Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.94 Billion |

| Market Size (2026) | USD 3.26 Billion |

| Market Size (2031) | USD 4.62 Billion |

| Growth Rate (2026 - 2031) | 7.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman E-commerce Market Analysis by Mordor Intelligence

The Oman e-commerce market size is projected to be USD 2.94 billion in 2025, USD 3.26 billion in 2026, and reach USD 4.62 billion by 2031, growing at a CAGR of 7.22% from 2026 to 2031. Rapid progress under Vision 2040, a national digital-transformation agenda that had already delivered 2,277 online government services by late 2025, sustains consumer confidence and vendor participation. Mobile-payment volumes rose more than eight-fold between 2022 and 2023, and 87% of all transactions moved to digital channels by the end of 2024, signaling that the checkout experience now matches consumer expectations for speed and security. Business-to-business (B2B) platforms are emerging as the next frontier as small and medium enterprises automate procurement, while rising cross-border shopping links Omani buyers to Chinese and Gulf Cooperation Council (GCC) sellers. Nevertheless, interior governorates still face high last-mile costs and limited consumer-protection enforcement, factors that temper short-term conversion rates and elevate logistics risk for merchants.

Key Report Takeaways

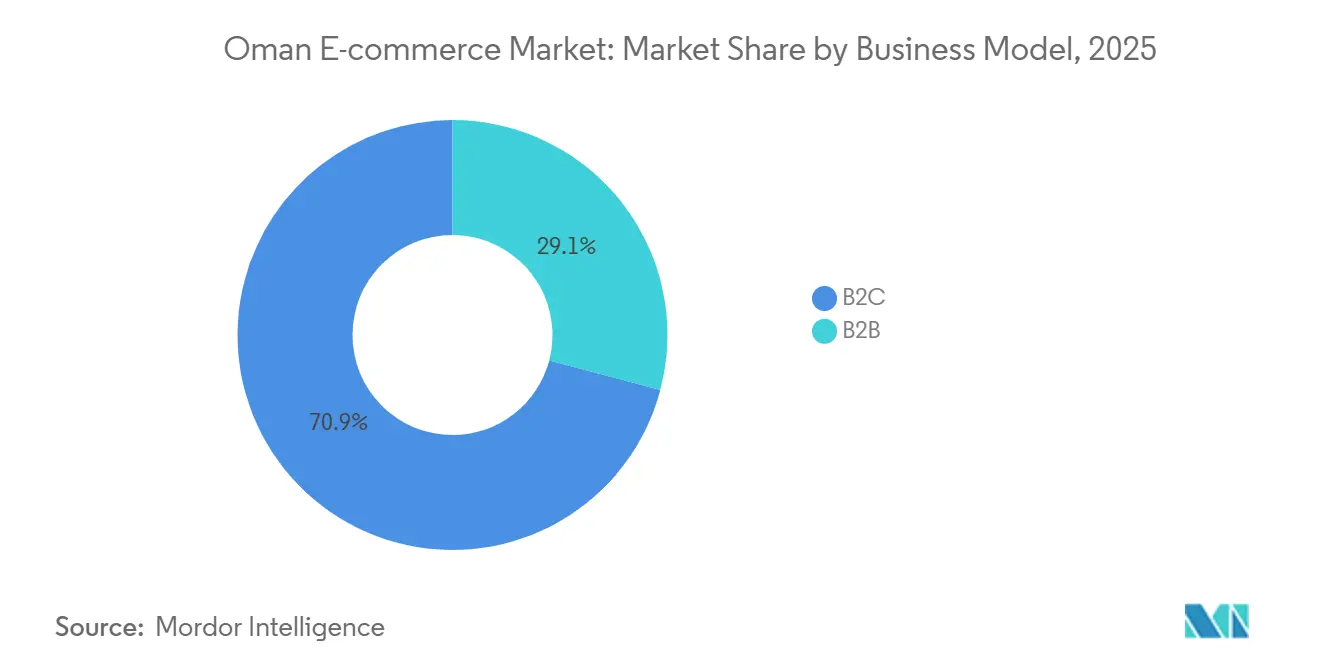

- By business model, business-to-consumer (B2C) transactions held 70.89% revenue share in 2025, while B2B is projected to expand at a 7.43% CAGR through 2031.

- By device type, smartphones captured 82.67% of the Oman e-commerce market share in 2025 and will grow at a 7.31% CAGR through 2031.

- By payment method, credit and debit cards accounted for 43.92% share of the Oman e-commerce market size in 2025, and digital wallets are advancing at an 8.27% CAGR through 2031.

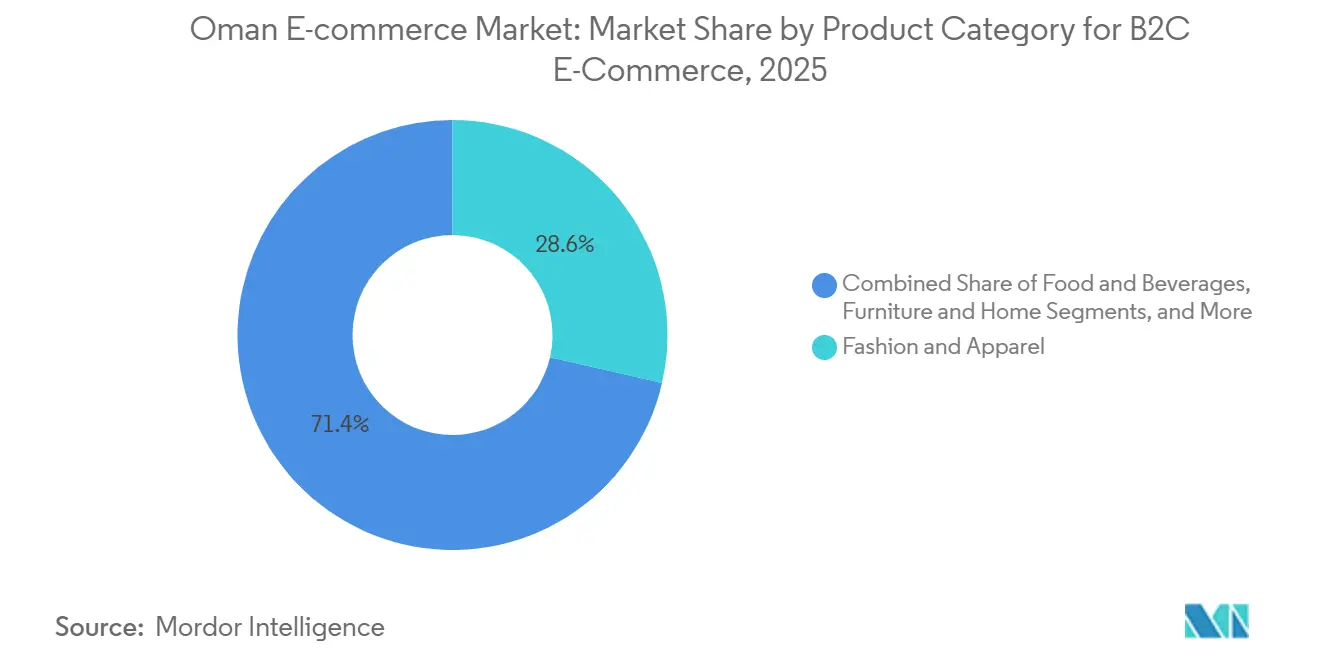

- By product category, fashion and apparel led with 28.59% share in 2025, while food and beverages are expected to grow at an 8.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Oman E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Mobile-Payment Transaction Volumes | +1.8% | National, concentration in Muscat and Al Batinah North | Short term (≤ 2 years) |

| Growing Cross-Border Shopping From China And GCC | +1.2% | National, early gains in Muscat and Dhofar | Medium term (2-4 years) |

| Expansion Of National E-Payment Gateway (CBO) | +1.5% | National | Medium term (2-4 years) |

| Government Vision 2040 Digital-Economy Programs | +1.0% | National | Long term (≥ 4 years) |

| Emergence Of Community Group-Buy Models In Interior Towns | +0.5% | Al Dakhiliyah and interior governorates | Medium term (2-4 years) |

| Rise Of Influencer-Led Live Commerce Among Omani Gen Z | +0.7% | National, concentration in Muscat | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Mobile-Payment Transaction Volumes

Mobile-payment transactions climbed from 4.9 million in 2022 to 40 million in 2023, a 551% leap that converted checkout frictions into instant “one-tap” confirmations.[1]Central Bank of Oman, “Digital Payment Statistics,” cbo.gov.om Apple Pay’s national launch in 2024, followed by Google Pay in 2025 and Global Pay in 2026, deepened wallet competition and nudged younger consumers away from cash-on-delivery. The Central Bank expects mobile volumes to sustain a 75% compound rate through 2026, shrinking cart-abandonment risk and lowering reverse-logistics costs. Point-of-sale terminals still account for half of digital payments, yet e-commerce’s share is rising, underlining a clear channel shift. Card-network reliance is easing, opening lanes for fintech newcomers focused on installment plans and micro-credit.

Growing Cross-Border Shopping from China and GCC

Chinese marketplaces and GCC platforms widen assortment for electronics, fashion, and beauty where local inventory remains thin. Shein’s semi-hosted service, introduced in April 2025, lets third-party merchants tap its logistics stack, while AliExpress sustains direct-from-factory pricing albeit with longer fulfillment. Partnerships between Asyad Express and global players such as Amazon and Shein have enhanced last-mile reliability for foreign parcels.[2]Asyad Express, “Asyad Express Expands Partnership with Amazon,” asyadexpress.com Customs bottlenecks during Ramadan sales remain a pain point, but progressive clearance reforms are cutting dwell times. Currency-conversion fees and limited dispute resolution keep a subset of shoppers anchored to domestic platforms, yet the value proposition of variety and price continues to pull traffic across borders.

Expansion of National E-Payment Gateway (CBO)

The Central Bank’s gateway, which reached 87% digital-transaction penetration by end-2024, unifies QR, wallet, and card rails into real-time clearing, compressing order-to-cash cycles from days to hours. Merchant fees drop as settlement becomes instant, and shoppers face fewer redirects during checkout. The government’s OMR 3.4 billion (USD 8.8 billion) infrastructure program finances 5G rollout and data-center capacity, ensuring that rural buyers experience similar latency to urban peers. Mandatory integration with the Naql address platform boosts successful deliveries and smooths returns. Cash still funds 25% of transactions, mainly among older and rural cohorts, so wallet providers are layering biometric authentication and Arabic interfaces to bridge trust gaps.

Government Vision 2040 Digital-Economy Programs

Vision 2040 sets a target for a cashless society and end-to-end digital service delivery, creating a policy bedrock for the Oman e-commerce market.[3]Oman Observer, “73% of Vision 2040 Digital Transformation Implemented,” omanobserver.om Royal Decree No. 39/2025 introduces penalties up to OMR 50,000 (USD 130,000) and five-year imprisonment for online fraud, reinforcing buyer protection. Ministerial Resolution No. 499/2023 established the Maroof Oman trust-badge program, which authenticates seller credentials and rates service quality. More than 70% of the digital-transformation roadmap was complete by November 2024, eliminating paper-based licensing that had slowed start-ups. Execution gaps remain, inspection capacity and cross-border cooperation lag, but long-term confidence in digital trade is rising.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Consumer-Protection Enforcement Online | -0.8% | National | Short term (≤ 2 years) |

| High Last-Mile Costs In Interior Governorates | -1.0% | Al Dakhiliyah, Dhofar, interior regions | Medium term (2-4 years) |

| Fragmented Delivery-Address System Causing Failed Deliveries | -0.6% | National, acute in interior towns | Short term (≤ 2 years) |

| Limited Arabic-Language UX Optimization On Global Platforms | -0.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Consumer-Protection Enforcement Online

The Consumer Protection Authority logged 1,851 e-commerce complaints in the first eight months of 2025 yet recovered only OMR 24,500 (USD 63,670), highlighting a gap between regulation and restitution. While Decree No. 39/2025 stiffens penalties, practical enforcement lags in dispute resolution, inspection, and cross-border cooperation. Shoppers who receive counterfeit or non-delivered goods often have limited recourse, pushing risk-averse buyers back to physical stores. The Maroof Oman registry remains voluntary, so many small sellers operate without accreditation. Trust deficits therefore linger, curbing repeat purchase rates and raising customer-acquisition costs for platforms.

High Last-Mile Costs In Interior Governorates

Mountainous terrain and sparse populations in Al Dakhiliyah, Dhofar, and parts of Al Batinah North inflate per-parcel delivery costs by up to 50% versus Muscat. Failed-delivery rates can top 15% because many addresses rely on informal landmarks rather than structured street names. Although the Naql platform standardizes geocodes, courier fleets still face longer drive times and under-utilized return legs. Asyad Express, despite processing more than 925,000 shipments in 2024, remains concentrated along coastal corridors. Merchants either absorb higher fulfillment costs or impose minimum-order thresholds, which deter low-ticket buyers in interior regions. Consequently, national penetration of the Oman e-commerce market remains skewed toward Muscat.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B Platforms Gain Momentum

B2C channels dominated the Oman e-commerce market in 2025, holding 70.89% of revenue as global marketplaces and local food-delivery apps catered to household demand. In absolute terms, this slice translated into roughly two-thirds of the Oman e-commerce market size that year, validating consumer-first design choices and aggressive wallet promotions. B2B, while smaller, is projected to expand at a 7.43% CAGR through 2031, outpacing overall growth as small enterprises digitize procurement and chase bulk-buy discounts.

Momentum on the B2B side rests on three levers: invoice-financing options of three to twelve months, automated purchase-order links to accounting software, and consolidated freight that lowers per-unit shipping costs. Platforms such as Tradeling already aggregate more than 97,000 suppliers and 40,000 buyers, giving wholesalers national reach without physical branch networks. As integration with enterprise resource-planning tools deepens, average order values are climbing and reorder cycles shortening, narrowing the gap with B2C volumes. The upshot is a gradual rebalancing in which B2B earns a larger Oman e-commerce market share and helps smooth seasonality that often skews consumer sales.

By Device Type For B2C E-Commerce: Smartphones Cement Leadership

Smartphones captured 82.67% of B2C sales in 2025, converting high mobile-penetration rates into checkout flows that take less than ten seconds. That dominance is forecast to continue at a 7.31% CAGR to 2031, keeping the handset as the primary gateway to the Oman e-commerce market. Dual-SIM ownership, ubiquitous 4G coverage, and expanding 5G corridors combine to eliminate bandwidth bottlenecks that once favored desktops.

Laptop and desktop sessions still matter for research-heavy categories, electronics, furniture, and high-end fashion, where side-by-side spec reviews require larger screens. Tablets and smart TVs remain marginal but could benefit from maturing voice-commerce interfaces in Arabic. Retailers are now optimizing progressive web apps that preload content, work offline, and integrate native wallets to cut data usage. As a result, mobile conversion rates are rising faster than traffic, yielding incremental gains in the Oman e-commerce market size even without dramatic new-user growth.

By Payment Method for B2C E-Commerce: Wallets Overtake at Checkout

Credit and debit cards held 43.92% of transaction value in 2025, a legacy advantage rooted in long-running card-network infrastructure. Digital wallets, however, are forecast to grow at an 8.27% CAGR through 2031 and are already closing in on parity as Apple Pay, Google Pay, and the newly launched Global Pay compete on rewards and biometric login speed. One-tap authentication trims form-fill friction, cutting abandonment rates that once plagued late-stage carts.

Merchants increasingly steer customers toward wallets by absorbing service fees that are lower than card interchange, while buy-now-pay-later providers test pilot programs tied to digital-wallet rails. Cash-on-delivery has slipped below 20% of regional e-commerce orders, freeing couriers from costly reverse-logistics loops. Cross-border shoppers still lean on cards when wallets lack foreign-exchange functionality, yet domestic purchases now default to phone-based payment. The shift boosts trusted tokenization and, by extension, expands the Oman e-commerce market share taken by fully digital tender.

By Product Category for B2C E-Commerce: Food and Beverages Sprint Ahead

Fashion and apparel led with a 28.59% slice of sales in 2025, underscoring social-media-driven discovery and the relative ease of shipping lightweight parcels. Food and beverages, though smaller, are projected to accelerate at an 8.02% CAGR to 2031, the fastest among major verticals. Quick-commerce dark stores and cloud-kitchen operators have trimmed average delivery windows in Muscat to under 30 minutes, pulling more grocery baskets online each month.

Beauty, electronics, and home furnishings occupy the middle tier, each requiring distinct content strategies and return policies. Beauty thrives on live-stream tutorials, electronics depend on spec transparency, and furniture leans on augmented-reality previews to cut fit-related returns. Seasonal tourism in Dhofar and holiday gifting in Muscat add predictable peaks for electronics and beauty, while Ramadan promotions boost food staples. As cold-chain capacity expands into Dhofar and Al Batinah North, grocery penetration will rise quickly, reshaping category weightings within the broader Oman e-commerce market.

Geography Analysis

Muscat dominates the Oman e-commerce market, benefiting from dense population pockets, higher per-capita income, and mature logistics corridors. The capital’s share remains bolstered by 5,700-square-meter fulfillment hubs that enable same-day or next-day delivery for most stock-keeping units.[4]Asyad Express, “Asyad Express Expands Partnership with Amazon,” asyadexpress.com Dhofar follows, aided by tourism demand during the Khareef season, while Al Batinah North leverages industrial clusters and port access to stimulate B2B order volumes.

Interior regions such as Al Dakhiliyah struggle with fragmented addressing and rugged terrain, pushing delivery costs high and service levels low. The Telecommunications Regulatory Authority’s mandate to integrate courier systems with the Naql geocode platform is beginning to reduce failed deliveries. Government investment of OMR 3.4 billion (USD 8.8 billion) in digital infrastructure aims to equalize service quality, yet many interior towns still see two-day fulfillment windows that blunt e-commerce’s convenience advantage.

Cross-border parcels into Muscat clear customs faster than shipments routed to secondary cities, encouraging importers to consolidate at capital hubs before domestic re-distribution. Quick-commerce players keep their cold chain largely within Muscat’s suburbs, underscoring the urban-centric nature of high-frequency grocery delivery. Until interior address systems mature, regional disparities will persist and shape incremental growth trajectories across the Oman e-commerce market.

Regulatory Landscape

Oman's e-commerce rulebook is anchored by Ministerial Resolution No. 499/2023, administered by the Ministry of Commerce, Industry and Investment Promotion (MOCIIP), which sets governance requirements for online selling and marketing across websites, marketplaces, and social media storefronts (including Instagram, TikTok, and WhatsApp). The framework ties market entry to licensing via the Oman Business Platform and links trust building to seller verification through the Maroof Oman program, which also functions as a visible trust badge for compliant stores.

The legal environment for electronic transactions was updated with Royal Decree No. 39/2025 (Electronic Transactions Law), which strengthens deterrence against online fraud with penalties of up to OMR 50,000 and potential imprisonment. Oversight is shared across bodies that directly shape e-commerce operations, including the Central Bank of Oman for payment rails and the Consumer Protection Authority for complaint handling, while the Telecommunications Regulatory Authority influences service quality through digital infrastructure and platform integration mandates (including addressing and courier-system interoperability).

Value Chain Analysis

The Oman e-commerce value chain begins with merchants and brands sourcing locally and through cross-border channels, then listing on marketplaces, retailer apps, and increasingly social commerce surfaces (Instagram, TikTok, and WhatsApp). Store onboarding and credibility are reinforced by MOCIIP licensing through the Oman Business Platform and voluntary Maroof Oman registration, while payments run through card networks and a fast-growing wallet layer connected to the Central Bank of Oman's national e-payment gateway.

Downstream, fulfillment is carried out via in-house fleets and third-party logistics. Asyad Express and Oman Post are central to nationwide coverage and returns management, while trade enablement platforms and digital clearance workflows take on greater importance for cross-border parcels and B2B replenishment. Government-backed processes, including the Hazm electronic platform for product safety conformity and customs-related workflows, and logistics digitization initiatives (including the National Port Community System) further support cross-border movement. The main friction points remain last-mile economics outside Muscat, addressing-related delivery failures, and trust issues that drive cancellations and disputes, which in turn raise fulfillment and customer-service costs for platforms and sellers.

Competitive Landscape

The Oman e-commerce market remains moderately fragmented. Amazon, Noon, and Talabat anchor regional scale, while domestic firms such as Asyad Express, eMushrif, and Tradeling focus on localized pain points. Noon’s USD 500 million raise in December 2025 values the platform near USD 10 billion and funds dual initial public offerings in the United Arab Emirates and Saudi Arabia, cementing resources for deeper fulfillment and advertising capabilities.

Talabat acquired InstaShop for USD 32 million in March 2025, bundling grocery and restaurant delivery into one ecosystem and locking in quick-commerce density. Asyad Express, leveraging its national postal network, expanded its Amazon partnership and posted 81% volume growth in 2024, followed by the launch of an automated fulfillment center in December 2025.

Market white space exists in B2B procurement and influencer-led live commerce, both of which remain underpenetrated. Technology differentiators such as augmented-reality visualization, AI-driven personalization, and blockchain supply-chain tracking will decide future competitive rankings. As platforms converge on pricing and assortment, fulfillment speed, localized content, and embedded financial services will define loyalty within the Oman e-commerce market.

Oman E-commerce Industry Leaders

Amazon Inc.

Noon AD Holdings Ltd.

Talabat Middle East LLC

Carrefour Oman (Majid Al Futtaim Retail LLC)

Lulu Group International LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Trust-led formalization remains a key opportunity as regulation moves from baseline licensing toward verification and visibility support. With Royal Decree No. 39/2025 strengthening the electronic transactions framework and the Maroof Oman trust-badge program in place, platforms and enablement providers can productize compliance as a service, covering onboarding, disclosure templates (returns and exchange rules), seller identity checks, and dispute-handling workflows that reduce the friction pushing some buyers back to offline retail.

Conversational commerce and merchant tooling offer a practical expansion lane because a large share of SMB selling already happens on social platforms. The observed shift toward WhatsApp as a storefront, alongside AI-assisted ordering and invoicing tools used by local businesses, creates whitespace for integrations that link chat-based ordering to wallet checkout and courier dispatch. On the infrastructure side, the National E-commerce Strategy and government digital transformation programs provide a clear implementation backdrop, with late-2025 delivery of 2,277 online government services and digitized permits supporting faster merchant setup and operational compliance for e-commerce-led SMEs.

Recent Industry Developments

- July 2026: The Ministry of Commerce, Industry and Investment Promotion invited verified e-stores to register to boost visibility on social media and digital platforms. The effort links regulatory verification to demand generation, encouraging more merchants to formalize and promoting trusted commerce signals for buyers.

- February 2026: talabat signed an MoU with Oman Post to establish a delivery driver resting area in Muscat, aligning with the governments Bikes Project initiative. The partnership supports more resilient last-mile operations by improving courier welfare and creating a blueprint for standardized delivery infrastructure.

- July 2025: Google Pay became available nationwide through a partnership with Sohar International Bank. Wider wallet acceptance strengthens one-tap checkout and reduces reliance on cash-on-delivery, supporting higher conversion rates for mobile-first commerce.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market means the value of goods and services sold through digital channels where the buyer is in Oman, and the transaction is completed online through websites or apps.

Scope exclusions: We exclude offline purchases that are only influenced by online advertising, and we also exclude purely digital content subscriptions when they are not part of an online retail checkout.

Segmentation Overview

- By Business Model

- B2B

- B2C

- By Device Type for B2C E-commerce

- Smartphone and Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method for B2C E-commerce

- Credit and Debit Cards

- Digital Wallets

- Buy Now Pay Later

- Other Payment Methods

- By Product Category for B2C E-commerce

- Beauty and Personal Care

- Hair Care

- Skin Care

- Cosmetics and Beauty

- Other Beauty and Personal Care Product Categories

- Consumer Electronics

- Mobile

- PC and Laptops

- Audio Devices

- Gaming Devices

- Other Consumer Electronics Product Categories

- Fashion and Apparel

- Clothing

- Footwear

- Fashion Accessories

- Other Fashion and Apparel Product Categories

- Food and Beverages

- Packaged Food

- Bakery and Confectionery

- Meat, Poultry, and Seafood

- Other Food and Beverages Product Categories

- Furniture and Home

- Home Furniture

- Office Furniture

- Outdoor Furniture

- Other Furniture and Home Product Categories

- Other Product Categories

- Beauty and Personal Care

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped us set the country context and build the first set of assumptions before numbers were modeled. We relied on public sources such as Oman National Centre for Statistics and Information releases, Telecommunications Regulatory Authority updates on connectivity, Central Bank of Oman publications on card and payment trends, and Universal Postal Union or similar postal and parcel indicators.

We also used company annual reports, investor presentations, and reputable press coverage to understand category mix shifts, payments adoption, and delivery lead time expectations. Where Oman specific splits were not clearly disclosed, we used paid subscriptions for company financials and intelligence, news and financials, and an import export shipment level database to sanity check trade linked categories and supply availability. The source list above is illustrative only, and many other public and paid references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with marketplace operators, brand led online sellers, logistics partners, payment ecosystem participants, and category specialists who track local basket behavior. Respondent input was cross-checked for Muscat led demand centers and the rest of Oman, and then reconciled with desk research so assumptions like take rates, delivery costs, and online conversion stayed anchored to on the ground reality.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 17% | |

| Mid tier: 51% | Functional/Unit leaders: 23% | |

| Smaller Players: 21% | Managers: 60% |

Market-Sizing & Forecasting

We modeled the Oman market using a top-down demand pool build that starts from total retail and services spending proxies, and then applies online penetration and category level online share to reach digital sales value. Results were then corroborated using selective bottom-up approximations, such as sampled order volumes from leading categories multiplied by observed average order values, followed by channel checks with logistics and payments stakeholders.

Key inputs used to shape the model included smartphone based shopping share, payment method mix (cards versus wallets and cash on delivery), average basket values by major categories, delivery coverage and last mile capacity, and the split between B2C and B2B online buying. Where primary inputs varied by respondent type, the assumption was narrowed through follow-up questions and anchored to a conservative mid-range that still matched observed adoption signals.

For forecasting, we used scenario analysis supported by regression style checks, where the growth path is tied to drivers like internet use, digital payment adoption, and logistics service quality, and then tempered for periods of slower consumer spending. Gaps in bottom-up checks were handled by scaling only within categories where a clear linkage could be validated, rather than forcing a full supplier roll-up.

Data Validation & Update Cycle

Validation was done in layers so that one source did not decide the outcome. Model outputs were compared against independent signals such as payments growth, parcel activity direction, and category level online intensity shared during interviews, and then abnormal jumps were reviewed before sign-off.

We run internal analyst reviews where assumptions, conversions, and currency handling are rechecked, and clarifications are re-confirmed when variance crosses a set threshold. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Oman E Commerce Market Size Versus Other Published Estimates

Published market values for Oman e-commerce do not always match, and the gap usually comes from what is being counted and how the value is measured. Differences show up quickly when one source is tracking seller revenue, while another uses GMV style transaction value or mixes in cross-border flows without stating it clearly.

By tracking revenue definitions, reconciling payment mix and device led shopping behavior, and refreshing scope checks annually, Mordor Intelligence keeps the Oman estimate aligned to what is actually earned from online transactions, and not inflated by double counted pass-through value. In practice, the spread below is mainly driven by GMV versus revenue treatment, base year choice, and how B2B is included alongside consumer online buying.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.94 B (2025) | |

| Global Consultancy A | USD 1.84 B (2023) | Uses an earlier base year and a different coverage window, and the study framing appears to mix several commerce types, which can shift the value boundary away from Oman only online checkout revenue. |

| Trade Journal B | USD 1.24 B (2029) | Targets a forward year and is presented closer to GMV style activity value, which can understate or overstate revenue depending on take rates, returns, and cross-border inclusion. |

Looking at the three values together, the main takeaway is that definition and timing drive most of the difference, not a single growth assumption. Keeping the market boundary tied to verified transaction channels, clear value logic, and repeatable checks makes the final number easier to trace and update over time.

Key Questions Answered in the Report

How large will online retail spending in Oman be by 2031?

The Oman e-commerce market is expected to reach USD 4.62 billion by 2031.

Which device drives most digital sales in Oman?

Smartphones accounted for 82.67% of all B2C orders in 2025 and continue to dominate growth.

What payment method is gaining traction fastest?

Digital wallets are projected to grow at an 8.27% CAGR through 2031, outpacing cards and cash.

Why are B2B platforms important to future growth?

B2B channels are forecast to expand at 7.43% annually as small enterprises digitize procurement and seek invoice financing.

Which product category is set to grow quickest?

Food and beverages lead the growth curve with an expected 8.02% CAGR to 2031, fueled by quick-commerce and cloud kitchens.

What regulation protects online shoppers?

Royal Decree No. 39/2025 enforces penalties up to OMR 50,000 (USD 130,000) and five-year imprisonment for electronic transaction fraud.

Page last updated on: