Starter Cultures Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

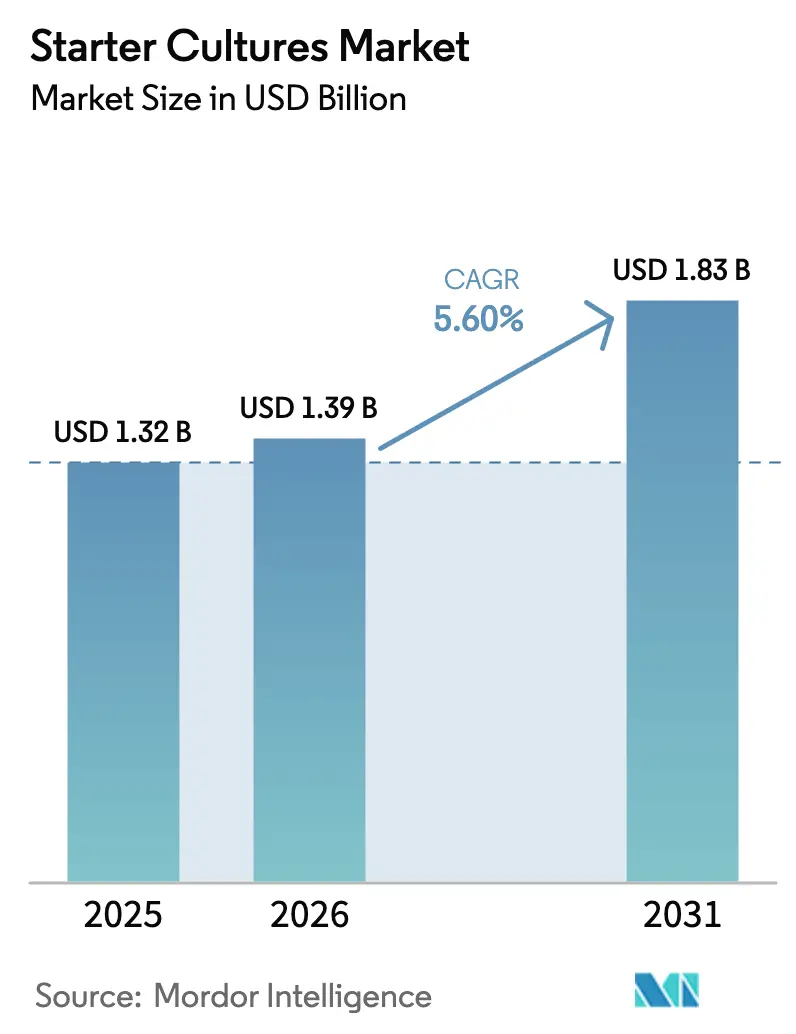

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 1.83 Billion |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Starter Cultures Market Analysis by Mordor Intelligence

Starter cultures market size in 2026 is estimated at USD 1.39 billion, growing from 2025 value of USD 1.32 billion with 2031 projections showing USD 1.83 billion, growing at 5.6% CAGR over 2026-2031. The market growth reflects the transition from traditional fermentation methods to engineered microbial solutions that enhance food safety, sustainability, and health benefits. The increasing demand for clean-label products, developments in synthetic biology, and the growing use of bioprotective cultures instead of chemical preservatives drive market growth across dairy, bakery, plant-based, and meat segments. The dairy segment dominates the market due to the extensive use of starter cultures in yogurt, cheese, and fermented milk products. In the bakery sector, these cultures improve dough fermentation, texture, and shelf life. The plant-based segment is experiencing rapid growth as manufacturers develop new fermented alternatives to dairy products. While Europe remains the primary market, Asia-Pacific shows the highest growth potential due to increasing consumption of fermented foods and stricter food safety regulations. The rising awareness of probiotics and their health benefits in these regions further accelerates market expansion. Industry consolidation among food manufacturers has led suppliers to expand their culture portfolios, while new patents focus on improved preparation methods to reduce production time and costs. The market also benefits from ongoing research and development in strain selection and optimization, enabling manufacturers to create cultures with enhanced functionality and performance.

Key Report Takeaways

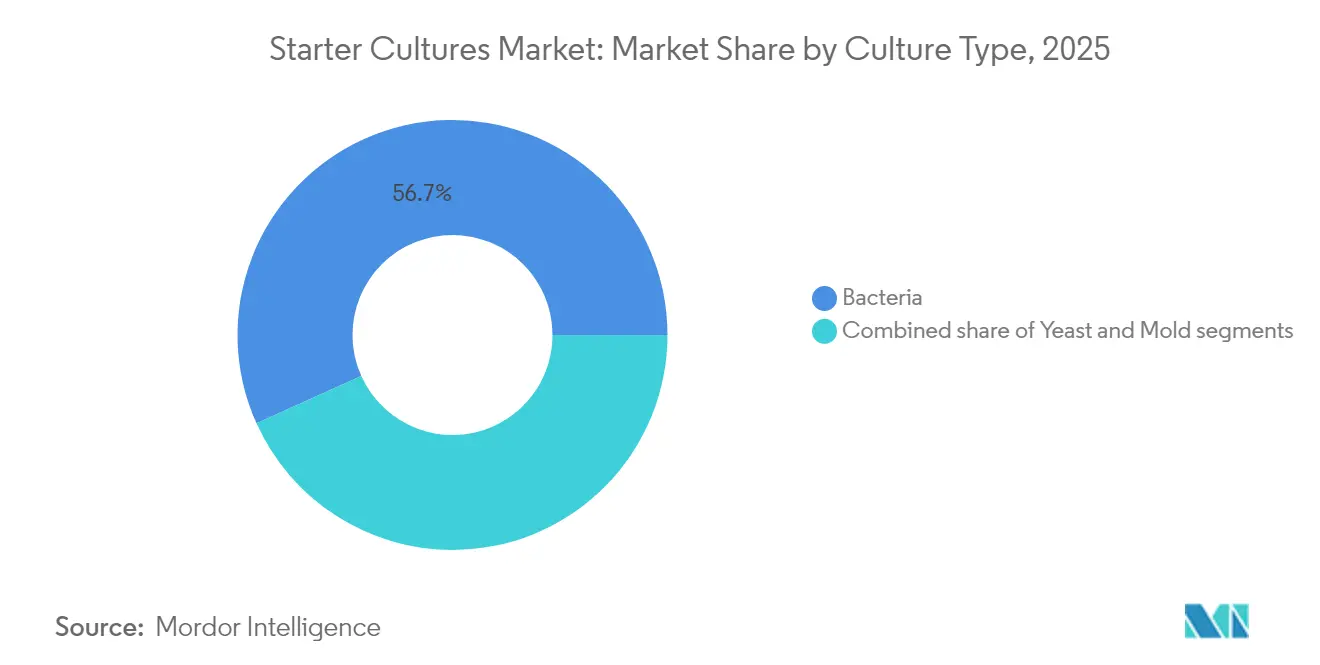

- By culture type, bacteria held 56.74% of the starter cultures market share in 2025; yeast is projected to advance at a 9.35% CAGR through 2031.

- By strain function, thermophilic cultures accounted for 40.12% of the starter cultures market size in 2025, whereas probiotic cultures are forecast to grow at an 8.6% CAGR through 2031.

- By form, freeze-dried formats led with 49.25% revenue share in 2025; liquid cultures are set to expand at a 9.45% CAGR through 2031.

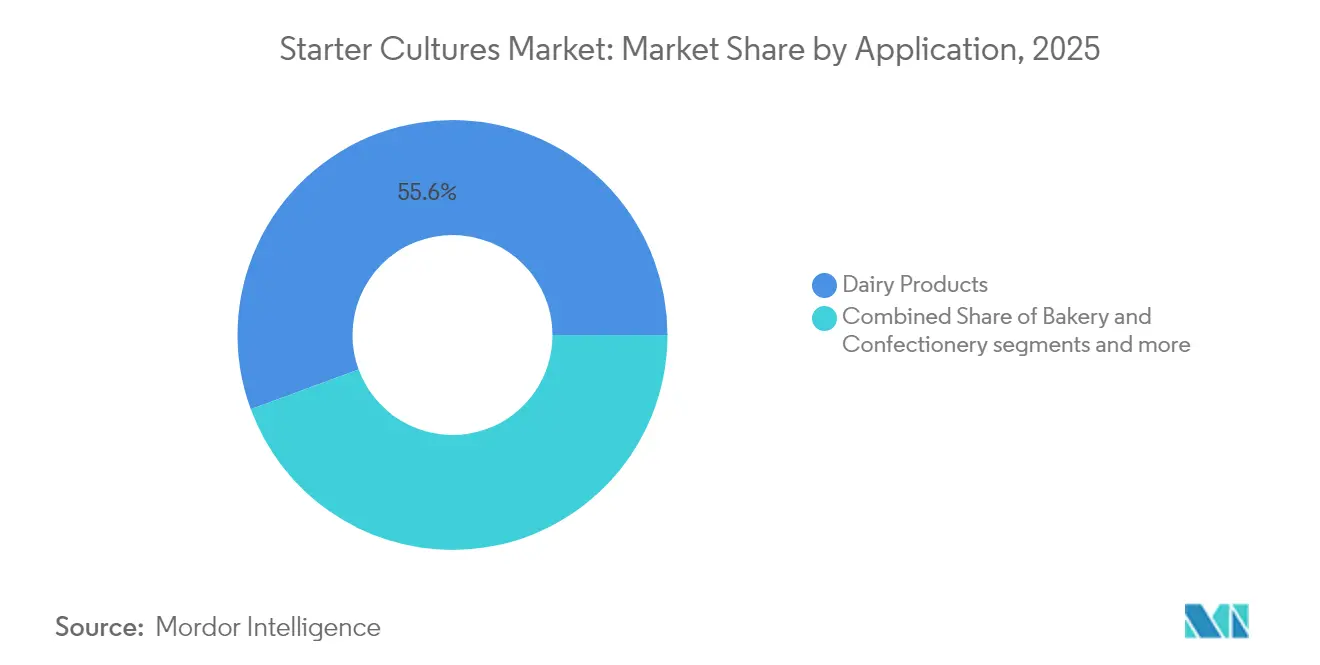

- By application, dairy products captured a 55.62% share of the starter cultures market size in 2025, while plant-based fermented foods are projected to rise at an 11.1% CAGR through 2031.

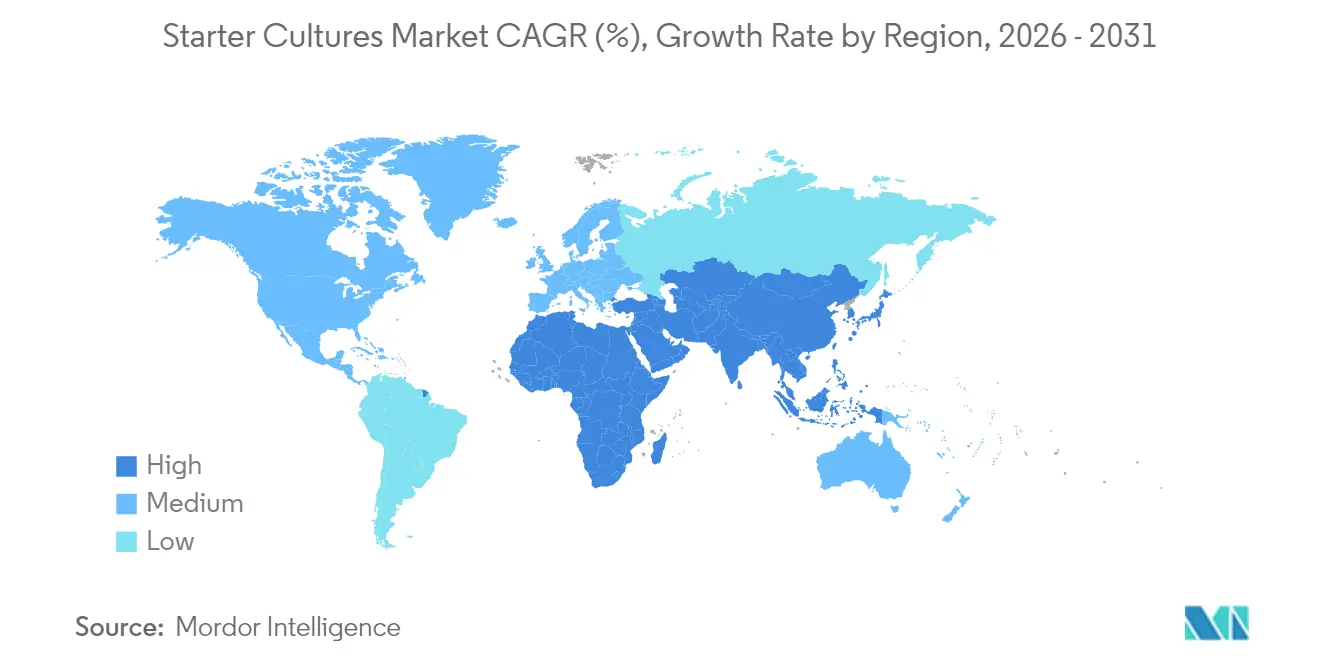

- By geography, Europe dominated with a 35.21% share in 2025; Asia-Pacific is pacing ahead at an 8.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Starter Cultures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label fermented foods | +1.8% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Growth in dairy alternatives using starter cultures | +1.2% | North America, Europe, Asia-Pacific urban centers | Long term (≥ 4 years) |

| Expansion of artisanal cheese and craft bakery segments | +0.9% | North America, Europe, with emerging presence in Asia-Pacific | Medium term (2-4 years) |

| Adoption of bioprotective cultures as alternatives to chemical preservatives | +1.5% | Global, accelerated in Europe due to regulatory pressure | Short term (≤ 2 years) |

| Advances in synthetic biology for customized, high-yield strains | +0.7% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Consolidation among large-scale food and beverage manufacturers | +0.3% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label fermented foods

The clean-label trend has become an industry requirement, as lactic acid bacteria produce natural antimicrobial compounds like bacteriocins that extend product shelf life. This application is particularly effective in dairy products, where protective cultures inhibit pathogens such as Listeria monocytogenes while maintaining product taste and texture. The effectiveness of these cultures in dairy applications has expanded their adoption across other food categories, including meat products, beverages, and bakery items. The global food industry's shift to natural preservation methods has gained momentum through successful implementations across various product categories. Regulatory support for biopreservation, including the European Food Safety Authority's expanded Qualified Presumption of Safety list with new strains like Lacticaseibacillus huelsenbergensis, validates industry investments in natural preservation methods.[1]Source: European Food Safety Authority, “Qualified Presumption of Safety (QPS) List – 2025 Update,” EFSA Journal, efsa.europa.eu This innovation supports the industry's transition toward natural preservation solutions while meeting consumer demands for clean-label products.

Growth in dairy alternatives using starter cultures

Specialized starter cultures in plant-based dairy alternatives help replicate traditional dairy textures and flavors through controlled fermentation processes. The combination of lactic acid bacteria and yeasts in mixed-culture fermentation creates improved nutritional profiles and sensory characteristics compared to single-strain methods, as multiple organisms work synergistically to develop complex flavors and textures. Companies are implementing these technologies at a commercial scale to meet market demands. For instance, Perfect Day produces animal-free whey protein through precision fermentation, using programmed microflora to convert sugar into milk proteins identical to those in cow's milk.[2]Source: Perfect Day, "How we Teach Microflora to Create Sustainable Protein", perfectday.com The protein undergoes extensive filtration and purification processes to create a lactose-free dairy alternative suitable for consumer applications. Similarly, TurtleTree also employs precision fermentation with specialized microorganisms to produce lactoferrin, a significant milk protein component with important nutritional properties. This method reduces environmental impact and meets increasing consumer demand for sustainable dairy alternatives without relying on traditional animal agriculture practices.

Expansion of artisanal cheese and craft bakery segments

The artisanal food market growth increases the demand for specialized starter cultures that create distinct regional flavors and textures in traditional food products. This development aligns with consumer preferences for authentic, craft-produced foods that maintain cultural heritage and traditional manufacturing methods. Cheese consumption is increasing as consumers show readiness to pay higher prices for authentic, locally-produced varieties across global markets, especially in regions with established dairy traditions. Industry investments support market growth, as demonstrated by Valio's EUR 60 million investment in cheese production processes at its Lapinlahti plant, Finland, in May 2024. Artisanal producers increasingly use backslopping techniques, where portions of previous batches inoculate new productions. This method enables the development of specific microbial ecosystems that differentiate their products in premium markets and maintain traditional production methods. The practice preserves traditional fermentation techniques and ensures consistent product characteristics across production batches.

Adoption of bioprotective cultures as alternatives to chemical preservatives

Bioprotective cultures enable food manufacturers to extend product shelf life through natural preservation methods while maintaining clean-label requirements. These cultures contain beneficial microorganisms that improve food safety through biological processes. The application spans across dairy, beverages, and fermented foods sectors. Recent regulatory developments support the use of biopreservation, with the FDA granting GRAS status to Bacillus subtilis NRRL 68053 for food applications at concentrations up to 1 x 10^10 CFU per serving in April 2023.[3]Source: Food and Drug Administration"GRAS Notice (GRN) 1143 Agency Response Letter", fda.gov The economic advantages include decreased chemical preservative usage and potential reductions in insurance and compliance costs. These cultures also meet growing consumer demand for natural ingredients and clean-label products. While maintaining culture viability during processing and storage remains a challenge, improvements in encapsulation technologies and freeze-drying methods have enhanced commercial applications across various food matrices. These advancements have improved stability and effectiveness under different environmental conditions, increasing the practical implementation of bioprotective cultures in commercial food production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of cold-chain logistics | -0.8% | Global, particularly acute in developing regions | Short term (≤ 2 years) |

| Volatility in dairy supply chains affecting culture utilization | -0.7% | Global, with severe impact in Australia, North America | Short term (≤ 2 years) |

| Intellectual property constraints around proprietary strains | -0.4% | Global, concentrated in developed markets with strong IP enforcement | Medium term (2-4 years) |

| Regulatory restrictions on genetically modified microorganisms (GMMs) | -0.6% | Europe primary impact, spillover to other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost of cold-chain logistics

Starter cultures require stable sub-zero temperatures for survival, as power disruptions or transportation delays can lead to cell death and product recalls. In regions with limited refrigeration infrastructure, distributors prefer freeze-dried formats that can withstand room temperature storage, despite their higher production costs. The cold-chain requirements for maintaining starter culture viability create substantial operational expenses throughout the supply chain. Temperature control failures result in culture deterioration and product recalls, negatively impacting manufacturer relationships. Infrastructure limitations particularly affect developing markets, where unreliable power supply and insufficient refrigeration networks restrict starter culture distribution. This challenge is more pronounced for liquid cultures requiring constant refrigeration compared to freeze-dried formats that can withstand ambient conditions. The rising energy costs for cold-chain maintenance have prompted facilities to implement LED lighting and ammonia-based refrigeration systems to reduce energy consumption while maintaining the required temperature conditions across the distribution network.

Regulatory restrictions on Genetically Modified Microorganisms (GMMs)

The European Union's regulatory framework requires comprehensive safety assessments for genetically modified microorganisms (GMMs), creating barriers for starter culture development. The European Union's risk assessment protocols require evaluation of GMM products across multiple parameters, including toxicity, allergenicity, nutritional impact, and environmental effects, before market approval. While food enzymes in Europe primarily originate from recombinant strains, consumer resistance to genetic modification limits the adoption of biotechnology methods. The contrasting approaches between the European Union's precautionary regulations and the US Generally Recognized as Safe (GRAS) system present compliance challenges for companies developing GMM-based starter cultures across markets. Patent protection on proprietary strains further restricts access to genetic modifications, as companies maintain intellectual property rights through licensing agreements that increase costs and create financial obstacles for smaller manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Culture Type: Bacteria Dominance Faces Yeast Innovation

Bacteria accounted for 56.74% of the starter cultures market share in 2025, with their primary applications in lactic acid production for dairy, bakery, and meat products. Yeast segments are experiencing growth at a 9.35% CAGR, driven by advancements in synthetic biology that enable enhanced aroma production and protein synthesis. Lacticaseibacillus and Streptococcus species maintain their essential role in acidification, texture development, and pathogen control. Yeast applications have expanded from traditional bread making to fermented beverages and dairy alternatives, where Saccharomyces provides consistent texture and mild sweetness. Mold cultures, particularly Aspergillus, remain important in Asian soy fermentation but represent smaller market volumes compared to bacterial and yeast segments.

The competitive landscape is evolving as manufacturers develop yeasts capable of producing dairy-equivalent proteins at an industrial scale, particularly for plant-based products. Bacterial strain development focuses on improving acidification rates and phage resistance to increase production efficiency. Mixed-culture starter solutions combining bacteria, yeast, and mold enable manufacturers to achieve complex flavor profiles while maintaining clean-label requirements.

By Strain Function: Thermophilic Leadership Challenged by Probiotic Growth

Thermophilic cultures account for 40.12% of the starter cultures market size in 2025, playing a vital role in yogurt and hard-cheese production processes operating at approximately 45°C. Mesophilic cultures facilitate the production of Cheddar and Gouda cheeses at lower temperatures, maintaining their distinct flavor profiles. The probiotic cultures segment is growing at an 8.6% CAGR, driven by clinical research demonstrating connections between gut microbiota, immune function, and metabolic health. Adjunct cultures enhance aged-cheese flavors, while protective cultures focus on extending product shelf life.

The market shows increasing demand for dual-function probiotics that deliver both processing advantages and health benefits. Manufacturers are incorporating Bifidobacterium and Lactobacillus strains into thermophilic blends to produce yogurt that meets texture requirements while providing digestive health benefits. Research initiatives in Brazil and South Korea focus on identifying native thermophilic strains with enhanced acidification and phage resistance properties to strengthen regional supply chains.

By Form: Freeze-Dried Stability Versus Liquid Convenience

Freeze-dried starters accounted for 49.25% of the market revenue share in 2025, due to their extended shelf life and stability during ambient temperature shipping. These starters remain effective for extended periods without specialized storage conditions, making them essential for international trade and regions with limited cold storage infrastructure. Liquid starter cultures are growing at a 9.45% CAGR, driven by their direct-vat-set convenience and minimal inoculation error risk. The liquid format enables precise dosing and immediate incorporation into production processes, improving manufacturing efficiency. Frozen cultures maintain a balanced position, offering high cell counts while requiring continuous cold chain storage.

Manufacturing decisions incorporate total cost of ownership, including energy consumption, product waste, and labor requirements. The selection of starter formats influences operational efficiency and production costs throughout the supply chain. Advances in encapsulation technology have enhanced freeze-dried probiotic viability, improving their stability and effectiveness during storage and application. Powdered starters with cyclodextrin show increased yeast survival rates, enhancing performance in fermentation processes. Environmental assessments indicate freeze-drying becomes more sustainable for storage periods beyond seven months, making it optimal for export markets. This sustainability benefit results from lower energy requirements for long-term storage compared to frozen or liquid formats.

By Application: Dairy Dominance Meets Plant-Based Disruption

Dairy products dominate the starter cultures market with a 55.62% revenue share in 2025. The manufacturing of cheese and yogurt requires acidifying and flavor-forming bacteria to achieve specific texture, pH levels, and food safety standards. These bacteria convert lactose into lactic acid, develop characteristic flavors, and maintain product consistency. The plant-based fermented foods segment exhibits a CAGR of 11.1% during the forecast period, supported by precision fermentation technology that produces dairy proteins and fat systems without animal inputs. The market expansion includes increased demand for sourdough bread, kombucha beverages, and fermented meat products, reflecting consumer preferences for functional and probiotic-rich foods.

Mixed cultures enhance the acceptance of plant-based products by resolving solubility issues and improving flavors in soy and pea-based alternatives. These cultures function together to decompose complex plant proteins and increase nutritional bioavailability. In dairy processing, heat-treated cultures minimize ripening and maturation times, allowing manufacturers to improve production efficiency while sustaining product quality. Starter cultures have become integral to both traditional dairy production and plant-based alternatives, with manufacturers focusing on research and development to create specialized culture combinations for diverse applications.

Geography Analysis

Europe generated 35.21% of starter cultures market revenue in 2025, supported by traditional cheese production, stringent hygiene standards, and established research and development networks. Protected Designation of Origin (PDO) cheeses require specific microbial consortia, ensuring consistent culture demand. The European Food Safety Authority's (EFSA) Qualified Presumption of Safety (QPS) list provides clear regulatory pathways, encouraging strain development and bioprotective applications.

Asia-Pacific is growing at an 8.55% CAGR, driven by increasing urban consumption of yogurt, kimchi, and probiotic beverages. Government investment in precision fermentation research supports market expansion. In June 2024, the University of Illinois Urbana-Champaign received a USD 14.8 million five-year grant to establish the Centre for Precision Fermentation and Sustainability (PreFerS). Funded by Singapore's National Research Foundation (NRF), the center focuses on microbial cell engineering to develop safe and nutritious food products. The Illinois Advanced Research Center at Singapore (Illinois ARCS) will conduct research on food-grade microorganisms and scale up production from laboratory to pilot level.

North America maintains steady growth through developed cold-chain infrastructure and the FDA GRAS (Generally Recognized as Safe) system. The plant-based cheese industry creates additional demand for specialized starter cultures that replicate dairy properties. Mexico's expanding cheese exports increase the need for cultures meeting U.S. standards, while Canada's regulated dairy industry ensures stable starter culture demand.

Competitive Landscape

The starter cultures market exhibits moderate concentration. Key market participants include Novonesis A/S, DSM-Firmenich AG, Dohler Group, and Lallemand Inc. These companies prioritize mergers and acquisitions to enhance their product portfolios and meet diverse manufacturer requirements. For instance, in October 2024, Lesaffre acquired a 70% stake in Biorigin from Zilor, strengthening its position in savory ingredients. This acquisition established Lesaffre as the controlling shareholder in a joint venture focused on developing yeast-based ingredients for food and animal feed markets.

Regional companies like Angel Yeast and Valio maintain their market position by utilizing local microbial libraries and providing proximity services. Industry leaders are investing in pilot plants, strain-bank digitization, and AI-guided selection tools to reduce development time for customized cultures.

Growth opportunities exist in plant-based dairy, fermented snacks, and temperature-resistant strains that can withstand supply chain temperature variations. Companies differentiate themselves through technical services, phage monitoring programs, and automated dosing systems that reduce operational errors. Increased patent activity in starter preparation and encapsulation technologies indicates growing competition in research and development.

Starter Cultures Industry Leaders

-

Novonesis A/S

-

DSM-Firmenich AG

-

Dohler Group

-

Lallemand Inc.

-

Angel Yeast Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: Novozymes and Chr. Hansen merger concluded with the formation of Novonesis A/S. The consolidation, announced in December 2022, received final approval from the Danish Business Authority in January 2024.

- September 2023: DSM-Firmenich launched Delvo Fresh Pioneer, a new generation of starter cultures for mild yogurts. The product provides pH stability during processing and throughout shelf life, addressing yogurt manufacturers' requirements for quality ingredients, stable production processes, and consistent product mildness.

- January 2023: IFF (International Flavors & Fragrances) introduced CHOOZIT VINTAGE, a cheese starter culture, in the United States and Canadian markets. The culture helps cheddar cheese manufacturers address flavor challenges during the aging process and ensures consistent, balanced flavors with a smooth, clean-cut texture in each production batch.

Global Starter Cultures Market Report Scope

Starter culture refers to the microbial culture technique to assemble commercial fermented products. The global started culture market (henceforth referred to as the market studied) is segmented by type, form, application, and geography. By type, the market is segmented into Yeast, Bacteria, and Mold. Based on the Form, the market is segmented into Dried, Liquid, and Frozen. Based on the application, the market studied is segmented into Dairy Products, Bakery Products, Non-Alcoholic Beverages, Alcoholic Beverages, and others. It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Bacteria |

| Yeast |

| Mold |

| Mesophilic Cultures |

| Thermophilic Cultures |

| Adjunct Cultures |

| Probiotic Cultures |

| Freeze-Dried |

| Liquid |

| Frozen |

| Dairy Products | Milk |

| Cheese | |

| Yogurt and Kefir | |

| Other Dairy Products | |

| Bakery and Confectionery | |

| Beverages | |

| Plant-based Fermented Foods | |

| Meat and Seafood Fermentation |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| UAE | |

| Rest of Middle East and Africa |

| By Culture Type | Bacteria | |

| Yeast | ||

| Mold | ||

| By Strain Function | Mesophilic Cultures | |

| Thermophilic Cultures | ||

| Adjunct Cultures | ||

| Probiotic Cultures | ||

| By Form | Freeze-Dried | |

| Liquid | ||

| Frozen | ||

| By Application | Dairy Products | Milk |

| Cheese | ||

| Yogurt and Kefir | ||

| Other Dairy Products | ||

| Bakery and Confectionery | ||

| Beverages | ||

| Plant-based Fermented Foods | ||

| Meat and Seafood Fermentation | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| UAE | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the starter cultures market?

The starter cultures market stands at USD 1.39 billion in 2026 and is forecast to reach USD 1.83 billion by 2031.

Which region is growing fastest?

Asia-Pacific is the fastest-growing region, posting an 8.55% CAGR through 2031 on rising demand for fermented foods and modernizing food-safety standards.

Which application segment leads revenue?

Dairy products lead, holding 55.62% of 2025 revenue, though plant-based fermented foods record the highest 11.1% CAGR.

Who are the leading companies?

Novonesis, DSM-Firmenich, and Lesaffre are among the market leaders, collectively accounting for approximately one-third of global revenue in 2024.

Page last updated on: