Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

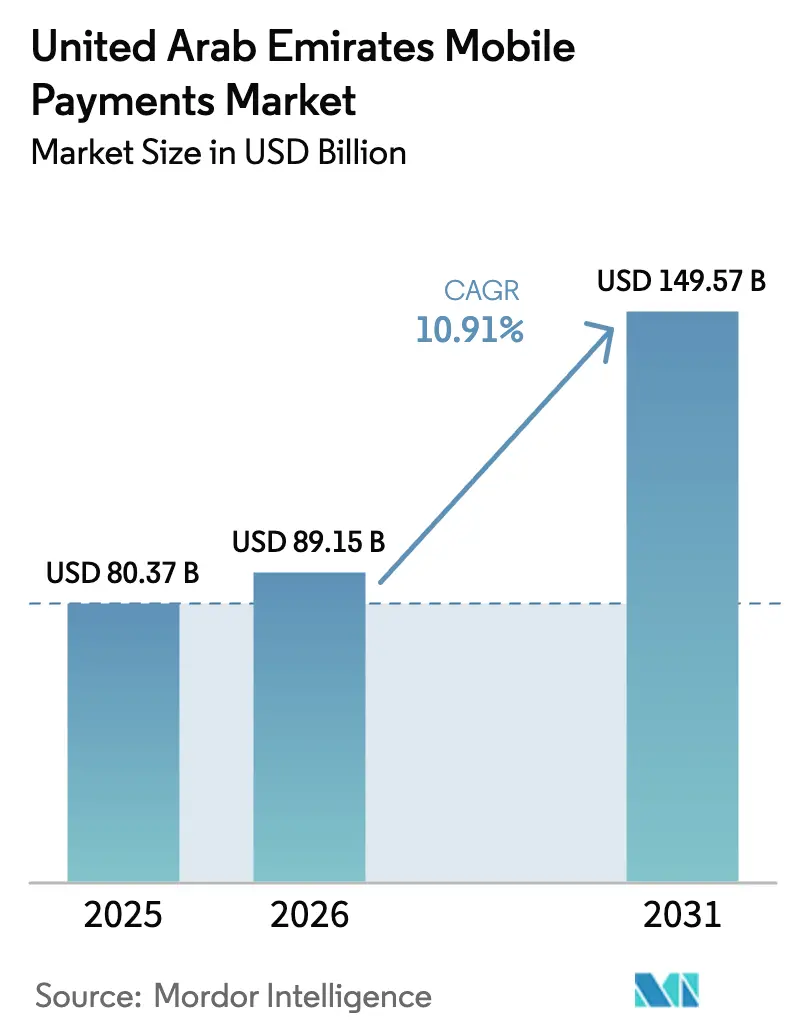

| Base Year Market Size (2025) | USD 80.37 Billion |

| Market Size (2026) | USD 89.15 Billion |

| Market Size (2031) | USD 149.57 Billion |

| Growth Rate (2026 - 2031) | 10.91% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Mobile Payments Market Analysis by Mordor Intelligence

The UAE mobile payments market size in 2026 is estimated at USD 89.15 billion, growing from 2025 value of USD 80.37 billion with 2031 projections showing USD 149.57 billion, growing at 10.91% CAGR over 2026-2031. Government commitments to double the digital economy’s GDP contribution, rapid 5G roll-out, and a near-universal smartphone penetration rate exceeding 95% underpin this sustained expansion.[1]Global Government Fintech, “UAE ‘Financial Infrastructure Transformation Programme’ Is 85 Per Cent Complete,” globalgovernmentfintech.com Regulatory milestones such as the Central Bank’s Financial Infrastructure Transformation Programme and the Open Finance Regulation have lowered transaction frictions, encouraged data-driven innovation, and created clear rulebooks for new entrants. Intensifying bank-telco alliances, accelerating peer-to-peer (P2P) transfers, and the late-2025 launch timetable for a retail Central Bank Digital Currency (the Digital Dirham) further strengthen the outlook. Despite rising cyber-fraud sophistication, a credible regulatory stance and multi-layered biometric security tools continue to improve consumer confidence, enabling merchants and financial institutions to deepen engagement across every emirate.

Key Report Takeaways

- By payment type, proximity payments commanded 67.30% of UAE mobile payments market share in 2025, while remote payments are forecast to post a 14.05% CAGR through 2031.

- By transaction type, in-store POS led with 39.40% revenue share in 2025; P2P transfers are the fastest-growing at a 13.63% CAGR through 2031.

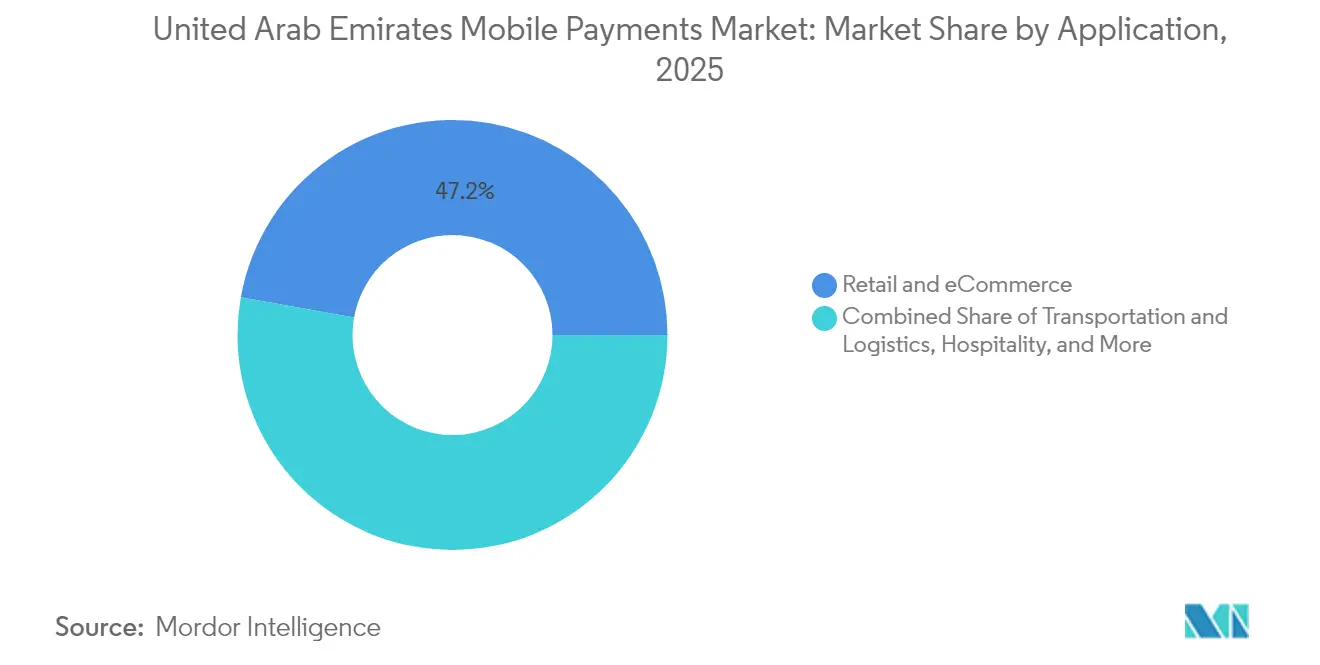

- By application, retail and eCommerce accounted for 47.20% share of the UAE mobile payments market size in 2025; transportation and logistics is advancing at a 15.31% CAGR through 2031.

- By end-user, personal users held 69.10% of value in 2025, whereas the business segment is expanding at a 12.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Mobile Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in Smartphone Penetration in UAE | +1.8% | National, concentrated in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Expansion of Mobile Wallet Ecosystem Backed by Local Banks & Telcos | +2.1% | National, with early gains in Dubai, Abu Dhabi, Sharjah | Long term (≥ 4 years) |

| Government-led Cashless Initiatives under UAE Vision 2031 | +1.5% | National, spill-over to broader GCC region | Long term (≥ 4 years) |

| Rising Acceptance of Contactless POS Infrastructure in Retail & Hospitality | +1.9% | Dubai core, expanding to Northern Emirates | Medium term (2-4 years) |

| Surge in Digital Remittance Inflows via Mobile Channels from Expat Workforce | +1.3% | National, concentrated in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Competitive Promotions and Loyalty Programs Accelerating User Acquisition | +1.2% | National, with focus on urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Smartphone Penetration Drives Infrastructure Investment

A nationwide smartphone penetration rate above 95% compels banks and telcos to scale digital channels rapidly. Emirates NBD’s ENBD X app now aggregates more than 200 services and records a 91% digital-adoption rate, evidencing the user appetite unlocked by ubiquitous 5G connectivity.[2]Emirates NBD, “ENBD X Application | Mobile Banking App in the UAE,” emiratesnbd.com Both e& and Du have spent heavily on 5G rollout; e& alone serves 189.3 million subscribers and reported 2.5× growth in monthly active users for its e& money fintech unit, underscoring ecosystem readiness.[3]e&, “e& Delivers Record Revenue and Net Profit in FY 2024,” eand.com High-speed mobile bandwidth reduces latency, enabling biometric authentication and real-time fraud analytics that are central to user trust in the UAE mobile payments market.

Banking–Telco Partnerships Reshape the Ecosystem

Integrated propositions such as First Abu Dhabi Bank’s Payit and du Pay illustrate how partnerships pool large customer bases and shared KYC frameworks to lower acquisition costs. Payit connects to 170+ corridors for remittances, while du Pay allows instant transfers to over 200 destinations, a capability welcomed by the 8.84 million expatriates who remit income regularly. These alliances create multi-service super-apps that deepen engagement and raise switching costs, bolstering revenue diversity across the UAE mobile payments market.

We the UAE 2031 Accelerates Cashless Uptake

The Vision 2031 agenda links non-oil diversification goals to digital-payment penetration, steering policy toward mandatory e-government disbursements and broadening the regulatory sandbox. Preparations to issue a retail Digital Dirham by late 2025 reflect a strategic bid to cement monetary sovereignty while testing programmable money use cases in tax collection and subsidy distribution. Such milestones act as signalling devices that bolster investor and merchant confidence in the UAE mobile payments market.

Contactless Infrastructure Expansion Drives Merchant Adoption

Over 70% of retailers reported revenue gains after enabling contactless payments, validating capex in tap-and-go terminals. Flying Tiger’s Scan & Go solution achieved a 50% user-adoption rate within the first week at Dubai Hills Mall, demonstrating consumer readiness for device-based self-checkout. As infrastructure densifies, the UAE mobile payments market gains resilience against friction that once slowed point-of-sale digitisation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer Concerns over Data Privacy amid Expanding Open Banking | -0.8% | National, particularly affecting tech-savvy demographics | Medium term (2-4 years) |

| Fragmented Merchant Acceptance for QR Codes vs NFC Causing Friction | -1.1% | National, more pronounced in smaller emirates | Short term (≤ 2 years) |

| High Cost of Compliance with UAE Central Bank Regulations for New Entrants | -0.6% | National, affecting fintech startups | Long term (≥ 4 years) |

| Cyber-fraud Sophistication Targeting Mobile Wallets in GCC | -0.9% | Regional GCC, with UAE as primary target | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-privacy concerns challenge open banking implementation

The Open Finance Regulation obliges all licensed financial institutions to facilitate safe data portability; however, many users remain wary of sharing personal details, citing risks of credential stuffing and social-engineering attacks. Although the UAE’s removal from the FATF grey list in 2024 reinforces supervisory credibility, sustained education campaigns and robust consent-handling protocols remain essential to mitigate churn and maintain the UAE mobile payments market growth trajectory.

Payment-infrastructure fragmentation impedes seamless adoption

A dual technology stack—QR and NFC—continues to tax merchant budgets. Retailers often juggle separate terminals to ensure compatibility with Apple Pay, Google Pay, and Samsung Pay, whose bank tie-ups still diverge. The digital transformation of the nol card underscores these hurdles; full iPhone compatibility is pending until 2025, limiting universal acceptance in the interim.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Type: Proximity payments anchor current value as remote channels sprint ahead

Proximity payments captured 67.30% of the UAE mobile payments market in 2025, reinforced by widespread contactless POS availability across malls, restaurants, and hospitality venues. Emirates NBD’s tap-to-pay flow legitimized sub-15-second transactions, which resonates with consumers who still prefer in-person verification when purchasing higher-ticket items. As a result, the segment contributes the majority of transaction counts, even though average ticket values lean smaller, reflecting quick-service retail frequency. A dense tourist flow—over 5.29 million Indian arrivals annually—further amplifies in-person spending, especially when UPI rails bridge foreign wallets to local terminals. Remote payments, though representing a lower baseline, are projected to outpace at 14.05% CAGR, spurred by eCommerce growth, gig-economy platform wages, and mobile remittance surges. The introduction of Palm ID biometrics illustrates how policymakers intend to raise security without undermining checkout speed, an initiative expected to lift both proximity and remote clearance rates once fully commercialized. Taken together, the respective growth arcs ensure that the UAE mobile payments market remains balanced across user contexts, with contactless cards and wallets dominating brick-and-mortar venues while API-driven wallets expand digital retail.

A structural shift toward hybrid commerce also widens addressable volume. Retailers such as Flying Tiger Copenhagen saw 50% shopper uptake within a week of activating “scan-and-go” checkout, validating the business case for minimal-friction store experiences. Merchants increasingly appreciate that wallet-enabled loyalty schemes heighten sell-through rates without discounting margins. Consequently, proximity solutions are evolving into all-in-one commerce hubs that fuse inventory insights with instant settlement, while remote channels integrate social-commerce plug-ins that capitalize on influencers’ reach. The blended strategy ultimately positions the UAE mobile payments market for omnichannel resilience through 2031 and beyond.

By Transaction Type: Rapid P2P acceleration reshapes liquidity cycles

In-store POS transactions maintained a 39.40% value share in 2025 and remain a cornerstone for the tourism, luxury, and F&B verticals. Yet the Aani instant-payment service is radically altering P2P expectations by completing transfers in under 10 seconds, pushing P2P volumes to a forecast 13.63% CAGR through 2031. The platform’s phone-number routing simplifies addressing, allowing unbanked or underbanked users to transact without IBAN familiarity. A material outcome is the speedier recycling of funds into consumer spending, shortening economic velocity cycles. Person-to-merchant flows also show solid traction due to QR code ubiquity, especially for micro-ticket cafés and parking services. Complementary innovation in bill-pay and government-fee segments via DubaiPay sustains around-the-clock service delivery, thereby widening the transaction canvas and progressively replacing cash envelopes.

P2P momentum creates spill-over effects for micro-lending, salary advances, and gig-worker disbursements. Platforms such as Ziina focus on zero-fee transfers and ride the social-network virality of request links, cementing stickiness among younger cohorts. Combined, these developments reinforce systemic liquidity, lessen reliance on traditional cash cycles, and anchor the secular strength of the UAE mobile payments market.

By Application: Transportation outpaces retail in CAGR terms

Retail and eCommerce uses generated 47.20% of transaction value in 2025, underscoring the UAE’s reputation as a regional shopping hub. Merchants continually layer reward points, cash-back, and instalment options such as Abu Dhabi Islamic Bank’s Shariah-compliant Visa Installments to convert higher-basket checkouts. The shift toward gateway-level tokenization via Mastercard and Visa further reduces fraud ratios, keeping chargeback rates low. Transportation and logistics, however, is posting the fastest 15.31% CAGR as Dubai’s Roads and Transport Authority embeds the nol Pay system into retail micro-payments beyond metro gates. NFC top-ups through smartphones not only substitute ticket booths but also let commuters purchase convenience-store items, illustrating mobility-commerce convergence.

Niche uses in hospitality, education, and health care add incremental momentum. AI-powered, cashier-less EASE stores in Dubai Mall highlight how embedded payments reduce queueing and enrich data trails for predictive restocking. Simultaneously, the UAE Pass provides a secure digital identity layer accepted by over 5,000 public- and private-sector portals, meaning mobile payments can be used seamlessly across fines, licensing, and visa renewals.

By End-User: SME digitization gains pace within a consumer-first landscape

Personal wallets constituted 69.10% of transaction counts in 2025 and remain the anchor segment for the UAE mobile payments market. High usability, fee-lite structures, and diverse top-up avenues maintain adoption momentum. Meanwhile, enterprises—especially SMEs—are onboarding at a 12.76% CAGR as management teams recognize tap-to-pay as table-stakes for millennial and Gen Z customers. Solutions such as Emirates NBD Pay handle 143 currencies, accept chip-and-PIN, QR, and tokenized wallets, and deliver auto-reconciliation files that collapse manual bookkeeping cycles. Commercial Bank International’s tie-up with areeba illustrates how acquirer-processor partnerships unlock white-label gateways for fintechs, opening new revenue linchpins targeting the USD 5.7 billion UAE fintech sector projected for 2029.

Corporate uptake extends to payroll cards, spend-management analytics, and in-app credit lines. Pine Labs’ Credit+ platform, co-developed with Emirates NBD, enables merchants to offer pay-by-link and buy-now-pay-later options, nudging average order values upward. These capabilities demonstrate how the UAE mobile payments industry is broadening beyond consumer wallets and embedding deep within enterprise resource planning layers.

Geography Analysis

Dubai and Abu Dhabi collectively accounted for roughly 74.60% of the UAE mobile payments market in 2025, expanding at an anticipated 11.34% CAGR to 2031. Dubai’s Economic Agenda 2033 positions the emirate as a world-class cashless hub, with the Dubai Cashless Working Group orchestrating merchant onboarding programs, bulk terminal subsidies, and digital-literacy drives. The emirate’s hospitality-driven economy attracts heavy cross-border card inflows, amplified by UPI-QR acceptance at 60,000 outlets that streamline spending for Indian tourists. Abu Dhabi’s AED 13 billion AI-native government program likewise catalyzes wallet usage for licensing, traffic fines, and land-department fees, embedding digital settlement into public-sector touchpoints.

The Northern Emirates—Sharjah, Ajman, Ras Al Khaimah, Fujairah, and Umm Al Quwain—collectively represented 25.40% of value in 2025 but are projected to grow at 10.05% CAGR. Merchant acceptance gaps persevere, particularly around QR readiness, yet public-sector salary disbursement cards and micro-merchant QR grants are narrowing the divide. Regional banks deploy branch-lite onboarding buses, while telecom kiosks in malls handle same-day SIM-wallet linking, progressively homogenizing user experiences across emirates. Such measures widen the UAE mobile payments market footprint beyond metropolitan cores.

At a regional level, the UAE is positioning itself as the GCC’s settlement hub. Intra-GCC trade rose to USD 143 billion in 2021, but clearing still leans on correspondent banking. Emirates NBD’s 24/7 USD-clearing collaboration with Citi compresses settlement lags, with Saudi Arabia queued next for rollout. Coupled with the Digital Dirham’s 2025 launch runway, the UAE mobile payments market is set to become the region’s reference rail for real-time, multi-currency transactions.

Competitive Landscape

The UAE mobile payments market demonstrates moderate concentration yet rising rivalry as large banks, telcos, and fintechs vie for user primacy. Emirates NBD maintains leadership through a one-third share of national credit-card spend and recorded AED 27.1 billion (USD 7.38 billion) profit before tax in 2024, of which digital channels contributed a sizable volume uplift. Its Aani instant-payment adoption fold brought cross-bank interoperability, internally cutting manual reconciliation costs and externally locking in customer stickiness. Telecommunications group e& leverages its vast subscriber base to cross-sell its e& money wallet, which tripled international transfer volumes in 2024, proving that telcos possess viable cost-of-acquisition advantages through embedded airtime incentives.

First Abu Dhabi Bank differentiates via Payit, which waives minimum balance requirements—an effective play to capture first-salary accounts for newly arrived expatriates and consequently own remittance flow adjacency. Abu Dhabi Islamic Bank takes an Islamic-finance angle, launching personal-finance managers and Shariah-compliant instalment products that appeal to faith-conscious demographics. Fintech-bank infrastructure partnerships are on the rise; Commercial Bank International’s areeba deal furnishes turnkey BIN-sponsorship and PCI infrastructure to challenger wallets, compressing time-to-market cycles.

International processors such as Checkout.com and Paymentology are embedding deeper by acting as orchestration layers for local players, thereby lowering latency and enabling A/B testing of new tender types. Disruptors including Ziina concentrate on social P2P flows, whereas palm-vein biometrics being trialled by the Federal Authority hints at a next wave of hardware-anchored differentiation. Competitive intensity therefore hinges on customer-experience depth, cross-border liquidity access, and compliance stamina as rules on tokenized assets evolve.

United Arab Emirates Mobile Payments Industry Leaders

Amazon Payment Services

Google Pay

Samsung Pay

Apple Pay

NOW Money

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Abu Dhabi Islamic Bank unveiled the ADIB Money Management Tracker with fintech Lune to boost customer engagement through gamified budgeting, aimed at lifting cross-sell rates for savings products by 5 percentage points over two years.

- February 2025: Paymentology partnered with Zand Bank to provide BIN-sponsorship and virtual IBAN services, speeding fintech onboarding while anchoring Paymentology’s processor footprint ahead of the Digital Dirham pilot phase.

- January 2025: Abu Dhabi Government launched its 2025-2027 Digital Strategy, allocating AED 13 billion (USD 3.5 billion) to deploy 200 AI solutions that integrate UAE Pass single-sign-on with mobile payment rails, targeting AED 24 billion GDP uplift and 5,000 new jobs.

- January 2025: Checkout.com allied with noqodi to merge its global orchestration platform with noqodi’s domestic network, broadening acceptance options for SMEs seeking multi-currency settlements within a single API stack.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Arab Emirates mobile payments market as the total value of transactions initiated through a smartphone or tablet using proximity technologies (NFC, QR, tokenized Bluetooth) and remote channels (in-app, web checkout, P2P transfers) that settle via cards, accounts, or stored value.

Scope exclusion: Cash-in at ATMs, card-present chip inserts, and cross-border payroll remittances sit outside this market.

Segmentation Overview

- By Payment Type

- Proximity Payments

- Remote Payments

- By Transaction Type

- Peer-to-Peer (P2P)

- In-store Point-of-Sale (POS)

- Person-to-Merchant (P2M/Checkout)

- Other Transaction Types

- By Application

- Retail and eCommerce

- Transportation and Logistics

- Hospitality and Food-Service

- Government and Public Sector

- Other Applications (Education, Healthcare)

- By End-user

- Personal

- Business

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts speak with bank acquirers, wallet product leads, fintech CEOs, regulators, and large merchants across Dubai, Abu Dhabi, and the Northern Emirates. These discussions clarify adoption barriers, price points, and annual throughput, which are then matched against desk findings to close data gaps.

Desk Research

We begin with publicly available datasets from the Central Bank of the UAE, Federal Competitiveness and Statistics Centre, GSMA Mobile Economy Middle East, UNCTAD B2C index, and Dubai Department of Economy and Tourism, which together anchor user counts, terminal density, retail mix, and inbound tourist spend. Company filings, investor decks, and media articles curated through Dow Jones Factiva, along with payment network rulebooks, complement these foundations.

Subscription sources such as D&B Hoovers for issuer and acquirer financials, Questel for wallet-related patents, and WSTS for secure element chip shipments help our team spot volume inflections. The sources listed are illustrative; many additional references inform our data collection and sense-checking.

Market-Sizing & Forecasting

A top-down spend pool is reconstructed from household consumption, online retail sales, bill-pay volumes, and CBUAE instant-rail statistics, before being further filtered through mobile payment penetration rates derived from survey inputs. Supplier roll-ups of sampled average spend per active user validate totals. Key variables like smartphone penetration, contactless POS share, QR terminal rollout, average ticket size drift, tourist receipts, and interchange caps feed a multivariate regression that projects values to 2030. Where bottom-up checks diverge, we adjust assumptions transparently.

Data Validation & Update Cycle

Outputs pass variance thresholds, peer review, and anomaly flags. Reports refresh every year and may be reopened after material regulatory or macro events. A final analyst pass just before publication ensures clients receive the freshest view.

Why Mordor's United Arab Emirates Mobile Payments Baseline Commands Reliability

Estimates from different publishers often differ because they track separate money flows, apply contrasting penetration assumptions, or refresh less frequently. We acknowledge these inherent gaps up front.

Key gap drivers include narrower scopes that ignore remote spend, models built on wallet revenue rather than transaction value, and inconsistent treatment of business payments, which cause figures to swing wide of consumer reality.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 80.37 Bn (2025) | Mordor Intelligence | |

| USD 9.88 Bn (2024) | Regional Consultancy A | Tracks merchant fee revenue only and omits remote in-app transactions |

| USD 4.18 Bn (2024) | Industry Journal B | Counts stored wallet balances, excludes tap-to-pay volume and most QR flows |

The comparison shows that when scope, variables, and update cadence align with real consumer spend, our baseline remains the most balanced and repeatable yardstick for decision-makers.

Key Questions Answered in the Report

What is the current value of the UAE mobile payments market?

The UAE mobile payments market size is valued at USD 89.15 billion in 2026 and is forecast to reach USD 149.57 billion by 2031.

Which payment type leads the UAE mobile payments market?

Proximity payments hold 67.30% market share, supported by extensive contactless POS infrastructure across retail and hospitality venues.

How fast are P2P mobile transfers growing in the UAE?

Peer-to-peer transfers are advancing at a 13.63% CAGR through 2031, driven by instant-payment platforms such as Aani.

Why is the transportation segment growing the fastest?

Dubai’s nol Pay integration into public transport and retail micro-payments is propelling transportation applications at a 15.31% CAGR through 2031.

What role will the Digital Dirham play?

The Digital Dirham, scheduled for late 2025, will introduce a retail central bank digital currency that can reduce settlement costs and support cross-border interoperability.

Which companies dominate the competitive landscape?

Emirates NBD, e&, and First Abu Dhabi Bank are leading players, with Emirates NBD alone capturing one-third of national credit-card spending.

Page last updated on: