Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

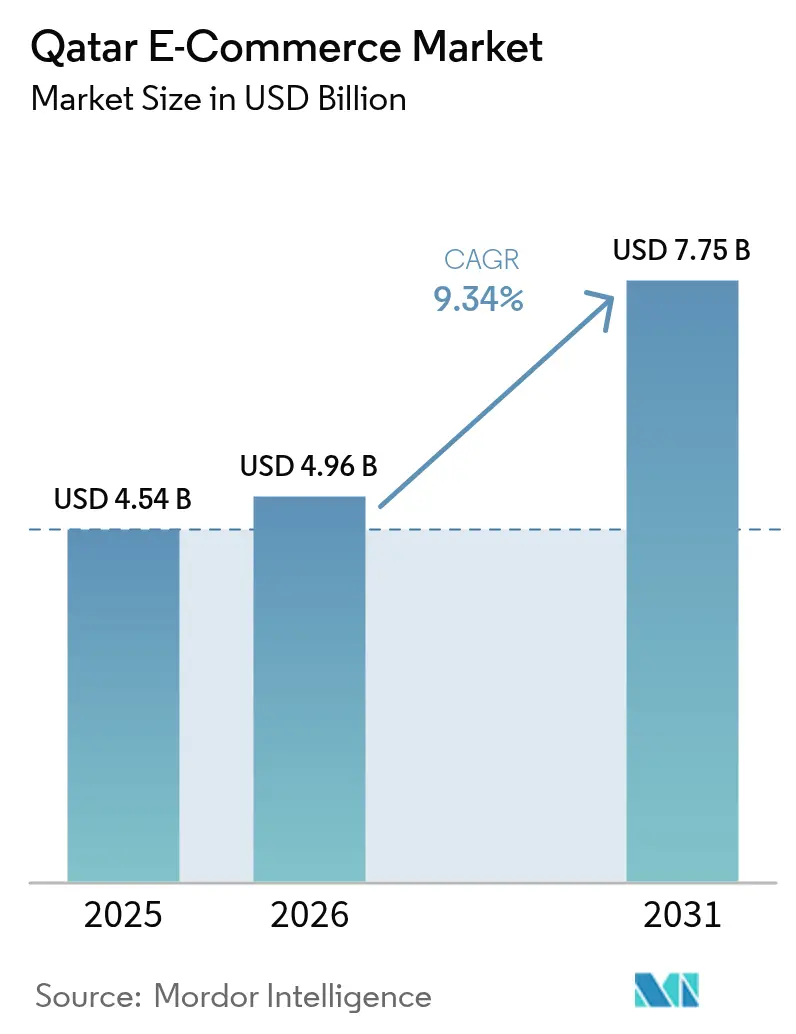

| Base Year Market Size (2025) | USD 4.54 Billion |

| Market Size (2026) | USD 4.96 Billion |

| Market Size (2031) | USD 7.75 Billion |

| Growth Rate (2026 - 2031) | 9.34% CAGR |

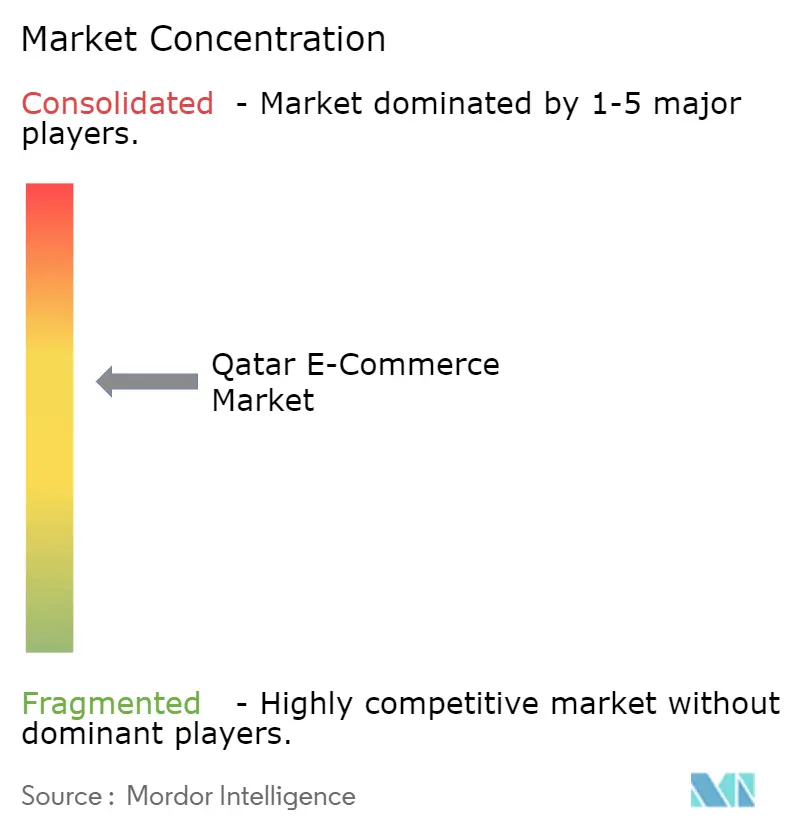

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar E-commerce Market Analysis by Mordor Intelligence

The Qatar E-commerce Market size is projected to expand from USD 4.54 billion in 2025 and USD 4.96 billion in 2026 to USD 7.75 billion by 2031, registering a CAGR of 9.34% between 2026 to 2031. Luxury-oriented consumer behavior, seamless 5G connectivity, and aggressive national diversification policies combine to keep transaction values rising even as regional peers slow. Domestic and cross-border platforms now target affluent Qataris and high-skill expatriates with curated premium assortments, while quick-commerce startups exploit Doha’s compact footprint to promise 15-minute grocery drops. Fintech licensing that legitimized Sharia-compliant buy-now-pay-later adds fresh liquidity to baskets that historically stalled at checkout. At the same time, procurement digitalization tied to stadium maintenance and smart-city pilots is converting business spending once handled by fax and phone into online orders, anchoring a second growth engine that is less cyclical than consumer retail.

Key Report Takeaways

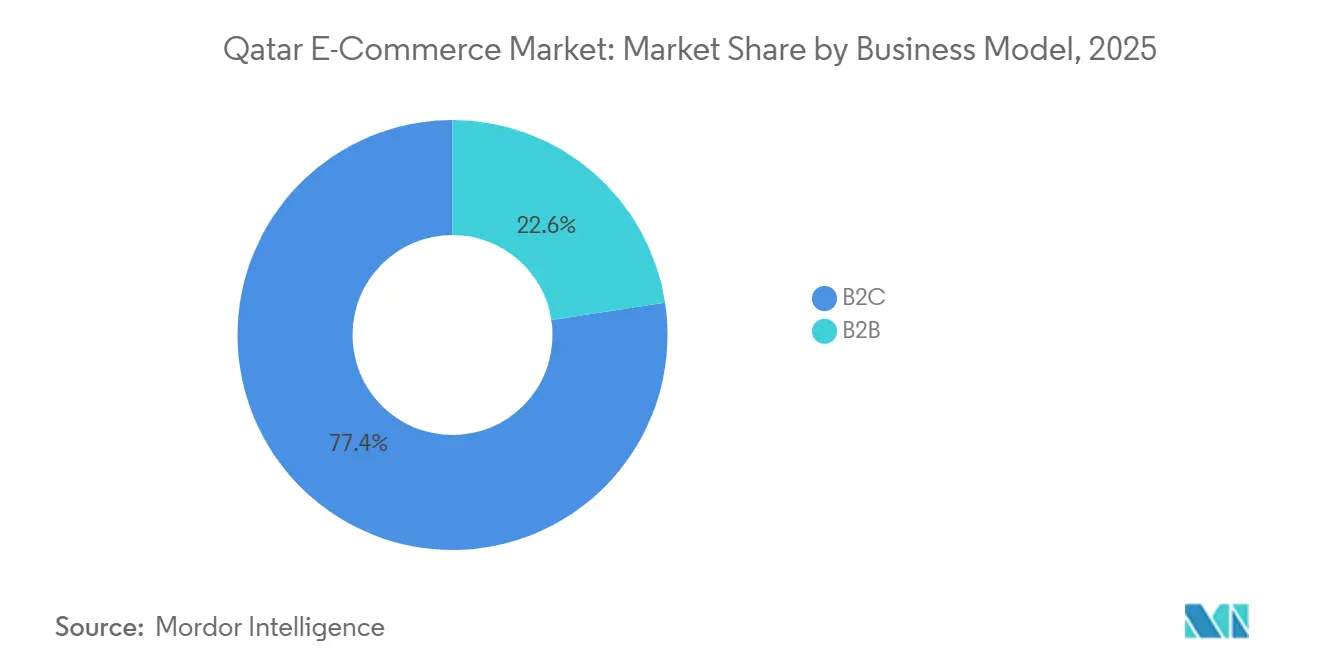

- By business model, business-to-consumer channels led with 77.39% of the Qatar E-commerce Market share in 2025 while business-to-business transactions are forecast to expand at a 10.37% CAGR through 2031.

- By device, smartphones captured 69.17% of transaction value in 2025 and are projected to grow at a 9.89% CAGR between 2026 and 2031.

- By payment method, credit and debit cards commanded a 38.92% share of checkout volume in 2025, whereas buy-now-pay-later records the fastest expected growth at 11.46% CAGR through 2031.

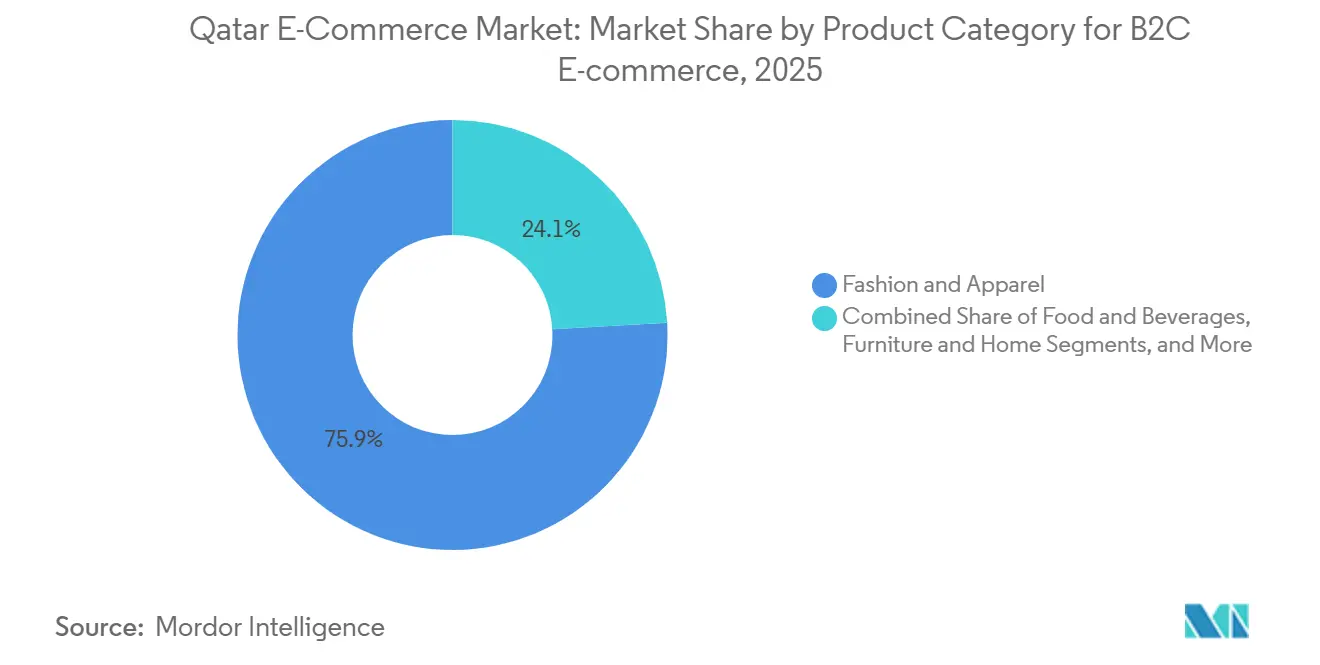

- By product category, fashion and apparel generated 31.59% of sales in 2025 and food and beverages is advancing at a 10.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationwide 5G Standalone Deployment in 2025 Unlocks High-speed Mobile Commerce | +2.1% | Doha, The Pearl-Qatar, Lusail, West Bay | Short term (≤ 2 years) |

| Qatar National Vision 2030 and TASMU Digital Programs Drive the Market | +1.8% | National, pilots in Doha, Lusail City, Education City | Medium term (2-4 years) |

| High Disposable Income and Luxury Consumption Culture | +1.5% | National, stronger in Qatari nationals and affluent expatriates | Long term (≥ 4 years) |

| Rapid Expansion of Same-day Hyper-local Delivery Start-ups | +1.3% | Doha metro, spreading to Al Rayyan and Al Wakrah | Short term (≤ 2 years) |

| Rising Penetration of Women-led Online Fashion Shopping | +0.9% | National urban centers | Medium term (2-4 years) |

| Cross-border Demand for High-end Imports via Tax-free Zones | +0.7% | National, leveraging Hamad International Airport | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nationwide 5G Standalone Deployment in 2025 Unlocks High-speed Mobile Commerce

Ooredoo and Vodafone achieved 98.9% population coverage with standalone 5G in 2025, cutting page-load times and enabling high-definition livestream shopping that converts hesitating browsers into buyers.[1]Ooredoo Qatar, “Ooredoo Qatar Launches 5G Standalone Network,” ooredoo.qa Millisecond-level latency now supports augmented-reality fittings for couture or cosmetics and lets shoppers track couriers on maps that refresh every few seconds. Dedicated spectrum slices reserved for e-commerce traffic during peak evenings curb cart abandonment linked to payment timeouts. Hyper-mobile consumers who carry multiple SIMs further magnify reach, pushing platforms to optimize progressive web apps that sidestep app-store delays. Logistics players equally benefit as 5G-enabled sensors broadcast van locations and thermologgers, allowing customers to reschedule within two-minute windows.

Qatar National Vision 2030 and TASMU Digital Programs Drive the Market

Economic diversification mandates under Qatar National Vision 2030 position e-commerce as a non-hydrocarbon pillar, channeling public grants into cloud hosting, open-data portals, and Arabic-language up-skilling that lower entry barriers for small sellers. TASMU requires ministries to route a portion of procurement through electronic marketplaces, guaranteeing baseline demand for B2B platforms and encouraging ERP integrations that automate catalog publishing.[2]Ministry of Transport and Communications, “Qatar Digital Inclusion Index 2025,” motc.gov.qa Smart-logistics pilots link delivery fleets to municipal traffic systems, shaving last-mile costs up to 18% and widening the serviceable radius for same-day grocery. Combined, Vision 2030 and TASMU embed e-commerce in national planning, insulating the sector from isolated consumer downturns.

High Disposable Income and Luxury Consumption Culture

Per-capita GDP above USD 80,000 supports repeat purchases of designer handbags, limited-edition sneakers, and premium electronics that many regional peers buy only on vacation. Online retailers capture holiday surges, with Ramadan 2025 generating a 35% lift in gross merchandise value and a 150% spike in gifting orders.[3]Qatar Central Bank, “Payment Systems Statistics – July 2025,” qcb.gov.qa Upscale shoppers gladly pay premia for white-glove delivery and bespoke packaging, letting platforms pad average order values and offset free-return policies. Still, Doha’s luxury malls remain experiential magnets, meaning online wins arise when immersive digital tools replicate in-store serendipity rather than when they undercut price.

Rapid Expansion of Same-day Hyper-local Delivery Start-ups

Snoonu, Baqaala, and Carriage blanketed Doha with dark stores and electric-scooter fleets that promise groceries in 15-30 minutes. Jahez Group’s USD 245 million buyout of Snoonu in 2025 merged Saudi demand-forecasting playbooks with Qatari geography, producing higher courier utilization and supplier bargaining power. Dense urban clusters where 90% of residents live within 25 km of city center let couriers average eight drops an hour, turning free delivery on baskets above QAR 50 (USD 13.7) into a profit generator. Hyper-local players also backfill Qatar’s thin convenience-store network, delivering milk or baby formula that otherwise requires weekend hypermarket trips.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Cash-on-Delivery Driving High Return Rates | -1.2% | National, stronger among lower-income expatriates | Medium term (2-4 years) |

| High Last-mile Costs Outside Doha Hinder the Market | -0.9% | Al Khor, Al Wakrah, Dukhan, rural corridors | Long term (≥ 4 years) |

| Small Addressable Population Base Restrains Growth | -0.6% | National | Long term (≥ 4 years) |

| Foreign-ownership Limits on Marketplace Localisation | -0.4% | National, cross-border entrants | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Cash-on-Delivery Driving High Return Rates

A sizable cohort of workers lacking local credit records still insists on paying the courier, forcing platforms to float inventory and suffer return rates that reach 25% in apparel. Each failed delivery triggers reverse-logistics costs and product write-downs that eat gross margins. The Central Bank licensed five buy-now-pay-later operators in 2024 to coax shoppers toward regulated digital credit, but early uptake remains thin, obliging retailers to fund education campaigns and loyalty perks.

High Last-mile Costs Outside Doha Hinder the Market

Deliveries to Al Khor, Al Wakrah, and Dukhan rarely achieve route density, inflating cost-per-drop and pressing platforms to add fuel surcharges or cap same-day promises. Labor laws that mandate minimum wages and end-of-service benefits raise the breakeven threshold further. Metro extensions ease passenger flows yet offer scant relief for freight, so rural baskets either get deferred into once-a-week slots or revert to bricks-and-mortar pickup, dampening the growth headroom beyond Doha’s primary catchment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B Procurement Digitalization Accelerates

Business-to-consumer orders dominated value at 77.39% in 2025, a legacy of early adoption by food delivery and fashion apps. The Qatar E-commerce Market size tied to corporate transactions, however, is projected to advance at a 10.37% CAGR as stadium operators, hotel groups, and ministries migrate tenders into electronic catalogs to meet TASMU compliance rules. Enterprises now seek bulk pricing, automated approval workflows, and invoice financing that consumer apps never offered. Platforms respond with punch-out integrations for SAP and Oracle, predictive reorder dashboards, and credit lines underwritten by local banks that capture float spread.

Platform traction in maintenance, repair, and operations supplies reflects Qatar’s post-World-Cup upkeep cycle, ensuring steady monthly ticket volumes rather than holiday spikes. Yet adoption hurdles persist because procurement managers value in-person supplier advice and flexible settlement terms. Marketplaces therefore bundle vendor-managed inventory, on-site installation, and warranty tracking to replicate the white-glove support of traditional distributors. If service parity holds, B2B’s share of the Qatar E-commerce Market share could climb sharply once electronic invoicing mandates broaden across state-owned enterprises.

By Device Type for B2C E-commerce: Mobile Dominance Reinforced by 5G

Smartphones delivered 69.17% of checkout value in 2025, and their lead widens behind sub-10 ms latency that supports video-first merchandising. Progressive web apps compress images, cache pages offline, and bypass app-store logjams, trimming acquisition costs while boosting time on site. The Qatar E-commerce Market size flowing through desktops still peaks during electronics or travel bookings that merit multi-tab comparisons, but its growth trails mobile’s projected 9.89% CAGR.

Voice commerce on smart speakers remains experimental owing to limited Arabic natural-language processing and privacy fears, yet automakers and telecoms are piloting dashboard interfaces that could surface fuel and parking payments by 2031. For now, retailers prioritize thumb-friendly checkout, tokenized card vaults, and zero-rating agreements that exempt video streams from data caps, ensuring that mobile retains priority in feature roadmaps and marketing spend.

By Payment Method for B2C E-commerce: BNPL Disrupts Traditional Instruments

Cards owned 38.92% of payment share in 2025 thanks to entrenched salary accounts and reward programs, but BNPL is racing ahead with an 11.46% CAGR now that the Central Bank codified consumer protections and Sharia-compliant Murabaha structures. Embedded installments inside checkout nudge hesitant shoppers to upgrade basket sizes without dipping into savings, a cultural fit for young families juggling remittances and rent. Digital wallets tie cashback and points across ride-hailing and food delivery super-apps, eroding bank card interchange.

Bank transfers persist for five-figure corporate orders where treasurers want explicit audit trails, while cryptocurrency stays niche given price volatility and ambiguous regulation. Overall, the Qatar E-commerce Market size handled through prepaid instruments is expected to surpass cash-on-delivery by 2027 as trust builds, fraud tools improve, and refund windows shrink from days to seconds.

By Product Category for B2C E-commerce: Food and Beverages Surge on Hyper-local Networks

Fashion and apparel claimed 31.59% of revenue in 2025, but food and beverages is the clear acceleration lane at a 10.02% CAGR because dark-store density lets couriers hit 15-minute rings that brick-and-mortar cannot match. Expatriates craving regional spices and levants finds staples absent in neighborhood grocers now load recurring baskets via subscription buttons that auto-ship each Friday. The Qatar E-commerce Market size tied to premium grocery also grows as refrigerated fleets backed by Lulu’s QAR 50 million (USD 13.7 million) investment safeguard organics and artisanal cheese integrity.[4]Lulu Group International, “QAR 50 Million Investment in Cold-Chain Logistics Infrastructure,” luluhypermarket.com

Electronics platforms chase loyalty with one-hour drop promises in Doha, installment financing, and extended warranty pick-ups, pushing conversion rates up despite commoditized SKUs. Beauty and personal care ride influencer livestreams that mix entertainment with instant shoppable links, and furniture players test augmented-reality placement to lower costly returns driven by size error.

Geography Analysis

Doha’s metropolitan corridor encompassing West Bay, The Pearl-Qatar, Lusail, and Al Sadd generated roughly 80% of 2025 sales as fiber backbones and 5G overlap with affluent households and expatriate professionals. Courier densification allows eight to ten deliveries per hour, turning same-day promises into sustainable gross margins. Talabat added three dark stores in Al Rayyan, Al Wakrah, and Lusail in February 2026 to extend 15-minute reach into suburbs, though profitability depends on volumes crossing break-even thresholds during non-peak slots.

Secondary cities such as Al Khor and Dukhan strain unit economics; low density forces fuel surcharges that steer shoppers back to hypermarkets. Government road spending and metro spurs improve passenger flow but yield only marginal benefit for freight, leaving rural households with longer delivery windows. Sandstorms and summer heat periodically shut highways, prompting platforms to hold buffer stock in micro-warehouses or reroute orders to click-and-collect lockers at petrol stations.

Cross-border hubs at Hamad International Airport and Qatar Free Zones let Amazon, Farfetch, and Noon bypass duties on re-exports, appealing to luxury seekers willing to wait three to ten days for niche brands. Amazon’s 2025 MoU with Qatar Development Bank to train 200 SMEs aims to on-board local artisans, shortening lead times and aligning with Vision 2030 diversification goals. Data-privacy laws modeled on EU standards are still maturing, exposing international sellers to compliance risk until enforcement clarity improves.

Competitive Landscape

Market concentration remains moderate; food delivery and grocery are led by Talabat, Lulu, Snoonu, and Carrefour Qatar, but no single group clears the 30% threshold across total gross merchandise value. Talabat’s USD 2 billion IPO funded AI-driven demand forecasting and potential bolt-on buys that could tighten leadership. Jahez’s Snoonu takeover imported Saudi scale benefits, introducing centralized rider dispatch and shared procurement across GCC nodes.

Cross-border majors leverage tax-free status and wide catalogs to capture considered purchases, leaving domestic apps to own perishables and instant-need items. Carrefour’s Mastercard wallet embeds 5% cashback that diverts traffic from competitors, while Jarir’s zero-interest Murabaha plans built with Qatar Islamic Bank pushed electronics ticket sizes up 30%.[5]Qatar Islamic Bank, “Sharia-Compliant Buy Now Pay Later with Jarir Marketing,” qib.com.qa

White-space remains in B2B verticals such as automotive spares, medical consumables, and construction aggregates where incumbents lack digital inventory visibility. Voice commerce in colloquial Arabic, subscription replenishment for household staples, and AI product advisors for luxury fashion are next-wave differentiators. Foreign-ownership law reforms allow 100% stakes, yet legacy sponsorship norms encourage joint ventures that trade equity for regulatory guidance, warehousing, and supplier goodwill.

Qatar E-commerce Industry Leaders

AliExpress.com

Carrefour Qatar (Majid Al Futtaim Retail L.L.C.)

Amazon.com, Inc.

Lulu Hypermarket (EMKE Group)

Al Anees Electronics W.L.L.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Talabat opened three dark stores in Al Rayyan, Al Wakrah, and Lusail City, expanding its 15-minute delivery footprint.

- January 2026: Carrefour Qatar and Mastercard launched a co-branded digital wallet that offers 5% cashback and free delivery above QAR 150 (USD 41).

- December 2025: Lulu Hypermarket committed QAR 50 million (USD 13.7 million) to refrigerated dark stores and temperature-controlled vehicles for fresh online grocery.

- November 2025: Jarir Marketing Company enabled Sharia-compliant BNPL through Qatar Islamic Bank, with installment orders climbing 37% year over year.

Qatar E-commerce Market Report Scope

The internet trade of goods and services is known as e-commerce (or electronic commerce). These commercial dealings are either B2B (business-to-business), B2C (business-to-consumer), or C2C (consumer-to-consumer). A more recent business model is "direct-to-consumer" (D2C), allowing brands to sell directly to consumers. The internet is what drives e-commerce. Consumers use their devices to access an online store to browse the selection and order goods or services. Qatar emerges as an ideal location for business growth, as the country has the world's highest GDP per capita, attracting companies to invest and expand their business reach.

The Qatar E-commerce Market Report is Segmented by Business Model (B2C and B2B), Device Type for B2C E-Commerce (Smartphone and Mobile, Desktop and Laptop, and Other Device Types), Payment Method for B2C E-Commerce (Credit and Debit Cards, Digital Wallets, Buy Now Pay Later, and Other Payment Methods), Product Category for B2C E-Commerce (Beauty and Personal Care, Consumer Electronics, Fashion and Apparel, Food and Beverages, Furniture and Home, and Other Product Categories). The Market Forecasts are Provided in Terms of Value (USD)

By Business Model

| B2C |

| B2B |

By Device Type for B2C E-commerce

| Smartphone and Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method for B2C E-commerce

| Credit and Debit Cards |

| Digital Wallets |

| Buy Now Pay Later |

| Other Payment Methods |

By Product Category for B2C E-commerce

| Beauty and Personal Care | Hair Care |

| Skin Care | |

| Cosmetics and Beauty | |

| Other Beauty and Personal Care Product Categories | |

| Consumer Electronics | Mobile |

| PC and Laptops | |

| Audio Devices | |

| Gaming Devices | |

| Other Consumer Electronics Product Categories | |

| Fashion and Apparel | Clothing |

| Footwear | |

| Fashion Accessories | |

| Other Fashion and Apparel Product Categories | |

| Food and Beverages | Packaged Food |

| Bakery and Confectionery | |

| Meat, Poultry, and Seafood | |

| Other Food and Beverages Product Categories | |

| Furniture and Home | Home Furniture |

| Office Furniture | |

| Outdoor Furniture | |

| Other Furniture and Home Product Categories | |

| Other Product Categories |

| By Business Model | B2C | |

| B2B | ||

| By Device Type for B2C E-commerce | Smartphone and Mobile | |

| Desktop and Laptop | ||

| Other Device Types | ||

| By Payment Method for B2C E-commerce | Credit and Debit Cards | |

| Digital Wallets | ||

| Buy Now Pay Later | ||

| Other Payment Methods | ||

| By Product Category for B2C E-commerce | Beauty and Personal Care | Hair Care |

| Skin Care | ||

| Cosmetics and Beauty | ||

| Other Beauty and Personal Care Product Categories | ||

| Consumer Electronics | Mobile | |

| PC and Laptops | ||

| Audio Devices | ||

| Gaming Devices | ||

| Other Consumer Electronics Product Categories | ||

| Fashion and Apparel | Clothing | |

| Footwear | ||

| Fashion Accessories | ||

| Other Fashion and Apparel Product Categories | ||

| Food and Beverages | Packaged Food | |

| Bakery and Confectionery | ||

| Meat, Poultry, and Seafood | ||

| Other Food and Beverages Product Categories | ||

| Furniture and Home | Home Furniture | |

| Office Furniture | ||

| Outdoor Furniture | ||

| Other Furniture and Home Product Categories | ||

| Other Product Categories | ||

Key Questions Answered in the Report

How large will online sales in Qatar become by 2031?

They are forecast to reach USD 7.75 billion, expanding at a 9.34% CAGR from 2026 to 2031.

Which customer segment is driving the fastest growth?

Business-to-business procurement orders are set to record a 10.37% CAGR as construction, hospitality, and public agencies digitize sourcing.

What device dominates online checkouts today?

Smartphones account for 69.17% of transaction value and continue to outpace desktops.

Why is buy-now-pay-later gaining traction in Qatar?

Central Bank licensing and Sharia-compliant structures fuel consumer trust, supporting an expected 11.46% CAGR for BNPL through 2031.

Which product category is projected to grow quickest?

Food and beverages leads with a 10.02% CAGR thanks to 15-minute hyper-local delivery models.

Do foreign players face ownership limits?

Law No. 1 of 2019 allows 100% foreign ownership in most sectors, though legacy sponsorship practices still influence local partnerships.

Page last updated on: