UK Pension Funds Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.23 Trillion |

| Market Size (2026) | USD 3.36 Trillion |

| Market Size (2031) | USD 4.09 Trillion |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Pension Funds Market Analysis by Mordor Intelligence

The UK pension funds market size was valued at USD 3.23 trillion in 2025 and estimated to grow from USD 3.36 trillion in 2026 to reach USD 4.09 trillion by 2031, at a CAGR of 4.01% during the forecast period (2026-2031). Ongoing policy reforms, mounting consolidation pressure, and the Mansion House Accord are reshaping investment appetites, steering fresh capital toward private markets and domestic infrastructure. Bulk-annuity activity is intensifying, de-risking mature defined benefit (DB) schemes while releasing corporate balance-sheet capacity for growth projects. Meanwhile, auto-enrolment keeps enlarging the contributor base, lifting defined contribution (DC) assets and compelling master trusts to refine digital member services. Although offshore allocations remain significant, a visible pivot toward onshore assets signals renewed confidence in the UK growth story.

Key Report Takeaways

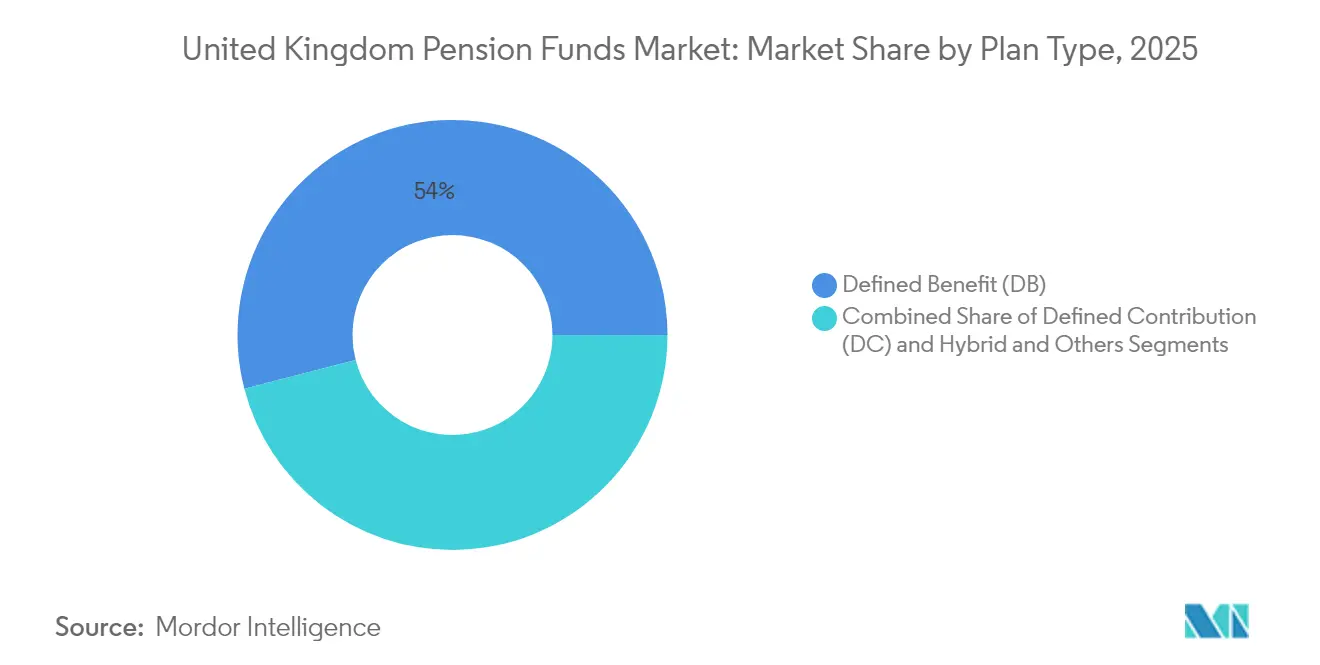

- By plan type, defined benefit schemes held 54.02% of the UK pension funds market share in 2025, while defined contribution assets are set to expand at a 6.92% CAGR through 2031.

- By investment strategy, active mandates controlled 63.05% of the UK pension funds market share in 2025; passive strategies are forecasted to grow at 5.75% CAGR to 2031.

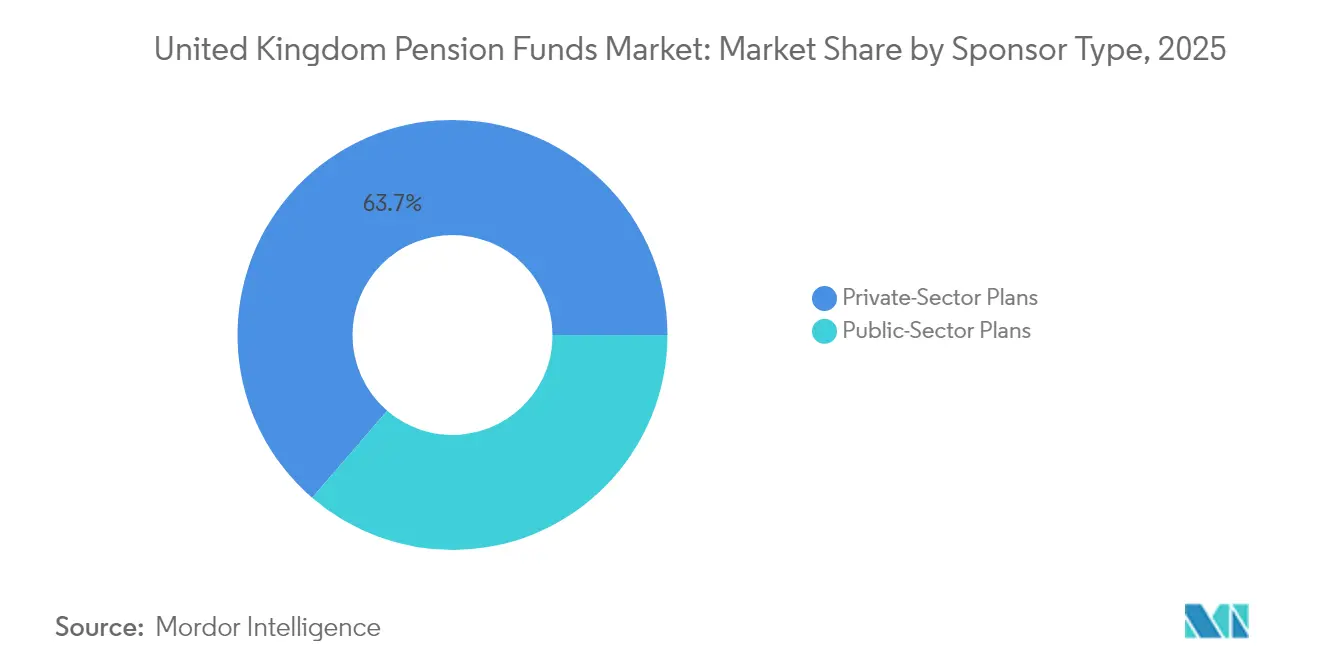

- By sponsor type, private-sector arrangements accounted for 63.68% of the UK pension funds market share in 2025, whereas public-sector schemes are projected to rise at a 5.51% CAGR through 2031.

- By geography of investment, offshore portfolios captured 56.54% share of the UK pension funds market size in 2025, and onshore allocations are advancing at a 4.97% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UK Pension Funds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Auto-enrolment expansion & rising minimum contributions | +1.2% | National, concentrated in England and Wales | Medium term (2-4 years) |

| Bulk-annuity buy-out momentum & risk-transfer deals | +0.8% | National, higher activity in private sector schemes | Long term (≥ 4 years) |

| Technology-enabled member engagement & digital advice | +0.4% | National, early adoption in master trusts | Medium term (2-4 years) |

| Shift from DB to DC schemes reshaping asset flows | +0.6% | National, accelerated in private sector | Long term (≥ 4 years) |

| Mansion House reforms channelling assets to productive UK finance | +0.7% | National, with focus on infrastructure and growth assets | Long term (≥ 4 years) |

| Consolidation into “mega-funds” enabling alternative-asset access | +0.5% | National, affecting LGPS and DC schemes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Auto-enrolment Expansion & Rising Minimum Contributions

Auto-enrolment thresholds remain unchanged for 2025-26, but the steady cadence of re-enrolment every three years keeps participation levels high [1]Department for Work and Pensions, “Automatic Enrolment Review,” gov.uk. The minimum 8% contribution rate, coupled with salary-sacrifice options that blunt higher National Insurance charges, is lifting cash inflows across master trusts. Providers enjoy scale benefits in administration and investment sourcing, which helps them maintain low charging structures even as member numbers rise. The UK pension funds market gains resilience from this predictable contribution stream, enabling longer-dated investments in illiquid assets. Regulatory oversight remains tight, yet it leaves room for design tweaks that sharpen member outcomes.

Bulk-annuity Buy-out Momentum & Risk-transfer Deals

Record funding levels and healthy gilt yields continue to unlock jumbo risk-transfer deals. Legal & General’s GBP 4.8 billion buy-in of the Boots Pension Scheme in June 2024 exemplified the appetite for comprehensive de-risking solutions. Multi-scheme transactions, such as Anglo American’s GBP 785 million package in March 2025, illustrate the search for operational efficiency and pricing certainty. Insurers are expanding underwriting capacity, intensifying competition, and compressing spreads paid by sponsors. Whole-scheme buy-ins now form a larger share of the pipeline, signaling confidence in surplus durability. This wave of activity funnels premium volumes into the UK pension funds market and encourages insurers to broaden risk-pooling strategies.

Technology-enabled Member Engagement & Digital Advice

Artificial-intelligence pilots, dashboard connectivity deadlines, and robo-advice integration are converging in 2025. Smart Pension joined an Innovate UK consortium to test AI-driven personalized nudges that could lift contribution rates and improve retirement adequacy. The Pensions Regulator’s data strategy calls for predictive analytics that safeguard savers while enabling dynamic communications. Pension dashboards will compel schemes to cleanse data and standardize interfaces, fostering industry interoperability. Master trusts exploit these tools to automate lifecycle rebalancing and cut operational overhead. Persistent cybersecurity vigilance remains mandatory to sustain member trust.

Shift from DB to DC Schemes Reshaping Asset Flows

With most private DB plans closed to new accrual, fresh contributions flow predominantly into DC vehicles, changing asset-mix demands. DC portfolios typically tilt toward equities and private market co-investments, contrasting with the liability-matching posture of maturing DB funds. Master trusts amass the scale needed to enter infrastructure and venture-capital arenas once reserved for larger DB peers. The UK pension funds market thus witnesses a redistribution of risk appetites, prompting asset managers to tailor growth-oriented strategies. Hybrid collective DC models are also gaining attention as policymakers explore avenues to improve risk sharing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interest-rate shocks & LDI-driven market-volatility risk | −0.6% | National, concentrated in DB schemes using LDI strategies | Short term (≤ 2 years) |

| Ageing demographics leading to higher benefit outflows than contributions | −0.4% | National, regional demographic variations | Long term (≥ 4 years) |

| DC charge-cap limits hindering private-market allocations | −0.3% | National, affecting DC schemes and master trusts | Medium term (2-4 years) |

| Data-intensive ESG/TCFD reporting cost burden | −0.2% | National, higher impact on smaller schemes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Interest-rate Shocks & LDI-Driven Market-volatility Risk

The January 2025 gilt sell-off pushed 10-year yields near 4.93%, triggering collateral calls for liability-driven investment (LDI) portfolios. Although improved buffers and a Bank of England repo backstop limited forced selling, the episode reminded trustees of liquidity fragilities. Pooled LDI funds still hold material leverage, and sudden rate jumps could require rapid asset sales. The UK pension funds market, therefore, remains exposed to mark-to-market volatility, demanding vigilant monitoring of leverage and liquidity.

Ageing Demographics Leading to Higher Benefit Outflows than Contributions

Pensioner numbers are set to climb 14% between 2025 and 2035, moving from 12.6 million to 14.4 million retirees [2]Institute of Chartered Accountants in England and Wales, “Aging Population and Fiscal Outlook,” icaew.com. Mature DB schemes already experience negative cash flow, forcing sales of liquid assets to cover benefits. A shrinking working-age population narrows the contribution base and weighs on payroll tax receipts, adding pressure on public finances. Long-dated liability profiles restrict investment flexibility and heighten the need for resilient liquidity planning. These demographic forces temper the growth potential of the UK pension funds market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Plan Type: DC Growth Accelerates Despite DB Dominance

Defined Benefit plans controlled 54.02% of the UK pension funds market size in 2025, illustrating the historical weight they carry within the UK pension funds market. Many schemes now enjoy near-full funding and are pursuing bulk-annuity solutions to hard-lock liabilities, which gradually shrink the pool yet preserve their sizeable footprint. Large public plans such as Universities Superannuation Scheme recorded GBP 77.9 billion in assets and a 114% funding level during 2024, underscoring the segment’s balance-sheet strength.

Defined Contribution assets, propelled by auto-enrolment and master-trust consolidation, are projected to expand at a 6.92% CAGR to 2031. That trajectory positions DC as the principal growth engine for the UK pension funds market, with collective DC experiments adding further momentum. The Mansion House Accord channels 10% of default DC assets into private markets, potentially enhancing long-term performance and engaging savers through tangible domestic-investment narratives. Hybrid structures provide transitional pathways for sponsors migrating away from DB obligations, yet the dominant flow of new money clearly sits with the DC side.

By Investment Strategy: Passive Gains Ground in Active-dominated Market

Active management accounted for 63.05% of the UK pension funds market size in 2025, fortified by complex liability hedging and bespoke ESG overlays in DB portfolios. Large schemes still rely on specialist duration and credit managers to navigate macro volatility and stewardship objectives. This preference sustains a robust revenue base for active shops, ensuring a steady pipeline of mandate renewals.

Passive strategies, however, are expected to grow 5.75% annually, driven by fee sensitivity and the regulator’s focus on value metrics. Master trusts often default to index funds to keep charges well below the cap, reinforcing scale benefits as membership balloons. The UK pension funds market size for passive vehicles is likely to swell alongside DC contributions, while active boutiques differentiate through private-market access, transition-aligned benchmarks, and deeper stewardship programmes. Mansion House reforms may revive demand for specialist active skills in illiquid assets where indexing remains impractical.

By Sponsor Type: Private Sector Leadership with Public Sector Momentum

Private-sector schemes accounted for 63.68% of the UK pension funds market size in 2025, reflecting decades of corporate provision and the surge in master-trust enrolments. Corporate sponsors leverage bulk annuity deals to eliminate balance-sheet volatility, freeing capital for core business investment. DC master trusts augment this dominance through targeted technology investment and white-label solutions for smaller employers.

Public-sector assets are projected to expand at a 5.51% CAGR through 2031, supported by Local Government Pension Scheme pooling and revised contribution frameworks. LGPS Central’s stewardship growth to GBP 29.9 billion highlights momentum generated by scale pooling . NHS Pension Scheme changes, including a rise in employer contributions to 23.7%, demonstrate the government's willingness to ensure sustainability. As consolidation gathers pace, public funds gain enhanced access to alternative assets and cost efficiencies, further enriching the UK pension funds market.

By Geography of Investment: Onshore Momentum Challenges Offshore Preference

Offshore holdings held 56.54% of the UK pension funds market size in 2025, a legacy of the search for diversification and a prolonged underweight to domestic equities. Many trustees value currency dispersion and exposure to high-growth overseas sectors absent in local indices. However, the Mansion House Accord mandates at least 5% of DC default assets in UK private markets, setting a roadmap for renewed domestic allocation.

Onshore investments are projected to grow at 4.97% CAGR as large players such as Phoenix Group and Schroders commit up to GBP 20 billion to high-growth UK businesses. British Growth Partnership support from Aegon UK further signals the directional shift. Trustees must balance fiduciary duty with policy nudges, ensuring domestic commitments do not compromise return objectives. Successful implementation will diversify capital sources for national infrastructure and scale start-ups, reinforcing the relevance of the UK pension funds market to broader economic strategy.

Geography Analysis

London and the Southeast remain the gravitational centre of pension assets, thanks to the concentration of financial headquarters, asset managers, and administrator hubs. Defined contribution master trusts tend to base decision-making functions in the capital, though member footprints span every region. Northern England and the Midlands rely heavily on Local Government Pension Schemes, whose pooling exercises aim to replicate the risk-adjusted returns achieved by larger sovereign peers.

Regional demographic disparities shape cash-flow profiles. Post-industrial areas with net outflows of younger workers see lower contribution inflows relative to benefit payments, raising liquidity management challenges for local schemes. Government “levelling up” policies nudge pension pools to consider regional infrastructure, housing, and private-equity projects. LGPS Central, for instance, has earmarked GBP 5.2 billion for UK investments, a portion of which targets real-asset projects that stimulate local job creation.

Cross-border considerations have grown since Brexit. The Finance Act 2025 introduced overseas transfer taxes and residency rules for scheme administrators, complicating operations for internationally mobile savers. Simultaneously, European consolidation, such as Allianz’s role in the EUR 3.5 billion Viridium Group transaction, highlights the scale race underway worldwide. The UK pension funds market thus balances domestic integration with global opportunity, ensuring its schemes remain competitive and diversified.

Competitive Landscape

The master-trust arena illustrates rising concentration: 84% of DC memberships sit with a handful of authorized providers. Nest, Aviva Master Trust, Legal & General Mastertrust, and The People’s Pension dominate inflows, leveraging technology and ESG frameworks to distinguish value propositions. Selective authorization keeps entry barriers high, prompting smaller trusts either to merge or exit.

Bulk annuity insurers compete intensely for jumbo transactions, with Legal & General strengthening its franchise through overseas partnerships that extend underwriting reach. Scottish Widows, meanwhile, has rolled out an open-architecture LTAF to satisfy private-market appetite from its 4 million workplace savers. Technology disruptors like Smart Pension experiment with AI-driven engagement, compressing administrative costs, and improving member experience.

Scale advantages manifest in fee negotiation, access to co-investments, and risk-pooling capabilities. Yet white-space remains around bespoke ESG integration, mid-market private credit, and post-retirement drawdown solutions. Providers that blend robust governance, competitive charges, and innovative investment design are poised to capture incremental share within the expanding UK pension funds market.

UK Pension Funds Industry Leaders

Nest Corporation

Aviva Master Trust

Legal & General Mastertrust

The People’s Pension (B&CE)

Scottish Widows Master Trust

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Legal & General sold its US protection business to Meiji Yasuda Life for USD 2.3 billion, forging a partnership to scale US pension-risk-transfer activities.

- May 2023: Seventeen pension providers signed the Mansion House Accord, pledging 10% of DC default assets to private markets, with 5% ring-fenced for UK investments.

- April 2025: Scottish Widows launched an open-architecture LTAF, offering workplace savers exposure to private equity, social housing and private credit.

- March 2025: Anglo American completed a GBP 785 million multi-scheme buy-in with Legal & General, covering 7,600 members under a price-lock structure.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom pension fund market as the total assets pooled by occupational and personal pension schemes domiciled in the UK, covering trust-based defined benefit, defined contribution, hybrid structures, and contract-based group personal pensions, whose capital is invested onshore or offshore with the objective of delivering retirement income. According to Mordor Intelligence analysts, plan liabilities transferred to insurers through bulk-annuity buy-ins and buy-outs remain inside the addressable base until final settlement, while assets managed for unfunded state pensions are excluded from the model.

Scope Exclusions: We leave out the state basic pension, unfunded public-sector pay-as-you-go arrangements, and non-UK schemes that merely allocate into UK securities.

Segmentation Overview

- By Plan Type

- Defined Contribution (DC)

- Defined Benefit (DB)

- Hybrid and Others

- By Investment Strategy

- Active

- Passive

- By Sponsor Type

- Public-Sector Plans

- Private-Sector Plans

- By Geography of Investment

- Onshore

- Offshore

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then interviewed trustee directors, master-trust CIOs, bulk-annuity specialists, and investment-consulting actuaries across England, Scotland, and Wales. Insights on consolidation thresholds, target-date glide-paths, and Mansion House private-market quotas helped us validate desk findings, plug data gaps, and fine-tune assumption ranges.

Desk Research

We began by mining authoritative, non-paywalled datasets such as the Office for National Statistics Financial Survey of Pension Schemes, The Pensions Regulator scheme returns, Bank of England capital-market tables, HM Treasury consultation papers, and trade-body compendiums from the Pensions Policy Institute and Investment Association. Company filings and parliamentary committee transcripts added narrative on funding ratios and regulatory intent. Subscription resources, including D&B Hoovers for sponsor financials and Dow Jones Factiva for deal flow, supplemented the public record. These sources anchored historical asset levels, contribution flows, and asset-allocation fingerprints. The list is illustrative, not exhaustive; many additional references informed data checks and clarifications.

A second scan assembled price, yield, and volume series for gilts, corporate bonds, equities, and private-market vehicles from BoE Interactive, London Stock Exchange, and Questel patent trends to benchmark innovation exposure. These feeds allowed us to reconcile valuation swings after the 2022 LDI liquidity episode.

Market-Sizing & Forecasting

We applied a blended top-down asset-pool reconstruction, starting with ONS asset stocks that were split by scheme type, and then layering plan-level contribution, benefit-outflow, and liability-hedge ratios to derive the baseline value. Select bottom-up cross-checks, such as sampled administrator asset-per-member counts and buy-in premium roll-ups, tested plausibility. Key model drivers include auto-enrollment penetration, average contribution rate, bulk-annuity transaction volume, portfolio shift toward private markets, interest-rate glide, and average asset-management fee compression. Forecasts through the forecast period use multivariate regression blended with scenario analysis, with stress cases reviewed by primary-research experts. Data voids, for instance smaller DC micro-schemes, were bridged with calibrated ratios drawn from larger peer cohorts.

Data Validation & Update Cycle

Outputs pass a three-step review: variance checks against independent metrics, senior-analyst sign-off, and a pre-publication refresh. We revisit the model each year, while material events, rate shocks, major policy papers, or GBP5 billion-plus bulk-annuity deals trigger interim updates.

Why Mordor's UK Pension Fund Baseline Commands Reliability

Market estimates often diverge because publishers choose different asset scopes, convert currencies at varying dates, or freeze refresh cycles for several years.

Key gap drivers include whether unfunded public liabilities are counted, how bulk-annuity assets are treated, the assumed pace of DC auto-enrollment growth, and the frequency of FX and mark-to-market resets. Mordor Intelligence refreshes annually and applies Bank of England daily FX fixes, whereas others may lock rates at report launch or omit insurer-held assets after buy-outs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.23 trillion | Mordor Intelligence | - |

| USD 4.29 trillion | Global Consultancy A | Includes unfunded public schemes and double-counts insurer-held assets |

| USD 0.85 trillion | Regional Consultancy B | Uses a narrow sample of contract-based DC plans and applies 2023 FX rates without mark-to-market update |

In summary, our disciplined scope selection, timely FX adjustment, and dual-track validation give decision-makers a balanced, transparent baseline that can be retraced to clear variables and repeated steps.

Key Questions Answered in the Report

What is the current size of the UK pension funds market?

The market holds USD 3.36 trillion in assets as of 2026 and is forecasted to reach USD 4.09 trillion by 2031.

How fast is the defined contribution segment growing?

Defined Contribution assets are expanding at 6.92% CAGR, the fastest among all plan types.

Why is there a push toward onshore investment?

The Mansion House Accord requires at least 5% of DC default assets to be invested in UK private markets, aiming to channel capital into domestic businesses and infrastructure.

What role do bulk-annuity deals play in the market?

Bulk annuities transfer pension liabilities to insurers, allowing corporate sponsors to remove risk from balance sheets and fueling insurer competition for large transactions.

How is technology changing member engagement?

AI-driven tools, pension dashboards, and robo-advice platforms are improving data clarity, personalizing communications, and reducing administrative costs across schemes.

What are the main risks facing DB schemes?

Interest-rate volatility exposes liability-driven investment strategies to collateral calls, while an ageing demographic pressures cash flow as benefit payments outpace contributions.

Page last updated on: