Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

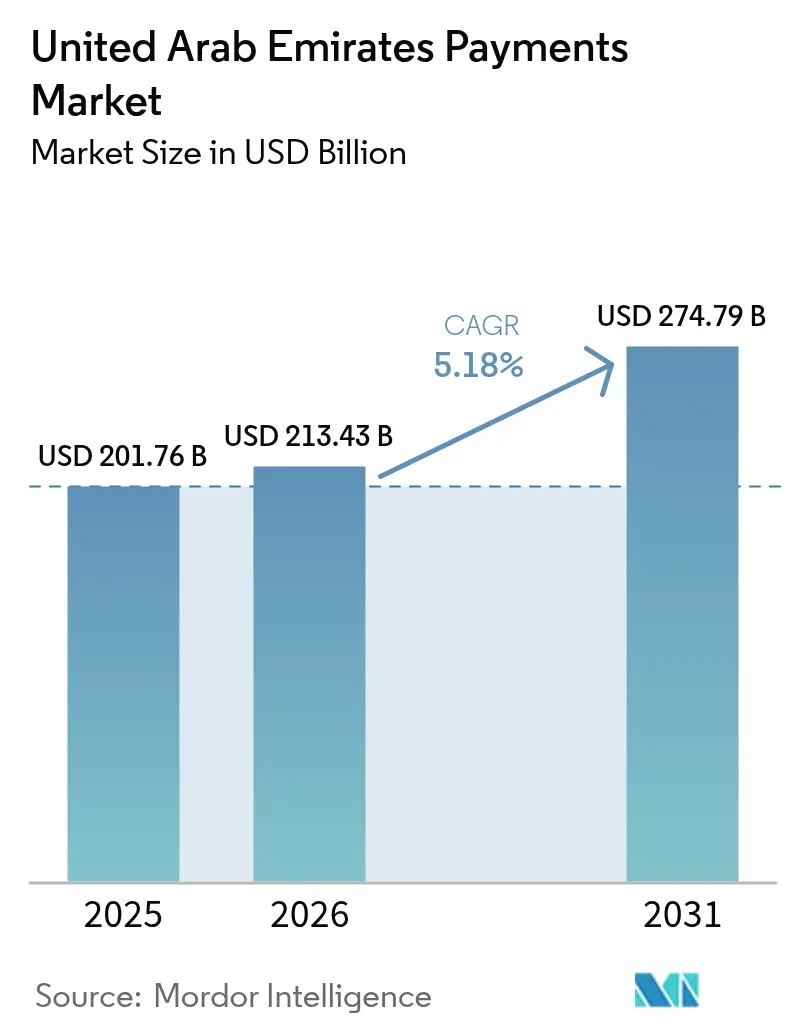

| Base Year Market Size (2025) | USD 201.76 Billion |

| Market Size (2026) | USD 213.43 Billion |

| Market Size (2031) | USD 274.79 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

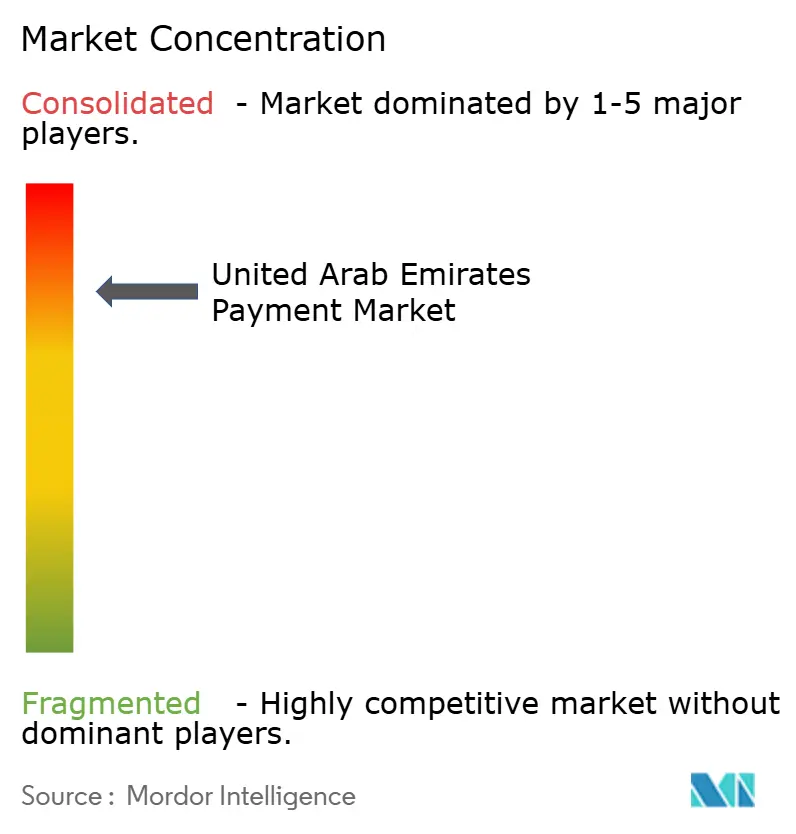

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Payments Market Analysis by Mordor Intelligence

The United Arab Emirates payments market size was valued at USD 201.76 billion in 2025 and is estimated to grow from USD 213.43 billion in 2026 to reach USD 274.79 billion by 2031, at a CAGR of 5.18% during the forecast period (2026-2031). Rising migration from legacy card rails to sovereign infrastructure, accelerated issuance of Jaywan-branded cards, and early-stage Digital Dirham pilots are reshaping retail checkout, invoice settlement, and cross-border spending patterns. Near-ubiquitous contactless acceptance, real-time AANI transfers, and QR interoperability with India’s UPI are lowering friction for both tourists and residents, while stringent data-residency mandates are forcing cloud processors to deploy in-country nodes, lifting fixed costs yet improving sovereign control. Incumbent acquirers continue to dominate physical commerce, but global platforms licensed in 2025 are pressuring pricing in e-commerce, which remains the fastest-growing channel. Heightened cyber-fraud targeting hospitality point-of-sale environments is simultaneously driving tokenization and biometric rollouts, albeit compressing margins for smaller providers.

Key Report Takeaways

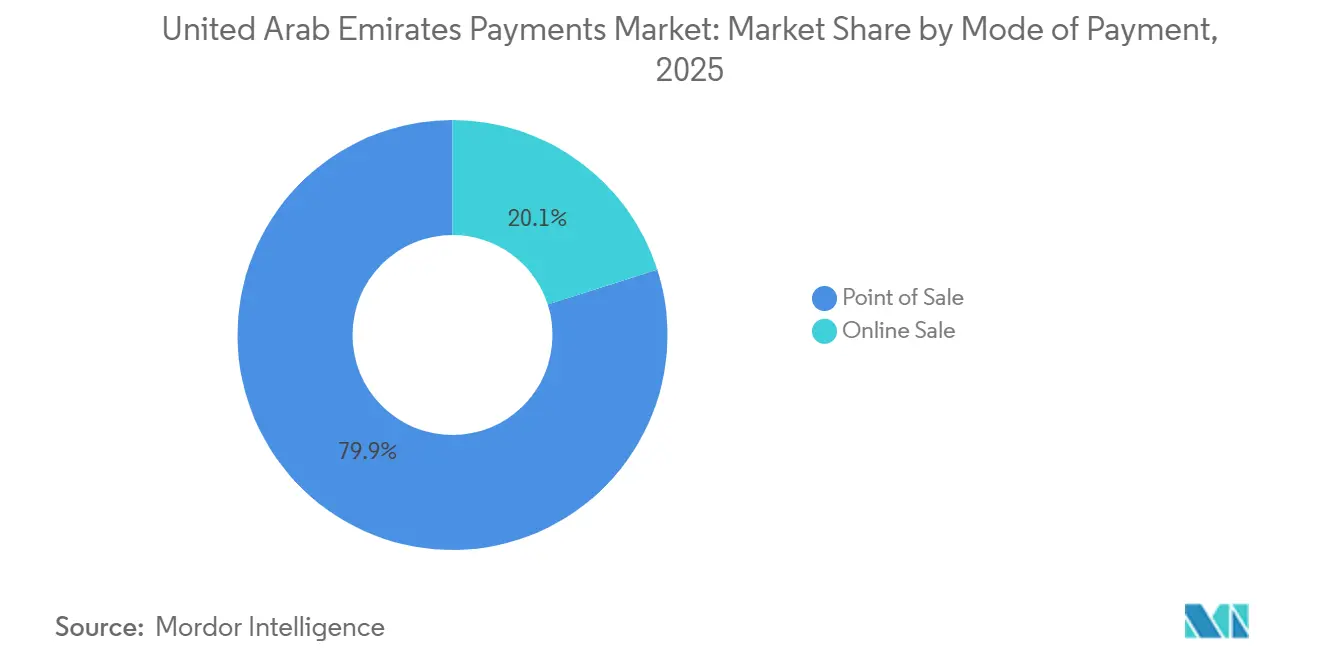

- By mode of payment, point-of-sale transactions held 79.92% of the United Arab Emirates payments market share in 2025, while online channels are projected to expand at a 6.37% CAGR through 2031.

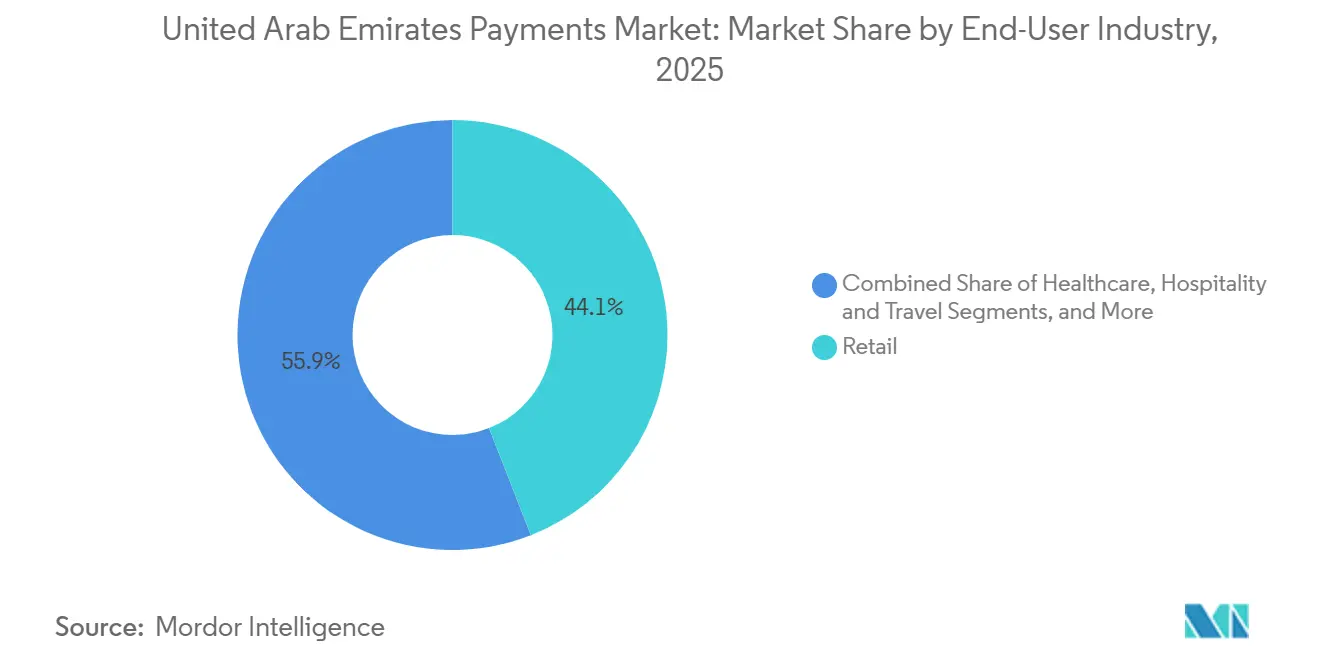

- By end-user industry, retail accounted for 44.06% share of the United Arab Emirates payments market size in 2025, whereas entertainment and digital content is poised to grow at a 5.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domestic Card-Scheme “Jaywan” Routing Keeps Interchange In-Country | +1.2% | National, early adoption in Dubai and Abu Dhabi | Medium term (2-4 years) |

| AANI Real-Time Rail Unlocks SME Instant Settlement and Bill-Pay | +1.0% | National, concentrated in Dubai, Abu Dhabi, Sharjah | Short term (≤ 2 years) |

| Tourist-Driven Cross-Border QR (UPI, RuPay) Traffic Surge | +0.9% | Dubai, Abu Dhabi, Sharjah (high tourist zones) | Short term (≤ 2 years) |

| CBDC “Digital Dirham” Lowers Cash-Handling Cost for Banks | +0.8% | National, pilot phase in Abu Dhabi and Dubai | Long term (≥ 4 years) |

| BNPL at POS Boosts High-Ticket Retail Conversion | +0.7% | Dubai, Abu Dhabi (premium retail corridors) | Medium term (2-4 years) |

| Open-Finance API Mandates Accelerate Fintech Product Launches | +0.6% | National, regulatory framework led by Central Bank | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Domestic Card-Scheme “Jaywan” Routing Keeps Interchange In-Country

Jaywan, introduced in 2024, reroutes domestic card traffic away from global networks and retains interchange inside the banking system, trimming acquirer costs by roughly 30-40 basis points per swipe.[1]Central Bank of the UAE, “Digital Dirham Pilot Launch and AANI Instant Payment Platform,” centralbank.ae By mid-2025 the scheme enrolled 12 banks and 8 million cardholders, with acceptance at 95% of terminals nationwide. Merchants see lower merchant-discount rates on local volume, funding faster device upgrades and nudging cash-heavy segments toward digital receipts. Co-badging with Visa and Mastercard protects cross-border acceptance, ensuring travelers retain spend flexibility. Mandatory inclusion of Jaywan on all new cards by 2027 compresses migration timelines and accelerates terminal replacement cycles.[2]Emirates NBD, “UnionPay QR Integration and Jaywan Card Issuance,” emiratesnbd.com

AANI Real-Time Rail Unlocks SME Instant Settlement and Bill-Pay

Operational since 2024, AANI clears payments under 10 seconds and had 1.4 million users executing 500,000 transactions daily by December 2025. Liquidity caps at AED 100,000 (USD 27,200) limit systemic risk yet satisfy 90% of SME invoices. Dubai’s licensing portal now embeds AANI, meaning entrepreneurs receive trade licenses within minutes after fee payment.[3]Dubai Department of Economy and Tourism, “AANI Integration in Business Licensing Portal,” dubaidet.ae Large utilities such as DEWA collect bills in real time, cutting reconciliation cycles and surfacing dynamic-pricing alerts to consumers. Fintechs access open APIs, embedding instant pay-by-link features into accounting software; Mashreqbank’s NEOPAY processed 320,000 such checkouts in its first three months.

Tourist-driven cross-border QR payments capture visitor spend

Network International enabled UPI QR codes at 150,000 merchants by December 2025, capturing spend from 3.5 million Indian tourists. Shoppers bypass currency-conversion fees, lifting purchase frequency 18% at Dubai Mall and Yas Island.[4]National Payments Corporation of India, “Cross-Border UPI Integration with UAE,” npci.org.in Settlement clears in dirhams via pre-funded pools, delivering funds within 24 hours. Emirates NBD replicated the model for UnionPay QR to serve 1.2 million Chinese visitors. Bilateral QR pacts with Saudi Arabia, Egypt, and Pakistan under the Central Bank’s 2025 road map position the United Arab Emirates payment market as a regional hub.

Digital Dirham CBDC reduces cash-handling overheads

A wholesale Digital Dirham pilot launched in Q4 2025 reduced interbank settlement from hours to seconds while eliminating correspondent fees. First Abu Dhabi Bank posted 40% cost savings on cross-border trade-finance transactions settled on the ledger. A retail pilot scheduled for mid-2026 in Masdar City will test programmable wallets for transit and utilities. Automated escrow functions could streamline real-estate deals, while conditional tax-withholding features offer fiscal transparency. Banks expect 20-25% lower cash-handling overhead as adoption scales, freeing staff for advisory services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ATM-Level Cash Preference in Rural Northern Emirates Persists | -0.5% | Ajman, Umm Al Quwain, Ras Al Khaimah, Fujairah | Long term (≥ 4 years) |

| Cyber-Fraud Rings Targeting Hospitality POS Increase Acquirer Risk | -0.4% | Dubai, Abu Dhabi (hospitality corridors) | Short term (≤ 2 years) |

| High MDR for Foreign Cards Suppresses SME Acceptance Growth | -0.3% | National, acute in Sharjah and Northern Emirates | Medium term (2-4 years) |

| Data-Residency Rules Raise Cloud-Cost Base for PSPs | -0.3% | National, enforcement by ADGM and DIFC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ATM-Level Cash Preference in Rural Northern Emirates Persists

ATM withdrawals in Ajman, Umm Al Quwain, Ras Al Khaimah, and Fujairah remain 40-50% higher than Dubai averages, reflecting sparse terminal density and cultural leanings toward cash for purchases under AED 50 (USD 13.6). A 2024 survey showed 62% of merchants lacked card readers because monthly fees erode slim grocery and fuel margins. Patchy mobile coverage in mountainous zones hampers QR and NFC uptake. Although a 2025 subsidy program waives device fees for a year, consumer mistrust and limited digital awareness slow conversion. Cross-border remittance workers also reinforce cash ecosystems by favoring exchange houses over e-wallets.

Cyber-Fraud Rings Targeting Hospitality POS Increase Acquirer Risk

Card-skimming and malware incidents in hotel and restaurant terminals climbed 35% in 2025, exploiting high staff turnover and tourist card volumes. Chargebacks at Network International’s hospitality merchants rose 22%, prompting a rapid shift to point-to-point encryption and tokenization across 18,000 devices. PCI-DSS v4.0 demands annual penetration testing and multi-factor authentication, costs that smaller acquirers struggle to absorb. Real-time breach reporting, mandated by the Central Bank in June 2025, carries fines up to AED 1 million (USD 0.27 million) for non-compliance. The resulting compliance burden tightens margins even as biometric authentication improves traveler confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Physical Rails Dominate, Yet Online Surges From a Smaller Base

Point-of-sale transactions controlled 79.92% of 2025 value in the United Arab Emirates payments market, supported by 92% NFC-enabled terminal coverage and contactless card penetration of 87%. The United Arab Emirates payments market size booked to online channels remains smaller but is expanding at a 6.37% CAGR on the back of wallet tokenization, one-click checkout, and AANI account-to-account links. Debit and credit cards still anchor in-store spend, yet buy-now-pay-later plans offered by Tabby and Tamara are diverting electronics and furniture receipts away from revolving credit, compressing interest revenue for issuers.[5]Tabby, “Tabby Raises USD 200 Million Series D,” tabby.ai

Digital wallets held 12% of in-store value in 2025, a share expected to climb as Payit, eWallet, and super-apps embed loyalty points and utility bill-pay inside single screens. Online‐only penetration is deeper: roughly 35% of e-commerce orders now close with wallet credentials instead of manual card entry, trimming checkout abandonment rates. Cash-on-delivery has fallen to 18% of parcels, partly because couriers levy fees for cash handling and partly due to merchant discounts on prepaid orders. High-ticket web purchases such as automobiles and jewelry increasingly settle via AANI transfers that dodge credit-card limits and currency-conversion surcharges, signaling a gradual tilt toward direct account debits in the United Arab Emirates payments market.

By End-User Industry: Retail Commands Volume, Entertainment Accelerates

Retail delivered 44.06% of 2025 transaction value, reflecting 70 shopping malls in Dubai and a tourist retail spend topping USD 30 billion in 2024. Nevertheless, the segment is maturing as shop floors already support near-universal contactless acceptance, pushing acquirers to differentiate on loyalty analytics and real-time fraud scoring. In contrast, entertainment and digital content is registering the fastest clip at a 5.89% CAGR, fueled by subscription streaming and in-game micro-transactions that leverage carrier billing to bypass app-store fees.

Healthcare payments are pivoting from cash counters to embedded insurance adjudication; telemedicine claims now reconcile in 48 hours after mandatory EHR integration. Government and utilities crossed the 98% digital-collection threshold in 2025, chiefly due to DEWA’s AANI integration, which cut reconciliation lags and eliminated AED 12 million in annual cash overhead. Hospitality and travel benefit from high tourist footfall but shoulder elevated chargeback and compliance costs, underscoring the need for biometric-first checkouts across the United Arab Emirates payments market.

Geography Analysis

Dubai and Abu Dhabi anchor investment and innovation, yet their regulatory hues diverge. Dubai’s DIFC sandbox licensed 15 new payment service providers in 2025, drawing Stripe, Checkout.com, and other API-first processors aiming to shave cross-border fees for e-commerce merchants. Tourist inflows amplify QR acceptance, with Network International activating UPI codes on 150,000 terminals, a maneuver that aligns the United Arab Emirates payments market with rupee-linked wallets. Abu Dhabi’s ADGM imposes tight data-residency rules, requiring in-country cloud nodes; the policy raises capex yet attracts corporates that value sovereign oversight.

Sharjah leverages municipal subsidies that waive device rental for micro-retailers but still grapples with high interchange on foreign cards, sustaining a price gap between domestic Jaywan volume and overseas tourist spend. Spillover from Dubai’s terminal network is visible, yet migrant workers in Sharjah tilt toward remittance-heavy cash ecosystems that slow wallet adoption. The Northern Emirates record ATM-to-digital ratios 50% above national averages, complicated by mountainous coverage gaps and legacy cash habits.

Financial-inclusion incentives launched in 2025 subsidize terminals and mandate zero monthly fees for micro-merchants, yet uptake is patchy outside urban cores. Consumer education campaigns now pair QR how-to videos with village-level merchant roadshows, a tactic intended to curb cash leakage and pull the Northern Emirates into the mainstream of the United Arab Emirates payments market.

Competitive Landscape

The United Arab Emirates payments market remains moderately concentrated: Network International, First Abu Dhabi Bank, and Emirates NBD process roughly 55-60% of acquiring volume, yet that grip is easing as licensed newcomers nibble at e-commerce lanes. Network International banks on scale, rolling out tokenization, biometric authentication, and UPI QR codes across 150,000 points of sale. Emirates NBD mirrors the strategy with UnionPay QR for Chinese tourists. First Abu Dhabi Bank, meanwhile, uses Digital Dirham pilots to seed long-term wholesale relationships.

Stripe, Checkout.com, and PayPal have entered with transparent pricing and developer-friendly SDKs, quickly onboarding SMEs that previously balked at opaque acquirer tariffs. Regional specialists Telr and PayBy differentiate through vertical modules bundling inventory management, loyalty, and financing, easing adoption hurdles for hospitality and groceries. Buy-now-pay-later leaders Tabby and Tamara processed USD 7 billion in gross merchandise value by mid-2025, converting credit-averse millennials and widening installment footprints to fashion and travel.

Emerging contenders include embedded-finance orchestrators such as M2P Fintech, which powers payroll cards for migrant workers through NowMoney. Super-apps Careem Pay and Talabat Pay weave ride-hailing, food delivery, and bill-pay into one experience, tightening user stickiness. The Central Bank’s upcoming open-banking mandate, slated for 2027, will allow account-to-account initiation, spurring direct debit models that could erode interchange further.

United Arab Emirates Payments Industry Leaders

Network International Holdings plc

First Abu Dhabi Bank PJSC

Emirates NBD Bank PJSC

Mashreqbank PSC

Checkout FZ-LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: First Abu Dhabi Bank expanded its wholesale Digital Dirham pilot to Saudi trade finance, settling 47 transactions worth AED 280 million (USD 76.2 million).

- December 2025: Network International completed UPI QR rollout at 150,000 merchants, processing 2.1 million transactions worth AED 420 million (USD 114.4 million).

- November 2025: Tabby secured USD 200 million in Series D funding at a USD 1.5 billion valuation to fuel regional expansion.

- October 2025: The Central Bank of the UAE launched the wholesale Digital Dirham pilot with First Abu Dhabi Bank and Abu Dhabi Commercial Bank.

United Arab Emirates Payments Market Report Scope

Payment is the transfer of money and goods in exchange for goods and services that the involved parties agree upon. Payment can be made in the form of services exchanged, cash, wire transfer, cheque, credit card, and debit card.

The United Arab Emirates Payments Market Report is Segmented by Mode of Payment (Point-of-Sale including Card Payments with Debit and Credit Cards, Bank Financing, Prepaid Cards, Digital Wallets, Other Point of Sale; Online Sale including Card Payments with Debit and Credit Cards, Bank Financing, Prepaid Cards, Digital Wallets, Other Online Sales), End-User Industry (Retail, Entertainment and Digital Content, Healthcare, Hospitality and Travel, Government and Utilities, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Mode of Payment

| Point-of-Sale (POS) | Card Payments | Debit Cards |

| Credit Cards | ||

| Bank Financing Prepaid Cards | ||

| Digital Wallets (includes Mobile Wallet) | ||

| Other Point of Sale | ||

| Online Sale | Card Payments | Debit Cards |

| Credit Cards | ||

| Bank Financing Prepaid Cards | ||

| Digital Wallets | ||

| Other Online Sales (includes Cash on Delivery, Bank Transfer, and Buy Now Pay Later) |

By End-User Industry

| Retail |

| Entertainment and Digital Content |

| Healthcare |

| Hospitality and Travel |

| Government and Utilities |

| Other End-User Industries |

| By Mode of Payment | Point-of-Sale (POS) | Card Payments | Debit Cards |

| Credit Cards | |||

| Bank Financing Prepaid Cards | |||

| Digital Wallets (includes Mobile Wallet) | |||

| Other Point of Sale | |||

| Online Sale | Card Payments | Debit Cards | |

| Credit Cards | |||

| Bank Financing Prepaid Cards | |||

| Digital Wallets | |||

| Other Online Sales (includes Cash on Delivery, Bank Transfer, and Buy Now Pay Later) | |||

| By End-User Industry | Retail | ||

| Entertainment and Digital Content | |||

| Healthcare | |||

| Hospitality and Travel | |||

| Government and Utilities | |||

| Other End-User Industries | |||

Key Questions Answered in the Report

What is the projected value of the United Arab Emirates payments market by 2031?

It is expected to reach USD 274.79 billion, rising at a 5.18% CAGR between 2026 and 2031.

Which payment mode currently owns the largest share of transactions?

Point-of-sale cards command 79.92% of 2025 value, helped by 92% NFC-enabled terminal coverage.

Which end-user sector is expanding fastest?

Entertainment and digital content is forecast to advance at a 5.89% CAGR through 2031.

How is the Digital Dirham expected to change settlement costs?

Wholesale pilots indicate a 40% cut in interbank settlement expenses and faster transaction finality.

Why do Northern Emirates still rely heavily on cash?

Sparse terminal coverage, cultural preferences, and limited mobile connectivity keep ATM withdrawals elevated.

What role does AANI play for small businesses?

It allows 24/7 instant settlements under 10 seconds, reducing working-capital lock-ups for SMEs.

Page last updated on: