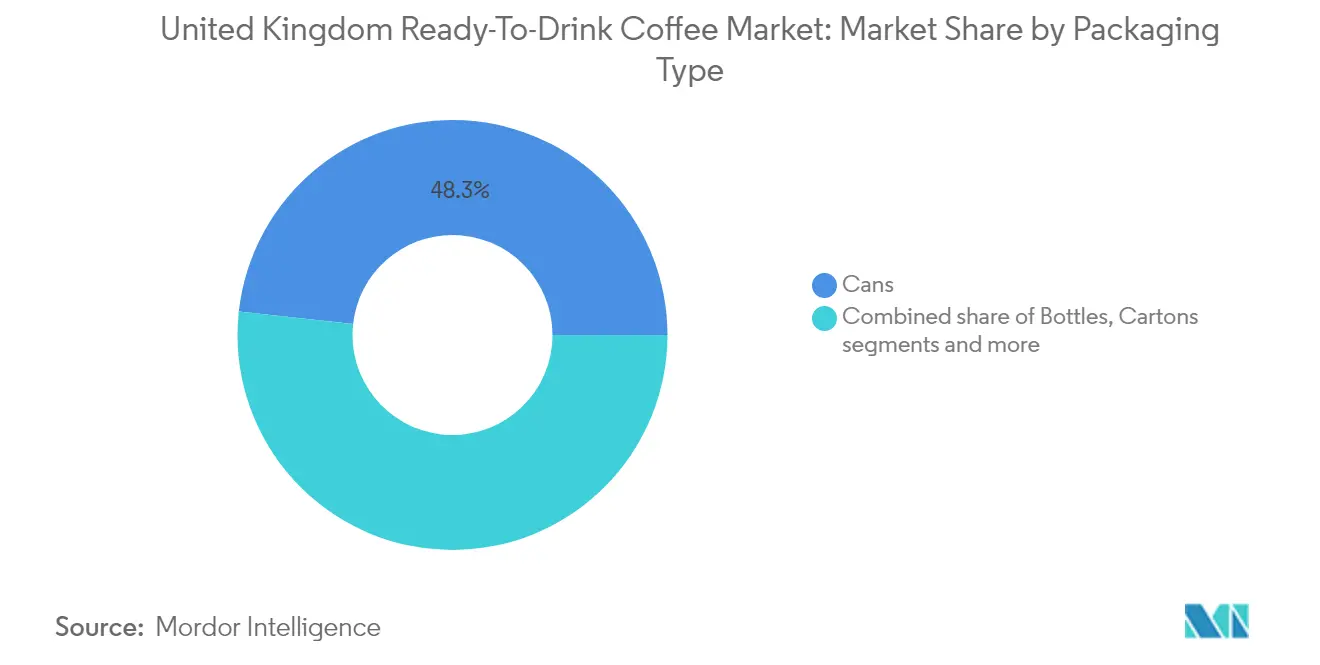

- By packaging type, cans retained 48.25% revenue share in 2025, whereas cartons are forecast to climb at a 5.05% CAGR to 2031.

- By product type, iced latte captured 51.62% of the UK RTD coffee market size in 2025; cold brew is poised for a 7.29% CAGR over 2026-2031.

- By ingredient base, dairy options accounted for 70.55% of the RTD coffee market size in 2025, but plant-based drinks will expand at an 8.19% CAGR.

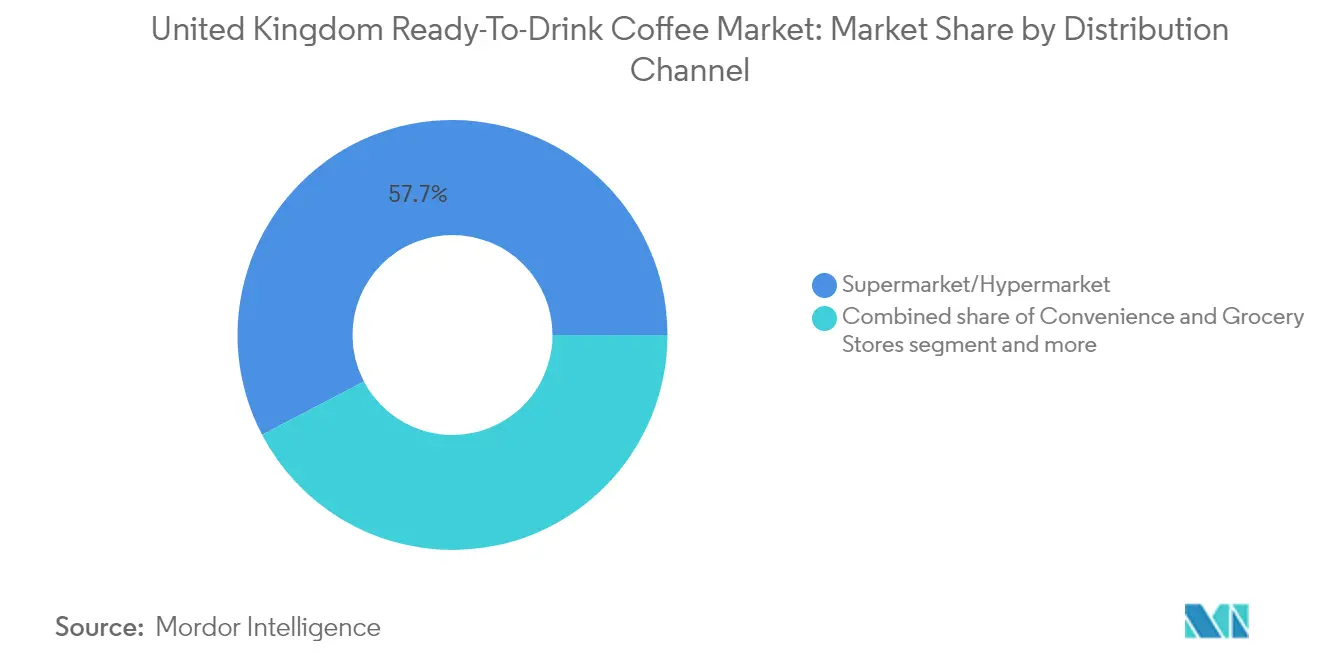

- By distribution channel, supermarkets/hypermarkets commanded 57.68% of 2025 sales, while online retail is set to post a 11.75% CAGR.

- By flavor profile, plain/classic formulations captured 51.74% share in 2025; flavored variants are forecast to accelerate at a 6.97% CAGR to 2031.

- By price positioning, mass-market SKUs held 62.41% revenue share in 2025, whereas the premium segment is projected to register a 6.26% CAGR through 2031.

- By geography, England led with 84.35% of RTD coffee market share in 2025; Northern Ireland is projected to log a 7.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Ready-to-Drink (RTD) Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience and on-the-go consumption on the rise | +1.8% | National, with stronger adoption in England and urban Scotland | Medium term (2-4 years) |

| Health trends spotting in RTD coffee beverages | +1.2% | National, with premium segments in England leading adoption | Long term (≥ 4 years) |

| Augmented expenditure on advertising and promotional activities | +0.9% | National, concentrated in England and Wales metropolitan areas | Short term (≤ 2 years) |

| Product innovation experiences notable surge | +1.1% | National, with Research and Development centers primarily in England | Medium term (2-4 years) |

| Brand-retailer partnerships strengthen market presence | +0.7% | National, with strongest impact in England through major retail chains | Medium term (2-4 years) |

| Cold brew variants appeal to younger demographics | +0.6% | National, with urban concentration in England and Scotland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Convenience and On-the-Go Consumption on the Rise

The United Kingdom's Ready-to-Drink (RTD) coffee market exhibits substantial expansion, propelled by increasing consumer preferences for convenient and portable caffeine solutions. The market trajectory demonstrates a strong correlation with transforming workplace dynamics, particularly the widespread implementation of hybrid working models. This fundamental shift in consumer behavior exemplifies broader societal transitions in work-life integration and heightened requirements for efficient caffeine consumption methods. For instance, Starbucks and Costa increased their ready-to-drink (RTD) coffee portfolio in UK retail stores through the addition of chilled lattes and espresso drinks in response to growing market demand. According to Costa Coffee's 'Lattenomics' report, a 15% increase in Drive-Thru locations and increased mobile consumption indicate the United Kingdom's shift toward flexible, on-the-go consumption patterns [1] Source: Costa Coffee, "Costa Coffee Lattenomics Report", costa.co.uk. This consumer behavior trend drives the expansion of Ready-to-Drink (RTD) coffee, as customers demand convenient caffeine options outside traditional cafes.

Health Trends Spotting in RTD Coffee Beverages

The United Kingdom ready-to-drink (RTD) coffee market is experiencing a significant transformation driven by increasing health consciousness among consumers, as manufacturers develop reduced-sugar formulations and functional additives that elevate coffee from a conventional caffeine delivery system to a wellness-oriented beverage. The protein-enhanced segment demonstrates this transformation in the market. For instance, in June 2024, Starbucks, in partnership with dairy company Arla, introduced a new line of high-protein coffee-based RTD beverages to the United Kingdom market. The Starbucks Protein Drink with Coffee range contains 20g of protein per bottle, utilizing low-fat milk with zero added sugar. This product development corresponds with the substantial growth in the United Kingdom protein beverage market. The wellness-oriented product development extends beyond protein to incorporate prebiotic fibers, marine collagen, and adaptogenic mushrooms.

Augmented Expenditure on Advertising and Promotional Activities

The intensifying competition for retail shelf space and consumer attention within the United Kingdom ready-to-drink (RTD) coffee market has necessitated substantial marketing investments across traditional and digital channels, with market participants implementing comprehensive strategic initiatives to enhance category awareness and establish distinct brand positioning in the competitive landscape. This strategic imperative is exemplified by Starbucks' significant investment of USD 507.8 million in advertising during its fiscal year ending in 2023, demonstrating the market's increasing emphasis on brand visibility and consumer engagement. Subsequently, this market development has prompted organizations to prioritize sophisticated packaging solutions that seamlessly integrate functionality with aesthetic appeal, thereby fostering meaningful consumer engagement and facilitating sustained purchase behavior in the United Kingdom's dynamic RTD coffee market environment.

Product Innovation Experiences Notable Surge

The United Kingdom's Ready-to-Drink (RTD) coffee market is experiencing significant transformation through strategic innovation initiatives across product development, packaging solutions, and consumption patterns. The market demonstrates substantial evolution, particularly in the cold brew segment, which has emerged as a key growth driver. For instance, in April 2025, UK functional beverage company Unconform introduced three new ready-to-drink (RTD) cold brew coffee beverages with wellness-focused ingredients. The vegan drinks combined oat milk with Arabica beans and nootropics - compounds associated with cognitive health benefits, including enhanced mood, focus, and sleep. The product line featured three variants: Flat White containing ashwagandha, ginkgo biloba, and vitamin B12; Salted Caramel Latte with inulin and turmeric; and Mocha enriched with niacin and biotin. Moreover, the market's infrastructure development is evident through Westrock Coffee's investments in advanced production capabilities, enabling diverse packaging formats, including multi-serve PET bottles and single-serve options in glass and aluminum cans.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High amount of HFSS sugar limiting iced coffee growth | -1.4% | National, with stricter enforcement in England and Wales | Short term (≤ 2 years) |

| Arabica cost volatility post-brexit tariffs | -0.8% | National, affecting all United Kingdom regions equally | Medium term (2-4 years) |

| RTD coffee faces stiff competition for shelf space from emerging alternatives | -0.9% | National, with intensified competition in England's dense retail market | Medium term (2-4 years) |

| Caffeine concerns curbing RTD coffee | -0.5% | National, with health-conscious segments in urban England leading concern | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Amount of HFSS Sugar Limiting Iced Coffee Growth

High sugar content in Ready-to-Drink (RTD) coffee products constrains market growth in the United Kingdom, despite the category's increasing popularity. Health-conscious consumers examining ingredient labels find that many RTD coffee products contain sugar levels similar to soft drinks. This conflicts with the current consumer preference for wellness and clean-label products, especially among Millennials and Gen Z consumers. The UK's Soft Drinks Industry Levy and public health initiatives have increased consumer awareness about sugar consumption risks, leading many to avoid high-sugar beverages. RTD coffee products from major United Kingdom chains reveal substantial sugar content - a Starbucks caramel frappuccino contains 48.5g of sugar, while a Caffe Nero Belgian chocolate frappe contains 44.5g. These sugar levels highlight the disconnect between current product offerings and consumer health preferences in the United Kingdom RTD coffee market.

Arabica Cost Volatility Post-Brexit Tariffs

The implementation of post-Brexit tariff structures has significantly increased arabica coffee price volatility, substantially impacting operational margins and supply chain dynamics within the United Kingdom's ready-to-drink (RTD) coffee manufacturing sector. The prevailing global climate conditions affecting coffee-growing regions have intensified market challenges. Tchibo, a significant European coffee roaster, has announced price adjustments of 50 cents to EUR 1 per pound commencing April 2025, attributing the increase to elevated world market costs. These price modifications particularly affect the United Kingdom's premium RTD coffee segment, which relies heavily on high-quality arabica beans, potentially constraining expansion in these rapidly growing market segments. Beyond raw material cost implications, supply chain disruptions have necessitated Tchibo to restructure its e-commerce logistics operations to optimize cost efficiency. United Kingdom manufacturers must additionally navigate complex post-Brexit import protocols, creating strategic advantages for organizations maintaining diversified sourcing frameworks and vertical integration capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Cans Dominate While Cartons Accelerate

Cans hold 48.25% of the UK RTD coffee market in 2025, making them the dominant packaging format due to their portability, extended shelf life, and premium positioning capabilities. This dominance aligns with consumer demand for on-the-go consumption. The Automatic Vending Association (AVM) reported that the Coffee-to-Go segment generated EUR 758 million in product revenue in 2023, underlining the importance of convenience in packaging choices . Cartons are expected to grow at a 5.05% CAGR from 2026-2031, driven by their environmental benefits and cost efficiency in a market increasingly focused on sustainability.

Bottles, including glass and PET formats, retain a substantial market share despite moderate growth rates. Premium RTD coffee brands use glass bottles to emphasize quality and sustainability. In 2024, Jimmy's Iced Coffee introduced its SlimCan range priced at EUR 1.39, targeting convenience stores and impulse purchases. The packaging market is advancing with the integration of smart packaging features, including QR codes and NFC technology, which enable digital interaction with physical products.

By Product Type: Cold Brew Challenges Iced Latte Dominance

In the United Kingdom, Iced Latte/Cappuccino products maintain a 51.62% market share in 2025, as British consumers demonstrate a preference for these familiar flavours when transitioning from hot coffee to RTD formats. Cold Brew RTD Coffee has established itself as the fastest-growing segment in the UK market, with a projected CAGR of 7.29% during 2026-2031. This growth is attributed to its refined taste profile and higher caffeine content, particularly resonating with the British youth demographic.

The Functional/Protein-Enhanced RTD Coffee segment represents a significant innovation frontier in the United Kingdom market, addressing British consumers' evolving preferences for beverages that deliver multiple nutritional benefits beyond refreshment and caffeine. Nitro RTD Coffee maintains a specialised position in the United Kingdom market, with its distinctive characteristics creating differentiation opportunities, particularly in premium British retail establishments where experiential factors influence purchasing behaviour.

By Flavor Profile: Plain Classics Lead While Flavored Options Accelerate

In the United Kingdom ready-to-drink coffee market, Plain/Classic flavors maintain a dominant 51.74% market share in 2025, demonstrating British consumers' strong preference for authentic coffee taste profiles. The flavored variants segment in the ready-to-drink coffee market is projected to grow at a 6.97% CAGR during 2026-2031, primarily driven by younger British consumers seeking new taste experiences and sweeter profiles that reduce coffee's natural bitterness. Ready-to-drink coffee ranks among the top categories for flavor experimentation among United Kingdom consumers.

The United Kingdom's ready-to-drink coffee market has expanded beyond basic vanilla and caramel offerings into more complex flavor combinations. In May 2025, Jimmy's Iced Coffee introduced a limited-edition Donut flavor to target consumers seeking differentiated coffee varieties. While flavor innovation presents growth opportunities, manufacturers in the United Kingdom must address increasing consumer concerns regarding sugar content and health considerations.

By Ingredient Base: Plant-Based Alternatives Challenge Dairy Dominance

In the United Kingdom's RTD coffee market, dairy-based products maintain a 70.55% market share in 2025, capitalising on milk's natural compatibility with coffee and its established position in British consumer preferences for creamy textures. Plant-based milk alternatives in the United Kingdom market are advancing at 8.19% CAGR (2026-2031), driven by the rising prevalence of lactose intolerance among British consumers, ethical considerations, and increasing health awareness. Oatly's introduction of "Barista Organic Oat Drink" in February 2024 in the United Kingdom retail channels exemplifies how plant-based manufacturers are emphasising premium offerings and health benefits to expand their presence in the British market.

The expansion of plant-based alternatives in the United Kingdom has fostered strategic partnerships between established British coffee brands and plant-based milk producers for co-branded products. The United Kingdom market is further diversifying beyond traditional dairy and plant-based segments to incorporate functional ingredients such as prebiotic fibers and adaptogens, aligning with British consumer preferences for health-enhanced beverages.

By Distribution Channel: Online Growth Outpaces Traditional Retail

Supermarkets/Hypermarkets hold the dominant position in RTD coffee distribution with a 57.68% market share in 2025, supported by their extensive retail presence and cold chain infrastructure that enables them to maintain the broadest RTD coffee product selection. The online retail channel projects significant expansion at 11.75% CAGR during 2026-2031, transforming consumer RTD coffee purchasing patterns in response to broader e-commerce adoption. According to the Office for National Statistics (UK), e-commerce sales constituted 26.8% of total retail sales in Great Britain as of March 2025, with food-related online sales representing over 9% . This market development demonstrates the increasing importance of online retail channels for Ready-to-Drink (RTD) coffee products. Companies are utilizing e-commerce platforms to expand their distribution networks, implement subscription-based revenue models, and provide direct-to-consumer beverage delivery services.

Convenience and grocery stores serve as key distribution points, with their consumer proximity generating spontaneous purchase opportunities for RTD coffee brands. The expansion of vending solutions offers additional distribution channels, exemplified by Lavazza Professional UK's introduction of 'Lavazza on the Move' self-serve coffee machines in May 2024, targeting high-traffic locations through partnerships with convenience stores and petrol stations (World Coffee Portal, 2024). This distribution expansion necessitates comprehensive omnichannel strategies from brands to maintain a consistent market presence across physical and digital platforms.

By Price Positioning: Premium Segment Narrows Gap with Mass Market

Mass-market products hold a 62.41% market share in 2025, supported by extensive distribution networks and competitive pricing that drive high sales volumes. The Premium segment is experiencing growth at 6.26% CAGR (2026-2031), as consumers demonstrate increased preference for higher quality products, unique flavors, and enhanced functional benefits.

The expanding premium segment has created market entry opportunities for specialty coffee brands moving from foodservice into retail channels. In 2024, Grind's nationwide launch in Tesco supermarkets exemplifies this shift, introducing café-quality RTD coffee products to mass retail environments. The market's price structure continues to evolve with super-premium products targeting luxury consumption and gift-giving segments. This market segmentation establishes distinct competitive environments across price tiers, where mass-market companies compete on price and distribution capabilities, while premium brands emphasize quality and brand identity.

Geography Analysis

England holds 84.35% of the UK RTD coffee market share in 2025, driven by its larger population, higher concentration of urban professionals, and established specialty coffee culture. London functions as the category's innovation center, where new product launches typically occur before national rollout. England maintains market leadership as Europe's largest specialty coffee market, driven by high out-of-home consumption of specialty-grade coffee, according to the Center for the Promotion of Imports.

Northern Ireland shows the highest growth rate with a projected 7.46% CAGR for 2026-2031, exceeding the national average despite its smaller population. This growth stems from Belfast's increasing urbanization and expanding retail distribution networks that enhance product accessibility. The region's growth is supported by its younger population and the trade opportunities arising from its unique post-Brexit trading position.

Scotland and Wales maintain modest but growing market shares, each with distinct consumption patterns. Scotland's market shows stronger performance in Edinburgh and Glasgow, while Wales demonstrates consumption across both urban and rural regions. Both areas offer growth opportunities for companies that customize their marketing and distribution approaches to regional preferences. The expansion of specialty coffee culture beyond London creates additional market opportunities, with regional events such as the Manchester Coffee Festival increasing specialty coffee awareness.

Competitive Landscape

The United Kingdom's ready-to-drink (RTD) coffee market is moderately consolidated, with major beverage manufacturers controlling distribution networks, while specialty coffee producers maintain market share through premium product offerings. The market structure encompasses major corporations, including Starbucks Corporation, The Coca-Cola Company, Carlsberg Group (Britvic plc), Emmi AG, and Luigi Lavazza S.p.A., each maintaining significant market presence.

These market leaders capitalize on their substantial economies of scale and comprehensive marketing infrastructure to implement rapid market responses and strategic product launches across diverse consumer demographics. Their competitive position is fortified through extensive manufacturing capabilities, established global procurement networks, and substantial resources for executing comprehensive marketing initiatives that create significant barriers to entry for smaller market participants.

The dominant market players consistently implement facility expansion strategies and production capacity enhancement programs to maintain their market position. Additionally, these corporations engage in strategic collaborations to develop innovative product portfolios aligned with evolving consumer preferences. Product innovation remains the primary competitive strategy employed by market participants to address dynamic market conditions and maintain competitive advantage.

United Kingdom Ready-to-Drink (RTD) Coffee Industry Leaders

-

Starbucks Corporation

-

The Coca-Cola Company

-

Luigi Lavazza S.p.A.

-

Carlsberg Group (Britvic plc)

-

Emmi AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Starbucks Corporation expanded its ready-to-drink (RTD) coffee product line in the United Kingdom with two plant-based varieties. The company introduced Oat-Based Cappuccino and Oat-Based Caramel Macchiato to its Chilled Classics range to address the growing consumer demand for dairy-free alternatives.

- February 2025: Tom Parker Creamery introduced The Guv'nor, a new line of ready-to-drink (RTD) iced coffees in Original, Mocha, and Caramel flavors. The beverages are packaged in recyclable glass bottles of 500 ml and 250 ml sizes with metal caps.

- July 2024: Perth-based coffee startup Hunt and Brew introduced three ready-to-drink coffee products in Tesco Express stores across the United Kingdom. The company produces coffee beverages using fresh milk without added sugar, emphasizing craftsmanship and artistry in its production process.

- June 2024: Ueshima Coffee Company introduced two ready-to-drink (RTD) canned coffee products in the United Kingdom market: Iced Latte and Iced Matcha Latte. The products were available for nationwide distribution.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom ready-to-drink coffee market as all shelf-stable, pre-packaged coffee beverages (plain or flavored, dairy or plant-based) that can be consumed without additional brewing, covering cans, bottles, and cartons sold through retail and on-premise channels.

Scope Exclusion: freshly brewed beverages served in cafés, coffee concentrates for foodservice, and powdered mixes lie outside this scope.

Segmentation Overview

-

By Packaging Type

-

Bottles

- Glass Bottles

- PET Bottles

- Cans

- Cartons

- Others

-

Bottles

-

By Product Type

- Cold Brew RTD Coffee

- Iced Latte/Cappuccino

- Nitro RTD Coffee

- Functional/Protein-Enhanced RTD Coffee

-

By Flavor Profile

- Plain/Classic

- Flavored

-

By Ingredient Base

- Dairy-Based

- Plant-Based Milk

-

By Price Positioning

- Mass

- Premium

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience and Grocery Stores

- Online Retail Stores

- Others (Vending Machine, Forecourt Stores, etc)

-

By Geography

- England

- Scotland

- Wales

- Northern Ireland

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed brand managers at regional bottlers, packaging converters, chilled distribution specialists, and convenience-store buyers across England, Scotland, and Wales. Follow-up surveys with Gen Z consumers helped benchmark purchase frequency, while talks with food-service procurement heads validated on-premise uptake. These discussions filled data gaps and aligned our desk estimates with on-ground sentiment.

Desk Research

We began by mapping the consumption universe using public touchpoints such as HM Revenue & Customs trade codes, Food Standards Agency labeling rules, the British Soft Drinks Association shipment updates, and consumer panels from the Office for National Statistics. Company filings and investor decks from leading beverage fillers provided average selling prices, while trend journals like Nutrition Bulletin illustrated flavor and health claims gaining shelf space. Subscription datasets, including D&B Hoovers for company revenue splits and Dow Jones Factiva for deal flow, helped size corporate footprints. The sources cited here are illustrative; many additional references informed data gathering, verification, and clarification.

Market-Sizing & Forecasting

We applied a top-down model that reconstructs national demand from import volumes, domestic roast-and-extract output, and retail scan data, which are then cross-checked with selective bottom-up roll-ups of leading suppliers' case sales. Key variables like per-capita iced-coffee occasions, convenience-store density, aluminum-can share, average unit price, sugar-tax impacts, and promotional frequency drive the historical base. A multivariate regression forecasts each driver, after which scenario analysis adjusts for macro shocks such as cost-of-living shifts. Data voids, for example from private brands, are bridged through channel-check ranges approved by two senior reviewers.

Data Validation & Update Cycle

Outputs pass three layers of variance checks, are peer-reviewed by a senior beverages specialist, and reconfirmed with at least one source from each respondent group. Mordor refreshes the model annually and issues interim tweaks within four weeks of any material event, ensuring clients receive the latest calibrated view.

Why Mordor's UK Ready-to-Drink (RTD) Coffee Baseline Earns Trust

Published estimates often diverge because firms differ in product scope, price conversion, and refresh cadence.

Key gap drivers include whether chilled short-shelf-life lattes are counted, if online-only private labels are tracked, and the currency year adopted. Mordor adopts a harmonized scope, converts all values to constant 2024 USD, and revalidates assumptions yearly; other publishers may rely on infrequent retailer scans or extrapolate Europe-wide ratios onto the UK.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 490.97 M (2025) | Mordor Intelligence | - |

| USD 292.0 M (2023) | Regional Consultancy A | Omits online grocery and food-service cans; early base year inflates CAGR |

| USD 145.5 M (2027) | Industry Database B | Tracks retail scan sales only and applies uniform 250 ml pack size for volume-to-value conversion |

The comparison shows that when scope breadth, timely data, and dual-source validation converge, Mordor's balanced baseline provides decision-makers with the most dependable reference point.

Key Questions Answered in the Report

What is the current value of the United Kingdom Ready-to-Drink (RTD) coffee market?

The United Kingdom Ready-to-Drink (RTD) coffee market is worth USD 520.84 million in 2026 and is projected to reach USD 699.46 million by 2031.

Which packaging format is growing fastest?

Carton packs are expanding at a 5.05% CAGR as consumers reward recyclable materials and longer shelf life.

How big is the plant-based RTD coffee segment?

Plant-based variants are rising at an 8.19% CAGR, challenging dairy’s 70.55% share by offering vegan and lactose-free options.

Which region in the UK is experiencing the fastest market growth?

Northern Ireland leads with a 7.46% CAGR through 2031, driven by urbanisation and rising demand for convenience beverages.

Page last updated on: