Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

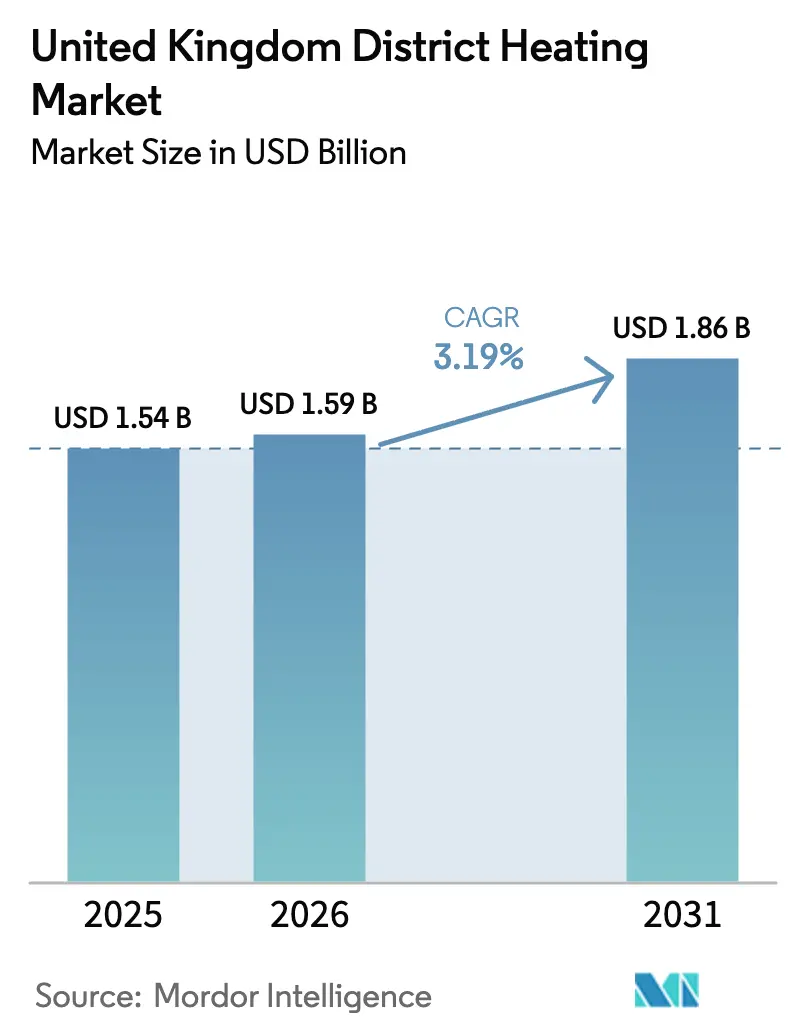

| Base Year Market Size (2025) | USD 1.54 Billion |

| Market Size (2026) | USD 1.59 Billion |

| Market Size (2031) | USD 1.86 Billion |

| Growth Rate (2026 - 2031) | 3.19% CAGR |

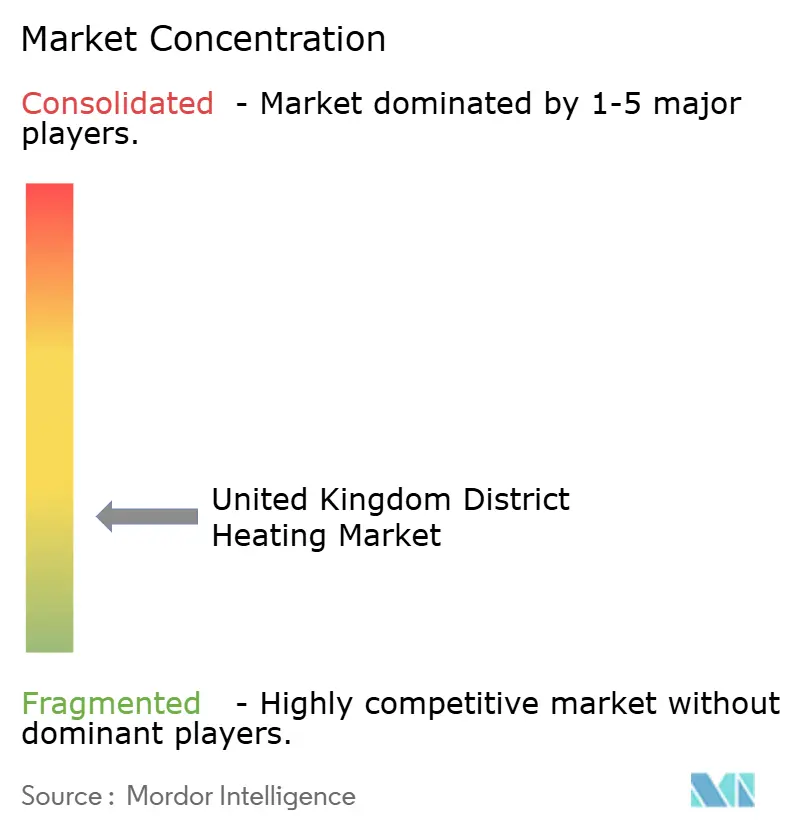

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom District Heating Market Analysis by Mordor Intelligence

The United Kingdom District Heating market size was valued at USD 1.54 billion in 2025 and estimated to grow from USD 1.59 billion in 2026 to reach USD 1.86 billion by 2031, at a CAGR of 3.19% during the forecast period (2026-2031). Steady rollout of statutory heat-network zoning, capital grants that cut project payback to within municipal borrowing limits, and falling costs for large-scale heat pumps together accelerate scheme approvals, especially in England’s urban cores. Developers recalibrate business cases around hybrid energy centers that couple water-source heat pumps with waste-heat offtake, mitigating spark-spread risk while meeting rising carbon-pricing penalties. Price-cap consultations by Ofgem, coupled with mandatory landlord tariff disclosure, temper perceived monopoly risks and nudge occupancy uptake rates higher once dwellings reach handover. Meanwhile, thermal-storage arbitrage in National Grid ESO’s flexibility markets adds a new ancillary-revenue layer that lifts internal rates of return on networks with ≥12 h hot-water pits. Competitive positioning crystallizes around utilities and specialist infrastructure funds able to blend construction and operational guarantees across 25-to-40-year concessions.

Key Report Takeaways

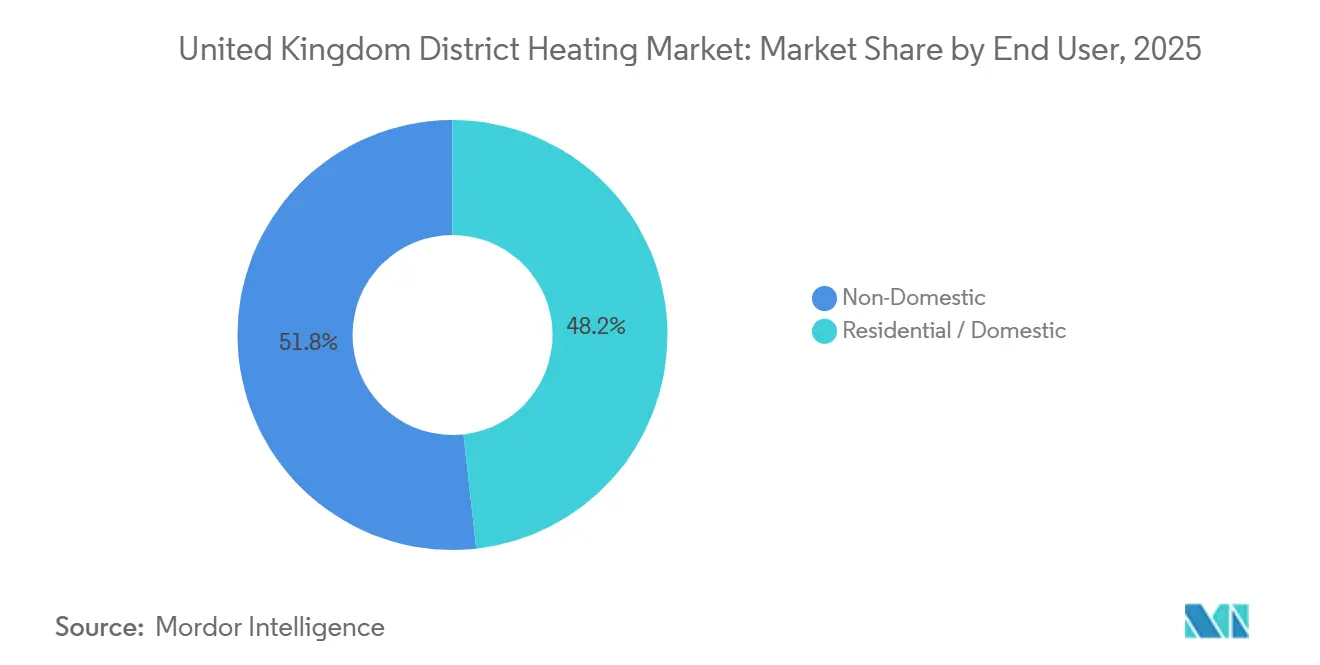

- By end user, residential and domestic applications led with 48.23% of United Kingdom District Heating market share in 2025, while non-domestic use cases are advancing at a 4.24% CAGR through 2031.

- By primary heat source, gas-CHP retained 37.73% share of the United Kingdom District Heating market size in 2025, whereas low-carbon heat-pump and waste-heat solutions are expanding at a 5.12% CAGR.

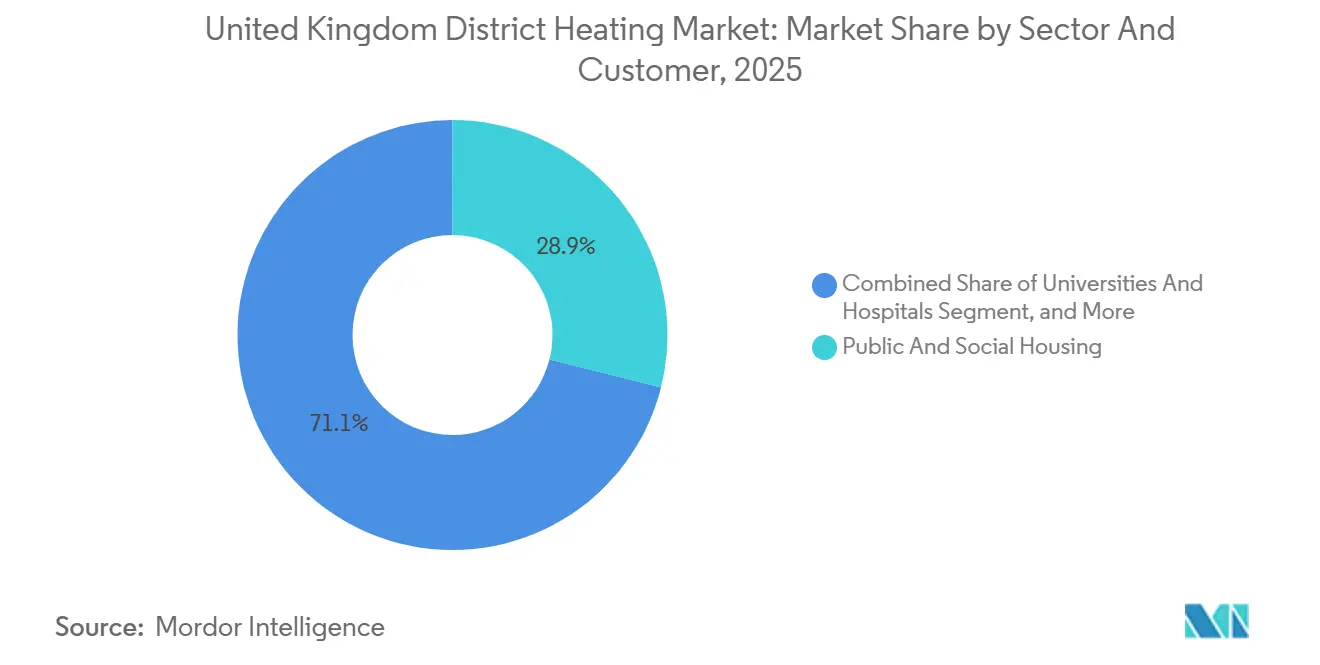

- By sector and customer, public and social housing commanded 28.93% revenue share in 2025; mixed-use regeneration districts are projected to post a 4.86% CAGR to 2031.

- By thermal-storage usage, systems with no integrated storage captured 52.12% of United Kingdom District Heating market share in 2025, and ≥12 h pit or tank storage configurations are growing at a 4.92% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom District Heating Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Statutory Heat-Network Zoning (2025-26) | +0.8% | England and Wales pilot zones in Greater Manchester, Bristol, Cardiff | Short term (≤ 2 years) |

| Green Heat Network Fund and HNES Grants | +0.6% | National, concentration in Scotland and Northern England estates | Medium term (2-4 years) |

| Waste-Heat Capture Mandate from EfW and Sewage Works | +0.4% | Urban centers hosting EfW plants and coastal wastewater facilities | Medium term (2-4 years) |

| Falling Cost of River and Mine-Water Heat Pumps | +0.3% | South Wales, Northeast England, Central Scotland | Long term (≥ 4 years) |

| Mandatory Landlord Tariff Disclosure | +0.2% | National, early enforcement in dense rental markets | Short term (≤ 2 years) |

| Aggregation of Thermal Storage into ESO Flexibility Markets | +0.2% | National grid-connected schemes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Statutory Heat-Network Zoning (2025-26)

Local authorities gained legal powers in 2025-26 to declare zones where new buildings must connect to communal heat or prove equivalent low-carbon alternatives. Councils now map anchor loads such as hospitals and leisure centers, then lock in 25-to-40-year revenue streams that de-risk private investment.[1]Department for Energy Security and Net Zero, “Green Heat Network Fund,” GOV.UK, gov.uk Early adopters like Bristol designated three priority zones covering 12 000 homes, capturing developer contributions through planning agreements. The policy compresses technology-selection cycles, pushing developers toward heat pumps and waste-heat links sooner than carbon targets alone would require. It also accelerates connection density, raising trunk-main utilization above 40% within two years of system launch. However, fragmented land titles and brownfield remediation still slow pipe routing, demanding higher pre-construction contingencies.

Green Heat Network Fund and HNES Grants

The GBP 288 million (USD 391.95 million) Green Heat Network Fund covers up to 50% of capital on low-carbon schemes and pairs with the Heat Network Efficiency Scheme for retrofits. Phase 3 awards in 2024 backed 21 projects totaling 15 000 connections, many anchored by water-source heat pumps. Scotland’s parallel fund offers grants of as much as 70%, effectively neutralizing rural density penalties. Mandatory match-funding favors consortium bids that combine engineering firms with social-housing landlords, sidelining smaller developers lacking balance-sheet depth. Resulting heat-pump adoption lifts renewable fractions above 70% on new networks, while retrofit grants raise seasonal performance factors from 1.8 to beyond 2.5, cutting operating costs by nearly one-third.

Waste-Heat Capture Mandate from EfW and Sewage Works

Since 2024, new energy-from-waste plants and major sewage works must pipe surplus heat to nearby networks or prove technical infeasibility. London’s Edmonton facility now exports 70 MW of low-grade heat, displacing gas for 5 000 homes and trimming carbon intensity 60%. The mandate forces EfW developers to locate near demand clusters, inflating peri-urban land values but embedding long-term offtake contracts into project finance. Sewage-derived heat requires pump-lift to domestic temperatures, adding GBP 800-1 200 per connection, yet industrial estates can accept lower supply temperatures, widening addressable markets. Overall, the rule converts waste heat from by-product to bankable revenue line, nudging IRRs up by 1-2 percentage points on compliant facilities.

Falling Cost of River and Mine-Water Heat Pumps

Standardized modular skids, greater tender competition, and cumulative installed capacity above 50 MW cut delivered capital cost for large water-source systems by roughly 20% between 2023 and 2025. Mine-water schemes achieve seasonal performance factors of 3.5-4.0, beating air-source units by a quarter on electricity consumption. The Coal Authority has pre-characterized 40 sites, slashing feasibility timelines to under nine months. Gateshead’s river-source network illustrates hybrid resilience, pairing a 3 MW water-source heat pump with a 1.5 MW gas-CHP to cover winter extremes. Pension funds now see inflation-linked heat revenues backed by statutory zoning as infrastructure-grade cash flows, broadening the investor base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Front-End CAPEX | -0.5% | Retrofit-dense inner cities nationwide | Short term (≤ 2 years) |

| Gas-Power Price-Spread Volatility | -0.3% | National, especially CHP-reliant schemes | Medium term (2-4 years) |

| Skilled-Labor Shortage in Pipe Welding and HIU Commissioning | -0.2% | Scotland and Northern England | Medium term (2-4 years) |

| Consumer Monopoly Billing Perception | -0.1% | Private rental and leasehold flats nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Front-End CAPEX

District heating demands GBP 2,500-4,500 (USD 3402.37-6124.27)per connection for new builds and more for retrofits, far above individual boiler installs. Road excavation in congested streets consumes up to half of budgets and can run GBP 150-250 (USD 201.44-335.74) per meter in central London.[2]Transport for London, “Road Closures and Permits,” tfl.gov.uk Social landlords face borrowing caps under PWLB rules, pushing them toward schemes with sub-15-year paybacks or blended UK Infrastructure Bank loans. Steel pipe inflation of 18% in 2024 and nine-month compressor lead times squeeze contingencies, occasionally flipping projects negative before first heat flows. Consequently, only sponsors with deep capital reserves or grant-backed models proceed at scale.

Gas-Power Price-Spread Volatility

Gas-fired CHP relies on a spark spread between fuel and power prices that narrowed to GBP 12 per MWh in late 2024, down from GBP 25 (USD 33.57) two years earlier. Operators lacking long-term PPAs face six-figure monthly cash-flow swings on 5 MW units. Heat-pump adoption eases gas exposure but heightens electricity risk, particularly during peak-tariff windows. Networks with ≥4 h of storage can offer demand-response services, yet telemetry upgrades cost GBP 100 000-200 000 (USD 134 294.50 - 268 589), a sum prohibitive for smaller schemes. Until spark spreads stabilize or flexibility revenue scales, financiers demand higher debt-coverage ratios, dampening rollout speed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Residential Load Density Lifts Bankability

Residential applications claimed 48.23% United Kingdom District Heating market share in 2025, reflecting zoning directives that prioritize household connections. Social landlords prefer 40-to-50-year asset horizons that dovetail with concession terms, while match-funded grants cut capital outlay. Victorian-era retrofit streets require sequential envelope upgrades and careful HIU phasing to avoid oversizing, yet once networked, nightly baseload smooths demand variance. Non-domestic buildings confront split-incentive obstacles, as landlords shoulder capex yet tenants capture savings, limiting uptake unless green-lease clauses compel participation. Universities and hospitals, however, supply 24/7 anchor loads that keep trunk pipes above 60% utilization. Corporate ESG mandates spur office conversions, but lease churn still trims certainty. Overall growth tilts residential because statutory join-up rules and GHNF scoring criteria both weight heavily toward housing volume.

Persistent residential dominance springs from longer asset cycles, home networks run 50 years, versus 25-30 years in commercial portfolios, and Part L regulations lowered design supply temperatures to 60 °C, favoring heat-pump solutions. Mixed-use districts blend daytime commercial loads with evening residential peaks, driving utilization toward 70% and trimming levelized cost by a fifth. Where anchor education or health campuses sign multi-decade offtake contracts, lenders treat revenue as quasi-sovereign, tightening debt spreads and releasing equity for further phases. Non-domestic growth should accelerate once revised landlord disclosure rules make cost pass-through transparent, but until then housing leads new connection counts.

By Primary Heat Source: Electrification Surpasses Legacy CHP

Gas-CHP retained 37.73% share of the 2025 mix, yet carbon pricing and compressed spark spreads now erode margins. The United Kingdom District Heating market size tied to low-carbon heat-pump and waste-heat inputs is rising at a 5.12% CAGR, underwritten by 50% GHNF grants and EfW heat-supply mandates. Installed cost for water-source heat pumps has fallen to GBP 400-600 per kWth, closing parity with CHP when ETS passes GBP 80 t⁻¹ CO₂. Biomass and biogas CHP fill rural gaps but face feedstock uncertainty and tighter air-quality permits. Hybrid plants that sequence heat pumps first, then top with backup gas or biomass, now dominate tender specifications, limiting fossil runtime to peak-cold hours.

As electrification deepens, operators deploy smart controls to switch between tariff-linked dispatch modes, selling surplus power or drawing off-peak electrons to charge thermal tanks. Networks with a renewable heat fraction above 70% qualify for preferential municipal green-bond rates, cutting financing costs by 50-75 basis points. Carbon-price escalation under the UK ETS squeezes residual gas-CHP viability to locations with reliable capacity-market payments of GBP 45 000-75 000 MW⁻¹ yr⁻¹. Consequently, low-carbon generation’s share is forecast to exceed 55% by 2031, relegating CHP to resilience duty only.

By Sector and Customer: Social Housing Anchors Yield

Public and social housing captured 28.93% United Kingdom District Heating market revenue in 2025 owing to centralized ownership that eliminates tenant-landlord frictions. Regulatory pressure to reach EPC Band C by 2030 funnels capital toward heat networks as a bulk compliance route. Mixed-use regeneration areas, though smaller today, grow at 4.86% CAGR because they allocate evening, retail, and office loads onto one backbone, lifting annual capacity factors above 65%. Universities and hospitals line up 20-year indexed offtake contracts that support asset-backed debt structures, while retail parks lag due to short 5-10 year leases that mismatch with 30-year concessions.

Housing associations monetize service charges to recover heat costs, protecting cash flow even under tariff caps. Combined with GHNF coverage, their projects often clear investment hurdles at sub-5% unlevered IRRs, enticing pension-fund equity. Regeneration zones leverage Section 106 agreements to compel developers into pre-installed pipe sleeves, avoiding retrofit premiums. University campuses increasingly outsource energy centers via design-build-operate contracts that push performance risk onto specialists but guarantee the university no-fault supply. Retail parks may see acceleration once reversible heat pumps add cooling, broadening seasonal revenue opportunities.

By Thermal-Storage Usage: Flexibility-Linked Economics Emerge

Networks without integrated storage still hold 52.12% United Kingdom District Heating market share, a legacy of CHP-centric design that matched production to near-constant baseload. Yet ≥12 h pit or tank systems are expanding at 4.92% CAGR as operators target time-of-use arbitrage spreads of GBP 100-200 MWh⁻¹ between night valleys and evening peaks. Short-duration 2-4 h tanks flatten morning demand spikes, lifting heat-pump performance factors by up to 0.3. Long-duration pits allow inter-day storage powered by surplus wind, slashing carbon intensity 30-40% and earning flexibility payments of GBP 20-50 MW⁻¹ h⁻¹.

Retrofit addition remains costly often GBP 0.5 million (USD 0.67 million) for a 500-connection scheme because space constraints and structural load bearers limit tank size. Where planning allows subsurface excavation, gravel-water pits of 1 000-5 000 m³ achieve marginal costs below GBP 70 kWh⁻¹, but groundwater contamination controls can prolong permitting. New builds in Scotland and Northern England now design seasonal pits in from day one, banking summer solar or EfW waste heat for winter. As ESO market rules mature, storage revenue predictability should tighten, unlocking cheaper project-finance debt and pushing overall storage penetration toward parity with non-storage schemes by 2031.

Geography Analysis

England dominated with 69.13% United Kingdom District Heating market share in 2025, propelled by London’s half-million connected dwellings and Greater Manchester’s zoning rollout. Dense building stock above 100 dwellings ha⁻¹ supports heat-demand density over 3 GWh km⁻¹, critical for trunk-main economics. Section 106 planning contributions streamline scheme funding, but legacy pipe corrosion in pre-2000 assets inflates OPEX and replacement capex, creating acquisition discounts of 20-30% against book value. Regional hubs like Birmingham and Leeds trail London by 12-24 months because of fragmented landholdings that slow consent. Nonetheless, pipeline projects tied to mixed-use regeneration will add at least 25 000 new English connections by 2028.

Scotland posts the fastest growth at a 5.12% CAGR, supported by a GBP 300 million (USD 402.88 million) devolved Heat Network Fund that grants up to 70% of capex in rural or island settings.[3]Scottish Government, “Local Heat and Energy Efficiency Strategies,” gov.scot Lower zoning thresholds of 2 GWh km⁻¹ broaden eligibility to smaller towns such as Inverness and Dumfries. Edinburgh’s Granton Waterfront, anchored by a 10 MW water-source heat pump, demonstrates scale in coastal pump applications, while Glasgow integrates a 2 MW mine-water unit beneath its social-housing estate, cutting household bills by GBP 150-200 yr⁻¹. Scotland’s lower urban land prices and shorter consent cycles encourage early-stage investors, though skilled-labor competition with offshore-wind fabrication yards can extend construction timelines.

Wales and Northern Ireland remain niche, holding mid-single-digit combined share, yet councils are leveraging mine-water and river-source feasibility grants under the Welsh Local Energy Programme. Cardiff’s Central Quay uses a 3 MW pump from Cardiff Bay to supply 1 000 waterfront homes, achieving an 80% renewable heat fraction. Northern Ireland’s Titanic Quarter biomass-CHP illustrates biomass reliance where grid gas is sparse, but feedstock constraints and air-quality permits cap scalability. Both regions depend on securing GHNF awards and preparing Local Heat and Energy Efficiency Strategies, tasks that demand GBP 0.1-0.2 million (USD 0.13-0.27 million) consultancy budgets that smaller councils must fund.

Competitive Landscape

The sector shows moderate concentration the top 10 operators managing about a major share of installed capacity, producing a market concentration score of 6. Large utilities and infrastructure funds leverage balance-sheet depth to lock in 25-to-40-year concessions, often acquiring mature schemes for inflation-linked cash flows. Specialist developers favor greenfield opportunities in zoning areas, winning bids by offering modular, factory-built energy centers that cut on-site assembly to six months. Smaller entrants often partner with heat-pump manufacturers, exchanging lower capital cost for outsourced maintenance, which trims margins.

Digital capability differentiates contenders. Operators investing in real-time SCADA, predictive maintenance, and dispatch algorithms monetize thermal storage through ESO flexibility markets, harvesting GBP 20-50 MW⁻¹ h⁻¹ that boosts IRR 1-2 points. Patent activity in variable-speed HIUs underlines a shift toward performance-based contracts that cap customer bills within ±5% of forecast, transferring efficiency risk from tenants to concessionaires. Regulatory overhead is rising; Ofgem’s draft price-cap rules could add GBP 0.05 MWh⁻¹ compliance cost, favoring operators with in-house legal and data teams.[4]Ofgem, “Heat Network Regulation Consultation,” ofgem.gov.uk

Consolidation is likely. Mid-tier players with 5 000-15 000 connections may either scale via M and A or exit at 1.5-2.0× revenue multiples, especially if they control exclusive waste-heat offtakes. Utilities pursuing geographic diversification have already paid premiums as seen in Veolia’s 2025 acquisition in Greater Manchester to secure EfW integration synergies. Skill shortages in pipe welders and HIU technicians elongate build programs by three-to-six months, so leading EPCs now pre-qualify subcontract rosters and pledge apprenticeship quotas in bids to de-risk delivery schedules.

United Kingdom District Heating Industry Leaders

Vital Energi Utilities Ltd

1 Energy Group Limited

Baxi Heating UK

Ramboll UK Limited

Veolia Environnement SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: ThamesWey Energy received a GBP 1.2 million (USD 1.61 million) Heat Network Efficiency Scheme grant to retrofit variable-speed pumps across its Woking network, targeting a 20% electricity reduction.

- January 2026: SSE Heat Networks committed GBP 45 million (USD 60.43 million) to extend Edinburgh’s scheme by 2,500 connections with a 6 MW water-source heat pump, co-funded by the Scottish Heat Network Fund.

- December 2025: Vital Energi won a 25-year, GBP 38 million (USD 51.03 million) concession for Bristol’s Temple Quarter, deploying a 5 MW river-source heat pump and 800 m³ storage.

- October 2025: E.ON and Kensa Utilities launched a GBP 28 million (USD 38.11 million) ground-source network for 1 800 Swansea social-housing homes, backed by a GBP 14 million (USD 19.05 million) GHNF grant.

United Kingdom District Heating Market Report Scope

District heating is the process of distributing heat in the form of hot water or steam through a network of insulated pipes from a centralized location to end users such as residential, commercial, or industrial.

The United Kingdom District Heating Market Report is Segmented by End User (Residential/Domestic, Non-Domestic), Primary Heat Source (Gas-CHP, Low-Carbon HP and Waste-Heat, Biomass/Biogas, Other Back-Up), Sector and Customer (Mixed-Use Regeneration Districts, Public and Social Housing, Universities and Hospitals, Commercial/Retail Parks), Thermal-Storage Usage (No Integrated Storage, ≥2 h Hot-Water Tanks, ≥12 h Pit/Tank Storage), and Geography (England, Scotland, Wales, Northern Ireland). The Market Forecasts are Provided in Terms of Value (USD).

By End User

| Residential / Domestic |

| Non-Domestic |

By Primary Heat Source

| Gas-CHP |

| Low-Carbon HP And Waste-Heat |

| Biomass / Biogas |

| Other Primary Heat Sources |

By Sector And Customer

| Mixed-Use Regeneration Districts |

| Public And Social Housing |

| Universities And Hospitals |

| Commercial / Retail Parks |

By Thermal-Storage Usage

| No Integrated Storage |

| ≥2 h Hot-Water Tanks |

| ≥12 h Pit / Tank Storage |

| By End User | Residential / Domestic |

| Non-Domestic | |

| By Primary Heat Source | Gas-CHP |

| Low-Carbon HP And Waste-Heat | |

| Biomass / Biogas | |

| Other Primary Heat Sources | |

| By Sector And Customer | Mixed-Use Regeneration Districts |

| Public And Social Housing | |

| Universities And Hospitals | |

| Commercial / Retail Parks | |

| By Thermal-Storage Usage | No Integrated Storage |

| ≥2 h Hot-Water Tanks | |

| ≥12 h Pit / Tank Storage |

Key Questions Answered in the Report

How large is the United Kingdom District Heating market today and where is it heading?

United Kingdom District Heating market size stands at USD 1.59 billion in 2026 and is forecast to reach USD 1.86 billion by 2031 at a 3.19% CAGR.

Which end-user segment grows fastest within district heating schemes?

Residential and domestic applications, already at 48.23% share in 2025, expand at a 4.24% CAGR through 2031 as zoning mandates and social-housing grants front-load connections.

Why are low-carbon heat pumps overtaking gas-CHP in new projects?

GHNF grants cover up to half of capital cost, carbon prices rise under the UK ETS, and water-source heat-pump capex has fallen 20%, making them cost-competitive while avoiding spark-spread volatility.

What role does thermal storage play in network economics?

≥12 h pit or tank systems let operators buy cheap overnight electricity and sell heat at peak, while also earning GBP 20-50 MW⁻¹ h⁻¹ from ESO flexibility markets, lifting project IRRs 1-2 points.

Which UK region is growing fastest for district heating?

Scotland leads with a 5.12% CAGR to 2031, supported by a generous 70% capital-grant regime and lower zoning thresholds that bring smaller towns into scope.

How is regulation addressing consumer protection in heat networks?

Ofgem is consulting on extending price-cap rules and mandating landlord tariff disclosure, measures aimed at curbing monopoly pricing concerns and improving billing transparency.

Page last updated on: