PMMA Microspheres Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

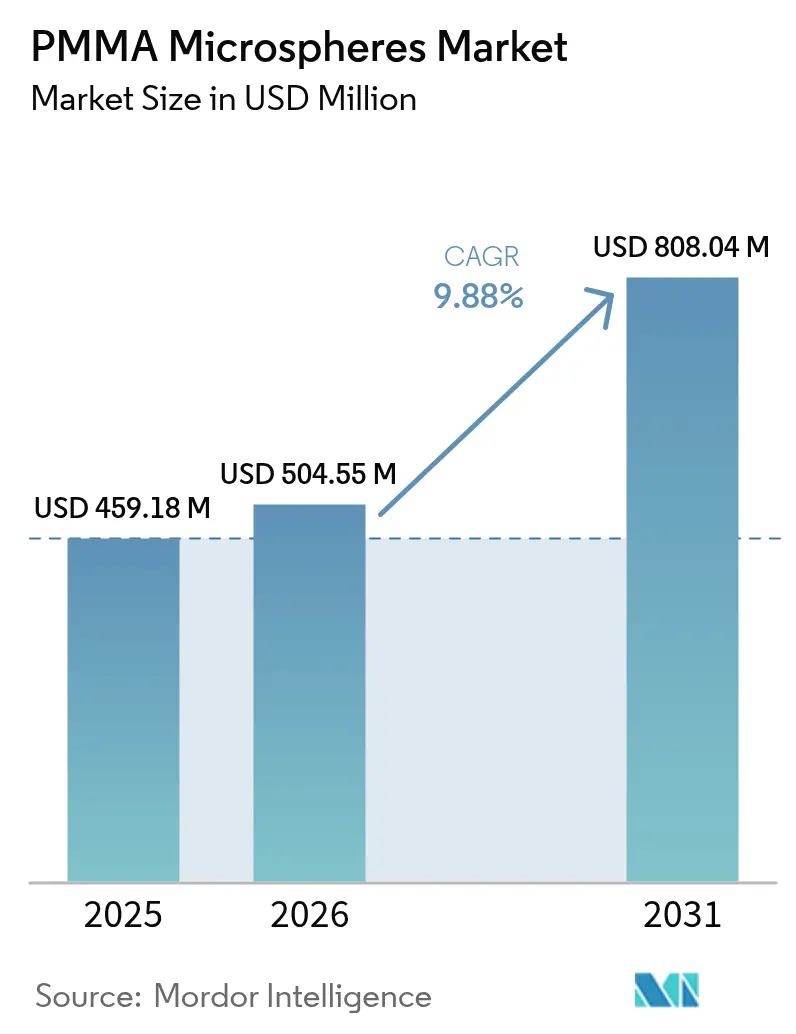

| Market Size (2026) | USD 504.55 Million |

| Market Size (2031) | USD 808.04 Million |

| Growth Rate (2026 - 2031) | 9.88% CAGR |

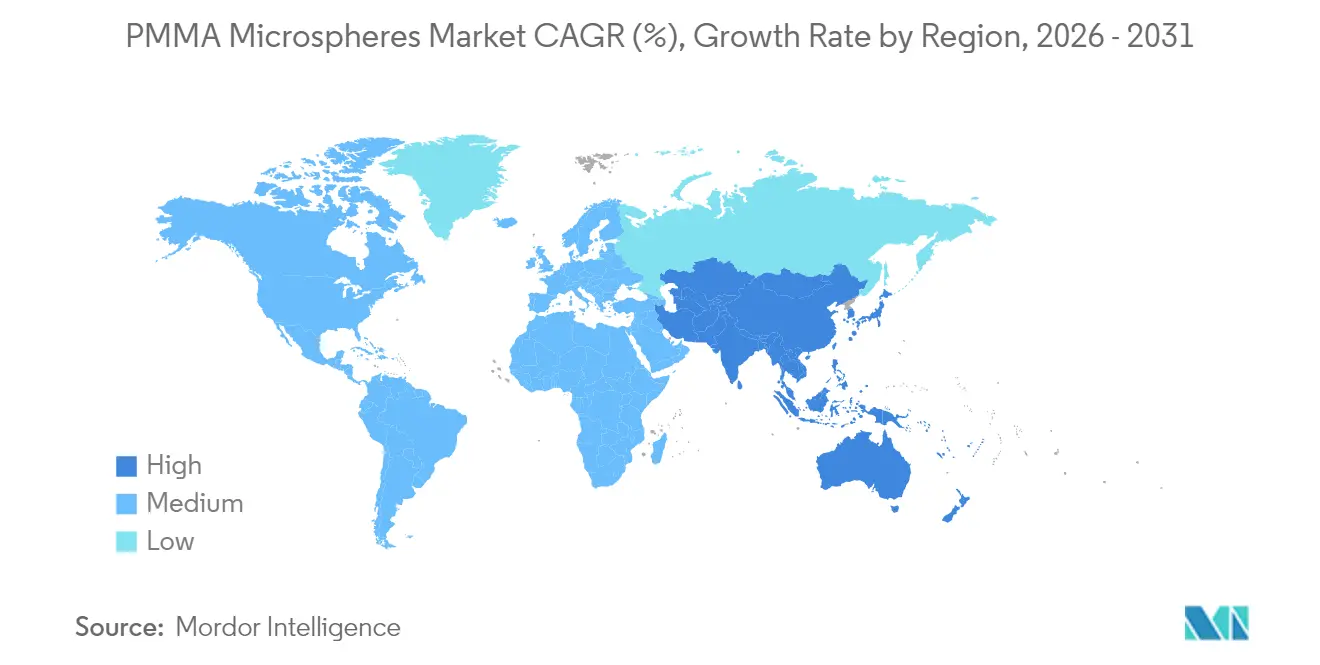

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

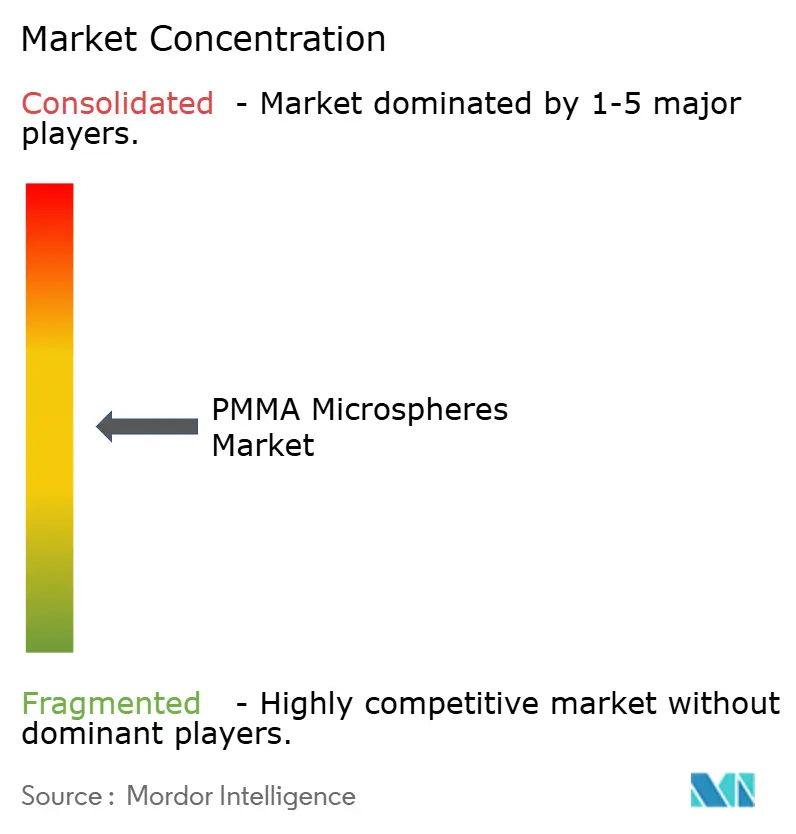

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PMMA Microspheres Market Analysis by Mordor Intelligence

The PMMA Microspheres market size is expected to grow from USD 459.18 million in 2025 to USD 504.55 million in 2026 and is forecast to reach USD 808.04 million by 2031 at 9.88% CAGR over 2026-2031. This strong trajectory reflects broadening adoption across aesthetic medicine, drug-delivery, advanced optics, and high-performance coatings. Growing demand for permanent dermal fillers, expansion of energy-efficient LED/LCD production, and the shift toward precision drug-delivery platforms are elevating volume and value growth. Producers are prioritizing monodisperse, surface-modified grades that command price premiums in life-science and electronics applications. Regulatory pressure on commodity microplastics is steering innovation toward sustainable or high-value niches rather than suppressing overall demand, while capacity optimization by large MMA suppliers is underpinning a tighter but more profitable supply environment.

Key Report Takeaways

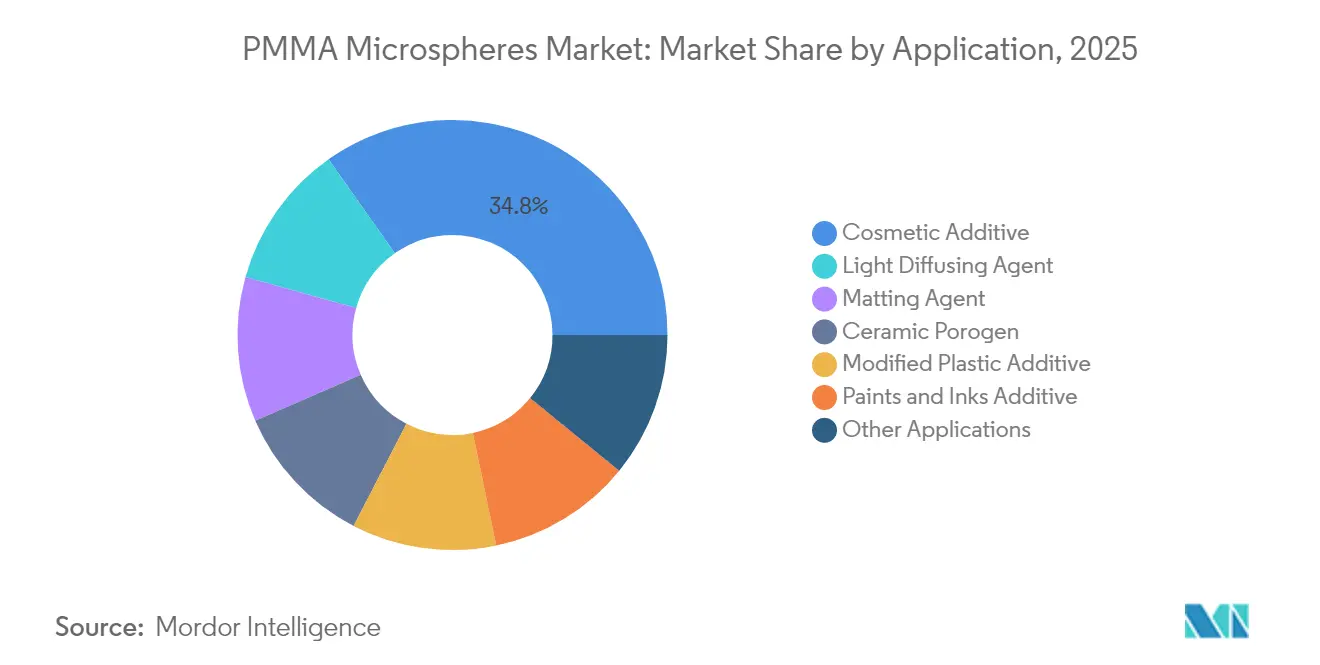

- By application, Cosmetic Additive led with 34.78% of PMMA microspheres market share in 2025; Ceramic Porogen applications are projected to expand at an 11.55% CAGR through 2031.

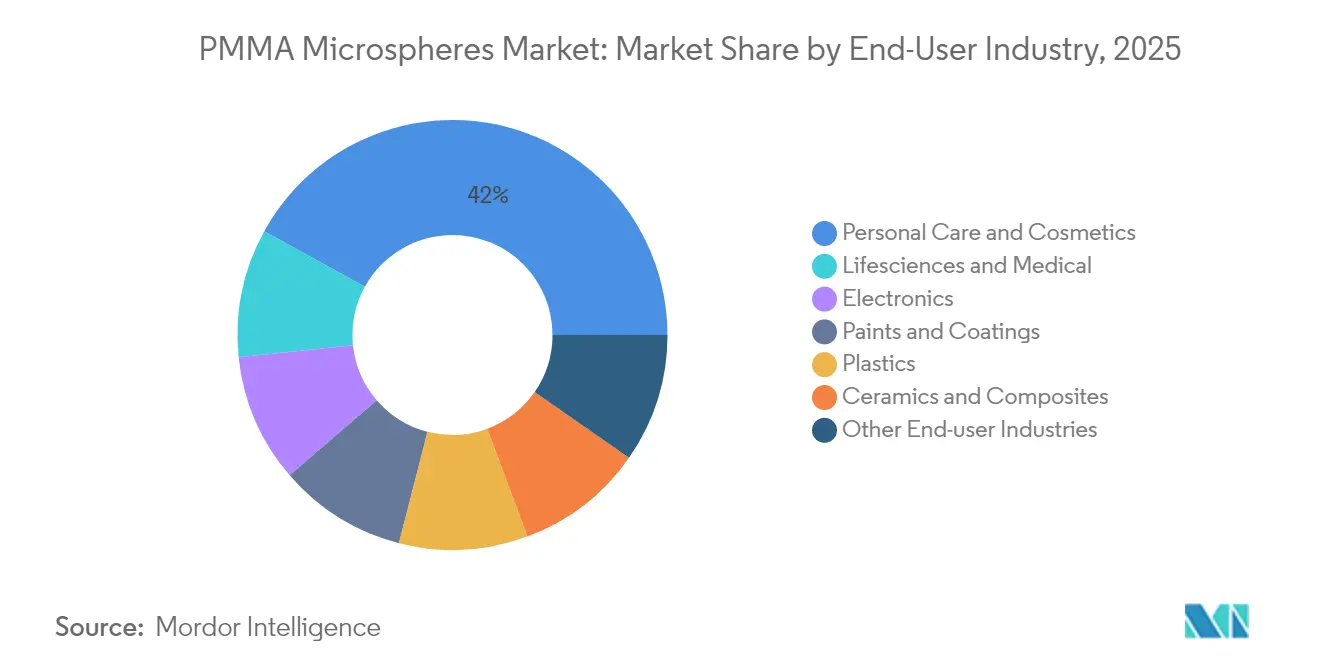

- By end-user industry, Personal Care & Cosmetics held 41.98% of the PMMA microspheres market share in 2025, while Lifesciences & Medical is forecast to grow the fastest at 12.35% CAGR to 2031.

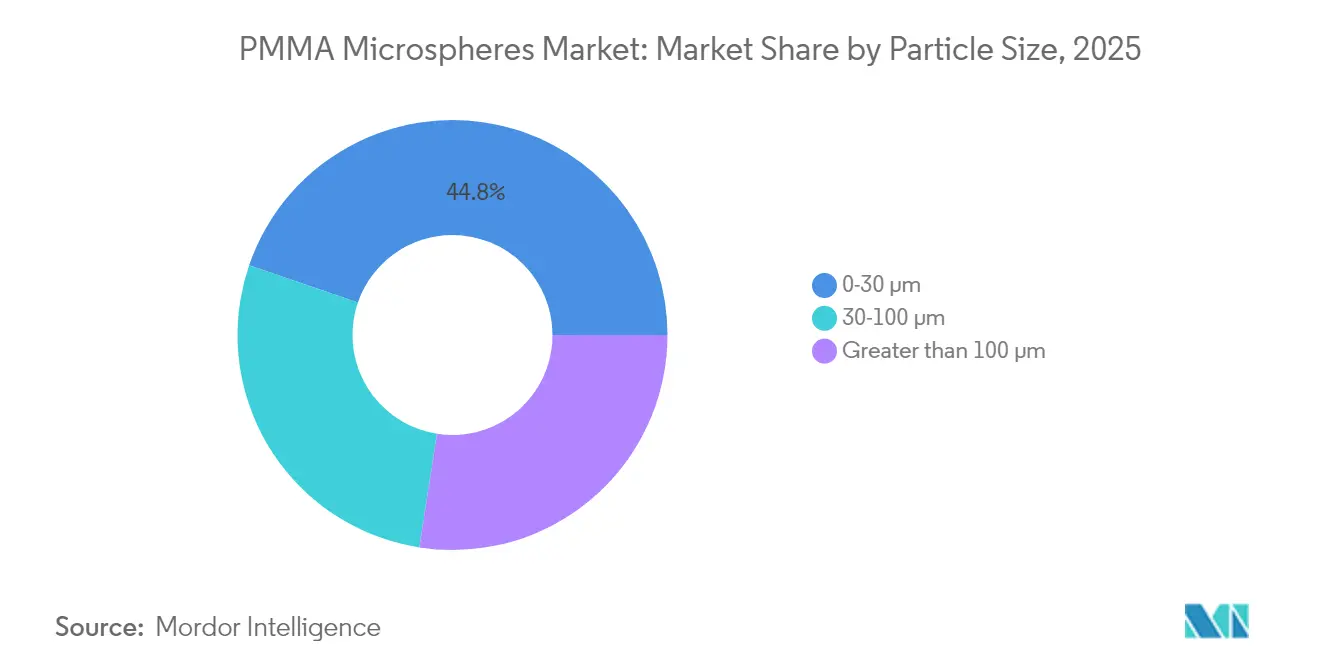

- By particle size, the 0-30 µm segment commanded 44.75% of the PMMA microspheres market size in 2025, whereas the 30-100 µm range is expected to post a 13.62% CAGR during 2026-2031.

- By region, Asia-Pacific captured 39.05% of PMMA microspheres market share in 2025 and is projected to expand at a 10.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global PMMA Microspheres Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for PMMA dermal fillers in minimally-invasive aesthetics | +2.80% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Expanding use in drug-delivery & embolization therapies | +2.10% | Global, with concentration in developed markets | Long term (≥ 4 years) |

| Adoption as light-diffusing & matting agents in LED/LCD, coatings | +1.90% | APAC core, spill-over to global electronics hubs | Short term (≤ 2 years) |

| Rising utilisation in personal-care formulations for texture enhancement | +1.70% | Global, led by premium cosmetics markets | Medium term (2-4 years) |

| Microfluidic diagnostic devices requiring PMMA calibration beads | +1.20% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for PMMA Dermal Fillers in Minimally-Invasive Aesthetics

Bellafill, the only FDA-approved permanent injectable containing 20% PMMA microspheres, delivers wrinkle correction that persists for up to 15 years. A low 0.011% granuloma incidence reported across 4,725 gluteal-augmentation procedures underscores long-term safety[1]Berthold Lemperle, “Fifteen-Year Follow-Up of PMMA Microsphere Fillers,” Aesthetic Surgery Journal, aestheticsurgeryjournal.org . Microspheres in the 30-50 µm range resist phagocytosis yet foster collagen ingrowth, providing durable tissue support. Large-volume body-contouring usage is expanding the PMMA microspheres market by broadening the patient base beyond facial aesthetics. Clinics value reduced retreatment frequency, creating steady pull-through for medical-grade suppliers.

Expanding Use in Drug-Delivery & Embolization Therapies

PMMA microspheres offer lower nonspecific protein binding than polystyrene, improving biocompatibility in controlled-release systems. Surface carboxyl functionality enhances drug conjugation, while the density of 1.19 g/cc eases centrifugation handling. Continuous production of monodisperse porous particles with 50 nm pores now supports oncology drug-eluting beads. Commercial interest is rising as continuous manufacturing cuts costs and tightens batch consistency.

Rising Utilisation in Personal-Care Formulations for Texture Enhancement

Encapsulation of ethylhexyl salicylate within PMMA microspheres increases SPF by 40% while mitigating skin irritation. Spray-dried PMMA-boron nitride composites deliver soft focus and thermal conductivity for high-definition makeup. EU Regulation 2023/2055 restricts synthetic polymer microparticles in rinse-off products by 2027 and leave-on products by 2029, encouraging premium brands to reserve PMMA microspheres for high-value leave-on creams and exploring bio-based substitutes for mass lines.

Microfluidic Diagnostic Devices Requiring PMMA Calibration Beads

Diagnostic-chip manufacturers employ monodisperse PMMA beads as flow-rate calibrants and optical reference standards, leveraging tight coefficient-of-variation control below 3%. As point-of-care testing expands, reliable bead supplies underpin assay reproducibility, especially in infectious-disease and oncology panels across advanced health-care markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory scrutiny over permanent dermal-filler safety | -1.40% | Global, stricter in EU and emerging markets | Medium term (2-4 years) |

| MMA monomer price volatility impacting production costs | -0.90% | Global, acute in regions with limited MMA capacity | Short term (≤ 2 years) |

| Limited global capacity for monodisperse high-precision grades | -0.70% | Global, concentrated in specialized applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Scrutiny Over Permanent Dermal-Filler Safety

Only one PMMA-based filler has FDA clearance, underscoring rigorous evidence requirements. Adverse events correlate with injection depth; submucosal placement increases nodule formation, prompting practitioner training mandates[2]João de Jesus, “Complication Rates in PMMA Gluteal Augmentation,” PubMed, pubmed.ncbi.nlm.nih.gov . Mandatory skin tests for bovine collagen carriers add cost. Emerging markets are tightening regulations, potentially lengthening approval timelines, and limiting broad uptake despite clinical durability advantages.

MMA Monomer Price Volatility Impacting Production Costs

Sumitomo Chemical cut 80% of MMA and 70% of PMMA capacity in Singapore in late 2024, tightening Asian supply and lifting spot prices. Kuraray’s integration moderates volatility in Japan, yet feedstock shortages periodically raise costs for downstream bead producers. Chemical recycling initiatives such as Mitsubishi Chemical’s microwave-depolymerization may temper input-price swings once scaled.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Cosmetic Additive Retains Leadership amid Sustainability Pivot

Cosmetic Additive applications held 34.78% of PMMA microspheres market share in 2025, valued for imparting silky texture, soft-focus optics, and controlled release of actives. Premium skincare, color cosmetics, and suncare continue to specify medical-grade, low-residual MMA beads to satisfy safety audits. EU microplastic rules, however, are shifting large-volume mass-market lotions toward bio-based fillers, redirecting PMMA demand into leave-on serums and targeted anti-aging lines. Ceramic Porogen uses are accelerating at an 11.55% CAGR, as additive-manufactured alumina and zirconia components require sacrificial PMMA templates to engineer uniform pore networks critical for thermal-shock resistance. Light-diffusing agents in display films and matting additives in industrial coatings sustain mid-single-digit growth by delivering energy efficiency and low-gloss finishes, respectively. Modified Plastic Additive and Paints & Inks Additive segments absorb steady volumes where PMMA microspheres improve impact strength and rheology control.

By End-User Industry: Personal Care Dominance Meets Medical Momentum

Personal Care & Cosmetics accounted for 41.98% of the PMMA microspheres market size in 2025, leveraging enduring consumer appetite for premium tactile and optical performance. Brand owners fund extensive formulation trials that keep demand resilient despite regulatory headwinds. Lifesciences & Medical applications are expanding at 12.35% CAGR on the back of durable dermal-fillers, embolization beads, and in vitro diagnostics. Electronics manufacturers rely on PMMA microspheres to balance luminance and haze in LED light-guides, sustaining double-digit demand as screen sizes enlarge. Paints & Coatings value beads for uniform gloss reduction in high-durability architectural finishes. Plastics compounders incorporate larger spheres to enhance impact resistance in PMMA-based alloys used in automotive lenses. Ceramics & Composites players exploit sacrificial porogens to fine-tune density in aerospace and energy-storage components, pushing technical-grade volume growth above industrial averages.

By Particle Size: Fine-Particle Dominance with Mid-Range Upswing

Fine 0-30 µm grades delivered 44.75% of PMMA microspheres market size in 2025, essential for smooth sensory feel in skincare and accurate calibration in immunoassays. High surface-area-to-volume ratios favor efficient drug loading and consistent optical diffusion in thin films. The 30-100 µm band is projected to expand at a 13.62% CAGR, reflecting rising usage in ceramic porogens, injectable body-contouring fillers, and lightweight composite cores. Demand in this range benefits from improved processability through narrowing size tolerances. Particles above 100 µm remain niche, serving specialty calibration kits, filtration media, and academic research. However, tighter monodispersity in large diameters attracts premium pricing that offsets smaller volumes, sustaining a profitable if specialized sub-market.

Geography Analysis

Asia-Pacific led with 39.05% of PMMA microspheres market share in 2025. China’s display-panel makers, Japanese fine-chemicals specialists, and South Korean consumer-electronics brands provide a robust demand backbone. Capacity consolidation, including Sumitomo Chemical’s Singapore restructuring, nudges regional supply toward specialty grades yet maintains volume growth through 2031 at a 10.44% CAGR. Government incentives for semiconductor and medical-device supply chains further broaden downstream consumption.

North America benefits from stringent FDA standards, which favor domestic output of ISO-13485-compliant beads for injectable fillers and diagnostics. The Bellafill franchise anchors steady medical demand, while Wisconsin-based Nouryon has scaled specialty microsphere output for packaging and construction additives. R&D tax credits and venture capital funding in drug-delivery start-ups sustain innovation-driven consumption even as commodity volumes migrate offshore.

Europe faces the most restrictive polymer-micro-particle regulation, yet advanced-manufacturing bases in Germany and the Netherlands channel PMMA microspheres into high-margin coatings, automotive optics, and implantable medical devices. Producers are investing in bio-based or chemically recycled feedstocks that align with EU circular-economy goals, sustaining modest but profitable growth. South America and the Middle East & Africa remain emerging opportunity zones where growing healthcare infrastructure and infrastructure coatings uptake create incremental demand, though import dependence and regulatory variability temper rapid expansion.

Competitive Landscape

The PMMA microspheres market is moderately fragmented. Polysciences and Sekisui Kasei leverage vertically integrated production and ISO-certified quality management to service critical medical and electronic accounts. Bangs Laboratories focuses on diagnostic-grade calibration beads, commanding premiums for lot-to-lot uniformity. Sumitomo Chemical exerts upstream influence through MMA monomer and bulk PMMA supply, increasingly channeling output toward value-added bead formulations.

Strategic moves emphasize specialty capacity. Sumitomo Chemical started pilot production of chemically recycled PMMA in Japan, positioning recycled feedstock for electronic-grade beads. Companies are also entering joint development projects with display and cosmetics leaders to engineer application-specific surface chemistries that enhance compatibility and performance, reinforcing supply-chain partnerships and raising switching costs for buyers.

Competitive intensity is rising in sustainability. Several mid-sized firms are trialing bio-based PMMA precursors derived from plant-derived isobutylene. Early results indicate comparable refractive index and hardness, presenting a potential long-term competitive differentiator once cost parity is achieved. Intellectual-property portfolios focusing on continuous-flow polymerization and low-residual-monomer purification create barriers to entry for new participants.

PMMA Microspheres Industry Leaders

Cospheric LLC

Matsumoto Yushi-Seiyaku Co.,Ltd

Phosphorex

Polysciences

Sekisui Kasei Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sumitomo Chemical has commenced mass production of chemically recycled PMMA for high-quality applications in electronics and the automotive sectors. This development is expected to drive innovation and sustainability in the PMMA Microspheres market, enhancing its growth potential.

- April 2024: Sumitomo Chemical has partnered with Star Jewelry to develop applications for its sustainable acrylic material, Meguri. The company has established a pilot facility in Japan to chemically recycle polymethyl methacrylate (PMMA) and plans to commercialize its recycled PMMA, SUMIPEX Meguri, by fiscal year 2025.

Global PMMA Microspheres Market Report Scope

The PMMA microspheres market report includes:

| Light Diffusing Agent |

| Matting Agent |

| Cosmetic Additive |

| Ceramic Porogen |

| Modified Plastic Additive |

| Paints and Inks Additive |

| Other Applications |

| Lifesciences and Medical |

| Personal Care and Cosmetics |

| Electronics |

| Paints and Coatings |

| Plastics |

| Ceramics and Composites |

| Other End-user Industries |

| 0 – 30 µm |

| 30 – 100 µm |

| Greater than 100 µm |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Light Diffusing Agent | |

| Matting Agent | ||

| Cosmetic Additive | ||

| Ceramic Porogen | ||

| Modified Plastic Additive | ||

| Paints and Inks Additive | ||

| Other Applications | ||

| By End-user Industry | Lifesciences and Medical | |

| Personal Care and Cosmetics | ||

| Electronics | ||

| Paints and Coatings | ||

| Plastics | ||

| Ceramics and Composites | ||

| Other End-user Industries | ||

| By Particle Size | 0 – 30 µm | |

| 30 – 100 µm | ||

| Greater than 100 µm | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current PMMA microspheres market size?

The PMMA microspheres market size is valued at USD 504.55 million in 2026 and is forecast to reach USD 808.04 million by 2031.

Which application segment leads the PMMA microspheres market?

Cosmetic Additive applications lead with 34.78% market share in 2025.

Which end-user industry is growing the fastest?

Lifesciences & Medical is advancing at a 12.35% CAGR to 2031, the fastest among all end-user groups.

Why are PMMA microspheres important in LED/LCD displays?

They provide high haze and transmittance, improving brightness uniformity while reducing warpage in backlighting units.

How is regulation affecting PMMA microspheres in cosmetics?

EU Regulation 2023/2055 restricts synthetic microplastics in rinse-off products by 2027 and leave-on products by 2029, redirecting PMMA microspheres toward premium leave-on formulations and prompting development of sustainable alternatives.

What sustainability initiatives exist for PMMA microspheres?

Sumitomo Chemical and Mitsubishi Chemical Group are commercializing chemically recycled PMMA feedstocks, aiming to lower carbon footprints while securing supply stability.

Page last updated on: